HI5017, T3 2019: Sunline Auto Insurance - Target Costing Case Analysis

VerifiedAdded on 2022/08/22

|9

|2658

|17

Case Study

AI Summary

This case study examines Sunline Auto Insurance, a company facing financial challenges in a competitive market. The case focuses on the 'Ride Cover' product and its 'cost-plus' pricing strategy, which is proving unsustainable due to customer price sensitivity. The analysis delves into Sunline's costs across various operational areas, including administration, sales and marketing, technology, and financing, highlighting the impact of these costs on profitability. The central theme revolves around applying target costing to improve financial outcomes. The case provides data on current premium revenues and costs per policy, illustrating the losses incurred. It then presents a target costing approach, calculating the required cost reduction to achieve a desired profit margin at a competitive price point. The case concludes by proposing strategic realignment activities to achieve the necessary cost reductions, emphasizing the need for a more strategic and customer-focused approach to cost management. The case is designed to facilitate discussion on how target costing can be used to improve product sales and financial performance.

1

Applying target costing to the service sector: Sunline

Auto Insurance case

Dr James Wakefield, UTS Business School and Dr Paul Thambar, Monash Business School wrote this case

solely to provide material for class room discussion. The authors do not intend to illustrate either an effective or

ineffective handling of a managerial situation. The authors have based this case on a real-life firm but may have

disguised certain names and other identifying information to protect confidentiality.

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

Applying target costing to the service sector: Sunline

Auto Insurance case

Dr James Wakefield, UTS Business School and Dr Paul Thambar, Monash Business School wrote this case

solely to provide material for class room discussion. The authors do not intend to illustrate either an effective or

ineffective handling of a managerial situation. The authors have based this case on a real-life firm but may have

disguised certain names and other identifying information to protect confidentiality.

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

TEACHING CASE

Background and strategy

Janet Pretty, Business Manager of Sunline Auto Insurance based in Los Angeles, was

in her office on a bright Monday morning in January 2017 reviewing her monthly

performance report. Janet was worried as she reviewed the performance of Sunline for the

last quarter (October to December 2016). The report showed that while sales were growing,

so were losses (Refer Exhibit 1-Table 1).

Sunline was wholly owned by Palm Investments, headquartered in San Francisco,

which owned eight other companies in the finance and insurance sector. Sunline was

managed on a decentralised management by exception basis. The headquarters provided legal

and compliance advice to the subsidiaries and ultimately closely monitored each subsidiary.

Janet Pretty had significant autonomy to develop, promote, sell and manage the activities of

Sunline. Accordingly, she was very concerned about the current state of performance, as she

was directly accountable for the performance realised, even though she had only been

working at Sunline for six months.

Auto insurance was very popular in the state of California due to the high levels of

motor vehicle ownership. Federal government statistics showed that on average, each family

in California owned four motor vehicles. Injury and property damage insurance were legally

required in California. Sunline was only established five years ago and faced a very

competitive market. Customers were quite demanding in the prices they paid for auto

insurance policies and also very selective in terms of the features of the policies. The unique

positioning of insurance policy products to acquire market share was therefore very

important. Since establishment Sunline had grown its market share and customer base

relatively quickly in Los Angeles.

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

TEACHING CASE

Background and strategy

Janet Pretty, Business Manager of Sunline Auto Insurance based in Los Angeles, was

in her office on a bright Monday morning in January 2017 reviewing her monthly

performance report. Janet was worried as she reviewed the performance of Sunline for the

last quarter (October to December 2016). The report showed that while sales were growing,

so were losses (Refer Exhibit 1-Table 1).

Sunline was wholly owned by Palm Investments, headquartered in San Francisco,

which owned eight other companies in the finance and insurance sector. Sunline was

managed on a decentralised management by exception basis. The headquarters provided legal

and compliance advice to the subsidiaries and ultimately closely monitored each subsidiary.

