Financial Analysis Report: Aristocrat Leisure Limited (FINC300)

VerifiedAdded on 2023/06/07

|22

|4241

|139

Report

AI Summary

This report presents a detailed financial analysis of Aristocrat Leisure Limited (ALL), a leading global manufacturer of gambling machines. It begins with an introduction to the company, its operations, and its diverse product offerings, followed by a shareholder analysis categorizing investors and their investment philosophies. The report then assesses ALL's current market position, types of returns, and risk-return profile, including shareholder returns for FY2017 and business risks such as economic conditions, competition, and government regulations. Cost of capital is computed using the CAPM and Dividend Growth Model, with a WACC calculation, and the report concludes with a financial statement analysis, including market value-based measures, profitability ratios, and a DuPont analysis to assess ALL's financial health and performance.

ANALYSIS OF

ARISTOCRAT

LEISURE

LIMITED

ARISTOCRAT

LEISURE

LIMITED

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENT

Introduction of the company.....................................................................2

Purpose of Report....................................................................................2

Shareholder Analysis...............................................................................2

Position of the company...........................................................................5

Types of Returns Capital Growth Vs Dividends.......................................6

Risk Return Analysis.............................................................................7

(a)Shareholders return for FY 2017.......................................................7

(b)Business Risks..................................................................................9

(c)Review of Capital projects and Market Reaction.............................11

Cost of Capital........................................................................................12

Cost of Equity using Capital Asset Pricing Model (CAPM)..................12

Cost of Equity using Dividend Growth Model......................................13

CAPM Vs DGM....................................................................................14

Cost of Debt...........................................................................................14

Weighted Average Cost of Capital.........................................................15

Comments on WACC..........................................................................16

Financial Statement Analysis.................................................................16

(a)Market Value Based Measures.......................................................16

(b)Market Value of Equity to Book Value of Equity..............................17

(c)Economic Value Added...................................................................17

Profitability Ratios................................................................................18

Return On Equity.............................................................................18

Return on Assets of the Company....................................................18

Return on Capital Employedof the Company....................................19

DU Pont Analysis...................................................................................19

Introduction of the company.....................................................................2

Purpose of Report....................................................................................2

Shareholder Analysis...............................................................................2

Position of the company...........................................................................5

Types of Returns Capital Growth Vs Dividends.......................................6

Risk Return Analysis.............................................................................7

(a)Shareholders return for FY 2017.......................................................7

(b)Business Risks..................................................................................9

(c)Review of Capital projects and Market Reaction.............................11

Cost of Capital........................................................................................12

Cost of Equity using Capital Asset Pricing Model (CAPM)..................12

Cost of Equity using Dividend Growth Model......................................13

CAPM Vs DGM....................................................................................14

Cost of Debt...........................................................................................14

Weighted Average Cost of Capital.........................................................15

Comments on WACC..........................................................................16

Financial Statement Analysis.................................................................16

(a)Market Value Based Measures.......................................................16

(b)Market Value of Equity to Book Value of Equity..............................17

(c)Economic Value Added...................................................................17

Profitability Ratios................................................................................18

Return On Equity.............................................................................18

Return on Assets of the Company....................................................18

Return on Capital Employedof the Company....................................19

DU Pont Analysis...................................................................................19

ASSIGNMENT

ANALYSIS OF ARISTOCRAT LEISUREE LIMITED

Introduction of the company

Aristocrat Leisure Limited (ALL) is a company listed on Australian Stock

Exchange. The company has its headquarters in Sydney, Australia. The

company is a leading global manufacturer of gambling machines and

gaming solutions. ALL has its marketing offices in Australia, United

States of America, South Africa and Russia1.

The company has obtained license for operation in more than 200

countries and marks its presence globally in more than 90 countries.

ALL offers a wide array of product encompassing electronic machines

for gaming, casino management systems etc. The Group has further

diversified itself in Social gaming and real money wager markets. The

company has an official website2

Purpose of Report

The report has been prepared with the intention to analyse the

company, its future prospects, interest of the shareholders, present

financial performance, competition in the industry, risk return profile

etc.

Shareholder Analysis

Every investor has its own intention behind investing in stock market.

The same may encompass long term vision to short term vision. There

are various types of philosophies that guide investment in securities of

a company. These philosophies in turn are influence by age, risk

appetite, long term, short term, size of the company and prospects.

Generally investors are categorised under three categories:

1https://en.wikipedia.org/wiki/Aristocrat_Leisure

2www.aristocrat.com.

ANALYSIS OF ARISTOCRAT LEISUREE LIMITED

Introduction of the company

Aristocrat Leisure Limited (ALL) is a company listed on Australian Stock

Exchange. The company has its headquarters in Sydney, Australia. The

company is a leading global manufacturer of gambling machines and

gaming solutions. ALL has its marketing offices in Australia, United

States of America, South Africa and Russia1.

The company has obtained license for operation in more than 200

countries and marks its presence globally in more than 90 countries.

ALL offers a wide array of product encompassing electronic machines

for gaming, casino management systems etc. The Group has further

diversified itself in Social gaming and real money wager markets. The

company has an official website2

Purpose of Report

The report has been prepared with the intention to analyse the

company, its future prospects, interest of the shareholders, present

financial performance, competition in the industry, risk return profile

etc.

Shareholder Analysis

Every investor has its own intention behind investing in stock market.

