Comparative Analysis: India and China Stock Market Finance Report

VerifiedAdded on 2023/01/05

|17

|4711

|48

Report

AI Summary

This report delves into the realm of international finance, providing a comparative analysis of the stock markets in India and China. It begins with an introduction to global finance, emphasizing the significance of foreign trade and its impact on international investment and currency valuations. The report then proceeds to compare the stock exchanges of China and India, examining their historical growth, market structures, and performance, including the effects of the COVID-19 pandemic. A detailed discussion on the Capital Market Line (CML) and the concept of dominance in portfolio management follows, alongside an analysis of various asset types and hedging instruments relevant to international finance. The report highlights the economic implications of the India-China boundary dispute and its potential impact on trade relations. By examining the performance of BSE and Shanghai stock exchanges and analyzing investment portfolios, the report offers valuable insights into the dynamics of international finance and the management of financial instruments in the context of these two major economies. The report concludes with a summary of key findings and references used.

Management of

International Finance

International Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1. Introduction .................................................................................................................................3

2. Comparative Analysis, Appraisal on Stock and the Fund Market Appraisal .............................3

3. Discussion A CML and Dominance............................................................................................8

4. Hedging Instruments..................................................................................................................15

5. CONCLUSION .........................................................................................................................16

6. REFERENCES .........................................................................................................................18

1. Introduction .................................................................................................................................3

2. Comparative Analysis, Appraisal on Stock and the Fund Market Appraisal .............................3

3. Discussion A CML and Dominance............................................................................................8

4. Hedging Instruments..................................................................................................................15

5. CONCLUSION .........................................................................................................................16

6. REFERENCES .........................................................................................................................18

1. Introduction

The analysis of monetary relations among two countries is global finance, also referred to as

foreign economics and finance, concentrating on fields such as international investment

including exchange commodity prices. The most significant influencer in economic wealth and

development is undoubtedly foreign trade. Yet there are questions over the fact that the United

States has moved from being the biggest foreign borrower to become the world's largest

borrower throughout the world, consuming excess sums of borrowing internationally from

organisations and nations. In unpredictable ways, this can impact international finance. In order

to measure the actual buying power of various currencies, minimum wage is the comparison of

costs in various areas that used a particular product or a certain group of products.

An equilibrium condition in which shareholders are oblivious to borrowing costs added to

deposit accounts in 2 distinct nations is defined by interest rate parity. In this report, investment

portfolio of two countries India and China have been discussed (Madura, 2020).

A collection of securities and other commodities that rely on overseas markets instead of

local companies is an international account. A foreign portfolio, if well planned, gives the

shareholder access to developing and established markets and offers liquidity. An international

portfolio applies to shareholders who by switching away from a household portfolio, wish to

diversify their holdings. Owing to possible political and economic uncertainty in some

developing markets, this sort of investment will bear higher incidence. There is also a possibility

that the economy of an international market could fall in value against the Dollar.

2. Comparative Analysis, Appraisal on Stock and the Fund Market Appraisal

In terms of comparison of China and India stock exchange, we can see that both nations have

larger number of stock exchanges. The rationale behind this is because of huge number of

population which leads to more amount of investment during a particular time period.

Underneath explanation of each nation's stock market is done in such manner which is as

follows:

China- During year 2006 to October 2007, the growth of Chinese market was on peak. China is a

nation that has number of savers which shows that there is saving rate is of 40%. In the same

time period, in China brokerage account opened at the rate of 2 Lakhs on each day. In china there

The analysis of monetary relations among two countries is global finance, also referred to as

foreign economics and finance, concentrating on fields such as international investment

including exchange commodity prices. The most significant influencer in economic wealth and

development is undoubtedly foreign trade. Yet there are questions over the fact that the United

States has moved from being the biggest foreign borrower to become the world's largest

borrower throughout the world, consuming excess sums of borrowing internationally from

organisations and nations. In unpredictable ways, this can impact international finance. In order

to measure the actual buying power of various currencies, minimum wage is the comparison of

costs in various areas that used a particular product or a certain group of products.

An equilibrium condition in which shareholders are oblivious to borrowing costs added to

deposit accounts in 2 distinct nations is defined by interest rate parity. In this report, investment

portfolio of two countries India and China have been discussed (Madura, 2020).

A collection of securities and other commodities that rely on overseas markets instead of

local companies is an international account. A foreign portfolio, if well planned, gives the

shareholder access to developing and established markets and offers liquidity. An international

portfolio applies to shareholders who by switching away from a household portfolio, wish to

diversify their holdings. Owing to possible political and economic uncertainty in some

developing markets, this sort of investment will bear higher incidence. There is also a possibility

that the economy of an international market could fall in value against the Dollar.

2. Comparative Analysis, Appraisal on Stock and the Fund Market Appraisal

In terms of comparison of China and India stock exchange, we can see that both nations have

larger number of stock exchanges. The rationale behind this is because of huge number of

population which leads to more amount of investment during a particular time period.

Underneath explanation of each nation's stock market is done in such manner which is as

follows:

China- During year 2006 to October 2007, the growth of Chinese market was on peak. China is a

nation that has number of savers which shows that there is saving rate is of 40%. In the same

time period, in China brokerage account opened at the rate of 2 Lakhs on each day. In china there

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is one stock exchange which is Shanghai stock exchange that is based in the city of Shanghai

China. This is the one of the stock exchange and the other one is Shenzhen stock exchange.

India- The Indian stock market is mainly exchanged on its two stock exchanges: The National

Stock Exchange (BSE) and the Stock Exchange (NSE) (NSE). The BSE has existed since 1875.

In comparison, the NSE was established in 1992 and began trading in 1994 (About comparison

of BSE and Shanghai , 2020). Both markets, however, adopt the same money system, operating

times, and method of payment.

Comparison- The Indian stock exchange is older than that of China and is much more diverse,

globalized and economy (Maxfield, 2019). Even so, the growth that the Indian stock market

achieved across upwards of a century took China just three decades to achieve. Global

investment organizations are required to be more encouraged as China's capital market begins to

speed up the starting phase. In Asia, the Indian stock exchange is regarded as the biggest. The

Bombay Stock market (BSE), the very first trading platform in Asia, was established in Mumbai

in 1875. India currently has two major national transactions: the BSE as well as the India

National Stock Exchange (NSE), which were founded in 1992 in Mumbai.