Janet Pretty had significant autonomy to develop, promote, sell and manage the activities of

Sunline. Accordingly, she was very concerned about the current state of performance, as she

was directly accountable for the performance realised, even though she had only been

working at Sunline for six months.

Auto insurance was very popular in the state of California due to the high levels of

motor vehicle ownership. Federal government statistics showed that on average, each family

in California owned four motor vehicles. Injury and property damage insurance were legally

required in California. Sunline was only established five years ago and faced a very

competitive market. Customers were quite demanding in the prices they paid for auto

insurance policies and also very selective in terms of the features of the policies. The unique

positioning of insurance policy products to acquire market share was therefore very

important. Since establishment Sunline had grown its market share and customer base

relatively quickly in Los Angeles.

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

3

Consistent with the management autonomy extended to each subsidiary, Sunline

management could develop unique product offerings. Sunline had developed and focused

solely on a unique product called Ride Cover, specifically targeted at car enthusiasts with

unique cars. The product packaged the compulsory insurance coverage (based on minimum

legal requirements in California1) with comprehensive and collision insurance. Ride Cover

offered unique benefits including full replacement value, a loan vehicle with no mileage limit

while the owner’s vehicle was off the road being repaired, the owner’s choice of repairer and

unlimited roadside assistance in the event of a breakdown. The product was particularly

appealing to customers with customised cars, who had spent significant money and time

modifying these vehicles. The modified nature of these vehicles also meant that mechanical

problems were more likely. Accordingly customers placed great value on the ability to take

the car to the owner’s repairer of choice and receive unlimited roadside assistance. Customers

could also opt for higher levels of injury and property coverage, beyond that required in

California, and lower deductibles as part of the Ride Cover policy.

Ride Cover could be acquired by customers through Sunline stores (in major shopping

centres such as Glendale Galleria, South Coast Plaza and The Beverley Centre), Sunline’s

webpage, Wells Fargo Banks and supermarkets (such as Ralphs). The company also had pop

up stalls at motoring events (including the annual LA Motor Show and various Cars and

Coffee meets) to specifically target enthusiast car owners. In each of these distribution

channels, dedicated staff and/or representatives from the Sunline were available to provide

customer service including assessing customer needs, answering inquiries, pricing policies

and providing general support to customers. The use of multiple distribution channels

provided customers with easy access to Ride Cover.

1 See http://www.dmv.org/ca-california/car-insurance.php

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

Consistent with the management autonomy extended to each subsidiary, Sunline

management could develop unique product offerings. Sunline had developed and focused

solely on a unique product called Ride Cover, specifically targeted at car enthusiasts with

unique cars. The product packaged the compulsory insurance coverage (based on minimum

legal requirements in California1) with comprehensive and collision insurance. Ride Cover

offered unique benefits including full replacement value, a loan vehicle with no mileage limit

while the owner’s vehicle was off the road being repaired, the owner’s choice of repairer and

unlimited roadside assistance in the event of a breakdown. The product was particularly

appealing to customers with customised cars, who had spent significant money and time

modifying these vehicles. The modified nature of these vehicles also meant that mechanical

problems were more likely. Accordingly customers placed great value on the ability to take

the car to the owner’s repairer of choice and receive unlimited roadside assistance. Customers

could also opt for higher levels of injury and property coverage, beyond that required in

California, and lower deductibles as part of the Ride Cover policy.

Ride Cover could be acquired by customers through Sunline stores (in major shopping

centres such as Glendale Galleria, South Coast Plaza and The Beverley Centre), Sunline’s

webpage, Wells Fargo Banks and supermarkets (such as Ralphs). The company also had pop

up stalls at motoring events (including the annual LA Motor Show and various Cars and

Coffee meets) to specifically target enthusiast car owners. In each of these distribution

channels, dedicated staff and/or representatives from the Sunline were available to provide

customer service including assessing customer needs, answering inquiries, pricing policies

and providing general support to customers. The use of multiple distribution channels

provided customers with easy access to Ride Cover.

