Investment Analysis Report: Interest Rate and Currency Swaps

VerifiedAdded on 2020/01/07

|13

|4200

|261

Report

AI Summary

This report provides a detailed analysis of investment strategies using swaps, covering their definition, benefits, and different types. The methodology section explains the meaning of swaps as derivative contracts used to exchange financial instruments and mitigate risks. The report explores the benefits of swaps, including risk management, financing access, cost-effectiveness, and long-term advantages. It then delves into the main types of swaps, such as interest rate swaps and currency swaps, with detailed analysis and findings. The report highlights how interest rate swaps can be used to hedge interest rate risk, providing a practical example with calculations. Furthermore, it examines currency swaps and their application in hedging currency risk, including a case study of a UK and Australian firm. The conclusion summarizes the key findings, followed by recommendations for effective swap utilization. The report aims to provide a comprehensive understanding of swaps as valuable financial instruments for risk management and investment analysis.

INVESTMENT ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................3

METHODOLOGY.....................................................................................................................3

Meaning of swaps ............................................................................................................3

Benefits of swaps..............................................................................................................3

Main types of swaps, analysis and findings......................................................................4

Interest rate risk hedging with the use of swaps...............................................................5

Currency risk hedging with swap.....................................................................................7

CONCLUSION........................................................................................................................10

RECOMMENDATIONS.........................................................................................................11

REFERENCES.........................................................................................................................12

INTRODUCTION......................................................................................................................3

METHODOLOGY.....................................................................................................................3

Meaning of swaps ............................................................................................................3

Benefits of swaps..............................................................................................................3

Main types of swaps, analysis and findings......................................................................4

Interest rate risk hedging with the use of swaps...............................................................5

Currency risk hedging with swap.....................................................................................7

CONCLUSION........................................................................................................................10

RECOMMENDATIONS.........................................................................................................11

REFERENCES.........................................................................................................................12

INTRODUCTION

In the present market, changes take place at a faster rate because of complexity and

uncertainty in the business environment. Therefore, organization uses variety of financial

instruments such as swaps, futures and forward contracts etc. to hedge different types of

business risks. Out of these, swaps is greatly using in the present market. It is a derivative

contract in which two counter parties can exchange their financial instruments to mitigate

their risks. Present project report will discuss the application of distinct types of swaps and its

benefits in the corporation. Moreover, the report will make in-depth evaluation that how

swaps can be used to hedge risks such as currency and inflation risks in the business.

METHODOLOGY

Meaning of swaps

Swaps is a derivative contract through which one party can exchange their cash flows

associated with their financial instrument with other person. It is a contract in which two

parties will be agreed to exchange their financial instruments with each other on a

predetermined date that is specified in the contract. It is greatly using in the current market by

all the business organizations to hedge against risk (Aıt-Sahalia, Karaman and Mancini,

2014). Swaps contract can be made for different types of financial instruments but essential

thing is that cash flows on one financial instrument must be fixed and other must be

uncertain. For instance, in case of financial instrument that has fixed interest rate, their

associated cash flows will be certain. While, in case of instrument that has floating interest

rates, their associated cash flows will be uncertain. But still, notional principal amount on

both the financial instruments will be fixed and it will not be exchanged by both the counter

parties. Swaps are generally traded on over the counter (OTC) market between private

business entities (Kiesel, Lücke and Schiereck, 2015). In this contracts, difference between

cash flow streams is called swap legs.

Benefits of swaps

Swaps provides number of benefits to the private entities, some of them are described

below:

Risk management: Swaps greatly helps to reduce business risk so managing risk is

one of the most important benefits of swaps contracts (Biffis and et.al., 2015). For instance,

exchanging floating interest bearing security with the fixed interest bearing security eliminate

risks that can be arise due to volatility and fluctuation in interest rate. Thus, hedge against

In the present market, changes take place at a faster rate because of complexity and

uncertainty in the business environment. Therefore, organization uses variety of financial

instruments such as swaps, futures and forward contracts etc. to hedge different types of

business risks. Out of these, swaps is greatly using in the present market. It is a derivative

contract in which two counter parties can exchange their financial instruments to mitigate

their risks. Present project report will discuss the application of distinct types of swaps and its

benefits in the corporation. Moreover, the report will make in-depth evaluation that how

swaps can be used to hedge risks such as currency and inflation risks in the business.

METHODOLOGY

Meaning of swaps

Swaps is a derivative contract through which one party can exchange their cash flows

associated with their financial instrument with other person. It is a contract in which two

parties will be agreed to exchange their financial instruments with each other on a

predetermined date that is specified in the contract. It is greatly using in the current market by

all the business organizations to hedge against risk (Aıt-Sahalia, Karaman and Mancini,

2014). Swaps contract can be made for different types of financial instruments but essential

thing is that cash flows on one financial instrument must be fixed and other must be

uncertain. For instance, in case of financial instrument that has fixed interest rate, their

associated cash flows will be certain. While, in case of instrument that has floating interest

rates, their associated cash flows will be uncertain. But still, notional principal amount on

both the financial instruments will be fixed and it will not be exchanged by both the counter

parties. Swaps are generally traded on over the counter (OTC) market between private

business entities (Kiesel, Lücke and Schiereck, 2015). In this contracts, difference between

cash flow streams is called swap legs.

Benefits of swaps

Swaps provides number of benefits to the private entities, some of them are described

below:

Risk management: Swaps greatly helps to reduce business risk so managing risk is

one of the most important benefits of swaps contracts (Biffis and et.al., 2015). For instance,

exchanging floating interest bearing security with the fixed interest bearing security eliminate

risks that can be arise due to volatility and fluctuation in interest rate. Thus, hedge against

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

risk will result in rising profitability, potential and business performance as well. This in turn,

both the parties will be able to take benefits of improved financial position.

Financing access: Swaps also helps to provide advantage of financing access through

variable interest rate rather than fixed borrowings (Filipović, Gourier and Mancini, 2016). It

enables firms to enlarge their credit worthiness as per the management desires.

Cheaper: Swap includes some premium charges which counter parties need to be pay

as their transaction costs. Hence, very low amount of premium provides facility to hedge risk

at very cheaper rate.

Long term benefits: Swaps contract can be done for a longer duration comparatively

than other contracts such as future and forwards. It is because under the swap contracts,

counter parties can agree to exchange their cash flow streams with the cash flows of other

party's financial instrument till the maturity period which is often very longer period

(Arentsen and et.al., 2015). Thus, it is clear that swaps contract facilitates benefits for longer

period.