Later, China's stock market launched. At the end of 1990, the Shanghai Stock Exchange (SSE)

was created. India is more mature compared with the Chinese mainland stock exchange. The

number of international fund managers (FIIs) with high risk exposure is far higher, while the

Chinese market consists mainly of marginal private investors.

China. This is the one of the stock exchange and the other one is Shenzhen stock exchange.

India- The Indian stock market is mainly exchanged on its two stock exchanges: The National

Stock Exchange (BSE) and the Stock Exchange (NSE) (NSE). The BSE has existed since 1875.

In comparison, the NSE was established in 1992 and began trading in 1994 (About comparison

of BSE and Shanghai , 2020). Both markets, however, adopt the same money system, operating

times, and method of payment.

Comparison- The Indian stock exchange is older than that of China and is much more diverse,

globalized and economy (Maxfield, 2019). Even so, the growth that the Indian stock market

achieved across upwards of a century took China just three decades to achieve. Global

investment organizations are required to be more encouraged as China's capital market begins to

speed up the starting phase. In Asia, the Indian stock exchange is regarded as the biggest. The

Bombay Stock market (BSE), the very first trading platform in Asia, was established in Mumbai

in 1875. India currently has two major national transactions: the BSE as well as the India

National Stock Exchange (NSE), which were founded in 1992 in Mumbai.

Later, China's stock market launched. At the end of 1990, the Shanghai Stock Exchange (SSE)

was created. India is more mature compared with the Chinese mainland stock exchange. The

number of international fund managers (FIIs) with high risk exposure is far higher, while the

Chinese market consists mainly of marginal private investors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

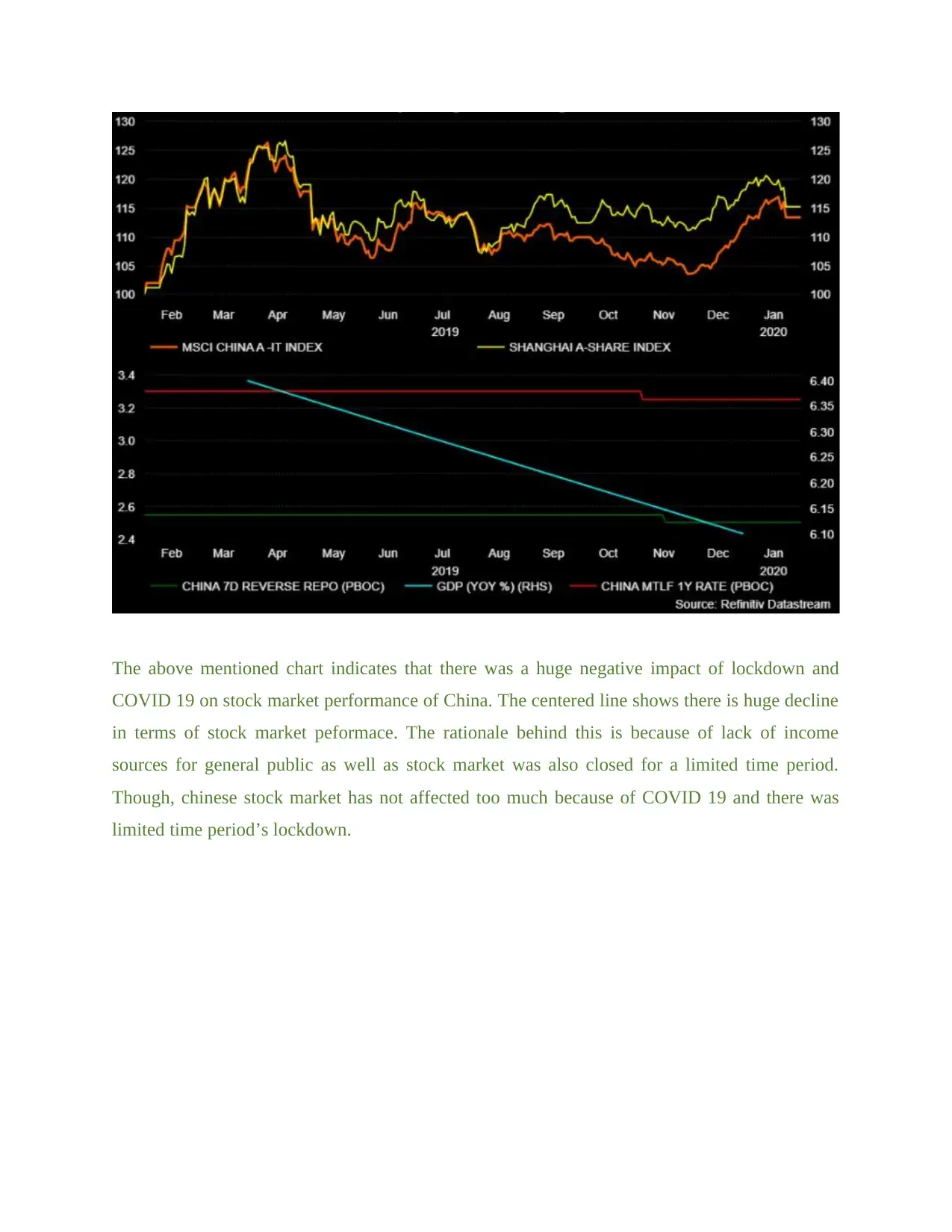

The above mentioned chart indicates that there was a huge negative impact of lockdown and

COVID 19 on stock market performance of China. The centered line shows there is huge decline

in terms of stock market peformace. The rationale behind this is because of lack of income

sources for general public as well as stock market was also closed for a limited time period.

Though, chinese stock market has not affected too much because of COVID 19 and there was

limited time period’s lockdown.

COVID 19 on stock market performance of China. The centered line shows there is huge decline

in terms of stock market peformace. The rationale behind this is because of lack of income

sources for general public as well as stock market was also closed for a limited time period.

Though, chinese stock market has not affected too much because of COVID 19 and there was

limited time period’s lockdown.

