Financial Management: Project Evaluation and Company Analysis

VerifiedAdded on 2019/09/16

|17

|3841

|401

Homework Assignment

AI Summary

This assignment presents a comprehensive analysis of financial management principles. It begins with a project evaluation, comparing two potential investments (Project A and Project B) using the Weighted Average Cost of Capital (WACC), payback period, and Net Present Value (NPV) methods. The analysis includes calculations for annual cash flows, discounted cash flows, and a sensitivity analysis considering best and worst-case scenarios. The assignment then shifts to a financial statement analysis of Marks and Spencer Plc, utilizing ratio analysis to assess profitability, liquidity, capital structure, and efficiency over two years (2015 and 2014). The report interprets these ratios, highlighting trends and providing insights into the company's financial health. Finally, the assignment addresses the needs of various stakeholders (suppliers, customers, and shareholders) and how they perceive the company's performance, followed by a discussion on the importance of ratio analysis as a financial tool.

ARUMBAFM003

Financial Management

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

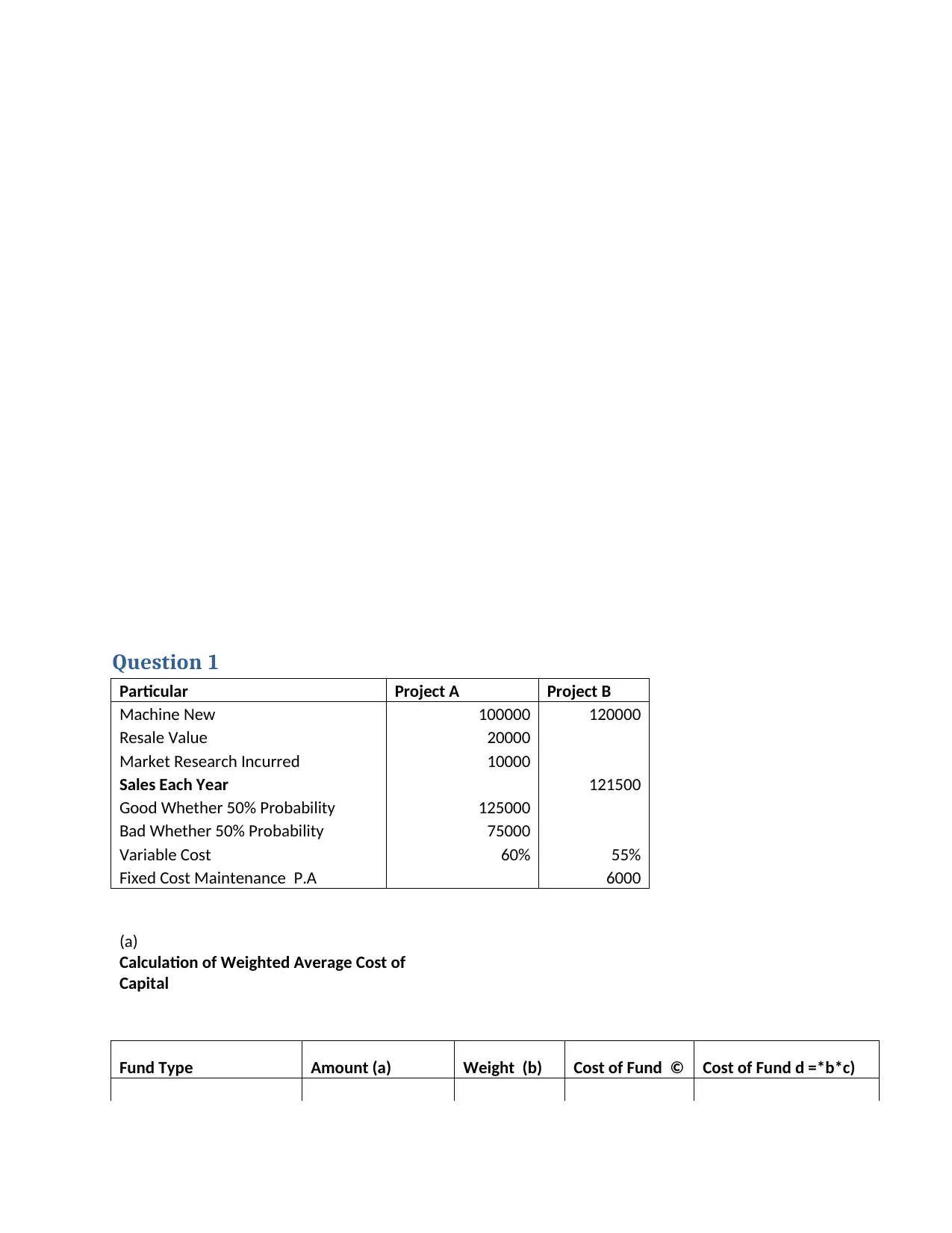

Question 1

Particular Project A Project B

Machine New 100000 120000

Resale Value 20000

Market Research Incurred 10000

Sales Each Year 121500

Good Whether 50% Probability 125000

Bad Whether 50% Probability 75000

Variable Cost 60% 55%

Fixed Cost Maintenance P.A 6000

(a)

Calculation of Weighted Average Cost of

Capital

Fund Type Amount (a) Weight (b) Cost of Fund © Cost of Fund d =*b*c)

Particular Project A Project B

Machine New 100000 120000

Resale Value 20000

Market Research Incurred 10000

Sales Each Year 121500

Good Whether 50% Probability 125000

Bad Whether 50% Probability 75000

Variable Cost 60% 55%

Fixed Cost Maintenance P.A 6000

(a)

Calculation of Weighted Average Cost of

Capital

Fund Type Amount (a) Weight (b) Cost of Fund © Cost of Fund d =*b*c)

Equity 8000000 0.8 7 5.6

Debt 2000000 0.2 12 2.4

Total 10000000 1 8

The weighting average cost of capital is 8%

(b)

Payback Period for each Project

Calculation of Annual Cash flow for each Project

particular Project A Project B

Sales 100000 121500

Less

Variable Cost 60000 66825

Annual Maintainance Cost 6000

Annual Cash Inflow for 5 Year 40000 48675

Paybck Period = ( Zero Year Outflow/ Annual Cash Flow)

Cost of Machinery 100000 121500

Payback Period In year 2.500 2.496

© Calculation for Net Present Value for Each Project

Particular Project A Project B

Debt 2000000 0.2 12 2.4

Total 10000000 1 8

The weighting average cost of capital is 8%

(b)

Payback Period for each Project

Calculation of Annual Cash flow for each Project

particular Project A Project B

Sales 100000 121500

Less

Variable Cost 60000 66825

Annual Maintainance Cost 6000

Annual Cash Inflow for 5 Year 40000 48675

Paybck Period = ( Zero Year Outflow/ Annual Cash Flow)