Main types of swaps, analysis and findings

There are wide range of swaps which can be used by the businesses to mitigate their

risks, these are explained below:

Interest rate swaps: It is a contractual agreement between two parties who are agreed

to exchange their financial instrument's cash flows with other person. In swap contracts, legs

are defined as series of related cash flows on party's financial assets such as bonds. Under the

interest rate swaps, one party's financial instrument contains fixed cash flows in terms of

fixed interest rate while other party's financial instrument has floating interest rate (Mele and

Obayashi, 2015). Hence, cash flows on fixed interest bearing security is known in advance

and cash flows on floating interest bearing security is an uncertain or random. Henceforth, in

this contract, counter parties will be agreed to exchange their fixed series of cash flows with

the other party's unknown cash payments. It helps to reduce risk against volatility in floating

interest rate through exchanging it with those of the other party's assets that have fixed

interest payments. Interest rate swaps focuses on all the conditions such as notional principal

amount, accrual method, effective date of contract, contract termination date, cash flow

frequency and basis of floating interest rate to administrate swaps effectively. Interest rate

swaps can be contracted for exchanging fixed cash flow stream with the floating interest

series (Byun and Chang, 2015). In the present market, interest rate fluctuation can be seen at

both the parties will be able to take benefits of improved financial position.

Financing access: Swaps also helps to provide advantage of financing access through

variable interest rate rather than fixed borrowings (Filipović, Gourier and Mancini, 2016). It

enables firms to enlarge their credit worthiness as per the management desires.

Cheaper: Swap includes some premium charges which counter parties need to be pay

as their transaction costs. Hence, very low amount of premium provides facility to hedge risk

at very cheaper rate.

Long term benefits: Swaps contract can be done for a longer duration comparatively

than other contracts such as future and forwards. It is because under the swap contracts,

counter parties can agree to exchange their cash flow streams with the cash flows of other

party's financial instrument till the maturity period which is often very longer period

(Arentsen and et.al., 2015). Thus, it is clear that swaps contract facilitates benefits for longer

period.

Main types of swaps, analysis and findings

There are wide range of swaps which can be used by the businesses to mitigate their

risks, these are explained below:

Interest rate swaps: It is a contractual agreement between two parties who are agreed

to exchange their financial instrument's cash flows with other person. In swap contracts, legs

are defined as series of related cash flows on party's financial assets such as bonds. Under the

interest rate swaps, one party's financial instrument contains fixed cash flows in terms of

fixed interest rate while other party's financial instrument has floating interest rate (Mele and

Obayashi, 2015). Hence, cash flows on fixed interest bearing security is known in advance

and cash flows on floating interest bearing security is an uncertain or random. Henceforth, in

this contract, counter parties will be agreed to exchange their fixed series of cash flows with

the other party's unknown cash payments. It helps to reduce risk against volatility in floating

interest rate through exchanging it with those of the other party's assets that have fixed

interest payments. Interest rate swaps focuses on all the conditions such as notional principal

amount, accrual method, effective date of contract, contract termination date, cash flow

frequency and basis of floating interest rate to administrate swaps effectively. Interest rate

swaps can be contracted for exchanging fixed cash flow stream with the floating interest

series (Byun and Chang, 2015). In the present market, interest rate fluctuation can be seen at

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

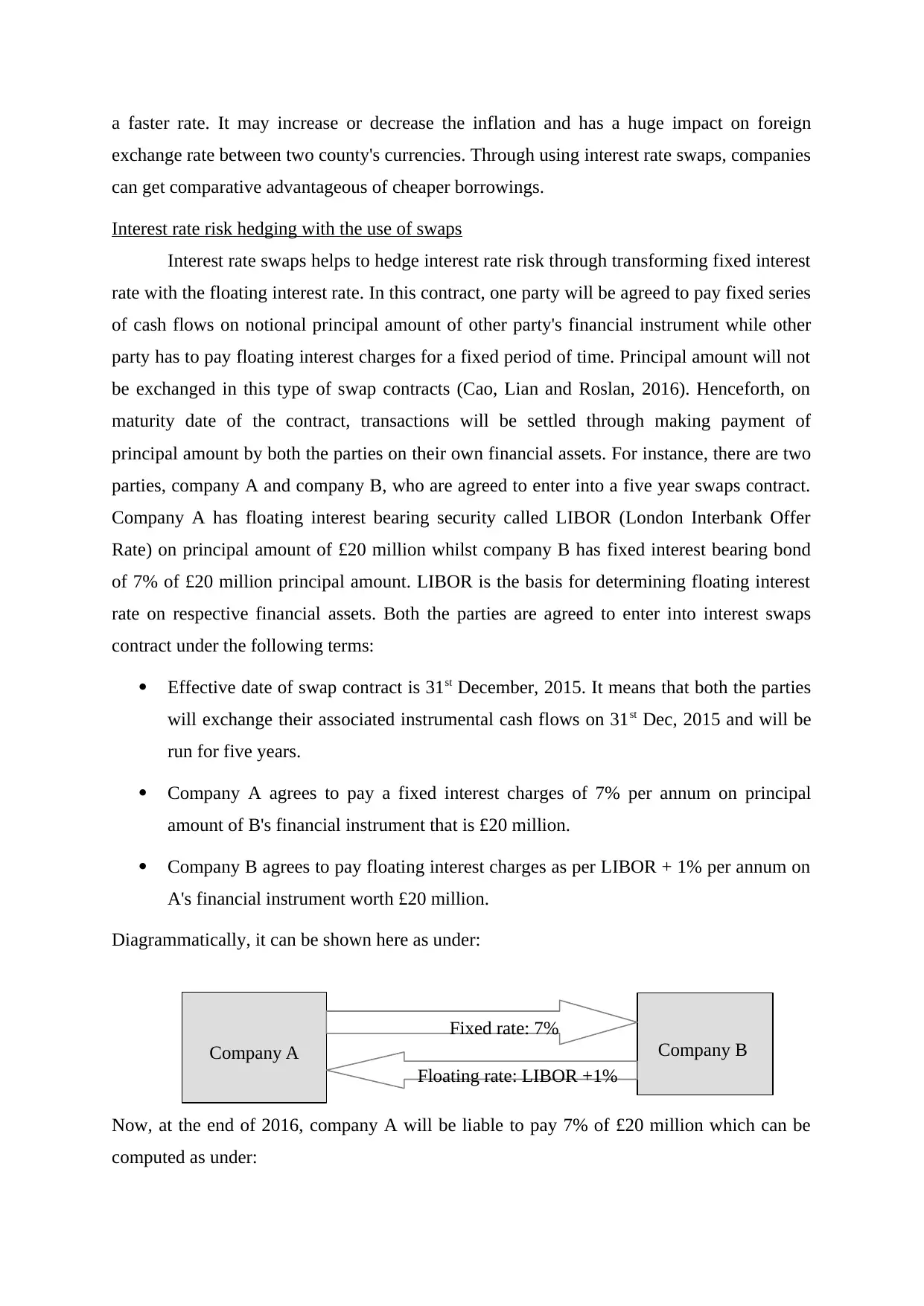

Company A

a faster rate. It may increase or decrease the inflation and has a huge impact on foreign

exchange rate between two county's currencies. Through using interest rate swaps, companies

can get comparative advantageous of cheaper borrowings.