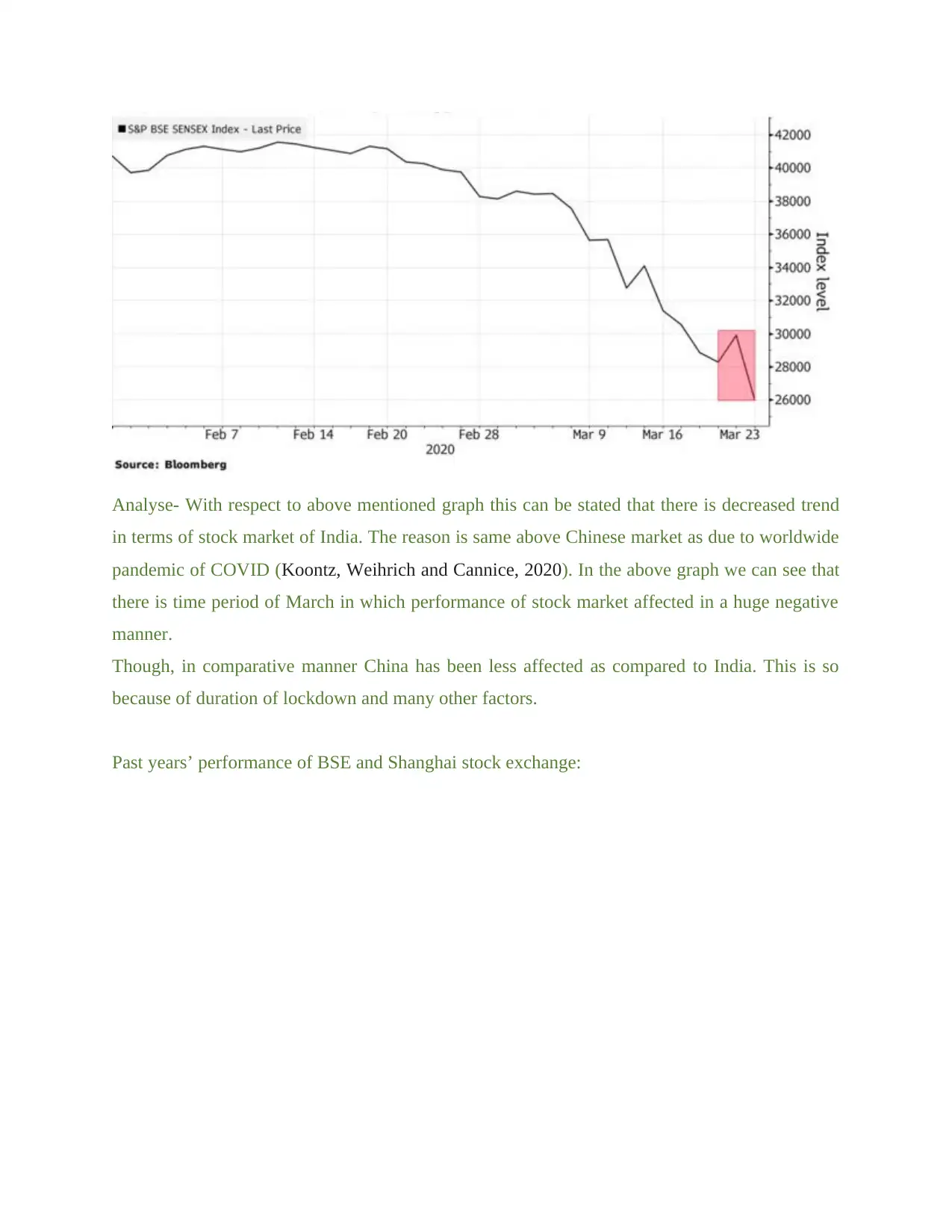

Analyse- With respect to above mentioned graph this can be stated that there is decreased trend

in terms of stock market of India. The reason is same above Chinese market as due to worldwide

pandemic of COVID (Koontz, Weihrich and Cannice, 2020). In the above graph we can see that

there is time period of March in which performance of stock market affected in a huge negative

manner.

Though, in comparative manner China has been less affected as compared to India. This is so

because of duration of lockdown and many other factors.

Past years’ performance of BSE and Shanghai stock exchange:

in terms of stock market of India. The reason is same above Chinese market as due to worldwide

pandemic of COVID (Koontz, Weihrich and Cannice, 2020). In the above graph we can see that

there is time period of March in which performance of stock market affected in a huge negative

manner.

Though, in comparative manner China has been less affected as compared to India. This is so

because of duration of lockdown and many other factors.

Past years’ performance of BSE and Shanghai stock exchange:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