The same may encompass long term vision to short term vision. There

are various types of philosophies that guide investment in securities of

a company. These philosophies in turn are influence by age, risk

appetite, long term, short term, size of the company and prospects.

Generally investors are categorised under three categories:

1https://en.wikipedia.org/wiki/Aristocrat_Leisure

2www.aristocrat.com.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

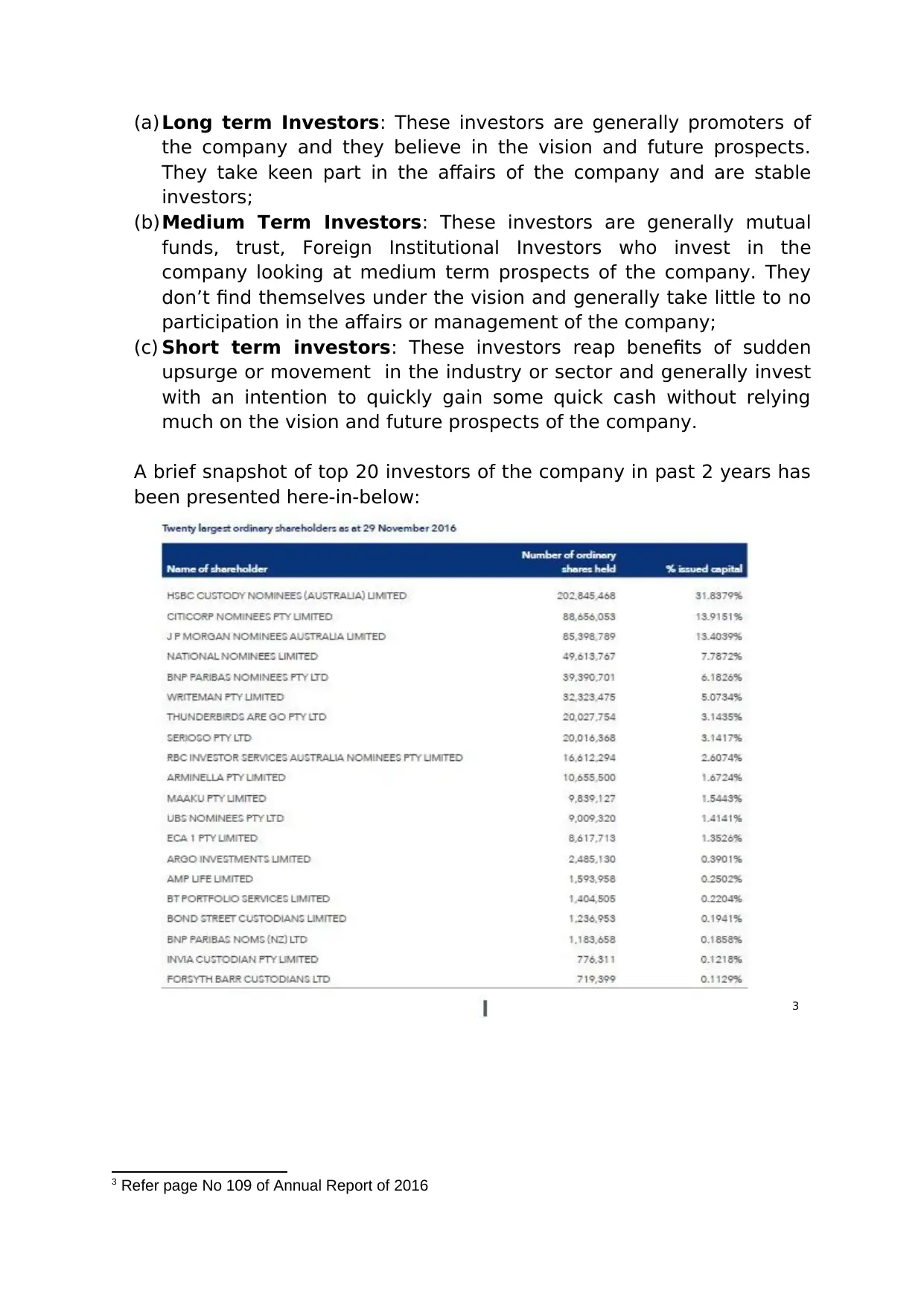

(a) Long term Investors: These investors are generally promoters of

the company and they believe in the vision and future prospects.

They take keen part in the affairs of the company and are stable

investors;

(b)Medium Term Investors: These investors are generally mutual

funds, trust, Foreign Institutional Investors who invest in the

company looking at medium term prospects of the company. They

don’t find themselves under the vision and generally take little to no

participation in the affairs or management of the company;

(c) Short term investors: These investors reap benefits of sudden

upsurge or movement in the industry or sector and generally invest

with an intention to quickly gain some quick cash without relying

much on the vision and future prospects of the company.

