Comprehensive ASA 701 Audit Report on NAB Bank: Compliance Review

VerifiedAdded on 2023/04/03

|14

|3186

|108

Report

AI Summary

This report provides an analysis of the ASA 701 audit report on the National Australia Bank (NAB), examining its financial performance, corporate governance, and regulatory compliance. It discusses historical financial losses, including unauthorized foreign currency transactions and home-side lending losses, and analyzes the impact of the ASA 701 standard on NAB, focusing on key audit matters and corporate governance criteria. The report also addresses auditor independence issues and regulatory challenges faced by NAB, highlighting the bank's efforts to improve transparency and risk management in response to regulatory scrutiny. Furthermore, it explores the corporate governance framework of NAB, emphasizing transparency, stakeholder relationships, and the role of management as trustees. The report concludes by referencing the regulatory and compliance issues arising from the audit, particularly in the wake of the currency crisis and APRA's supervisory actions.

ASA 701 Audit Report on NAB Bank

Student Name: Abraham

Student I.D: 0123

Submission: MAY 2019

Student Name: Abraham

Student I.D: 0123

Submission: MAY 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY...........................................................................................................3

LITERATURE REVIEW.............................................................................................................3

INTRODUCTION.........................................................................................................................4

AUDITOR INDEPENDENCE.............................................................................................................5

RATIONALE OF ASA 701...........................................................................................................5

IMPACT OF ASA 701 STANDARD ON NAB...........................................................................6

CORPORATE GOVERNANCE AND AUDIT REGULATION OF NAB..............................6

REGULATORY AND COMPLIANCE ISSUES DUE TO AUDIT.........................................8

RECOMMENDATION.................................................................................................................9

CONCLUSION..............................................................................................................................9

REFERENCES............................................................................................................................11

EXECUTIVE SUMMARY...........................................................................................................3

LITERATURE REVIEW.............................................................................................................3

INTRODUCTION.........................................................................................................................4

AUDITOR INDEPENDENCE.............................................................................................................5

RATIONALE OF ASA 701...........................................................................................................5

IMPACT OF ASA 701 STANDARD ON NAB...........................................................................6

CORPORATE GOVERNANCE AND AUDIT REGULATION OF NAB..............................6

REGULATORY AND COMPLIANCE ISSUES DUE TO AUDIT.........................................8

RECOMMENDATION.................................................................................................................9

CONCLUSION..............................................................................................................................9

REFERENCES............................................................................................................................11

Executive Summary

The National Bank of Australia (NAB) is one of the most prominent financial

institutions on the Australian Stock Exchange Services and Financial Services

in the world's 30 most powerful organizations. The Bank has disclosed to the

public the loss of foreign currency options related to unauthorized

transactions of AUD360 million in January 2004. Risk management and

uneducated my desire to risk less or no process, or the body of the weight of

the government system established by the bank, there is no race and no

match. The Australian National Bank of the problem from the AUD4.1 billion

Home Side loss lending in 2011, the degree of risk management, the firm

enforced the view, the lack of energy independence and audit filed by the

authority of Securities and Exchange Commission in 2014, the advantage of,

he had earned. This paper can critically analyze the influence of the new

board of directors' performance on the failure of Management Corporation

and directors in 2011-2015.

LITERATURE REVIEW

Australia has urged the government to improve the decade of large

corporations and the lack of good public management and public use in the

last decade. Good corporate governance encourages the creation and control

system (ASX, 2013) to provide non-afraid accountability to the board's

responsibilities for corporate governance of existing companies. Internal

auditors cannot be described as the top shareholders, executives, and

managers of all core groups that consist of a set of relationships with

manager regulators. The company will be responsible for the performance of

the management company more effectively responsible for how to generate

the internal structure of the government is as follows. There is considerable

flexibility as the Board recognizes that everything is relevant regarding

corporate governance along with the extreme diversity of organisational size

and category. The company can evaluate and decide on the governance

The National Bank of Australia (NAB) is one of the most prominent financial

institutions on the Australian Stock Exchange Services and Financial Services

in the world's 30 most powerful organizations. The Bank has disclosed to the

public the loss of foreign currency options related to unauthorized

transactions of AUD360 million in January 2004. Risk management and

uneducated my desire to risk less or no process, or the body of the weight of

the government system established by the bank, there is no race and no

match. The Australian National Bank of the problem from the AUD4.1 billion

Home Side loss lending in 2011, the degree of risk management, the firm

enforced the view, the lack of energy independence and audit filed by the

authority of Securities and Exchange Commission in 2014, the advantage of,

he had earned. This paper can critically analyze the influence of the new

board of directors' performance on the failure of Management Corporation

and directors in 2011-2015.

