Preparation of Accounting Records using Spreadsheets

VerifiedAdded on 2023/01/09

|31

|4903

|93

AI Summary

This document provides a detailed explanation of how to prepare accounting records using spreadsheets. It includes journal entries, T-accounts, unadjusted trial balance, types of adjusting entries, and a ten-column worksheet. The content is relevant to accounting and finance courses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Assessment item 1

Assignment 1

Assignment 1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

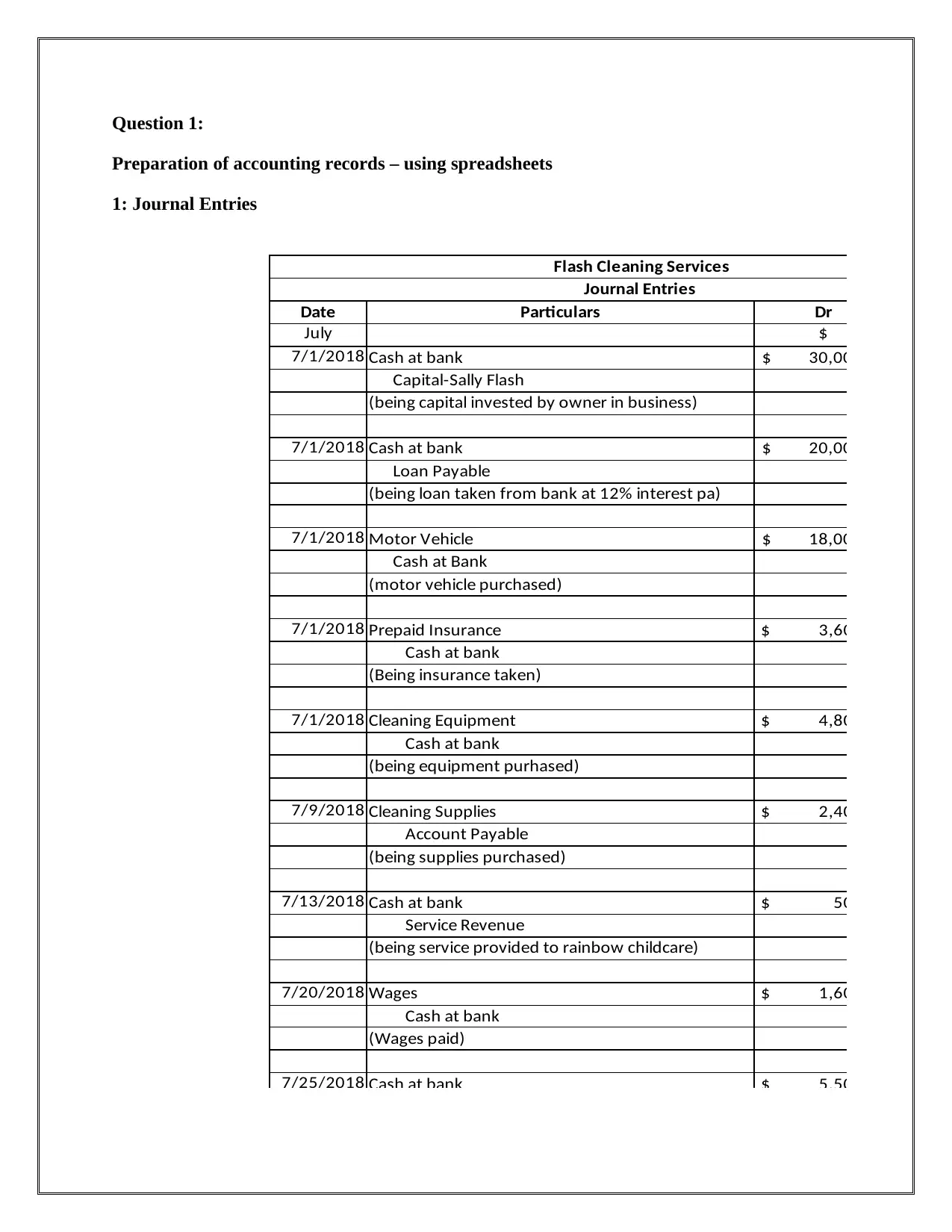

Question 1:

Preparation of accounting records – using spreadsheets

1: Journal Entries

Flash Cleaning Services

Journal Entries

Date Particulars Dr

July $

7/1/2018 Cash at bank $ 30,000.00

Capital-Sally Flash

(being capital invested by owner in business)

7/1/2018 Cash at bank $ 20,000.00

Loan Payable

(being loan taken from bank at 12% interest pa)

7/1/2018 Motor Vehicle $ 18,000.00

Cash at Bank

(motor vehicle purchased)

7/1/2018 Prepaid Insurance $ 3,600.00

Cash at bank

(Being insurance taken)

7/1/2018 Cleaning Equipment $ 4,800.00

Cash at bank

(being equipment purhased)

7/9/2018 Cleaning Supplies $ 2,400.00

Account Payable

(being supplies purchased)

7/13/2018 Cash at bank $ 500.00

Service Revenue

(being service provided to rainbow childcare)

7/20/2018 Wages $ 1,600.00

Cash at bank

(Wages paid)

7/25/2018 Cash at bank $ 5,500.00

Preparation of accounting records – using spreadsheets

1: Journal Entries

Flash Cleaning Services

Journal Entries

Date Particulars Dr

July $

7/1/2018 Cash at bank $ 30,000.00

Capital-Sally Flash

(being capital invested by owner in business)

7/1/2018 Cash at bank $ 20,000.00

Loan Payable

(being loan taken from bank at 12% interest pa)

7/1/2018 Motor Vehicle $ 18,000.00

Cash at Bank

(motor vehicle purchased)

7/1/2018 Prepaid Insurance $ 3,600.00

Cash at bank

(Being insurance taken)

7/1/2018 Cleaning Equipment $ 4,800.00

Cash at bank

(being equipment purhased)

7/9/2018 Cleaning Supplies $ 2,400.00

Account Payable

(being supplies purchased)

7/13/2018 Cash at bank $ 500.00

Service Revenue

(being service provided to rainbow childcare)

7/20/2018 Wages $ 1,600.00

Cash at bank

(Wages paid)

7/25/2018 Cash at bank $ 5,500.00

7/27/2018 Account Payable $ 2,000.00

Cash at bank $ 2,000.00

(Amount paid to supplier)

7/31/2018 Interest on loan $ 300.00

Cash at bank $ 300.00

(Interest paid)

7/31/2018 Advertising Expenses $ 1,600.00

Cash at bank $ 1,600.00

$ 90,300.00 $ 90,300.00

(Damodaran, 2011)

Formula view:

Cash at bank $ 2,000.00

(Amount paid to supplier)

7/31/2018 Interest on loan $ 300.00

Cash at bank $ 300.00

(Interest paid)

7/31/2018 Advertising Expenses $ 1,600.00

Cash at bank $ 1,600.00

$ 90,300.00 $ 90,300.00

(Damodaran, 2011)

Formula view:

### Cash at bank ###

Service Revenue

(being service provided to rainbow childcare)

Service Revenue

(being service provided to rainbow childcare)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

