Budgeting and Investment Appraisal in Applied Management Accounting

VerifiedAdded on 2023/06/17

|11

|1475

|105

Homework Assignment

AI Summary

This assignment solution provides a detailed analysis of applied management accounting concepts, focusing on budgeting and investment decisions. It includes the preparation of a production budget, a direct material purchase budget, and a cash budget for April, May, and June. The solution also discusses the negative effects of budgeting within an organization, such as time consumption and strategic rigidity. Furthermore, it analyzes whether a company should manufacture a product or purchase it from an external supplier, considering both quantitative and qualitative factors. Finally, the assignment evaluates a potential investment using payback period, net present value (NPV), and internal rate of return (IRR) methods, concluding that the investment is financially viable due to its high IRR and positive NPV. Desklib offers numerous resources for students, including similar solved assignments and study tools.

APPLIED MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENT

QUESTION 1...................................................................................................................................3

a)..................................................................................................................................................3

b)..................................................................................................................................................3

c)..................................................................................................................................................4

d)..................................................................................................................................................4

QUESTION 2...................................................................................................................................4

QUESTION 3...................................................................................................................................4

a)..................................................................................................................................................4

b)..................................................................................................................................................5

QUESTION 4...................................................................................................................................6

a)..................................................................................................................................................6

b)..................................................................................................................................................6

c)..................................................................................................................................................7

d)..................................................................................................................................................7

REFERENCES................................................................................................................................8

QUESTION 1...................................................................................................................................3

a)..................................................................................................................................................3

b)..................................................................................................................................................3

c)..................................................................................................................................................4

d)..................................................................................................................................................4

QUESTION 2...................................................................................................................................4

QUESTION 3...................................................................................................................................4

a)..................................................................................................................................................4

b)..................................................................................................................................................5

QUESTION 4...................................................................................................................................6

a)..................................................................................................................................................6

b)..................................................................................................................................................6

c)..................................................................................................................................................7

d)..................................................................................................................................................7

REFERENCES................................................................................................................................8

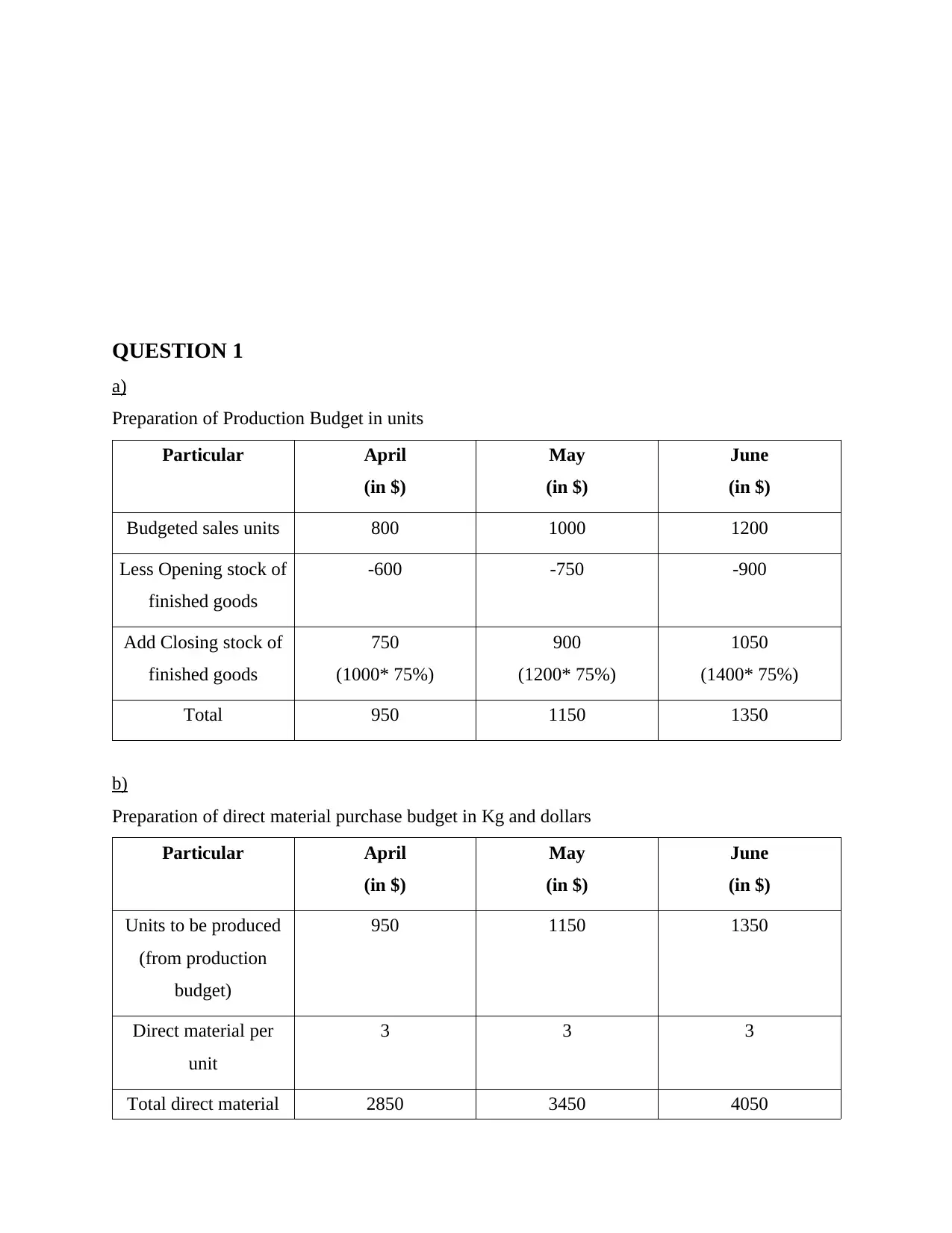

QUESTION 1

a)