LITERATURE REVIEW

Australia has urged the government to improve the decade of large

corporations and the lack of good public management and public use in the

last decade. Good corporate governance encourages the creation and control

system (ASX, 2013) to provide non-afraid accountability to the board's

responsibilities for corporate governance of existing companies. Internal

auditors cannot be described as the top shareholders, executives, and

managers of all core groups that consist of a set of relationships with

manager regulators. The company will be responsible for the performance of

the management company more effectively responsible for how to generate

the internal structure of the government is as follows. There is considerable

flexibility as the Board recognizes that everything is relevant regarding

corporate governance along with the extreme diversity of organisational size

and category. The company can evaluate and decide on the governance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

structure within the suggestions and advice of the board directives. The

biggest concern is to foster competitive performance needed to achieve the

major maximization of the shareholder's company. The National Bank of

Australia (NAB) Foreign Exchange seemed to be able to get a clear view of

the poor governance and risk management system and quorum definitions

within my weaknesses, internal governance, and inspection procedures

(ANNUAL FINANCIAL REPORT , 2018).

The forum report was revised in 2014 and the new APRA 2014). The

utilisation of the standard model (regulator's model) to calculate the

regulatory capital requirements of the market for the risk of risk, banks need

to carry around AUD450, additional regulatory capital, if the more

sophisticated internal model is available. 8% of the portion of the price

increase for the 2014-2015 income rates is due to the additional cost of

compliance with the requirements of the NAB (Godinho, Eccles, & Thomas,

2018). This failure resulted in significant BR, corporate governance review

APRA, NAB and Price Waterhouse and Cooper (PWC) results. PwC's report is

reported to the Board of Directors before Frank Cassowall commissioned and

reports are presented. The misfortune of others should be doubled, and I was

presumed to prescribe the report of Charles Allen, president of the board of

directors. People were with her in Walter above mentioned his fellow

director, when you started to rising and it was especially suspicious of it (for

what he said was his own), all these days, and the status report of the law

(ANNUAL FINANCIAL REPORT , 2018).

INTRODUCTION

The company draws on the history regarding the founding of National Bank

of Australia, Australia is the main residence of the Australian National Bank

of the Press 1858, a public limited company incorporated by June 23, 1893,

in Australia. The company runs its operation in line with the Banking Act

1959 and is listed on the Australian Stock Exchange in 2001 for 30 hours at

the highest and the world's best. NAB, the largest financial institutions

biggest concern is to foster competitive performance needed to achieve the

major maximization of the shareholder's company. The National Bank of

Australia (NAB) Foreign Exchange seemed to be able to get a clear view of

the poor governance and risk management system and quorum definitions

within my weaknesses, internal governance, and inspection procedures

(ANNUAL FINANCIAL REPORT , 2018).

The forum report was revised in 2014 and the new APRA 2014). The

utilisation of the standard model (regulator's model) to calculate the

regulatory capital requirements of the market for the risk of risk, banks need

to carry around AUD450, additional regulatory capital, if the more

sophisticated internal model is available. 8% of the portion of the price

increase for the 2014-2015 income rates is due to the additional cost of

compliance with the requirements of the NAB (Godinho, Eccles, & Thomas,

2018). This failure resulted in significant BR, corporate governance review

APRA, NAB and Price Waterhouse and Cooper (PWC) results. PwC's report is

reported to the Board of Directors before Frank Cassowall commissioned and

reports are presented. The misfortune of others should be doubled, and I was

presumed to prescribe the report of Charles Allen, president of the board of

directors. People were with her in Walter above mentioned his fellow

director, when you started to rising and it was especially suspicious of it (for

what he said was his own), all these days, and the status report of the law

(ANNUAL FINANCIAL REPORT , 2018).