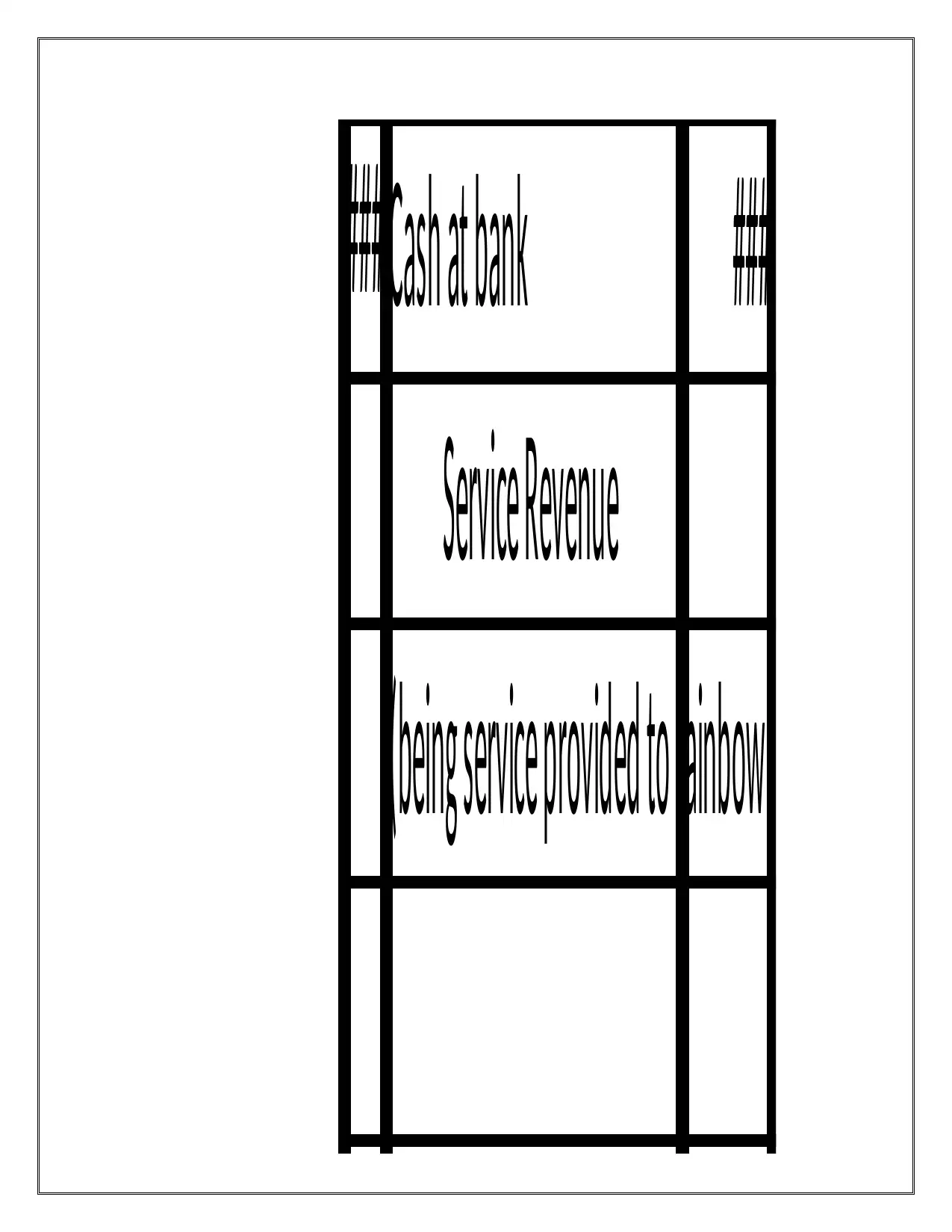

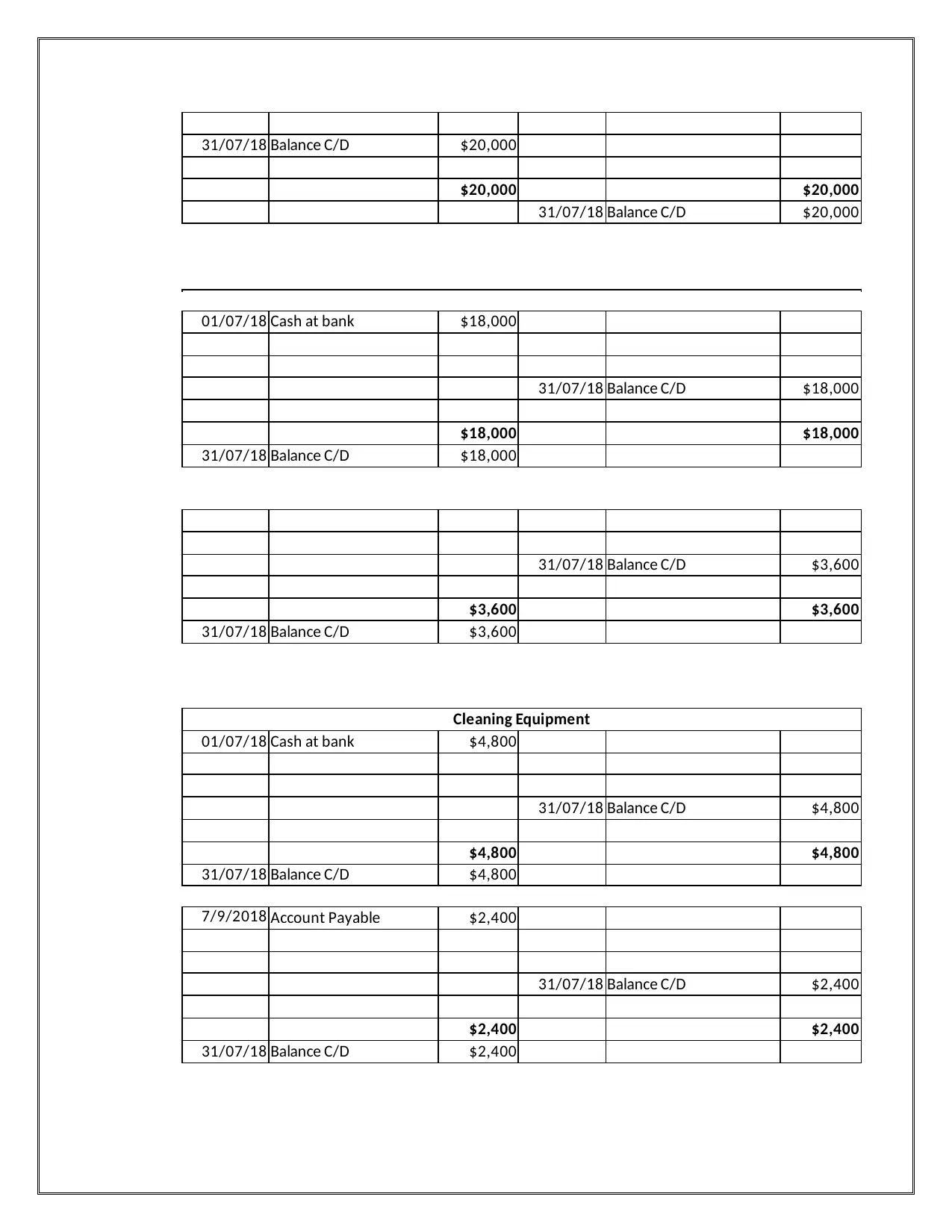

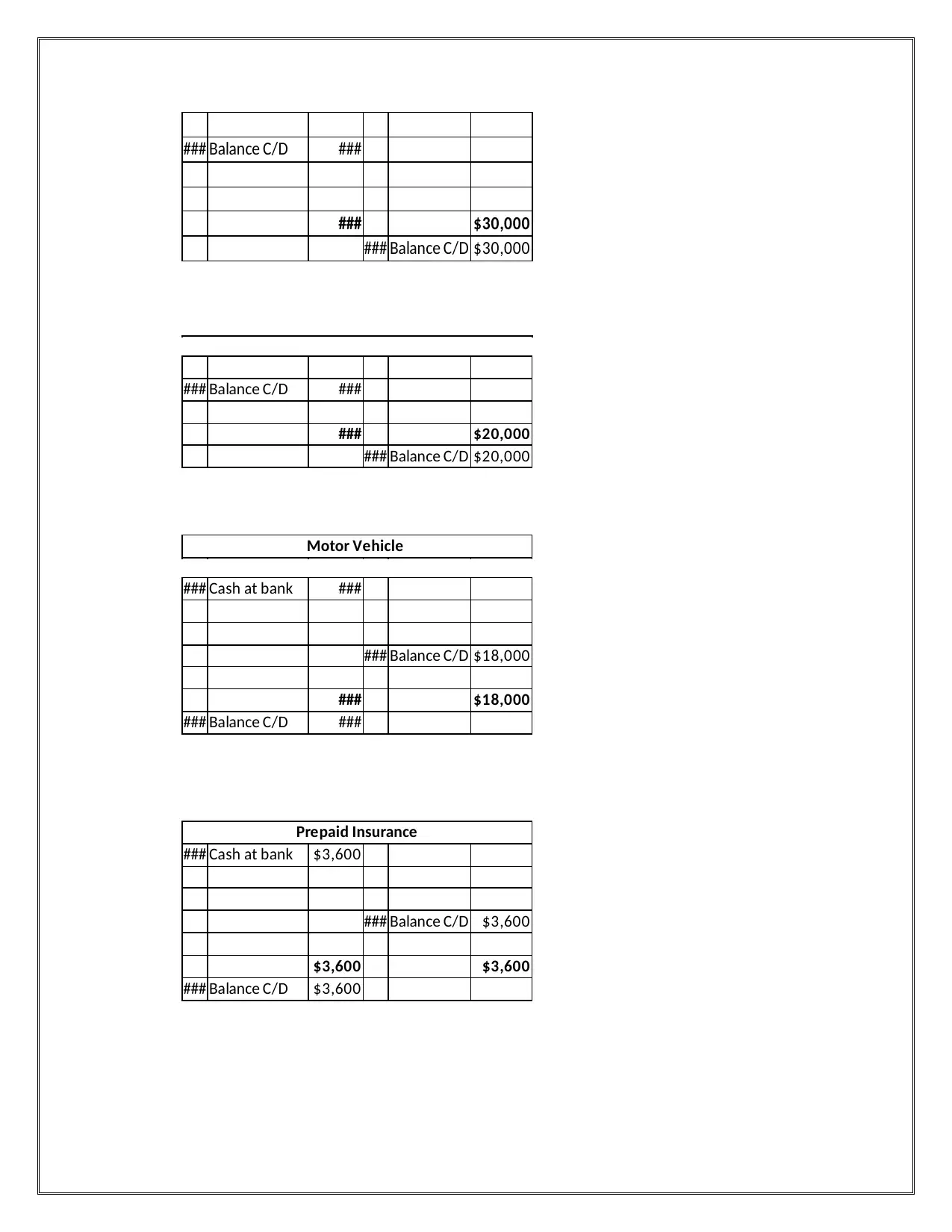

2: T-Accounts

Debit Flash Cleaning Services Credit

General Ledger for the period ending on July 2018

Cash at bank

01/07/18 Capital-Sally Flash $30,000 01/07/18 Motor Vehicle $18,000

01/07/18 Loan Payable $20,000 01/07/18 Prepaid Insurance $3,600

7/13/2018 Service Revenue $500 01/07/18 Cleaning Equipment $4,800

7/25/2018 $5,500 20/07/18 Wages $1,600

27/07/18 Account payable $2,000

31/07/18 Interest on loan $300

31/07/18 Advertising Expenses $1,600

31/07/18 Balance C/D $24,100

$56,000 $56,000

Unearned service

revenue

31/07/18 Advertising Expenses $1,600

31/07/18 Balance C/D $24,100

$56,000 $56,000

31/07/18 Balance C/D $24,100

( Damodaran, 2011)

31/07/18 Balance C/D $30,000

$30,000 $30,000

31/07/18 Balance C/D $30,000

Debit Flash Cleaning Services Credit

General Ledger for the period ending on July 2018

Cash at bank

01/07/18 Capital-Sally Flash $30,000 01/07/18 Motor Vehicle $18,000

01/07/18 Loan Payable $20,000 01/07/18 Prepaid Insurance $3,600

7/13/2018 Service Revenue $500 01/07/18 Cleaning Equipment $4,800

7/25/2018 $5,500 20/07/18 Wages $1,600

27/07/18 Account payable $2,000

31/07/18 Interest on loan $300

31/07/18 Advertising Expenses $1,600

31/07/18 Balance C/D $24,100

$56,000 $56,000

Unearned service

revenue

31/07/18 Advertising Expenses $1,600

31/07/18 Balance C/D $24,100

$56,000 $56,000

31/07/18 Balance C/D $24,100

( Damodaran, 2011)

31/07/18 Balance C/D $30,000

$30,000 $30,000

31/07/18 Balance C/D $30,000

31/07/18 Balance C/D $20,000

$20,000 $20,000

31/07/18 Balance C/D $20,000

01/07/18 Cash at bank $18,000

31/07/18 Balance C/D $18,000

$18,000 $18,000

31/07/18 Balance C/D $18,000

31/07/18 Balance C/D $3,600

$3,600 $3,600

31/07/18 Balance C/D $3,600

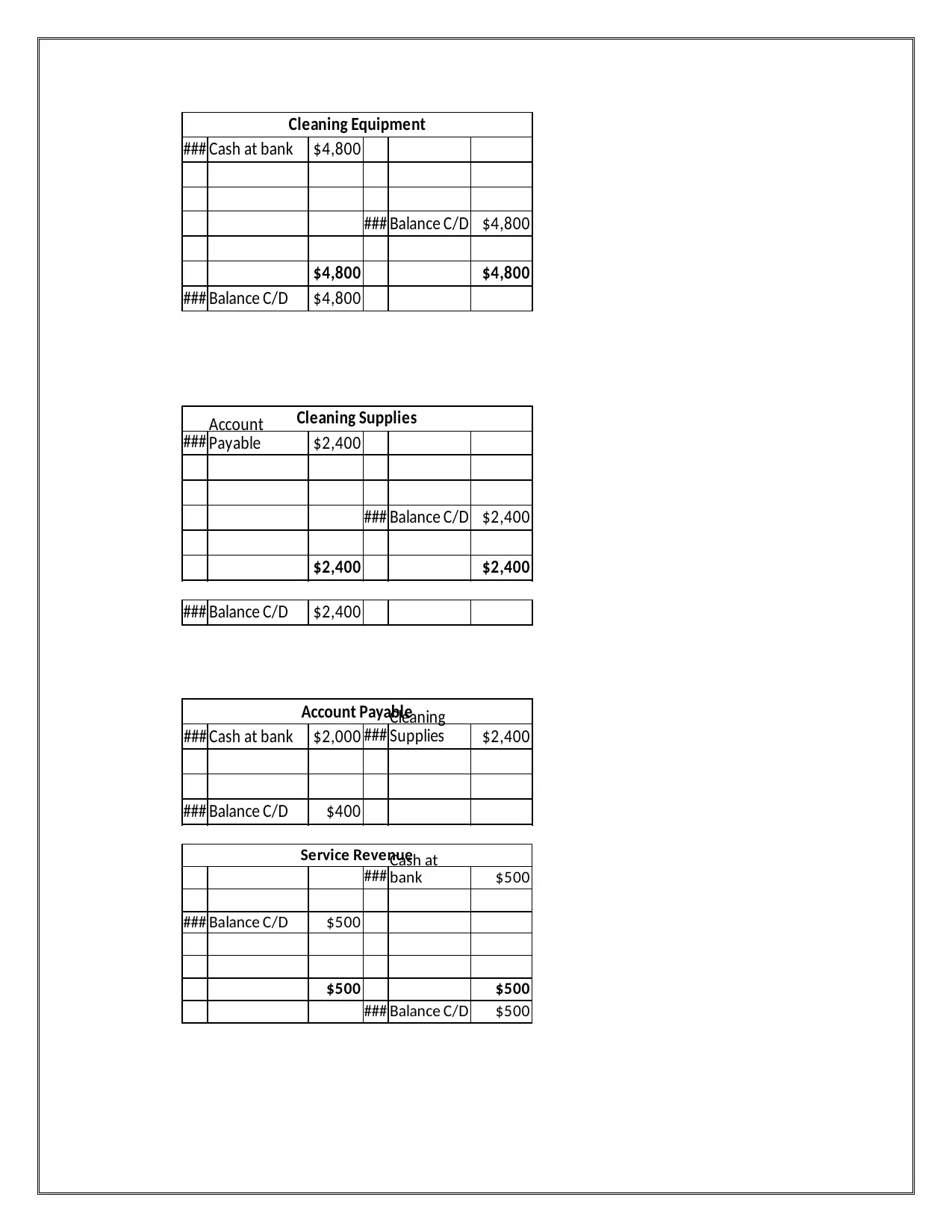

Cleaning Equipment

01/07/18 Cash at bank $4,800

31/07/18 Balance C/D $4,800

$4,800 $4,800

31/07/18 Balance C/D $4,800

7/9/2018 Account Payable $2,400

31/07/18 Balance C/D $2,400

$2,400 $2,400

31/07/18 Balance C/D $2,400

$20,000 $20,000

31/07/18 Balance C/D $20,000

01/07/18 Cash at bank $18,000

31/07/18 Balance C/D $18,000

$18,000 $18,000

31/07/18 Balance C/D $18,000

31/07/18 Balance C/D $3,600

$3,600 $3,600

31/07/18 Balance C/D $3,600

Cleaning Equipment

01/07/18 Cash at bank $4,800

31/07/18 Balance C/D $4,800

$4,800 $4,800

31/07/18 Balance C/D $4,800

7/9/2018 Account Payable $2,400

31/07/18 Balance C/D $2,400

$2,400 $2,400

31/07/18 Balance C/D $2,400

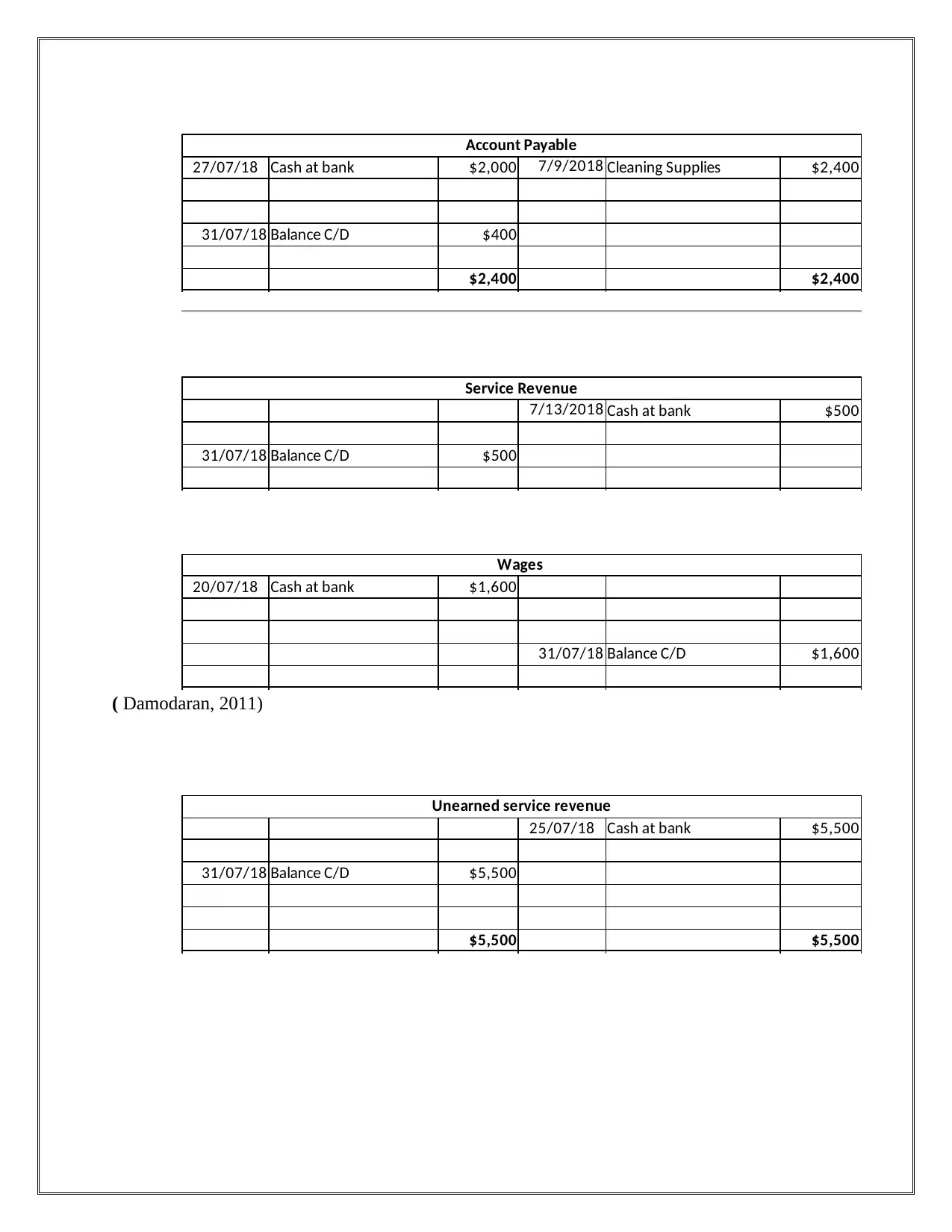

Account Payable

27/07/18 Cash at bank $2,000 7/9/2018 Cleaning Supplies $2,400

31/07/18 Balance C/D $400

$2,400 $2,400

Service Revenue

7/13/2018 Cash at bank $500

31/07/18 Balance C/D $500

Wages

20/07/18 Cash at bank $1,600

31/07/18 Balance C/D $1,600

( Damodaran, 2011)

