Assessment 1: Financial Accounting for Linda's Sole Trader Business

VerifiedAdded on 2022/12/29

|16

|2596

|57

Homework Assignment

AI Summary

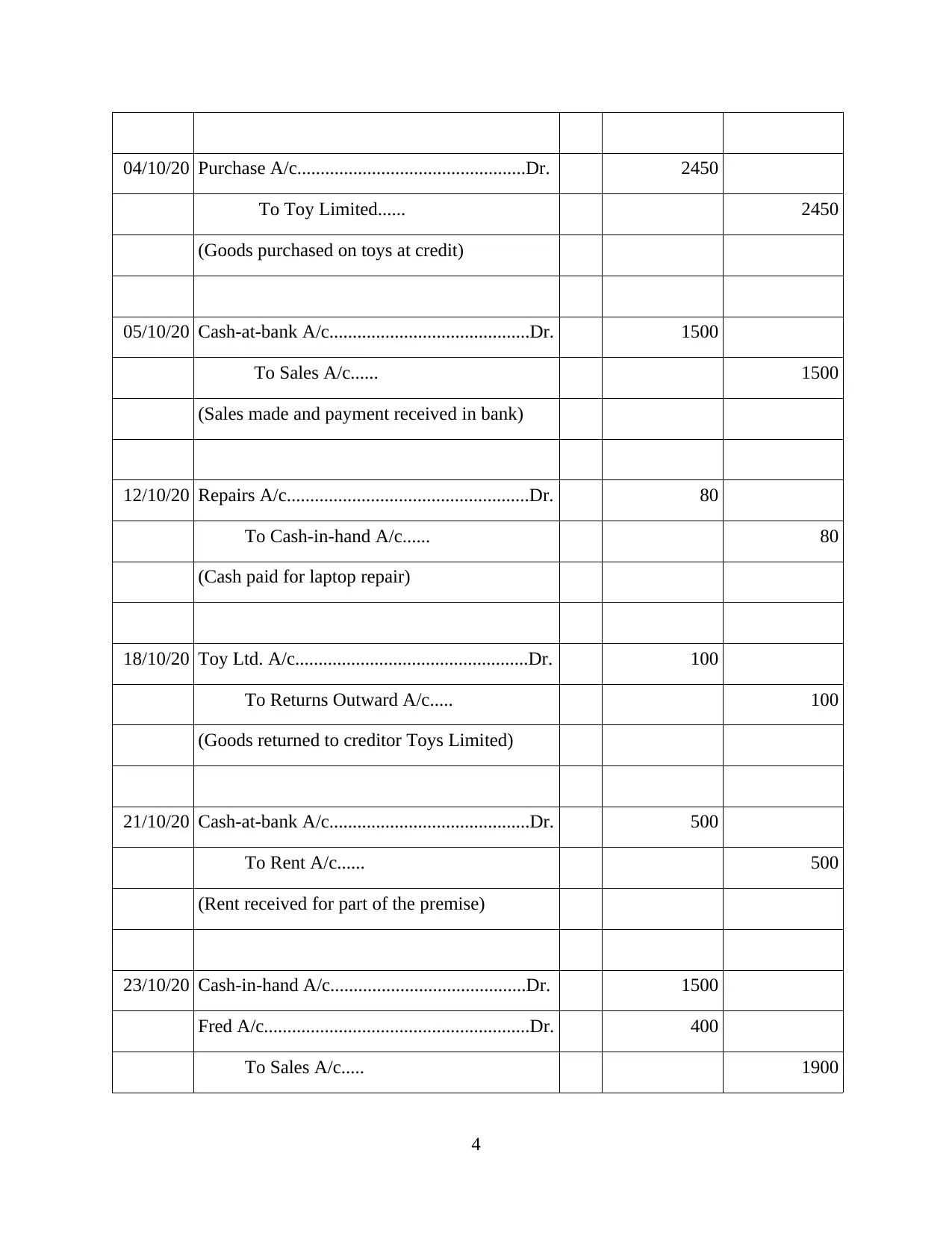