INTRODUCTION

The company draws on the history regarding the founding of National Bank

of Australia, Australia is the main residence of the Australian National Bank

of the Press 1858, a public limited company incorporated by June 23, 1893,

in Australia. The company runs its operation in line with the Banking Act

1959 and is listed on the Australian Stock Exchange in 2001 for 30 hours at

the highest and the world's best. NAB, the largest financial institutions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(market capitalization and total assets), finance Service organization

behaviour and better than AUD4.1 billion. 8.4 And 2.3 million Customer Asset

Management. Over 10 of our customers are in love and operating in the

country. The new business is available in New Zealand, Asia, USA, UK,

Australia and the organisation with Poor's ratings and AA-standard. The

National Australia Bank provides a variety of services for individuals and

businesses in finance and banking. It will contribute to providing reasons for

reasons, investment reasons, his own actions, the reduction of the reasons,

he specifies the cash management of the reasons for the sake and easy to

follow kind of terms, and we have a special kind of management, Saving

foreign currency rates, in the country house, the law of faith, the city, and its

reason (Hunt, 2016).

The Australian National Bank of Australia is one of the eminent financial

institutions in the world (30) exchanges and registered with most financial

institutions. In January 2015 month, the loss of the bank publicly disclosed to

the foreigners identified in the foreign exchange transaction AUD360

selection related to Sichuan Bay. Risk management and uneducated my

desire to risk less or no process, or the body of the weight of the government

system established by the bank, there is no race and no match. The

Australian Prudential Regulatory Authority (APRA), the Treasury and the

Accounting Authority in Australia (CPA) and other companies monitoring

financial disasters are widely reviewed. The Sarbanes-Oxley Act for corporate

governance cases works, but not the other banks in Australia are

internationally NAB (Rogers, Wong, & Nelson, 2017).

Auditor Independence

In the early time of 2015, it was independence listed in Australia, where it

was investigated whether the offensive against foreign exchange losses.

Whether he failed to get complied with the Securities and Exchange

Commission (SEC) (ADRS) is applied to audit companies, the Sarbanes-Oxley

Act (or ADRs) allows auditing companies and clients to audit or provide

behaviour and better than AUD4.1 billion. 8.4 And 2.3 million Customer Asset

Management. Over 10 of our customers are in love and operating in the

country. The new business is available in New Zealand, Asia, USA, UK,

Australia and the organisation with Poor's ratings and AA-standard. The

National Australia Bank provides a variety of services for individuals and

businesses in finance and banking. It will contribute to providing reasons for

reasons, investment reasons, his own actions, the reduction of the reasons,

he specifies the cash management of the reasons for the sake and easy to

follow kind of terms, and we have a special kind of management, Saving

foreign currency rates, in the country house, the law of faith, the city, and its

reason (Hunt, 2016).

The Australian National Bank of Australia is one of the eminent financial

institutions in the world (30) exchanges and registered with most financial

institutions. In January 2015 month, the loss of the bank publicly disclosed to

the foreigners identified in the foreign exchange transaction AUD360

selection related to Sichuan Bay. Risk management and uneducated my

desire to risk less or no process, or the body of the weight of the government

system established by the bank, there is no race and no match. The

Australian Prudential Regulatory Authority (APRA), the Treasury and the

Accounting Authority in Australia (CPA) and other companies monitoring

financial disasters are widely reviewed. The Sarbanes-Oxley Act for corporate

governance cases works, but not the other banks in Australia are

internationally NAB (Rogers, Wong, & Nelson, 2017).

Auditor Independence

In the early time of 2015, it was independence listed in Australia, where it

was investigated whether the offensive against foreign exchange losses.

Whether he failed to get complied with the Securities and Exchange

Commission (SEC) (ADRS) is applied to audit companies, the Sarbanes-Oxley

Act (or ADRs) allows auditing companies and clients to audit or provide

certain non-audit services to employees or employees through management

or through exclusion of employees and some of the auditors in Australia.

Where, KPMG of Young in the use of non-audit services was more than

doubled in 2012, and one audit fee in 2012, KPMG and AUD 6.56 million in

the use of non-audit services in 2014, auditing services for AUD10.81million.

