Assessable Income and Expenditure Information Report 2022

VerifiedAdded on 2022/09/25

|13

|2886

|16

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Introduction:...............................................................................................................................2

Assessable Income and Expenditure Information:.....................................................................2

Part A: Income from Employment:............................................................................................3

Part B: Income and Expenses from business:............................................................................4

Income from Business:...............................................................................................................5

Part C: Income from Rental Property:.......................................................................................8

Dependent Tax offset:................................................................................................................9

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

Table of Contents

Introduction:...............................................................................................................................2

Assessable Income and Expenditure Information:.....................................................................2

Part A: Income from Employment:............................................................................................3

Part B: Income and Expenses from business:............................................................................4

Income from Business:...............................................................................................................5

Part C: Income from Rental Property:.......................................................................................8

Dependent Tax offset:................................................................................................................9

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

2TAXATION LAW

Introduction:

The report is associated with analysing the different types of transactions that are

reported by taxpayer to understand their inclusion in the tax return as income and determining

those expenses that will be allowed for deduction. The report is prepared by focusing on

different sources of taxation laws to ascertain whether Eric will be held assessable or not for

the invalid and invalid carer tax offset. The report will be computing the overall taxable

income of Eric will be considered assessable in agreement with the given provision of “ITAA

1997”.

Assessable Income and Expenditure Information:

Before computing the taxable earnings of Eric it is essential to have an understanding

of assessable income. The assessable earnings is a subject of assessment and it is added into

the taxable pay. The taxpayers should understand that ordinary income amounts to “income

in agreement with the ordinary conception” and it is treated chargeable within legislative

provision of “sec 6-5 ITAA 1997” (Smith, 2014). The case facts of Eric furnishes that he

held a joint term deposit with Linda his spouse in ANZ bank account and derived an interest

of 500 from that account. Interest constitute an “ordinary income” under “sec 6-5 ITAA

1997”. The commissioner in “Riches v Westminster Bank Ltd (1947)” explained that

interest is regarded as the return which streams from the advancing of money and the capital

sum that is not impacted by imbursement of interest (Smith, 2018). Likewise, the interest

which Eric has earned jointly with his wife in ANZ bank is included for assessment as

“ordinary income” under “sec 6-5 ITAA 1997”.

Expenditure that is paid by the taxpayer for management of tax affairs is given the

permission for deduction in “sec 25-5 (1) ITAA 1997”. A payment of $400 was paid to a

Introduction:

The report is associated with analysing the different types of transactions that are

reported by taxpayer to understand their inclusion in the tax return as income and determining

those expenses that will be allowed for deduction. The report is prepared by focusing on

different sources of taxation laws to ascertain whether Eric will be held assessable or not for

the invalid and invalid carer tax offset. The report will be computing the overall taxable

income of Eric will be considered assessable in agreement with the given provision of “ITAA

1997”.

Assessable Income and Expenditure Information:

Before computing the taxable earnings of Eric it is essential to have an understanding

of assessable income. The assessable earnings is a subject of assessment and it is added into

the taxable pay. The taxpayers should understand that ordinary income amounts to “income

in agreement with the ordinary conception” and it is treated chargeable within legislative

provision of “sec 6-5 ITAA 1997” (Smith, 2014). The case facts of Eric furnishes that he

held a joint term deposit with Linda his spouse in ANZ bank account and derived an interest

of 500 from that account. Interest constitute an “ordinary income” under “sec 6-5 ITAA

1997”. The commissioner in “Riches v Westminster Bank Ltd (1947)” explained that

interest is regarded as the return which streams from the advancing of money and the capital

sum that is not impacted by imbursement of interest (Smith, 2018). Likewise, the interest

which Eric has earned jointly with his wife in ANZ bank is included for assessment as

“ordinary income” under “sec 6-5 ITAA 1997”.

Expenditure that is paid by the taxpayer for management of tax affairs is given the

permission for deduction in “sec 25-5 (1) ITAA 1997”. A payment of $400 was paid to a

3TAXATION LAW

registered tax agent by Eric to prepare for his tax return for tax year of 2018. Therefore, the

tax agent payment is a permissible tax deduction in “sec 25-5 (1) ITAA 1997”.

Part A: Income from Employment:

Under “sec 6 (1) ITAA 1936”, earnings that is made by the taxpayer from individual

effort generally involves receipts that is earned through working as employee in an

employment. As noted in “McNeil v FC (2007)” whether or not the amount is an income is

dependent on the quality for those that receives the amount and it is not regarded as the

character of expenditure by other person (Diewert & Lawrence, 2015). This is important until

the payments which is received carries adequate nexus with the income of the recipient

employment and professional service and not on personal level. Eric earned a gross wages of

$7,800 from his employment. The gross wages of Eric is an earnings from personal exertion

under “sec 6 (1) ITAA 1936”. Denoting to “McNeil v FC (2007)” the gross wages which is

received by Eric carries adequate nexus with his income from employment and professional

service. Under “sec 6-5 ITA Act 97” it will be taxable as “ordinary income”.

There are common issues whether the payment made to the employee constitutes

allowances or reimbursement. Under the “sec 15-2 (1) ITAA 1997” allowance involves usual

“salary or wages” and hence it is not a “fringe benefit”. It is taxable to the employee

ordinary income. While reimbursement is not a salary and wages. It was established in

“Roads and Traffic Authority of New South Wales v FCT (1993)” usually, a reimbursement

is characterised as imbursement made for the actual expenditure.

