Analysis of Apple's Financial Statement and Risk Factors

VerifiedAdded on 2023/01/13

|18

|3444

|36

AI Summary

This document provides a detailed analysis of Apple's financial statement from 1995 to 2012, including liquidity ratios, profitability ratios, leverage ratios, and income statement analysis. It also discusses the reasons for issuing new common stock by Apple and the traditional ratios that might be distorted. Additionally, it explores the return on equity of Apple based on book and market value and identifies the major risk factors that can impact Apple's future business.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Apple - Time to Think Different

about cash

about cash

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

1. Analysis of the financial statement..............................................................................................4

a. Providing brief analysis of the Apple's current final reports and key evolutions over a period

of 1995-2012................................................................................................................................4

b. Stating the reason of issuing new common stock every year by Apple, despite the abundant

cash position and the shortage of requirement in raising an additional capital...........................8

c. With respect to Apple's peculiarities, stating the traditional ratio that might be hugely

distorted.......................................................................................................................................8

d. Assessing return on Equity of Apple on the basis of the book and market value...................8

e. reason for decreasing operating cash flow of Apple than Exon..............................................9

2.......................................................................................................................................................9

Detecting the major risk factors that adversely affects future business of an enterprise.............9

3.....................................................................................................................................................10

(a)...............................................................................................................................................10

(b)...............................................................................................................................................11

©................................................................................................................................................11

(4)...............................................................................................................................................14

4.....................................................................................................................................................15

a. representing that Apple's cash pile comes at an expense of the shareholders.......................15

5.....................................................................................................................................................15

a. Analysing past and the new dividend policy of Apple..........................................................15

b. Explaining the foremost objective of the share repurchase program and the way in which it

is financed..................................................................................................................................15

c. Describing and evaluating the capital structure of Apple......................................................15

REFERENCES..............................................................................................................................17

Table 1EV/EBIT calculation.........................................................................................................10

Table 2EV/sales ratio.....................................................................................................................11

Table 3Cash flow...........................................................................................................................11

Table 4Discounted cash flow.........................................................................................................12

1. Analysis of the financial statement..............................................................................................4

a. Providing brief analysis of the Apple's current final reports and key evolutions over a period

of 1995-2012................................................................................................................................4

b. Stating the reason of issuing new common stock every year by Apple, despite the abundant

cash position and the shortage of requirement in raising an additional capital...........................8

c. With respect to Apple's peculiarities, stating the traditional ratio that might be hugely

distorted.......................................................................................................................................8

d. Assessing return on Equity of Apple on the basis of the book and market value...................8

e. reason for decreasing operating cash flow of Apple than Exon..............................................9

2.......................................................................................................................................................9

Detecting the major risk factors that adversely affects future business of an enterprise.............9

3.....................................................................................................................................................10

(a)...............................................................................................................................................10

(b)...............................................................................................................................................11

©................................................................................................................................................11

(4)...............................................................................................................................................14

4.....................................................................................................................................................15

a. representing that Apple's cash pile comes at an expense of the shareholders.......................15

5.....................................................................................................................................................15

a. Analysing past and the new dividend policy of Apple..........................................................15

b. Explaining the foremost objective of the share repurchase program and the way in which it

is financed..................................................................................................................................15

c. Describing and evaluating the capital structure of Apple......................................................15

REFERENCES..............................................................................................................................17

Table 1EV/EBIT calculation.........................................................................................................10

Table 2EV/sales ratio.....................................................................................................................11

Table 3Cash flow...........................................................................................................................11

Table 4Discounted cash flow.........................................................................................................12

Table 5CAPM model.....................................................................................................................12

Table 6Enterprise value.................................................................................................................12

Table 7SDebt equity weight and WACC calculation....................................................................13

Table 8Terminal value...................................................................................................................13

Table 9Equity value.......................................................................................................................14

Table 10Intrinsic value of equity...................................................................................................14

Table 6Enterprise value.................................................................................................................12

Table 7SDebt equity weight and WACC calculation....................................................................13

Table 8Terminal value...................................................................................................................13

Table 9Equity value.......................................................................................................................14

Table 10Intrinsic value of equity...................................................................................................14