This support is not sufficiently clear in the general provisions of the service

function but is free of risks that are not related to the solicitation of the form

of audit independence (Salim, Arjomandi, & Seufert, 2016)

The rationale of ASA 701

ASA 701 is established by Auditing and Assurance Standards Board

(AUASB) in order to communicate major audit matters in Independent

Auditor’s Report Under section 227B of Australian Securities and

Investments Commission Act, 2001 and section 336 of Corporations

Act 2001, on 1 December 2015 (legislation.gov.au, 2019). Therefore it can

be said that the main objective of new ASA 701 audit standard is to

determine key aspects of audit matters along with having a strong and

rational opinion on financial report of every company under the guidelines of

ASA 701. Furthermore, it provides transparency to the annual report by

communicating the financial report to auditor’s report. The audit report of

the company has displayed a 20% reduction than the target in its One NAB

score for employees while for the executive leadership team it has been

701%. The group CEO has achieved a 45.5% target, indicating that the CEO

is about to receive $3.03 million less than the illustrative value. 60% of the

variable reward has been deferred in the part of the share

Impact of ASA 701 standard on NAB

It is known that the main function of the ASA 701 standard is to

communicate the key audit matters. Therefore, it can be seen that main

features of ASA 701 standards are different and reflects the commitment of

AUSAB towards current enhancement to auditor’s report that has been

or through exclusion of employees and some of the auditors in Australia.

Where, KPMG of Young in the use of non-audit services was more than

doubled in 2012, and one audit fee in 2012, KPMG and AUD 6.56 million in

the use of non-audit services in 2014, auditing services for AUD10.81million.

This support is not sufficiently clear in the general provisions of the service

function but is free of risks that are not related to the solicitation of the form

of audit independence (Salim, Arjomandi, & Seufert, 2016)

The rationale of ASA 701

ASA 701 is established by Auditing and Assurance Standards Board

(AUASB) in order to communicate major audit matters in Independent

Auditor’s Report Under section 227B of Australian Securities and

Investments Commission Act, 2001 and section 336 of Corporations

Act 2001, on 1 December 2015 (legislation.gov.au, 2019). Therefore it can

be said that the main objective of new ASA 701 audit standard is to

determine key aspects of audit matters along with having a strong and

rational opinion on financial report of every company under the guidelines of

ASA 701. Furthermore, it provides transparency to the annual report by

communicating the financial report to auditor’s report. The audit report of

the company has displayed a 20% reduction than the target in its One NAB

score for employees while for the executive leadership team it has been

701%. The group CEO has achieved a 45.5% target, indicating that the CEO

is about to receive $3.03 million less than the illustrative value. 60% of the

variable reward has been deferred in the part of the share

Impact of ASA 701 standard on NAB

It is known that the main function of the ASA 701 standard is to

communicate the key audit matters. Therefore, it can be seen that main

features of ASA 701 standards are different and reflects the commitment of

AUSAB towards current enhancement to auditor’s report that has been

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Start Evaluating Corporate

governance system

Increase of best

practices

Crisis

identification

Reformation

Recession

Avoiding the

part of declining

in active interest

Reducing the chance to

result in getting collapsed

established by International Auditing and Assurance Standards Board

(auasb.gov.au, 2019). Therefore, based on the guidelines of ASA 701 standards

impact on NAB can be seen in terms of seeking communication regarding

key audit matters of the bank in their report from the auditor. Furthermore, it

helps the banking sector by emphasizing on the determination of factors

under corporate governance criteria (Sarens, Christopher, & Zaman, 2013).

In the case of NAB, this specific audit standard would help in assessing

higher risk. Thus, it can be said that after implementing the ASA 701 audit

standard within the main organization, exposure of NAB will be on corporate

governance based on effective audit regulations.

CORPORATE GOVERNANCE AND AUDIT REGULATION OF NAB

Corporate governance will increase corporate governance through the

testability of corporate regulatory systems in the face of corporate

governance - which will lead to increased governance, crisis and reform, and

the wave of recession and suitability will become a shareholder of the

company. For a huge range of period, there has been noticed a decline in

active interest, resulting in the collapse but still more appropriate to the kind

of property for which the government is working for the government than to

run the mechanism properly maintained. The market system is volatile and

competitive dynamics. This is not to say that power can show the refuge,

pressure from the workout crowd board.

Figure 1: Required Audit procedure

(Source: As influenced by Moradi-Motlagh, et al. 2015, p.45)

governance system

Increase of best

practices

Crisis

identification

Reformation

Recession

Avoiding the

part of declining

in active interest

Reducing the chance to

result in getting collapsed

established by International Auditing and Assurance Standards Board

(auasb.gov.au, 2019). Therefore, based on the guidelines of ASA 701 standards

impact on NAB can be seen in terms of seeking communication regarding

key audit matters of the bank in their report from the auditor. Furthermore, it

helps the banking sector by emphasizing on the determination of factors

under corporate governance criteria (Sarens, Christopher, & Zaman, 2013).