Cost of Machinery 100000 121500

Payback Period In year 2.500 2.496

© Calculation for Net Present Value for Each Project

Particular Project A Project B

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

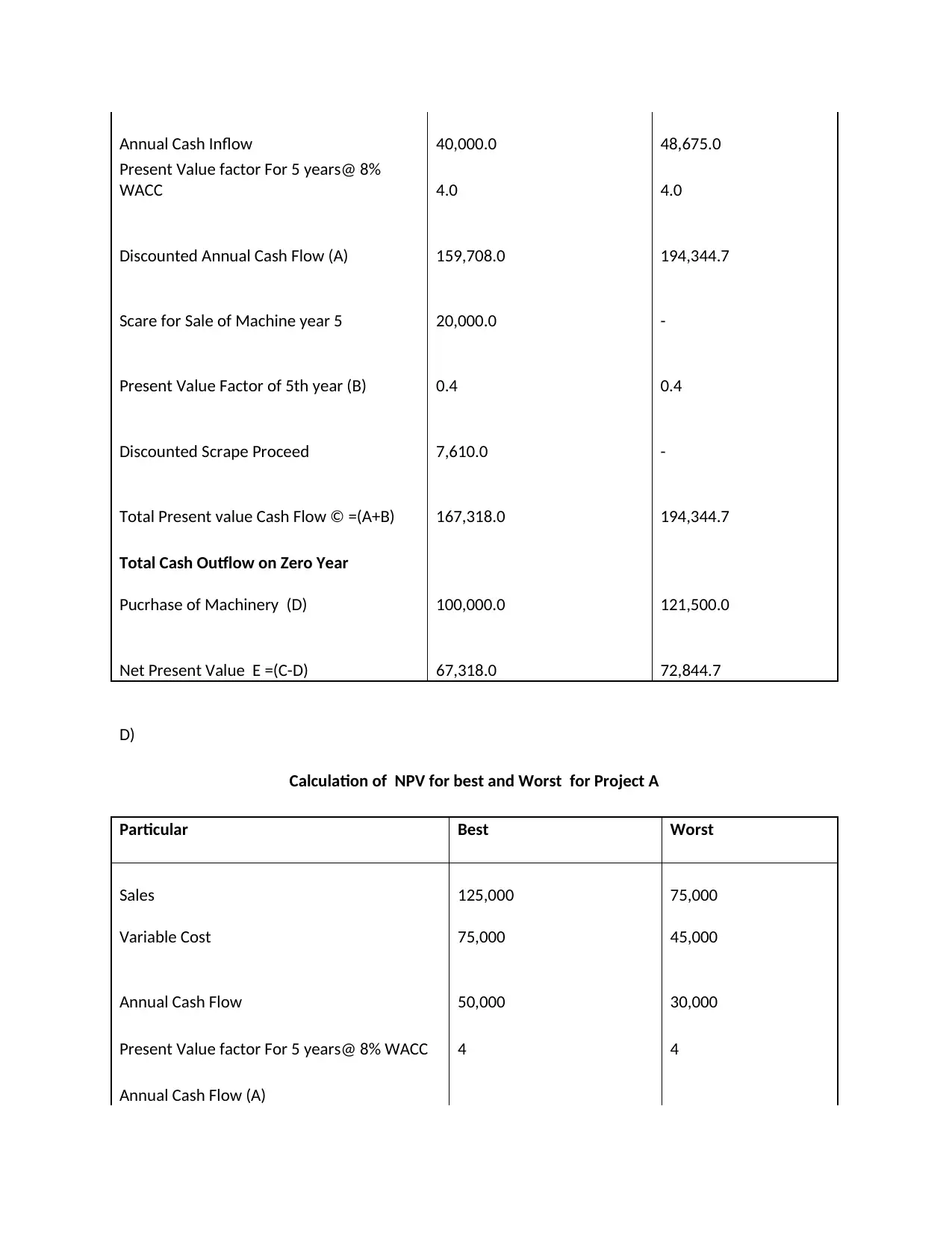

Annual Cash Inflow 40,000.0 48,675.0

Present Value factor For 5 years@ 8%

WACC 4.0 4.0

Discounted Annual Cash Flow (A) 159,708.0 194,344.7

Scare for Sale of Machine year 5 20,000.0 -

Present Value Factor of 5th year (B) 0.4 0.4

Discounted Scrape Proceed 7,610.0 -

Total Present value Cash Flow © =(A+B) 167,318.0 194,344.7

Total Cash Outflow on Zero Year

Pucrhase of Machinery (D) 100,000.0 121,500.0

Net Present Value E =(C-D) 67,318.0 72,844.7

D)

Calculation of NPV for best and Worst for Project A

Particular Best Worst

Sales 125,000 75,000

Variable Cost 75,000 45,000

Annual Cash Flow 50,000 30,000

Present Value factor For 5 years@ 8% WACC 4 4

Annual Cash Flow (A)

Present Value factor For 5 years@ 8%

WACC 4.0 4.0

Discounted Annual Cash Flow (A) 159,708.0 194,344.7

Scare for Sale of Machine year 5 20,000.0 -

Present Value Factor of 5th year (B) 0.4 0.4

Discounted Scrape Proceed 7,610.0 -

Total Present value Cash Flow © =(A+B) 167,318.0 194,344.7

Total Cash Outflow on Zero Year

Pucrhase of Machinery (D) 100,000.0 121,500.0

Net Present Value E =(C-D) 67,318.0 72,844.7

D)