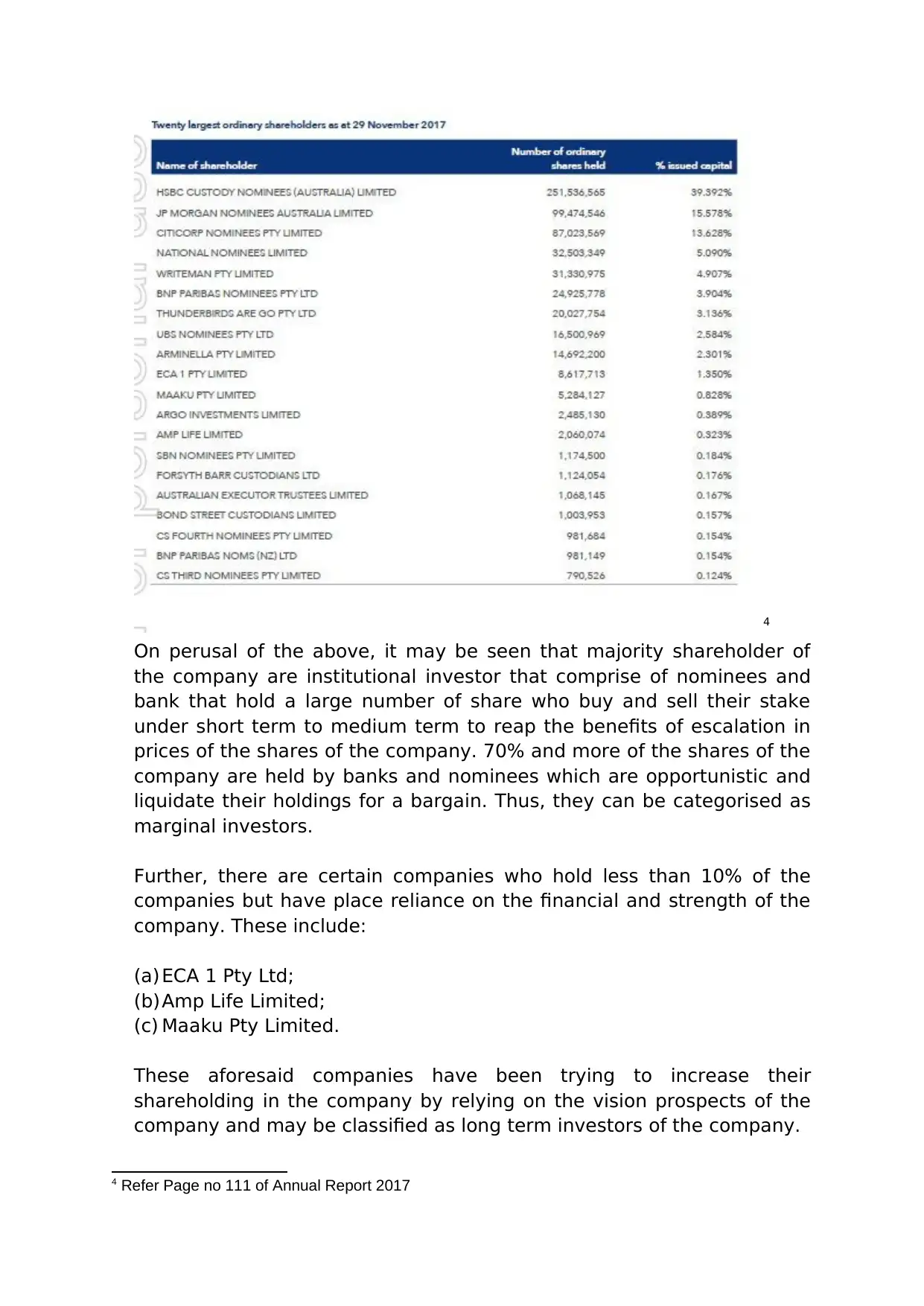

A brief snapshot of top 20 investors of the company in past 2 years has

been presented here-in-below:

3

3 Refer page No 109 of Annual Report of 2016

the company and they believe in the vision and future prospects.

They take keen part in the affairs of the company and are stable

investors;

(b)Medium Term Investors: These investors are generally mutual

funds, trust, Foreign Institutional Investors who invest in the

company looking at medium term prospects of the company. They

don’t find themselves under the vision and generally take little to no

participation in the affairs or management of the company;

(c) Short term investors: These investors reap benefits of sudden

upsurge or movement in the industry or sector and generally invest

with an intention to quickly gain some quick cash without relying

much on the vision and future prospects of the company.

A brief snapshot of top 20 investors of the company in past 2 years has

been presented here-in-below:

3

3 Refer page No 109 of Annual Report of 2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

On perusal of the above, it may be seen that majority shareholder of

the company are institutional investor that comprise of nominees and

bank that hold a large number of share who buy and sell their stake

under short term to medium term to reap the benefits of escalation in

prices of the shares of the company. 70% and more of the shares of the

company are held by banks and nominees which are opportunistic and

liquidate their holdings for a bargain. Thus, they can be categorised as

marginal investors.

Further, there are certain companies who hold less than 10% of the

companies but have place reliance on the financial and strength of the

company. These include:

(a) ECA 1 Pty Ltd;

(b)Amp Life Limited;

(c) Maaku Pty Limited.

These aforesaid companies have been trying to increase their

shareholding in the company by relying on the vision prospects of the

company and may be classified as long term investors of the company.

4 Refer Page no 111 of Annual Report 2017

On perusal of the above, it may be seen that majority shareholder of

the company are institutional investor that comprise of nominees and

bank that hold a large number of share who buy and sell their stake

under short term to medium term to reap the benefits of escalation in

prices of the shares of the company. 70% and more of the shares of the

company are held by banks and nominees which are opportunistic and

liquidate their holdings for a bargain. Thus, they can be categorised as

marginal investors.

Further, there are certain companies who hold less than 10% of the

companies but have place reliance on the financial and strength of the

company. These include:

(a) ECA 1 Pty Ltd;

(b)Amp Life Limited;

(c) Maaku Pty Limited.