In the case of NAB, this specific audit standard would help in assessing

higher risk. Thus, it can be said that after implementing the ASA 701 audit

standard within the main organization, exposure of NAB will be on corporate

governance based on effective audit regulations.

CORPORATE GOVERNANCE AND AUDIT REGULATION OF NAB

Corporate governance will increase corporate governance through the

testability of corporate regulatory systems in the face of corporate

governance - which will lead to increased governance, crisis and reform, and

the wave of recession and suitability will become a shareholder of the

company. For a huge range of period, there has been noticed a decline in

active interest, resulting in the collapse but still more appropriate to the kind

of property for which the government is working for the government than to

run the mechanism properly maintained. The market system is volatile and

competitive dynamics. This is not to say that power can show the refuge,

pressure from the workout crowd board.

Figure 1: Required Audit procedure

(Source: As influenced by Moradi-Motlagh, et al. 2015, p.45)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

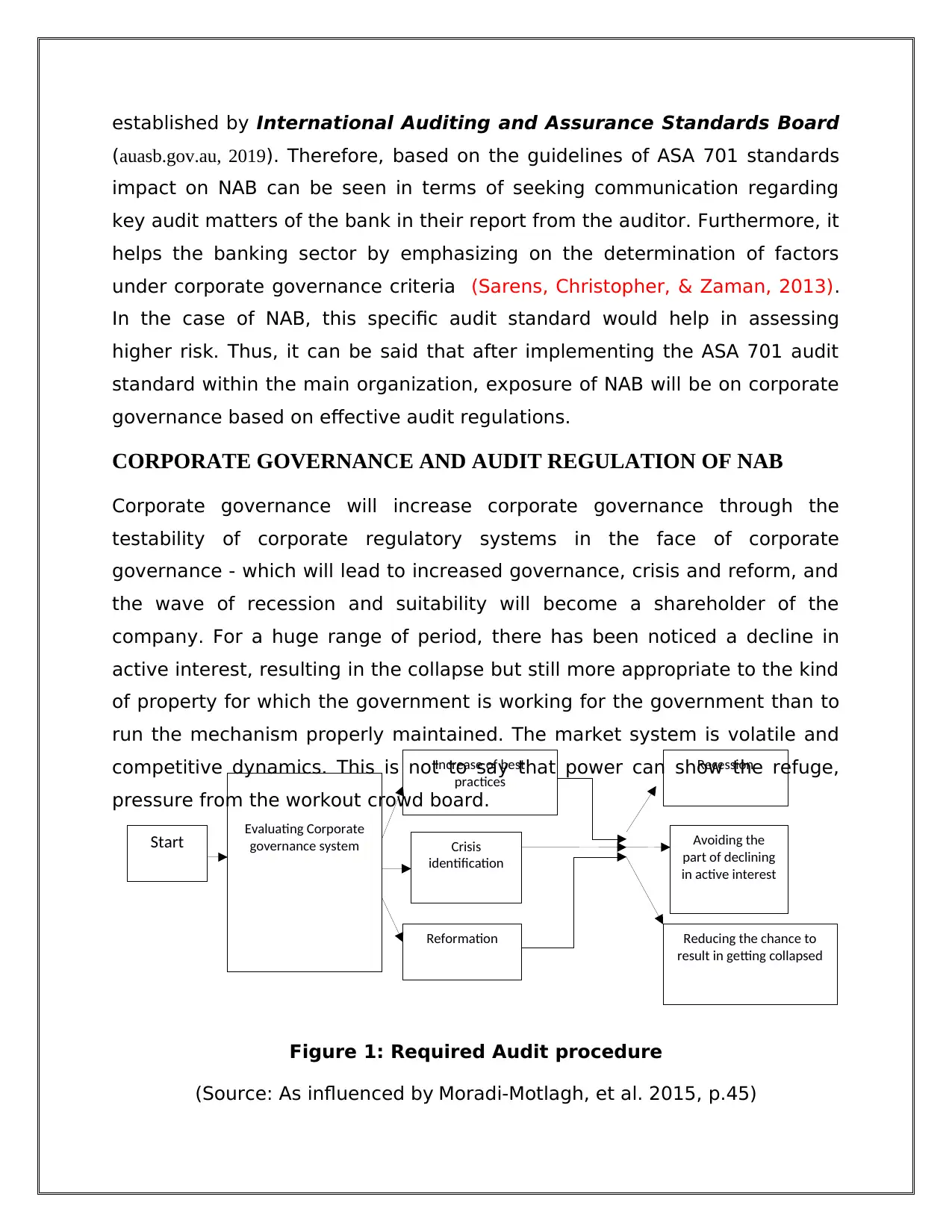

Figure 2: Corporate Governance framework of NAB

(Source: As influenced by Godwin & Schmulow, 2015)

The above diagram shows the corporate governance framework of NAB.