Preparation of Production Budget in units

Particular April

(in $)

May

(in $)

June

(in $)

Budgeted sales units 800 1000 1200

Less Opening stock of

finished goods

-600 -750 -900

Add Closing stock of

finished goods

750

(1000* 75%)

900

(1200* 75%)

1050

(1400* 75%)

Total 950 1150 1350

b)

Preparation of direct material purchase budget in Kg and dollars

Particular April

(in $)

May

(in $)

June

(in $)

Units to be produced

(from production

budget)

950 1150 1350

Direct material per

unit

3 3 3

Total direct material 2850 3450 4050

a)

Preparation of Production Budget in units

Particular April

(in $)

May

(in $)

June

(in $)

Budgeted sales units 800 1000 1200

Less Opening stock of

finished goods

-600 -750 -900

Add Closing stock of

finished goods

750

(1000* 75%)

900

(1200* 75%)

1050

(1400* 75%)

Total 950 1150 1350

b)

Preparation of direct material purchase budget in Kg and dollars

Particular April

(in $)

May

(in $)

June

(in $)

Units to be produced

(from production

budget)

950 1150 1350

Direct material per

unit

3 3 3

Total direct material 2850 3450 4050

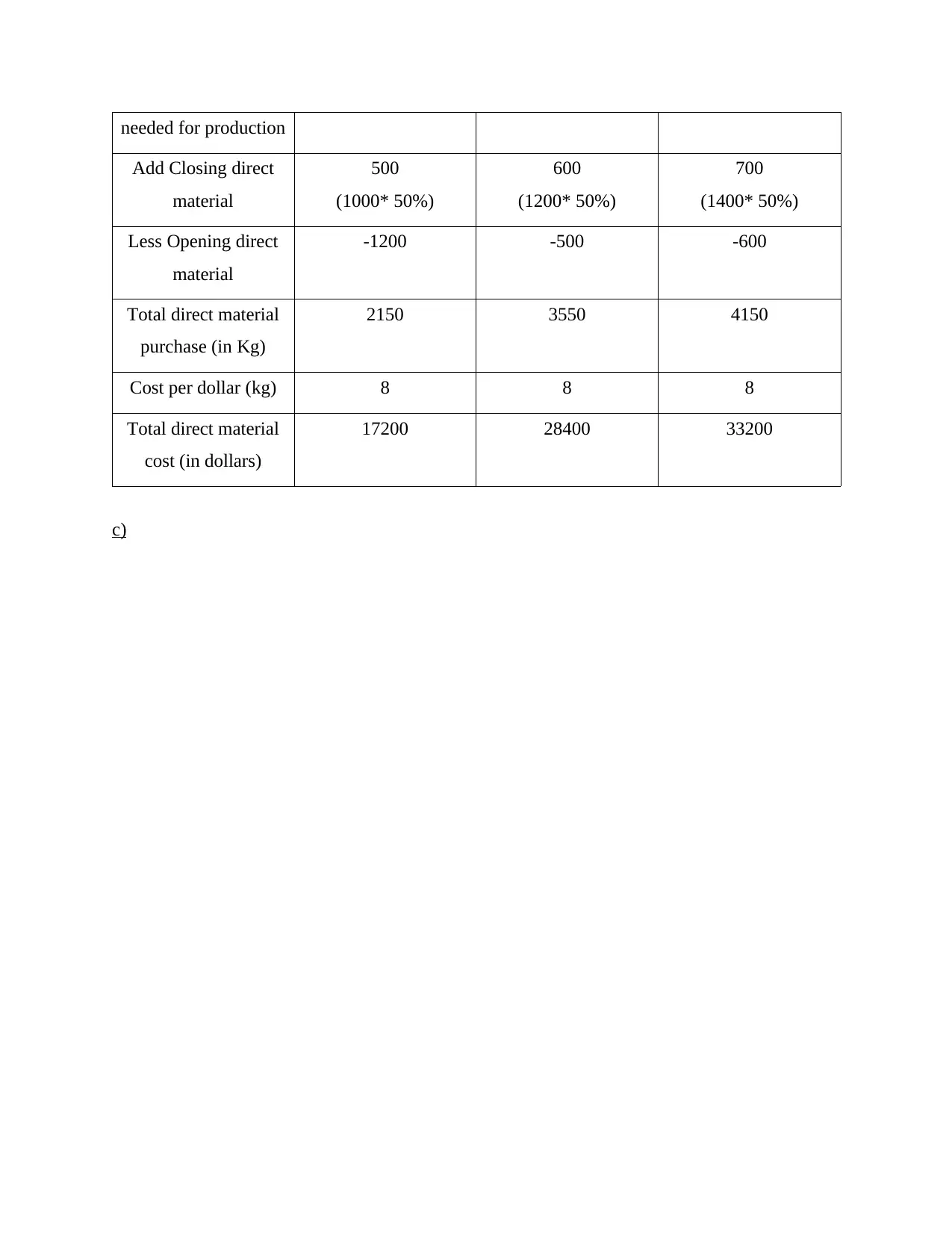

needed for production

Add Closing direct

material

500

(1000* 50%)

600

(1200* 50%)

700

(1400* 50%)

Less Opening direct

material

-1200 -500 -600

Total direct material

purchase (in Kg)

2150 3550 4150

Cost per dollar (kg) 8 8 8

Total direct material

cost (in dollars)

17200 28400 33200

c)

Add Closing direct

material

500

(1000* 50%)

600

(1200* 50%)

700

(1400* 50%)

Less Opening direct

material

-1200 -500 -600

Total direct material

purchase (in Kg)

2150 3550 4150

Cost per dollar (kg) 8 8 8

Total direct material

cost (in dollars)