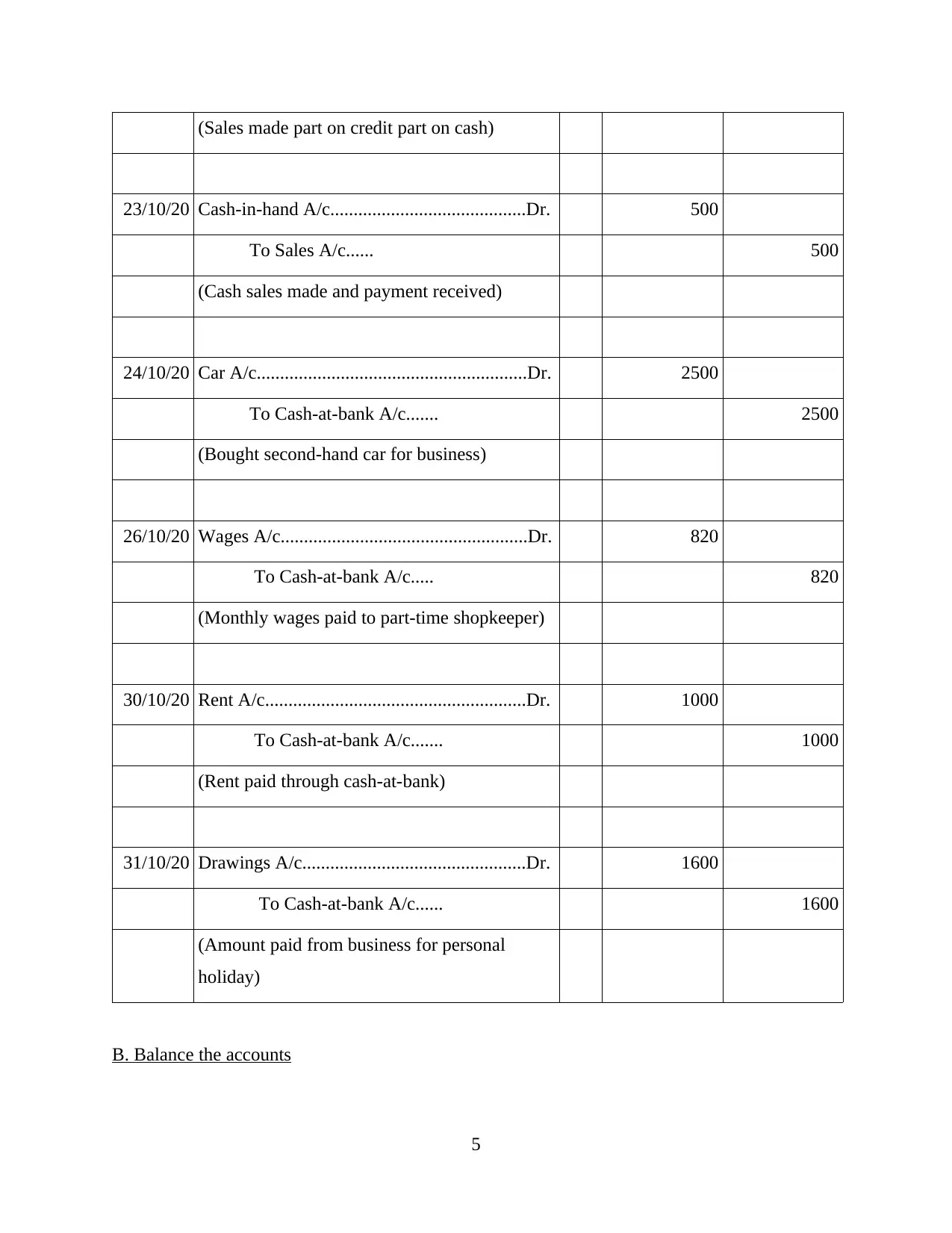

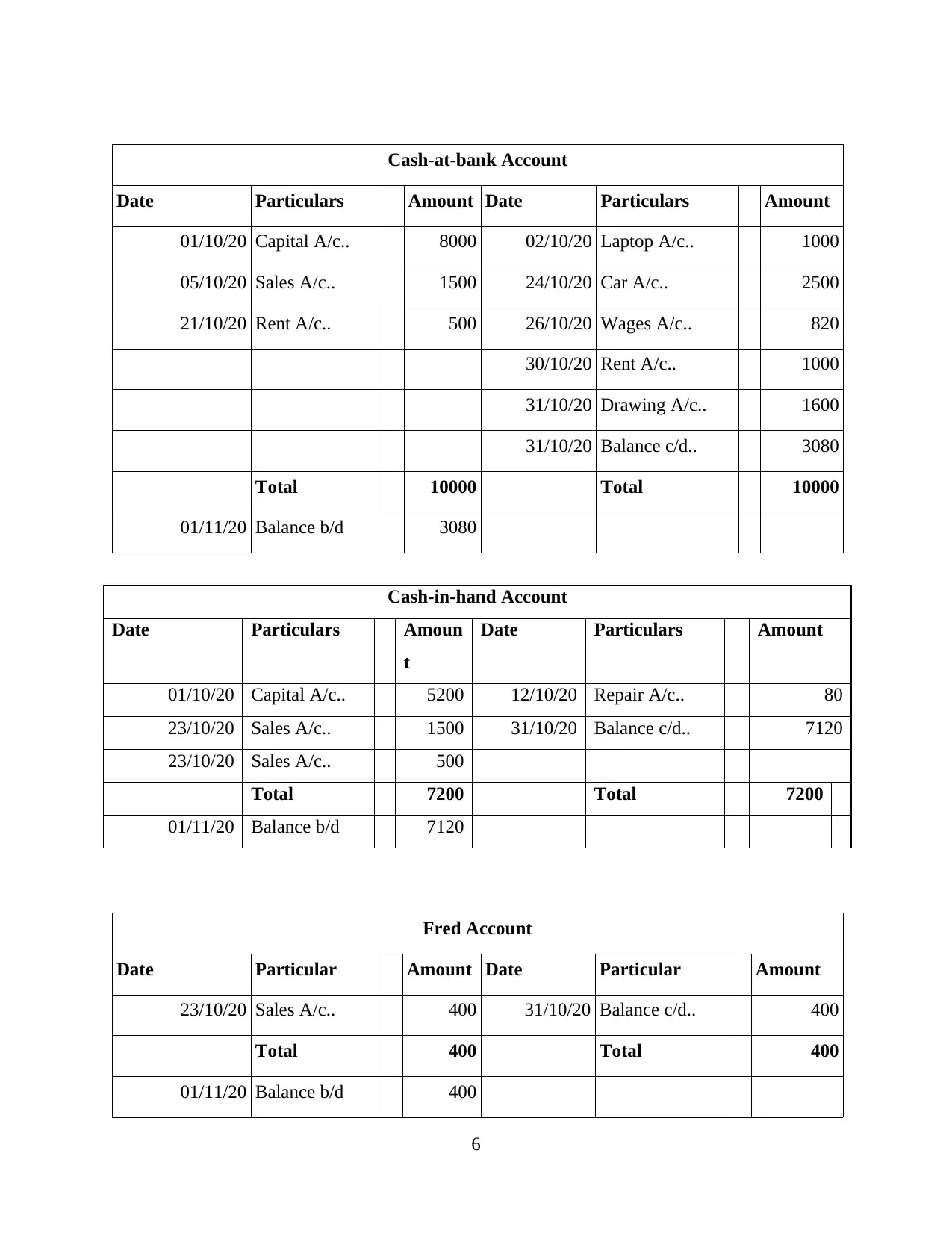

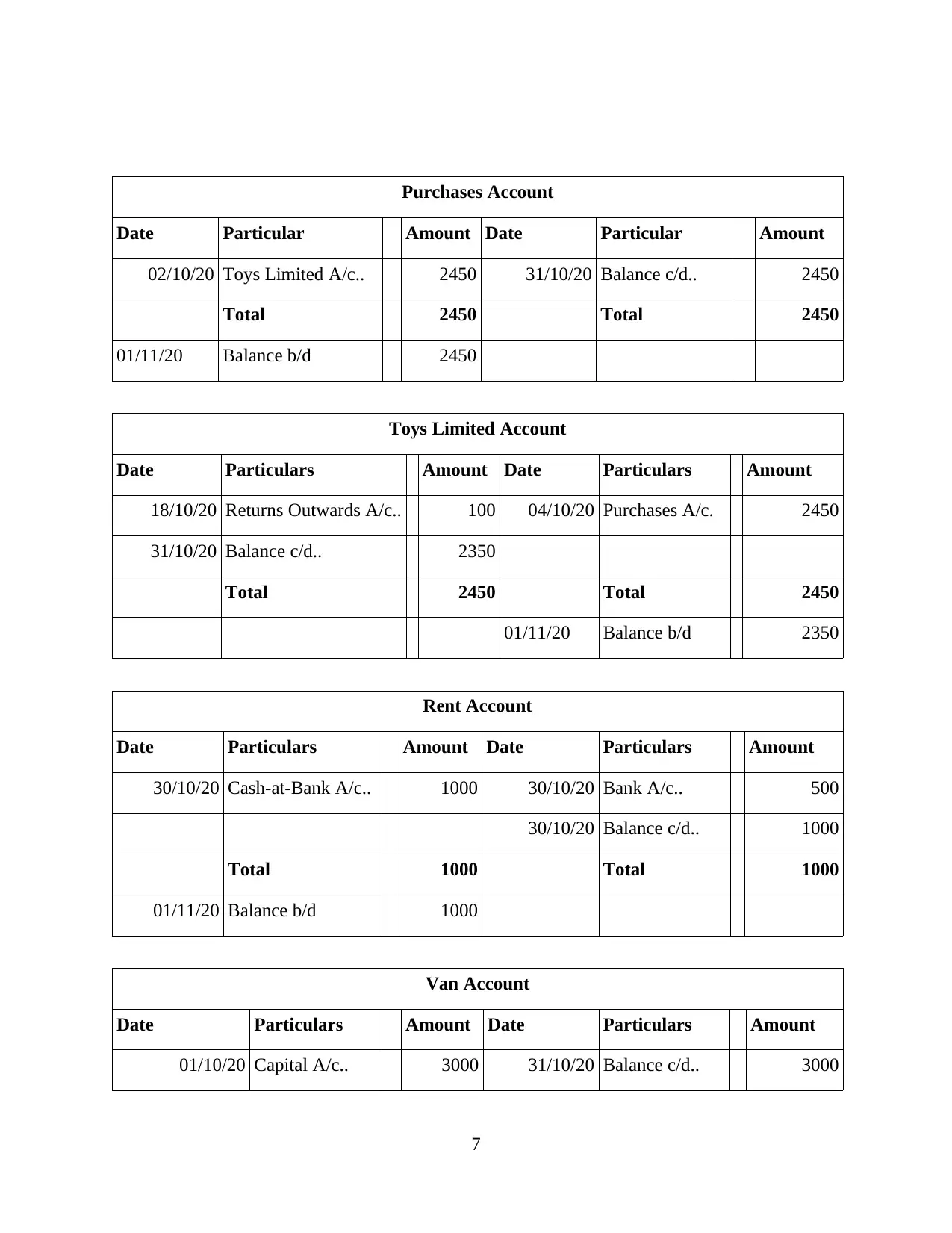

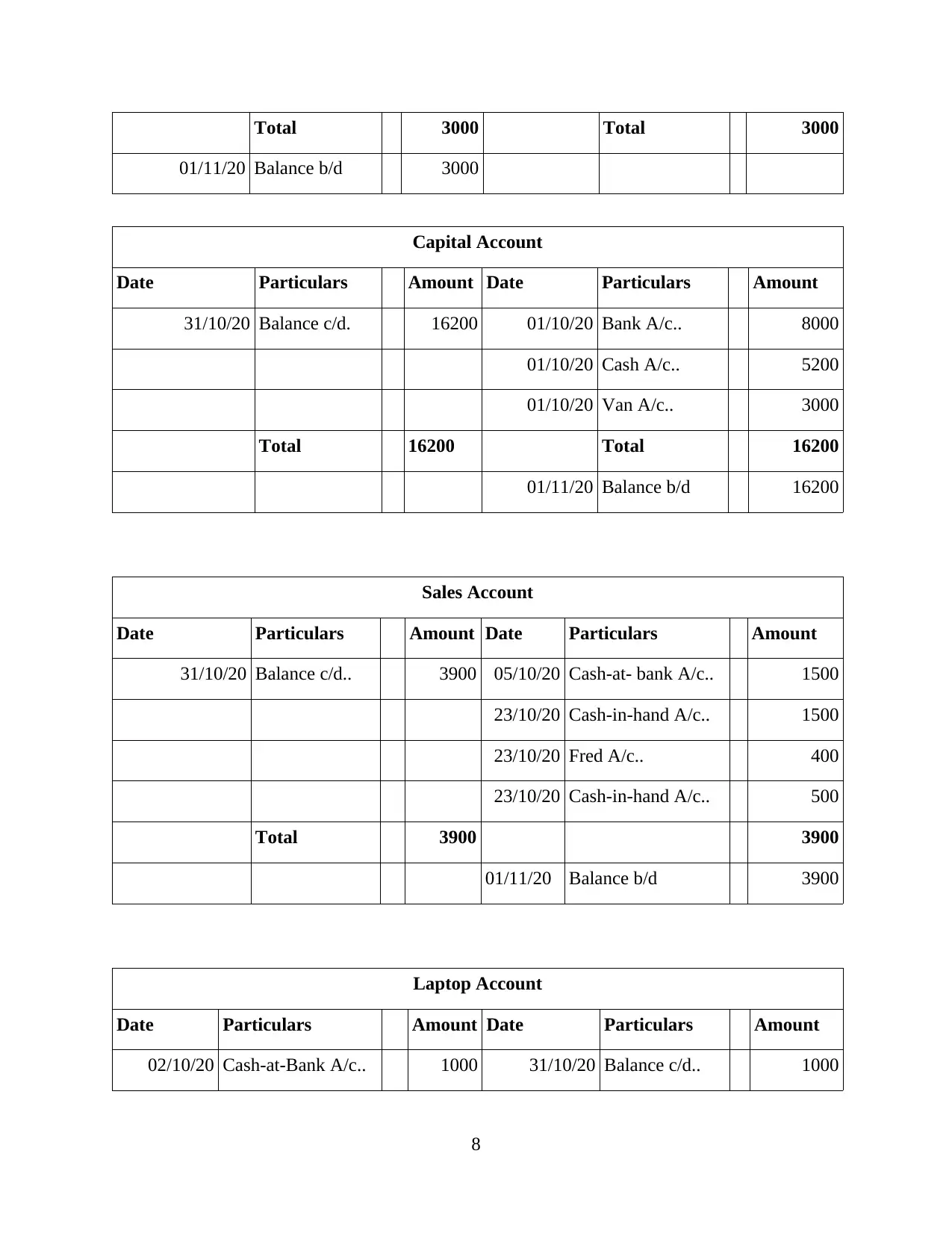

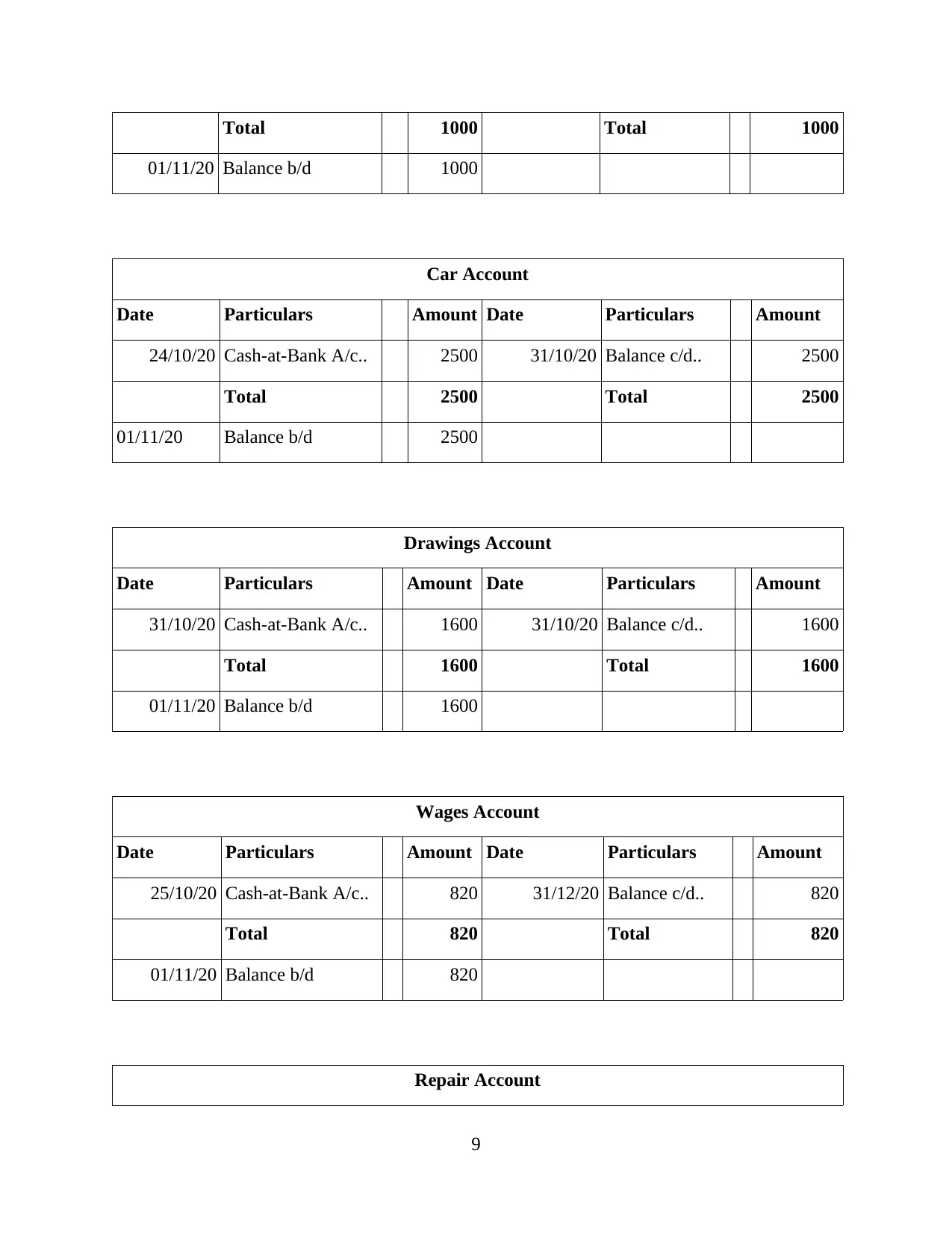