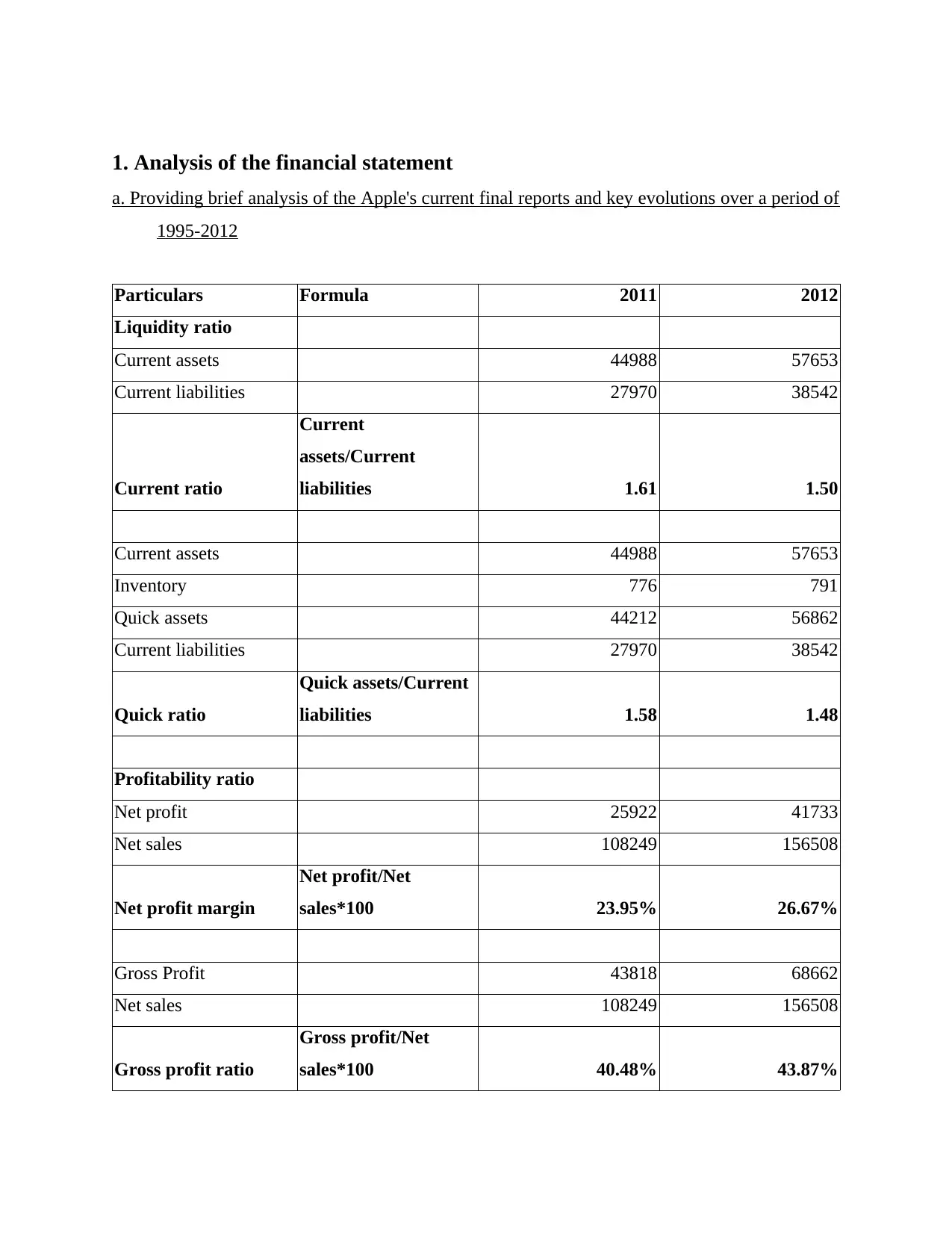

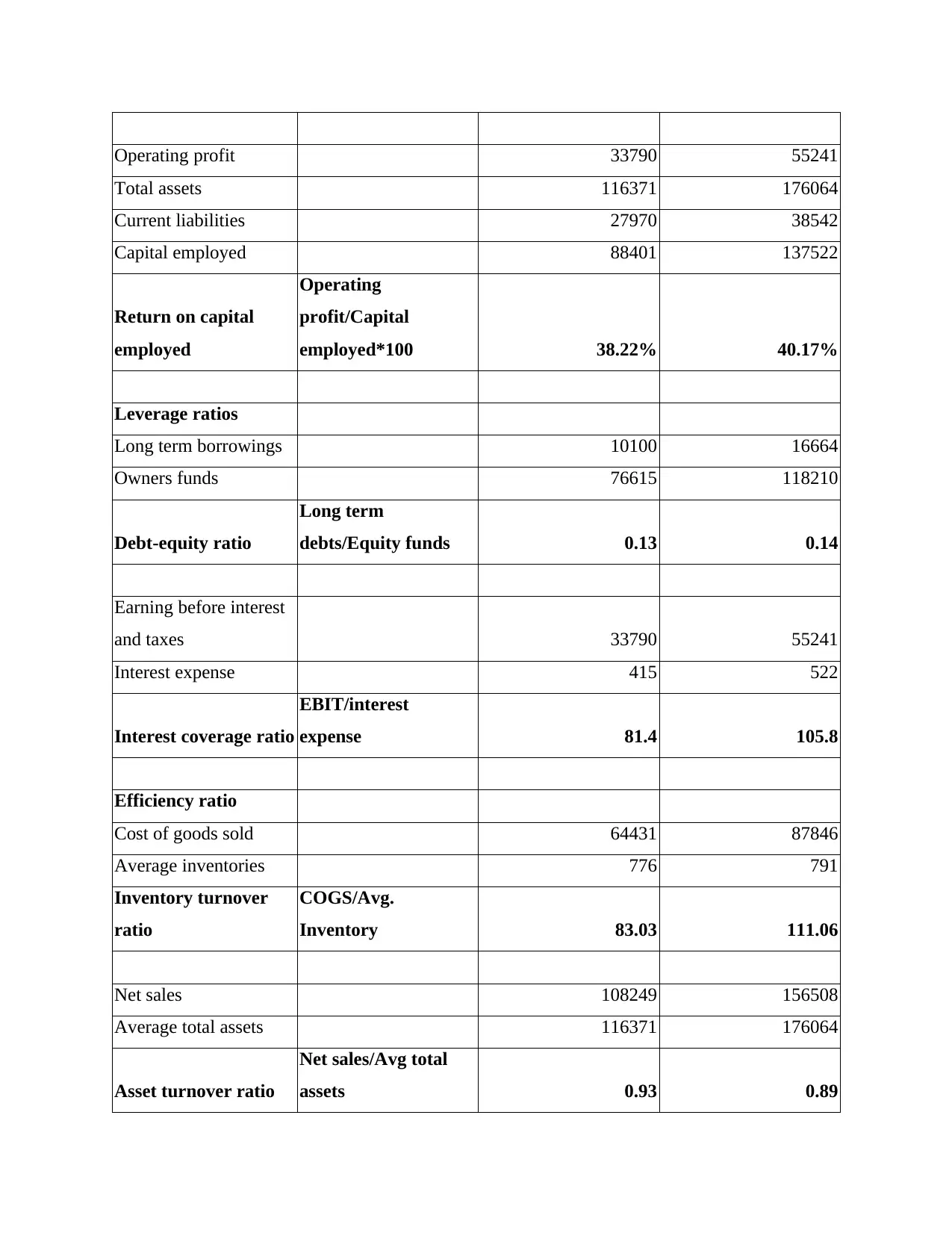

1. Analysis of the financial statement

a. Providing brief analysis of the Apple's current final reports and key evolutions over a period of

1995-2012

Particulars Formula 2011 2012

Liquidity ratio

Current assets 44988 57653

Current liabilities 27970 38542

Current ratio

Current

assets/Current

liabilities 1.61 1.50

Current assets 44988 57653

Inventory 776 791

Quick assets 44212 56862

Current liabilities 27970 38542

Quick ratio

Quick assets/Current

liabilities 1.58 1.48

Profitability ratio

Net profit 25922 41733

Net sales 108249 156508

Net profit margin

Net profit/Net

sales*100 23.95% 26.67%

Gross Profit 43818 68662

Net sales 108249 156508

Gross profit ratio

Gross profit/Net

sales*100 40.48% 43.87%

a. Providing brief analysis of the Apple's current final reports and key evolutions over a period of

1995-2012

Particulars Formula 2011 2012

Liquidity ratio

Current assets 44988 57653

Current liabilities 27970 38542

Current ratio

Current

assets/Current

liabilities 1.61 1.50

Current assets 44988 57653

Inventory 776 791

Quick assets 44212 56862

Current liabilities 27970 38542

Quick ratio

Quick assets/Current

liabilities 1.58 1.48

Profitability ratio

Net profit 25922 41733

Net sales 108249 156508

Net profit margin

Net profit/Net

sales*100 23.95% 26.67%

Gross Profit 43818 68662

Net sales 108249 156508

Gross profit ratio

Gross profit/Net

sales*100 40.48% 43.87%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Operating profit 33790 55241

Total assets 116371 176064

Current liabilities 27970 38542

Capital employed 88401 137522

Return on capital

employed

Operating

profit/Capital

employed*100 38.22% 40.17%

Leverage ratios

Long term borrowings 10100 16664

Owners funds 76615 118210

Debt-equity ratio

Long term

debts/Equity funds 0.13 0.14

Earning before interest

and taxes 33790 55241

Interest expense 415 522

Interest coverage ratio

EBIT/interest

expense 81.4 105.8

Efficiency ratio

Cost of goods sold 64431 87846

Average inventories 776 791

Inventory turnover

ratio

COGS/Avg.

Inventory 83.03 111.06

Net sales 108249 156508

Average total assets 116371 176064

Asset turnover ratio

Net sales/Avg total

assets 0.93 0.89

Total assets 116371 176064

Current liabilities 27970 38542

Capital employed 88401 137522

Return on capital

employed

Operating

profit/Capital

employed*100 38.22% 40.17%

Leverage ratios

Long term borrowings 10100 16664

Owners funds 76615 118210

Debt-equity ratio

Long term

debts/Equity funds 0.13 0.14

Earning before interest

and taxes 33790 55241

Interest expense 415 522

Interest coverage ratio

EBIT/interest

expense 81.4 105.8

Efficiency ratio

Cost of goods sold 64431 87846

Average inventories 776 791

Inventory turnover

ratio

COGS/Avg.

Inventory 83.03 111.06

Net sales 108249 156508

Average total assets 116371 176064

Asset turnover ratio

Net sales/Avg total

assets 0.93 0.89

Interpretation- from the above analysis it has been depicted that liquidity ratio of Apple

in the recent years is declining which clearly shows that liquidity position of the company is not

good. The current ratio of an entity is showing a declining trend that is from 1.61 in the year

2011 to 1.50 in 2012. This reflects that Apple has to focus on managing its current assets

effectively in order to meet its short term obligations. Similarly, the quick ratio of the firm is also

decreasing from 1.58 to 1.48 in recent years. On the other side, the profitability ratios of Apple

shows an increasing trend which indicates that an enterprise is earning higher profits from one

period to another after paying off all its cost, expenses and the tax liability (Monahan, 2018).

The leverage position of Apple is seen as better because it has maintained adequate proportion of

the debt against its equities and its interest ratio is rising which clearly reflects that it has the

capability in meeting its interest expenses adequately because profits are increasing with greater

value. Moreover, it has been analysed from the evaluation that Apple is not efficient in turning

out its inventory into cash on a quack basis as its cost of sales is increasing which results to

increase in the ratio. Also it is not making effective use of its assets for increasing its sales.

Overall, the performance and position of Apple is becoming better as per the recent final reports.