A shift allowance of $2,000 was received during the year by Eric. Referring to “sec

15-2 (1) ITAA 1997” allowance involves usual “salary or wages” and hence it is not a

“fringe benefit”. It is included in the taxable earnings of Eric for tax purpose. Eric was also

reimbursed for work related software fees by his employer (Wales, 2017). The

registered tax agent by Eric to prepare for his tax return for tax year of 2018. Therefore, the

tax agent payment is a permissible tax deduction in “sec 25-5 (1) ITAA 1997”.

Part A: Income from Employment:

Under “sec 6 (1) ITAA 1936”, earnings that is made by the taxpayer from individual

effort generally involves receipts that is earned through working as employee in an

employment. As noted in “McNeil v FC (2007)” whether or not the amount is an income is

dependent on the quality for those that receives the amount and it is not regarded as the

character of expenditure by other person (Diewert & Lawrence, 2015). This is important until

the payments which is received carries adequate nexus with the income of the recipient

employment and professional service and not on personal level. Eric earned a gross wages of

$7,800 from his employment. The gross wages of Eric is an earnings from personal exertion

under “sec 6 (1) ITAA 1936”. Denoting to “McNeil v FC (2007)” the gross wages which is

received by Eric carries adequate nexus with his income from employment and professional

service. Under “sec 6-5 ITA Act 97” it will be taxable as “ordinary income”.

There are common issues whether the payment made to the employee constitutes

allowances or reimbursement. Under the “sec 15-2 (1) ITAA 1997” allowance involves usual

“salary or wages” and hence it is not a “fringe benefit”. It is taxable to the employee

ordinary income. While reimbursement is not a salary and wages. It was established in

“Roads and Traffic Authority of New South Wales v FCT (1993)” usually, a reimbursement

is characterised as imbursement made for the actual expenditure.

A shift allowance of $2,000 was received during the year by Eric. Referring to “sec

15-2 (1) ITAA 1997” allowance involves usual “salary or wages” and hence it is not a

“fringe benefit”. It is included in the taxable earnings of Eric for tax purpose. Eric was also

reimbursed for work related software fees by his employer (Wales, 2017). The

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

reimbursement received by Eric is not a salary and wages. Denoting “Roads and Traffic

Authority of New South Wales v FCT (1993)” the reimbursement made to Eric is

characterised as imbursement made for the actual expenditure.

A car fringe benefit only takes place upon the receipt of car by employee from the

employer regarding their private usage under “sec 7 (1)”. When the employer gives the

employee with the benefit then it becomes “non-taxable earnings” for the employee under

“sec 23L ITAA 1936”. The employer in such condition is required to FBT regarding the

value of benefit. Eric has been a car by his employer (McCluskey & Franzsen, 2017). Under

the “sec 7 (1)” receipt of car by Eric is a car fringe benefit. The car is “non-taxable

earnings” for Eric under “sec 23L ITAA 1936”. The employer Merlin Blue is required to

FBT concerning the value of benefit.

Fringe Benefit

Particulars Amount ($)

Value of car $60,000

FBT Gross up rate 1.8868

Taxable value of car FBT $113,208

The positive limbs given in “sec 8-1 ITAA 1997” says that a deduction from the

taxpayers taxable income is permitted for any “loss or outgoing” till the amount it is

experienced in producing taxable earnings or it is has happened in conducting any business

activities for earning taxable earnings (Arnold et al., 2019). Eric has incurred work related

telephone and stationary expenditure of $300. A general deduction under “sec 8-1 ITAA

1997” is allowable for same to Eric.

Part B: Income and Expenses from business:

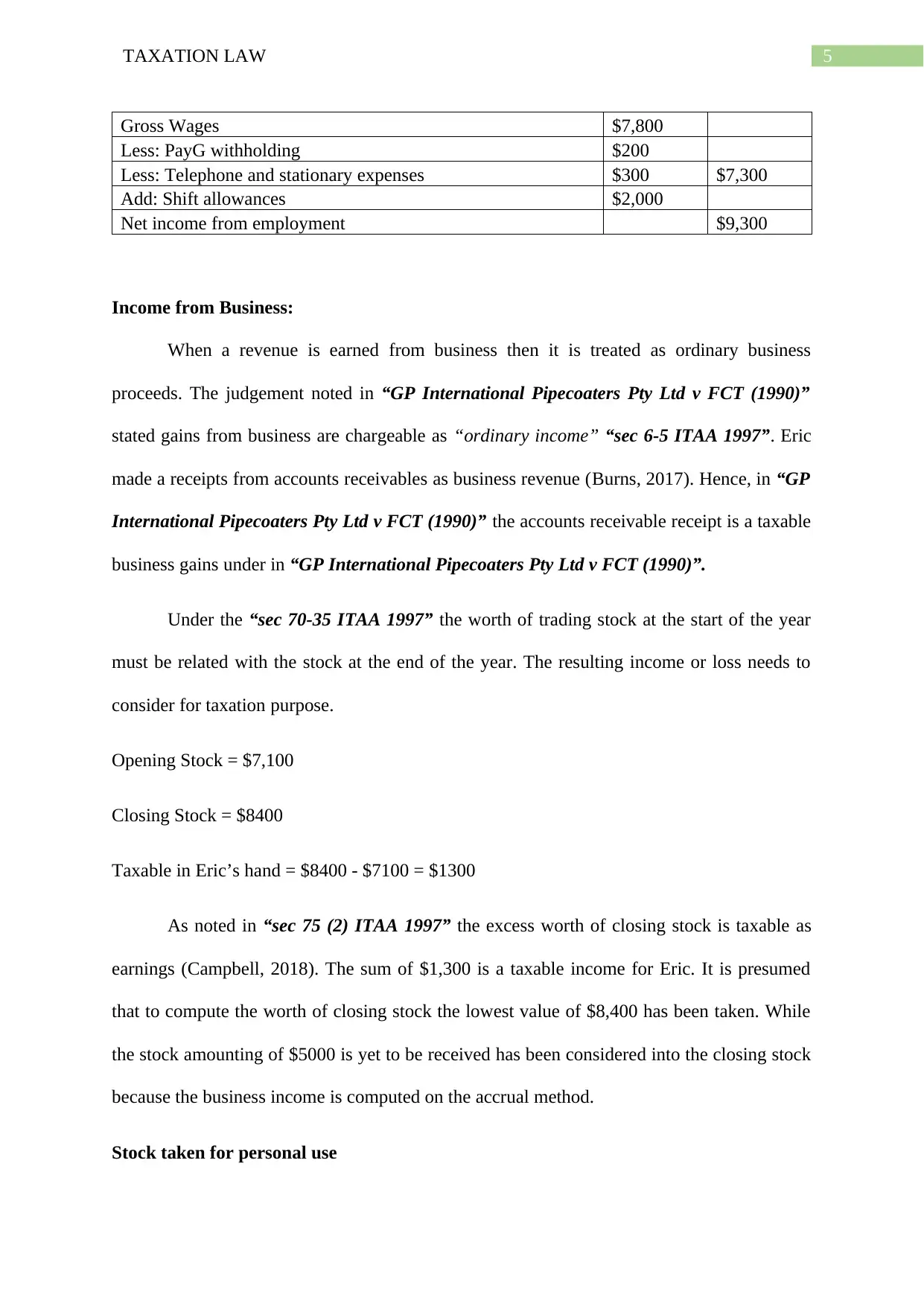

Income From Employment

Particulars Amount ($) Amount ($)

Assessable Income

reimbursement received by Eric is not a salary and wages. Denoting “Roads and Traffic

Authority of New South Wales v FCT (1993)” the reimbursement made to Eric is

characterised as imbursement made for the actual expenditure.

A car fringe benefit only takes place upon the receipt of car by employee from the

employer regarding their private usage under “sec 7 (1)”. When the employer gives the

employee with the benefit then it becomes “non-taxable earnings” for the employee under

“sec 23L ITAA 1936”. The employer in such condition is required to FBT regarding the

value of benefit. Eric has been a car by his employer (McCluskey & Franzsen, 2017). Under

the “sec 7 (1)” receipt of car by Eric is a car fringe benefit. The car is “non-taxable

earnings” for Eric under “sec 23L ITAA 1936”. The employer Merlin Blue is required to

FBT concerning the value of benefit.

Fringe Benefit

Particulars Amount ($)

Value of car $60,000

FBT Gross up rate 1.8868

Taxable value of car FBT $113,208

The positive limbs given in “sec 8-1 ITAA 1997” says that a deduction from the

taxpayers taxable income is permitted for any “loss or outgoing” till the amount it is

experienced in producing taxable earnings or it is has happened in conducting any business

activities for earning taxable earnings (Arnold et al., 2019). Eric has incurred work related

telephone and stationary expenditure of $300. A general deduction under “sec 8-1 ITAA

1997” is allowable for same to Eric.

Part B: Income and Expenses from business:

Income From Employment

Particulars Amount ($) Amount ($)

Assessable Income

5TAXATION LAW

Gross Wages $7,800

Less: PayG withholding $200

Less: Telephone and stationary expenses $300 $7,300

Add: Shift allowances $2,000

Net income from employment $9,300

Income from Business:

When a revenue is earned from business then it is treated as ordinary business

proceeds. The judgement noted in “GP International Pipecoaters Pty Ltd v FCT (1990)”

stated gains from business are chargeable as “ordinary income” “sec 6-5 ITAA 1997”. Eric

made a receipts from accounts receivables as business revenue (Burns, 2017). Hence, in “GP

International Pipecoaters Pty Ltd v FCT (1990)” the accounts receivable receipt is a taxable

business gains under in “GP International Pipecoaters Pty Ltd v FCT (1990)”.

Under the “sec 70-35 ITAA 1997” the worth of trading stock at the start of the year

must be related with the stock at the end of the year. The resulting income or loss needs to

consider for taxation purpose.

Opening Stock = $7,100

Closing Stock = $8400

Taxable in Eric’s hand = $8400 - $7100 = $1300

As noted in “sec 75 (2) ITAA 1997” the excess worth of closing stock is taxable as

earnings (Campbell, 2018). The sum of $1,300 is a taxable income for Eric. It is presumed

that to compute the worth of closing stock the lowest value of $8,400 has been taken. While

the stock amounting of $5000 is yet to be received has been considered into the closing stock

because the business income is computed on the accrual method.

Stock taken for personal use

Gross Wages $7,800

Less: PayG withholding $200

Less: Telephone and stationary expenses $300 $7,300

Add: Shift allowances $2,000

Net income from employment $9,300

Income from Business:

When a revenue is earned from business then it is treated as ordinary business

proceeds. The judgement noted in “GP International Pipecoaters Pty Ltd v FCT (1990)”

stated gains from business are chargeable as “ordinary income” “sec 6-5 ITAA 1997”. Eric

made a receipts from accounts receivables as business revenue (Burns, 2017). Hence, in “GP

International Pipecoaters Pty Ltd v FCT (1990)” the accounts receivable receipt is a taxable

business gains under in “GP International Pipecoaters Pty Ltd v FCT (1990)”.

Under the “sec 70-35 ITAA 1997” the worth of trading stock at the start of the year

must be related with the stock at the end of the year. The resulting income or loss needs to

consider for taxation purpose.