1 See http://www.dmv.org/ca-california/car-insurance.php

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Product costing and pricing strategy

Sunline operated a “cost plus” product costing and pricing strategy, which had been in

place since establishment, five years ago. The cost-plus pricing model was based on the

assumption that customers were willing to wear a reasonable level of pricing for the auto

insurance product. Essentially the cost associated with all operations were added up, referring

to actual and budgeted costs, and averaged across the number of estimated policies sold in the

period. An average target profit margin was then added to the average costs, to price the

product. This was an “average target profit margin” as product pricing was determined to a

great extent by individual customer risk profile and government insurance pricing

regulations, and accordingly policy pricing for different customers.

Table 2 in Exhibit 1 outlines the costs related to Sunline. There are five groups of

costs that relate to operating the business: administration, sales and marketing, technology,

financing and headquarter costs. Administration costs were incurred for training programs of

sales staff and representatives, administration of traffic accident cases and claims,

recruitment, payroll and financial accounting and performance reporting. Sales staff training

programs were a key element in preparing staff to understand market requirements and

product features, helping to lift product sales through channel partners. However, training

costs had continued to rise and this issue was not helped by high staff turnover.

Administration and payment of insurance claims was the largest component of administrative

costs and how this process was managed, how timely they were paid out for Ride Cover

customers with choice of repairer, had a direct bearing on customer service, future sales and

market share growth. This cost continued to grow and headquarters felt Janet and her team

were not doing enough in a focused manner to educate staff and customers on how to reduce

accidents, improve claims processes and to enable reduction of these costs.

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

Product costing and pricing strategy

Sunline operated a “cost plus” product costing and pricing strategy, which had been in

place since establishment, five years ago. The cost-plus pricing model was based on the

assumption that customers were willing to wear a reasonable level of pricing for the auto

insurance product. Essentially the cost associated with all operations were added up, referring

to actual and budgeted costs, and averaged across the number of estimated policies sold in the

period. An average target profit margin was then added to the average costs, to price the

product. This was an “average target profit margin” as product pricing was determined to a

great extent by individual customer risk profile and government insurance pricing

regulations, and accordingly policy pricing for different customers.

Table 2 in Exhibit 1 outlines the costs related to Sunline. There are five groups of

costs that relate to operating the business: administration, sales and marketing, technology,

financing and headquarter costs. Administration costs were incurred for training programs of

sales staff and representatives, administration of traffic accident cases and claims,

recruitment, payroll and financial accounting and performance reporting. Sales staff training

programs were a key element in preparing staff to understand market requirements and

product features, helping to lift product sales through channel partners. However, training

costs had continued to rise and this issue was not helped by high staff turnover.

Administration and payment of insurance claims was the largest component of administrative

costs and how this process was managed, how timely they were paid out for Ride Cover

customers with choice of repairer, had a direct bearing on customer service, future sales and

market share growth. This cost continued to grow and headquarters felt Janet and her team

were not doing enough in a focused manner to educate staff and customers on how to reduce

accidents, improve claims processes and to enable reduction of these costs.

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

The sales and marketing team focused on promoting the Ride Cover policy through

different advertising campaigns and event engagement. The policy was heavily promoted

through local television and billboards to convey the unique benefits and value of the Ride

Cover policy to potential customers. Online advertising and social media engagement was

also used to promote products. Some attention was directed to engaging with local

automotive events, through pop up stalls. Headquarters had expressed concern about the

effectiveness of the marketing spend and if Sunline had realised the full impact expected

from the marking campaigns.

Technology costs related to the online sales channels and information systems used by

Sunline to manage the operations of auto insurance sales. These costs also included costs of

new media platform, cloud based database systems and related data analytics which were

increasingly used to understand customer behaviour and to predict future sales and market

share growth. The increased use of technology at Sunline had not been accompanied by

improvements to operational efficiency and effectiveness. Since joining Sunline, Janet was of

the view that operations required a transformation project to leverage the benefits of the

greater use of technology through efficiencies in processes and staffing. Janet wondered if the

cost-plus approach to pricing had created a management perspective that didn’t focus

strategically on cost management.

