The Arbitrage Pricing Model and Capital

11 Pages2620 Words55 Views

Added on 2020-04-13

The Arbitrage Pricing Model and Capital

Added on 2020-04-13

ShareRelated Documents

Running Head: Financial StudiesMergers and Acquisition

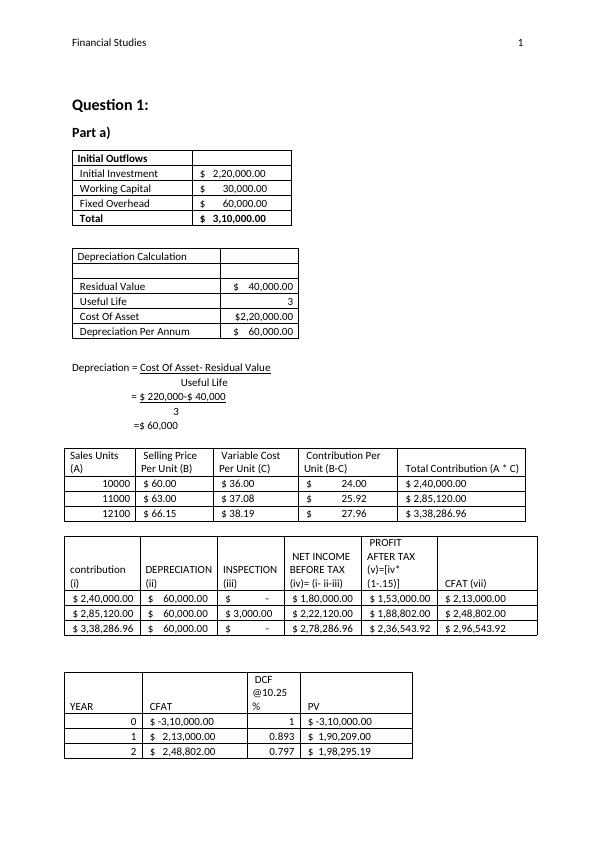

Financial Studies1Question 1:Part a)Initial Outflows Initial Investment $ 2,20,000.00 Working Capital $ 30,000.00 Fixed Overhead $ 60,000.00 Total $ 3,10,000.00 Depreciation Calculation Residual Value $ 40,000.00 Useful Life 3 Cost Of Asset $2,20,000.00 Depreciation Per Annum $ 60,000.00 Depreciation = Cost Of Asset- Residual Value Useful Life = $ 220,000-$ 40,000 3 =$ 60,000Sales Units(A) Selling Price Per Unit (B) Variable Cost Per Unit (C) Contribution Per Unit (B-C) Total Contribution (A * C)10000 $ 60.00 $ 36.00 $ 24.00 $ 2,40,000.00 11000 $ 63.00 $ 37.08 $ 25.92 $ 2,85,120.00 12100 $ 66.15 $ 38.19 $ 27.96 $ 3,38,286.96 contribution (i)DEPRECIATION(ii) INSPECTION(iii) NET INCOME BEFORE TAX (iv)= (i- ii-iii) PROFIT AFTER TAX (v)=[iv* (1-.15)]CFAT (vii) $ 2,40,000.00 $ 60,000.00 $ - $ 1,80,000.00 $ 1,53,000.00 $ 2,13,000.00 $ 2,85,120.00 $ 60,000.00 $ 3,000.00 $ 2,22,120.00 $ 1,88,802.00 $ 2,48,802.00 $ 3,38,286.96 $ 60,000.00 $ - $ 2,78,286.96 $ 2,36,543.92 $ 2,96,543.92 YEAR CFAT DCF @10.25% PV 0 $ -3,10,000.00 1 $ -3,10,000.00 1 $ 2,13,000.00 0.893 $ 1,90,209.00 2 $ 2,48,802.00 0.797 $ 1,98,295.19