Calculation of NPV for best and Worst for Project A

Particular Best Worst

Sales 125,000 75,000

Variable Cost 75,000 45,000

Annual Cash Flow 50,000 30,000

Present Value factor For 5 years@ 8% WACC 4 4

Annual Cash Flow (A)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

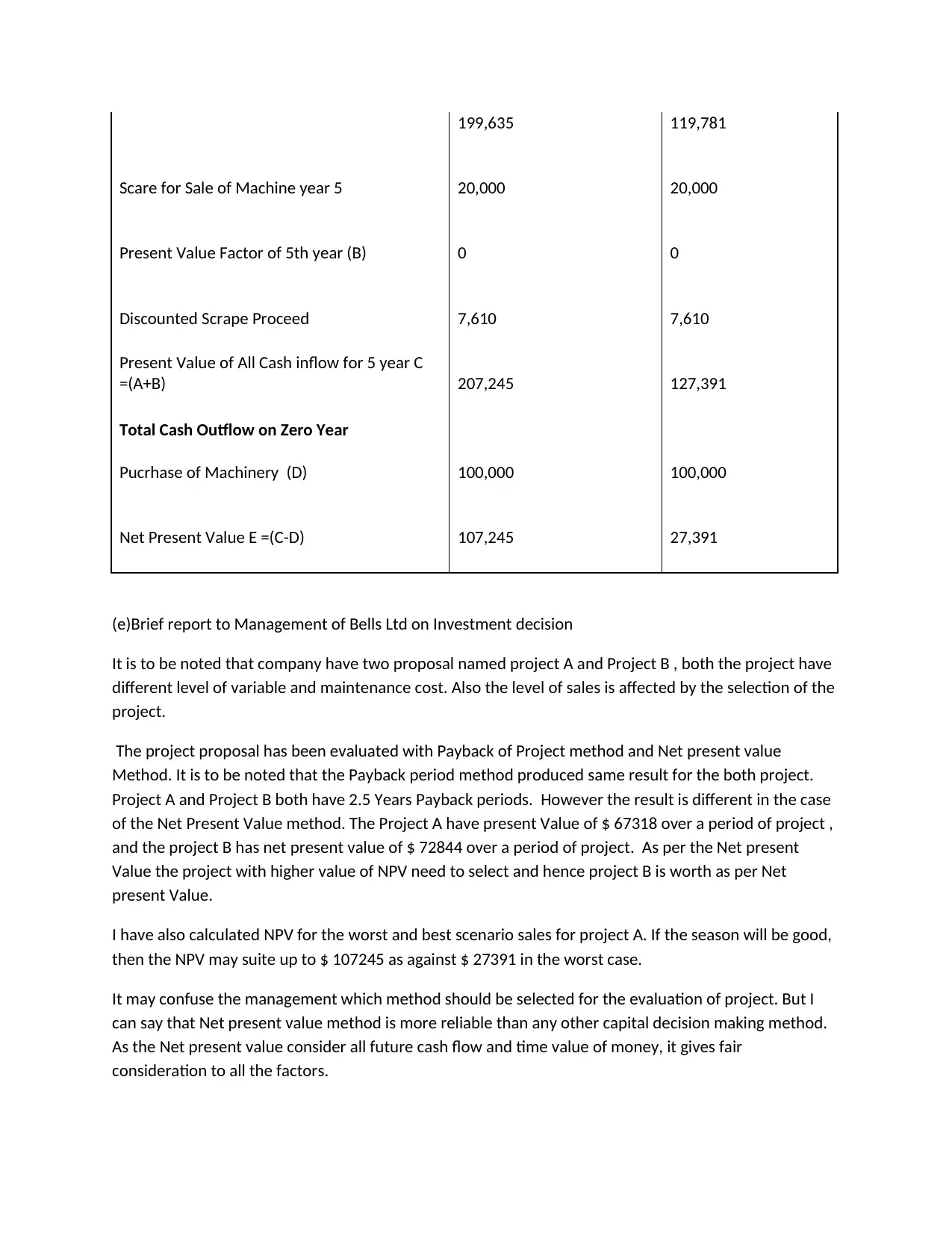

199,635 119,781

Scare for Sale of Machine year 5 20,000 20,000

Present Value Factor of 5th year (B) 0 0

Discounted Scrape Proceed 7,610 7,610

Present Value of All Cash inflow for 5 year C

=(A+B) 207,245 127,391

Total Cash Outflow on Zero Year

Pucrhase of Machinery (D) 100,000 100,000

Net Present Value E =(C-D) 107,245 27,391

(e)Brief report to Management of Bells Ltd on Investment decision

It is to be noted that company have two proposal named project A and Project B , both the project have

different level of variable and maintenance cost. Also the level of sales is affected by the selection of the

project.

The project proposal has been evaluated with Payback of Project method and Net present value

Method. It is to be noted that the Payback period method produced same result for the both project.

Project A and Project B both have 2.5 Years Payback periods. However the result is different in the case

of the Net Present Value method. The Project A have present Value of $ 67318 over a period of project ,

and the project B has net present value of $ 72844 over a period of project. As per the Net present

Value the project with higher value of NPV need to select and hence project B is worth as per Net

present Value.

I have also calculated NPV for the worst and best scenario sales for project A. If the season will be good,

then the NPV may suite up to $ 107245 as against $ 27391 in the worst case.

It may confuse the management which method should be selected for the evaluation of project. But I

can say that Net present value method is more reliable than any other capital decision making method.

As the Net present value consider all future cash flow and time value of money, it gives fair

consideration to all the factors.

Scare for Sale of Machine year 5 20,000 20,000

Present Value Factor of 5th year (B) 0 0

Discounted Scrape Proceed 7,610 7,610

Present Value of All Cash inflow for 5 year C

=(A+B) 207,245 127,391

Total Cash Outflow on Zero Year

Pucrhase of Machinery (D) 100,000 100,000

Net Present Value E =(C-D) 107,245 27,391

(e)Brief report to Management of Bells Ltd on Investment decision

It is to be noted that company have two proposal named project A and Project B , both the project have

different level of variable and maintenance cost. Also the level of sales is affected by the selection of the

project.

The project proposal has been evaluated with Payback of Project method and Net present value

Method. It is to be noted that the Payback period method produced same result for the both project.

Project A and Project B both have 2.5 Years Payback periods. However the result is different in the case

of the Net Present Value method. The Project A have present Value of $ 67318 over a period of project ,

and the project B has net present value of $ 72844 over a period of project. As per the Net present

Value the project with higher value of NPV need to select and hence project B is worth as per Net

present Value.

I have also calculated NPV for the worst and best scenario sales for project A. If the season will be good,

then the NPV may suite up to $ 107245 as against $ 27391 in the worst case.

It may confuse the management which method should be selected for the evaluation of project. But I

can say that Net present value method is more reliable than any other capital decision making method.

As the Net present value consider all future cash flow and time value of money, it gives fair

consideration to all the factors.

It is to be noted that as per the calculation made in later part Project B should be accepted , however if

the management want to take risk for higher return than they can even for project A , assuming the

season will be good.

(f)

It is to be noted that that when any company or organization invest in any project they invest their

liquidity in the project , Now is very obvious that the possession of cash in present is more worth then

in future. The amount invested in the project is not fetching the interest that might have received if

given to bank. And hence the time value of money concept takes into consideration the very

fundamental and logical fact the value of money invested today has more worth that the future cash

flow.

The above concept helps the decision maker to discount all the future cash flow as on today by applying

the appropriate discounting rate. Such discounted rate takes into consideration the forgone benefit on

the money invested in the project. And hence we can say that time value of money is very much

important to take into consideration in the investment appraisal .