Interest rate risk hedging with the use of swaps

Interest rate swaps helps to hedge interest rate risk through transforming fixed interest

rate with the floating interest rate. In this contract, one party will be agreed to pay fixed series

of cash flows on notional principal amount of other party's financial instrument while other

party has to pay floating interest charges for a fixed period of time. Principal amount will not

be exchanged in this type of swap contracts (Cao, Lian and Roslan, 2016). Henceforth, on

maturity date of the contract, transactions will be settled through making payment of

principal amount by both the parties on their own financial assets. For instance, there are two

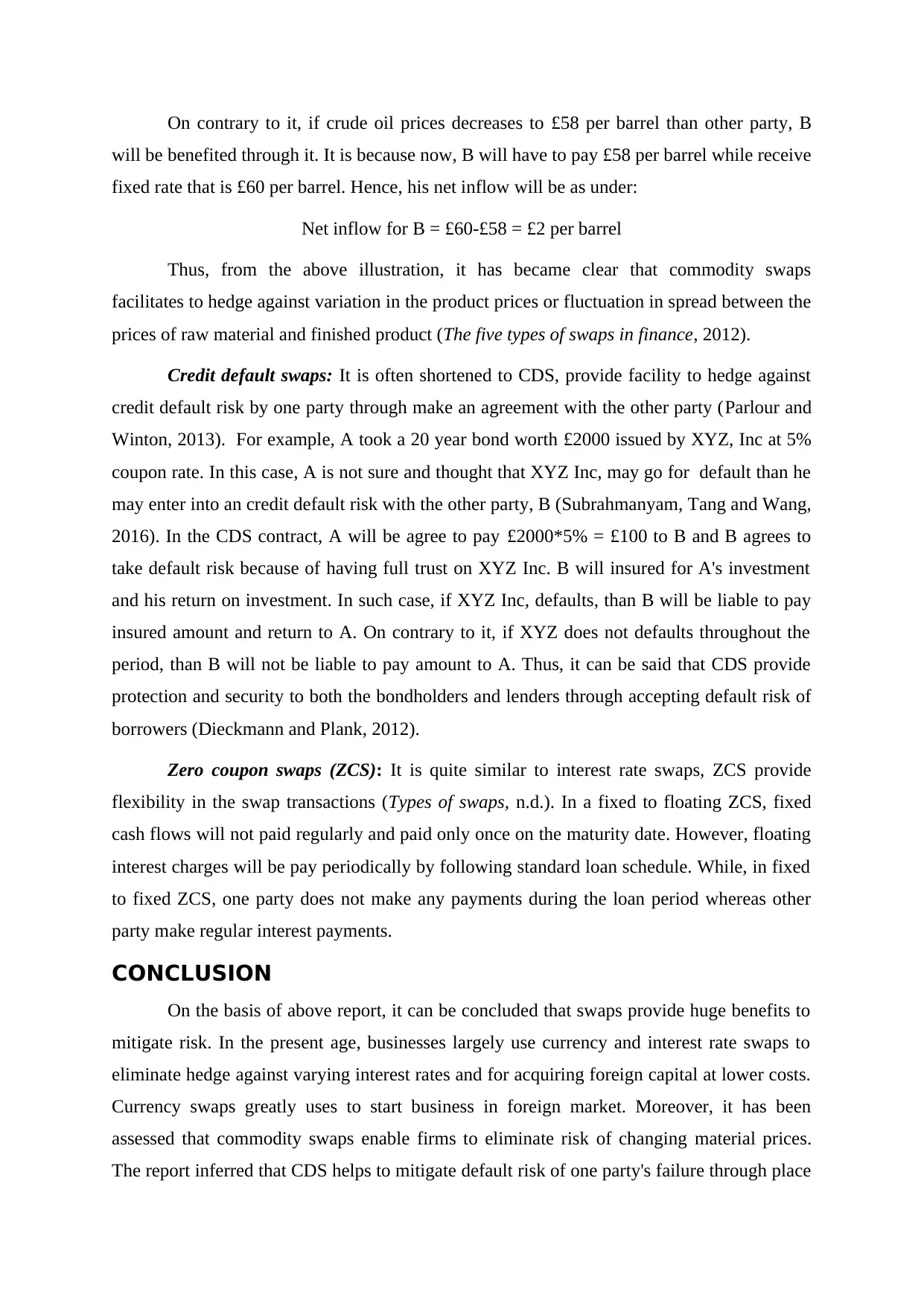

parties, company A and company B, who are agreed to enter into a five year swaps contract.

Company A has floating interest bearing security called LIBOR (London Interbank Offer

Rate) on principal amount of £20 million whilst company B has fixed interest bearing bond

of 7% of £20 million principal amount. LIBOR is the basis for determining floating interest

rate on respective financial assets. Both the parties are agreed to enter into interest swaps

contract under the following terms:

Effective date of swap contract is 31st December, 2015. It means that both the parties

will exchange their associated instrumental cash flows on 31st Dec, 2015 and will be

run for five years.

Company A agrees to pay a fixed interest charges of 7% per annum on principal

amount of B's financial instrument that is £20 million.

Company B agrees to pay floating interest charges as per LIBOR + 1% per annum on

A's financial instrument worth £20 million.

Diagrammatically, it can be shown here as under:

Now, at the end of 2016, company A will be liable to pay 7% of £20 million which can be

computed as under:

Company B

Fixed rate: 7%

Floating rate: LIBOR +1%

a faster rate. It may increase or decrease the inflation and has a huge impact on foreign

exchange rate between two county's currencies. Through using interest rate swaps, companies

can get comparative advantageous of cheaper borrowings.

Interest rate risk hedging with the use of swaps

Interest rate swaps helps to hedge interest rate risk through transforming fixed interest

rate with the floating interest rate. In this contract, one party will be agreed to pay fixed series

of cash flows on notional principal amount of other party's financial instrument while other

party has to pay floating interest charges for a fixed period of time. Principal amount will not

be exchanged in this type of swap contracts (Cao, Lian and Roslan, 2016). Henceforth, on

maturity date of the contract, transactions will be settled through making payment of

principal amount by both the parties on their own financial assets. For instance, there are two

parties, company A and company B, who are agreed to enter into a five year swaps contract.

Company A has floating interest bearing security called LIBOR (London Interbank Offer

Rate) on principal amount of £20 million whilst company B has fixed interest bearing bond

of 7% of £20 million principal amount. LIBOR is the basis for determining floating interest

rate on respective financial assets. Both the parties are agreed to enter into interest swaps

contract under the following terms:

Effective date of swap contract is 31st December, 2015. It means that both the parties

will exchange their associated instrumental cash flows on 31st Dec, 2015 and will be

run for five years.

Company A agrees to pay a fixed interest charges of 7% per annum on principal

amount of B's financial instrument that is £20 million.

Company B agrees to pay floating interest charges as per LIBOR + 1% per annum on

A's financial instrument worth £20 million.