Financing costs involved funding the operations of Sunline and investing the cash

from Ride Cover premia raised. The dedicated and specialised financing support team also

invested excess cash in sophisticated equity and debt securities. The costs associated with

these investment transactions were covered by the revenue raised by this team through its

investment activities. Janet considered this team made an important contribution to Sunline

performance, however she had little interaction with them.

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

The sales and marketing team focused on promoting the Ride Cover policy through

different advertising campaigns and event engagement. The policy was heavily promoted

through local television and billboards to convey the unique benefits and value of the Ride

Cover policy to potential customers. Online advertising and social media engagement was

also used to promote products. Some attention was directed to engaging with local

automotive events, through pop up stalls. Headquarters had expressed concern about the

effectiveness of the marketing spend and if Sunline had realised the full impact expected

from the marking campaigns.

Technology costs related to the online sales channels and information systems used by

Sunline to manage the operations of auto insurance sales. These costs also included costs of

new media platform, cloud based database systems and related data analytics which were

increasingly used to understand customer behaviour and to predict future sales and market

share growth. The increased use of technology at Sunline had not been accompanied by

improvements to operational efficiency and effectiveness. Since joining Sunline, Janet was of

the view that operations required a transformation project to leverage the benefits of the

greater use of technology through efficiencies in processes and staffing. Janet wondered if the

cost-plus approach to pricing had created a management perspective that didn’t focus

strategically on cost management.

Financing costs involved funding the operations of Sunline and investing the cash

from Ride Cover premia raised. The dedicated and specialised financing support team also

invested excess cash in sophisticated equity and debt securities. The costs associated with

these investment transactions were covered by the revenue raised by this team through its

investment activities. Janet considered this team made an important contribution to Sunline

performance, however she had little interaction with them.