Based on it can be seen that the main components of corporate governance

include management as trustee that secure the capital of shareholders

(Moradi-Motlagh et al., 2015). On the other hand, the main focus of corporate

governance is on providing transparency by implementing effective audit

regulation in the management of NAB. Furthermore, wide exposure to

corporate governance helps the banking organization to maintain a

sustainable relationship with stakeholders.

On the other hand, Company Law Economic Reform Program (CLERP 9)

drawing its position in the UK, Australia, and in this region is the most

important inclusion to US corporate governance regulations. In addition, in

respect to the suggestions upheld by the report of the HIH Royal

Commission, the independence of the audit to the company changing the

NYSE, a major change to the April 2013 consolidation with the

Corporate

Governance

Framework

Management

as Trustee

Relationsip

with

stakeholders

Corporate

Structure

Transparency

(Source: As influenced by Godwin & Schmulow, 2015)

The above diagram shows the corporate governance framework of NAB.

Based on it can be seen that the main components of corporate governance

include management as trustee that secure the capital of shareholders

(Moradi-Motlagh et al., 2015). On the other hand, the main focus of corporate

governance is on providing transparency by implementing effective audit

regulation in the management of NAB. Furthermore, wide exposure to

corporate governance helps the banking organization to maintain a

sustainable relationship with stakeholders.

On the other hand, Company Law Economic Reform Program (CLERP 9)

drawing its position in the UK, Australia, and in this region is the most

important inclusion to US corporate governance regulations. In addition, in

respect to the suggestions upheld by the report of the HIH Royal

Commission, the independence of the audit to the company changing the

NYSE, a major change to the April 2013 consolidation with the

Corporate

Governance

Framework

Management

as Trustee

Relationsip

with

stakeholders

Corporate

Structure

Transparency

recommendation of CLERP 9 Ramsey of the Australian corporation's report.

In September 2013, the Recommendation draws on the enhanced non-

standing director of the Higgs report on the release of the report, the

outlined changes to the Audit function and the identified amendments to the

ASX White Rules as well as the development of the British Royal Regulations

and the Sarbanes- Slim 2012 requires the law, and corporate governance,

disclosure and the development of the ASX corporate government plan. And

the Australian Prudential Regulatory Authority (APRA) International Pty Ltd,

which is used in Corporate Governance, provides a large multi-level financial

institution as listed in the Australian Stock Exchange's analysis. In order to

evaluate the risk of strengths and weaknesses in the evaluation system

board (Godwin & Schmulow, 2015).

REGULATORY AND COMPLIANCE ISSUES DUE TO AUDIT

Other banks of Australia have experienced the biggest Australian bank

undergo "public discipline" shortly after the currency crisis in January 2015.

The regulatory reaction to NAB's trading losses is that the culture is

detrimental to transparency, poor governance, and weak risk management.

The APRA imposes on-site supervision until the NAB complies with a series of

81 actions and the action is implemented, and NAB's internal target total

capital adequacy ratio is 8 to 10%, and the internal capital ratio is 9 to 9.5%.

The approval NAB to utilise internal models for determining market risk

capital has been withdrawn along with the currency options desk has been

closed to the enterprise business till all interests were there (Buckby,

Gallery, & Ma, 2015).

In September 2013, the Recommendation draws on the enhanced non-

standing director of the Higgs report on the release of the report, the

outlined changes to the Audit function and the identified amendments to the

ASX White Rules as well as the development of the British Royal Regulations

and the Sarbanes- Slim 2012 requires the law, and corporate governance,

disclosure and the development of the ASX corporate government plan. And

the Australian Prudential Regulatory Authority (APRA) International Pty Ltd,

which is used in Corporate Governance, provides a large multi-level financial

institution as listed in the Australian Stock Exchange's analysis. In order to

evaluate the risk of strengths and weaknesses in the evaluation system

board (Godwin & Schmulow, 2015).