Diagrammatically, it can be shown here as under:

Now, at the end of 2016, company A will be liable to pay 7% of £20 million which can be

computed as under:

Company B

Fixed rate: 7%

Floating rate: LIBOR +1%

Fixed interest = £20000000 * 7% = £1400000

However, company B will be obliged to pay interest according to the LIBOR rate. For

example, it has been assumed that LIBOR is 6.50%, so company B's liability can be

computed here as under:

Floating interest rate = 6.50% + 1% = 7.5 %

Company B's liability = £20,000,000*7.50% = £1500000

In order to eliminate unnecessary transactions or payment, interest rate swap contract

is adjusted by computing net liability. Hence, for the given contract, net liability has been

determined hereunder:

Net liability = Company B's Liability – Company A's liability

Net liability = £1500000-£1400000 = £100000

Thus, it has became clear that company B will be liable to pay net amount worth

£1000000 to company A to while company A has no need to pay because its interest

obligation has been set off by B's liability amounted to worth £1400000. From the above

swap contract, it can be seen that company A hedged himself against high interest payment.

worth £1500000.

On contrary to it, if LIBOR is 5.50% than company B will be liable to pay 6.50%

interest rate on £20,000,000. In this case, A's liability will remain constant worth £1400000

while B's liability has been computed here as under:

Company B = £20000000*6.50% = £1300000

Net liability of company A = £1400000-£1300000 = £100000

Thus, it can be seen that in this case, A will be obliged to pay for worth £100000. In

the given situation, company B hedged himself against from higher fixed interest rate

obligations by 0.5% amounted to £100000. On the maturity date, both the counter parties will

pay their notional principal amount of £20,000,000.

From the following example, it has became clear that under the interest rate swap, if

the floating interest rate goes increase than fixed interest rate, than party who holds floating

interest bearing assets can hedge himself against high interest obligations (Harris, Wu and

Yang, 2015). However, if floating rate goes decrease than fixed interest rate, than person who

holds fixed interest assets can mitigate their higher interest liability through transferring their

underlying assets with the other floating interest rate security.

However, company B will be obliged to pay interest according to the LIBOR rate. For

example, it has been assumed that LIBOR is 6.50%, so company B's liability can be

computed here as under:

Floating interest rate = 6.50% + 1% = 7.5 %

Company B's liability = £20,000,000*7.50% = £1500000

In order to eliminate unnecessary transactions or payment, interest rate swap contract

is adjusted by computing net liability. Hence, for the given contract, net liability has been

determined hereunder:

Net liability = Company B's Liability – Company A's liability

Net liability = £1500000-£1400000 = £100000

Thus, it has became clear that company B will be liable to pay net amount worth

£1000000 to company A to while company A has no need to pay because its interest

obligation has been set off by B's liability amounted to worth £1400000. From the above

swap contract, it can be seen that company A hedged himself against high interest payment.

worth £1500000.

On contrary to it, if LIBOR is 5.50% than company B will be liable to pay 6.50%

interest rate on £20,000,000. In this case, A's liability will remain constant worth £1400000

while B's liability has been computed here as under:

Company B = £20000000*6.50% = £1300000

Net liability of company A = £1400000-£1300000 = £100000

Thus, it can be seen that in this case, A will be obliged to pay for worth £100000. In

the given situation, company B hedged himself against from higher fixed interest rate

obligations by 0.5% amounted to £100000. On the maturity date, both the counter parties will

pay their notional principal amount of £20,000,000.

From the following example, it has became clear that under the interest rate swap, if

the floating interest rate goes increase than fixed interest rate, than party who holds floating

interest bearing assets can hedge himself against high interest obligations (Harris, Wu and

Yang, 2015). However, if floating rate goes decrease than fixed interest rate, than person who

holds fixed interest assets can mitigate their higher interest liability through transferring their

underlying assets with the other floating interest rate security.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Currency swaps: As discussed earlier, under the interest rate swaps counter parties

does not exchange principal amount of their own financial instruments. However, currency

swaps involves exchange of principal amount and fixed interest obligations with the other

party's financial instrument in different currency so as to take comparative advantage (Han,

2016). Thus, currency swaps entails swapping of both the principal amount and the cash flow

stream between in different currencies between two counter parties. Interest rate fluctuations

have an significant affect on exchange rate between two currencies. Thus, parties who took

foreign loans can face currency risk. Hence, currency swaps facilitates parties to mitigate

their foreign exchange risk. Characteristics of currency risk are given below:

It transforms both the principal and interest obligations in one currency with the other

currency.

Transactions will be made on a specified date which will be given in the contract.

Both the parties will be agree to exchange same principal amount but in different

currency. Hence, it is also considered as a foreign exchange transaction which

companies does not require to show in their financial accounts (Dow and Kunz,

2015).