Opening Stock = $7,100

Closing Stock = $8400

Taxable in Eric’s hand = $8400 - $7100 = $1300

As noted in “sec 75 (2) ITAA 1997” the excess worth of closing stock is taxable as

earnings (Campbell, 2018). The sum of $1,300 is a taxable income for Eric. It is presumed

that to compute the worth of closing stock the lowest value of $8,400 has been taken. While

the stock amounting of $5000 is yet to be received has been considered into the closing stock

because the business income is computed on the accrual method.

Stock taken for personal use

6TAXATION LAW

If a person takes the business stock purchased for the purpose of sale in business for

their private usage and consumption, then the value of such stock taken will be considered as

sold (Davis et al., 2019). The case facts obtained suggest that a stock valuing $2,500 has been

taken by Eric for his personal consumption. The value of such stock drawn is included in the

sales amount.

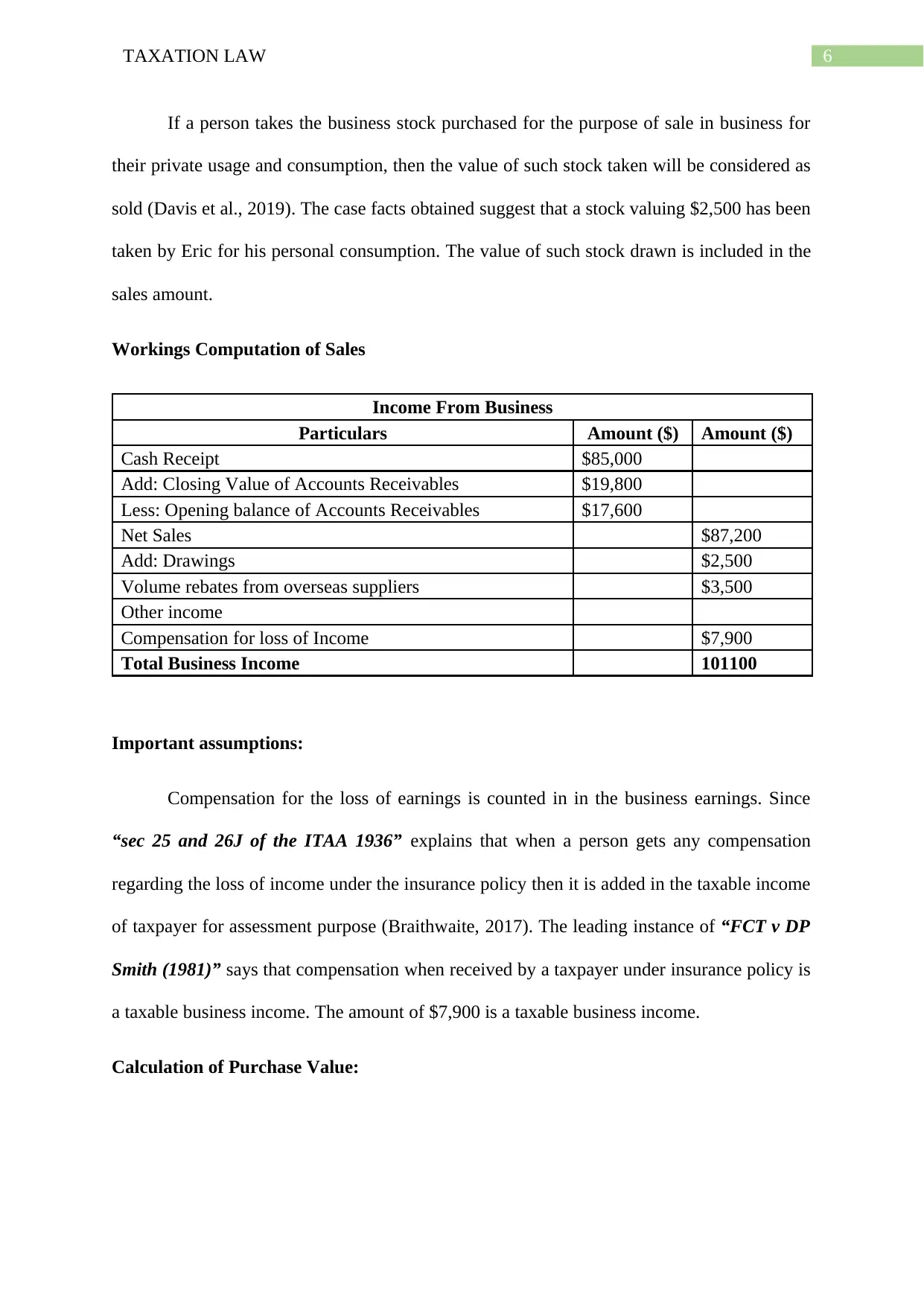

Workings Computation of Sales

Income From Business

Particulars Amount ($) Amount ($)

Cash Receipt $85,000

Add: Closing Value of Accounts Receivables $19,800

Less: Opening balance of Accounts Receivables $17,600

Net Sales $87,200

Add: Drawings $2,500

Volume rebates from overseas suppliers $3,500

Other income

Compensation for loss of Income $7,900

Total Business Income 101100

Important assumptions:

Compensation for the loss of earnings is counted in in the business earnings. Since

“sec 25 and 26J of the ITAA 1936” explains that when a person gets any compensation

regarding the loss of income under the insurance policy then it is added in the taxable income

of taxpayer for assessment purpose (Braithwaite, 2017). The leading instance of “FCT v DP

Smith (1981)” says that compensation when received by a taxpayer under insurance policy is

a taxable business income. The amount of $7,900 is a taxable business income.