Answer 2

(a)

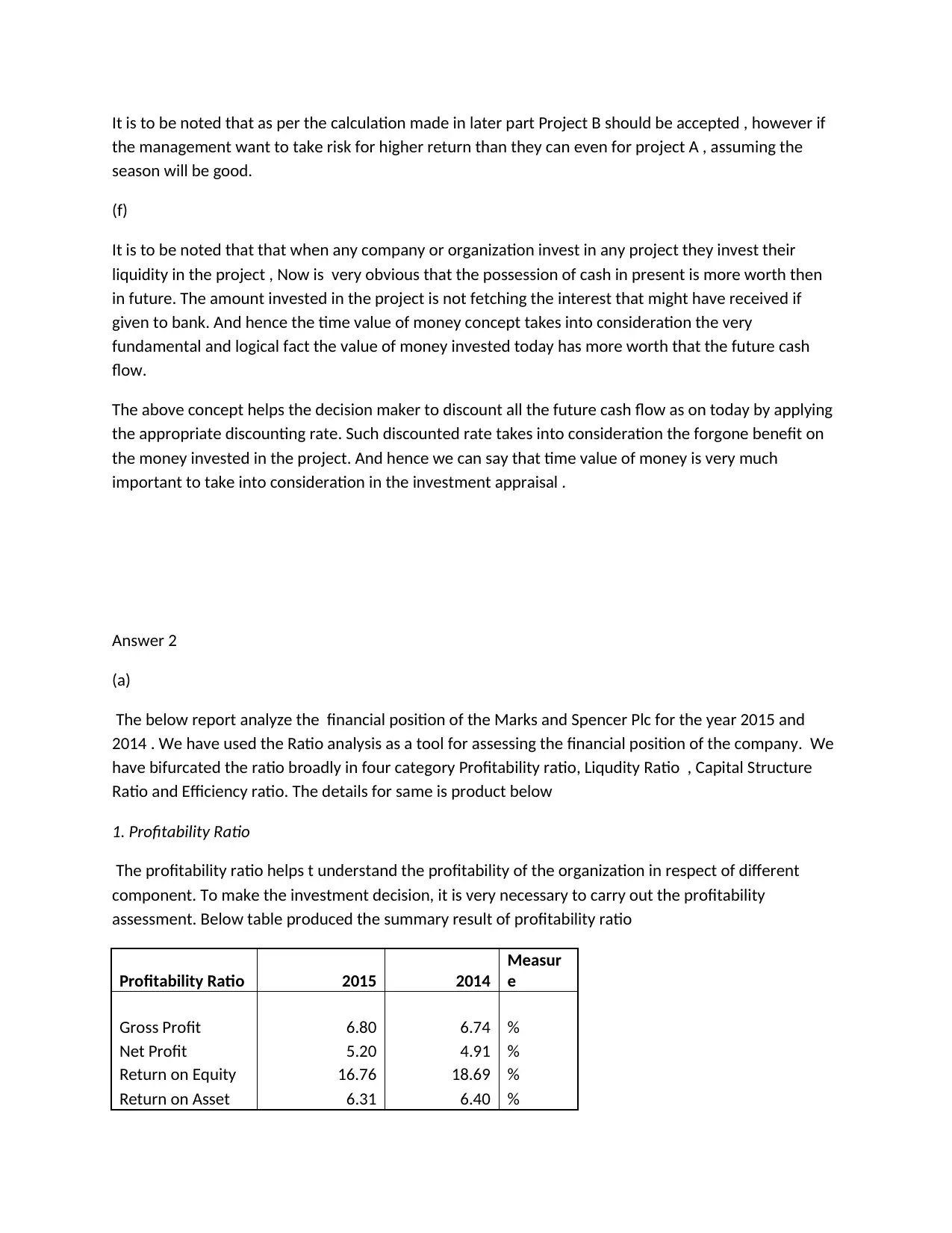

The below report analyze the financial position of the Marks and Spencer Plc for the year 2015 and

2014 . We have used the Ratio analysis as a tool for assessing the financial position of the company. We

have bifurcated the ratio broadly in four category Profitability ratio, Liqudity Ratio , Capital Structure

Ratio and Efficiency ratio. The details for same is product below

1. Profitability Ratio

The profitability ratio helps t understand the profitability of the organization in respect of different

component. To make the investment decision, it is very necessary to carry out the profitability

assessment. Below table produced the summary result of profitability ratio

Profitability Ratio 2015 2014

Measur

e

Gross Profit 6.80 6.74 %

Net Profit 5.20 4.91 %

Return on Equity 16.76 18.69 %

Return on Asset 6.31 6.40 %

the management want to take risk for higher return than they can even for project A , assuming the

season will be good.

(f)

It is to be noted that that when any company or organization invest in any project they invest their

liquidity in the project , Now is very obvious that the possession of cash in present is more worth then

in future. The amount invested in the project is not fetching the interest that might have received if

given to bank. And hence the time value of money concept takes into consideration the very

fundamental and logical fact the value of money invested today has more worth that the future cash

flow.

The above concept helps the decision maker to discount all the future cash flow as on today by applying

the appropriate discounting rate. Such discounted rate takes into consideration the forgone benefit on

the money invested in the project. And hence we can say that time value of money is very much

important to take into consideration in the investment appraisal .

Answer 2

(a)

The below report analyze the financial position of the Marks and Spencer Plc for the year 2015 and

2014 . We have used the Ratio analysis as a tool for assessing the financial position of the company. We

have bifurcated the ratio broadly in four category Profitability ratio, Liqudity Ratio , Capital Structure

Ratio and Efficiency ratio. The details for same is product below

1. Profitability Ratio

The profitability ratio helps t understand the profitability of the organization in respect of different

component. To make the investment decision, it is very necessary to carry out the profitability

assessment. Below table produced the summary result of profitability ratio

Profitability Ratio 2015 2014

Measur

e

Gross Profit 6.80 6.74 %

Net Profit 5.20 4.91 %

Return on Equity 16.76 18.69 %

Return on Asset 6.31 6.40 %

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Data Interpretation on Profitability Ratios

The Gross profit ration of the company for the year 2015 and 2014 is 6.80% and 6.74% respectively. We

can say that there is not major change in gross profitability of the company. However if we check the

result Net Profit ratio , the same has shown upward trend in the year 2015. The net profit ratio in the

year 2015 is 5.2% as against 4.91% in the year 2014. We can say that company has exercised good

control over the administrative and other general cost. The reason for increase in profit is reduction in

the Finance cost. On the other return on equity has shown the downward trend in the year 2015. The

ratio of Return on equity in the year 2015 was 18.69% as against 16.76% in the year 2014. It should be

noted that though the profit for the year 2015 is increased , the return on equity decreased due to

increased in the shareholder’s fund in the year 2015. On the other had the ratio return on asset also

showed slight decrease in the year of 2015 which us 6.31% as against 6.4% in the year 2014. The ratio is

decreased due to increase in the total asset of the company in the year 2015 in comparison to the year

2014.