Currency risk hedging with swap

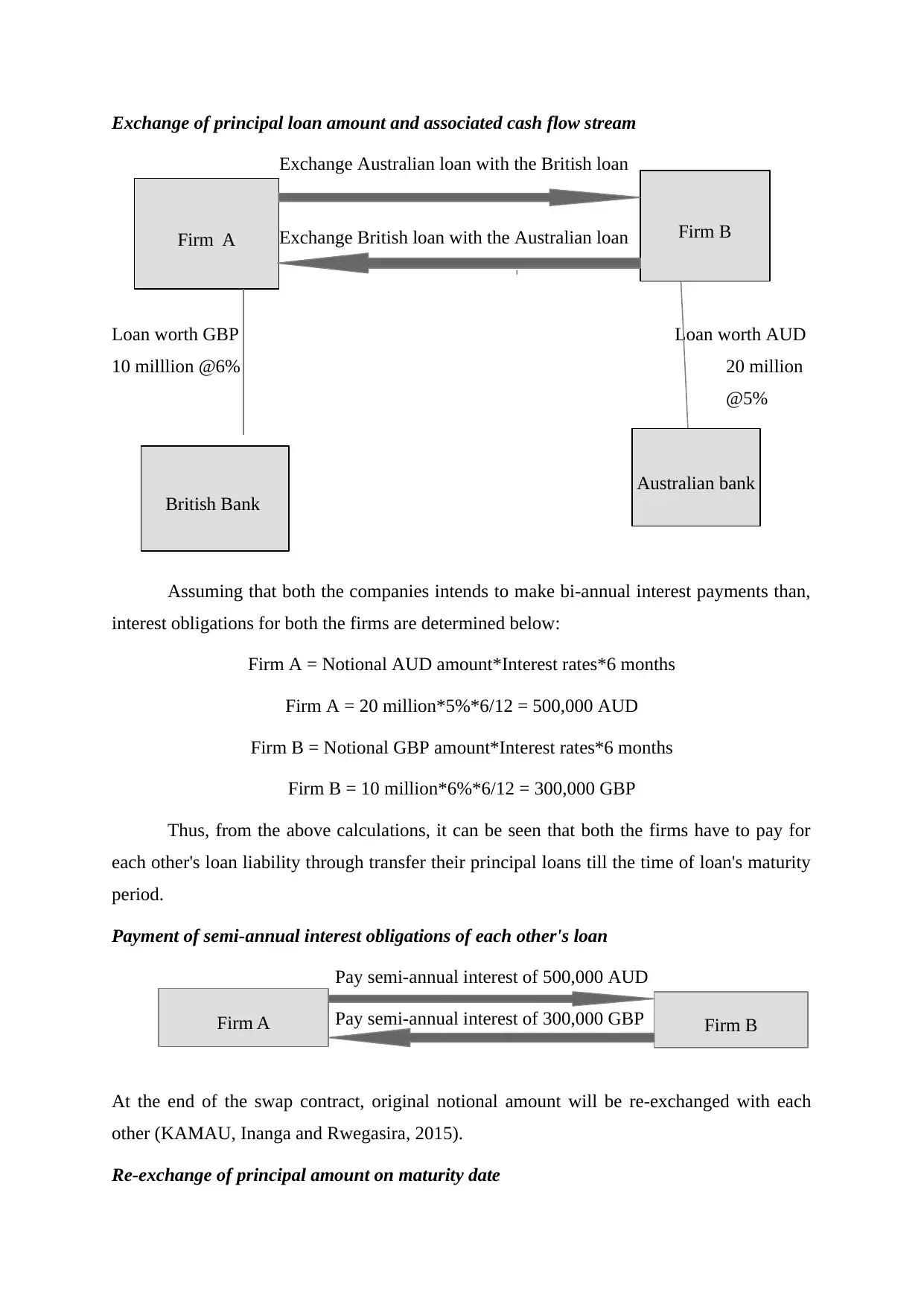

For instance, a UK established firm, A wishes to start its business in Australia and an

Australian firm, B intends to open its new business in London. Australian bank offer loan to

domestic enterprises at 5% interest rate while for foreigners it is 9%. However, in UK, costs

of loan for foreigners is 10% and for local firms, it is 6%. In order to set up their new

businesses, UK based firm, A wants amount of 20 million AUD while Australian firm, B

wants amount of 10 million GBP. Thus, in both the countries, interest rate is comparatively

higher for foreign companies. Hence, both A and B firms have to pay high interest charges on

foreign loans. Moreover, due to procedural difficulties, it seems to be very difficult to take

borrowings from the foreign countries. Thus, in this case, both the firms can enter into a

currency swap contract to hedge their currency risk.

In this case, A firm took loan worth 20 million AUD @ lower cost of 5% and English

firm took loan of 10 million GBP @ 6% interest rate. After entering into currency swaps,

both A and B firms will exchange their principal loan amount with the interest obligations on

AUD 20 million and GBP 10 million with each other. Diagrammatically, it can be presented

here as under:

does not exchange principal amount of their own financial instruments. However, currency

swaps involves exchange of principal amount and fixed interest obligations with the other

party's financial instrument in different currency so as to take comparative advantage (Han,

2016). Thus, currency swaps entails swapping of both the principal amount and the cash flow

stream between in different currencies between two counter parties. Interest rate fluctuations

have an significant affect on exchange rate between two currencies. Thus, parties who took

foreign loans can face currency risk. Hence, currency swaps facilitates parties to mitigate

their foreign exchange risk. Characteristics of currency risk are given below:

It transforms both the principal and interest obligations in one currency with the other

currency.

Transactions will be made on a specified date which will be given in the contract.

Both the parties will be agree to exchange same principal amount but in different

currency. Hence, it is also considered as a foreign exchange transaction which

companies does not require to show in their financial accounts (Dow and Kunz,

2015).

Currency risk hedging with swap

For instance, a UK established firm, A wishes to start its business in Australia and an

Australian firm, B intends to open its new business in London. Australian bank offer loan to

domestic enterprises at 5% interest rate while for foreigners it is 9%. However, in UK, costs

of loan for foreigners is 10% and for local firms, it is 6%. In order to set up their new

businesses, UK based firm, A wants amount of 20 million AUD while Australian firm, B

wants amount of 10 million GBP. Thus, in both the countries, interest rate is comparatively

higher for foreign companies. Hence, both A and B firms have to pay high interest charges on

foreign loans. Moreover, due to procedural difficulties, it seems to be very difficult to take

borrowings from the foreign countries. Thus, in this case, both the firms can enter into a

currency swap contract to hedge their currency risk.

In this case, A firm took loan worth 20 million AUD @ lower cost of 5% and English

firm took loan of 10 million GBP @ 6% interest rate. After entering into currency swaps,

both A and B firms will exchange their principal loan amount with the interest obligations on

AUD 20 million and GBP 10 million with each other. Diagrammatically, it can be presented