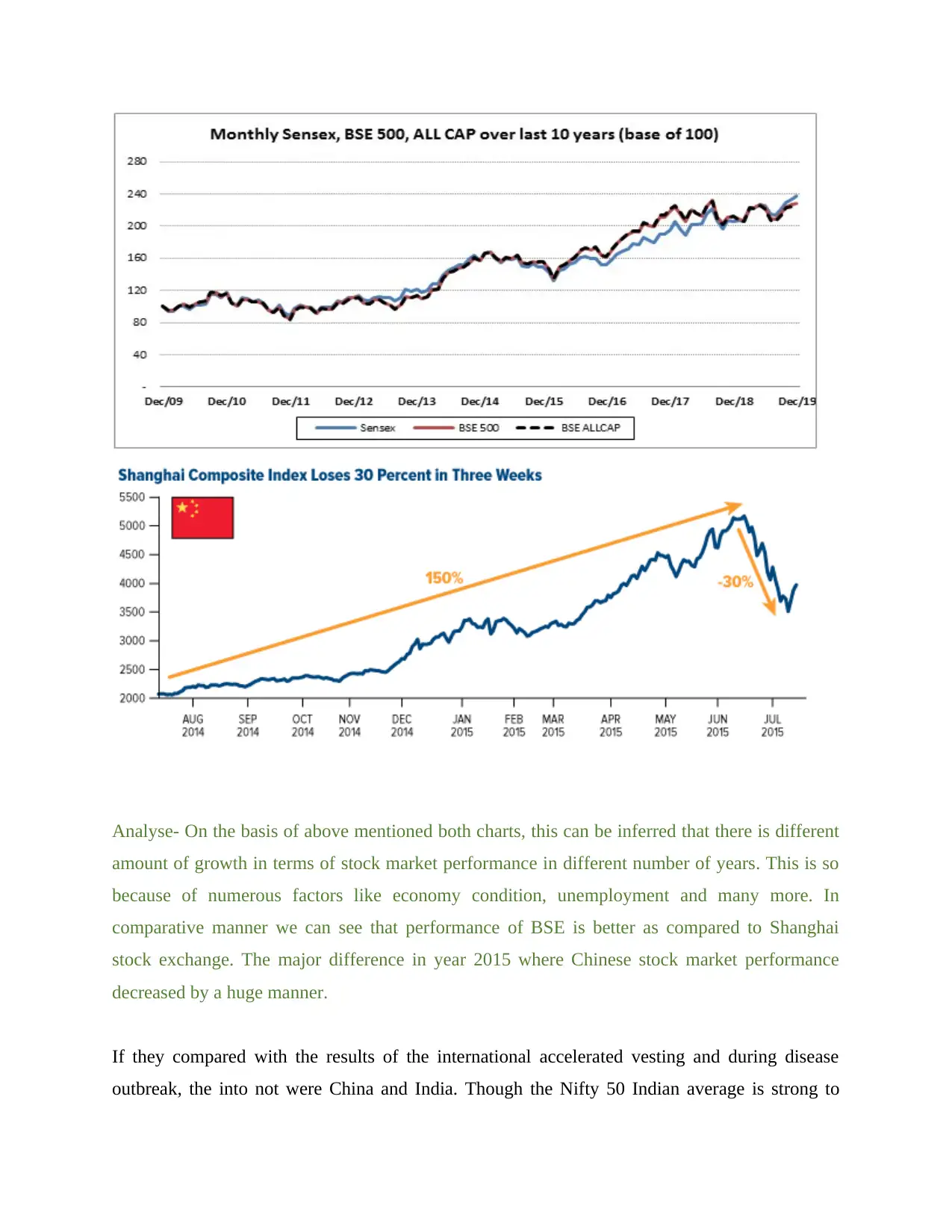

Analyse- On the basis of above mentioned both charts, this can be inferred that there is different

amount of growth in terms of stock market performance in different number of years. This is so

because of numerous factors like economy condition, unemployment and many more. In

comparative manner we can see that performance of BSE is better as compared to Shanghai

stock exchange. The major difference in year 2015 where Chinese stock market performance

decreased by a huge manner.

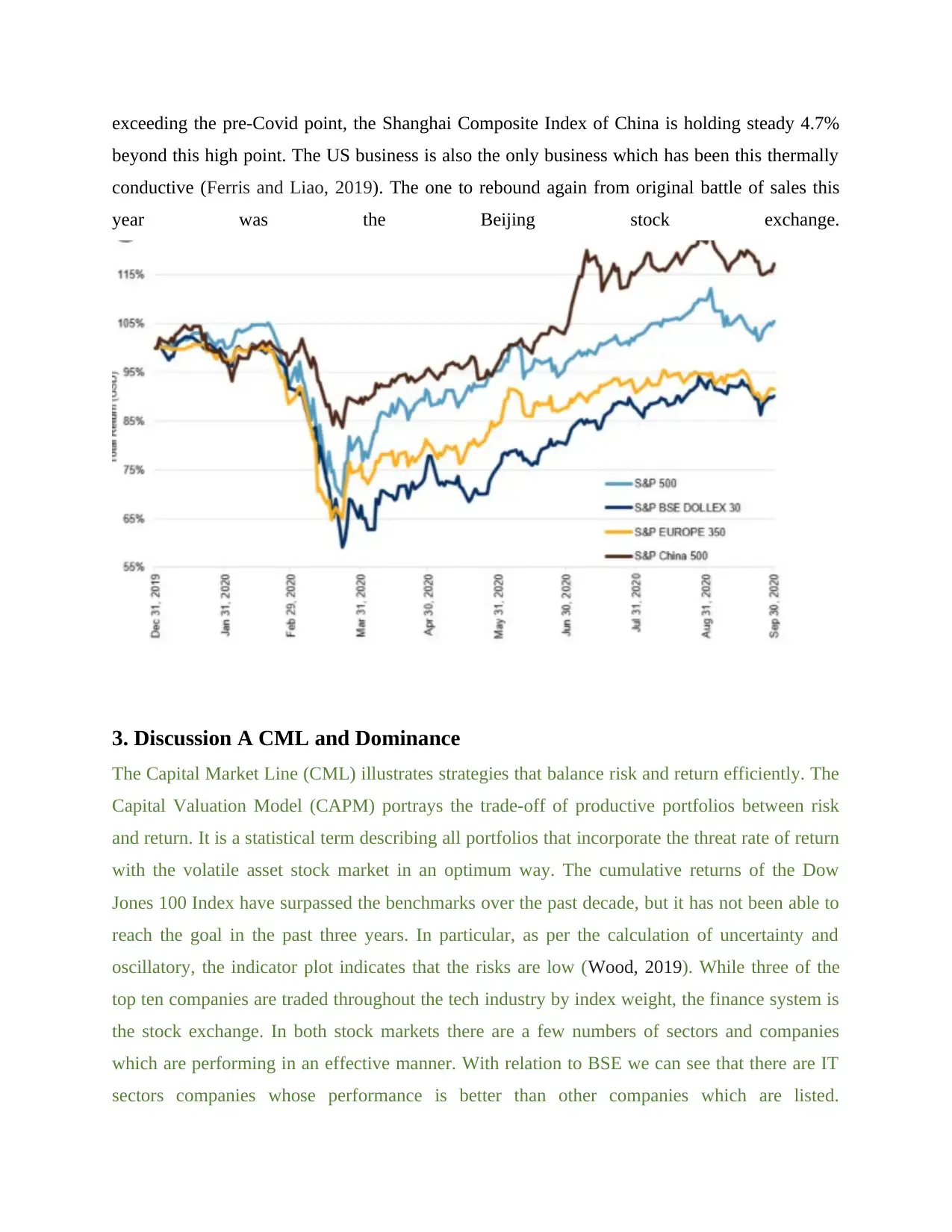

If they compared with the results of the international accelerated vesting and during disease

outbreak, the into not were China and India. Though the Nifty 50 Indian average is strong to

amount of growth in terms of stock market performance in different number of years. This is so

because of numerous factors like economy condition, unemployment and many more. In

comparative manner we can see that performance of BSE is better as compared to Shanghai

stock exchange. The major difference in year 2015 where Chinese stock market performance

decreased by a huge manner.