17200 28400 33200

c)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

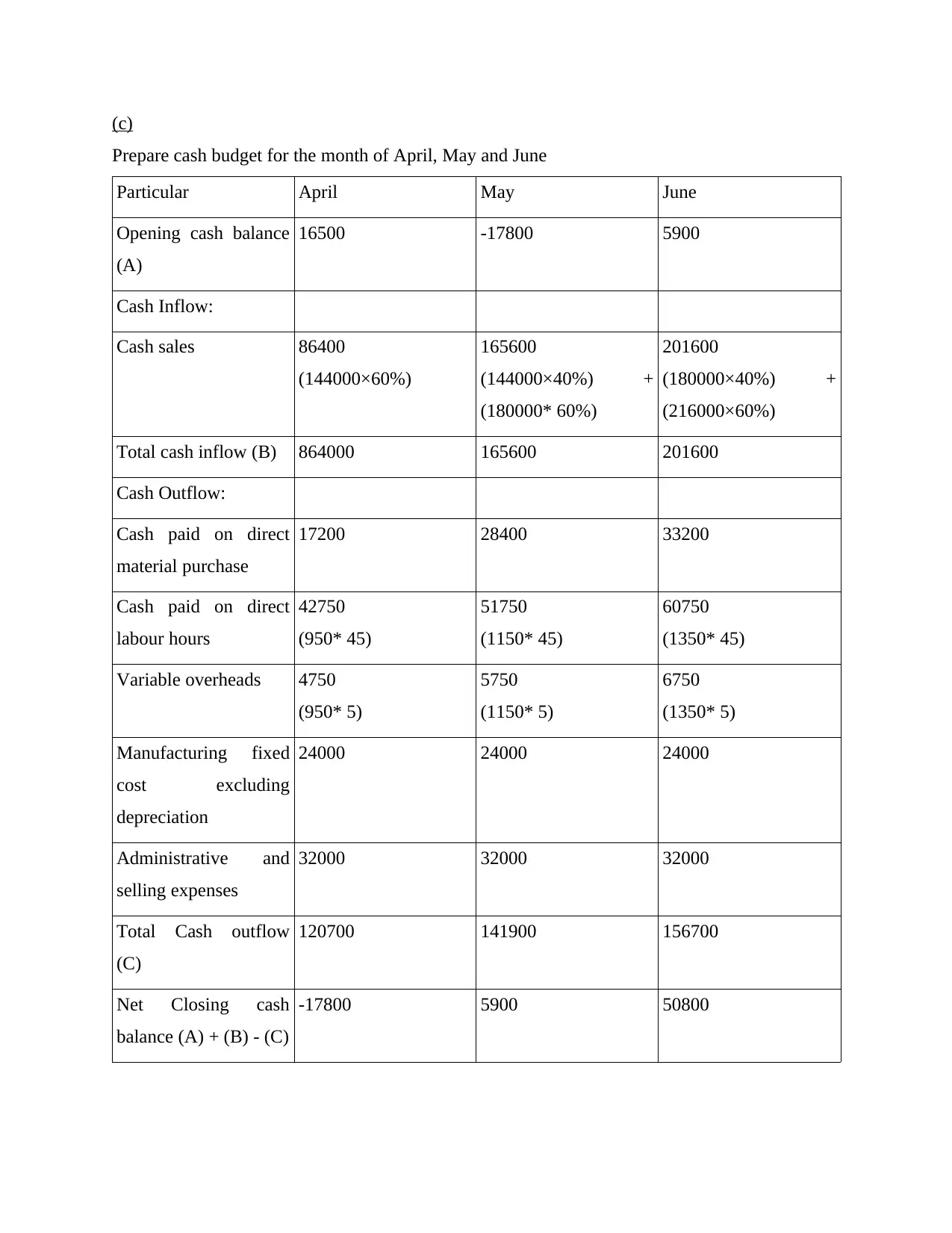

(c)

Prepare cash budget for the month of April, May and June

Particular April May June

Opening cash balance

(A)

16500 -17800 5900

Cash Inflow:

Cash sales 86400

(144000×60%)

165600

(144000×40%) +

(180000* 60%)

201600

(180000×40%) +

(216000×60%)

Total cash inflow (B) 864000 165600 201600

Cash Outflow:

Cash paid on direct

material purchase

17200 28400 33200

Cash paid on direct

labour hours

42750

(950* 45)

51750

(1150* 45)

60750

(1350* 45)

Variable overheads 4750

(950* 5)

5750

(1150* 5)

6750

(1350* 5)

Manufacturing fixed

cost excluding

depreciation

24000 24000 24000

Administrative and

selling expenses

32000 32000 32000

Total Cash outflow

(C)

120700 141900 156700

Net Closing cash

balance (A) + (B) - (C)

-17800 5900 50800

Prepare cash budget for the month of April, May and June

Particular April May June

Opening cash balance

(A)

16500 -17800 5900

Cash Inflow:

Cash sales 86400

(144000×60%)

165600

(144000×40%) +

(180000* 60%)

201600

(180000×40%) +

(216000×60%)

Total cash inflow (B) 864000 165600 201600

Cash Outflow:

Cash paid on direct

material purchase

17200 28400 33200

Cash paid on direct

labour hours

42750

(950* 45)

51750

(1150* 45)

60750

(1350* 45)

Variable overheads 4750

(950* 5)

5750

(1150* 5)

6750

(1350* 5)

Manufacturing fixed

cost excluding

depreciation

24000 24000 24000

Administrative and

selling expenses

32000 32000 32000

Total Cash outflow

(C)

120700 141900 156700

Net Closing cash

balance (A) + (B) - (C)