Calculation of Purchase Value:

If a person takes the business stock purchased for the purpose of sale in business for

their private usage and consumption, then the value of such stock taken will be considered as

sold (Davis et al., 2019). The case facts obtained suggest that a stock valuing $2,500 has been

taken by Eric for his personal consumption. The value of such stock drawn is included in the

sales amount.

Workings Computation of Sales

Income From Business

Particulars Amount ($) Amount ($)

Cash Receipt $85,000

Add: Closing Value of Accounts Receivables $19,800

Less: Opening balance of Accounts Receivables $17,600

Net Sales $87,200

Add: Drawings $2,500

Volume rebates from overseas suppliers $3,500

Other income

Compensation for loss of Income $7,900

Total Business Income 101100

Important assumptions:

Compensation for the loss of earnings is counted in in the business earnings. Since

“sec 25 and 26J of the ITAA 1936” explains that when a person gets any compensation

regarding the loss of income under the insurance policy then it is added in the taxable income

of taxpayer for assessment purpose (Braithwaite, 2017). The leading instance of “FCT v DP

Smith (1981)” says that compensation when received by a taxpayer under insurance policy is

a taxable business income. The amount of $7,900 is a taxable business income.

Calculation of Purchase Value:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

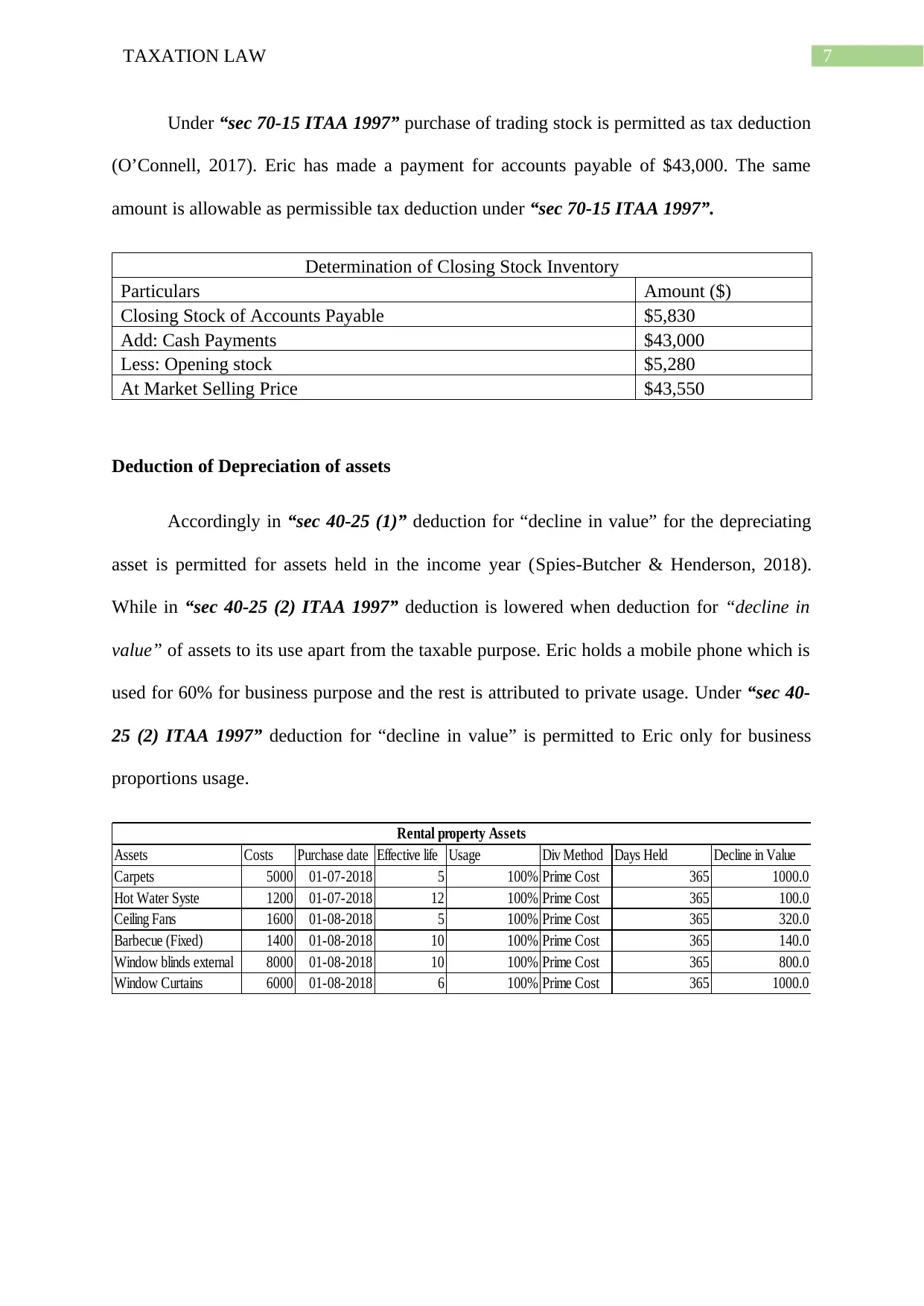

Under “sec 70-15 ITAA 1997” purchase of trading stock is permitted as tax deduction

(O’Connell, 2017). Eric has made a payment for accounts payable of $43,000. The same

amount is allowable as permissible tax deduction under “sec 70-15 ITAA 1997”.

Determination of Closing Stock Inventory

Particulars Amount ($)

Closing Stock of Accounts Payable $5,830

Add: Cash Payments $43,000

Less: Opening stock $5,280

At Market Selling Price $43,550

Deduction of Depreciation of assets

Accordingly in “sec 40-25 (1)” deduction for “decline in value” for the depreciating

asset is permitted for assets held in the income year (Spies-Butcher & Henderson, 2018).