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

6

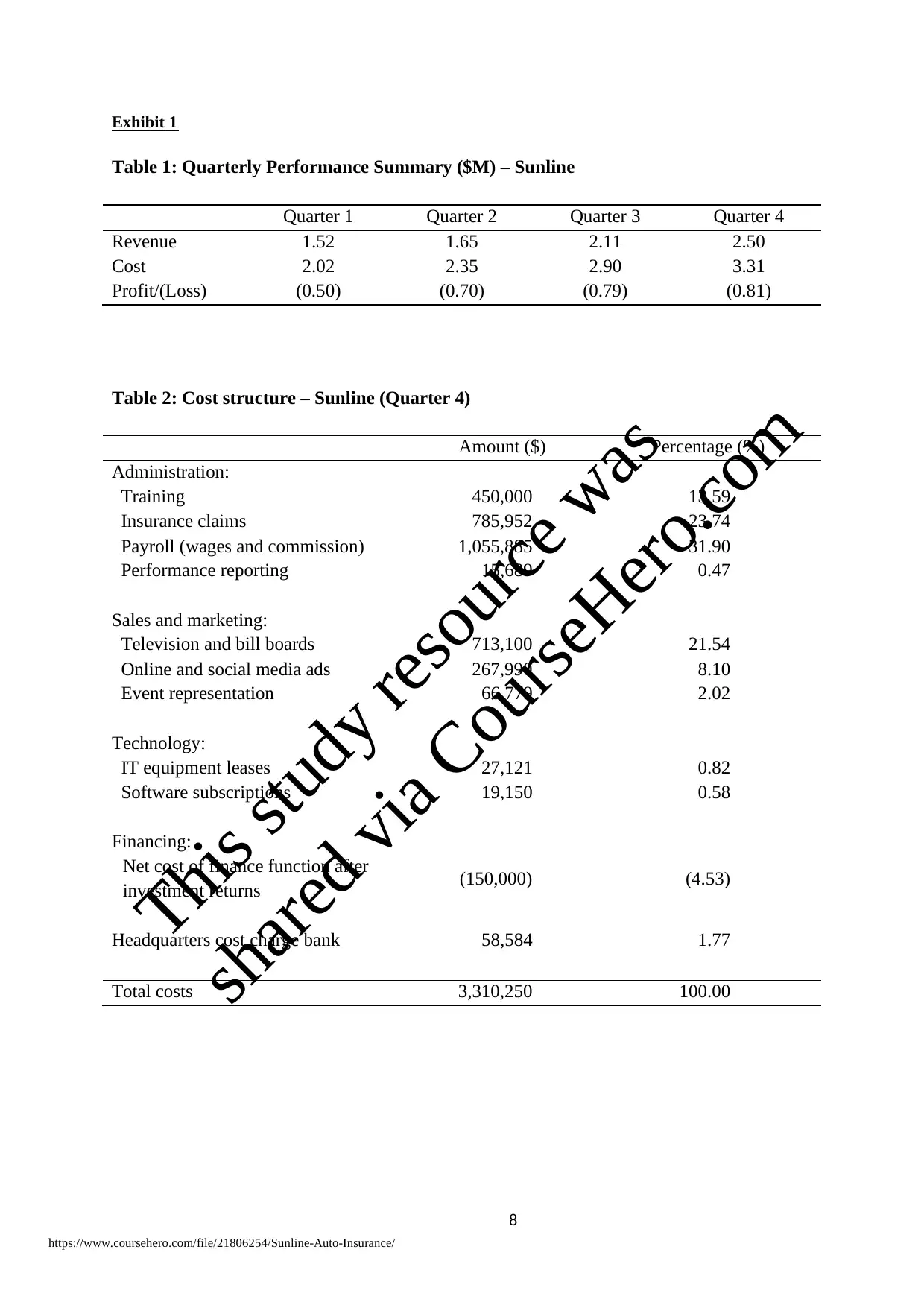

The total cost of operating the headquarters was charged back to the nine subsidiaries.

To keep matters simple, headquarters charged back one ninth of the cost to each of the nine

subsidiaries. Janet was not convinced that the simple allocation basis matched the actual level

of services and transactions at Sunline. While this caused some tension between the different

subsidiaries, the overall cost associated with this was relatively small.