2.

Liquidity Ratio

We have take two ratio to represent the liquidity position of the company named Current ratio and

Quick ratio. The same is presented in below table for the year 2015 and 2014

Liquidity ratio 2015.00 2014.00 Measure

Current Ratio 0.69 0.58 Times

Quick Ratio 0.31 0.22 Times

Data interpretation

The current ratio below 1 times indicate that company cannot pay its current liability with its current

asset if requires to be paid as on day. In the current case of Marks and Spencer Plc the same is below 1

times for both years. In the year 2014 the ratio was 0.58 and in the year 2015 it was 0.69. On the other

hand the Quick ratio does not count the inventory liquid asset and the ratio for the year 2015 is 0.22

times and in the year 2014 it is 0.31. To sum up we can say that the liquidity position of the company is

on alarming stage and the company needs to work to improve the same

3.Capital Structure Ratio

The Gross profit ration of the company for the year 2015 and 2014 is 6.80% and 6.74% respectively. We

can say that there is not major change in gross profitability of the company. However if we check the

result Net Profit ratio , the same has shown upward trend in the year 2015. The net profit ratio in the

year 2015 is 5.2% as against 4.91% in the year 2014. We can say that company has exercised good

control over the administrative and other general cost. The reason for increase in profit is reduction in

the Finance cost. On the other return on equity has shown the downward trend in the year 2015. The

ratio of Return on equity in the year 2015 was 18.69% as against 16.76% in the year 2014. It should be

noted that though the profit for the year 2015 is increased , the return on equity decreased due to

increased in the shareholder’s fund in the year 2015. On the other had the ratio return on asset also

showed slight decrease in the year of 2015 which us 6.31% as against 6.4% in the year 2014. The ratio is

decreased due to increase in the total asset of the company in the year 2015 in comparison to the year

2014.

2.

Liquidity Ratio

We have take two ratio to represent the liquidity position of the company named Current ratio and

Quick ratio. The same is presented in below table for the year 2015 and 2014

Liquidity ratio 2015.00 2014.00 Measure

Current Ratio 0.69 0.58 Times

Quick Ratio 0.31 0.22 Times

Data interpretation

The current ratio below 1 times indicate that company cannot pay its current liability with its current

asset if requires to be paid as on day. In the current case of Marks and Spencer Plc the same is below 1

times for both years. In the year 2014 the ratio was 0.58 and in the year 2015 it was 0.69. On the other

hand the Quick ratio does not count the inventory liquid asset and the ratio for the year 2015 is 0.22

times and in the year 2014 it is 0.31. To sum up we can say that the liquidity position of the company is

on alarming stage and the company needs to work to improve the same

3.Capital Structure Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

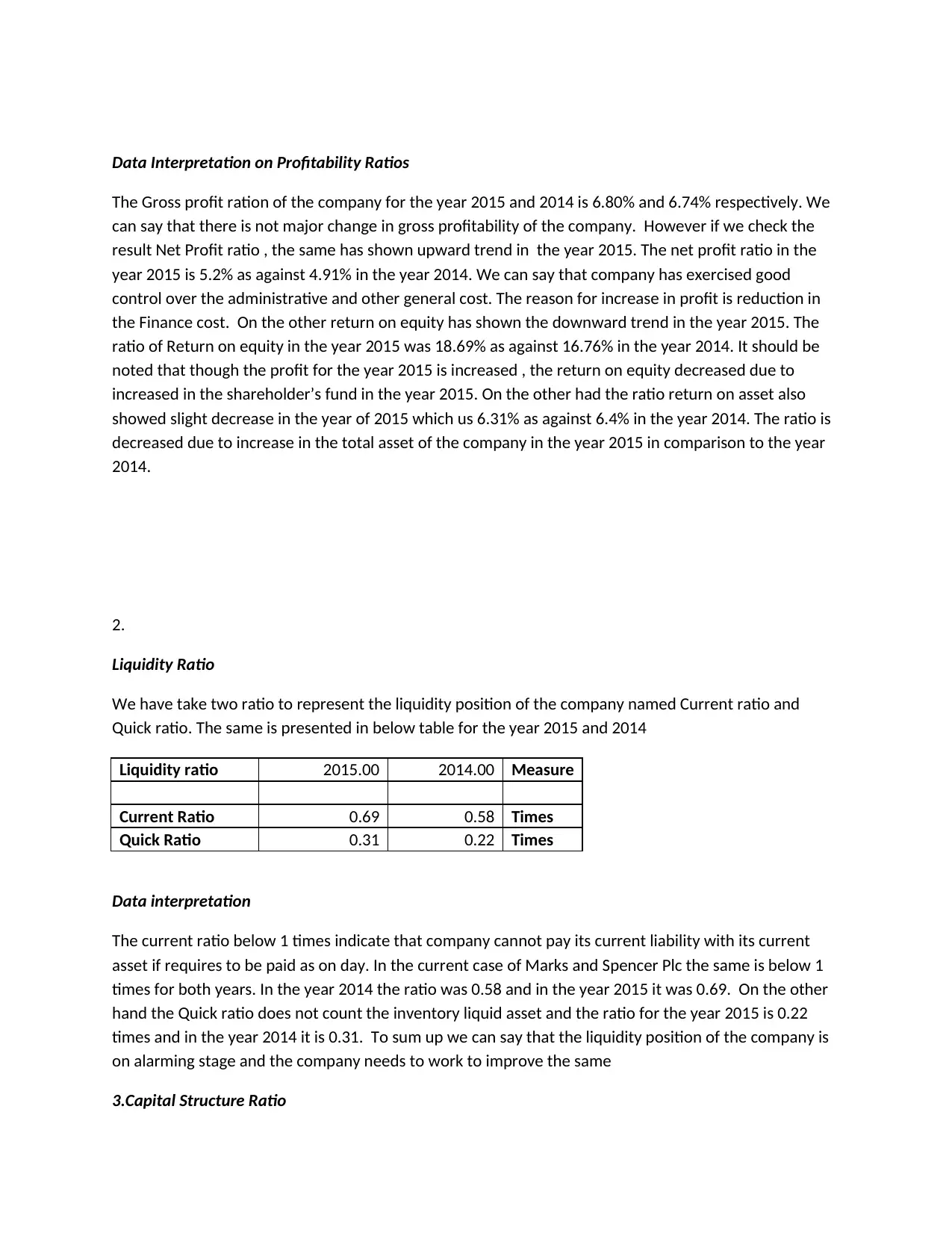

Capital structure ratios help to identify the pattern of the funding opted by the company. Here we have

taken debt ratio and interest coverage ratio for the assessment of the capital structure of the company.