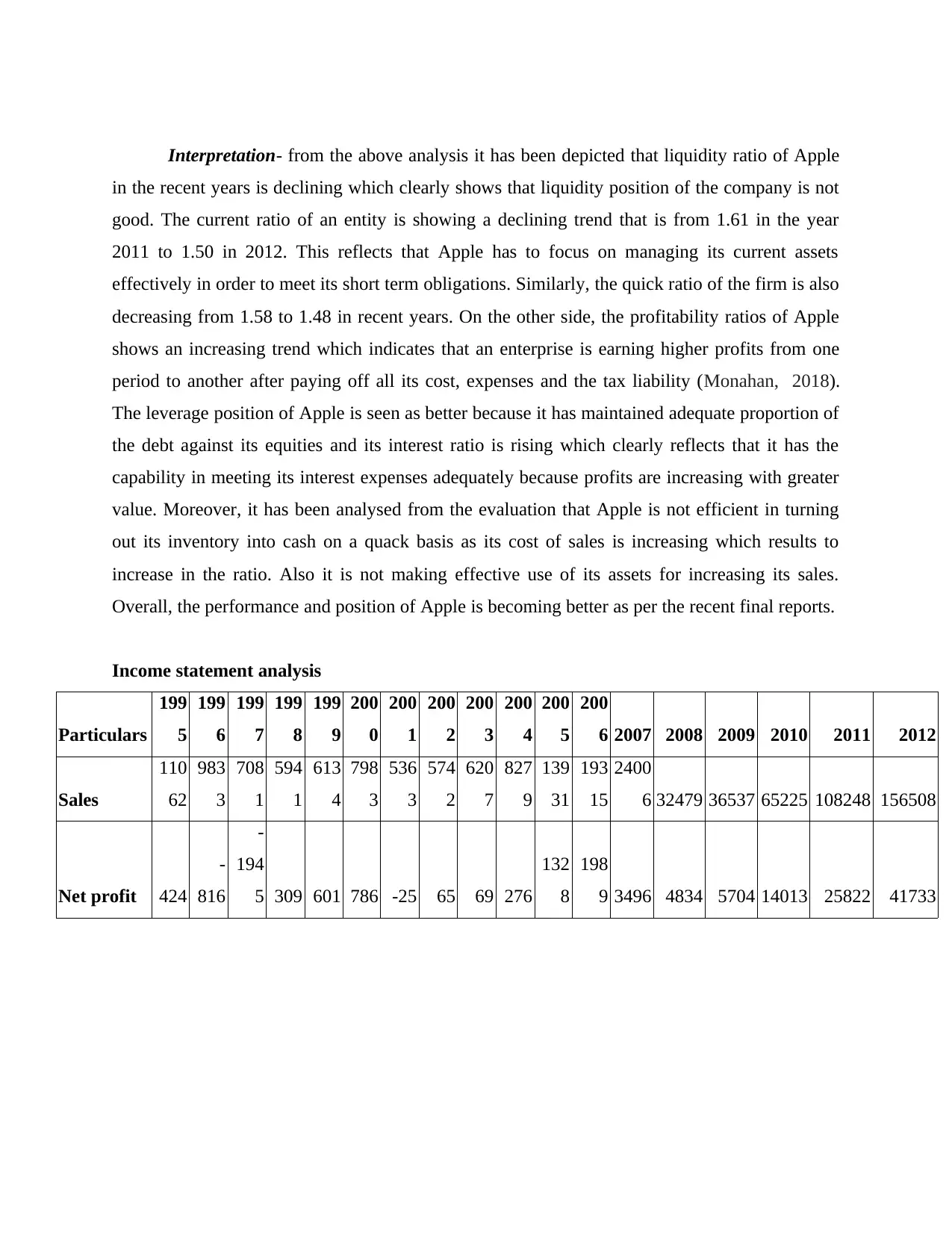

Income statement analysis

Particulars

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6 2007 2008 2009 2010 2011 2012

Sales

110

62

983

3

708

1

594

1

613

4

798

3

536

3

574

2

620

7

827

9

139

31

193

15

2400

6 32479 36537 65225 108248 156508

Net profit 424

-

816

-

194

5 309 601 786 -25 65 69 276

132

8

198

9 3496 4834 5704 14013 25822 41733

in the recent years is declining which clearly shows that liquidity position of the company is not

good. The current ratio of an entity is showing a declining trend that is from 1.61 in the year

2011 to 1.50 in 2012. This reflects that Apple has to focus on managing its current assets

effectively in order to meet its short term obligations. Similarly, the quick ratio of the firm is also

decreasing from 1.58 to 1.48 in recent years. On the other side, the profitability ratios of Apple

shows an increasing trend which indicates that an enterprise is earning higher profits from one

period to another after paying off all its cost, expenses and the tax liability (Monahan, 2018).

The leverage position of Apple is seen as better because it has maintained adequate proportion of

the debt against its equities and its interest ratio is rising which clearly reflects that it has the

capability in meeting its interest expenses adequately because profits are increasing with greater

value. Moreover, it has been analysed from the evaluation that Apple is not efficient in turning

out its inventory into cash on a quack basis as its cost of sales is increasing which results to

increase in the ratio. Also it is not making effective use of its assets for increasing its sales.

Overall, the performance and position of Apple is becoming better as per the recent final reports.

Income statement analysis

Particulars

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6 2007 2008 2009 2010 2011 2012

Sales

110

62

983

3

708

1

594

1

613

4

798

3

536

3

574

2

620

7

827

9

139

31

193

15

2400

6 32479 36537 65225 108248 156508

Net profit 424

-

816

-

194

5 309 601 786 -25 65 69 276

132

8

198

9 3496 4834 5704 14013 25822 41733

Interpretation- The above table shows that over the years from 1995 to 2012 the revenue

and the net profit of Apple seems to be increasing which clearly depicts that its performance with

passage of the years is becoming better and better. This seen as the positive sign for the firm as

its sales is getting higher which in turn leads to higher profits earned by the company. It clearly

reflects that performance of Apple has been improved within the period of 17 years that is 1995-

2012.

Balance sheet analysis

Particulars

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0 2011 2012

Assets

623

1

536

4

423

3

428

9

516

1

680

3

602

1

629

8

681

5

805

0

115

51

172

05

253

47

395

72

538

51

751

83

11637

1 176064

Liabilities

333

0

330

6

303

3

264

7

205

7

269

6

210

1

220

3

259

2

297

4

408

5

722

1

108

15

185

42

260

19

273

92 39756 57854

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

-20000

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

Sales

Net profit

and the net profit of Apple seems to be increasing which clearly depicts that its performance with

passage of the years is becoming better and better. This seen as the positive sign for the firm as

its sales is getting higher which in turn leads to higher profits earned by the company. It clearly

reflects that performance of Apple has been improved within the period of 17 years that is 1995-

2012.

Balance sheet analysis

Particulars

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0 2011 2012

Assets

623

1

536

4

423

3

428

9

516

1

680

3

602

1

629

8

681

5

805

0

115

51

172

05

253

47

395

72

538

51

751

83

11637

1 176064

Liabilities

333

0

330

6

303

3

264

7

205

7

269

6

210

1

220

3

259

2

297

4

408

5

722

1

108

15

185

42

260

19

273

92 39756 57854

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

-20000

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

Sales

Net profit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation- The above assessment shows that in between the period of 1995 and

2012, with increase in the assets, liabilities of the company also get increased. It has identified

that the change in the proportion of the assets is higher as compared to the proportion of the

liabilities (Ahmed and Safdar, 2018). This reflects that better financial state of Apple as its assets

are rising with a greater change and liabilities with less percentage change.

b. Stating the reason of issuing new common stock every year by Apple, despite the abundant

cash position and the shortage of requirement in raising an additional capital

Despite the abundant economic turmoil and the global financial crisis in the recent years,

Apple had kept on issuing new common stock because its value of stock reflected as increasing

or surging (West and Bhattacharya, 2016). This happens because particularly, an overwhelming

success of the iTunes, iPad, iPhone significantly boosted a share price.

c. With respect to Apple's peculiarities, stating the traditional ratio that might be hugely distorted

In accordance to the peculiarities, it has been stated that the ratio relating to net earning

would highly be distorted such as return on equity, profit margin and return on capital employed,

earning per shares etc. It is been analysed by viewing the final reports that shows in the previous

years the in respect to sales the net profit of the company resulted as very low or reflected a huge

amount of losses. Thus, the financial ratios that includes assessment of the net earnings with

respect to the sales, capital employed and an equity.

d. Assessing return on Equity of Apple on the basis of the book and market value

As per book value and

market value

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

Assets

Liabilities

2012, with increase in the assets, liabilities of the company also get increased. It has identified

that the change in the proportion of the assets is higher as compared to the proportion of the

liabilities (Ahmed and Safdar, 2018). This reflects that better financial state of Apple as its assets

are rising with a greater change and liabilities with less percentage change.

b. Stating the reason of issuing new common stock every year by Apple, despite the abundant

cash position and the shortage of requirement in raising an additional capital

Despite the abundant economic turmoil and the global financial crisis in the recent years,

Apple had kept on issuing new common stock because its value of stock reflected as increasing

or surging (West and Bhattacharya, 2016). This happens because particularly, an overwhelming

success of the iTunes, iPad, iPhone significantly boosted a share price.

c. With respect to Apple's peculiarities, stating the traditional ratio that might be hugely distorted

In accordance to the peculiarities, it has been stated that the ratio relating to net earning

would highly be distorted such as return on equity, profit margin and return on capital employed,

earning per shares etc. It is been analysed by viewing the final reports that shows in the previous

years the in respect to sales the net profit of the company resulted as very low or reflected a huge

amount of losses. Thus, the financial ratios that includes assessment of the net earnings with

respect to the sales, capital employed and an equity.