-17800 5900 50800

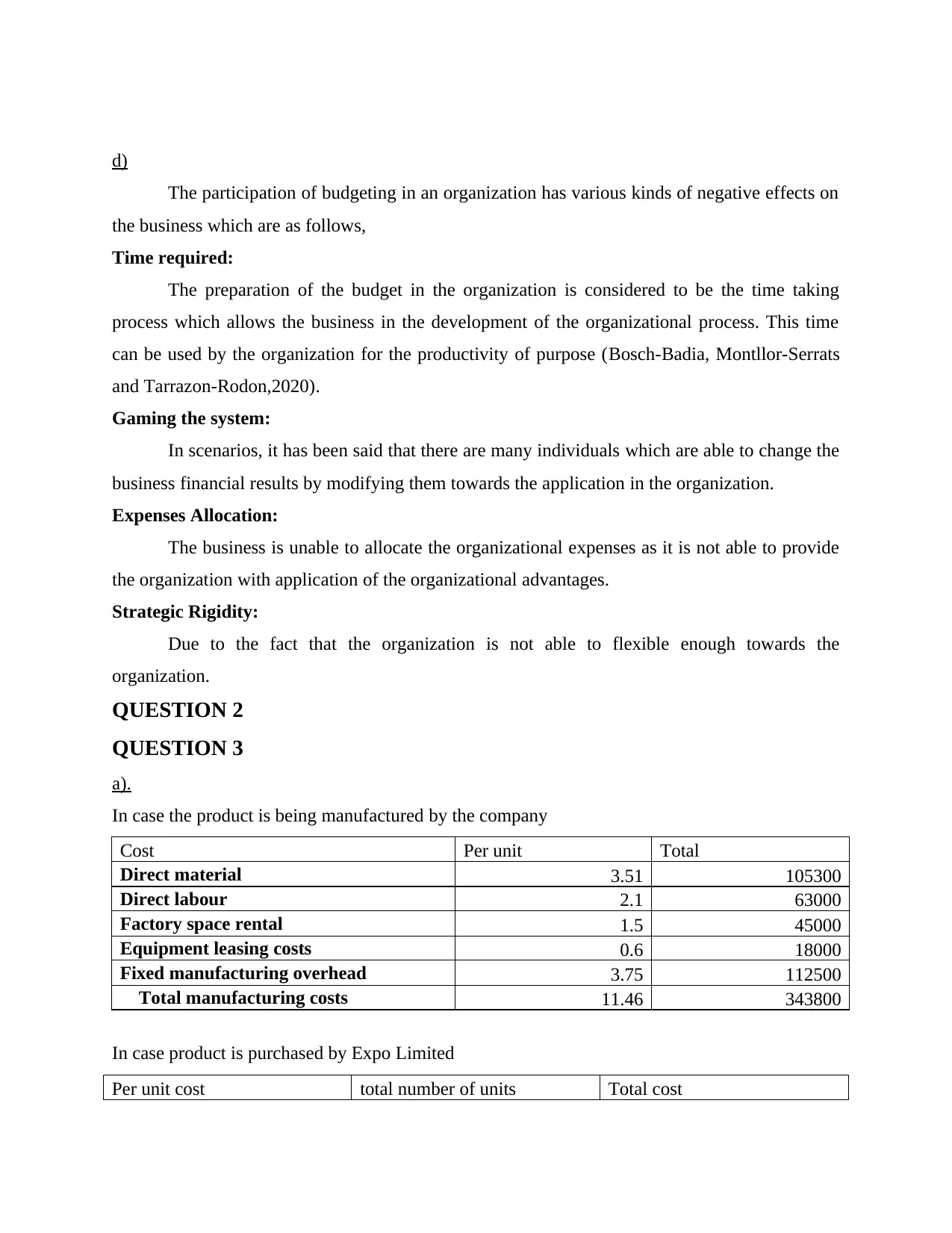

d)

The participation of budgeting in an organization has various kinds of negative effects on

the business which are as follows,

Time required:

The preparation of the budget in the organization is considered to be the time taking

process which allows the business in the development of the organizational process. This time

can be used by the organization for the productivity of purpose (Bosch-Badia, Montllor-Serrats

and Tarrazon-Rodon,2020).

Gaming the system:

In scenarios, it has been said that there are many individuals which are able to change the

business financial results by modifying them towards the application in the organization.

Expenses Allocation:

The business is unable to allocate the organizational expenses as it is not able to provide

the organization with application of the organizational advantages.

Strategic Rigidity:

Due to the fact that the organization is not able to flexible enough towards the

organization.

QUESTION 2

QUESTION 3

a).

In case the product is being manufactured by the company

Cost Per unit Total

Direct material 3.51 105300

Direct labour 2.1 63000

Factory space rental 1.5 45000

Equipment leasing costs 0.6 18000

Fixed manufacturing overhead 3.75 112500

Total manufacturing costs 11.46 343800

In case product is purchased by Expo Limited

Per unit cost total number of units Total cost

The participation of budgeting in an organization has various kinds of negative effects on

the business which are as follows,

Time required:

The preparation of the budget in the organization is considered to be the time taking

process which allows the business in the development of the organizational process. This time

can be used by the organization for the productivity of purpose (Bosch-Badia, Montllor-Serrats

and Tarrazon-Rodon,2020).

Gaming the system:

In scenarios, it has been said that there are many individuals which are able to change the

business financial results by modifying them towards the application in the organization.

Expenses Allocation:

The business is unable to allocate the organizational expenses as it is not able to provide

the organization with application of the organizational advantages.

Strategic Rigidity:

Due to the fact that the organization is not able to flexible enough towards the

organization.

QUESTION 2

QUESTION 3

a).