These aforesaid companies have been trying to increase their

shareholding in the company by relying on the vision prospects of the

company and may be classified as long term investors of the company.

4 Refer Page no 111 of Annual Report 2017

Further Len Ainsworth who holds a substantial holding in the company

through custodian and other means is the promoter of the company and

is associated with the long term vision of the company.

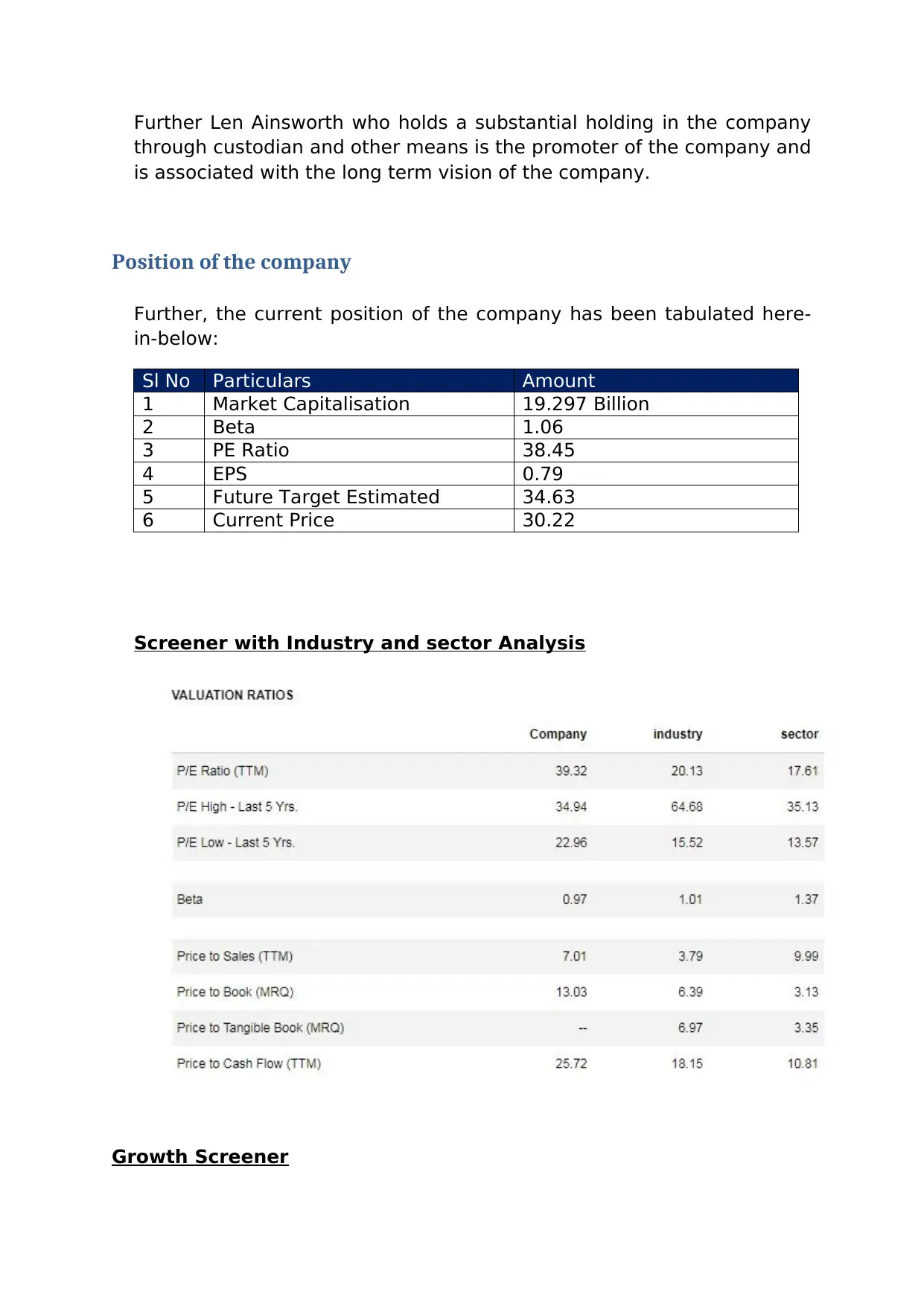

Position of the company

Further, the current position of the company has been tabulated here-

in-below:

Sl No Particulars Amount

1 Market Capitalisation 19.297 Billion

2 Beta 1.06

3 PE Ratio 38.45

4 EPS 0.79

5 Future Target Estimated 34.63

6 Current Price 30.22

Screener with Industry and sector Analysis

Growth Screener

through custodian and other means is the promoter of the company and

is associated with the long term vision of the company.