d. Assessing return on Equity of Apple on the basis of the book and market value

As per book value and

market value

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

Assets

Liabilities

Particulars Formula 2011 2012

Net income 25922 41733

Shareholders funds 76615 118210

Return on equity

Net

income/Shareholders

funds 33.83% 35.30%

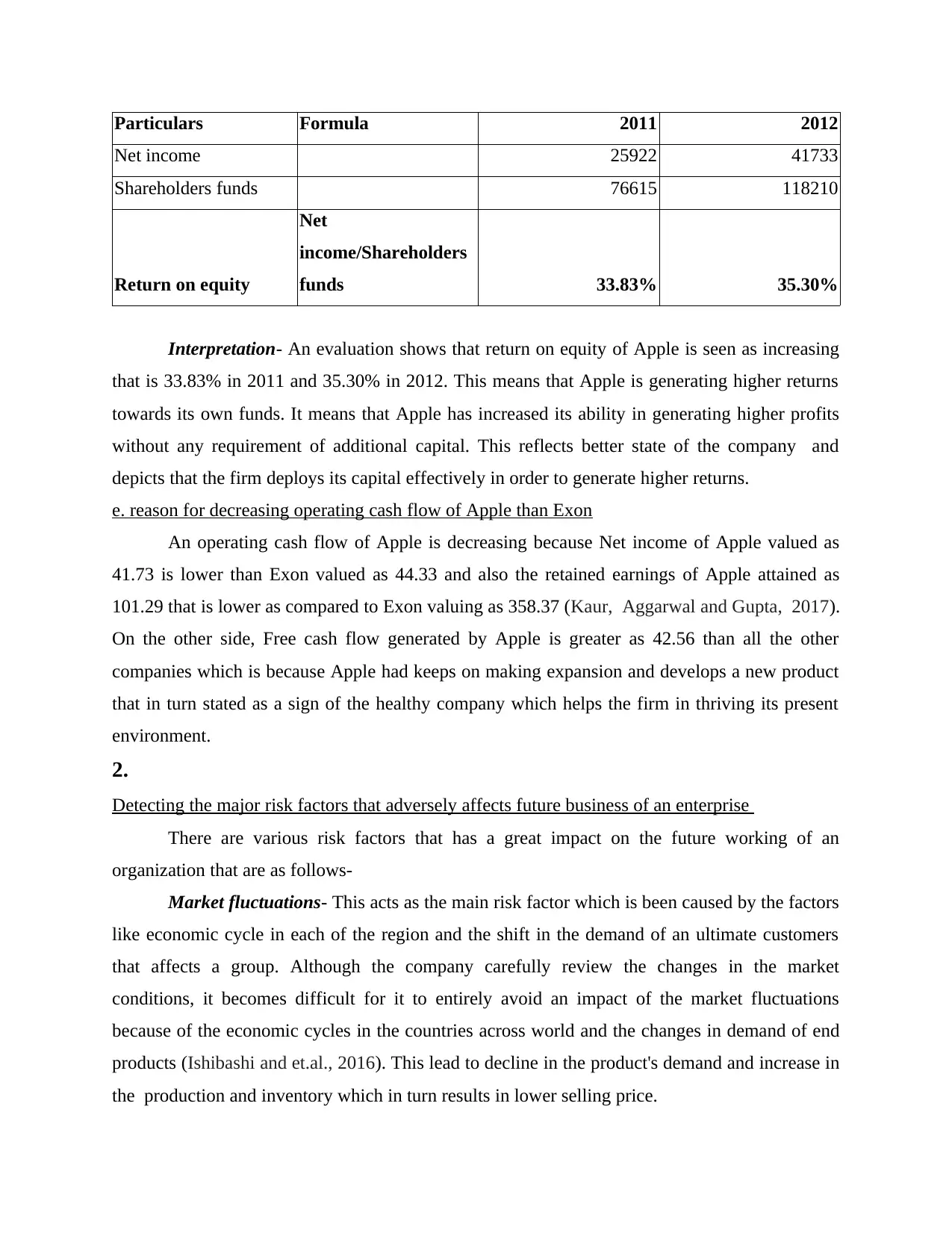

Interpretation- An evaluation shows that return on equity of Apple is seen as increasing

that is 33.83% in 2011 and 35.30% in 2012. This means that Apple is generating higher returns

towards its own funds. It means that Apple has increased its ability in generating higher profits

without any requirement of additional capital. This reflects better state of the company and

depicts that the firm deploys its capital effectively in order to generate higher returns.

e. reason for decreasing operating cash flow of Apple than Exon

An operating cash flow of Apple is decreasing because Net income of Apple valued as

41.73 is lower than Exon valued as 44.33 and also the retained earnings of Apple attained as

101.29 that is lower as compared to Exon valuing as 358.37 (Kaur, Aggarwal and Gupta, 2017).

On the other side, Free cash flow generated by Apple is greater as 42.56 than all the other

companies which is because Apple had keeps on making expansion and develops a new product

that in turn stated as a sign of the healthy company which helps the firm in thriving its present

environment.

2.

Detecting the major risk factors that adversely affects future business of an enterprise

There are various risk factors that has a great impact on the future working of an

organization that are as follows-

Market fluctuations- This acts as the main risk factor which is been caused by the factors

like economic cycle in each of the region and the shift in the demand of an ultimate customers

that affects a group. Although the company carefully review the changes in the market

conditions, it becomes difficult for it to entirely avoid an impact of the market fluctuations

because of the economic cycles in the countries across world and the changes in demand of end

products (Ishibashi and et.al., 2016). This lead to decline in the product's demand and increase in

the production and inventory which in turn results in lower selling price.

Net income 25922 41733

Shareholders funds 76615 118210

Return on equity

Net

income/Shareholders

funds 33.83% 35.30%

Interpretation- An evaluation shows that return on equity of Apple is seen as increasing

that is 33.83% in 2011 and 35.30% in 2012. This means that Apple is generating higher returns

towards its own funds. It means that Apple has increased its ability in generating higher profits

without any requirement of additional capital. This reflects better state of the company and

depicts that the firm deploys its capital effectively in order to generate higher returns.

e. reason for decreasing operating cash flow of Apple than Exon

An operating cash flow of Apple is decreasing because Net income of Apple valued as

41.73 is lower than Exon valued as 44.33 and also the retained earnings of Apple attained as

101.29 that is lower as compared to Exon valuing as 358.37 (Kaur, Aggarwal and Gupta, 2017).

On the other side, Free cash flow generated by Apple is greater as 42.56 than all the other

companies which is because Apple had keeps on making expansion and develops a new product

that in turn stated as a sign of the healthy company which helps the firm in thriving its present

environment.

2.

Detecting the major risk factors that adversely affects future business of an enterprise

There are various risk factors that has a great impact on the future working of an

organization that are as follows-

Market fluctuations- This acts as the main risk factor which is been caused by the factors

like economic cycle in each of the region and the shift in the demand of an ultimate customers

that affects a group. Although the company carefully review the changes in the market

conditions, it becomes difficult for it to entirely avoid an impact of the market fluctuations

because of the economic cycles in the countries across world and the changes in demand of end

products (Ishibashi and et.al., 2016). This lead to decline in the product's demand and increase in

the production and inventory which in turn results in lower selling price.

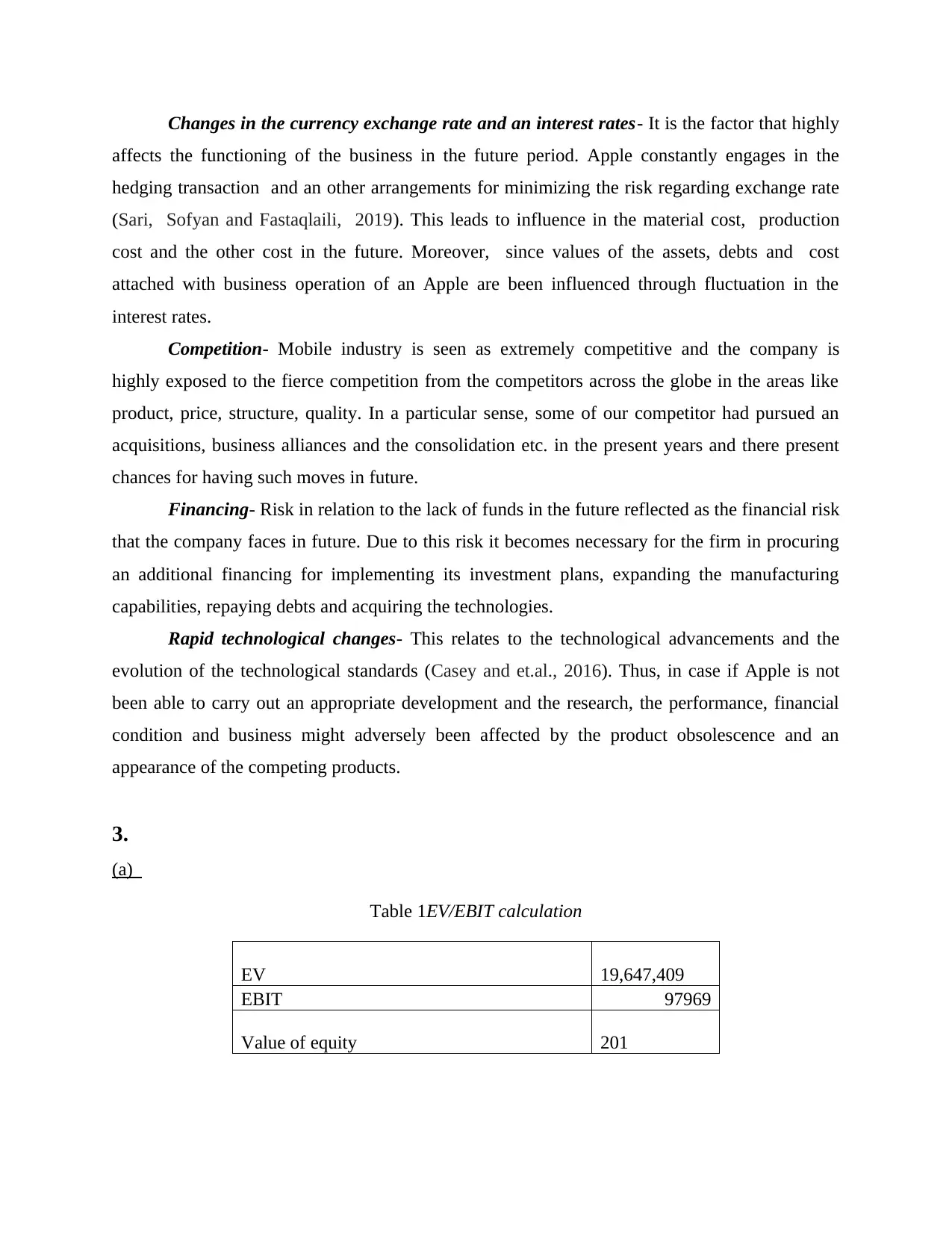

Changes in the currency exchange rate and an interest rates- It is the factor that highly

affects the functioning of the business in the future period. Apple constantly engages in the

hedging transaction and an other arrangements for minimizing the risk regarding exchange rate

(Sari, Sofyan and Fastaqlaili, 2019). This leads to influence in the material cost, production

cost and the other cost in the future. Moreover, since values of the assets, debts and cost

attached with business operation of an Apple are been influenced through fluctuation in the

interest rates.