The summary capital structure ratio presented below :

Capital Structure Ratio 2015 2014

Measur

e

Debt Ratio 0.61 0.66 Times

Interest Coverage Ratio 6.53 4.99 Times

Data Interpretation

It is to be noted that the debt ratio in the year 2015 was 0.61 times as against 0.66 in the year 2014. We

can say that the company has financed 66% for its asset by its debt in the year 2014 and 61% of its in the

year 2015. The debt component is reduced in the year 2015. On the other the interest coverage ratio for

the year 2014 was 4.99 times as against 6.53 times in the year 2015. As in the year the debt component

decreased and also profitability increased the interest coverage ratio increased in the year 2015 in

comparison with year 2014

4. Efficiency ratio

The efficiency ratio helps to identify the management’s control over various policy of the company. We

have taken Debtors days ratio to analyze the efficiency ratio of the company

Efficiency Ratio 2015 2014

Measur

e

Debtors Days Ratio in days 11.39 10.96 Days

Data interrelation

The debtor’s days ratio in the year 2014 is 10.96 days as against 11.39 days in the year 2015. The control

over policy is slightly decreased in the year 2015. It is to be noted that we have assumed that all the

sales is credit sales for the purpose of carrying out calculation of above ratio.

Overall conclusion

taken debt ratio and interest coverage ratio for the assessment of the capital structure of the company.

The summary capital structure ratio presented below :

Capital Structure Ratio 2015 2014

Measur

e

Debt Ratio 0.61 0.66 Times

Interest Coverage Ratio 6.53 4.99 Times

Data Interpretation

It is to be noted that the debt ratio in the year 2015 was 0.61 times as against 0.66 in the year 2014. We

can say that the company has financed 66% for its asset by its debt in the year 2014 and 61% of its in the

year 2015. The debt component is reduced in the year 2015. On the other the interest coverage ratio for

the year 2014 was 4.99 times as against 6.53 times in the year 2015. As in the year the debt component

decreased and also profitability increased the interest coverage ratio increased in the year 2015 in

comparison with year 2014

4. Efficiency ratio

The efficiency ratio helps to identify the management’s control over various policy of the company. We

have taken Debtors days ratio to analyze the efficiency ratio of the company

Efficiency Ratio 2015 2014

Measur

e

Debtors Days Ratio in days 11.39 10.96 Days

Data interrelation

The debtor’s days ratio in the year 2014 is 10.96 days as against 11.39 days in the year 2015. The control

over policy is slightly decreased in the year 2015. It is to be noted that we have assumed that all the

sales is credit sales for the purpose of carrying out calculation of above ratio.

Overall conclusion

It is to be noted that the profitability, efficiency and capital structure ratio are good and consistent over

a period of 2 years. The company has relied more on the debt fund to run the business. However, the

liquidity position of the company is worst in both year. Management should take necessary step to

improve the same

(b)

Need of the Stakeholder listed below in the company and discussion on

How they perceive the company to have performed during 2015 and 2014

a. Supplier

Supplier is the most important stakeholder in the company; they contribute considerably in growth of the

company. To manufacture any product the company needs raw material, the same is required in time with

the quality. Providing the good quality material within the given deadline is the best advantage for the

company.

b. Customer

As far as customer concern they are the most important stakeholder for the company. The company runs

due to them. The main purpose of the company is to achieve the profit and the same is possible due to the

existence of the customer. For any company, it is very important that the establish the relationship with

the customer as they are the key to the success of the company.

The customer can perceive the company in the form of turnover which is 103111.1 Pound M in the year

2015 and 10309.7 Pound M in the year 2014.

c. Shareholder

They are the real owner of the company and they do provide the startup fund generally for the

company. The shareholder are the one who takes the profit of the company an also bear the loss of the

company. It is to be noted that shareholders are directly interested in the company’s performance and

hence it is very necessary for the management that the company is running in good faith on they behalf.

a period of 2 years. The company has relied more on the debt fund to run the business. However, the

liquidity position of the company is worst in both year. Management should take necessary step to

improve the same

(b)

Need of the Stakeholder listed below in the company and discussion on

How they perceive the company to have performed during 2015 and 2014

a. Supplier

Supplier is the most important stakeholder in the company; they contribute considerably in growth of the

company. To manufacture any product the company needs raw material, the same is required in time with

the quality. Providing the good quality material within the given deadline is the best advantage for the

company.

b. Customer

As far as customer concern they are the most important stakeholder for the company. The company runs

due to them. The main purpose of the company is to achieve the profit and the same is possible due to the

existence of the customer. For any company, it is very important that the establish the relationship with

the customer as they are the key to the success of the company.

The customer can perceive the company in the form of turnover which is 103111.1 Pound M in the year

2015 and 10309.7 Pound M in the year 2014.

c. Shareholder

They are the real owner of the company and they do provide the startup fund generally for the

company. The shareholder are the one who takes the profit of the company an also bear the loss of the

company. It is to be noted that shareholders are directly interested in the company’s performance and

hence it is very necessary for the management that the company is running in good faith on they behalf.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The shareholder contributes the company in the form of shareholder Fund which is 3199.6 Pound

Million in the year 2015 and 2707.3 Pound Million in the year of 2014.

(c)

Ratio analysis is one of the widely used analytical tool to assess the financial position of the company ,

The ratio analysis helps to measure the performance of the company in the appropriate unit either in

days , times and % as per the nature of the ratio. It helps in identifying the relationship of different

component of the financial statement for the past data.

It is very necessary for the company to compare the company’s result with other company’s

performance and with own past data. For such comparison it is very necessary for the company to have

uniform unites to be compared. Ratio analysis helps by giving such uniform measure for the comparison.

As far as management is concern they also need the performance of the company in concise format ,

and such management information data can be provided by ratio analysis tool very easily, Moreover

ratio analysis is widely accepted and easy method to understand and hence it can be understand by

most of the stakeholder of the company also . Thus we can say that ratio analysis is an important tool in

analysis the company’position.

Answer to question 3

A) Profit and loss refer to the margin left after charging all fixed expenses and variable expenses

from all income and revenues. Profit and loss is a basic measure for calculating the profitability

of any project (Kumar, Nottestad, and Macklin, 2007). Profit and loss can be measured by using

profit and loss statement. Hence profit and loss in each condition is required to calculate.