If they compared with the results of the international accelerated vesting and during disease

outbreak, the into not were China and India. Though the Nifty 50 Indian average is strong to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

exceeding the pre-Covid point, the Shanghai Composite Index of China is holding steady 4.7%

beyond this high point. The US business is also the only business which has been this thermally

conductive (Ferris and Liao, 2019). The one to rebound again from original battle of sales this

year was the Beijing stock exchange.

3. Discussion A CML and Dominance

The Capital Market Line (CML) illustrates strategies that balance risk and return efficiently. The

Capital Valuation Model (CAPM) portrays the trade-off of productive portfolios between risk

and return. It is a statistical term describing all portfolios that incorporate the threat rate of return

with the volatile asset stock market in an optimum way. The cumulative returns of the Dow

Jones 100 Index have surpassed the benchmarks over the past decade, but it has not been able to

reach the goal in the past three years. In particular, as per the calculation of uncertainty and

oscillatory, the indicator plot indicates that the risks are low (Wood, 2019). While three of the

top ten companies are traded throughout the tech industry by index weight, the finance system is

the stock exchange. In both stock markets there are a few numbers of sectors and companies

which are performing in an effective manner. With relation to BSE we can see that there are IT

sectors companies whose performance is better than other companies which are listed.

beyond this high point. The US business is also the only business which has been this thermally

conductive (Ferris and Liao, 2019). The one to rebound again from original battle of sales this

year was the Beijing stock exchange.

3. Discussion A CML and Dominance

The Capital Market Line (CML) illustrates strategies that balance risk and return efficiently. The

Capital Valuation Model (CAPM) portrays the trade-off of productive portfolios between risk

and return. It is a statistical term describing all portfolios that incorporate the threat rate of return

with the volatile asset stock market in an optimum way. The cumulative returns of the Dow

Jones 100 Index have surpassed the benchmarks over the past decade, but it has not been able to

reach the goal in the past three years. In particular, as per the calculation of uncertainty and

oscillatory, the indicator plot indicates that the risks are low (Wood, 2019). While three of the

top ten companies are traded throughout the tech industry by index weight, the finance system is

the stock exchange. In both stock markets there are a few numbers of sectors and companies

which are performing in an effective manner. With relation to BSE we can see that there are IT

sectors companies whose performance is better than other companies which are listed.

Companies like Reliance Jio and Tata group are higher revenue generating companies. While in

the aspect of Shanghai stock exchange manufacturing companies are leading as top revenue

generating companies.

Tata Group has access to the installation and configuration of power plants throughout the utility

space within our reporting domain. It also means that the company has been requested by the

Government of India to compile a list of Chinese imports. In addition, several individual states

have revoked company finally approved to Chinese companies (Maharashtra and Haryana). The

continuing conflict between two nations may have a larger economic influence than a physical

one (Yukhov, 2019). India-China boundary dispute is a century’s tussle. It is an incredibly

significant issue strategically and can have broader implications on the global politics of the

South Asia throughout the longer term. India had a trade surplus of USD48.6b (1.7 percent of

GDP) with China in FY20 from hardly any surplus in FY 2000. India's Chinese imports grew

sharply from just 2.6% of overall exports in FY00 to the all high to 16.4% in FY18 until slipping

to 14% (USD65.3b) in FY20 (about top trading companies in BSE, 2020). The continued

boundary disputes are subject to fluctuate mutual bilateral trade throughout the potential.

Throughout the post-COVID environment, a big change could occur. A border dispute could

contribute in the past to a shift in trade relations. India has a significant trade deficits and imports

are in most situations, an integral part of the economy. Industries such as vehicles, electronics,

bulk medicines, chemicals, imports from China and manufacturing. At the very same time, if

they actually develop alternative inside India and from other nations, China might also meet the

threat of decreased shipments to India over moment. There may be a shift in the way

multinational firms outsource from China after Covid-19. Here, India does have a chance to draw

foreign businesses to set up its industries would attract further FDI (Di Tella, 2019).