Competition- Mobile industry is seen as extremely competitive and the company is

highly exposed to the fierce competition from the competitors across the globe in the areas like

product, price, structure, quality. In a particular sense, some of our competitor had pursued an

acquisitions, business alliances and the consolidation etc. in the present years and there present

chances for having such moves in future.

Financing- Risk in relation to the lack of funds in the future reflected as the financial risk

that the company faces in future. Due to this risk it becomes necessary for the firm in procuring

an additional financing for implementing its investment plans, expanding the manufacturing

capabilities, repaying debts and acquiring the technologies.

Rapid technological changes- This relates to the technological advancements and the

evolution of the technological standards (Casey and et.al., 2016). Thus, in case if Apple is not

been able to carry out an appropriate development and the research, the performance, financial

condition and business might adversely been affected by the product obsolescence and an

appearance of the competing products.

3.

(a)

Table 1EV/EBIT calculation

EV 19,647,409

EBIT 97969

Value of equity 201

affects the functioning of the business in the future period. Apple constantly engages in the

hedging transaction and an other arrangements for minimizing the risk regarding exchange rate

(Sari, Sofyan and Fastaqlaili, 2019). This leads to influence in the material cost, production

cost and the other cost in the future. Moreover, since values of the assets, debts and cost

attached with business operation of an Apple are been influenced through fluctuation in the

interest rates.

Competition- Mobile industry is seen as extremely competitive and the company is

highly exposed to the fierce competition from the competitors across the globe in the areas like

product, price, structure, quality. In a particular sense, some of our competitor had pursued an

acquisitions, business alliances and the consolidation etc. in the present years and there present

chances for having such moves in future.

Financing- Risk in relation to the lack of funds in the future reflected as the financial risk

that the company faces in future. Due to this risk it becomes necessary for the firm in procuring

an additional financing for implementing its investment plans, expanding the manufacturing

capabilities, repaying debts and acquiring the technologies.

Rapid technological changes- This relates to the technological advancements and the

evolution of the technological standards (Casey and et.al., 2016). Thus, in case if Apple is not

been able to carry out an appropriate development and the research, the performance, financial

condition and business might adversely been affected by the product obsolescence and an

appearance of the competing products.

3.

(a)

Table 1EV/EBIT calculation

EV 19,647,409

EBIT 97969

Value of equity 201

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

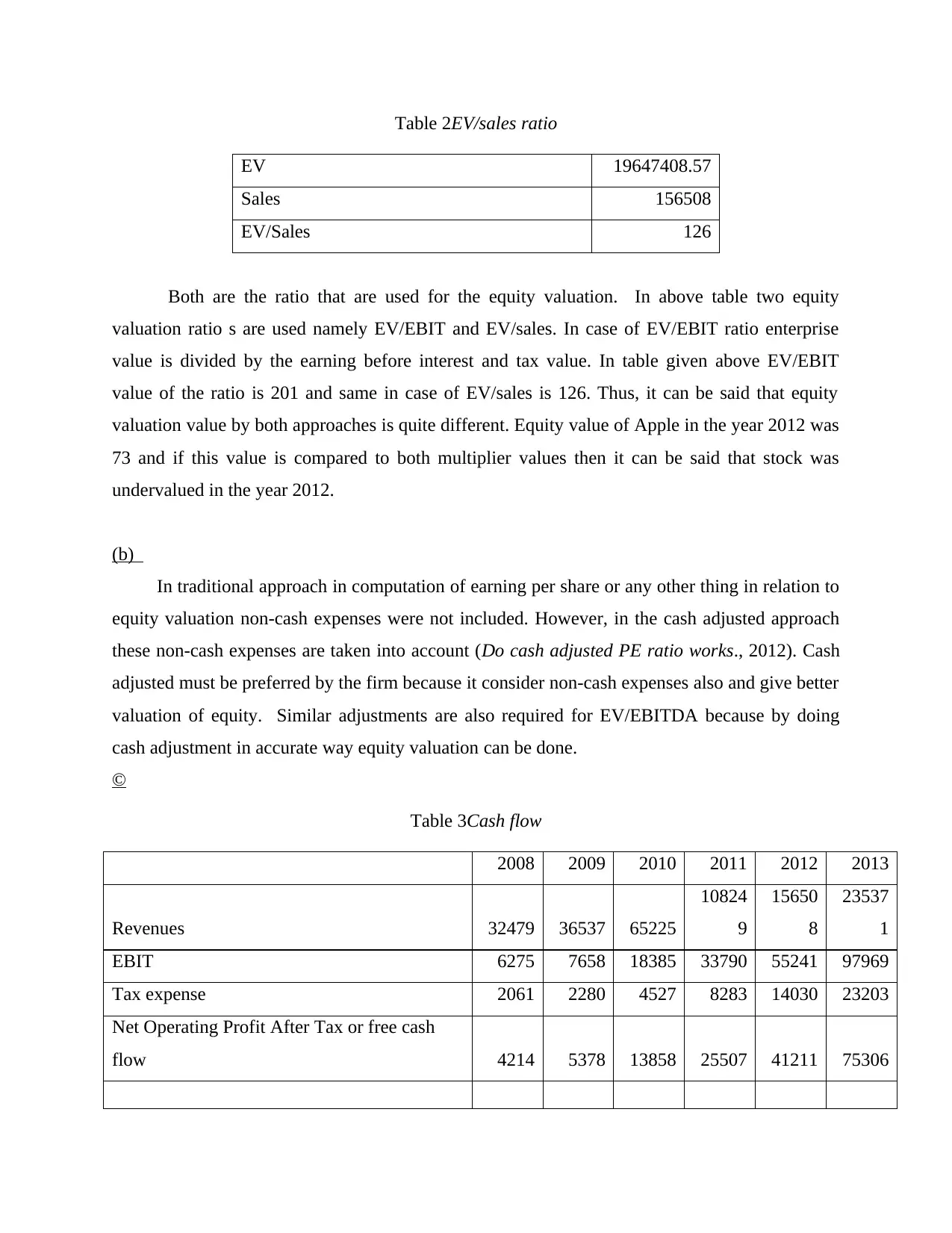

Table 2EV/sales ratio

EV 19647408.57

Sales 156508

EV/Sales 126

Both are the ratio that are used for the equity valuation. In above table two equity

valuation ratio s are used namely EV/EBIT and EV/sales. In case of EV/EBIT ratio enterprise

value is divided by the earning before interest and tax value. In table given above EV/EBIT

value of the ratio is 201 and same in case of EV/sales is 126. Thus, it can be said that equity

valuation value by both approaches is quite different. Equity value of Apple in the year 2012 was

73 and if this value is compared to both multiplier values then it can be said that stock was

undervalued in the year 2012.

(b)

In traditional approach in computation of earning per share or any other thing in relation to

equity valuation non-cash expenses were not included. However, in the cash adjusted approach

these non-cash expenses are taken into account (Do cash adjusted PE ratio works., 2012). Cash

adjusted must be preferred by the firm because it consider non-cash expenses also and give better

valuation of equity. Similar adjustments are also required for EV/EBITDA because by doing

cash adjustment in accurate way equity valuation can be done.

©

Table 3Cash flow

2008 2009 2010 2011 2012 2013

Revenues 32479 36537 65225

10824

9

15650

8

23537

1

EBIT 6275 7658 18385 33790 55241 97969

Tax expense 2061 2280 4527 8283 14030 23203

Net Operating Profit After Tax or free cash

flow 4214 5378 13858 25507 41211 75306

EV 19647408.57

Sales 156508

EV/Sales 126

Both are the ratio that are used for the equity valuation. In above table two equity

valuation ratio s are used namely EV/EBIT and EV/sales. In case of EV/EBIT ratio enterprise

value is divided by the earning before interest and tax value. In table given above EV/EBIT

value of the ratio is 201 and same in case of EV/sales is 126. Thus, it can be said that equity

valuation value by both approaches is quite different. Equity value of Apple in the year 2012 was

73 and if this value is compared to both multiplier values then it can be said that stock was

undervalued in the year 2012.