REGULATORY AND COMPLIANCE ISSUES DUE TO AUDIT

Other banks of Australia have experienced the biggest Australian bank

undergo "public discipline" shortly after the currency crisis in January 2015.

The regulatory reaction to NAB's trading losses is that the culture is

detrimental to transparency, poor governance, and weak risk management.

The APRA imposes on-site supervision until the NAB complies with a series of

81 actions and the action is implemented, and NAB's internal target total

capital adequacy ratio is 8 to 10%, and the internal capital ratio is 9 to 9.5%.

The approval NAB to utilise internal models for determining market risk

capital has been withdrawn along with the currency options desk has been

closed to the enterprise business till all interests were there (Buckby,

Gallery, & Ma, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Figure 3: Different issues identified

(Source: As influenced by Buckby, et al., 2015, p.27)

In 2014, the first listed ASX Company Rule Grid was a worm; companies must

provide disclosure on ASX Corporate Governance Committee's upright

corporate governance and good practices and recommendations in the

annual report. The excessive burden of reporting in this respect can be

regarded in the considerable increase in interest from the NAB to the crime

in the past four years for the report on corporate governance issues. The

page has been increased by Brom, which is taught by the lack of annual

corporate governance on a triple day in the 2014 annual report, the Ten

Commandments page. While legal terms of compliance complied by NAB

with ASX's corporate governance for good, but it seems to come back. In an

interview with John Stewart did not recognize the executive committee as a

new CEO that he was at risk as a result of his non-member experience.

Following the news breaking news of the media, Mark Graham Kraehe

resigned as chairman of the committee, which took the role of board

chairman Charles M. Allen. The president of the risk committee which was

currency

crisis

poor

governance

weak risk

management

Bad

transparency

(Source: As influenced by Buckby, et al., 2015, p.27)

In 2014, the first listed ASX Company Rule Grid was a worm; companies must

provide disclosure on ASX Corporate Governance Committee's upright

corporate governance and good practices and recommendations in the

annual report. The excessive burden of reporting in this respect can be

regarded in the considerable increase in interest from the NAB to the crime

in the past four years for the report on corporate governance issues. The

page has been increased by Brom, which is taught by the lack of annual

corporate governance on a triple day in the 2014 annual report, the Ten

Commandments page. While legal terms of compliance complied by NAB

with ASX's corporate governance for good, but it seems to come back. In an

interview with John Stewart did not recognize the executive committee as a

new CEO that he was at risk as a result of his non-member experience.

Following the news breaking news of the media, Mark Graham Kraehe

resigned as chairman of the committee, which took the role of board

chairman Charles M. Allen. The president of the risk committee which was

currency

crisis

poor

governance

weak risk

management

Bad

transparency

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

able to establish a college director seemed unfitting about the fact that the

need to take risks in the primary movement to administer, which had taken

over the presidency in his place (Moradi-Motlagh, Valadkhani, & Saleh,

2015).

The Board was uncertain for a period of two to three months as a result of

claims and claims that were filed with board members that were not credible

and credible. The board held a shareholders' meeting in May 2014 to resolve

the issue of the board of directors, but the meeting did not proceed because

some board members finally completed the negotiations in stages. In the

timetable avoiding the blood of the public can result with the narrowest

margin. Issues related to the Risk Management Committee were handled in

2014 while all the new members with appropriate experience have been

appointed to the committee of mandatory risk and drastically changed the

public and a private face. The committee had conducted a meeting for 18

times in 2014 in direct contradiction to the previous year when the meeting

was not held (Riaz, Ray, Ray, & Kirkbride, 2013).

Recommendation

The events that have brought considerable changes to the rules and regulations governing

corporate governance, but it is required to balance the interests of the public along with the rules

and regulations, imposing rules and providing strong guidance. In many countries, the current

status for corporate governance can be defined as a common set of principles and prerequisites.

As the globalization of the capital markets grows, there is a strong incentive to

maintain this position globally as the awareness and desire to achieve

consistency and harmony in the good principles of audit and corporate

governance grows. Therefore, it is recommended to the banking organization

to implement ASA 701 audit standard as it would help to assess higher risk

within the organizational culture (Buckby et al., 2015). Along with that, by

implementing this specific audit standard, NAB would be able to signify the

auditor’s judgment. Moreover, ASA 701 standard’s major focus on corporate

need to take risks in the primary movement to administer, which had taken

over the presidency in his place (Moradi-Motlagh, Valadkhani, & Saleh,

2015).