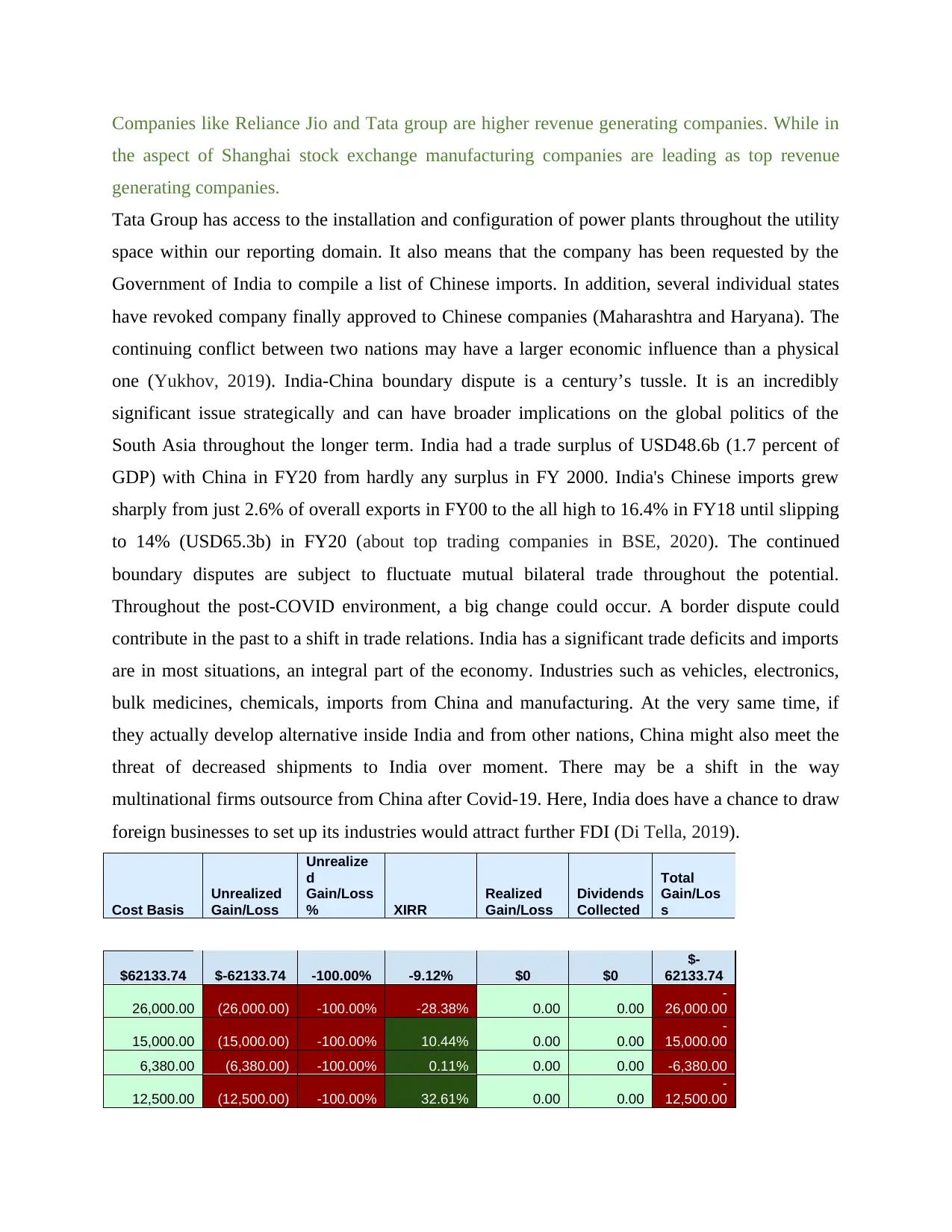

Cost Basis

Unrealized

Gain/Loss

Unrealize

d

Gain/Loss

% XIRR

Realized

Gain/Loss

Dividends

Collected

Total

Gain/Los

s

$62133.74 $-62133.74 -100.00% -9.12% $0 $0

$-

62133.74

26,000.00 (26,000.00) -100.00% -28.38% 0.00 0.00

-

26,000.00

15,000.00 (15,000.00) -100.00% 10.44% 0.00 0.00

-

15,000.00

6,380.00 (6,380.00) -100.00% 0.11% 0.00 0.00 -6,380.00

12,500.00 (12,500.00) -100.00% 32.61% 0.00 0.00

-

12,500.00

the aspect of Shanghai stock exchange manufacturing companies are leading as top revenue

generating companies.

Tata Group has access to the installation and configuration of power plants throughout the utility

space within our reporting domain. It also means that the company has been requested by the

Government of India to compile a list of Chinese imports. In addition, several individual states

have revoked company finally approved to Chinese companies (Maharashtra and Haryana). The

continuing conflict between two nations may have a larger economic influence than a physical

one (Yukhov, 2019). India-China boundary dispute is a century’s tussle. It is an incredibly

significant issue strategically and can have broader implications on the global politics of the

South Asia throughout the longer term. India had a trade surplus of USD48.6b (1.7 percent of

GDP) with China in FY20 from hardly any surplus in FY 2000. India's Chinese imports grew

sharply from just 2.6% of overall exports in FY00 to the all high to 16.4% in FY18 until slipping

to 14% (USD65.3b) in FY20 (about top trading companies in BSE, 2020). The continued

boundary disputes are subject to fluctuate mutual bilateral trade throughout the potential.

Throughout the post-COVID environment, a big change could occur. A border dispute could

contribute in the past to a shift in trade relations. India has a significant trade deficits and imports

are in most situations, an integral part of the economy. Industries such as vehicles, electronics,

bulk medicines, chemicals, imports from China and manufacturing. At the very same time, if

they actually develop alternative inside India and from other nations, China might also meet the

threat of decreased shipments to India over moment. There may be a shift in the way

multinational firms outsource from China after Covid-19. Here, India does have a chance to draw

foreign businesses to set up its industries would attract further FDI (Di Tella, 2019).

Cost Basis

Unrealized

Gain/Loss

Unrealize

d

Gain/Loss

% XIRR

Realized

Gain/Loss

Dividends

Collected

Total

Gain/Los

s

$62133.74 $-62133.74 -100.00% -9.12% $0 $0

$-

62133.74

26,000.00 (26,000.00) -100.00% -28.38% 0.00 0.00

-

26,000.00

15,000.00 (15,000.00) -100.00% 10.44% 0.00 0.00

-

15,000.00

6,380.00 (6,380.00) -100.00% 0.11% 0.00 0.00 -6,380.00

12,500.00 (12,500.00) -100.00% 32.61% 0.00 0.00

-

12,500.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7,250.00 (7,250.00) -100.00% 3.29% 0.00 0.00 -7,250.00

Response because of an expectations beating in financial statements, resources, and

health the beat proportion (net earnings reward separated by a full group of securities) increased

to 50 percent QoQ. On the basis of rising prices of raw materials and operating costs, the

profitability has increased. The local brokerage business increased the S&p bse EPS for Q1FY21

towards INR 470, up 6 percent, for FY21E as well as to INR 640 per FY22E, down 2 percent. At

present, they anticipate flat Revenue increase in FY21E versus 36% EPS growth in FY22E,

based on the expansion of EPS in the disposable consumer, finance and energy industries. The

local brokerage lifted the Nifty 50 EPS towards Rs 470, up 6 percent, for FY21E, and also for

FY22E to Rs 640, down 2 percent, since the last half, as prices settle and the market starts to

recover, monitoring the turnaround throughout the economy. BSE100's FY22E net income ratio

dropped to 30 per cent QoQ against 89 percent in the previous quarter, powered by significant

net, demonstrated and material upgrades.

B. Assets types

In the nation's infrastructure and even beyond, the biggest Chinese firms weigh heavily. The top

30 Chinese publicly listed firms, some of the larger components of the Shanghai Composite

Response because of an expectations beating in financial statements, resources, and

health the beat proportion (net earnings reward separated by a full group of securities) increased

to 50 percent QoQ. On the basis of rising prices of raw materials and operating costs, the

profitability has increased. The local brokerage business increased the S&p bse EPS for Q1FY21

towards INR 470, up 6 percent, for FY21E as well as to INR 640 per FY22E, down 2 percent. At

present, they anticipate flat Revenue increase in FY21E versus 36% EPS growth in FY22E,

based on the expansion of EPS in the disposable consumer, finance and energy industries. The

local brokerage lifted the Nifty 50 EPS towards Rs 470, up 6 percent, for FY21E, and also for

FY22E to Rs 640, down 2 percent, since the last half, as prices settle and the market starts to

recover, monitoring the turnaround throughout the economy. BSE100's FY22E net income ratio

dropped to 30 per cent QoQ against 89 percent in the previous quarter, powered by significant

net, demonstrated and material upgrades.