In case the product is being manufactured by the company

Cost Per unit Total

Direct material 3.51 105300

Direct labour 2.1 63000

Factory space rental 1.5 45000

Equipment leasing costs 0.6 18000

Fixed manufacturing overhead 3.75 112500

Total manufacturing costs 11.46 343800

In case product is purchased by Expo Limited

Per unit cost total number of units Total cost

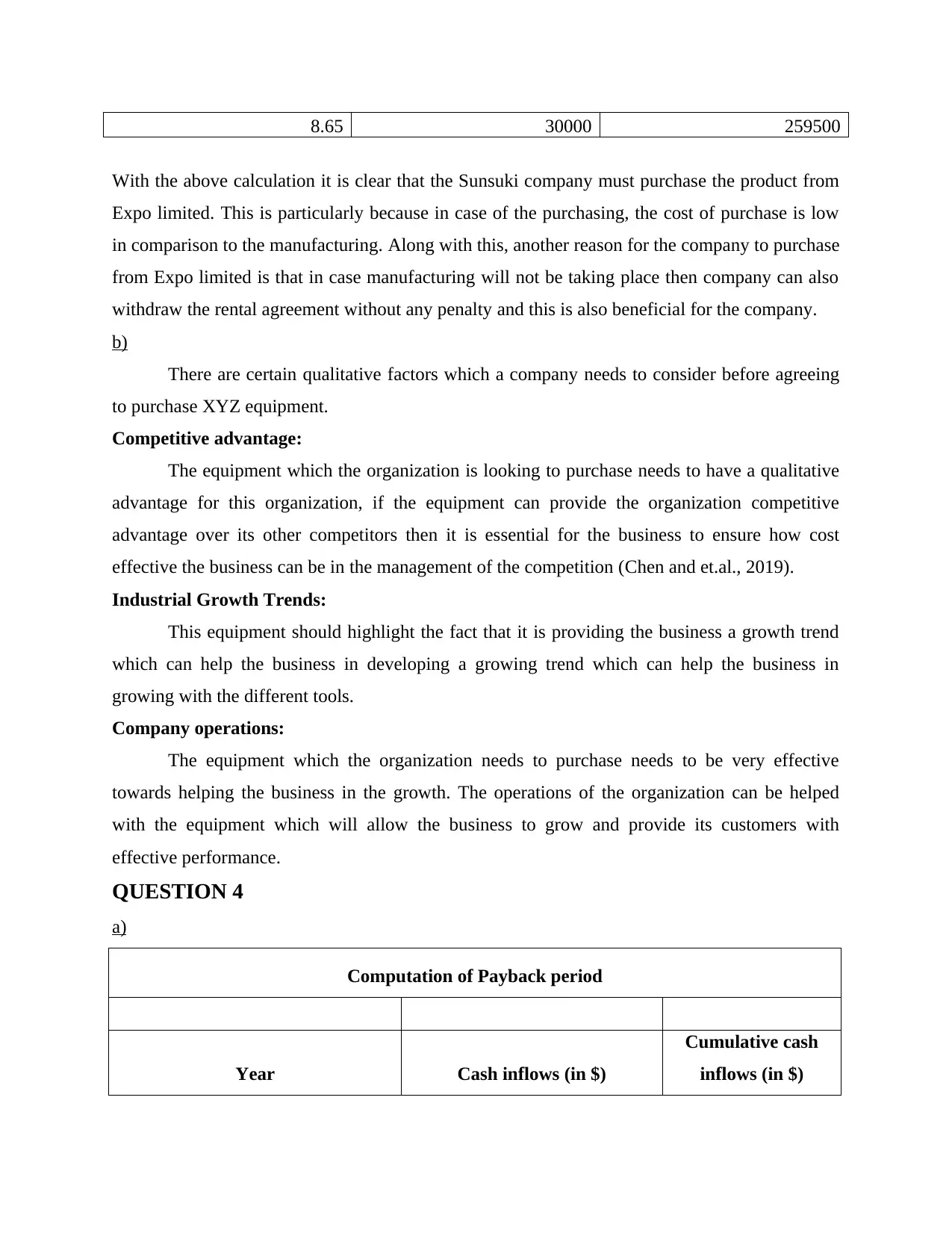

8.65 30000 259500

With the above calculation it is clear that the Sunsuki company must purchase the product from

Expo limited. This is particularly because in case of the purchasing, the cost of purchase is low

in comparison to the manufacturing. Along with this, another reason for the company to purchase

from Expo limited is that in case manufacturing will not be taking place then company can also

withdraw the rental agreement without any penalty and this is also beneficial for the company.

b)

There are certain qualitative factors which a company needs to consider before agreeing

to purchase XYZ equipment.

Competitive advantage:

The equipment which the organization is looking to purchase needs to have a qualitative

advantage for this organization, if the equipment can provide the organization competitive

advantage over its other competitors then it is essential for the business to ensure how cost

effective the business can be in the management of the competition (Chen and et.al., 2019).

Industrial Growth Trends:

This equipment should highlight the fact that it is providing the business a growth trend

which can help the business in developing a growing trend which can help the business in

growing with the different tools.

Company operations:

The equipment which the organization needs to purchase needs to be very effective

towards helping the business in the growth. The operations of the organization can be helped

with the equipment which will allow the business to grow and provide its customers with

effective performance.

QUESTION 4

a)

Computation of Payback period

Year Cash inflows (in $)

Cumulative cash

inflows (in $)

With the above calculation it is clear that the Sunsuki company must purchase the product from

Expo limited. This is particularly because in case of the purchasing, the cost of purchase is low

in comparison to the manufacturing. Along with this, another reason for the company to purchase

from Expo limited is that in case manufacturing will not be taking place then company can also

withdraw the rental agreement without any penalty and this is also beneficial for the company.

b)

There are certain qualitative factors which a company needs to consider before agreeing

to purchase XYZ equipment.

Competitive advantage:

The equipment which the organization is looking to purchase needs to have a qualitative

advantage for this organization, if the equipment can provide the organization competitive

advantage over its other competitors then it is essential for the business to ensure how cost

effective the business can be in the management of the competition (Chen and et.al., 2019).