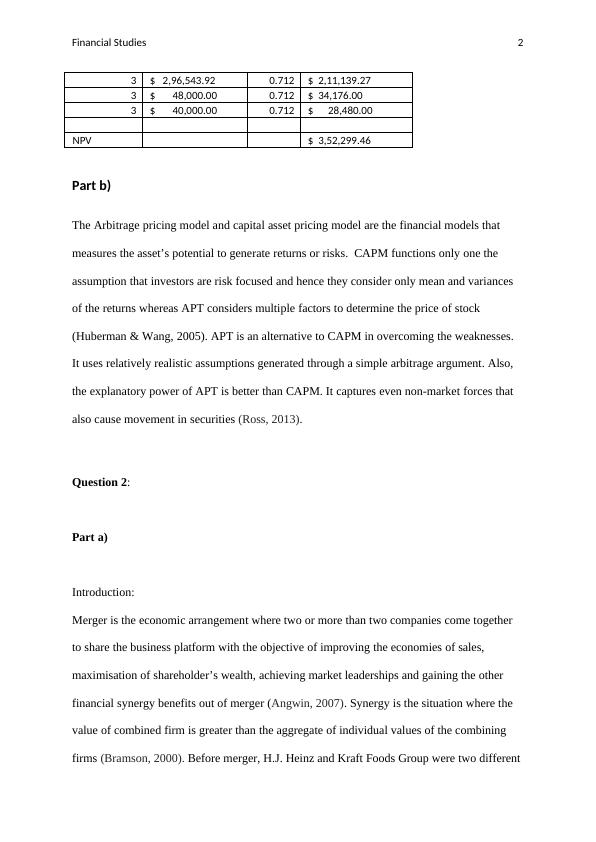

Financial Studies23 $ 2,96,543.92 0.712 $ 2,11,139.27 3 $ 48,000.00 0.712 $ 34,176.00 3 $ 40,000.00 0.712 $ 28,480.00 NPV $ 3,52,299.46 Part b)The Arbitrage pricing model and capital asset pricing model are the financial models that measures the asset’s potential to generate returns or risks. CAPM functions only one the assumption that investors are risk focused and hence they consider only mean and variances of the returns whereas APT considers multiple factors to determine the price of stock (Huberman & Wang, 2005). APT is an alternative to CAPM in overcoming the weaknesses. It uses relatively realistic assumptions generated through a simple arbitrage argument. Also, the explanatory power of APT is better than CAPM. It captures even non-market forces that also cause movement in securities (Ross, 2013). Question 2:Part a) Introduction:Merger is the economic arrangement where two or more than two companies come together to share the business platform with the objective of improving the economies of sales, maximisation of shareholder’s wealth, achieving market leaderships and gaining the other financial synergy benefits out of merger (Angwin, 2007). Synergy is the situation where the value of combined firm is greater than the aggregate of individual values of the combining firms (Bramson, 2000). Before merger, H.J. Heinz and Kraft Foods Group were two different

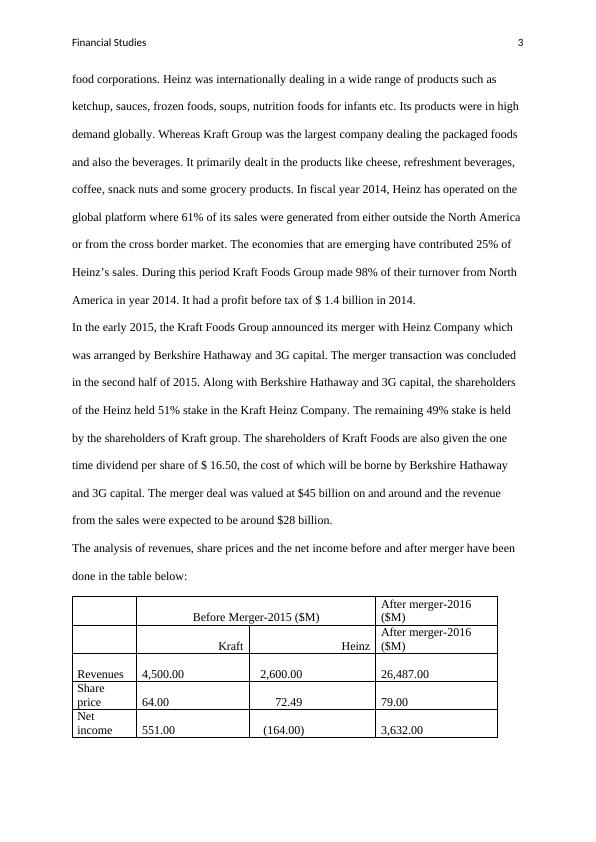

Financial Studies3food corporations. Heinz was internationally dealing in a wide range of products such as ketchup, sauces, frozen foods, soups, nutrition foods for infants etc. Its products were in high demand globally. Whereas Kraft Group was the largest company dealing the packaged foods and also the beverages. It primarily dealt in the products like cheese, refreshment beverages, coffee, snack nuts and some grocery products. In fiscal year 2014, Heinz has operated on the global platform where 61% of its sales were generated from either outside the North Americaor from the cross border market. The economies that are emerging have contributed 25% of Heinz’s sales. During this period Kraft Foods Group made 98% of their turnover from North America in year 2014. It had a profit before tax of $ 1.4 billion in 2014. In the early 2015, the Kraft Foods Group announced its merger with Heinz Company which was arranged by Berkshire Hathaway and 3G capital. The merger transaction was concluded in the second half of 2015. Along with Berkshire Hathaway and 3G capital, the shareholders of the Heinz held 51% stake in the Kraft Heinz Company. The remaining 49% stake is held by the shareholders of Kraft group. The shareholders of Kraft Foods are also given the one time dividend per share of $ 16.50, the cost of which will be borne by Berkshire Hathaway and 3G capital. The merger deal was valued at $45 billion on and around and the revenue from the sales were expected to be around $28 billion. The analysis of revenues, share prices and the net income before and after merger have been done in the table below:Before Merger-2015 ($M)After merger-2016 ($M)KraftHeinzAfter merger-2016 ($M)Revenues4,500.00 2,600.00 26,487.00 Share price64.00 72.49 79.00 Net income551.00 (164.00)3,632.00

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Corporate Financial Management Reportlg...

|10

|2161

|33