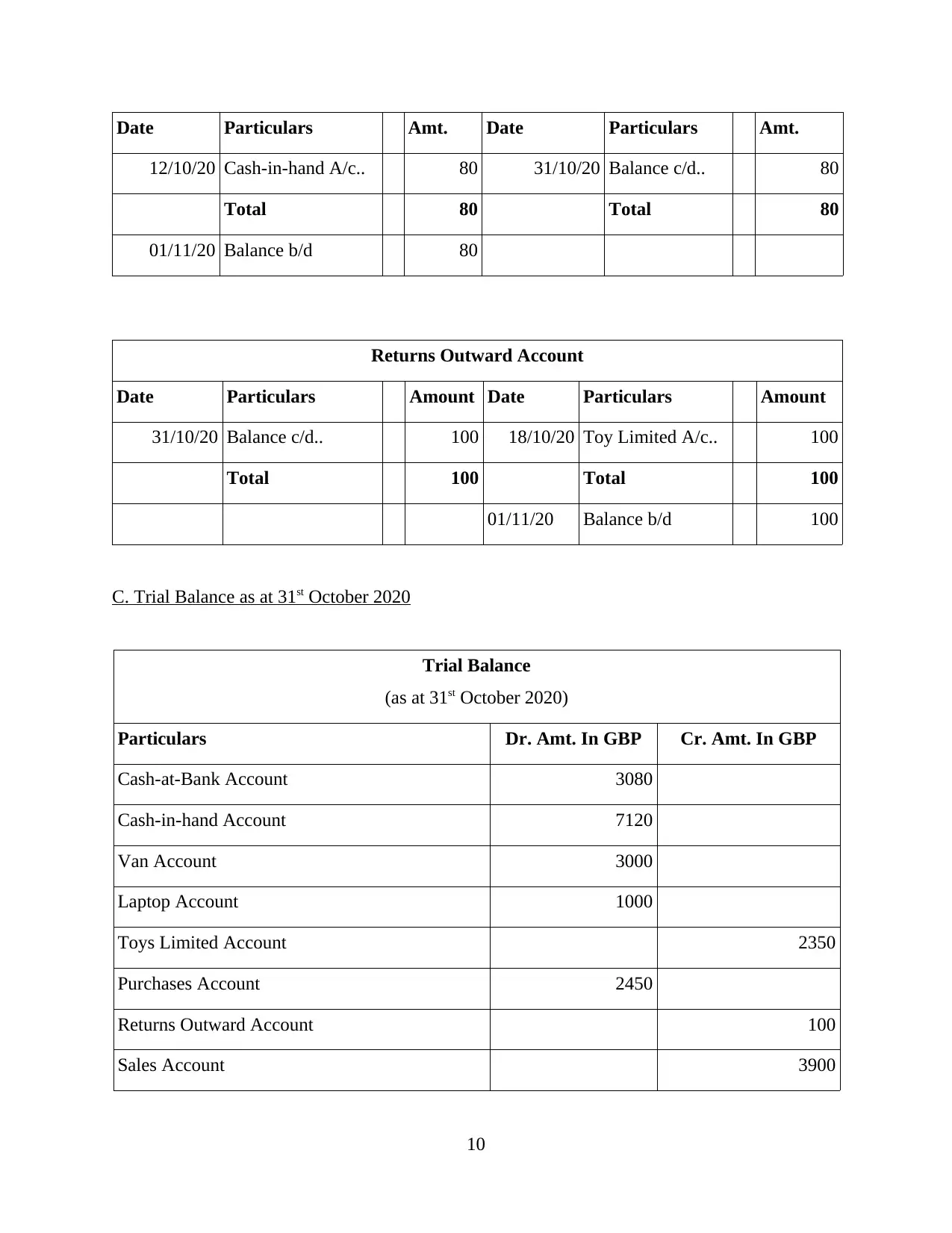

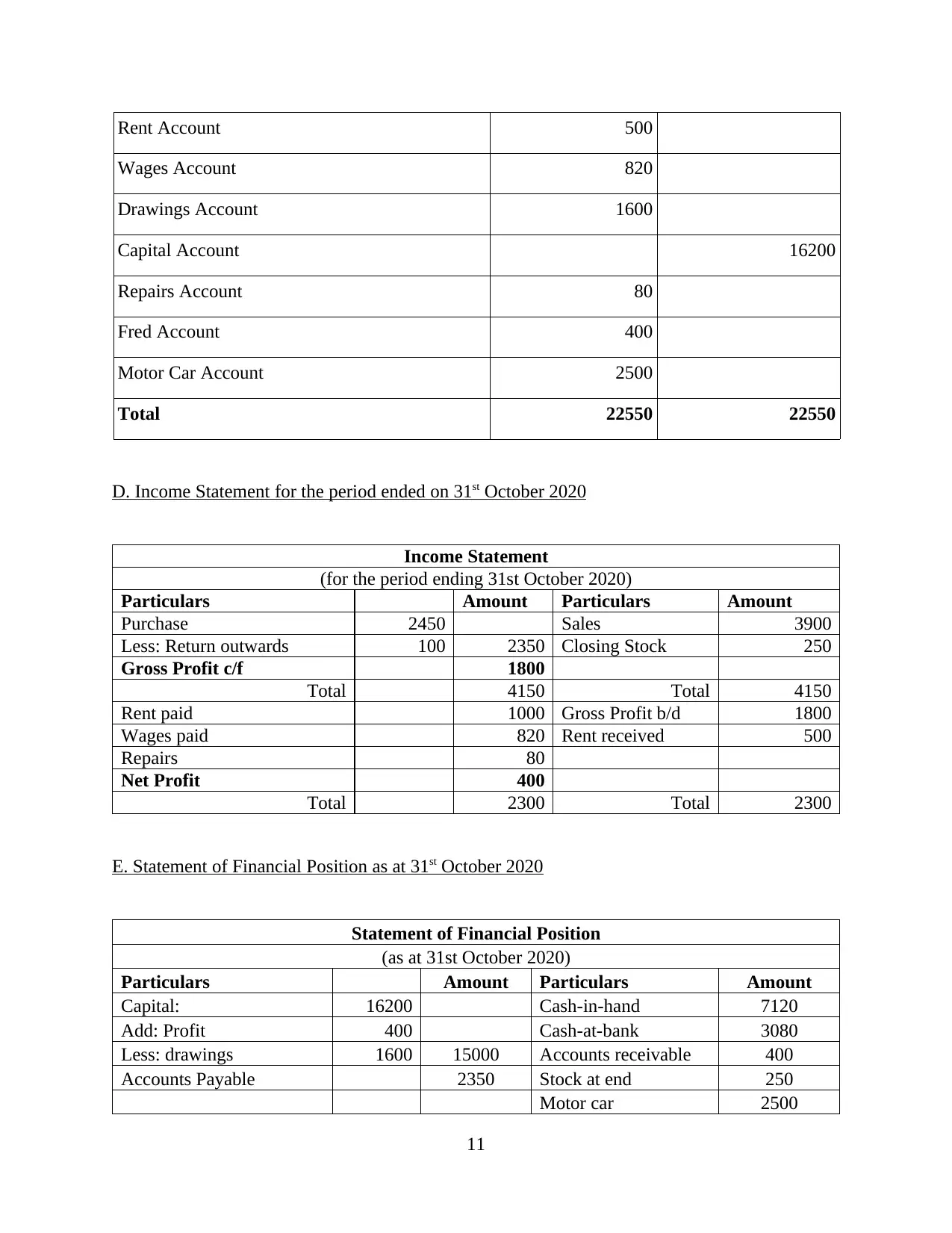

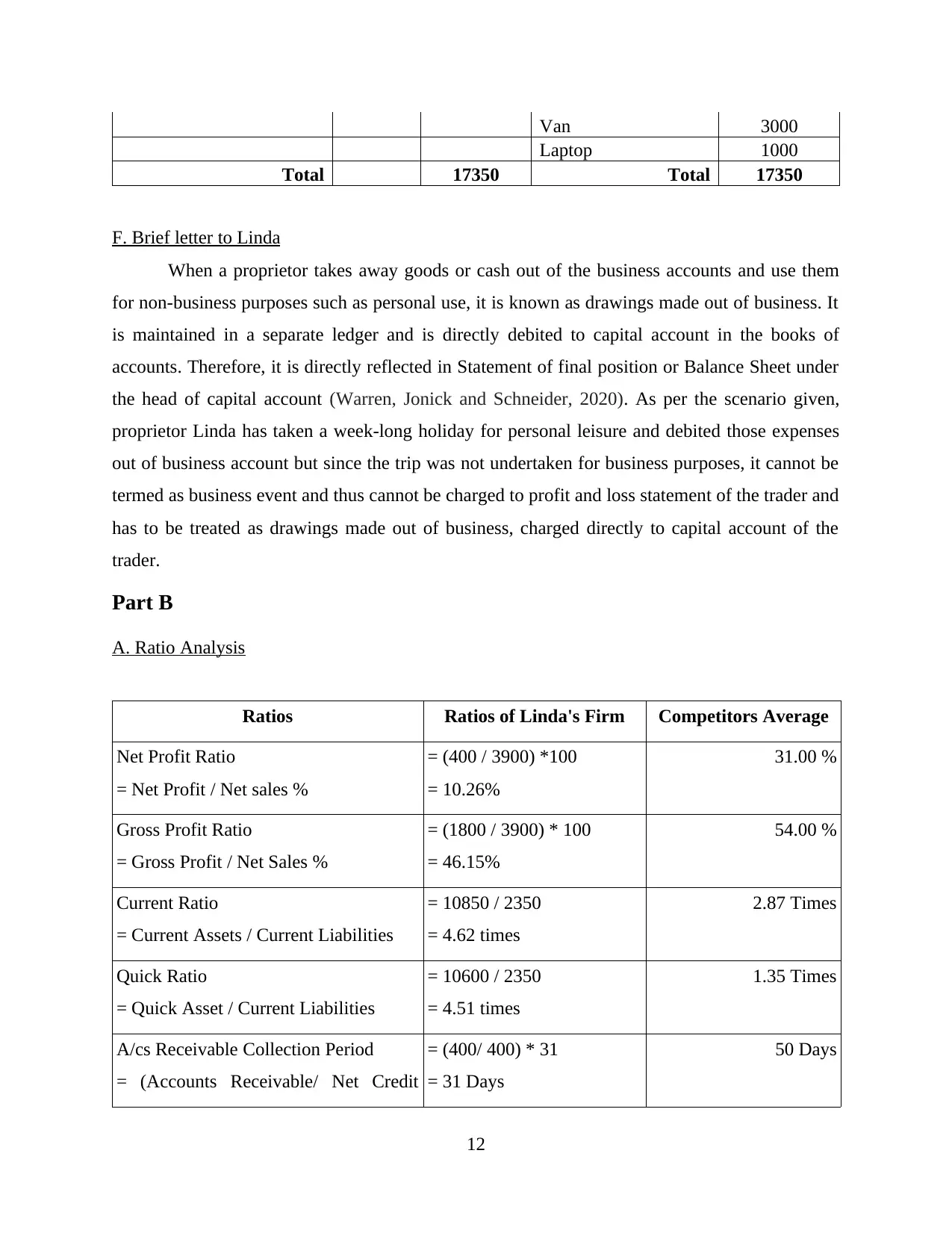

This assignment analyzes the financial performance of a sole trader, Linda, for the month of October 2020. The assignment begins with double-entry bookkeeping entries for various transactions, including cash, sales, purchases, and expenses. These entries are then used to balance the accounts and prepare a trial balance. Based on the trial balance, an income statement and a statement of financial position are created to assess Linda's financial performance. The assignment also includes a brief letter explaining the treatment of drawings. Finally, the assignment delves into ratio analysis, calculating and interpreting key ratios such as the net profit ratio, gross profit ratio, current ratio, quick ratio, accounts receivable collection period, and accounts payable payment period. A comparison is made with industry averages to evaluate Linda's business's financial health and identify areas for improvement, providing insights into working capital management and overall profitability.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.