Industrial Growth Trends:

This equipment should highlight the fact that it is providing the business a growth trend

which can help the business in developing a growing trend which can help the business in

growing with the different tools.

Company operations:

The equipment which the organization needs to purchase needs to be very effective

towards helping the business in the growth. The operations of the organization can be helped

with the equipment which will allow the business to grow and provide its customers with

effective performance.

QUESTION 4

a)

Computation of Payback period

Year Cash inflows (in $)

Cumulative cash

inflows (in $)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

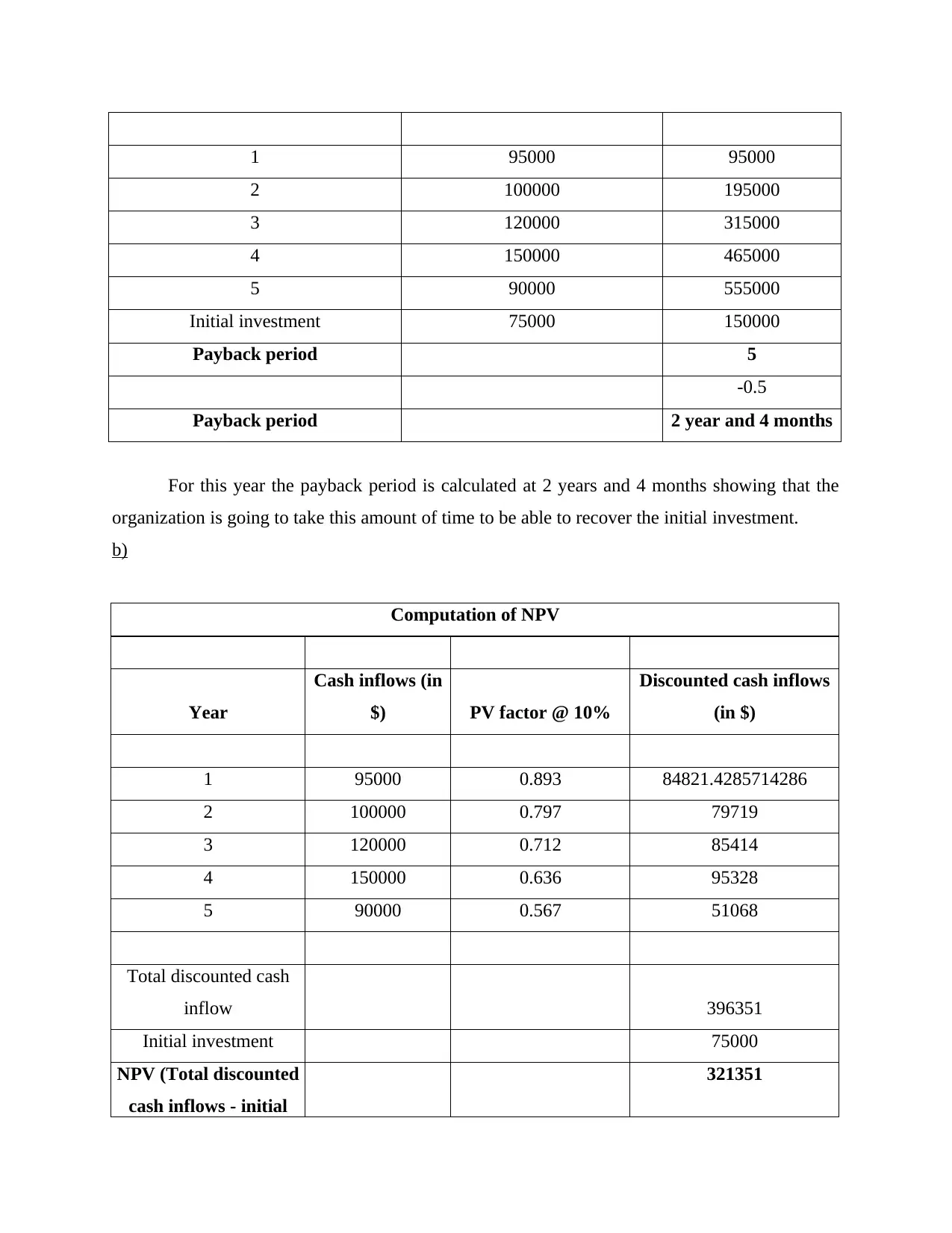

1 95000 95000

2 100000 195000

3 120000 315000

4 150000 465000

5 90000 555000

Initial investment 75000 150000

Payback period 5

-0.5

Payback period 2 year and 4 months

For this year the payback period is calculated at 2 years and 4 months showing that the

organization is going to take this amount of time to be able to recover the initial investment.

b)

Computation of NPV

Year

Cash inflows (in

$) PV factor @ 10%

Discounted cash inflows

(in $)

1 95000 0.893 84821.4285714286

2 100000 0.797 79719

3 120000 0.712 85414

4 150000 0.636 95328

5 90000 0.567 51068

Total discounted cash

inflow 396351

Initial investment 75000

NPV (Total discounted

cash inflows - initial

321351

2 100000 195000

3 120000 315000

4 150000 465000

5 90000 555000

Initial investment 75000 150000

Payback period 5

-0.5

Payback period 2 year and 4 months

For this year the payback period is calculated at 2 years and 4 months showing that the

organization is going to take this amount of time to be able to recover the initial investment.

b)

Computation of NPV

Year

Cash inflows (in

$) PV factor @ 10%

Discounted cash inflows

(in $)

1 95000 0.893 84821.4285714286

2 100000 0.797 79719

3 120000 0.712 85414

4 150000 0.636 95328

5 90000 0.567 51068

Total discounted cash

inflow 396351

Initial investment 75000

NPV (Total discounted

cash inflows - initial

321351

investment)