(b)

In traditional approach in computation of earning per share or any other thing in relation to

equity valuation non-cash expenses were not included. However, in the cash adjusted approach

these non-cash expenses are taken into account (Do cash adjusted PE ratio works., 2012). Cash

adjusted must be preferred by the firm because it consider non-cash expenses also and give better

valuation of equity. Similar adjustments are also required for EV/EBITDA because by doing

cash adjustment in accurate way equity valuation can be done.

©

Table 3Cash flow

2008 2009 2010 2011 2012 2013

Revenues 32479 36537 65225

10824

9

15650

8

23537

1

EBIT 6275 7658 18385 33790 55241 97969

Tax expense 2061 2280 4527 8283 14030 23203

Net Operating Profit After Tax or free cash

flow 4214 5378 13858 25507 41211 75306

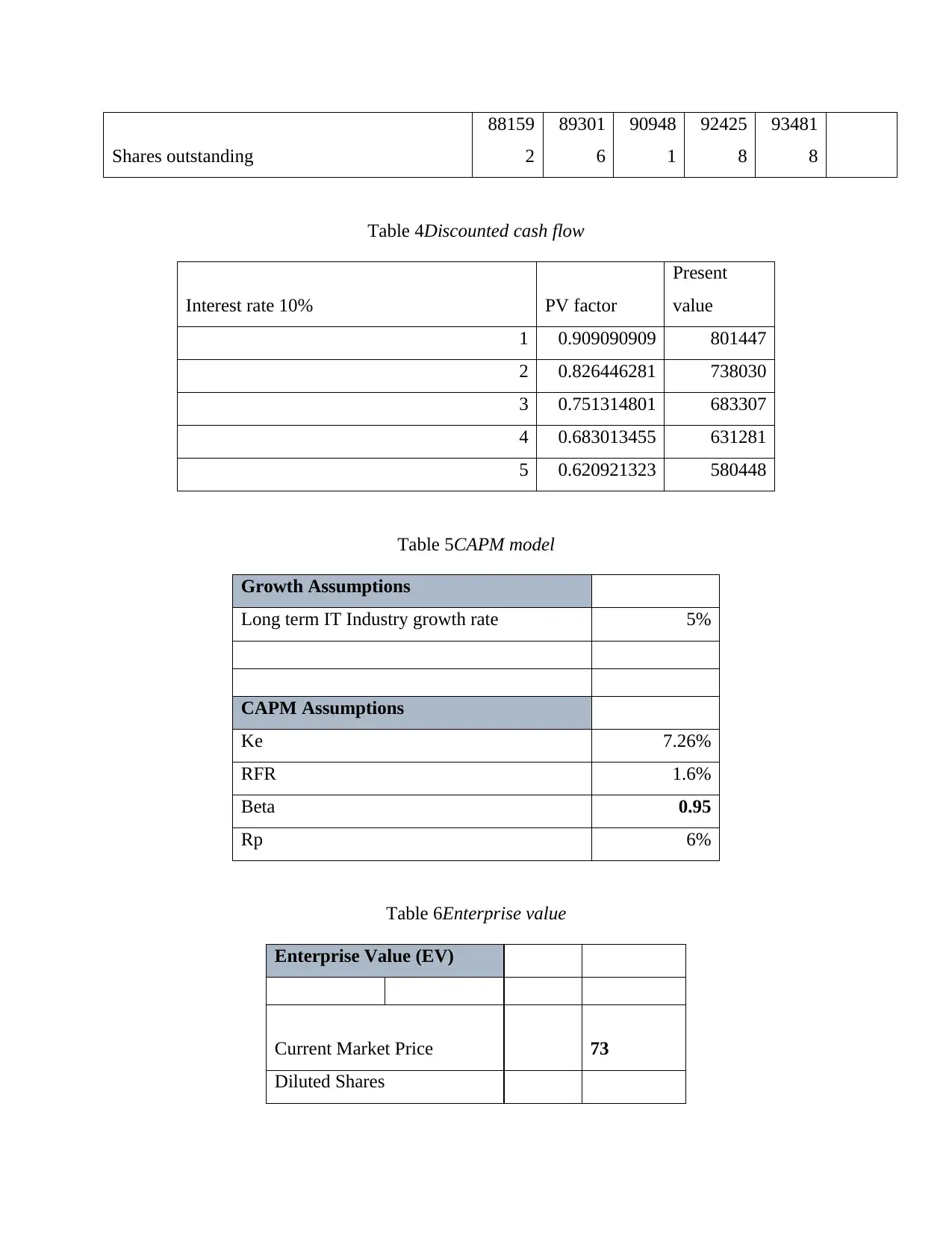

Shares outstanding

88159

2

89301

6

90948

1

92425

8

93481

8

Table 4Discounted cash flow

Interest rate 10% PV factor

Present

value

1 0.909090909 801447

2 0.826446281 738030

3 0.751314801 683307

4 0.683013455 631281

5 0.620921323 580448

Table 5CAPM model

Growth Assumptions

Long term IT Industry growth rate 5%

CAPM Assumptions

Ke 7.26%

RFR 1.6%

Beta 0.95

Rp 6%

Table 6Enterprise value

Enterprise Value (EV)

Current Market Price 73

Diluted Shares

88159

2

89301

6

90948

1

92425

8

93481

8

Table 4Discounted cash flow

Interest rate 10% PV factor

Present

value

1 0.909090909 801447

2 0.826446281 738030

3 0.751314801 683307

4 0.683013455 631281

5 0.620921323 580448

Table 5CAPM model

Growth Assumptions

Long term IT Industry growth rate 5%

CAPM Assumptions

Ke 7.26%

RFR 1.6%

Beta 0.95

Rp 6%

Table 6Enterprise value

Enterprise Value (EV)