Million in the year 2015 and 2707.3 Pound Million in the year of 2014.

(c)

Ratio analysis is one of the widely used analytical tool to assess the financial position of the company ,

The ratio analysis helps to measure the performance of the company in the appropriate unit either in

days , times and % as per the nature of the ratio. It helps in identifying the relationship of different

component of the financial statement for the past data.

It is very necessary for the company to compare the company’s result with other company’s

performance and with own past data. For such comparison it is very necessary for the company to have

uniform unites to be compared. Ratio analysis helps by giving such uniform measure for the comparison.

As far as management is concern they also need the performance of the company in concise format ,

and such management information data can be provided by ratio analysis tool very easily, Moreover

ratio analysis is widely accepted and easy method to understand and hence it can be understand by

most of the stakeholder of the company also . Thus we can say that ratio analysis is an important tool in

analysis the company’position.

Answer to question 3

A) Profit and loss refer to the margin left after charging all fixed expenses and variable expenses

from all income and revenues. Profit and loss is a basic measure for calculating the profitability

of any project (Kumar, Nottestad, and Macklin, 2007). Profit and loss can be measured by using

profit and loss statement. Hence profit and loss in each condition is required to calculate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

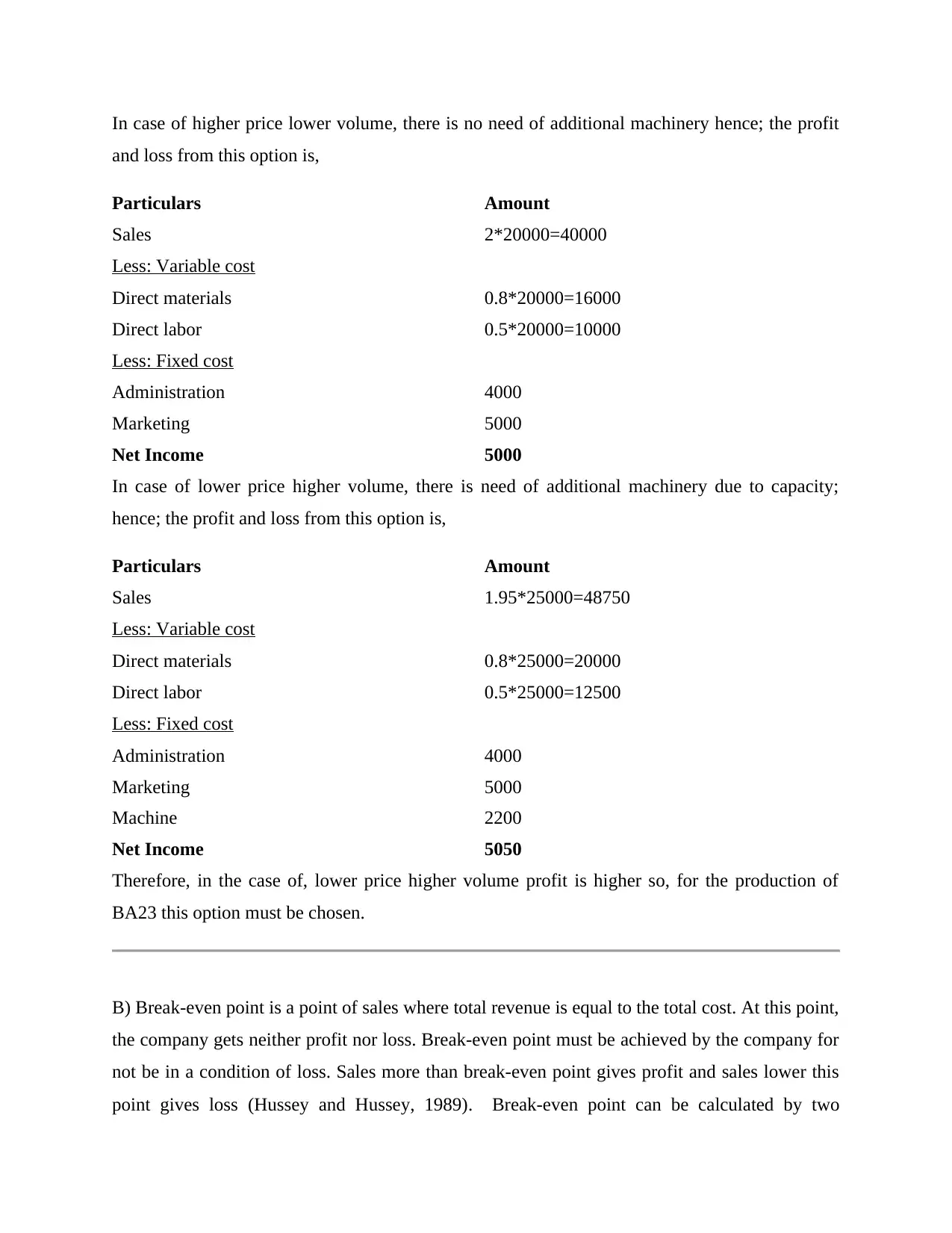

In case of higher price lower volume, there is no need of additional machinery hence; the profit

and loss from this option is,

Particulars Amount

Sales 2*20000=40000

Less: Variable cost

Direct materials 0.8*20000=16000

Direct labor 0.5*20000=10000

Less: Fixed cost

Administration 4000

Marketing 5000

Net Income 5000

In case of lower price higher volume, there is need of additional machinery due to capacity;

hence; the profit and loss from this option is,

Particulars Amount

Sales 1.95*25000=48750

Less: Variable cost

Direct materials 0.8*25000=20000

Direct labor 0.5*25000=12500

Less: Fixed cost

Administration 4000

Marketing 5000

Machine 2200

Net Income 5050

Therefore, in the case of, lower price higher volume profit is higher so, for the production of

BA23 this option must be chosen.

B) Break-even point is a point of sales where total revenue is equal to the total cost. At this point,

the company gets neither profit nor loss. Break-even point must be achieved by the company for

not be in a condition of loss. Sales more than break-even point gives profit and sales lower this

point gives loss (Hussey and Hussey, 1989). Break-even point can be calculated by two

and loss from this option is,

Particulars Amount

Sales 2*20000=40000

Less: Variable cost

Direct materials 0.8*20000=16000

Direct labor 0.5*20000=10000

Less: Fixed cost

Administration 4000

Marketing 5000

Net Income 5000

In case of lower price higher volume, there is need of additional machinery due to capacity;

hence; the profit and loss from this option is,

Particulars Amount

Sales 1.95*25000=48750

Less: Variable cost

Direct materials 0.8*25000=20000

Direct labor 0.5*25000=12500

Less: Fixed cost

Administration 4000

Marketing 5000

Machine 2200

Net Income 5050

Therefore, in the case of, lower price higher volume profit is higher so, for the production of

BA23 this option must be chosen.