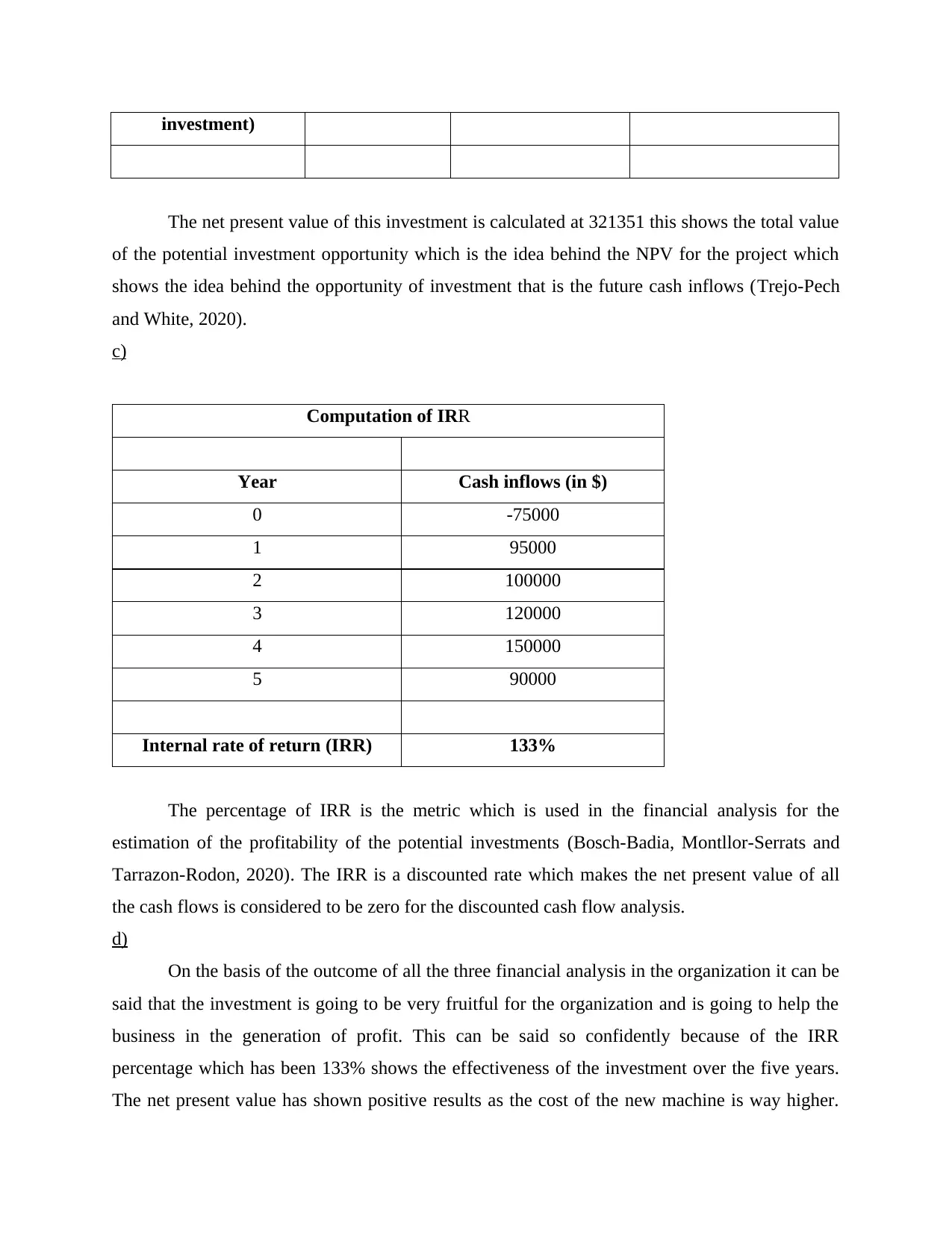

The net present value of this investment is calculated at 321351 this shows the total value

of the potential investment opportunity which is the idea behind the NPV for the project which

shows the idea behind the opportunity of investment that is the future cash inflows (Trejo-Pech

and White, 2020).

c)