B. Assets types

In the nation's infrastructure and even beyond, the biggest Chinese firms weigh heavily. The top

30 Chinese publicly listed firms, some of the larger components of the Shanghai Composite

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Index, along with their operations, logos and links pointing, are described here. In China, large

corporations must receive approval from the Equity Regulation Department of state Government

until their shares can be exchanged on the Shanghai Stock Exchange-SSE, a various Trading

platform. Several of the world's Biggest firms mentioned on the Shanghai Stock Exchange were

either established or spun off from public bodies (such as departments, province or local

municipalities) or state-owned companies because of China's traditionally centralized

administration and development (Zang, 2019).

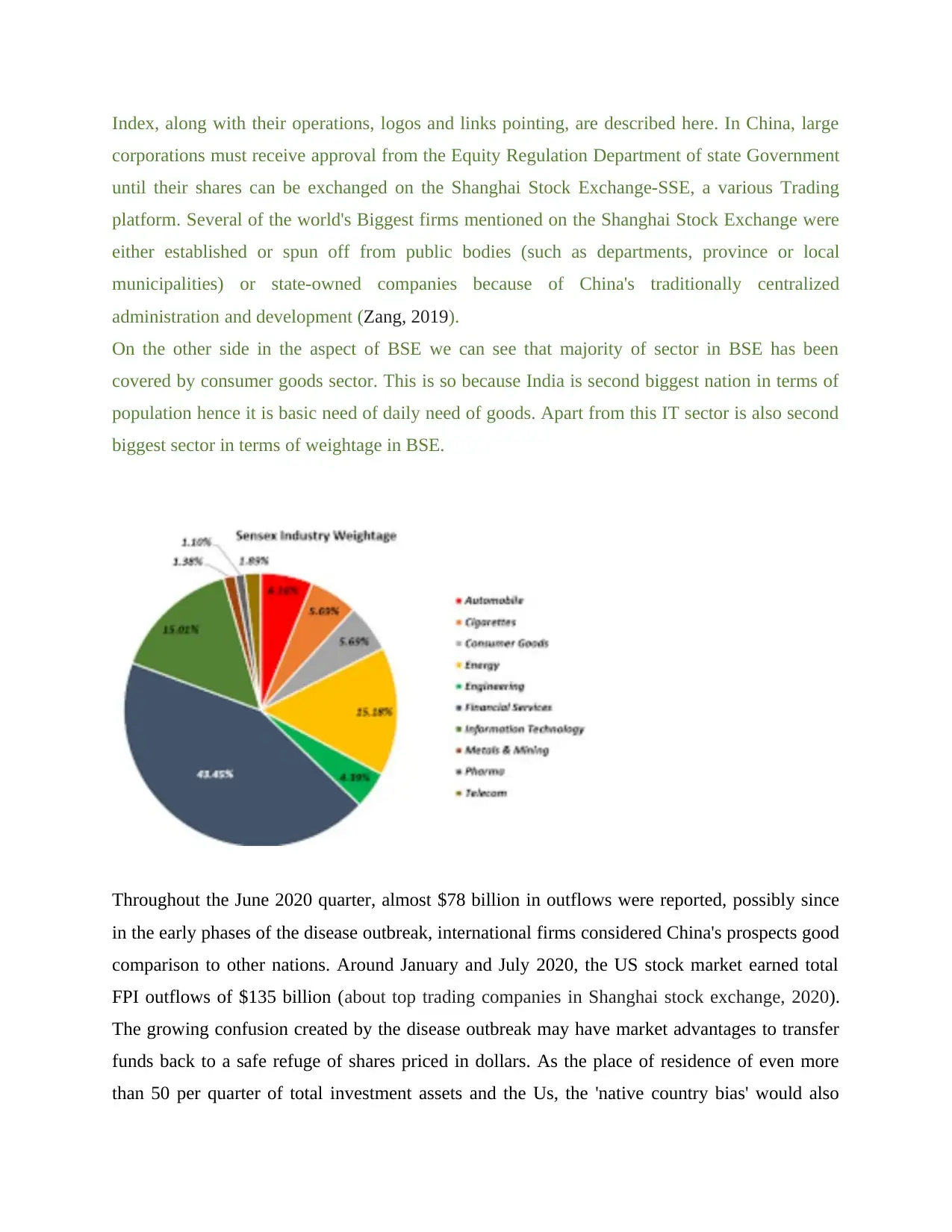

On the other side in the aspect of BSE we can see that majority of sector in BSE has been

covered by consumer goods sector. This is so because India is second biggest nation in terms of

population hence it is basic need of daily need of goods. Apart from this IT sector is also second

biggest sector in terms of weightage in BSE.

Throughout the June 2020 quarter, almost $78 billion in outflows were reported, possibly since

in the early phases of the disease outbreak, international firms considered China's prospects good

comparison to other nations. Around January and July 2020, the US stock market earned total

FPI outflows of $135 billion (about top trading companies in Shanghai stock exchange, 2020).

The growing confusion created by the disease outbreak may have market advantages to transfer

funds back to a safe refuge of shares priced in dollars. As the place of residence of even more

than 50 per quarter of total investment assets and the Us, the 'native country bias' would also

corporations must receive approval from the Equity Regulation Department of state Government

until their shares can be exchanged on the Shanghai Stock Exchange-SSE, a various Trading

platform. Several of the world's Biggest firms mentioned on the Shanghai Stock Exchange were

either established or spun off from public bodies (such as departments, province or local

municipalities) or state-owned companies because of China's traditionally centralized

administration and development (Zang, 2019).

On the other side in the aspect of BSE we can see that majority of sector in BSE has been

covered by consumer goods sector. This is so because India is second biggest nation in terms of

population hence it is basic need of daily need of goods. Apart from this IT sector is also second

biggest sector in terms of weightage in BSE.

Throughout the June 2020 quarter, almost $78 billion in outflows were reported, possibly since

in the early phases of the disease outbreak, international firms considered China's prospects good

comparison to other nations. Around January and July 2020, the US stock market earned total

FPI outflows of $135 billion (about top trading companies in Shanghai stock exchange, 2020).