Unearned service revenue

25/07/18 Cash at bank $5,500

31/07/18 Balance C/D $5,500

$5,500 $5,500

27/07/18 Cash at bank $2,000 7/9/2018 Cleaning Supplies $2,400

31/07/18 Balance C/D $400

$2,400 $2,400

Service Revenue

7/13/2018 Cash at bank $500

31/07/18 Balance C/D $500

Wages

20/07/18 Cash at bank $1,600

31/07/18 Balance C/D $1,600

( Damodaran, 2011)

Unearned service revenue

25/07/18 Cash at bank $5,500

31/07/18 Balance C/D $5,500

$5,500 $5,500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

31/07/18 Balance C/D $300

$300 $300

31/07/18 Balance C/D $300

( Damodaran, 2011)

$300 $300

31/07/18 Balance C/D $300

( Damodaran, 2011)

Formula view of T-Accounts

Flash Cleaning Services Credit

Cash at bank

### ### ### $18,000

### Loan Payable ### ### $3,600

### $500 ### $4,800

### $5,500 ### Wages $1,600

### Account pay $2,000

### Interest on l $300

### Advertising $1,600

### Balance C/D $24,100

### $56,000

### Balance C/D ###

Capital-Sally Flash

### $30,000

### Balance C/D ###

De

bit General Ledger for the period

ending on July 2018

Capital-Sally

Flash

Motor

VehiclePrepaid

InsuranceService

Revenue

Cleaning

Equipment

Unearned

service

revenue

Cash at

bank

### Balance C/D $24,100

### $56,000

### Balance C/D ###

Capital-Sally Flash

### $30,000

Cash at

bank

Flash Cleaning Services Credit

Cash at bank

### ### ### $18,000

### Loan Payable ### ### $3,600

### $500 ### $4,800

### $5,500 ### Wages $1,600

### Account pay $2,000

### Interest on l $300

### Advertising $1,600

### Balance C/D $24,100

### $56,000

### Balance C/D ###

Capital-Sally Flash

### $30,000

### Balance C/D ###

De

bit General Ledger for the period

ending on July 2018

Capital-Sally

Flash

Motor

VehiclePrepaid

InsuranceService

Revenue

Cleaning

Equipment

Unearned

service

revenue

Cash at

bank

### Balance C/D $24,100

### $56,000

### Balance C/D ###

Capital-Sally Flash

### $30,000

Cash at

bank

### Balance C/D ###

### $30,000

### Balance C/D $30,000

### Balance C/D ###

### $20,000

### Balance C/D $20,000

Motor Vehicle

### Cash at bank ###

### Balance C/D $18,000

### $18,000

### Balance C/D ###

Prepaid Insurance

### Cash at bank $3,600

### Balance C/D $3,600

$3,600 $3,600

### Balance C/D $3,600

### $30,000

### Balance C/D $30,000

### Balance C/D ###

### $20,000

### Balance C/D $20,000

Motor Vehicle

### Cash at bank ###

### Balance C/D $18,000

### $18,000

### Balance C/D ###

Prepaid Insurance

### Cash at bank $3,600

### Balance C/D $3,600

$3,600 $3,600

### Balance C/D $3,600

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Cleaning Equipment

### Cash at bank $4,800

### Balance C/D $4,800

$4,800 $4,800

### Balance C/D $4,800

Cleaning Supplies

### $2,400

### Balance C/D $2,400

$2,400 $2,400

Account

Payable

### Balance C/D $2,400

Account Payable

### Cash at bank $2,000 ### $2,400

### Balance C/D $400

Cleaning

Supplies

Service Revenue

### $500

### Balance C/D $500

$500 $500

### Balance C/D $500

Cash at

bank

### Cash at bank $4,800

### Balance C/D $4,800

$4,800 $4,800

### Balance C/D $4,800

Cleaning Supplies

### $2,400

### Balance C/D $2,400

$2,400 $2,400

Account

Payable

### Balance C/D $2,400

Account Payable

### Cash at bank $2,000 ### $2,400

### Balance C/D $400

Cleaning

Supplies

Service Revenue

### $500

### Balance C/D $500

$500 $500

### Balance C/D $500

Cash at

bank

### Balance C/D $1,600

$1,600 $1,600

### Balance C/D $1,600

Unearned service revenue

### $5,500

Cash at

bank

$5,500 $5,500

### Balance C/D $5,500

Interest on loan

### Cash at bank $300

$300 $300

### Balance C/D $300

Advertising Expenses

### Cash at bank $1,600

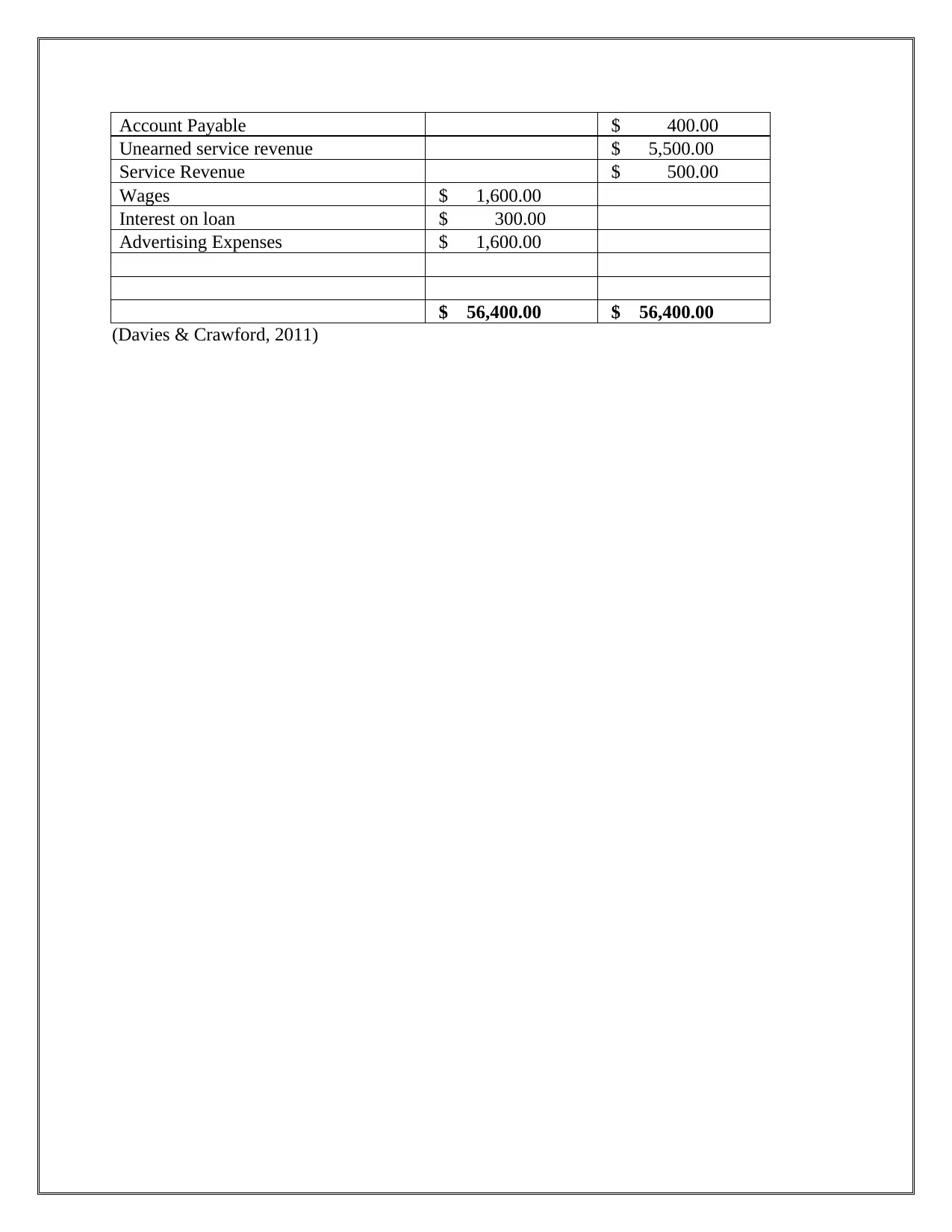

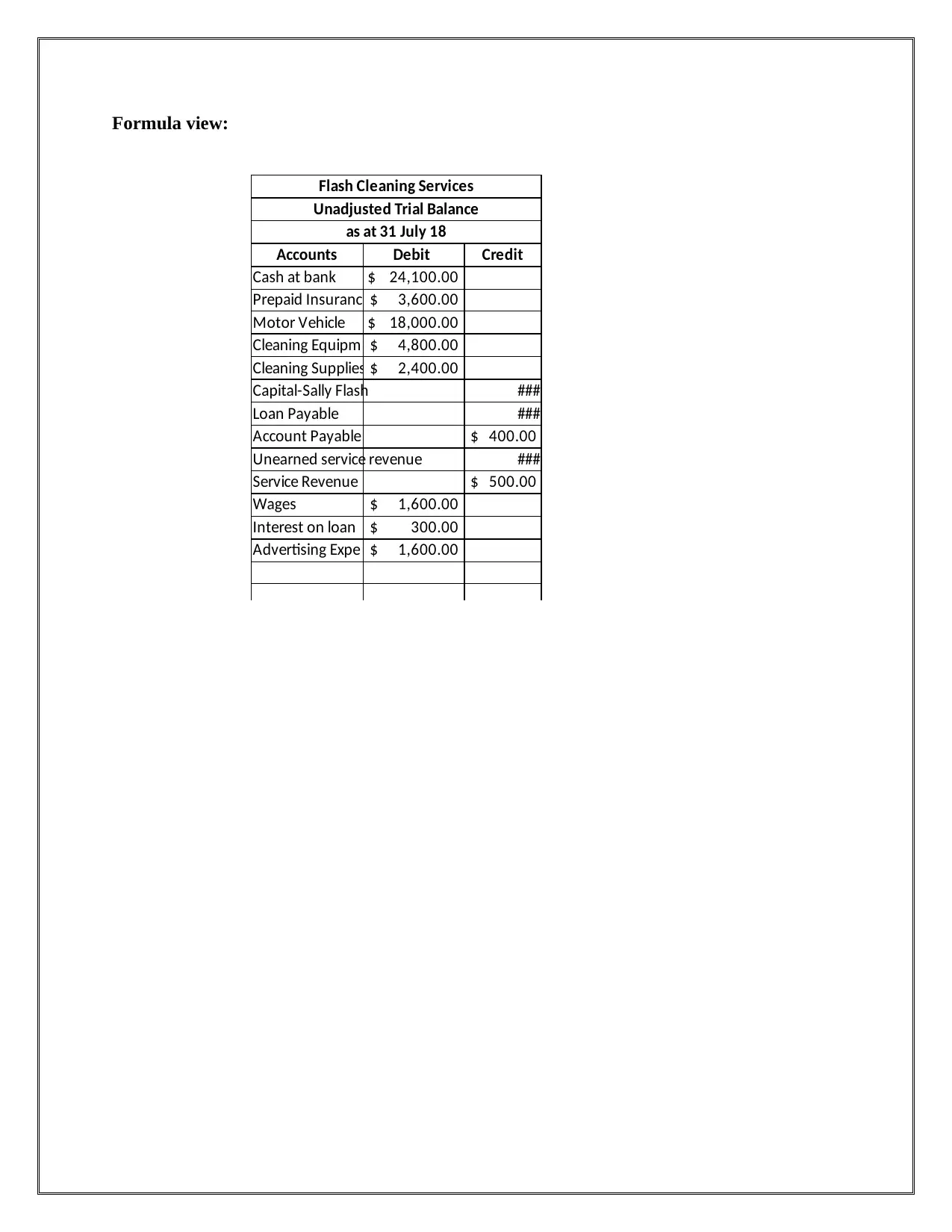

3: Unadjusted Trial Balance

Flash Cleaning Services

Unadjusted Trial Balance

as at 31 July 18

Accounts Debit Credit

Cash at bank $ 24,100.00

Prepaid Insurance $ 3,600.00

Motor Vehicle $ 18,000.00

Cleaning Equipment $ 4,800.00

Cleaning Supplies $ 2,400.00

Capital-Sally Flash $ 30,000.00

Loan Payable $ 20,000.00

$1,600 $1,600

### Balance C/D $1,600

Unearned service revenue

### $5,500

Cash at

bank

$5,500 $5,500

### Balance C/D $5,500

Interest on loan

### Cash at bank $300

$300 $300

### Balance C/D $300

Advertising Expenses

### Cash at bank $1,600

3: Unadjusted Trial Balance

Flash Cleaning Services

Unadjusted Trial Balance

as at 31 July 18

Accounts Debit Credit

Cash at bank $ 24,100.00

Prepaid Insurance $ 3,600.00

Motor Vehicle $ 18,000.00

Cleaning Equipment $ 4,800.00

Cleaning Supplies $ 2,400.00

Capital-Sally Flash $ 30,000.00

Loan Payable $ 20,000.00

Account Payable $ 400.00

Unearned service revenue $ 5,500.00

Service Revenue $ 500.00

Wages $ 1,600.00

Interest on loan $ 300.00

Advertising Expenses $ 1,600.00

$ 56,400.00 $ 56,400.00

(Davies & Crawford, 2011)

Unearned service revenue $ 5,500.00

Service Revenue $ 500.00

Wages $ 1,600.00

Interest on loan $ 300.00

Advertising Expenses $ 1,600.00

$ 56,400.00 $ 56,400.00

(Davies & Crawford, 2011)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Formula view:

Flash Cleaning Services

Unadjusted Trial Balance

as at 31 July 18

Accounts Debit Credit

Cash at bank $ 24,100.00

Prepaid Insuranc $ 3,600.00

Motor Vehicle $ 18,000.00

Cleaning Equipm $ 4,800.00

Cleaning Supplies $ 2,400.00

Capital-Sally Flash ###

Loan Payable ###

Account Payable $ 400.00

Unearned service revenue ###

Service Revenue $ 500.00

Wages $ 1,600.00

Interest on loan $ 300.00

Advertising Expe $ 1,600.00

Flash Cleaning Services

Unadjusted Trial Balance

as at 31 July 18

Accounts Debit Credit

Cash at bank $ 24,100.00

Prepaid Insuranc $ 3,600.00

Motor Vehicle $ 18,000.00

Cleaning Equipm $ 4,800.00

Cleaning Supplies $ 2,400.00

Capital-Sally Flash ###

Loan Payable ###

Account Payable $ 400.00

Unearned service revenue ###

Service Revenue $ 500.00

Wages $ 1,600.00

Interest on loan $ 300.00

Advertising Expe $ 1,600.00

4: Types of adjusting entries and adjusting entries in the book of accounts of Flash

Cleaning Services as at 31 July 2018

Types of adjusting entries

Prepaid Expenses: Expenses for which liability has not been arise but they have been paid is

termed as prepaid expenses. It create current assets in the balance sheet.