Position of the company

Further, the current position of the company has been tabulated here-

in-below:

Sl No Particulars Amount

1 Market Capitalisation 19.297 Billion

2 Beta 1.06

3 PE Ratio 38.45

4 EPS 0.79

5 Future Target Estimated 34.63

6 Current Price 30.22

Screener with Industry and sector Analysis

Growth Screener

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

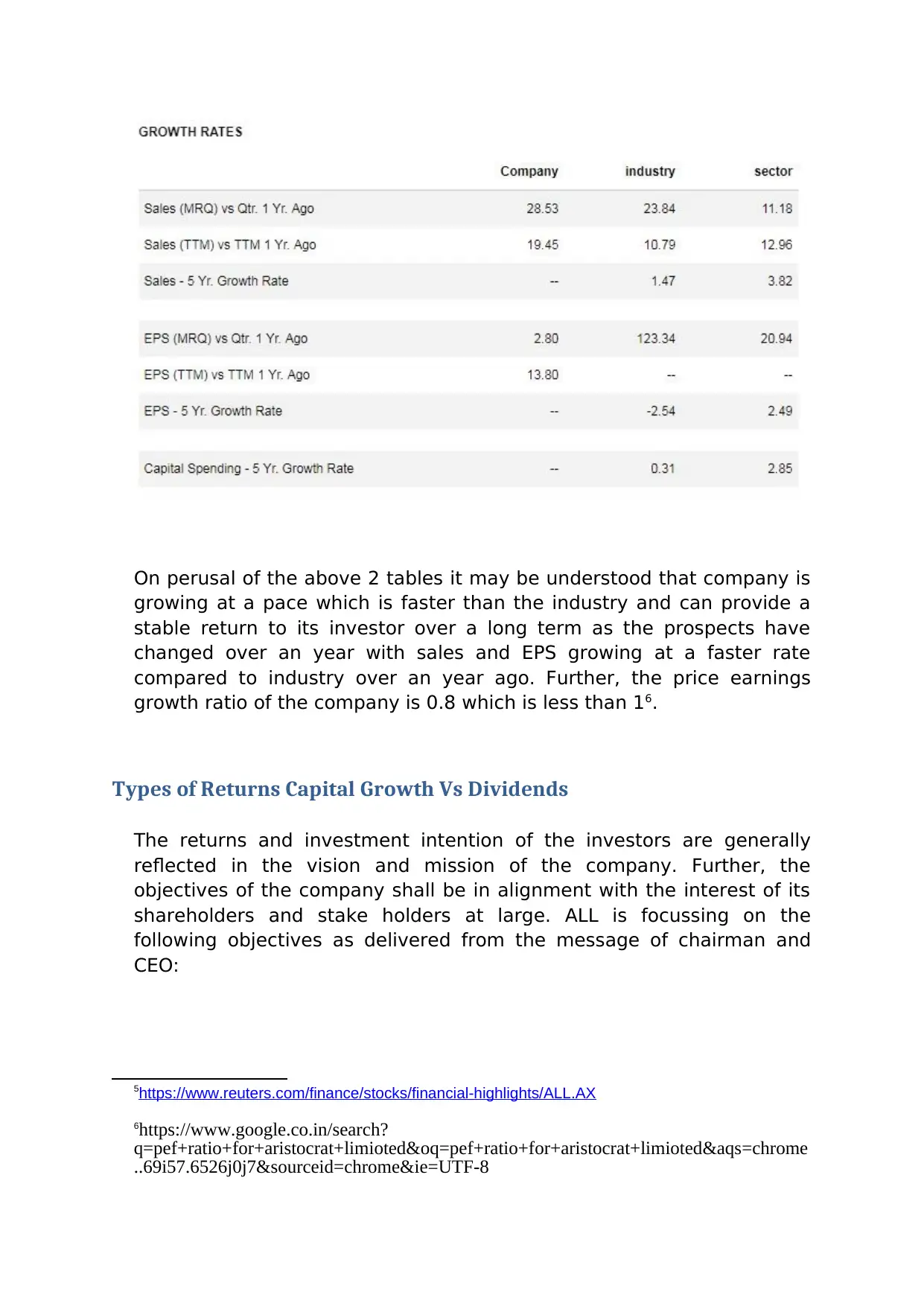

On perusal of the above 2 tables it may be understood that company is

growing at a pace which is faster than the industry and can provide a

stable return to its investor over a long term as the prospects have

changed over an year with sales and EPS growing at a faster rate

compared to industry over an year ago. Further, the price earnings

growth ratio of the company is 0.8 which is less than 16.

Types of Returns Capital Growth Vs Dividends

The returns and investment intention of the investors are generally

reflected in the vision and mission of the company. Further, the

objectives of the company shall be in alignment with the interest of its

shareholders and stake holders at large. ALL is focussing on the

following objectives as delivered from the message of chairman and

CEO:

5https://www.reuters.com/finance/stocks/financial-highlights/ALL.AX

6https://www.google.co.in/search?

q=pef+ratio+for+aristocrat+limioted&oq=pef+ratio+for+aristocrat+limioted&aqs=chrome

..69i57.6526j0j7&sourceid=chrome&ie=UTF-8

growing at a pace which is faster than the industry and can provide a

stable return to its investor over a long term as the prospects have

changed over an year with sales and EPS growing at a faster rate

compared to industry over an year ago. Further, the price earnings

growth ratio of the company is 0.8 which is less than 16.

Types of Returns Capital Growth Vs Dividends

The returns and investment intention of the investors are generally

reflected in the vision and mission of the company. Further, the

objectives of the company shall be in alignment with the interest of its

shareholders and stake holders at large. ALL is focussing on the

following objectives as delivered from the message of chairman and

CEO:

5https://www.reuters.com/finance/stocks/financial-highlights/ALL.AX

6https://www.google.co.in/search?

q=pef+ratio+for+aristocrat+limioted&oq=pef+ratio+for+aristocrat+limioted&aqs=chrome

..69i57.6526j0j7&sourceid=chrome&ie=UTF-8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(a) Digital strategy and growth which shall be in alignment with the

increase in revenue and growth of the company to further the

interest of shareholders;

(b)Foundations of recurring revenue growth;

(c) Acquisition of Social Games Plarium Global Limited for expansion,

proposed acquisition of Big Fish;

(d)Consistent increase in cash flow and cash earnings per share;

Thus, the above clearly highlights that shareholders of the company are

primarily more focussed on growth rather than dividend as many

acquisition are taking place and the company is exploring opportunities

to be number 1.