The growing confusion created by the disease outbreak may have market advantages to transfer

funds back to a safe refuge of shares priced in dollars. As the place of residence of even more

than 50 per quarter of total investment assets and the Us, the 'native country bias' would also

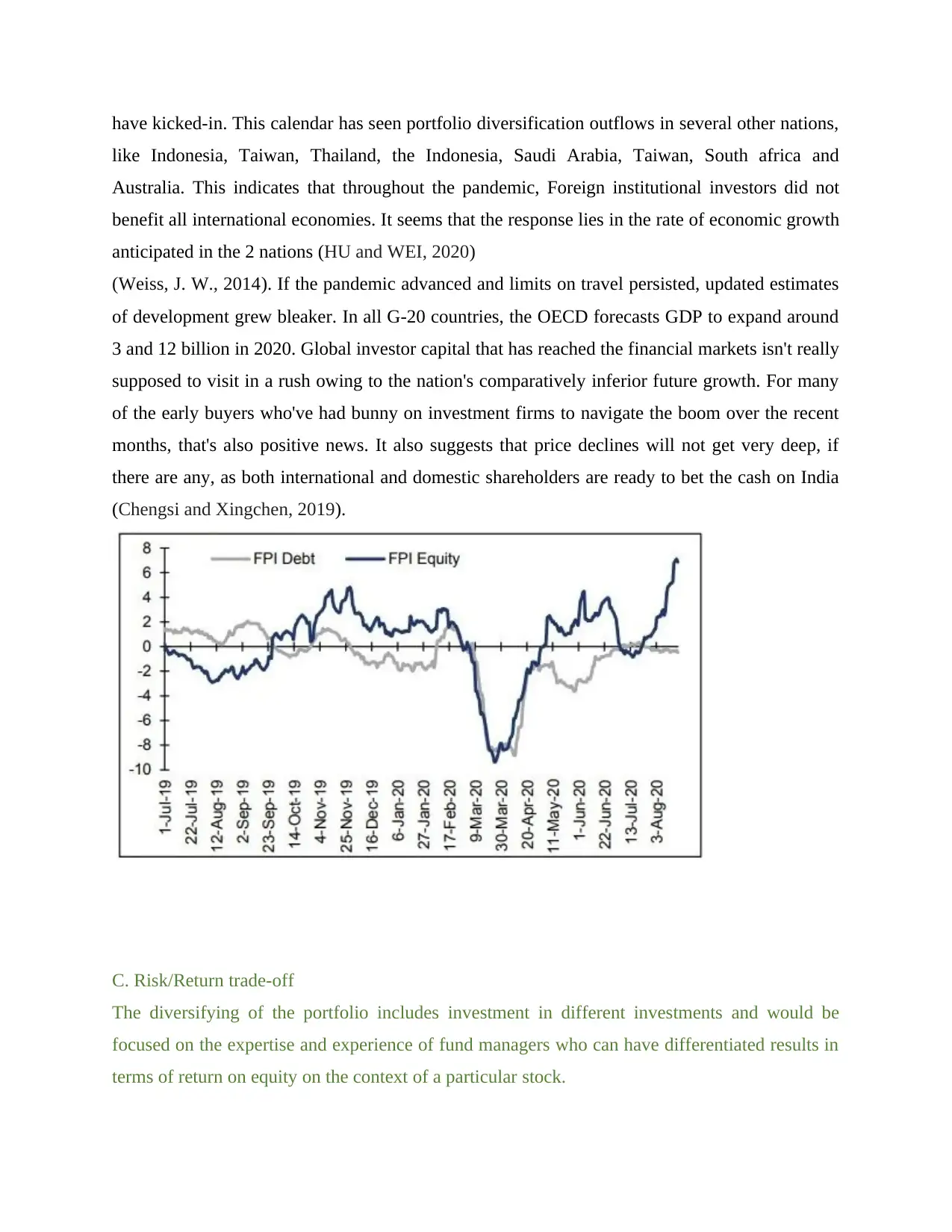

have kicked-in. This calendar has seen portfolio diversification outflows in several other nations,

like Indonesia, Taiwan, Thailand, the Indonesia, Saudi Arabia, Taiwan, South africa and

Australia. This indicates that throughout the pandemic, Foreign institutional investors did not

benefit all international economies. It seems that the response lies in the rate of economic growth

anticipated in the 2 nations (HU and WEI, 2020)

(Weiss, J. W., 2014). If the pandemic advanced and limits on travel persisted, updated estimates

of development grew bleaker. In all G-20 countries, the OECD forecasts GDP to expand around

3 and 12 billion in 2020. Global investor capital that has reached the financial markets isn't really

supposed to visit in a rush owing to the nation's comparatively inferior future growth. For many

of the early buyers who've had bunny on investment firms to navigate the boom over the recent

months, that's also positive news. It also suggests that price declines will not get very deep, if

there are any, as both international and domestic shareholders are ready to bet the cash on India

(Chengsi and Xingchen, 2019).

C. Risk/Return trade-off

The diversifying of the portfolio includes investment in different investments and would be

focused on the expertise and experience of fund managers who can have differentiated results in

terms of return on equity on the context of a particular stock.

like Indonesia, Taiwan, Thailand, the Indonesia, Saudi Arabia, Taiwan, South africa and

Australia. This indicates that throughout the pandemic, Foreign institutional investors did not

benefit all international economies. It seems that the response lies in the rate of economic growth

anticipated in the 2 nations (HU and WEI, 2020)

(Weiss, J. W., 2014). If the pandemic advanced and limits on travel persisted, updated estimates

of development grew bleaker. In all G-20 countries, the OECD forecasts GDP to expand around

3 and 12 billion in 2020. Global investor capital that has reached the financial markets isn't really

supposed to visit in a rush owing to the nation's comparatively inferior future growth. For many

of the early buyers who've had bunny on investment firms to navigate the boom over the recent

months, that's also positive news. It also suggests that price declines will not get very deep, if

there are any, as both international and domestic shareholders are ready to bet the cash on India

(Chengsi and Xingchen, 2019).

C. Risk/Return trade-off

The diversifying of the portfolio includes investment in different investments and would be

focused on the expertise and experience of fund managers who can have differentiated results in

terms of return on equity on the context of a particular stock.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.