Unearned Revenue: This involves the amount that has been received for services that are not

yet given or for the products that have not been delivered. These are recognized as liability till

the service is performed completely.

Accrued Expenses: This involve the adjusting entries that re developed at the end of an

accounting year for recording the amounts that have been incurred in the current years but have

not been recorded in the ledger.

Accrued Revenue: Revenue which has been earned but received has been classified as accrued

revenue and it create debit balance in books of accounts

Depreciation expense: Depreciation is the adjusting amount that is used to divide the cost of

assets into its useful life (Damodaran, 2011)

Cleaning Services as at 31 July 2018

Types of adjusting entries

Prepaid Expenses: Expenses for which liability has not been arise but they have been paid is

termed as prepaid expenses. It create current assets in the balance sheet.

Unearned Revenue: This involves the amount that has been received for services that are not

yet given or for the products that have not been delivered. These are recognized as liability till

the service is performed completely.

Accrued Expenses: This involve the adjusting entries that re developed at the end of an

accounting year for recording the amounts that have been incurred in the current years but have

not been recorded in the ledger.

Accrued Revenue: Revenue which has been earned but received has been classified as accrued

revenue and it create debit balance in books of accounts

Depreciation expense: Depreciation is the adjusting amount that is used to divide the cost of

assets into its useful life (Damodaran, 2011)

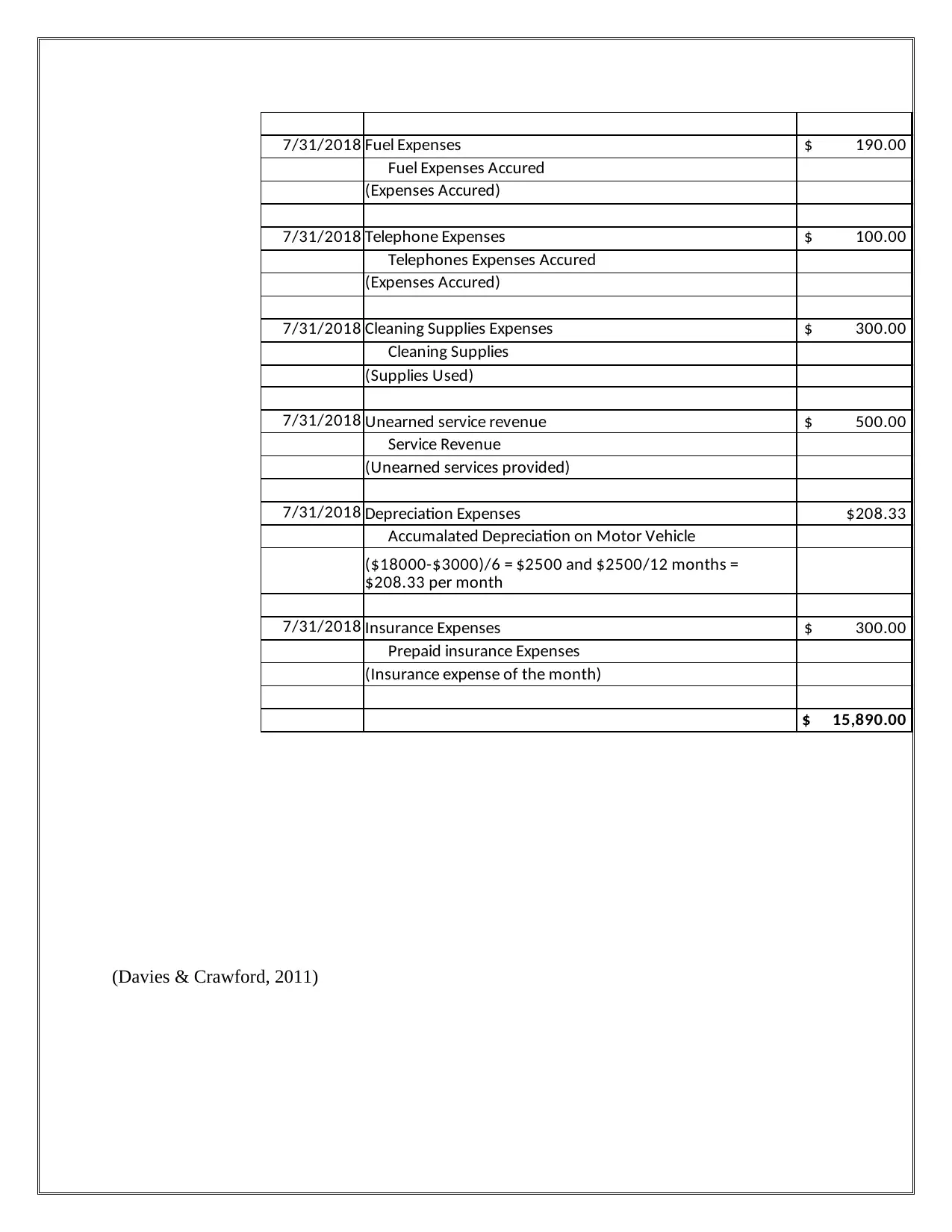

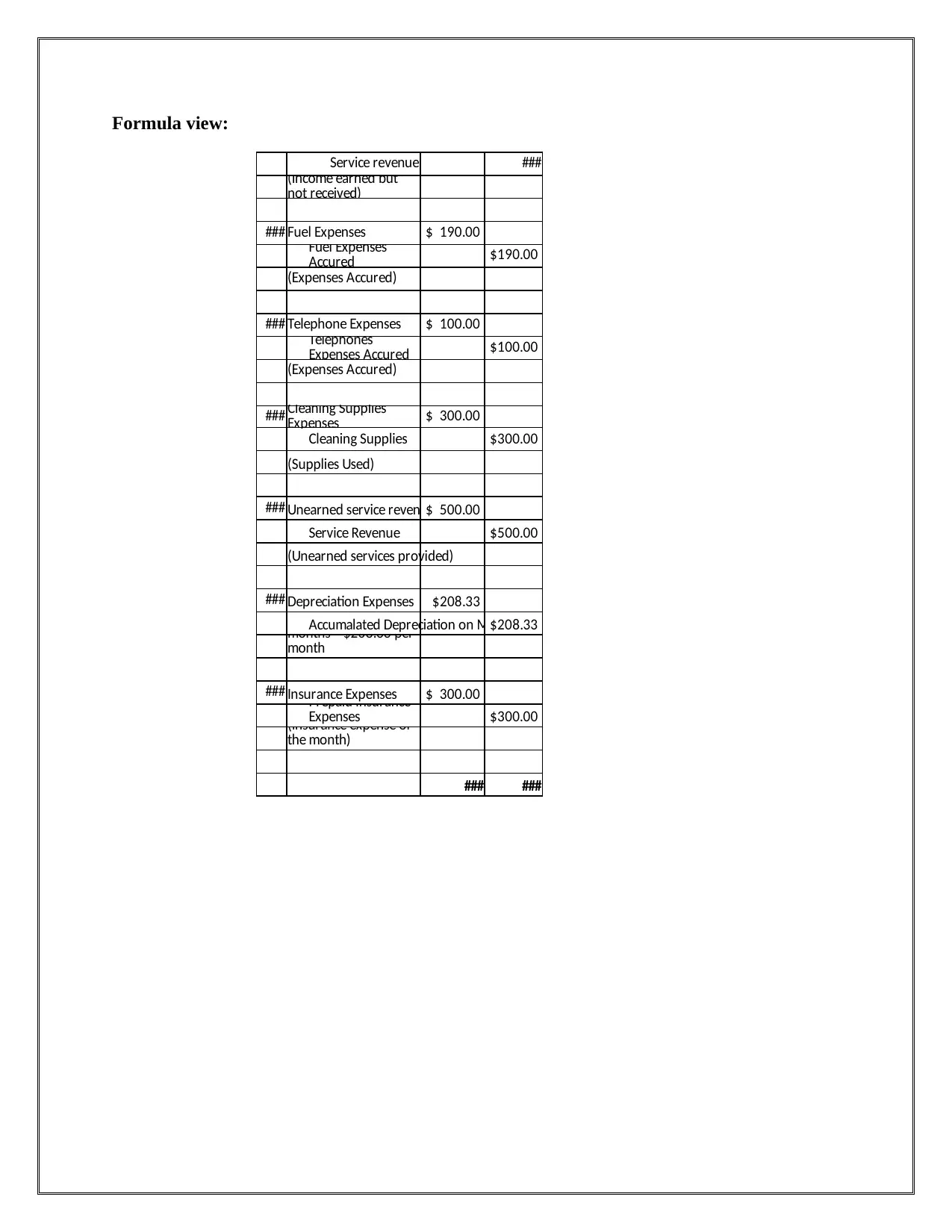

7/31/2018 Fuel Expenses $ 190.00

Fuel Expenses Accured

(Expenses Accured)

7/31/2018 Telephone Expenses $ 100.00

Telephones Expenses Accured

(Expenses Accured)

7/31/2018 Cleaning Supplies Expenses $ 300.00

Cleaning Supplies

(Supplies Used)

7/31/2018 Unearned service revenue $ 500.00

Service Revenue

(Unearned services provided)

7/31/2018 Depreciation Expenses $208.33

Accumalated Depreciation on Motor Vehicle

7/31/2018 Insurance Expenses $ 300.00

Prepaid insurance Expenses

(Insurance expense of the month)

$ 15,890.00

($18000-$3000)/6 = $2500 and $2500/12 months =

$208.33 per month

(Davies & Crawford, 2011)

Fuel Expenses Accured

(Expenses Accured)

7/31/2018 Telephone Expenses $ 100.00

Telephones Expenses Accured

(Expenses Accured)

7/31/2018 Cleaning Supplies Expenses $ 300.00

Cleaning Supplies

(Supplies Used)

7/31/2018 Unearned service revenue $ 500.00

Service Revenue

(Unearned services provided)

7/31/2018 Depreciation Expenses $208.33

Accumalated Depreciation on Motor Vehicle

7/31/2018 Insurance Expenses $ 300.00

Prepaid insurance Expenses

(Insurance expense of the month)

$ 15,890.00

($18000-$3000)/6 = $2500 and $2500/12 months =

$208.33 per month

(Davies & Crawford, 2011)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Formula view:

Service revenue ###

### Fuel Expenses $ 190.00

$190.00

(Expenses Accured)

### Telephone Expenses $ 100.00

$100.00

(Expenses Accured)

### $ 300.00

Cleaning Supplies $300.00

(Supplies Used)

### Unearned service reven $ 500.00

Service Revenue $500.00

(Unearned services provided)

### Depreciation Expenses $208.33

Accumalated Depreciation on M$208.33

### Insurance Expenses $ 300.00

$300.00

### ###

(Income earned but

not received)

Fuel Expenses

Accured

Telephones

Expenses Accured

Cleaning Supplies

Expenses

($18000-$3000)/6 =

$2500 and $2500/12

months = $208.33 per

month

Prepaid insurance

Expenses

(Insurance expense of

the month)

Service revenue ###

### Fuel Expenses $ 190.00

$190.00

(Expenses Accured)

### Telephone Expenses $ 100.00

$100.00

(Expenses Accured)

### $ 300.00

Cleaning Supplies $300.00

(Supplies Used)

### Unearned service reven $ 500.00

Service Revenue $500.00

(Unearned services provided)

### Depreciation Expenses $208.33

Accumalated Depreciation on M$208.33

### Insurance Expenses $ 300.00

$300.00

### ###

(Income earned but

not received)

Fuel Expenses

Accured

Telephones

Expenses Accured

Cleaning Supplies

Expenses

($18000-$3000)/6 =

$2500 and $2500/12

months = $208.33 per

month

Prepaid insurance

Expenses

(Insurance expense of

the month)