While in “sec 40-25 (2) ITAA 1997” deduction is lowered when deduction for “decline in

value” of assets to its use apart from the taxable purpose. Eric holds a mobile phone which is

used for 60% for business purpose and the rest is attributed to private usage. Under “sec 40-

25 (2) ITAA 1997” deduction for “decline in value” is permitted to Eric only for business

proportions usage.

Assets Costs Purchase date Effective life Usage Div Method Days Held Decline in Value

Carpets 5000 01-07-2018 5 100% Prime Cost 365 1000.0

Hot Water Syste 1200 01-07-2018 12 100% Prime Cost 365 100.0

Ceiling Fans 1600 01-08-2018 5 100% Prime Cost 365 320.0

Barbecue (Fixed) 1400 01-08-2018 10 100% Prime Cost 365 140.0

Window blinds external 8000 01-08-2018 10 100% Prime Cost 365 800.0

Window Curtains 6000 01-08-2018 6 100% Prime Cost 365 1000.0

Rental property Assets

Under “sec 70-15 ITAA 1997” purchase of trading stock is permitted as tax deduction

(O’Connell, 2017). Eric has made a payment for accounts payable of $43,000. The same

amount is allowable as permissible tax deduction under “sec 70-15 ITAA 1997”.

Determination of Closing Stock Inventory

Particulars Amount ($)

Closing Stock of Accounts Payable $5,830

Add: Cash Payments $43,000

Less: Opening stock $5,280

At Market Selling Price $43,550

Deduction of Depreciation of assets

Accordingly in “sec 40-25 (1)” deduction for “decline in value” for the depreciating

asset is permitted for assets held in the income year (Spies-Butcher & Henderson, 2018).

While in “sec 40-25 (2) ITAA 1997” deduction is lowered when deduction for “decline in

value” of assets to its use apart from the taxable purpose. Eric holds a mobile phone which is

used for 60% for business purpose and the rest is attributed to private usage. Under “sec 40-

25 (2) ITAA 1997” deduction for “decline in value” is permitted to Eric only for business

proportions usage.

Assets Costs Purchase date Effective life Usage Div Method Days Held Decline in Value

Carpets 5000 01-07-2018 5 100% Prime Cost 365 1000.0

Hot Water Syste 1200 01-07-2018 12 100% Prime Cost 365 100.0

Ceiling Fans 1600 01-08-2018 5 100% Prime Cost 365 320.0

Barbecue (Fixed) 1400 01-08-2018 10 100% Prime Cost 365 140.0

Window blinds external 8000 01-08-2018 10 100% Prime Cost 365 800.0

Window Curtains 6000 01-08-2018 6 100% Prime Cost 365 1000.0

Rental property Assets

8TAXATION LAW

Part C: Income from Rental Property:

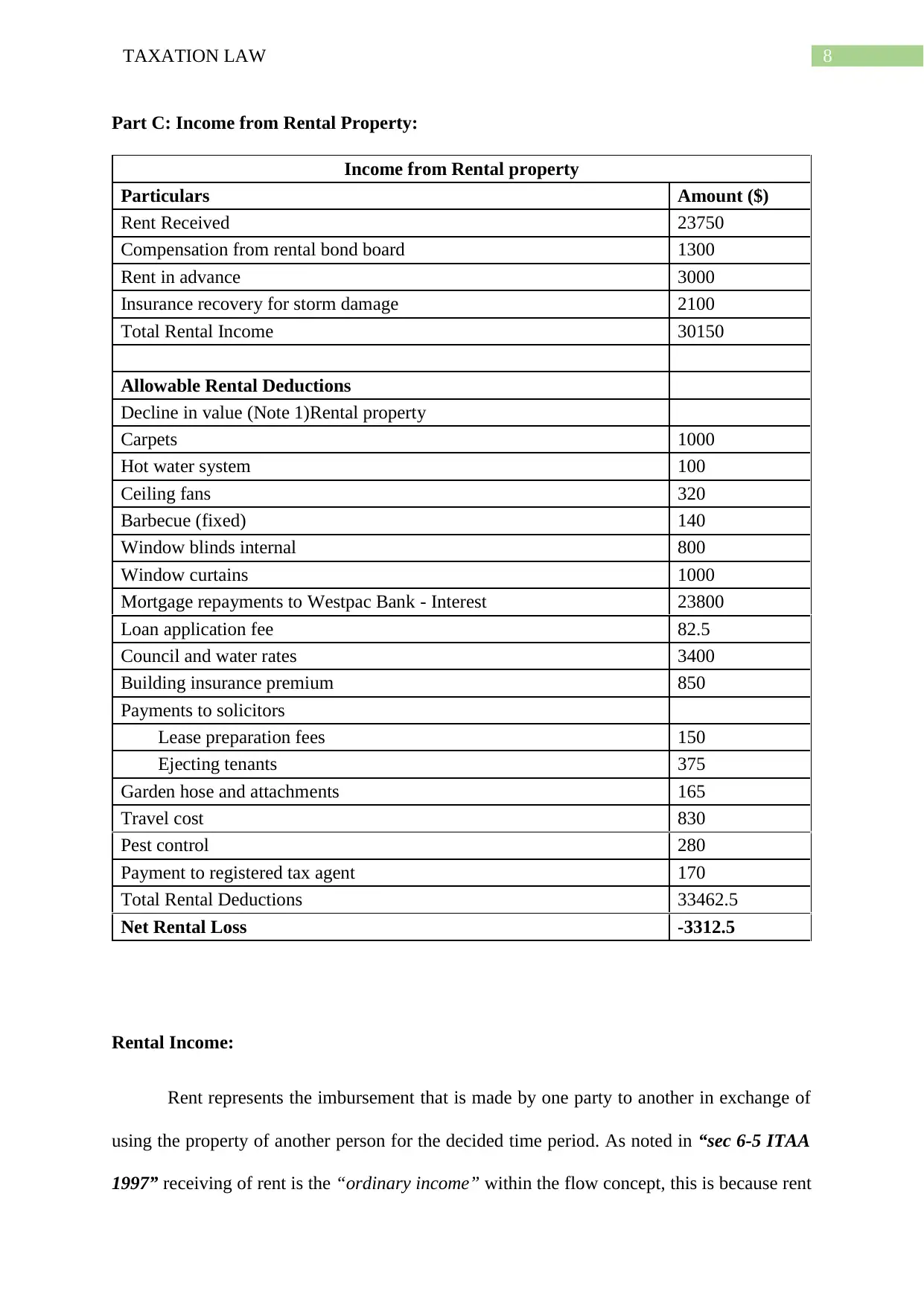

Income from Rental property

Particulars Amount ($)

Rent Received 23750

Compensation from rental bond board 1300

Rent in advance 3000

Insurance recovery for storm damage 2100

Total Rental Income 30150

Allowable Rental Deductions

Decline in value (Note 1)Rental property

Carpets 1000

Hot water system 100

Ceiling fans 320

Barbecue (fixed) 140

Window blinds internal 800

Window curtains 1000

Mortgage repayments to Westpac Bank - Interest 23800

Loan application fee 82.5

Council and water rates 3400

Building insurance premium 850

Payments to solicitors

Lease preparation fees 150

Ejecting tenants 375

Garden hose and attachments 165

Travel cost 830

Pest control 280

Payment to registered tax agent 170

Total Rental Deductions 33462.5

Net Rental Loss -3312.5

Rental Income:

Rent represents the imbursement that is made by one party to another in exchange of

using the property of another person for the decided time period. As noted in “sec 6-5 ITAA

1997” receiving of rent is the “ordinary income” within the flow concept, this is because rent

Part C: Income from Rental Property:

Income from Rental property

Particulars Amount ($)

Rent Received 23750

Compensation from rental bond board 1300

Rent in advance 3000

Insurance recovery for storm damage 2100

Total Rental Income 30150

Allowable Rental Deductions

Decline in value (Note 1)Rental property

Carpets 1000

Hot water system 100

Ceiling fans 320

Barbecue (fixed) 140

Window blinds internal 800

Window curtains 1000

Mortgage repayments to Westpac Bank - Interest 23800

Loan application fee 82.5

Council and water rates 3400

Building insurance premium 850

Payments to solicitors

Lease preparation fees 150

Ejecting tenants 375

Garden hose and attachments 165

Travel cost 830

Pest control 280

Payment to registered tax agent 170

Total Rental Deductions 33462.5

Net Rental Loss -3312.5

Rental Income:

Rent represents the imbursement that is made by one party to another in exchange of

using the property of another person for the decided time period. As noted in “sec 6-5 ITAA

1997” receiving of rent is the “ordinary income” within the flow concept, this is because rent

9TAXATION LAW

streams from the investment property (Butler, 2019). Eric has earned rent of $23,750 during

the year from rental property. The rent is an “ordinary income” for Eric and assessable under

“sec 6-5 ITAA 1997”.

Deduction for repairs:

As per “subsec 25-10 (1)” repairs is permitted for deduction occurred by taxpayer on

the property which the taxpayer holds for generating income. Under “sec 25-10 (3) ITAA

1997” initial repairs will be considered as capital in nature completely when it is conducted

on the newly purchased item since the cost of item is regarded as the part of purchase price to

function the item. In “Law Shipping Co Ltd v CIR (1924)” deduction for initial repairs were

denied to taxpayer for ship that was in a state of significant repair (Yuan, 2016). Eric carried

out repairs by painting the outside walls of house on 10th July soon after its acquisition.

Referring “Law Shipping Co Ltd v CIR (1924)” the painting done by Eric is an initial repair.

Within the “sec 25-10 (3) ITAA 1997” no deduction will be permitted to Eric in this case.

Deduction for borrowing expenses:

Under “section 25-25(3) of ITA Act 1997” a taxpayer is permitted to obtain

deduction for borrowing expenses over numerous years that relates rental property

(O’Connell, 2017). If the total borrowing expenditures is more than $100 then a deduction is

spread over five years. A loan application fee of $825 has been occurred by Eric for rental

property. Eric can obtain a deduction for loan application fee should be spread over the term

of loan.

Dependent Tax offset:

As stated by the ATO a dependent tax offset is allowed to those that maintain their

spouse who is invalid or those that cares for the invalid. A carer should have care for their

spouse’s invalid child, brother or sister that is below 16 years (Butler, 2019). The carer

streams from the investment property (Butler, 2019). Eric has earned rent of $23,750 during

the year from rental property. The rent is an “ordinary income” for Eric and assessable under

“sec 6-5 ITAA 1997”.

Deduction for repairs:

As per “subsec 25-10 (1)” repairs is permitted for deduction occurred by taxpayer on

the property which the taxpayer holds for generating income. Under “sec 25-10 (3) ITAA

1997” initial repairs will be considered as capital in nature completely when it is conducted

on the newly purchased item since the cost of item is regarded as the part of purchase price to

function the item. In “Law Shipping Co Ltd v CIR (1924)” deduction for initial repairs were

denied to taxpayer for ship that was in a state of significant repair (Yuan, 2016). Eric carried

out repairs by painting the outside walls of house on 10th July soon after its acquisition.