Current Market Price 73

Diluted Shares

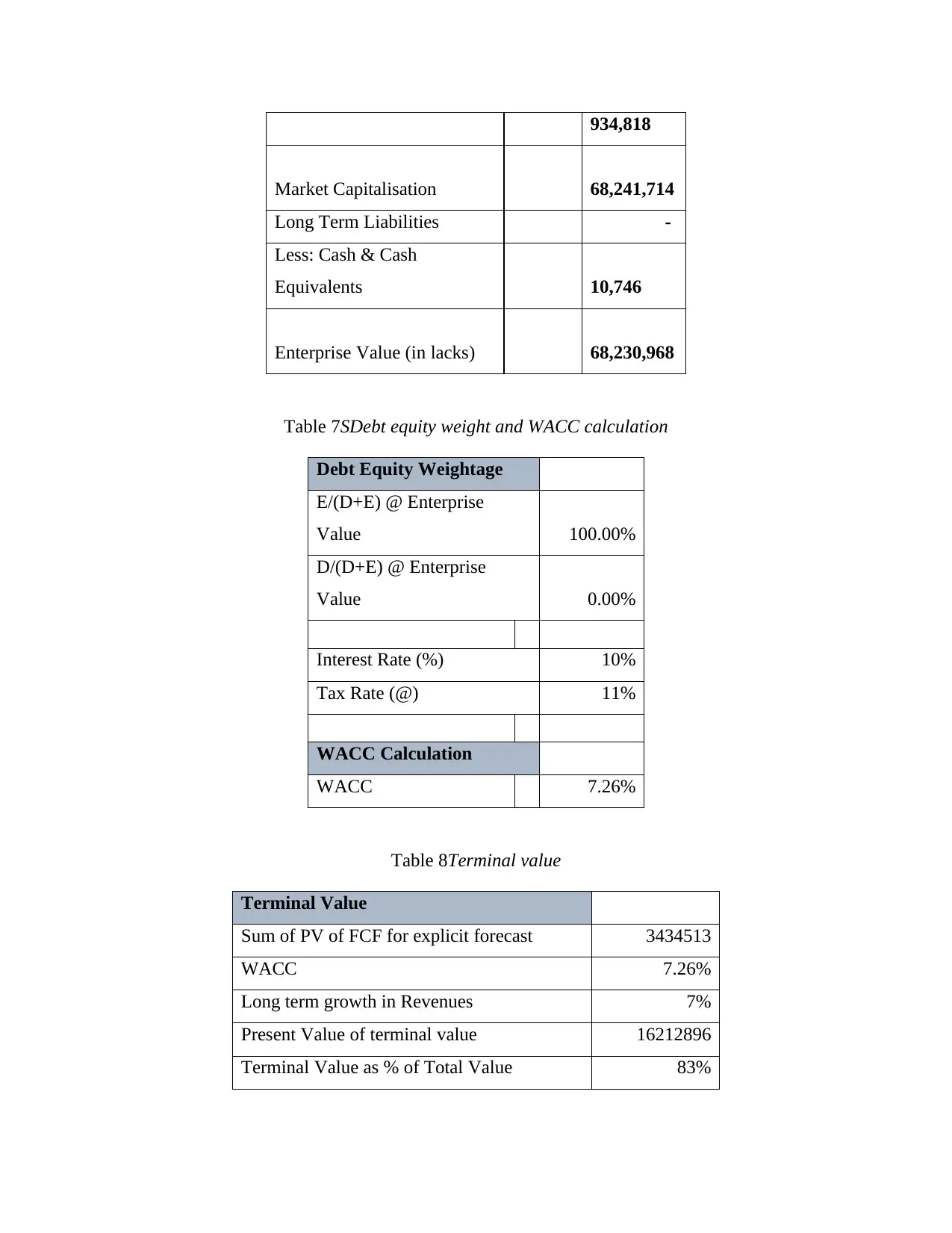

934,818

Market Capitalisation 68,241,714

Long Term Liabilities -

Less: Cash & Cash

Equivalents 10,746

Enterprise Value (in lacks) 68,230,968

Table 7SDebt equity weight and WACC calculation

Debt Equity Weightage

E/(D+E) @ Enterprise

Value 100.00%

D/(D+E) @ Enterprise

Value 0.00%

Interest Rate (%) 10%

Tax Rate (@) 11%

WACC Calculation

WACC 7.26%

Table 8Terminal value

Terminal Value

Sum of PV of FCF for explicit forecast 3434513

WACC 7.26%

Long term growth in Revenues 7%

Present Value of terminal value 16212896

Terminal Value as % of Total Value 83%

Market Capitalisation 68,241,714

Long Term Liabilities -

Less: Cash & Cash

Equivalents 10,746

Enterprise Value (in lacks) 68,230,968

Table 7SDebt equity weight and WACC calculation

Debt Equity Weightage

E/(D+E) @ Enterprise

Value 100.00%

D/(D+E) @ Enterprise

Value 0.00%

Interest Rate (%) 10%

Tax Rate (@) 11%

WACC Calculation

WACC 7.26%

Table 8Terminal value

Terminal Value

Sum of PV of FCF for explicit forecast 3434513

WACC 7.26%

Long term growth in Revenues 7%

Present Value of terminal value 16212896

Terminal Value as % of Total Value 83%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

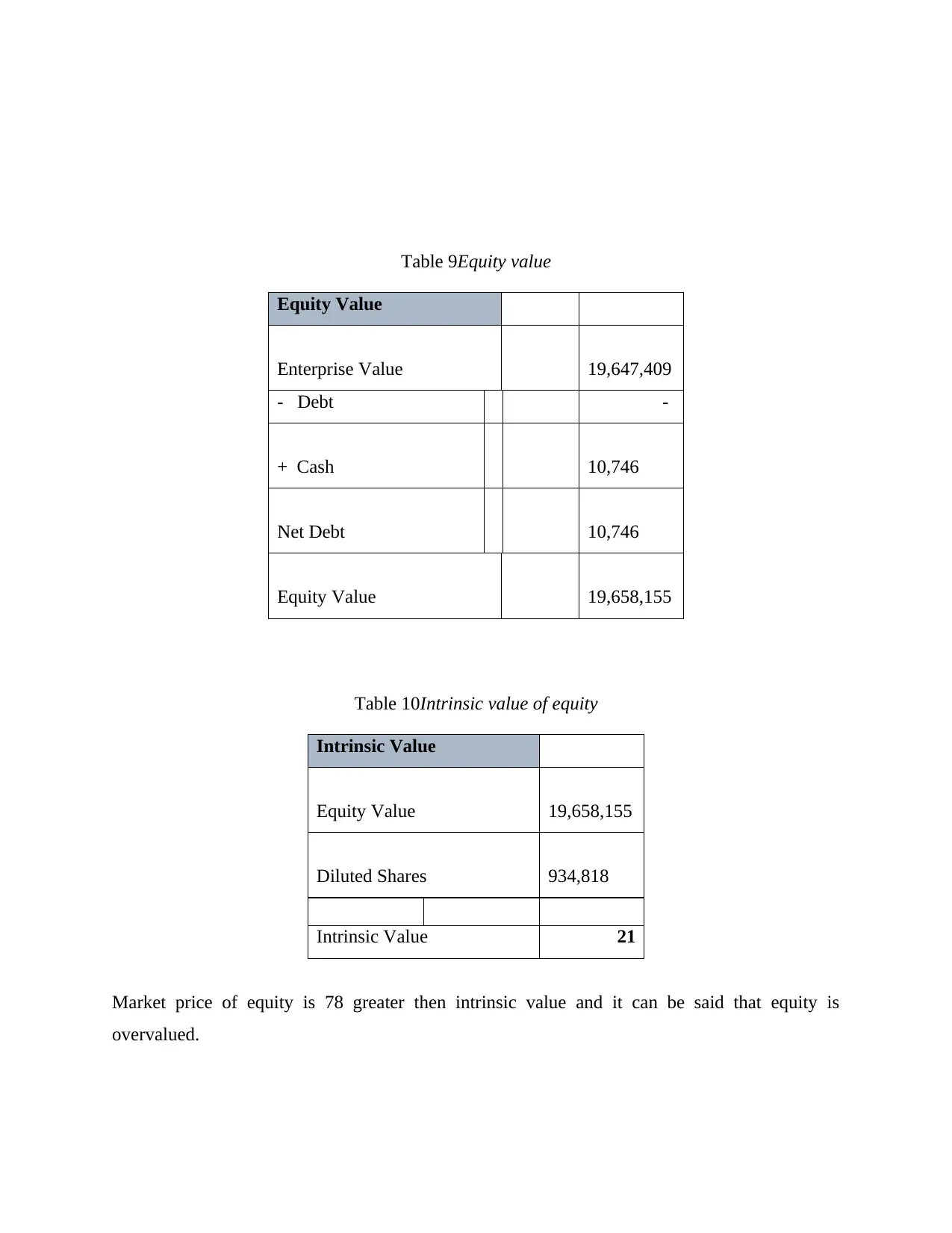

Table 9Equity value

Equity Value

Enterprise Value 19,647,409

- Debt -

+ Cash 10,746

Net Debt 10,746

Equity Value 19,658,155

Table 10Intrinsic value of equity

Intrinsic Value

Equity Value 19,658,155

Diluted Shares 934,818

Intrinsic Value 21

Market price of equity is 78 greater then intrinsic value and it can be said that equity is

overvalued.

Equity Value

Enterprise Value 19,647,409

- Debt -

+ Cash 10,746

Net Debt 10,746

Equity Value 19,658,155

Table 10Intrinsic value of equity

Intrinsic Value

Equity Value 19,658,155

Diluted Shares 934,818

Intrinsic Value 21

Market price of equity is 78 greater then intrinsic value and it can be said that equity is

overvalued.

(4)

Stock split happened to curb multiple times increase in stock price. Reverse stock split is

done to elevate equity price (Apple stock split history what you need to know., 2019). When

stock price is too low and company intend to increase price, it combine equity that is in market in

ratio 5 to 1 etc which lead to increase in price of shares.

4.

a. representing that Apple's cash pile comes at an expense of the shareholders

In my opinion, I believe that large amount of cash pile has been generated by Apple in

respect of the shareholder money. Apple serve as the caretakers for the cash which actually

belongs directly to its shareholders. With the Brae-burn Capital, an asset management company

is been founded in the year 2006 for managing its parent company and the growing cash pile on a

quick basis, the firm owns for world's largest or highest hedge funds.

5.

a. Analysing past and the new dividend policy of Apple

In past period it has been seen that Apple followed a stable dividend policy where it

distributes a stable amount of dividend every years. However, in the year 2012, the board of

directors has approved a dividend policy as per planned by CEO with subject to the subsequent

declaration, amounting to quarterly dividend of $ 2.65 per share. The new dividend policy seems

to be better for the shareholders because they would be getting dividends on the quarterly basis

with a higher return and not a stable amount of dividend.

b. Explaining the foremost objective of the share repurchase program and the way in which it is

financed

In the year march 2012, BODs are authorized with the program for repurchasing $ 10

billion of the common stock of company in beginning of 2013. The program relating to

repurchase is been expected to implement over the period of three years with an objective of

neutralizing an effect of the dilution from the equity grants of future employee and stock

purchase program of an employee (West and Bhattacharya, 2016). Apple anticipated that it

would be using around $ 45 billion of the domestic cash in paying the dividends, repurchasing

shares and in remitting the withheld taxes in relation to the net share settlement of the restricted

units of stock in first 3 years of dividend and the repurchase program regarding stock. This

Stock split happened to curb multiple times increase in stock price. Reverse stock split is

done to elevate equity price (Apple stock split history what you need to know., 2019). When

stock price is too low and company intend to increase price, it combine equity that is in market in

ratio 5 to 1 etc which lead to increase in price of shares.

4.

a. representing that Apple's cash pile comes at an expense of the shareholders

In my opinion, I believe that large amount of cash pile has been generated by Apple in

respect of the shareholder money. Apple serve as the caretakers for the cash which actually

belongs directly to its shareholders. With the Brae-burn Capital, an asset management company

is been founded in the year 2006 for managing its parent company and the growing cash pile on a

quick basis, the firm owns for world's largest or highest hedge funds.