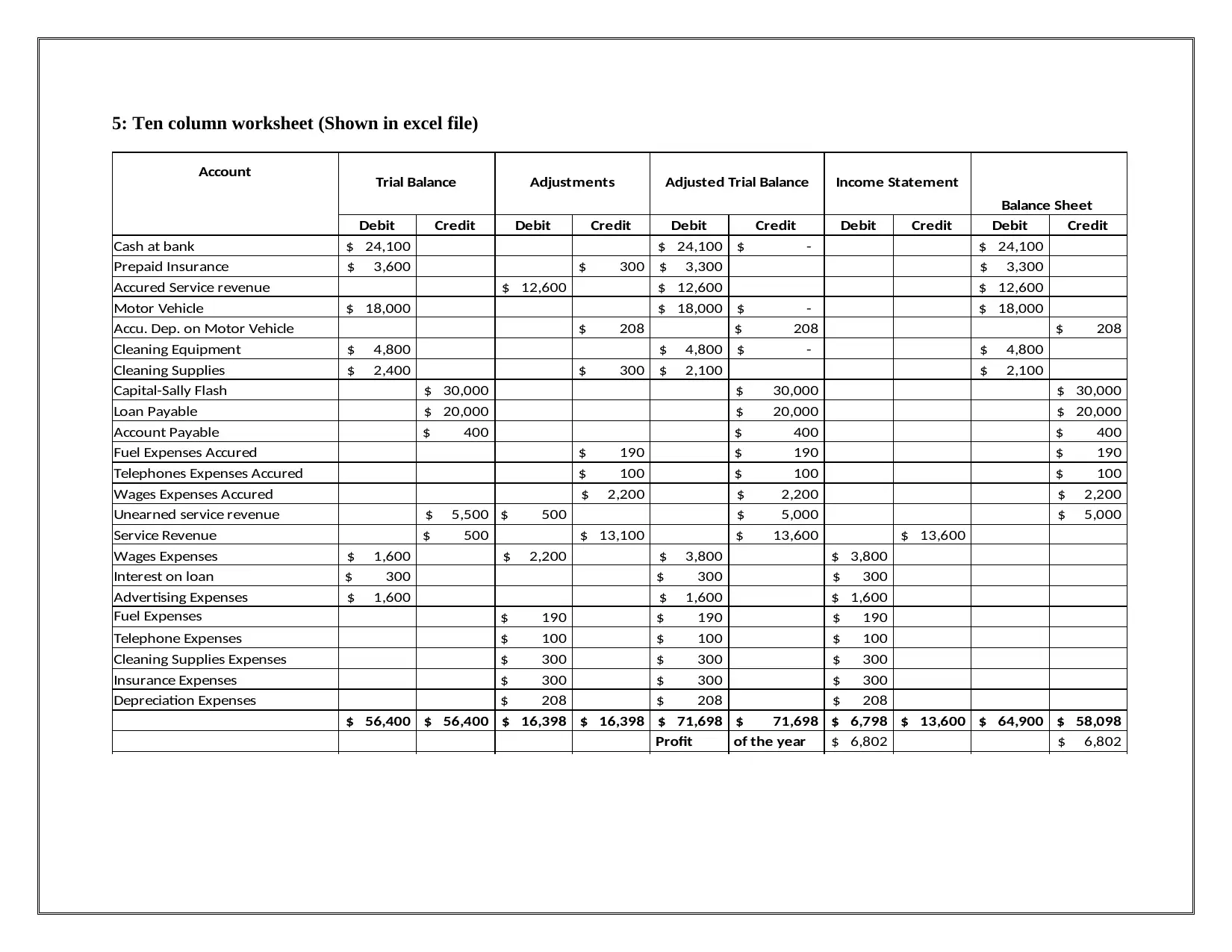

5: Ten column worksheet (Shown in excel file)

Account Trial Balance Adjustments Adjusted Trial Balance Income Statement

Balance Sheet

Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

Cash at bank $ 24,100 $ 24,100 $ - $ 24,100

Prepaid Insurance $ 3,600 $ 300 $ 3,300 $ 3,300

Accured Service revenue $ 12,600 $ 12,600 $ 12,600

Motor Vehicle $ 18,000 $ 18,000 $ - $ 18,000

Accu. Dep. on Motor Vehicle $ 208 $ 208 $ 208

Cleaning Equipment $ 4,800 $ 4,800 $ - $ 4,800

Cleaning Supplies $ 2,400 $ 300 $ 2,100 $ 2,100

Capital-Sally Flash $ 30,000 $ 30,000 $ 30,000

Loan Payable $ 20,000 $ 20,000 $ 20,000

Account Payable $ 400 $ 400 $ 400

Fuel Expenses Accured $ 190 $ 190 $ 190

Telephones Expenses Accured $ 100 $ 100 $ 100

Wages Expenses Accured $ 2,200 $ 2,200 $ 2,200

Unearned service revenue $ 5,500 $ 500 $ 5,000 $ 5,000

Service Revenue $ 500 $ 13,100 $ 13,600 $ 13,600

Wages Expenses $ 1,600 $ 2,200 $ 3,800 $ 3,800

Interest on loan $ 300 $ 300 $ 300

Advertising Expenses $ 1,600 $ 1,600 $ 1,600

Fuel Expenses $ 190 $ 190 $ 190

Telephone Expenses $ 100 $ 100 $ 100

Cleaning Supplies Expenses $ 300 $ 300 $ 300

Insurance Expenses $ 300 $ 300 $ 300

Depreciation Expenses $ 208 $ 208 $ 208

$ 56,400 $ 56,400 $ 16,398 $ 16,398 $ 71,698 $ 71,698 $ 6,798 $ 13,600 $ 64,900 $ 58,098

Profit of the year $ 6,802 $ 6,802

Account Trial Balance Adjustments Adjusted Trial Balance Income Statement

Balance Sheet

Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit

Cash at bank $ 24,100 $ 24,100 $ - $ 24,100

Prepaid Insurance $ 3,600 $ 300 $ 3,300 $ 3,300

Accured Service revenue $ 12,600 $ 12,600 $ 12,600

Motor Vehicle $ 18,000 $ 18,000 $ - $ 18,000

Accu. Dep. on Motor Vehicle $ 208 $ 208 $ 208

Cleaning Equipment $ 4,800 $ 4,800 $ - $ 4,800

Cleaning Supplies $ 2,400 $ 300 $ 2,100 $ 2,100

Capital-Sally Flash $ 30,000 $ 30,000 $ 30,000

Loan Payable $ 20,000 $ 20,000 $ 20,000

Account Payable $ 400 $ 400 $ 400

Fuel Expenses Accured $ 190 $ 190 $ 190

Telephones Expenses Accured $ 100 $ 100 $ 100

Wages Expenses Accured $ 2,200 $ 2,200 $ 2,200

Unearned service revenue $ 5,500 $ 500 $ 5,000 $ 5,000

Service Revenue $ 500 $ 13,100 $ 13,600 $ 13,600

Wages Expenses $ 1,600 $ 2,200 $ 3,800 $ 3,800

Interest on loan $ 300 $ 300 $ 300

Advertising Expenses $ 1,600 $ 1,600 $ 1,600

Fuel Expenses $ 190 $ 190 $ 190

Telephone Expenses $ 100 $ 100 $ 100

Cleaning Supplies Expenses $ 300 $ 300 $ 300

Insurance Expenses $ 300 $ 300 $ 300

Depreciation Expenses $ 208 $ 208 $ 208

$ 56,400 $ 56,400 $ 16,398 $ 16,398 $ 71,698 $ 71,698 $ 6,798 $ 13,600 $ 64,900 $ 58,098

Profit of the year $ 6,802 $ 6,802

Formula View

Account

DebitCreditDebitCreditDebitCreditDebitCreditDebitCredit

Cash at bank ### ### $ - ###

### ### ### ###

### ### ###

### ### $ - ###

### ### ###

### ### $ - ###

### ### ### ###

### ### ###

Loan Payable ### ### ###

### ### ###

### ### ###

### ### ###

### ### ###

### ### ### ###

### ### ### ###

### ### ### ###

### ### ###

### ### ###

### ### ###

### ### ###

### ### ###

### ### ###

### ### ###

### ### ### ### ### ### ### ### ### ###

Trial

Balance

Adjustmen

ts

Adjusted

Trial

Balance

Income

Statement Balance

Sheet

Prepaid

Insurance

Accured

Service

revenueMotor

Vehicle

Accu. Dep. on

Motor

VehicleCleaning

EquipmentCleaning

SuppliesCapital-Sally

Flash

Account

Payable

Fuel

Expenses

Accured

Telephones

Expenses

Accured

Wages

Expenses

Accured

Unearned

service

revenueService

RevenueWages

ExpensesInterest on

loanAdvertising

Expenses

Fuel

ExpensesTelephone

Expenses

Cleaning

Supplies

ExpensesInsurance

ExpensesDepreciation

Expenses

Account

DebitCreditDebitCreditDebitCreditDebitCreditDebitCredit

Cash at bank ### ### $ - ###

### ### ### ###

### ### ###

### ### $ - ###

### ### ###

### ### $ - ###

### ### ### ###

### ### ###

Loan Payable ### ### ###

### ### ###

### ### ###

### ### ###

### ### ###

### ### ### ###

### ### ### ###

### ### ### ###

### ### ###

### ### ###

### ### ###

### ### ###

### ### ###

### ### ###

### ### ###

### ### ### ### ### ### ### ### ### ###

Trial

Balance

Adjustmen

ts

Adjusted

Trial

Balance

Income

Statement Balance

Sheet

Prepaid

Insurance

Accured

Service

revenueMotor

Vehicle

Accu. Dep. on

Motor

VehicleCleaning

EquipmentCleaning

SuppliesCapital-Sally

Flash

Account

Payable

Fuel

Expenses

Accured

Telephones

Expenses

Accured

Wages

Expenses

Accured

Unearned

service

revenueService

RevenueWages

ExpensesInterest on

loanAdvertising

Expenses

Fuel

ExpensesTelephone

Expenses

Cleaning

Supplies

ExpensesInsurance

ExpensesDepreciation

Expenses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

20

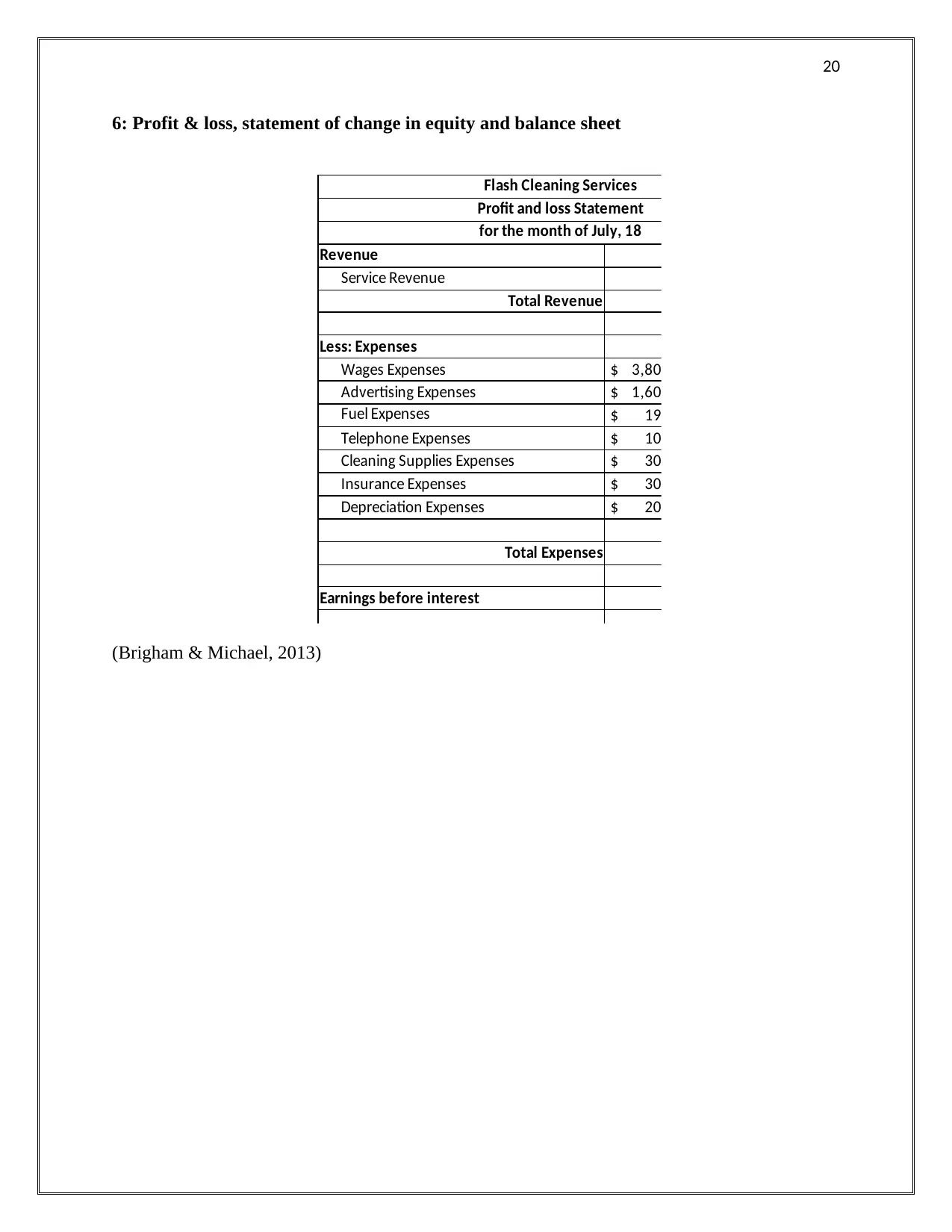

6: Profit & loss, statement of change in equity and balance sheet

Flash Cleaning Services

Profit and loss Statement

for the month of July, 18

Revenue

Service Revenue

Total Revenue

Less: Expenses

Wages Expenses $ 3,800.00

Advertising Expenses $ 1,600.00

Fuel Expenses $ 190.00

Telephone Expenses $ 100.00

Cleaning Supplies Expenses $ 300.00

Insurance Expenses $ 300.00

Depreciation Expenses $ 208.33

Total Expenses

Earnings before interest

(Brigham & Michael, 2013)

6: Profit & loss, statement of change in equity and balance sheet

Flash Cleaning Services

Profit and loss Statement

for the month of July, 18

Revenue

Service Revenue

Total Revenue

Less: Expenses

Wages Expenses $ 3,800.00

Advertising Expenses $ 1,600.00

Fuel Expenses $ 190.00

Telephone Expenses $ 100.00

Cleaning Supplies Expenses $ 300.00

Insurance Expenses $ 300.00

Depreciation Expenses $ 208.33

Total Expenses

Earnings before interest

(Brigham & Michael, 2013)

21

Formula view:

Flash Cleaning Services

Profit and loss Statement

for the month of July, 18

Revenue

Service Revenue $ 13,600.00

Total Revenue $ 13,600.00

Less: Expenses

Wages Expenses $ 3,800.00

Advertising Expen $ 1,600.00

Fuel Expenses $ 190.00

Telephone Expens $ 100.00

Cleaning Supplies $ 300.00

Insurance Expense$ 300.00

Depreciation Expe $ 208.33

Total Expenses $ 6,498.33

Earnings before interest $ 7,101.67

Formula view:

Flash Cleaning Services

Profit and loss Statement

for the month of July, 18

Revenue

Service Revenue $ 13,600.00

Total Revenue $ 13,600.00

Less: Expenses

Wages Expenses $ 3,800.00

Advertising Expen $ 1,600.00

Fuel Expenses $ 190.00

Telephone Expens $ 100.00

Cleaning Supplies $ 300.00

Insurance Expense$ 300.00

Depreciation Expe $ 208.33

Total Expenses $ 6,498.33

Earnings before interest $ 7,101.67

22

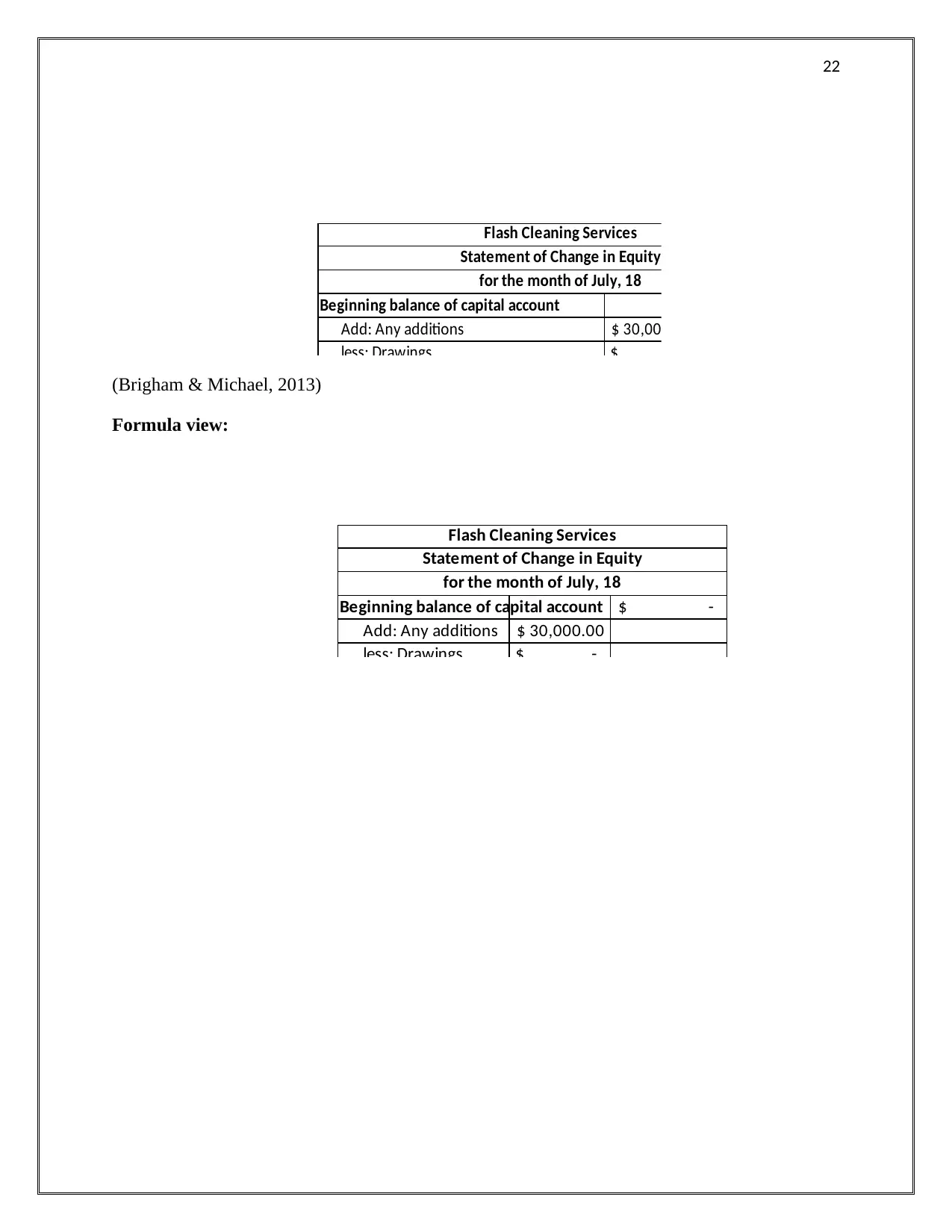

Flash Cleaning Services

Statement of Change in Equity

for the month of July, 18

Beginning balance of capital account

Add: Any additions $ 30,000.00

less: Drawings $ -

(Brigham & Michael, 2013)

Formula view:

Flash Cleaning Services

Statement of Change in Equity

for the month of July, 18

Beginning balance of capital account $ -

Add: Any additions $ 30,000.00

less: Drawings $ -

Flash Cleaning Services

Statement of Change in Equity

for the month of July, 18

Beginning balance of capital account

Add: Any additions $ 30,000.00

less: Drawings $ -

(Brigham & Michael, 2013)

Formula view:

Flash Cleaning Services

Statement of Change in Equity

for the month of July, 18

Beginning balance of capital account $ -

Add: Any additions $ 30,000.00

less: Drawings $ -

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

23

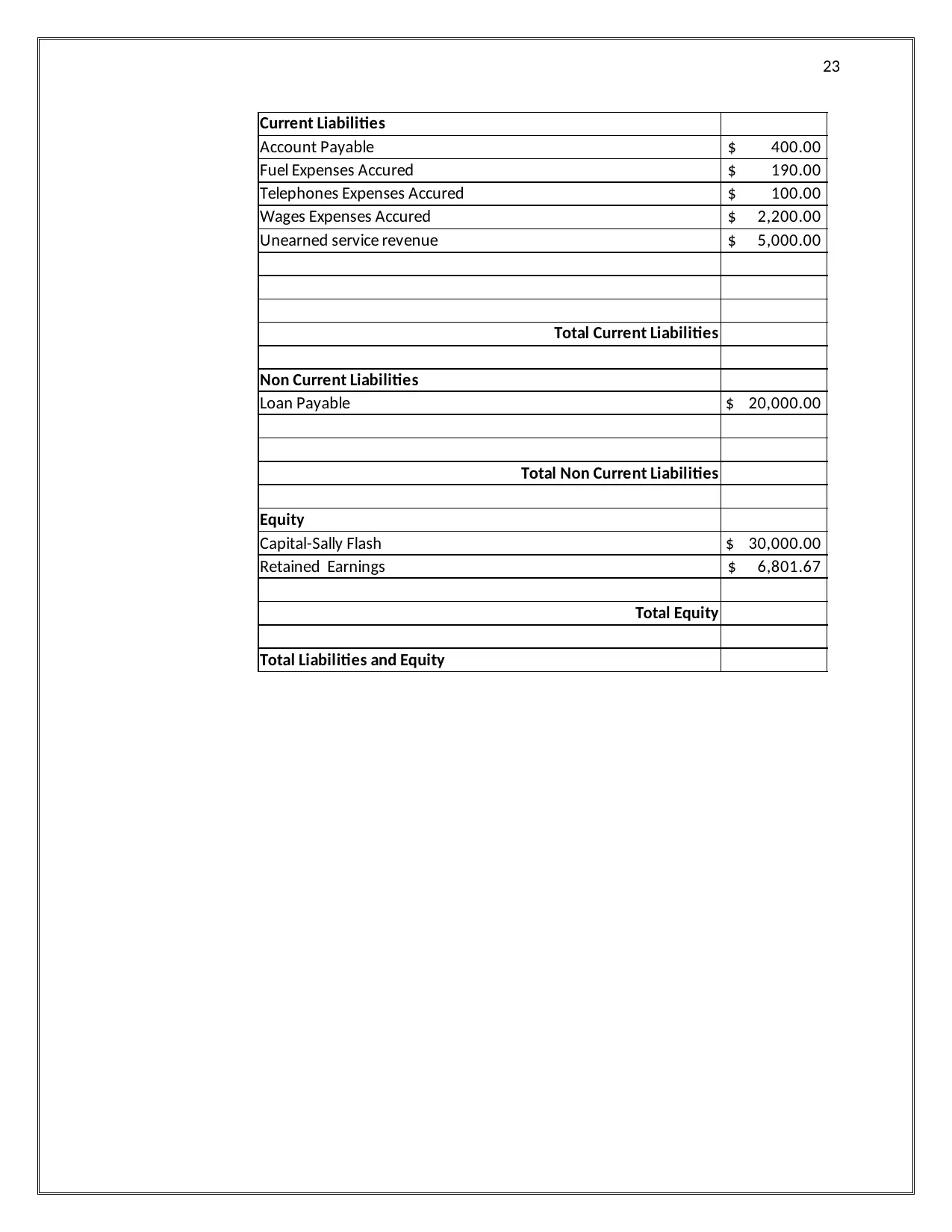

Current Liabilities

Account Payable $ 400.00

Fuel Expenses Accured $ 190.00

Telephones Expenses Accured $ 100.00

Wages Expenses Accured $ 2,200.00

Unearned service revenue $ 5,000.00

Total Current Liabilities

Non Current Liabilities

Loan Payable $ 20,000.00

Total Non Current Liabilities

Equity

Capital-Sally Flash $ 30,000.00

Retained Earnings $ 6,801.67

Total Equity

Total Liabilities and Equity

Current Liabilities

Account Payable $ 400.00

Fuel Expenses Accured $ 190.00

Telephones Expenses Accured $ 100.00

Wages Expenses Accured $ 2,200.00

Unearned service revenue $ 5,000.00

Total Current Liabilities

Non Current Liabilities

Loan Payable $ 20,000.00

Total Non Current Liabilities

Equity

Capital-Sally Flash $ 30,000.00

Retained Earnings $ 6,801.67

Total Equity

Total Liabilities and Equity

24

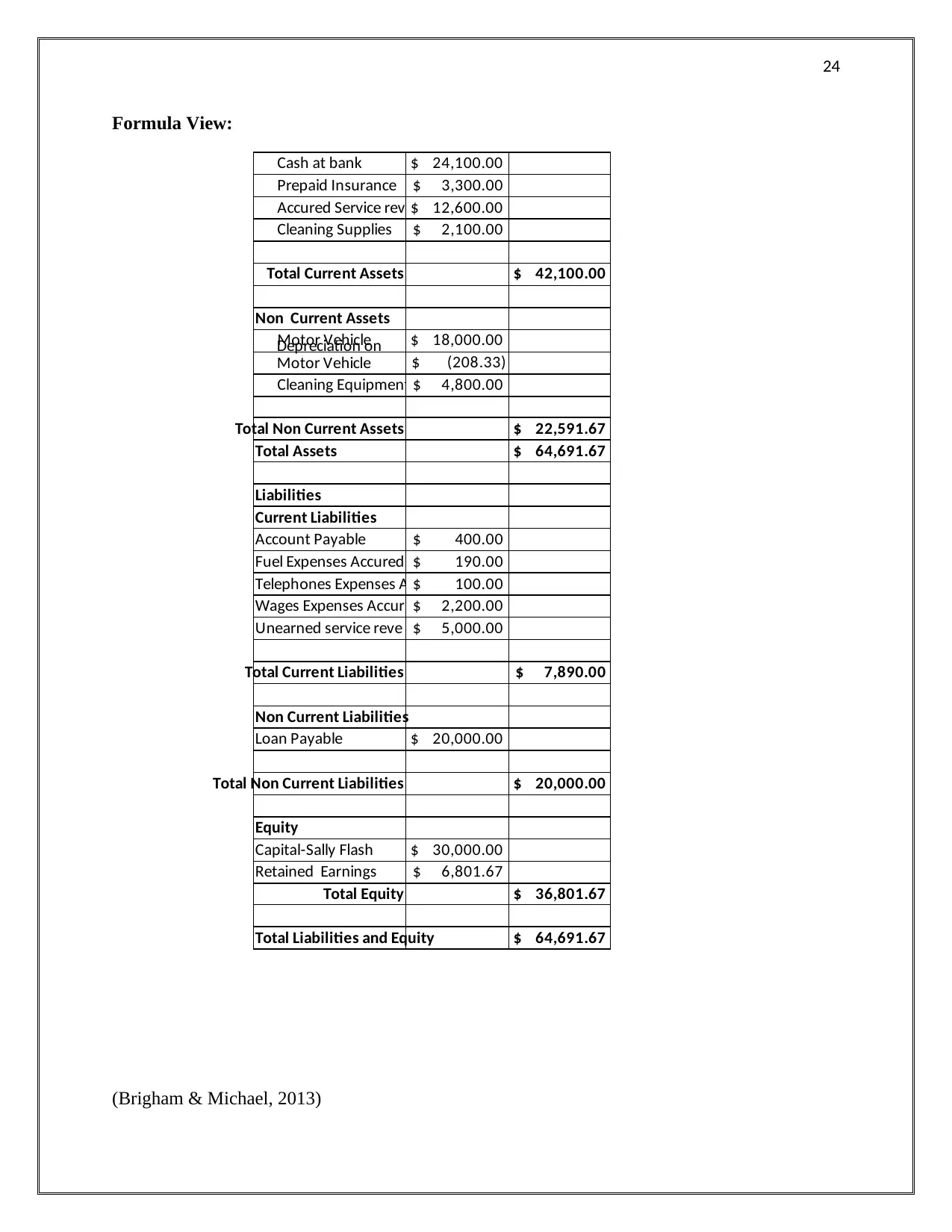

Formula View:

Cash at bank $ 24,100.00

Prepaid Insurance $ 3,300.00

Accured Service rev $ 12,600.00

Cleaning Supplies $ 2,100.00

Total Current Assets $ 42,100.00

Non Current Assets

Motor Vehicle $ 18,000.00

$ (208.33)

Cleaning Equipment $ 4,800.00

Total Non Current Assets $ 22,591.67

Total Assets $ 64,691.67

Liabilities

Current Liabilities

Account Payable $ 400.00

Fuel Expenses Accured $ 190.00

Telephones Expenses A $ 100.00

Wages Expenses Accur $ 2,200.00

Unearned service reve $ 5,000.00

Total Current Liabilities $ 7,890.00

Non Current Liabilities

Loan Payable $ 20,000.00

Total Non Current Liabilities $ 20,000.00

Equity

Capital-Sally Flash $ 30,000.00

Retained Earnings $ 6,801.67

Total Equity $ 36,801.67

Total Liabilities and Equity $ 64,691.67

Depreciation on

Motor Vehicle

(Brigham & Michael, 2013)