here as under:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

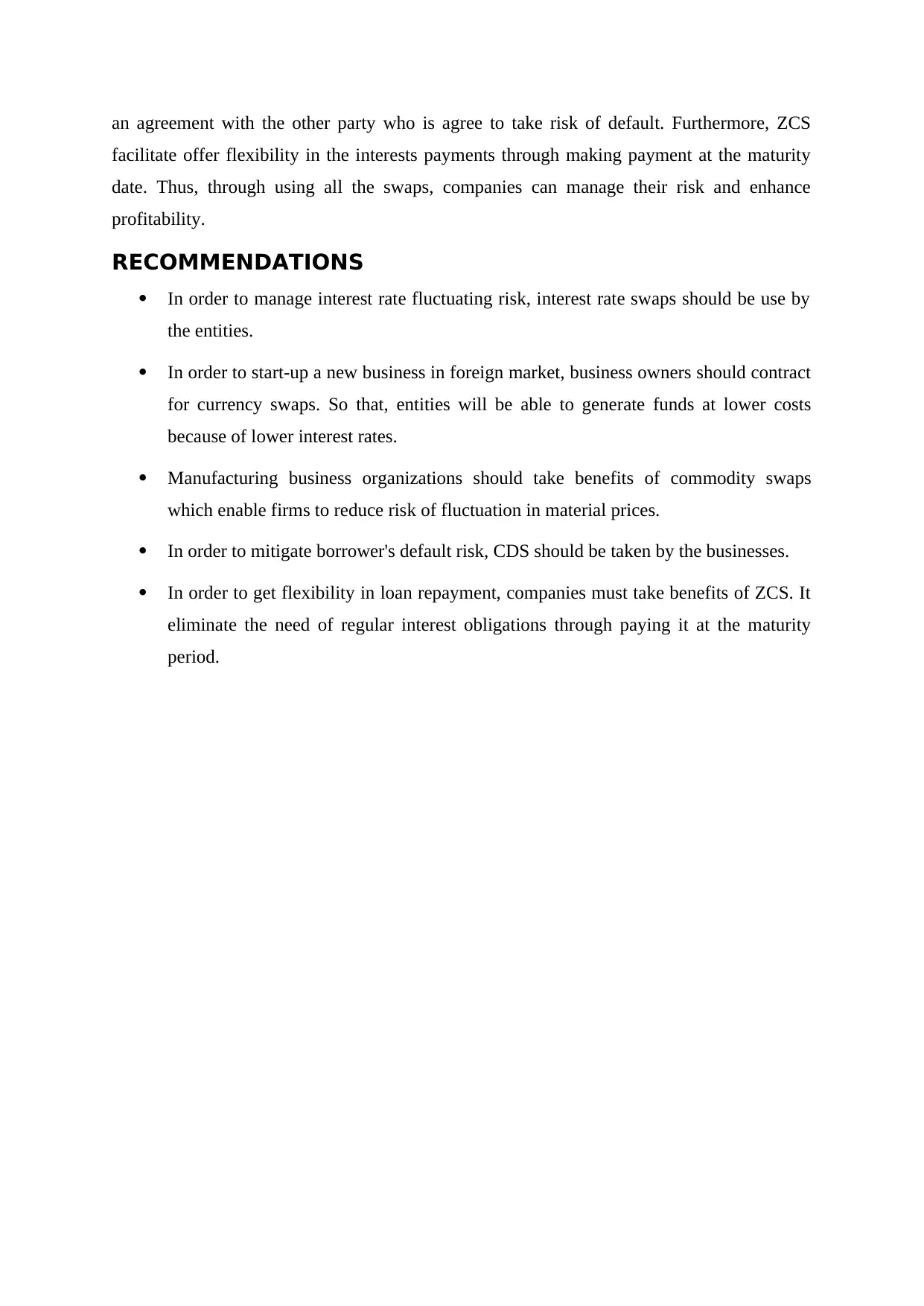

Firm A Firm B

Exchange of principal loan amount and associated cash flow stream

Exchange Australian loan with the British loan

Exchange British loan with the Australian loan

Loan worth GBP Loan worth AUD

10 milllion @6% 20 million

@5%

Assuming that both the companies intends to make bi-annual interest payments than,

interest obligations for both the firms are determined below:

Firm A = Notional AUD amount*Interest rates*6 months

Firm A = 20 million*5%*6/12 = 500,000 AUD

Firm B = Notional GBP amount*Interest rates*6 months

Firm B = 10 million*6%*6/12 = 300,000 GBP

Thus, from the above calculations, it can be seen that both the firms have to pay for

each other's loan liability through transfer their principal loans till the time of loan's maturity

period.

Payment of semi-annual interest obligations of each other's loan

Pay semi-annual interest of 500,000 AUD

Pay semi-annual interest of 300,000 GBP

At the end of the swap contract, original notional amount will be re-exchanged with each

other (KAMAU, Inanga and Rwegasira, 2015).

Re-exchange of principal amount on maturity date

British Bank

Australian bank

Firm A Firm B

Exchange of principal loan amount and associated cash flow stream

Exchange Australian loan with the British loan

Exchange British loan with the Australian loan

Loan worth GBP Loan worth AUD

10 milllion @6% 20 million

@5%

Assuming that both the companies intends to make bi-annual interest payments than,

interest obligations for both the firms are determined below:

Firm A = Notional AUD amount*Interest rates*6 months

Firm A = 20 million*5%*6/12 = 500,000 AUD

Firm B = Notional GBP amount*Interest rates*6 months

Firm B = 10 million*6%*6/12 = 300,000 GBP

Thus, from the above calculations, it can be seen that both the firms have to pay for

each other's loan liability through transfer their principal loans till the time of loan's maturity

period.

Payment of semi-annual interest obligations of each other's loan

Pay semi-annual interest of 500,000 AUD

Pay semi-annual interest of 300,000 GBP

At the end of the swap contract, original notional amount will be re-exchanged with each

other (KAMAU, Inanga and Rwegasira, 2015).

Re-exchange of principal amount on maturity date

British Bank

Australian bank

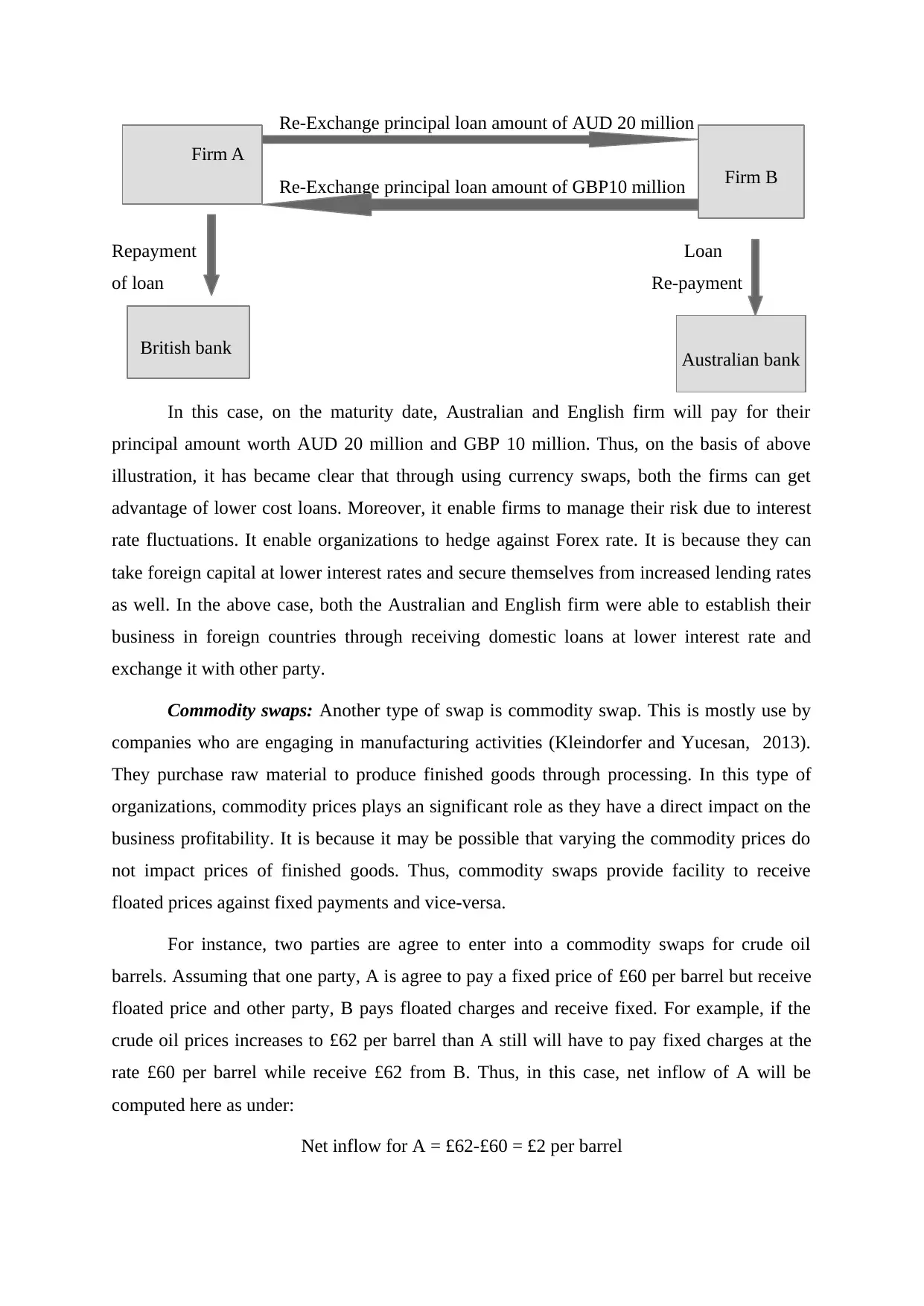

Firm A Firm B

Re-Exchange principal loan amount of AUD 20 million

Re-Exchange principal loan amount of GBP10 million

Repayment Loan

of loan Re-payment

In this case, on the maturity date, Australian and English firm will pay for their

principal amount worth AUD 20 million and GBP 10 million. Thus, on the basis of above

illustration, it has became clear that through using currency swaps, both the firms can get

advantage of lower cost loans. Moreover, it enable firms to manage their risk due to interest

rate fluctuations. It enable organizations to hedge against Forex rate. It is because they can

take foreign capital at lower interest rates and secure themselves from increased lending rates

as well. In the above case, both the Australian and English firm were able to establish their

business in foreign countries through receiving domestic loans at lower interest rate and

exchange it with other party.