Risk Return Analysis

For the purpose of analysing the risk return of ALL, one needs to look at

the return earned by shareholders on their investment, business profile

and risk associated with the company and review of capital projects and

market reaction.

(a)Shareholders return for FY 2017

The return to shareholders can be computed as a summation of return

in the form of dividend to shareholders and return in the form of capital

appreciation. The same has been computed herein below:

(i) For computation of return in the form of dividend to shareholders,

one needs to look at the dividend paid by the company during the

Financial Year including both interim and final dividend. The total

dividend received by the shareholder in FY 2017-18 is 34 cents.

Further, the price of the share at the beginning of the financial year

stood at 22.5 dollar.

Thus, the return earned by shareholders as dividend equals to

(Dividend received during the year/ beginning share price) which is

(34/2250)*100= 1.51%

Further, the return earned by the shareholders in the form of capital

appreciation has been computed by using the value of the shares of the

company on 30-06-2018 i.e. 31.21 dollar and the value of the company

increase in revenue and growth of the company to further the

interest of shareholders;

(b)Foundations of recurring revenue growth;

(c) Acquisition of Social Games Plarium Global Limited for expansion,

proposed acquisition of Big Fish;

(d)Consistent increase in cash flow and cash earnings per share;

Thus, the above clearly highlights that shareholders of the company are

primarily more focussed on growth rather than dividend as many

acquisition are taking place and the company is exploring opportunities

to be number 1.

Risk Return Analysis

For the purpose of analysing the risk return of ALL, one needs to look at

the return earned by shareholders on their investment, business profile

and risk associated with the company and review of capital projects and

market reaction.

(a)Shareholders return for FY 2017

The return to shareholders can be computed as a summation of return

in the form of dividend to shareholders and return in the form of capital

appreciation. The same has been computed herein below:

(i) For computation of return in the form of dividend to shareholders,

one needs to look at the dividend paid by the company during the

Financial Year including both interim and final dividend. The total

dividend received by the shareholder in FY 2017-18 is 34 cents.

Further, the price of the share at the beginning of the financial year

stood at 22.5 dollar.

Thus, the return earned by shareholders as dividend equals to

(Dividend received during the year/ beginning share price) which is

(34/2250)*100= 1.51%

Further, the return earned by the shareholders in the form of capital

appreciation has been computed by using the value of the shares of the

company on 30-06-2018 i.e. 31.21 dollar and the value of the company

at the beginning of the Financial Year i.e. 22.5 dollar. Thus the capital

increment during the year is (31.21/22.5-1)*100= 38.71%.