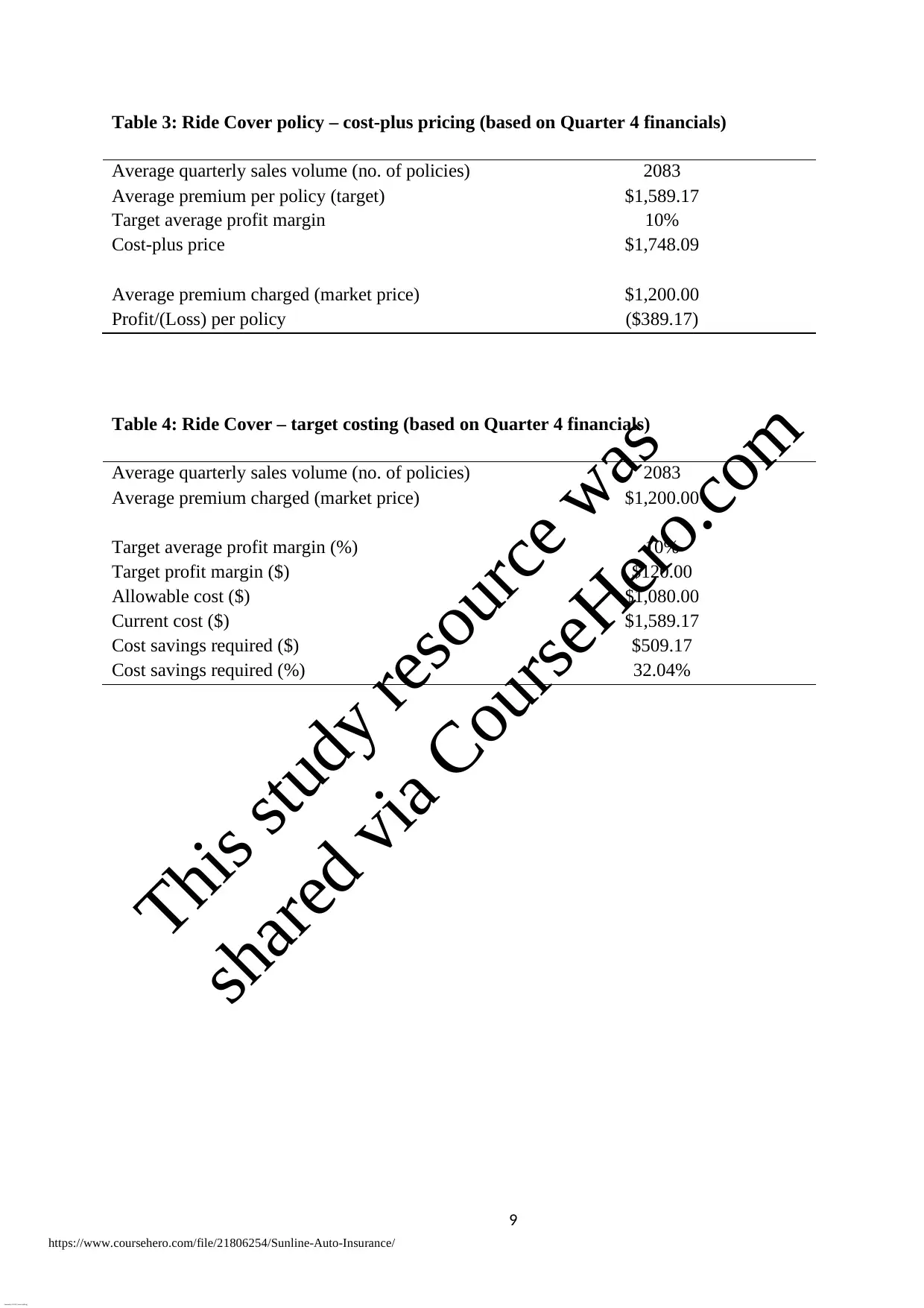

Table 3 in Exhibit 1 sets out the key financials related to the cost-plus pricing

approach undertaken for Ride Cover policy. These financials relate to quarter 4 and show the

average premium revenue and costs per policy. The loss per policy is $389.17 based on an

average target policy premium of $1,589.17. Due to market pressure, including customers

threatening to take their business elsewhere, the average premium is actually $1,200,

inconsistent with the cost-plus approach.

Strategic cost and revenue management

As she pondered on the performance in the last quarter, it became clear to Janet that

the current revenue and cost strategy based on a “cost plus” approach was not sustainable in

the future. Customers were becoming very choosy about the pricing of auto insurance

products and were demanding cheaper insurance products. She recalled reading an article on

Target Costing (TC) which was a strategic cost and revenue approach for improving product

sales through a more strategic view of customers’ preferences and needs. Janet wondered if

she could develop a position paper on TC to demonstrate to headquarters how Sunline would

strategically consider cost priorities and manage down cost not closely associated with the

competitive position of the product offering.

As she recalled, TC focused on the price the customer was willing to pay for a

product and enabled a firm to reverse engineer its product cost structure based on this target

price. A firm estimated the target price by carrying out market analysis, to understand what

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

The total cost of operating the headquarters was charged back to the nine subsidiaries.

To keep matters simple, headquarters charged back one ninth of the cost to each of the nine

subsidiaries. Janet was not convinced that the simple allocation basis matched the actual level

of services and transactions at Sunline. While this caused some tension between the different

subsidiaries, the overall cost associated with this was relatively small.