Commodity swaps: Another type of swap is commodity swap. This is mostly use by

companies who are engaging in manufacturing activities (Kleindorfer and Yucesan, 2013).

They purchase raw material to produce finished goods through processing. In this type of

organizations, commodity prices plays an significant role as they have a direct impact on the

business profitability. It is because it may be possible that varying the commodity prices do

not impact prices of finished goods. Thus, commodity swaps provide facility to receive

floated prices against fixed payments and vice-versa.

For instance, two parties are agree to enter into a commodity swaps for crude oil

barrels. Assuming that one party, A is agree to pay a fixed price of £60 per barrel but receive

floated price and other party, B pays floated charges and receive fixed. For example, if the

crude oil prices increases to £62 per barrel than A still will have to pay fixed charges at the

rate £60 per barrel while receive £62 from B. Thus, in this case, net inflow of A will be

computed here as under:

Net inflow for A = £62-£60 = £2 per barrel

Firm A

Firm B

British bank Australian bank

Re-Exchange principal loan amount of GBP10 million

Repayment Loan

of loan Re-payment

In this case, on the maturity date, Australian and English firm will pay for their

principal amount worth AUD 20 million and GBP 10 million. Thus, on the basis of above

illustration, it has became clear that through using currency swaps, both the firms can get

advantage of lower cost loans. Moreover, it enable firms to manage their risk due to interest

rate fluctuations. It enable organizations to hedge against Forex rate. It is because they can

take foreign capital at lower interest rates and secure themselves from increased lending rates

as well. In the above case, both the Australian and English firm were able to establish their

business in foreign countries through receiving domestic loans at lower interest rate and

exchange it with other party.

Commodity swaps: Another type of swap is commodity swap. This is mostly use by

companies who are engaging in manufacturing activities (Kleindorfer and Yucesan, 2013).

They purchase raw material to produce finished goods through processing. In this type of

organizations, commodity prices plays an significant role as they have a direct impact on the

business profitability. It is because it may be possible that varying the commodity prices do

not impact prices of finished goods. Thus, commodity swaps provide facility to receive

floated prices against fixed payments and vice-versa.

For instance, two parties are agree to enter into a commodity swaps for crude oil

barrels. Assuming that one party, A is agree to pay a fixed price of £60 per barrel but receive

floated price and other party, B pays floated charges and receive fixed. For example, if the

crude oil prices increases to £62 per barrel than A still will have to pay fixed charges at the

rate £60 per barrel while receive £62 from B. Thus, in this case, net inflow of A will be

computed here as under:

Net inflow for A = £62-£60 = £2 per barrel

Firm A

Firm B

British bank Australian bank

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On contrary to it, if crude oil prices decreases to £58 per barrel than other party, B

will be benefited through it. It is because now, B will have to pay £58 per barrel while receive

fixed rate that is £60 per barrel. Hence, his net inflow will be as under:

Net inflow for B = £60-£58 = £2 per barrel

Thus, from the above illustration, it has became clear that commodity swaps

facilitates to hedge against variation in the product prices or fluctuation in spread between the

prices of raw material and finished product (The five types of swaps in finance, 2012).

Credit default swaps: It is often shortened to CDS, provide facility to hedge against

credit default risk by one party through make an agreement with the other party (Parlour and

Winton, 2013). For example, A took a 20 year bond worth £2000 issued by XYZ, Inc at 5%

coupon rate. In this case, A is not sure and thought that XYZ Inc, may go for default than he

may enter into an credit default risk with the other party, B (Subrahmanyam, Tang and Wang,

2016). In the CDS contract, A will be agree to pay £2000*5% = £100 to B and B agrees to

take default risk because of having full trust on XYZ Inc. B will insured for A's investment

and his return on investment. In such case, if XYZ Inc, defaults, than B will be liable to pay

insured amount and return to A. On contrary to it, if XYZ does not defaults throughout the

period, than B will not be liable to pay amount to A. Thus, it can be said that CDS provide

protection and security to both the bondholders and lenders through accepting default risk of

borrowers (Dieckmann and Plank, 2012).

Zero coupon swaps (ZCS): It is quite similar to interest rate swaps, ZCS provide

flexibility in the swap transactions (Types of swaps, n.d.). In a fixed to floating ZCS, fixed

cash flows will not paid regularly and paid only once on the maturity date. However, floating

interest charges will be pay periodically by following standard loan schedule. While, in fixed

to fixed ZCS, one party does not make any payments during the loan period whereas other

party make regular interest payments.

CONCLUSION

On the basis of above report, it can be concluded that swaps provide huge benefits to

mitigate risk. In the present age, businesses largely use currency and interest rate swaps to

eliminate hedge against varying interest rates and for acquiring foreign capital at lower costs.

Currency swaps greatly uses to start business in foreign market. Moreover, it has been

assessed that commodity swaps enable firms to eliminate risk of changing material prices.

The report inferred that CDS helps to mitigate default risk of one party's failure through place

will be benefited through it. It is because now, B will have to pay £58 per barrel while receive

fixed rate that is £60 per barrel. Hence, his net inflow will be as under:

Net inflow for B = £60-£58 = £2 per barrel

Thus, from the above illustration, it has became clear that commodity swaps

facilitates to hedge against variation in the product prices or fluctuation in spread between the

prices of raw material and finished product (The five types of swaps in finance, 2012).

Credit default swaps: It is often shortened to CDS, provide facility to hedge against

credit default risk by one party through make an agreement with the other party (Parlour and

Winton, 2013). For example, A took a 20 year bond worth £2000 issued by XYZ, Inc at 5%

coupon rate. In this case, A is not sure and thought that XYZ Inc, may go for default than he

may enter into an credit default risk with the other party, B (Subrahmanyam, Tang and Wang,

2016). In the CDS contract, A will be agree to pay £2000*5% = £100 to B and B agrees to

take default risk because of having full trust on XYZ Inc. B will insured for A's investment

and his return on investment. In such case, if XYZ Inc, defaults, than B will be liable to pay

insured amount and return to A. On contrary to it, if XYZ does not defaults throughout the

period, than B will not be liable to pay amount to A. Thus, it can be said that CDS provide

protection and security to both the bondholders and lenders through accepting default risk of

borrowers (Dieckmann and Plank, 2012).

Zero coupon swaps (ZCS): It is quite similar to interest rate swaps, ZCS provide

flexibility in the swap transactions (Types of swaps, n.d.). In a fixed to floating ZCS, fixed

cash flows will not paid regularly and paid only once on the maturity date. However, floating

interest charges will be pay periodically by following standard loan schedule. While, in fixed

to fixed ZCS, one party does not make any payments during the loan period whereas other

party make regular interest payments.