5.

a. Analysing past and the new dividend policy of Apple

In past period it has been seen that Apple followed a stable dividend policy where it

distributes a stable amount of dividend every years. However, in the year 2012, the board of

directors has approved a dividend policy as per planned by CEO with subject to the subsequent

declaration, amounting to quarterly dividend of $ 2.65 per share. The new dividend policy seems

to be better for the shareholders because they would be getting dividends on the quarterly basis

with a higher return and not a stable amount of dividend.

b. Explaining the foremost objective of the share repurchase program and the way in which it is

financed

In the year march 2012, BODs are authorized with the program for repurchasing $ 10

billion of the common stock of company in beginning of 2013. The program relating to

repurchase is been expected to implement over the period of three years with an objective of

neutralizing an effect of the dilution from the equity grants of future employee and stock

purchase program of an employee (West and Bhattacharya, 2016). Apple anticipated that it

would be using around $ 45 billion of the domestic cash in paying the dividends, repurchasing

shares and in remitting the withheld taxes in relation to the net share settlement of the restricted

units of stock in first 3 years of dividend and the repurchase program regarding stock. This

program is financed from the present domestic cash and from an ongoing operating activities of

US and generated cash from these activities.

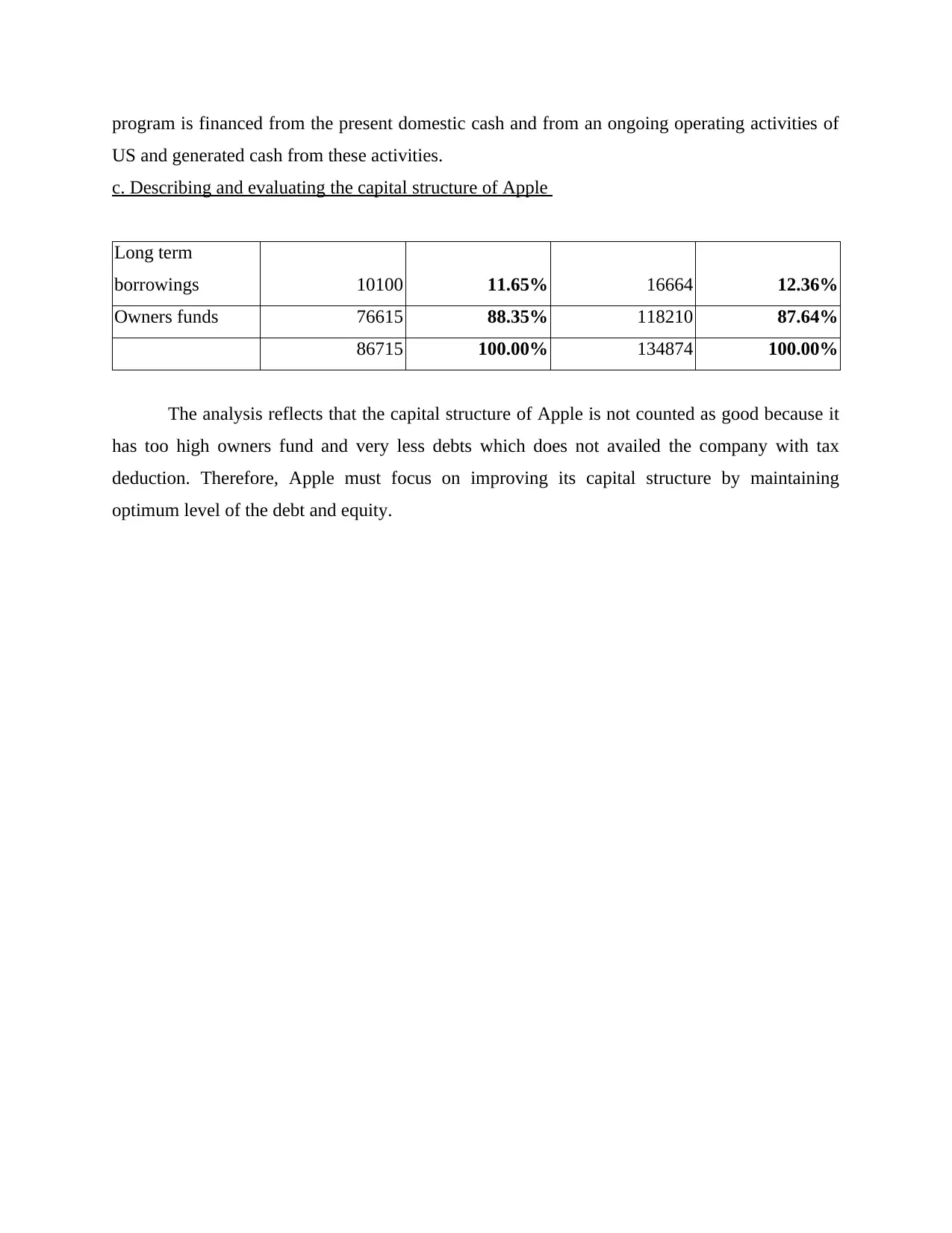

c. Describing and evaluating the capital structure of Apple

Long term

borrowings 10100 11.65% 16664 12.36%

Owners funds 76615 88.35% 118210 87.64%

86715 100.00% 134874 100.00%

The analysis reflects that the capital structure of Apple is not counted as good because it

has too high owners fund and very less debts which does not availed the company with tax

deduction. Therefore, Apple must focus on improving its capital structure by maintaining

optimum level of the debt and equity.

US and generated cash from these activities.

c. Describing and evaluating the capital structure of Apple

Long term

borrowings 10100 11.65% 16664 12.36%

Owners funds 76615 88.35% 118210 87.64%

86715 100.00% 134874 100.00%

The analysis reflects that the capital structure of Apple is not counted as good because it

has too high owners fund and very less debts which does not availed the company with tax

deduction. Therefore, Apple must focus on improving its capital structure by maintaining

optimum level of the debt and equity.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and journals

Ahmed, A. S. and Safdar, I., 2018. Dissecting stock price momentum using financial statement

analysis. Accounting & Finance. 58. pp.3-43.

Casey, R. J. and et.al., 2016. Do Compustat financial statement data articulate?. Journal of

Financial Reporting. 1(1). pp.37-59.

Ishibashi, K. and et.al., 2016. Model selection for financial statement analysis: Variable

selection with data mining technique. Procedia Computer Science. 96. pp.1681-1690.

Kaur, M., Aggarwal, N. and Gupta, M., 2017. An Investigation into Returns from Financial

Statement Analysis among High Book-to-Market Stocks. Indian Journal of Economics

and Development. 13(2). pp.353-358.

Monahan, S. J., 2018. Financial Statement Analysis and Earnings Forecasting. Foundations and

Trends® in Accounting. 12(2). pp.105-215.

Sari, N. S., Sofyan, A. and Fastaqlaili, N., 2019. ANALYSIS OF FRAUD DIAMOND

DIMENSION IN DETECTING FINANCIAL STATEMENT FRAUD. Jurnal Akuntansi

Trisakti. 5(2). pp.171-182.

West, J. and Bhattacharya, M., 2016. Intelligent financial fraud detection: a comprehensive

review. Computers & security. 57. pp.47-66.

Online

Apple stock split history what you need to know., 2019. [Online]. Available through:<

https://www.ig.com/en/news-and-trade-ideas/shares-news/apple-stock-split-history--what-

you-need-to-know-190523>.

Do cash adjusted PE ratio works., 2012. [Online]. Available through:

<https://alphaarchitect.com/2012/05/22/do-cash-adjusted-pe-ratios-work/>.

Books and journals

Ahmed, A. S. and Safdar, I., 2018. Dissecting stock price momentum using financial statement

analysis. Accounting & Finance. 58. pp.3-43.

Casey, R. J. and et.al., 2016. Do Compustat financial statement data articulate?. Journal of

Financial Reporting. 1(1). pp.37-59.

Ishibashi, K. and et.al., 2016. Model selection for financial statement analysis: Variable

selection with data mining technique. Procedia Computer Science. 96. pp.1681-1690.

Kaur, M., Aggarwal, N. and Gupta, M., 2017. An Investigation into Returns from Financial

Statement Analysis among High Book-to-Market Stocks. Indian Journal of Economics

and Development. 13(2). pp.353-358.

Monahan, S. J., 2018. Financial Statement Analysis and Earnings Forecasting. Foundations and

Trends® in Accounting. 12(2). pp.105-215.

Sari, N. S., Sofyan, A. and Fastaqlaili, N., 2019. ANALYSIS OF FRAUD DIAMOND

DIMENSION IN DETECTING FINANCIAL STATEMENT FRAUD. Jurnal Akuntansi

Trisakti. 5(2). pp.171-182.

West, J. and Bhattacharya, M., 2016. Intelligent financial fraud detection: a comprehensive

review. Computers & security. 57. pp.47-66.

Online

Apple stock split history what you need to know., 2019. [Online]. Available through:<

https://www.ig.com/en/news-and-trade-ideas/shares-news/apple-stock-split-history--what-

you-need-to-know-190523>.

Do cash adjusted PE ratio works., 2012. [Online]. Available through:

<https://alphaarchitect.com/2012/05/22/do-cash-adjusted-pe-ratios-work/>.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.