Formula View:

Cash at bank $ 24,100.00

Prepaid Insurance $ 3,300.00

Accured Service rev $ 12,600.00

Cleaning Supplies $ 2,100.00

Total Current Assets $ 42,100.00

Non Current Assets

Motor Vehicle $ 18,000.00

$ (208.33)

Cleaning Equipment $ 4,800.00

Total Non Current Assets $ 22,591.67

Total Assets $ 64,691.67

Liabilities

Current Liabilities

Account Payable $ 400.00

Fuel Expenses Accured $ 190.00

Telephones Expenses A $ 100.00

Wages Expenses Accur $ 2,200.00

Unearned service reve $ 5,000.00

Total Current Liabilities $ 7,890.00

Non Current Liabilities

Loan Payable $ 20,000.00

Total Non Current Liabilities $ 20,000.00

Equity

Capital-Sally Flash $ 30,000.00

Retained Earnings $ 6,801.67

Total Equity $ 36,801.67

Total Liabilities and Equity $ 64,691.67

Depreciation on

Motor Vehicle

(Brigham & Michael, 2013)

25

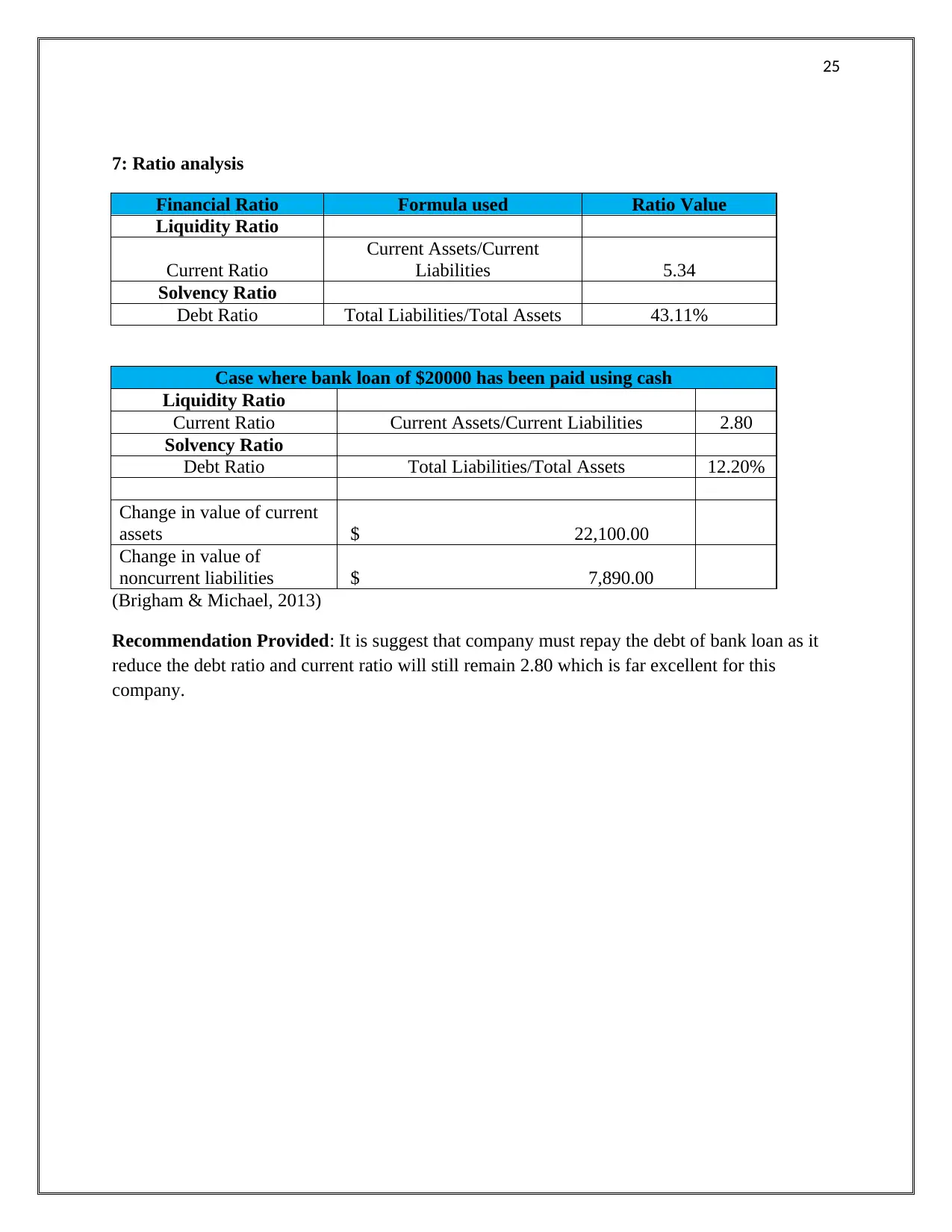

7: Ratio analysis

Financial Ratio Formula used Ratio Value

Liquidity Ratio

Current Ratio

Current Assets/Current

Liabilities 5.34

Solvency Ratio

Debt Ratio Total Liabilities/Total Assets 43.11%

Case where bank loan of $20000 has been paid using cash

Liquidity Ratio

Current Ratio Current Assets/Current Liabilities 2.80

Solvency Ratio

Debt Ratio Total Liabilities/Total Assets 12.20%

Change in value of current

assets $ 22,100.00

Change in value of

noncurrent liabilities $ 7,890.00

(Brigham & Michael, 2013)

Recommendation Provided: It is suggest that company must repay the debt of bank loan as it

reduce the debt ratio and current ratio will still remain 2.80 which is far excellent for this

company.

7: Ratio analysis

Financial Ratio Formula used Ratio Value

Liquidity Ratio

Current Ratio

Current Assets/Current

Liabilities 5.34

Solvency Ratio

Debt Ratio Total Liabilities/Total Assets 43.11%

Case where bank loan of $20000 has been paid using cash

Liquidity Ratio

Current Ratio Current Assets/Current Liabilities 2.80

Solvency Ratio

Debt Ratio Total Liabilities/Total Assets 12.20%

Change in value of current

assets $ 22,100.00

Change in value of

noncurrent liabilities $ 7,890.00

(Brigham & Michael, 2013)

Recommendation Provided: It is suggest that company must repay the debt of bank loan as it

reduce the debt ratio and current ratio will still remain 2.80 which is far excellent for this

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

26

Question 2:

Topic: Double entry bookkeeping system

Introduction

Business accounting practice have undergone major changes since its evolution and new

accounting systems have been emerged for bookkeeping to record the business transactions and

produce financial statements. Among all the business accounting systems, Double entry

bookkeeping has received great importance and all the modern accounting software and business

accounting is based on the principle defined under this system. This essay has been drafted to

provide discussion on origin of double entry bookkeeping in the world of accounting and in

addition to this importance of double entry system has been discussed in detail. This essay will

provide the insight on how the double entry bookkeeping differ from the earlier bookkeeping

methods.

Discussion on origin of double entry bookkeeping process through explaining its

importance and how it differs from earlier bookkeeping methods

Origin of Double entry bookkeeping

Double entry bookkeeping system has been invented and developed by an Italian writer

name Luca Pacioli in year 1494. The double entry bookkeeping method has been regarded as the

part of the accounting system for very long period and it has been evolved since its origin.

Double entry bookkeeping method has been used for recoding the business transactions and it is

also useful to make the financial statements. Since the bookkeeping has been come in existence it

has undergone several changes and among those changes double entry bookkeeping is the major

change (Walshaw, 2018). This system has changed the way accounting was being performed and

it has completely modified the structure of keeping the account books. As discussed above Luca

Pacioli has invented this system in year 1494 and it has written first book on double entry

bookkeeping and after than this system of accounting has gained major attention by the many of

the accountant worldwide. Luca Pacioli has treated as the father of accounting as he has given

the base on whole business accounting can be performed. Before the evolution of double entry

bookkeeping, it is not possible to make record every type of business transactions as there are

many transactions that impact many business accounts at the same time which is not possible to

record in single entry bookkeeping. Double entry bookkeeping has helped small as well as large

enterprises to make record of the business transactions and make financial statements to verify

the accuracy as well as to make better presentation of accounts. It is not possible in the case of

single entry bookkeeping (Gleeson-White, 2011).

Importance of double entry bookkeeping

Question 2:

Topic: Double entry bookkeeping system

Introduction

Business accounting practice have undergone major changes since its evolution and new

accounting systems have been emerged for bookkeeping to record the business transactions and

produce financial statements. Among all the business accounting systems, Double entry

bookkeeping has received great importance and all the modern accounting software and business

accounting is based on the principle defined under this system. This essay has been drafted to

provide discussion on origin of double entry bookkeeping in the world of accounting and in

addition to this importance of double entry system has been discussed in detail. This essay will

provide the insight on how the double entry bookkeeping differ from the earlier bookkeeping

methods.

Discussion on origin of double entry bookkeeping process through explaining its

importance and how it differs from earlier bookkeeping methods

Origin of Double entry bookkeeping

Double entry bookkeeping system has been invented and developed by an Italian writer

name Luca Pacioli in year 1494. The double entry bookkeeping method has been regarded as the

part of the accounting system for very long period and it has been evolved since its origin.

Double entry bookkeeping method has been used for recoding the business transactions and it is

also useful to make the financial statements. Since the bookkeeping has been come in existence it

has undergone several changes and among those changes double entry bookkeeping is the major

change (Walshaw, 2018). This system has changed the way accounting was being performed and

it has completely modified the structure of keeping the account books. As discussed above Luca

Pacioli has invented this system in year 1494 and it has written first book on double entry

bookkeeping and after than this system of accounting has gained major attention by the many of

the accountant worldwide. Luca Pacioli has treated as the father of accounting as he has given

the base on whole business accounting can be performed. Before the evolution of double entry

bookkeeping, it is not possible to make record every type of business transactions as there are

many transactions that impact many business accounts at the same time which is not possible to

record in single entry bookkeeping. Double entry bookkeeping has helped small as well as large

enterprises to make record of the business transactions and make financial statements to verify

the accuracy as well as to make better presentation of accounts. It is not possible in the case of

single entry bookkeeping (Gleeson-White, 2011).

Importance of double entry bookkeeping

27

Double entry booking is also refers to as modern day accounting as this has not been

changed since it has been evolved. The principle on which it has been based it that every

business transactions impacts two accounts and it can be also verified through cross checking the

same. Double entry bookkeeping has its importance due to its accuracy, reliability and presenting

of the accounting information. The business transaction when entered in the books of accounting

it impacts two accounts and transaction entry has debit and credit balance associated with it. For

example, when owner of the business bring in capital in form of cash to the business than this

accounting entry will impact two accounts, one is cash account which is debited (as amount is

received) and other account is capital account which is credit (as it is liability for the business). It

means every debit entry there is equal credit entry which is main reason this system of

accounting is highly accurate and if any error occurred can be rectified or identifies easily

(Walshaw, 2018). Double entry bookkeeping consists of following stages:

Recording and classification of transactions: It is the initial stage where all the business

transactions are recorded in form of journal entries and posting them ledger accounts.

Adjusting entries and preparation of trial balance: After ledgers have been made,

adjusting entries will be done at the year end and

Preparation of final accounts: Preparation of final accounts requires drafting profit &loss

account, balance sheet and statement of change in equity (Gleeson-White, 2011).

Some of the major advantages of double entry bookkeeping are as follows:

Reliability: As this system of accounting records every business transaction two times in

books of accounts that helps to create the equilibrium of the financial records in the

books of account. Each and every business transaction can be easily verified and cross

checked after they have been entered in the books of accounts. In this was reliability of

bookkeeping is highly increased.

Accuracy: Accuracy of financial records is greatly increased through use of double entry

bookkeeping (Andreica, 2016)

Preparation of financial statements: Through use of double entry bookkeeping one can

prepare financial statements such as income statement, balance sheet and other statements

Promotes comparability of financial information: It promotes comparability of financial

information as financial statements of two years can be easily compared with each other

and also it can compared with other company financial statements (Wolfe, 2019)

Difference between double entry bookkeeping and earlier method book keeping

The major difference that is present between double and single entry system of

bookkeeping is difference in the records of financial transactions. The double entry bookkeeping

system involves recording of a financial transactions twice while single entry system involves

recording it only once (Hofstrand, 2009). The double entry system involves developing different

types of accounts such as assets, liability, capital, expenses and revenue while singe entry system

Double entry booking is also refers to as modern day accounting as this has not been

changed since it has been evolved. The principle on which it has been based it that every

business transactions impacts two accounts and it can be also verified through cross checking the

same. Double entry bookkeeping has its importance due to its accuracy, reliability and presenting

of the accounting information. The business transaction when entered in the books of accounting

it impacts two accounts and transaction entry has debit and credit balance associated with it. For

example, when owner of the business bring in capital in form of cash to the business than this

accounting entry will impact two accounts, one is cash account which is debited (as amount is

received) and other account is capital account which is credit (as it is liability for the business). It

means every debit entry there is equal credit entry which is main reason this system of

accounting is highly accurate and if any error occurred can be rectified or identifies easily

(Walshaw, 2018). Double entry bookkeeping consists of following stages:

Recording and classification of transactions: It is the initial stage where all the business

transactions are recorded in form of journal entries and posting them ledger accounts.

Adjusting entries and preparation of trial balance: After ledgers have been made,

adjusting entries will be done at the year end and

Preparation of final accounts: Preparation of final accounts requires drafting profit &loss

account, balance sheet and statement of change in equity (Gleeson-White, 2011).

Some of the major advantages of double entry bookkeeping are as follows:

Reliability: As this system of accounting records every business transaction two times in

books of accounts that helps to create the equilibrium of the financial records in the

books of account. Each and every business transaction can be easily verified and cross

checked after they have been entered in the books of accounts. In this was reliability of

bookkeeping is highly increased.