Table 3 in Exhibit 1 sets out the key financials related to the cost-plus pricing

approach undertaken for Ride Cover policy. These financials relate to quarter 4 and show the

average premium revenue and costs per policy. The loss per policy is $389.17 based on an

average target policy premium of $1,589.17. Due to market pressure, including customers

threatening to take their business elsewhere, the average premium is actually $1,200,

inconsistent with the cost-plus approach.

Strategic cost and revenue management

As she pondered on the performance in the last quarter, it became clear to Janet that

the current revenue and cost strategy based on a “cost plus” approach was not sustainable in

the future. Customers were becoming very choosy about the pricing of auto insurance

products and were demanding cheaper insurance products. She recalled reading an article on

Target Costing (TC) which was a strategic cost and revenue approach for improving product

sales through a more strategic view of customers’ preferences and needs. Janet wondered if

she could develop a position paper on TC to demonstrate to headquarters how Sunline would

strategically consider cost priorities and manage down cost not closely associated with the

competitive position of the product offering.

As she recalled, TC focused on the price the customer was willing to pay for a

product and enabled a firm to reverse engineer its product cost structure based on this target

price. A firm estimated the target price by carrying out market analysis, to understand what

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

features of the product were attractive to the customer and how much customers were willing

to pay for each feature. Once a target price was determined, the firm had to take profit margin

away to arrive at a target cost. This cost was labelled the allowable cost which, usually,

would be lower than the current product costs within the firm. The firm then had to carry out

cost management activities and strategic realignment to bring the current product costs down

to the target cost (allowable cost) over a period of time.

Table 4 in Exhibit 1 sets out the pricing for Ride Cover if it was based on a target

costing approach. Current market research suggests that the average premium for a policy

would need to be set at an average of $1,200 (based on the current average premium actually

charged) to maintain current sales volumes and market share. Based on earning a profit

margin of 10%, the allowable cost of a policy would need to be set at $1,080 which would

require a 32.04% reduction from the current level of product costs. Cost management and

strategic realignment activities would need to be carried out to improve the costs of Ride

Cover.

The Target Cost approach focused the firm on all aspects of the revenue and costs of a

product and brought in a questioning attitude to all operational activities. Long used in

Japanese firms, Target Costing as a strategic approach to revenue and cost management had

been neglected in Western firms as it required management and cultural changes to enforce.

But, Janet felt it was a useful approach for Sunline to consider and began to gather

information to develop a paper on Target Costing. She began to consider some key issues:

what is the process of Target Costing and how can it be adapted for auto insurance products?

What are the changes to operational priorities and management processes required when

moving Sunline from a cost-plus pricing strategy to a strategic revenue and cost management

strategy such as TC? What key steps should Janet propose to improve performance using TC?

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

features of the product were attractive to the customer and how much customers were willing

to pay for each feature. Once a target price was determined, the firm had to take profit margin

away to arrive at a target cost. This cost was labelled the allowable cost which, usually,

would be lower than the current product costs within the firm. The firm then had to carry out

cost management activities and strategic realignment to bring the current product costs down

to the target cost (allowable cost) over a period of time.

Table 4 in Exhibit 1 sets out the pricing for Ride Cover if it was based on a target

costing approach. Current market research suggests that the average premium for a policy

would need to be set at an average of $1,200 (based on the current average premium actually

charged) to maintain current sales volumes and market share. Based on earning a profit

margin of 10%, the allowable cost of a policy would need to be set at $1,080 which would

require a 32.04% reduction from the current level of product costs. Cost management and

strategic realignment activities would need to be carried out to improve the costs of Ride

Cover.

The Target Cost approach focused the firm on all aspects of the revenue and costs of a

product and brought in a questioning attitude to all operational activities. Long used in

Japanese firms, Target Costing as a strategic approach to revenue and cost management had

been neglected in Western firms as it required management and cultural changes to enforce.

But, Janet felt it was a useful approach for Sunline to consider and began to gather

information to develop a paper on Target Costing. She began to consider some key issues:

what is the process of Target Costing and how can it be adapted for auto insurance products?