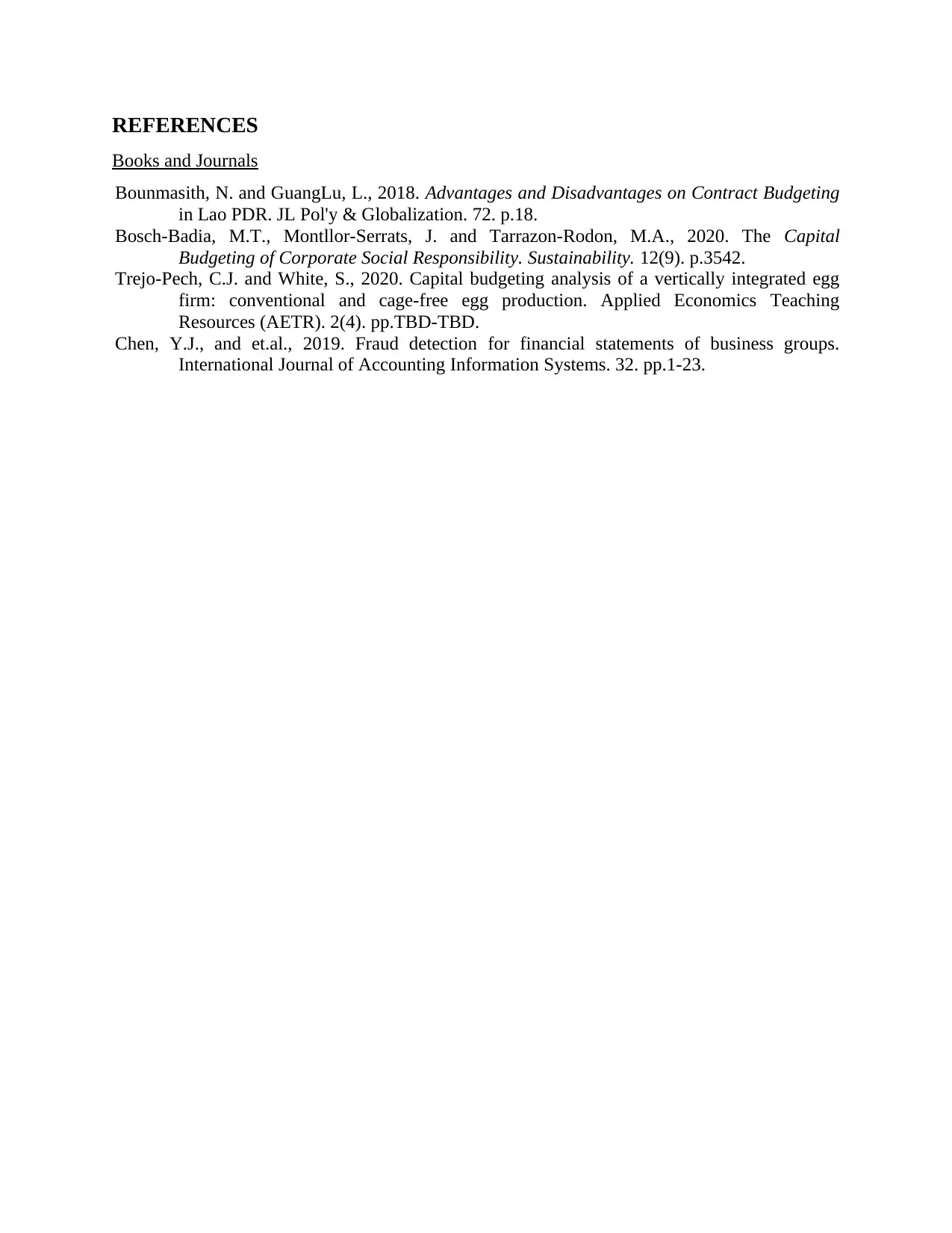

Computation of IRR

Year Cash inflows (in $)

0 -75000

1 95000

2 100000

3 120000

4 150000

5 90000

Internal rate of return (IRR) 133%

The percentage of IRR is the metric which is used in the financial analysis for the

estimation of the profitability of the potential investments (Bosch-Badia, Montllor-Serrats and

Tarrazon-Rodon, 2020). The IRR is a discounted rate which makes the net present value of all

the cash flows is considered to be zero for the discounted cash flow analysis.

d)

On the basis of the outcome of all the three financial analysis in the organization it can be

said that the investment is going to be very fruitful for the organization and is going to help the

business in the generation of profit. This can be said so confidently because of the IRR

percentage which has been 133% shows the effectiveness of the investment over the five years.

The net present value has shown positive results as the cost of the new machine is way higher.

The net present value of this investment is calculated at 321351 this shows the total value

of the potential investment opportunity which is the idea behind the NPV for the project which

shows the idea behind the opportunity of investment that is the future cash inflows (Trejo-Pech

and White, 2020).

c)

Computation of IRR

Year Cash inflows (in $)

0 -75000

1 95000

2 100000

3 120000

4 150000

5 90000

Internal rate of return (IRR) 133%

The percentage of IRR is the metric which is used in the financial analysis for the

estimation of the profitability of the potential investments (Bosch-Badia, Montllor-Serrats and

Tarrazon-Rodon, 2020). The IRR is a discounted rate which makes the net present value of all

the cash flows is considered to be zero for the discounted cash flow analysis.

d)

On the basis of the outcome of all the three financial analysis in the organization it can be

said that the investment is going to be very fruitful for the organization and is going to help the

business in the generation of profit. This can be said so confidently because of the IRR

percentage which has been 133% shows the effectiveness of the investment over the five years.

The net present value has shown positive results as the cost of the new machine is way higher.

The payback period is almost 50% of the total estimated life of the asset showing that this

organization is able to recover its investment in the time of 2 years and 4 months.

organization is able to recover its investment in the time of 2 years and 4 months.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Bounmasith, N. and GuangLu, L., 2018. Advantages and Disadvantages on Contract Budgeting

in Lao PDR. JL Pol'y & Globalization. 72. p.18.

Bosch-Badia, M.T., Montllor-Serrats, J. and Tarrazon-Rodon, M.A., 2020. The Capital

Budgeting of Corporate Social Responsibility. Sustainability. 12(9). p.3542.

Trejo-Pech, C.J. and White, S., 2020. Capital budgeting analysis of a vertically integrated egg

firm: conventional and cage-free egg production. Applied Economics Teaching

Resources (AETR). 2(4). pp.TBD-TBD.

Chen, Y.J., and et.al., 2019. Fraud detection for financial statements of business groups.

International Journal of Accounting Information Systems. 32. pp.1-23.

Books and Journals

Bounmasith, N. and GuangLu, L., 2018. Advantages and Disadvantages on Contract Budgeting

in Lao PDR. JL Pol'y & Globalization. 72. p.18.

Bosch-Badia, M.T., Montllor-Serrats, J. and Tarrazon-Rodon, M.A., 2020. The Capital

Budgeting of Corporate Social Responsibility. Sustainability. 12(9). p.3542.

Trejo-Pech, C.J. and White, S., 2020. Capital budgeting analysis of a vertically integrated egg

firm: conventional and cage-free egg production. Applied Economics Teaching

Resources (AETR). 2(4). pp.TBD-TBD.

Chen, Y.J., and et.al., 2019. Fraud detection for financial statements of business groups.

International Journal of Accounting Information Systems. 32. pp.1-23.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.