Thus, the overall return earned by investors during the financial year

stood at 40.22% which is substantially good. Thus, the stock is more of

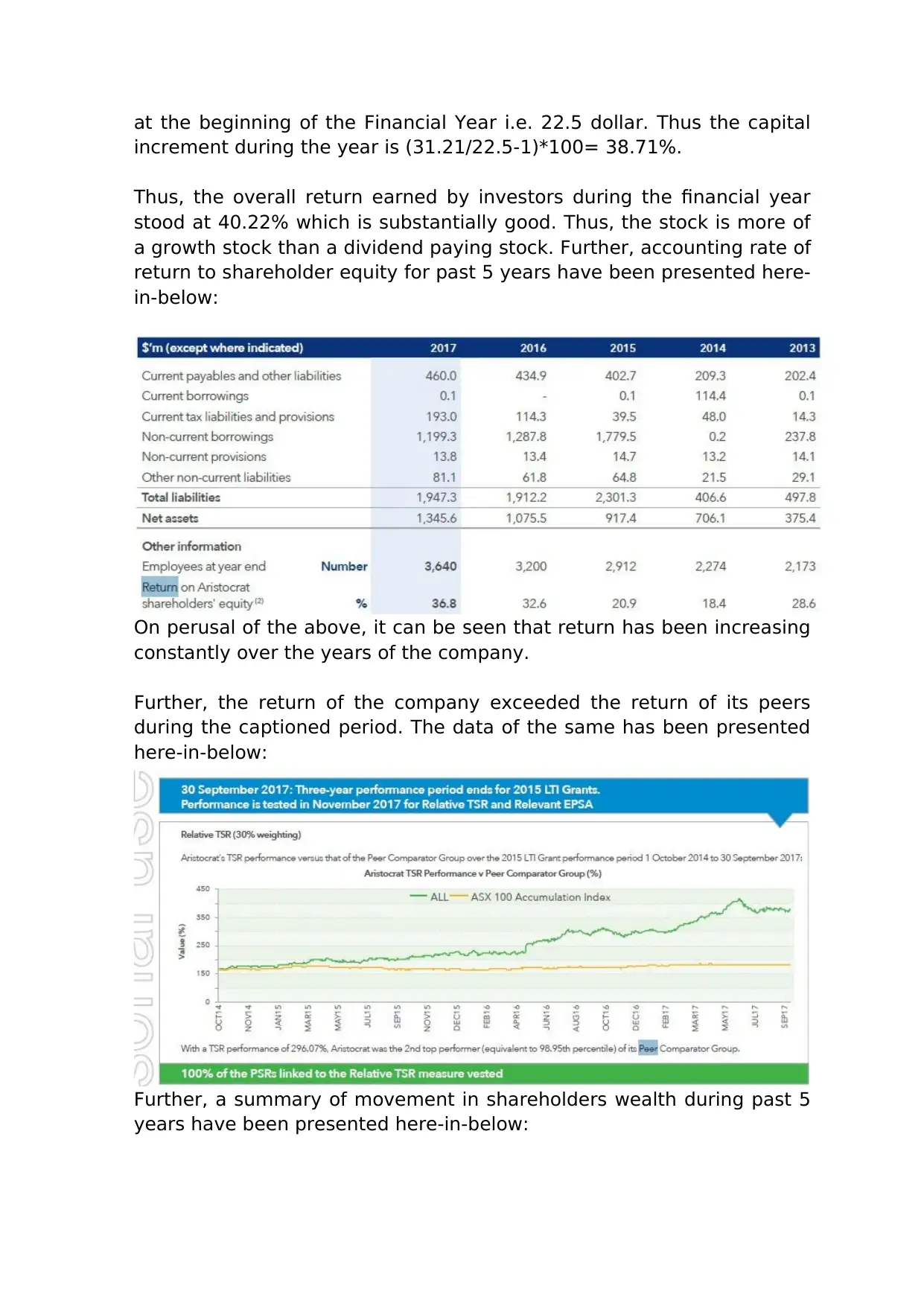

a growth stock than a dividend paying stock. Further, accounting rate of

return to shareholder equity for past 5 years have been presented here-

in-below:

On perusal of the above, it can be seen that return has been increasing

constantly over the years of the company.

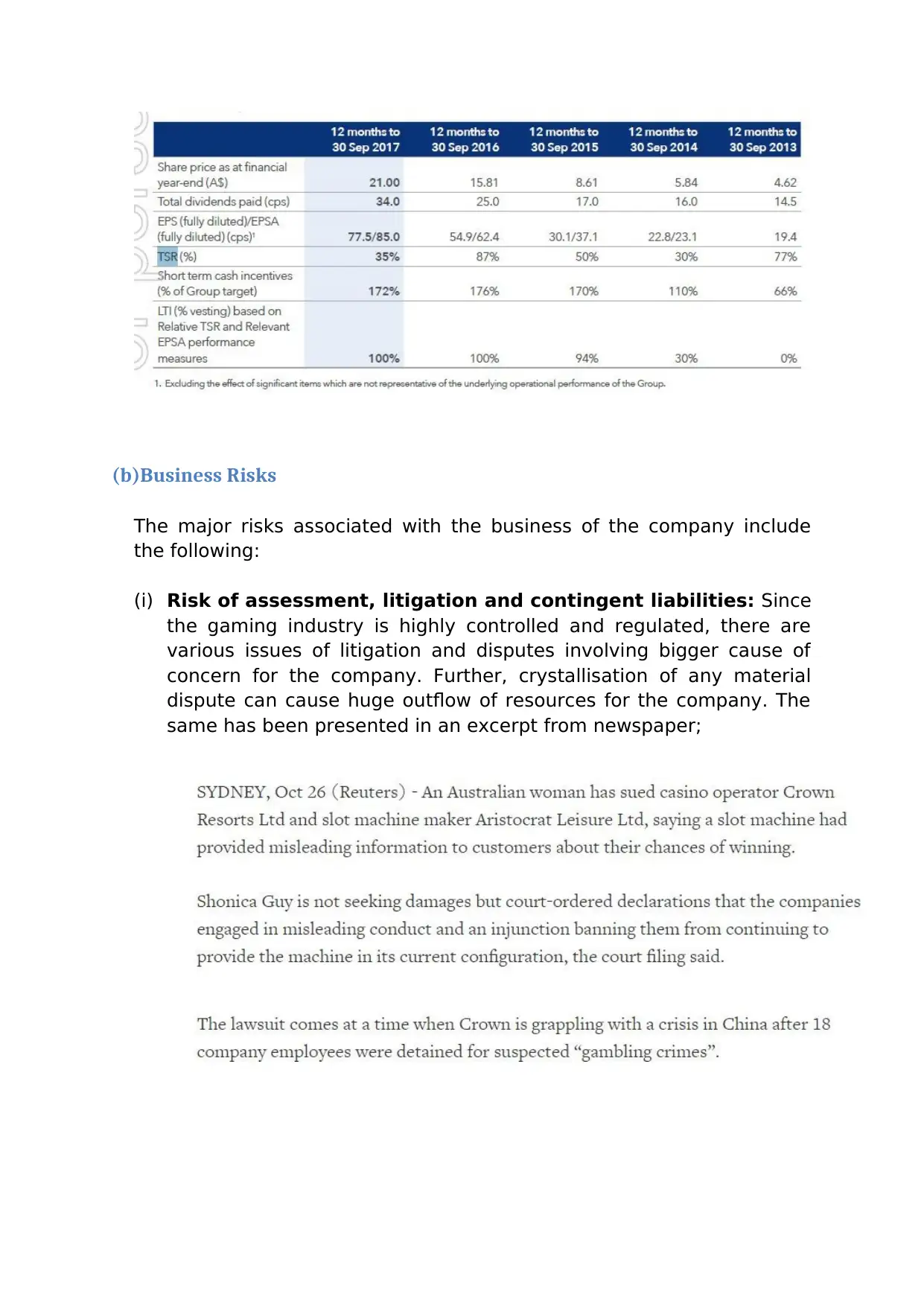

Further, the return of the company exceeded the return of its peers

during the captioned period. The data of the same has been presented

here-in-below:

Further, a summary of movement in shareholders wealth during past 5

years have been presented here-in-below:

increment during the year is (31.21/22.5-1)*100= 38.71%.