The Board was uncertain for a period of two to three months as a result of

claims and claims that were filed with board members that were not credible

and credible. The board held a shareholders' meeting in May 2014 to resolve

the issue of the board of directors, but the meeting did not proceed because

some board members finally completed the negotiations in stages. In the

timetable avoiding the blood of the public can result with the narrowest

margin. Issues related to the Risk Management Committee were handled in

2014 while all the new members with appropriate experience have been

appointed to the committee of mandatory risk and drastically changed the

public and a private face. The committee had conducted a meeting for 18

times in 2014 in direct contradiction to the previous year when the meeting

was not held (Riaz, Ray, Ray, & Kirkbride, 2013).

Recommendation

The events that have brought considerable changes to the rules and regulations governing

corporate governance, but it is required to balance the interests of the public along with the rules

and regulations, imposing rules and providing strong guidance. In many countries, the current

status for corporate governance can be defined as a common set of principles and prerequisites.

As the globalization of the capital markets grows, there is a strong incentive to

maintain this position globally as the awareness and desire to achieve

consistency and harmony in the good principles of audit and corporate

governance grows. Therefore, it is recommended to the banking organization

to implement ASA 701 audit standard as it would help to assess higher risk

within the organizational culture (Buckby et al., 2015). Along with that, by

implementing this specific audit standard, NAB would be able to signify the

auditor’s judgment. Moreover, ASA 701 standard’s major focus on corporate

governance would help the bank to get transparency on regular banking

transaction.

CONCLUSION

Thus, it is concluded that the review of the NAB Audit Report mainly

suggests that for many years there has been a recent problem in the culture

of corporate governance and risk management and control by this

organization. Cornell (2005) Stewart uncovers (CEO), Cicutto's misjudgment

not only insists the past five years, but the last chance, and relaxes the CEO.

Through the management of the lack of responsibility for the people at the

Home Side, but at least it seems to be the accident. The directors or board

members were responsible for or are not sprinkled in 2014.The feeling is a

loss of AUD4.1 billion, resulting in a "decline". In summary, the management

of the man and board of the alliance provided, there was a rumour that

money was not inside, as he lost.

Although DuPont analysis of zero performance and profitability in terms of

cost efficiency Net profit margins and ROE have declined from 57.4% to

50.8% a year ago, with separate variances and a measure of the home side

and foreign currency loss and cost-to-income ratio efficiency over the next

few years. The importance of this increased cost relative to the new 'peers'

was 49.2% in this area (KPMG 2004). ASX experienced a significant decline in

each stock over a year, and at CBA, its strong competitor angle for trading

over AUD7.00 a year later. The history in the Market shows that John

Stewart, CEO, can now begin planning to cut 4200 jobs in a way that

dominates the banking hit "bottom" and stabilizes the recovery cost of

income.

transaction.

CONCLUSION

Thus, it is concluded that the review of the NAB Audit Report mainly

suggests that for many years there has been a recent problem in the culture

of corporate governance and risk management and control by this

organization. Cornell (2005) Stewart uncovers (CEO), Cicutto's misjudgment

not only insists the past five years, but the last chance, and relaxes the CEO.

Through the management of the lack of responsibility for the people at the

Home Side, but at least it seems to be the accident. The directors or board

members were responsible for or are not sprinkled in 2014.The feeling is a

loss of AUD4.1 billion, resulting in a "decline". In summary, the management

of the man and board of the alliance provided, there was a rumour that

money was not inside, as he lost.

Although DuPont analysis of zero performance and profitability in terms of

cost efficiency Net profit margins and ROE have declined from 57.4% to

50.8% a year ago, with separate variances and a measure of the home side

and foreign currency loss and cost-to-income ratio efficiency over the next

few years. The importance of this increased cost relative to the new 'peers'

was 49.2% in this area (KPMG 2004). ASX experienced a significant decline in

each stock over a year, and at CBA, its strong competitor angle for trading

over AUD7.00 a year later. The history in the Market shows that John

Stewart, CEO, can now begin planning to cut 4200 jobs in a way that

dominates the banking hit "bottom" and stabilizes the recovery cost of

income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.