Referring “Law Shipping Co Ltd v CIR (1924)” the painting done by Eric is an initial repair.

Within the “sec 25-10 (3) ITAA 1997” no deduction will be permitted to Eric in this case.

Deduction for borrowing expenses:

Under “section 25-25(3) of ITA Act 1997” a taxpayer is permitted to obtain

deduction for borrowing expenses over numerous years that relates rental property

(O’Connell, 2017). If the total borrowing expenditures is more than $100 then a deduction is

spread over five years. A loan application fee of $825 has been occurred by Eric for rental

property. Eric can obtain a deduction for loan application fee should be spread over the term

of loan.

Dependent Tax offset:

As stated by the ATO a dependent tax offset is allowed to those that maintain their

spouse who is invalid or those that cares for the invalid. A carer should have care for their

spouse’s invalid child, brother or sister that is below 16 years (Butler, 2019). The carer

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

should receive a carer imbursement or carer allowance within “Social Security Act 1991”. A

deduction is only permitted for their spouse that has total income of $11,346 and the carer

adjustable income is not greater than $100,000.

Similarly, Eric will be permitted to claim an invalid tax offset for his spouse because,

Linda receives a social disability payment of $9,200 and Eric’s taxable is not greater than

$100,000. Therefore, a dependent tax offset is permitted to Eric.

Conclusion:

The circumstance can be settled by stating that Eric will be assessable for his

employment, business receipts and rental income. While an invalid tax offset will be

permitted to Eric for being the carer of his wife Linda.

should receive a carer imbursement or carer allowance within “Social Security Act 1991”. A

deduction is only permitted for their spouse that has total income of $11,346 and the carer

adjustable income is not greater than $100,000.

Similarly, Eric will be permitted to claim an invalid tax offset for his spouse because,

Linda receives a social disability payment of $9,200 and Eric’s taxable is not greater than

$100,000. Therefore, a dependent tax offset is permitted to Eric.

Conclusion:

The circumstance can be settled by stating that Eric will be assessable for his

employment, business receipts and rental income. While an invalid tax offset will be

permitted to Eric for being the carer of his wife Linda.

11TAXATION LAW

References:

Smith, J. P. (2014). Taxing popularity: The story of taxation in Australia. Australian Tax

Research Foundation Research Studies, viii.

Smith, J. (2018). Gambling taxation in Australia. Australian Tax Research Foundation

Research Studies, 109.

Diewert, W. E., & Lawrence, D. (2015). The deadweight costs of capital taxation in

Australia. In Efficiency in the public sector (pp. 103-167). Springer, Boston, MA.

Wales, N. S. (2017). TAXATION IN AUSTRALIA| MARCH 2017 452.

McCluskey, W. J., & Franzsen, R. C. (2017). Land value taxation: An applied analysis.

Routledge.

Arnold, B. J., Ault, H. J., & Cooper, G. (Eds.). (2019). Comparative income taxation: a

structural analysis. Kluwer Law International BV.

Burns, A. (2017). Mid market focus: Tax considerations when doing business

offshore. Taxation in Australia, 51(10), 535.

Campbell, S. (2018). Personal liability of a trustee to tax on trust income: Part 1. Taxation in

Australia, 53(5), 263.

Davis, G., Akroyd, P., Pearl, D., & Sainsbury, T. (2019). Recent personal income tax

progressivity trends in Australia (No. 2019-05). Treasury Working Paper.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

O’Connell, A. (2017). Australia. In Capital Gains Taxation. Edward Elgar Publishing.

Spies-Butcher, B., & Henderson, T. (2018). Towards Basic Income in Australia.

References:

Smith, J. P. (2014). Taxing popularity: The story of taxation in Australia. Australian Tax

Research Foundation Research Studies, viii.

Smith, J. (2018). Gambling taxation in Australia. Australian Tax Research Foundation

Research Studies, 109.

Diewert, W. E., & Lawrence, D. (2015). The deadweight costs of capital taxation in

Australia. In Efficiency in the public sector (pp. 103-167). Springer, Boston, MA.

Wales, N. S. (2017). TAXATION IN AUSTRALIA| MARCH 2017 452.

McCluskey, W. J., & Franzsen, R. C. (2017). Land value taxation: An applied analysis.

Routledge.

Arnold, B. J., Ault, H. J., & Cooper, G. (Eds.). (2019). Comparative income taxation: a

structural analysis. Kluwer Law International BV.

Burns, A. (2017). Mid market focus: Tax considerations when doing business

offshore. Taxation in Australia, 51(10), 535.

Campbell, S. (2018). Personal liability of a trustee to tax on trust income: Part 1. Taxation in

Australia, 53(5), 263.

Davis, G., Akroyd, P., Pearl, D., & Sainsbury, T. (2019). Recent personal income tax

progressivity trends in Australia (No. 2019-05). Treasury Working Paper.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

O’Connell, A. (2017). Australia. In Capital Gains Taxation. Edward Elgar Publishing.

Spies-Butcher, B., & Henderson, T. (2018). Towards Basic Income in Australia.

12TAXATION LAW

Butler, D. (2019). Who can provide taxation advice?. Taxation in Australia, 53(7), 381.

Yuan, H. (2016). Mid market focus: The sharing economy and taxation. Taxation in

Australia, 51(6), 293.

Butler, D. (2019). Who can provide taxation advice?. Taxation in Australia, 53(7), 381.

Yuan, H. (2016). Mid market focus: The sharing economy and taxation. Taxation in

Australia, 51(6), 293.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.