B) Break-even point is a point of sales where total revenue is equal to the total cost. At this point,

the company gets neither profit nor loss. Break-even point must be achieved by the company for

not be in a condition of loss. Sales more than break-even point gives profit and sales lower this

point gives loss (Hussey and Hussey, 1989). Break-even point can be calculated by two

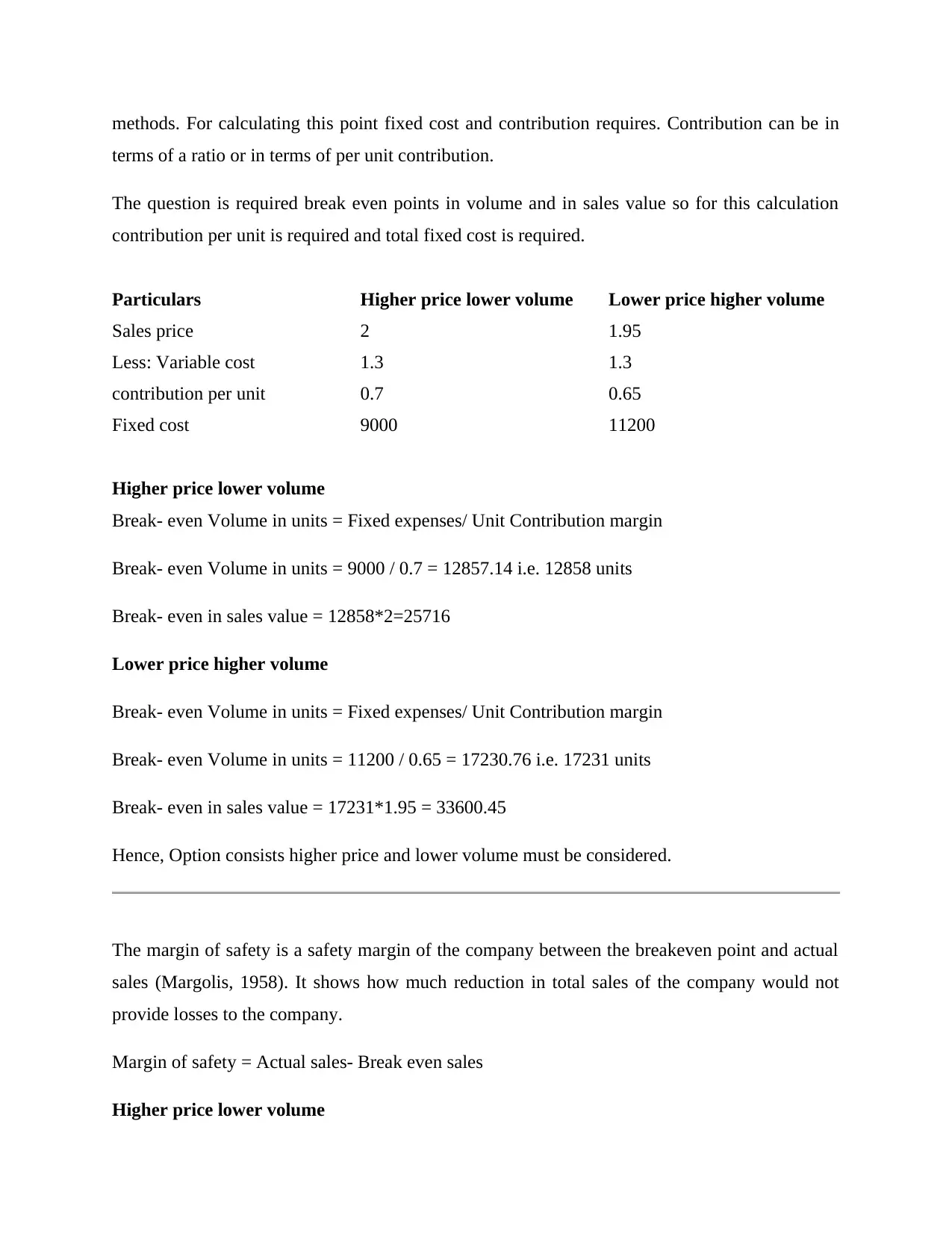

methods. For calculating this point fixed cost and contribution requires. Contribution can be in

terms of a ratio or in terms of per unit contribution.

The question is required break even points in volume and in sales value so for this calculation

contribution per unit is required and total fixed cost is required.

Particulars Higher price lower volume Lower price higher volume

Sales price 2 1.95

Less: Variable cost 1.3 1.3

contribution per unit 0.7 0.65

Fixed cost 9000 11200

Higher price lower volume

Break- even Volume in units = Fixed expenses/ Unit Contribution margin

Break- even Volume in units = 9000 / 0.7 = 12857.14 i.e. 12858 units

Break- even in sales value = 12858*2=25716

Lower price higher volume

Break- even Volume in units = Fixed expenses/ Unit Contribution margin

Break- even Volume in units = 11200 / 0.65 = 17230.76 i.e. 17231 units

Break- even in sales value = 17231*1.95 = 33600.45

Hence, Option consists higher price and lower volume must be considered.

The margin of safety is a safety margin of the company between the breakeven point and actual

sales (Margolis, 1958). It shows how much reduction in total sales of the company would not

provide losses to the company.

Margin of safety = Actual sales- Break even sales

Higher price lower volume

terms of a ratio or in terms of per unit contribution.

The question is required break even points in volume and in sales value so for this calculation

contribution per unit is required and total fixed cost is required.

Particulars Higher price lower volume Lower price higher volume

Sales price 2 1.95

Less: Variable cost 1.3 1.3

contribution per unit 0.7 0.65

Fixed cost 9000 11200

Higher price lower volume

Break- even Volume in units = Fixed expenses/ Unit Contribution margin

Break- even Volume in units = 9000 / 0.7 = 12857.14 i.e. 12858 units

Break- even in sales value = 12858*2=25716

Lower price higher volume

Break- even Volume in units = Fixed expenses/ Unit Contribution margin

Break- even Volume in units = 11200 / 0.65 = 17230.76 i.e. 17231 units

Break- even in sales value = 17231*1.95 = 33600.45

Hence, Option consists higher price and lower volume must be considered.

The margin of safety is a safety margin of the company between the breakeven point and actual

sales (Margolis, 1958). It shows how much reduction in total sales of the company would not

provide losses to the company.

Margin of safety = Actual sales- Break even sales

Higher price lower volume

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17