What are the changes to operational priorities and management processes required when

moving Sunline from a cost-plus pricing strategy to a strategic revenue and cost management

strategy such as TC? What key steps should Janet propose to improve performance using TC?

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Exhibit 1

Table 1: Quarterly Performance Summary ($M) – Sunline

Quarter 1 Quarter 2 Quarter 3 Quarter 4

Revenue 1.52 1.65 2.11 2.50

Cost 2.02 2.35 2.90 3.31

Profit/(Loss) (0.50) (0.70) (0.79) (0.81)

Table 2: Cost structure – Sunline (Quarter 4)

Amount ($) Percentage (%)

Administration:

Training 450,000 13.59

Insurance claims 785,952 23.74

Payroll (wages and commission) 1,055,885 31.90

Performance reporting 15,689 0.47

Sales and marketing:

Television and bill boards 713,100 21.54

Online and social media ads 267,990 8.10

Event representation 66,779 2.02

Technology:

IT equipment leases 27,121 0.82

Software subscriptions 19,150 0.58

Financing:

Net cost of finance function after

investment returns (150,000) (4.53)

Headquarters cost charge bank 58,584 1.77

Total costs 3,310,250 100.00

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

Exhibit 1

Table 1: Quarterly Performance Summary ($M) – Sunline

Quarter 1 Quarter 2 Quarter 3 Quarter 4

Revenue 1.52 1.65 2.11 2.50

Cost 2.02 2.35 2.90 3.31

Profit/(Loss) (0.50) (0.70) (0.79) (0.81)

Table 2: Cost structure – Sunline (Quarter 4)

Amount ($) Percentage (%)

Administration:

Training 450,000 13.59

Insurance claims 785,952 23.74

Payroll (wages and commission) 1,055,885 31.90

Performance reporting 15,689 0.47

Sales and marketing:

Television and bill boards 713,100 21.54

Online and social media ads 267,990 8.10

Event representation 66,779 2.02

Technology:

IT equipment leases 27,121 0.82

Software subscriptions 19,150 0.58

Financing:

Net cost of finance function after

investment returns (150,000) (4.53)

Headquarters cost charge bank 58,584 1.77

Total costs 3,310,250 100.00

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

9

Table 3: Ride Cover policy – cost-plus pricing (based on Quarter 4 financials)

Average quarterly sales volume (no. of policies) 2083

Average premium per policy (target) $1,589.17

Target average profit margin 10%

Cost-plus price $1,748.09

Average premium charged (market price) $1,200.00

Profit/(Loss) per policy ($389.17)

Table 4: Ride Cover – target costing (based on Quarter 4 financials)

Average quarterly sales volume (no. of policies) 2083

Average premium charged (market price) $1,200.00

Target average profit margin (%) 10%

Target profit margin ($) $120.00

Allowable cost ($) $1,080.00

Current cost ($) $1,589.17

Cost savings required ($) $509.17

Cost savings required (%) 32.04%

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

Powered by TCPDF (www.tcpdf.org)

Table 3: Ride Cover policy – cost-plus pricing (based on Quarter 4 financials)

Average quarterly sales volume (no. of policies) 2083

Average premium per policy (target) $1,589.17

Target average profit margin 10%

Cost-plus price $1,748.09

Average premium charged (market price) $1,200.00

Profit/(Loss) per policy ($389.17)

Table 4: Ride Cover – target costing (based on Quarter 4 financials)

Average quarterly sales volume (no. of policies) 2083

Average premium charged (market price) $1,200.00

Target average profit margin (%) 10%

Target profit margin ($) $120.00

Allowable cost ($) $1,080.00

Current cost ($) $1,589.17

Cost savings required ($) $509.17

Cost savings required (%) 32.04%

https://www.coursehero.com/file/21806254/Sunline-Auto-Insurance/

This study resource was

shared via CourseHero.com

Powered by TCPDF (www.tcpdf.org)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.