Accuracy: Accuracy of financial records is greatly increased through use of double entry

bookkeeping (Andreica, 2016)

Preparation of financial statements: Through use of double entry bookkeeping one can

prepare financial statements such as income statement, balance sheet and other statements

Promotes comparability of financial information: It promotes comparability of financial

information as financial statements of two years can be easily compared with each other

and also it can compared with other company financial statements (Wolfe, 2019)

Difference between double entry bookkeeping and earlier method book keeping

The major difference that is present between double and single entry system of

bookkeeping is difference in the records of financial transactions. The double entry bookkeeping

system involves recording of a financial transactions twice while single entry system involves

recording it only once (Hofstrand, 2009). The double entry system involves developing different

types of accounts such as assets, liability, capital, expenses and revenue while singe entry system

28

involves maintaining of cash and personal accounts. The double entry system of accounting

involves easier detection of mistakes and deflections whereas single entry system involves the

occurrence of large number of error and frauds due to lack of accuracy in financial reporting.

The double entry system involves following a systematic method of recording the financial

transactions in the journals and then to ledger and developing a trial balance. However, the

method of single entry bookkeeping does not follow any systematic procedure and does not

involve developing journal, ledge or trail balance (Suntook, 2010).

Conclusion

It can be said from the overall discussion held in the essay that double entry booking

system has been widely used by businesses all over the world after it was highlighted by the

Luca Pacioli book. The method is regarded to be superior than single entry system of

bookkeeping as it helps in maintaining accuracy in the accounting information thus facilitating

better decision-making of a company’s stakeholders.

involves maintaining of cash and personal accounts. The double entry system of accounting

involves easier detection of mistakes and deflections whereas single entry system involves the

occurrence of large number of error and frauds due to lack of accuracy in financial reporting.

The double entry system involves following a systematic method of recording the financial

transactions in the journals and then to ledger and developing a trial balance. However, the

method of single entry bookkeeping does not follow any systematic procedure and does not

involve developing journal, ledge or trail balance (Suntook, 2010).

Conclusion

It can be said from the overall discussion held in the essay that double entry booking

system has been widely used by businesses all over the world after it was highlighted by the

Luca Pacioli book. The method is regarded to be superior than single entry system of

bookkeeping as it helps in maintaining accuracy in the accounting information thus facilitating

better decision-making of a company’s stakeholders.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

29

Answer 3: ABC Learning Case Study

Part 1: Reasons for ABC Learning’s Failure and Identifying Warning Signs in the

Company’s Financial Reports Indicating the Company Trouble

ABC Learning Centre that was once recognized to be one of the largest childcare

providers across the world collapsed on account of its fraudulent financial accounting practices.

The company was established in the year 1988 and since then has recorded enormous growth on

account of its acquisition and expansion plans. The company was established as a non-profit

organization that intends to provide childcare services and carried out its operations through

subsidy provided by government. The company gained rapid expansion after the government

decided to grant subsidy in the form of direct cash payment. The company utilizes the subsidy

provided to acquire properties and establishing its child care centers within prime locations. It

has been estimated that the company by the end of the year 2005 has established about 660

centers across Australia and has also gained international expansion by opening its stores within

the US and the UK. Its market capitalization has been rapidly increased through acquisitions and

has reported after-tax profit of about $143.1 million in the year 2007 before its collapse. The

company collapsed during the time of global financial crisis due to its inability to repay huge

debts at the times of economic and financial breakdown of capital market. The company was

liquidated in the year 2008 and it has to sell 60 per cent of its US and UK subsidiary for meeting

its debt repayments (Smith & Betts, 2008).

It has been identified by the investigation held by the Australian Securities and

Investments Commission (ASIC) that major reason for the failure of the company is the use of

fraudulent accounting practices. The company implemented the financial reporting practices for

creating apparent value for shareholders that is based on the future net cash flows of the

company that are expected to be realized (Walsh, 2011). This is largely on account of the use of

fair value accounting practices that reports the value of assets based on the future expected cash

flows and thus misleading the investors. As such, the volatility in the market at the time of global

financial crisis lead to breakdown of the company due to decline in asset value and thus causing

high debt that it was unable to repay. The company ahs rather adopted a complex business model

as stated by its new auditors after its liquidation and the major items in its balance sheet such as

assets, derivates, and goodwill and intangible assets were largely difficult to be valued. As such,

it has been stated by ASIC that the main reason for the collapse of the company it is business

model, faulty accounting practices, aggressive acquisitions and high capital expenditure for

acquiring properties to establish its child care centers.

It has been stated by Ernst & Young, the new auditor of the company after it went into

administrative receivership that there were many red flags in the financial statements of the

company before its collapse that indicates its troublesome situation. These were rapid increase in

its profitability through acquisitions that have raised concerns regarding the underlying value of

its assets out of which about 70 per cent were intangibles. The regulator was not able to identify

Answer 3: ABC Learning Case Study

Part 1: Reasons for ABC Learning’s Failure and Identifying Warning Signs in the

Company’s Financial Reports Indicating the Company Trouble

ABC Learning Centre that was once recognized to be one of the largest childcare

providers across the world collapsed on account of its fraudulent financial accounting practices.

The company was established in the year 1988 and since then has recorded enormous growth on

account of its acquisition and expansion plans. The company was established as a non-profit

organization that intends to provide childcare services and carried out its operations through

subsidy provided by government. The company gained rapid expansion after the government

decided to grant subsidy in the form of direct cash payment. The company utilizes the subsidy

provided to acquire properties and establishing its child care centers within prime locations. It

has been estimated that the company by the end of the year 2005 has established about 660

centers across Australia and has also gained international expansion by opening its stores within

the US and the UK. Its market capitalization has been rapidly increased through acquisitions and

has reported after-tax profit of about $143.1 million in the year 2007 before its collapse. The

company collapsed during the time of global financial crisis due to its inability to repay huge

debts at the times of economic and financial breakdown of capital market. The company was

liquidated in the year 2008 and it has to sell 60 per cent of its US and UK subsidiary for meeting

its debt repayments (Smith & Betts, 2008).

It has been identified by the investigation held by the Australian Securities and

Investments Commission (ASIC) that major reason for the failure of the company is the use of

fraudulent accounting practices. The company implemented the financial reporting practices for

creating apparent value for shareholders that is based on the future net cash flows of the

company that are expected to be realized (Walsh, 2011). This is largely on account of the use of

fair value accounting practices that reports the value of assets based on the future expected cash

flows and thus misleading the investors. As such, the volatility in the market at the time of global

financial crisis lead to breakdown of the company due to decline in asset value and thus causing

high debt that it was unable to repay. The company ahs rather adopted a complex business model

as stated by its new auditors after its liquidation and the major items in its balance sheet such as

assets, derivates, and goodwill and intangible assets were largely difficult to be valued. As such,

it has been stated by ASIC that the main reason for the collapse of the company it is business

model, faulty accounting practices, aggressive acquisitions and high capital expenditure for

acquiring properties to establish its child care centers.

It has been stated by Ernst & Young, the new auditor of the company after it went into

administrative receivership that there were many red flags in the financial statements of the

company before its collapse that indicates its troublesome situation. These were rapid increase in

its profitability through acquisitions that have raised concerns regarding the underlying value of

its assets out of which about 70 per cent were intangibles. The regulator was not able to identify

30

the issue of massive intangible assets possessed by the company that played a significant role in

promoting its business expansion and leading to its collapse. There was lack of independent

opinion provided by the company’s auditors in its financial reports questioning the credibility

and reliability of its financial statements.

Part 2: Identification and discussion of ethical issues from this case study

The analysis of the ABC Learning case study has presented the following ethical issues:

Lack of Adequate Corporate Governance System: The major reason that is responsible

for the breakdown of ABC Learning is attributed to be the lack of an adequate corporate

governance system. The presence of an effective corporate governance system is essential

to establish ethical code of conduct within workplace for monitoring and reviewing the

daily operational activities of a corporation. As such, there were prevalence of faulty

accounting practices and development of complex business model in which assets were

valued inappropriately. Thus, the absence of an adequate corporate governance system

within the company lead to un-identification of the internet financial debt risk and thus

eventually leading to its collapse at the time of challenging financial condition during

crisis of the year 2007. Thus, the failure of the company ahs emphasize on the presence

of an adequate corporate governance system within an organization for regulatory and

monitoring its functions and activities as per ethical standards and guidelines.

Lack of Transparency: ABC Learning has developed a complicated business model and

as such there was lack of adequate transparency in its financial reporting system. It was

largely difficult to assess the value of different financial items and thus it was different to

estimate the debt payment of the company. The lack of transparency in the business

operations leads to the inability of the company for identifying its debt obligations which

became a major reason for its collapse.

Professional Competence: It has been analyzed the board members of the company were

mainly politicians who lack sufficient expertise and knowledge to carry out the business

operations. As such, there was lack of adequate risk management system for identifying

the potential risks in advance. Also, the senior managers were not able to conduct

business operations adequate in the lack of ethical policies and procedures that are

developed by the Board. As such, they adopted the use of faulty accounting practices

leading to higher earning potential of the company and negatively impacting the interest

and welfare of the stakeholders.

the issue of massive intangible assets possessed by the company that played a significant role in

promoting its business expansion and leading to its collapse. There was lack of independent

opinion provided by the company’s auditors in its financial reports questioning the credibility

and reliability of its financial statements.

Part 2: Identification and discussion of ethical issues from this case study

The analysis of the ABC Learning case study has presented the following ethical issues:

Lack of Adequate Corporate Governance System: The major reason that is responsible

for the breakdown of ABC Learning is attributed to be the lack of an adequate corporate

governance system. The presence of an effective corporate governance system is essential

to establish ethical code of conduct within workplace for monitoring and reviewing the

daily operational activities of a corporation. As such, there were prevalence of faulty

accounting practices and development of complex business model in which assets were

valued inappropriately. Thus, the absence of an adequate corporate governance system

within the company lead to un-identification of the internet financial debt risk and thus

eventually leading to its collapse at the time of challenging financial condition during

crisis of the year 2007. Thus, the failure of the company ahs emphasize on the presence

of an adequate corporate governance system within an organization for regulatory and

monitoring its functions and activities as per ethical standards and guidelines.

Lack of Transparency: ABC Learning has developed a complicated business model and

as such there was lack of adequate transparency in its financial reporting system. It was

largely difficult to assess the value of different financial items and thus it was different to

estimate the debt payment of the company. The lack of transparency in the business

operations leads to the inability of the company for identifying its debt obligations which

became a major reason for its collapse.

Professional Competence: It has been analyzed the board members of the company were

mainly politicians who lack sufficient expertise and knowledge to carry out the business

operations. As such, there was lack of adequate risk management system for identifying

the potential risks in advance. Also, the senior managers were not able to conduct

business operations adequate in the lack of ethical policies and procedures that are

developed by the Board. As such, they adopted the use of faulty accounting practices

leading to higher earning potential of the company and negatively impacting the interest

and welfare of the stakeholders.

31

References

Andreica, I. (2016). Double-entry Bookkeeping versus Simple-entry Bookkeeping. Horticulture

73(2), 282-290.

Brigham, F., & Michael C. (2013). Financial management: Theory & practice. Canada: Cengage

Learning.

Damodaran, A, (2011). Applied corporate finance. USA: John Wiley & sons.

Davies, T. & Crawford, I. (2011). Business accounting and finance. USA: Pearson.

Gleeson-White, J. (2011). Double Entry: How the merchants of Venice shaped the modern world

- and how their invention could make or break the planet. Sydney: Allen & Unwin.

Hofstrand, L. (2009). Understanding Double Entry Accounting. Retrieved 3 April, 2019, from

https://www.extension.iastate.edu/agdm/wholefarm/pdf/c6-33.pdf

Smith, P. & Betts, P. (2008). ABC Learning’s failure sparks governance debate. Retrieved 3

April, 2019, from https://www.ft.com/content/6afc9090-ac2d-11dd-aa46-000077b07658

Suntook, Z. (2010). Learning Accountancy: The Novel Way. UK: Cambridge Scholars

Publishing.

Walsh, L. (2011). ABC Learning childcare founder Eddy Groves to face criminal charges.

Retrieved 3 April, 2019, from https://www.dailytelegraph.com.au/abc-childcare-founder-

eddy-groves-to-face-criminal-charges/news-story/e7bcc24885b3dbf9078f3d4730d4ba59?

sv=9203b5f4be6a30ed1819f72aa0d1e61e

Walshaw, T. (2018). Double Entry Bookkeeping. Lulu.com.

Wolfe, L. 2019. Double-Entry Bookkeeping vs Single-Entry Accounting. Retrieved 2 April,

2019, from https://www.thebalancecareers.com/double-vs-single-entry-3515788

References

Andreica, I. (2016). Double-entry Bookkeeping versus Simple-entry Bookkeeping. Horticulture

73(2), 282-290.

Brigham, F., & Michael C. (2013). Financial management: Theory & practice. Canada: Cengage

Learning.

Damodaran, A, (2011). Applied corporate finance. USA: John Wiley & sons.

Davies, T. & Crawford, I. (2011). Business accounting and finance. USA: Pearson.

Gleeson-White, J. (2011). Double Entry: How the merchants of Venice shaped the modern world

- and how their invention could make or break the planet. Sydney: Allen & Unwin.

Hofstrand, L. (2009). Understanding Double Entry Accounting. Retrieved 3 April, 2019, from

https://www.extension.iastate.edu/agdm/wholefarm/pdf/c6-33.pdf

Smith, P. & Betts, P. (2008). ABC Learning’s failure sparks governance debate. Retrieved 3

April, 2019, from https://www.ft.com/content/6afc9090-ac2d-11dd-aa46-000077b07658

Suntook, Z. (2010). Learning Accountancy: The Novel Way. UK: Cambridge Scholars

Publishing.

Walsh, L. (2011). ABC Learning childcare founder Eddy Groves to face criminal charges.

Retrieved 3 April, 2019, from https://www.dailytelegraph.com.au/abc-childcare-founder-

eddy-groves-to-face-criminal-charges/news-story/e7bcc24885b3dbf9078f3d4730d4ba59?

sv=9203b5f4be6a30ed1819f72aa0d1e61e

Walshaw, T. (2018). Double Entry Bookkeeping. Lulu.com.

Wolfe, L. 2019. Double-Entry Bookkeeping vs Single-Entry Accounting. Retrieved 2 April,

2019, from https://www.thebalancecareers.com/double-vs-single-entry-3515788

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.