CONCLUSION

On the basis of above report, it can be concluded that swaps provide huge benefits to

mitigate risk. In the present age, businesses largely use currency and interest rate swaps to

eliminate hedge against varying interest rates and for acquiring foreign capital at lower costs.

Currency swaps greatly uses to start business in foreign market. Moreover, it has been

assessed that commodity swaps enable firms to eliminate risk of changing material prices.

The report inferred that CDS helps to mitigate default risk of one party's failure through place

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

an agreement with the other party who is agree to take risk of default. Furthermore, ZCS

facilitate offer flexibility in the interests payments through making payment at the maturity

date. Thus, through using all the swaps, companies can manage their risk and enhance

profitability.

RECOMMENDATIONS

In order to manage interest rate fluctuating risk, interest rate swaps should be use by

the entities.

In order to start-up a new business in foreign market, business owners should contract

for currency swaps. So that, entities will be able to generate funds at lower costs

because of lower interest rates.

Manufacturing business organizations should take benefits of commodity swaps

which enable firms to reduce risk of fluctuation in material prices.

In order to mitigate borrower's default risk, CDS should be taken by the businesses.

In order to get flexibility in loan repayment, companies must take benefits of ZCS. It

eliminate the need of regular interest obligations through paying it at the maturity

period.

facilitate offer flexibility in the interests payments through making payment at the maturity

date. Thus, through using all the swaps, companies can manage their risk and enhance

profitability.

RECOMMENDATIONS

In order to manage interest rate fluctuating risk, interest rate swaps should be use by

the entities.

In order to start-up a new business in foreign market, business owners should contract

for currency swaps. So that, entities will be able to generate funds at lower costs

because of lower interest rates.

Manufacturing business organizations should take benefits of commodity swaps

which enable firms to reduce risk of fluctuation in material prices.

In order to mitigate borrower's default risk, CDS should be taken by the businesses.

In order to get flexibility in loan repayment, companies must take benefits of ZCS. It

eliminate the need of regular interest obligations through paying it at the maturity

period.

REFERENCES

Books and Journals

Aıt-Sahalia, Y., Karaman, M. and Mancini, L., 2014. The term structure of variance swaps

and risk premia. Unpublished working paper, Princeton University, University of

Zurich, EPFL and Swiss Finance Institute.

Arentsen, E. and et.al., 2015. Subprime mortgage defaults and credit default swaps. The

Journal of Finance. 70(2). pp. 689-731.

Biffis, E. and et.al., 2015. The cost of counterparty risk and collateralization in longevity

swaps. Journal of Risk and Insurance.

Byun, S.J. and Chang, K.C., 2015. Volatility risk premium in the interest rate market:

Evidence from delta-hedged gains on USD interest rate swaps. International Review

of Financial Analysis. 40. pp. 88-102.

Cao, J., Lian, G. and Roslan, T.R.N., 2016. Pricing variance swaps under stochastic volatility

and stochastic interest rate. Applied Mathematics and Computation. 277. pp. 72-81.

Dieckmann, S. and Plank, T., 2012. Default risk of advanced economies: An empirical

analysis of credit default swaps during the financial crisis. Review of Finance. 16(4).

pp. 903-934.

Dow III, B.L. and Kunz, D., 2015. Utilizing Currency Swaps to Hedge Risk at Slc. Journal of

the International Academy for Case Studies. 21(3). p. 57.

Filipović, D., Gourier, E. and Mancini, L., 2016. Quadratic variance swap models. Journal of

Financial Economics. 119(1). pp. 44-68.

Han, Y.Y., 2016. Currency Derivatives and their role in Asian bond markets. IRA-

International Journal of Management & Social Sciences (ISSN 2455-2267). 1(4).

Harris, G.R., Wu, T.L. and Yang, J., 2015. The relationship between counterparty default and

interest rate volatility and its impact on the credit risk of interest rate derivatives. The

Journal of Credit Risk. 11(1). p. 93.

KAMAU, P., Inanga, E.L. and Rwegasira, K., 2015. The usage of currency derivatives in

multilateral banks. Management Research Review. 38(5). pp. 482-504.

Kiesel, F., Lücke, F. and Schiereck, D., 2015. Regulation of uncovered sovereign credit

default swaps–evidence from the European Union. The Journal of Risk Finance.

16(4). pp. 425-443.

Kleindorfer, P. and Yucesan, E., 2013, December. Managing commodity procurement risk

through hedging. In Simulation Conference (WSC). Winter. IEEE. pp. 136-146.

Books and Journals

Aıt-Sahalia, Y., Karaman, M. and Mancini, L., 2014. The term structure of variance swaps

and risk premia. Unpublished working paper, Princeton University, University of

Zurich, EPFL and Swiss Finance Institute.

Arentsen, E. and et.al., 2015. Subprime mortgage defaults and credit default swaps. The

Journal of Finance. 70(2). pp. 689-731.

Biffis, E. and et.al., 2015. The cost of counterparty risk and collateralization in longevity

swaps. Journal of Risk and Insurance.

Byun, S.J. and Chang, K.C., 2015. Volatility risk premium in the interest rate market:

Evidence from delta-hedged gains on USD interest rate swaps. International Review

of Financial Analysis. 40. pp. 88-102.

Cao, J., Lian, G. and Roslan, T.R.N., 2016. Pricing variance swaps under stochastic volatility

and stochastic interest rate. Applied Mathematics and Computation. 277. pp. 72-81.

Dieckmann, S. and Plank, T., 2012. Default risk of advanced economies: An empirical

analysis of credit default swaps during the financial crisis. Review of Finance. 16(4).

pp. 903-934.

Dow III, B.L. and Kunz, D., 2015. Utilizing Currency Swaps to Hedge Risk at Slc. Journal of

the International Academy for Case Studies. 21(3). p. 57.

Filipović, D., Gourier, E. and Mancini, L., 2016. Quadratic variance swap models. Journal of

Financial Economics. 119(1). pp. 44-68.

Han, Y.Y., 2016. Currency Derivatives and their role in Asian bond markets. IRA-

International Journal of Management & Social Sciences (ISSN 2455-2267). 1(4).

Harris, G.R., Wu, T.L. and Yang, J., 2015. The relationship between counterparty default and

interest rate volatility and its impact on the credit risk of interest rate derivatives. The

Journal of Credit Risk. 11(1). p. 93.

KAMAU, P., Inanga, E.L. and Rwegasira, K., 2015. The usage of currency derivatives in

multilateral banks. Management Research Review. 38(5). pp. 482-504.

Kiesel, F., Lücke, F. and Schiereck, D., 2015. Regulation of uncovered sovereign credit

default swaps–evidence from the European Union. The Journal of Risk Finance.

16(4). pp. 425-443.

Kleindorfer, P. and Yucesan, E., 2013, December. Managing commodity procurement risk

through hedging. In Simulation Conference (WSC). Winter. IEEE. pp. 136-146.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.