Thus, the overall return earned by investors during the financial year

stood at 40.22% which is substantially good. Thus, the stock is more of

a growth stock than a dividend paying stock. Further, accounting rate of

return to shareholder equity for past 5 years have been presented here-

in-below:

On perusal of the above, it can be seen that return has been increasing

constantly over the years of the company.

Further, the return of the company exceeded the return of its peers

during the captioned period. The data of the same has been presented

here-in-below:

Further, a summary of movement in shareholders wealth during past 5

years have been presented here-in-below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(b)Business Risks

The major risks associated with the business of the company include

the following:

(i) Risk of assessment, litigation and contingent liabilities: Since

the gaming industry is highly controlled and regulated, there are

various issues of litigation and disputes involving bigger cause of

concern for the company. Further, crystallisation of any material

dispute can cause huge outflow of resources for the company. The

same has been presented in an excerpt from newspaper;

The major risks associated with the business of the company include

the following:

(i) Risk of assessment, litigation and contingent liabilities: Since

the gaming industry is highly controlled and regulated, there are

various issues of litigation and disputes involving bigger cause of

concern for the company. Further, crystallisation of any material

dispute can cause huge outflow of resources for the company. The

same has been presented in an excerpt from newspaper;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(ii) Change in economic conditions and other allied factors

affecting the gaming industry:

The demand for products and services in a gaming industry are

highly dependent on market conditions, personal disposable income

of gamers, their gaming preferences and social upbringing etc.

Since the expenditure on gaming is discretionary the same can fall

without any control of the group. Thus, the economic outlook has a

huge impact on the business of ALL.

(iii) Gaming Competition: The ever increasing competition in

the gaming industry both land based and online has a huge impact

of profitability of the company. Further, the competition has

increased with entry of new customers. The critical factors to

survival include innovation, pricing and reliability. Further, the group

shall explore other segments mostly digital for continuous growth

otherwise the business shall stabilise and revenue will fall. The same

is evident by various acquisitions of the companies in the recent

years.

(iv) Government Gaming Regulation: The entire gaming

industry has been subject to huge regulations imposed by

government of respective countries. Significant expenditure is

incurred towards complying these regulations which include

obtaining license, permits, finding suitability of location,

documentations, major shareholders, key employees etc. Any

affecting the gaming industry:

The demand for products and services in a gaming industry are

highly dependent on market conditions, personal disposable income

of gamers, their gaming preferences and social upbringing etc.

Since the expenditure on gaming is discretionary the same can fall

without any control of the group. Thus, the economic outlook has a

huge impact on the business of ALL.

(iii) Gaming Competition: The ever increasing competition in

the gaming industry both land based and online has a huge impact

of profitability of the company. Further, the competition has

increased with entry of new customers. The critical factors to

survival include innovation, pricing and reliability. Further, the group

shall explore other segments mostly digital for continuous growth

otherwise the business shall stabilise and revenue will fall. The same

is evident by various acquisitions of the companies in the recent

years.

(iv) Government Gaming Regulation: The entire gaming

industry has been subject to huge regulations imposed by

government of respective countries. Significant expenditure is

incurred towards complying these regulations which include

obtaining license, permits, finding suitability of location,

documentations, major shareholders, key employees etc. Any

change in these regulations can impact the profitability of the

company as a whole.

(v) Cyber risk and Privacy regulation: Integrity and privacy of data

is crucial under gaming market on account of various laws and

regulation relating to privacy. Further, any breach of data can

impact significantly as the business of company is evolving digitally

over time.

(vi) Tax: It is one of major concern for the company as huge tax is

imposed on gaming businesses. Any change in tax requirements of

the company can impact its profitability and return to its

shareholder. Further, a different interpretation to law can have a

suit or law crystallised against the company and can result in

material outflow.

In short, company is surrounded with risk most associated with

technology and regulation. Thus, the company is trying to establish a

robust mechanism to manage the same.

(c)Review of Capital projects and Market Reaction

The company made a major announcement during the fiscal year in

October regarding acquisition of Social games business Plarium Global

Limited. The impact of the same has been shown in the graph in the

form of price movement:

7Yahoo.finance.com

company as a whole.

(v) Cyber risk and Privacy regulation: Integrity and privacy of data

is crucial under gaming market on account of various laws and

regulation relating to privacy. Further, any breach of data can

impact significantly as the business of company is evolving digitally

over time.

(vi) Tax: It is one of major concern for the company as huge tax is

imposed on gaming businesses. Any change in tax requirements of

the company can impact its profitability and return to its

shareholder. Further, a different interpretation to law can have a

suit or law crystallised against the company and can result in

material outflow.

In short, company is surrounded with risk most associated with

technology and regulation. Thus, the company is trying to establish a

robust mechanism to manage the same.

(c)Review of Capital projects and Market Reaction

The company made a major announcement during the fiscal year in

October regarding acquisition of Social games business Plarium Global

Limited. The impact of the same has been shown in the graph in the

form of price movement:

7Yahoo.finance.com

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.