Comparative Analysis of International Portfolios: India and China

VerifiedAdded on 2023/01/05

|15

|5033

|27

Report

AI Summary

This report provides a comprehensive analysis of the international portfolios of India and China, focusing on Foreign Portfolio Investment (FPI) flows and their implications. It explores the outperformance of both countries in the global market, driven by FPI inflows, and examines the impact of geopolitical factors and policy changes, such as India's investment curbs on China. The report delves into relevant financial concepts like interest rate parity and international diversification, comparing the performance of the Nifty 50 and Shanghai Composite Index. It also discusses the implications of these trends, including the potential for continued growth and the impact of the COVID-19 pandemic. The analysis incorporates data on FPI flows, including the significant investments made by Chinese entities in Indian firms and the regulatory responses by the Indian government. The report concludes by highlighting the importance of understanding these dynamics for investors and policymakers.

Management of

International Finance

International Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

MAIN BODY..................................................................................................................................3

International Portfolio of china and India....................................................................................3

Outperformance of India, China..................................................................................................5

Driven by FPI flows.....................................................................................................................5

Implications.................................................................................................................................6

Appropriate financial concepts, theory, and practices.................................................................6

India’s portfolio investment curbs on China signal bumpy road.................................................7

Indo-China Conflict: These 12 stocks are likely to be affected the most....................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Introduction......................................................................................................................................3

MAIN BODY..................................................................................................................................3

International Portfolio of china and India....................................................................................3

Outperformance of India, China..................................................................................................5

Driven by FPI flows.....................................................................................................................5

Implications.................................................................................................................................6

Appropriate financial concepts, theory, and practices.................................................................6

India’s portfolio investment curbs on China signal bumpy road.................................................7

Indo-China Conflict: These 12 stocks are likely to be affected the most....................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Introduction

The analysis of monetary relations among two countries is global finance, also referred to as

foreign economics and finance, concentrating on fields such as international investment

including exchange commodity prices. The most significant influencer in economic wealth and

development is undoubtedly foreign trade. Yet there are questions over the fact that the United

States has moved from being the biggest foreign borrower to become the world's largest

borrower throughout the world, consuming excess sums of borrowing internationally from

organisations and nations. In unpredictable ways, this can impact international finance. In order

to measure the actual buying power of various currencies, minimum wage is the comparison of

costs in various areas that used a particular product or a certain group of products.

An equilibrium condition in which shareholders are oblivious to borrowing costs added to

deposit accounts in 2 distinct nations is defined by interest rate parity. In this report, investment

portfolio of two countries India and China have been discussed (Argade, 2020).

A collection of securities and other commodities that rely on overseas markets instead of

local companies is an international account. A foreign portfolio, if well planned, gives the

shareholder access to developing and established markets and offers liquidity. An international

portfolio applies to shareholders who by switching away from a household portfolio, wish to

diversify their holdings. Owing to possible political and economic uncertainty in some

developing markets, this sort of investment will bear higher incidence. There is also a possibility

that the economy of an international market could fall in value against the Dollar.

MAIN BODY

International Portfolio of china and India

The united states began gathering data on contributions and recipients under Foreign Portfolio

Investment (FPI) flowing in through China at a breath-taking pace confrontations are occurring

between Indian and Chinese units in Ladakh. By implementing tighter Foreign Direct Investment

(FDI) requirements for firms from places with which India sharing geographic borders, India has

recently updated its overseas investment framework to monitor China trade aspirations. Security

services are wary of Chinese attempts, not only spatially, but politically, militarily and

financially, to extend (Raza and Hanif, 2013). Officials claimed recent trends and evidence

indicated that China could switch to alternative options of growth in the Indian current

The analysis of monetary relations among two countries is global finance, also referred to as

foreign economics and finance, concentrating on fields such as international investment

including exchange commodity prices. The most significant influencer in economic wealth and

development is undoubtedly foreign trade. Yet there are questions over the fact that the United

States has moved from being the biggest foreign borrower to become the world's largest

borrower throughout the world, consuming excess sums of borrowing internationally from

organisations and nations. In unpredictable ways, this can impact international finance. In order

to measure the actual buying power of various currencies, minimum wage is the comparison of

costs in various areas that used a particular product or a certain group of products.

An equilibrium condition in which shareholders are oblivious to borrowing costs added to

deposit accounts in 2 distinct nations is defined by interest rate parity. In this report, investment

portfolio of two countries India and China have been discussed (Argade, 2020).

A collection of securities and other commodities that rely on overseas markets instead of

local companies is an international account. A foreign portfolio, if well planned, gives the

shareholder access to developing and established markets and offers liquidity. An international

portfolio applies to shareholders who by switching away from a household portfolio, wish to

diversify their holdings. Owing to possible political and economic uncertainty in some

developing markets, this sort of investment will bear higher incidence. There is also a possibility

that the economy of an international market could fall in value against the Dollar.

MAIN BODY

International Portfolio of china and India

The united states began gathering data on contributions and recipients under Foreign Portfolio

Investment (FPI) flowing in through China at a breath-taking pace confrontations are occurring

between Indian and Chinese units in Ladakh. By implementing tighter Foreign Direct Investment

(FDI) requirements for firms from places with which India sharing geographic borders, India has

recently updated its overseas investment framework to monitor China trade aspirations. Security

services are wary of Chinese attempts, not only spatially, but politically, militarily and

financially, to extend (Raza and Hanif, 2013). Officials claimed recent trends and evidence

indicated that China could switch to alternative options of growth in the Indian current

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

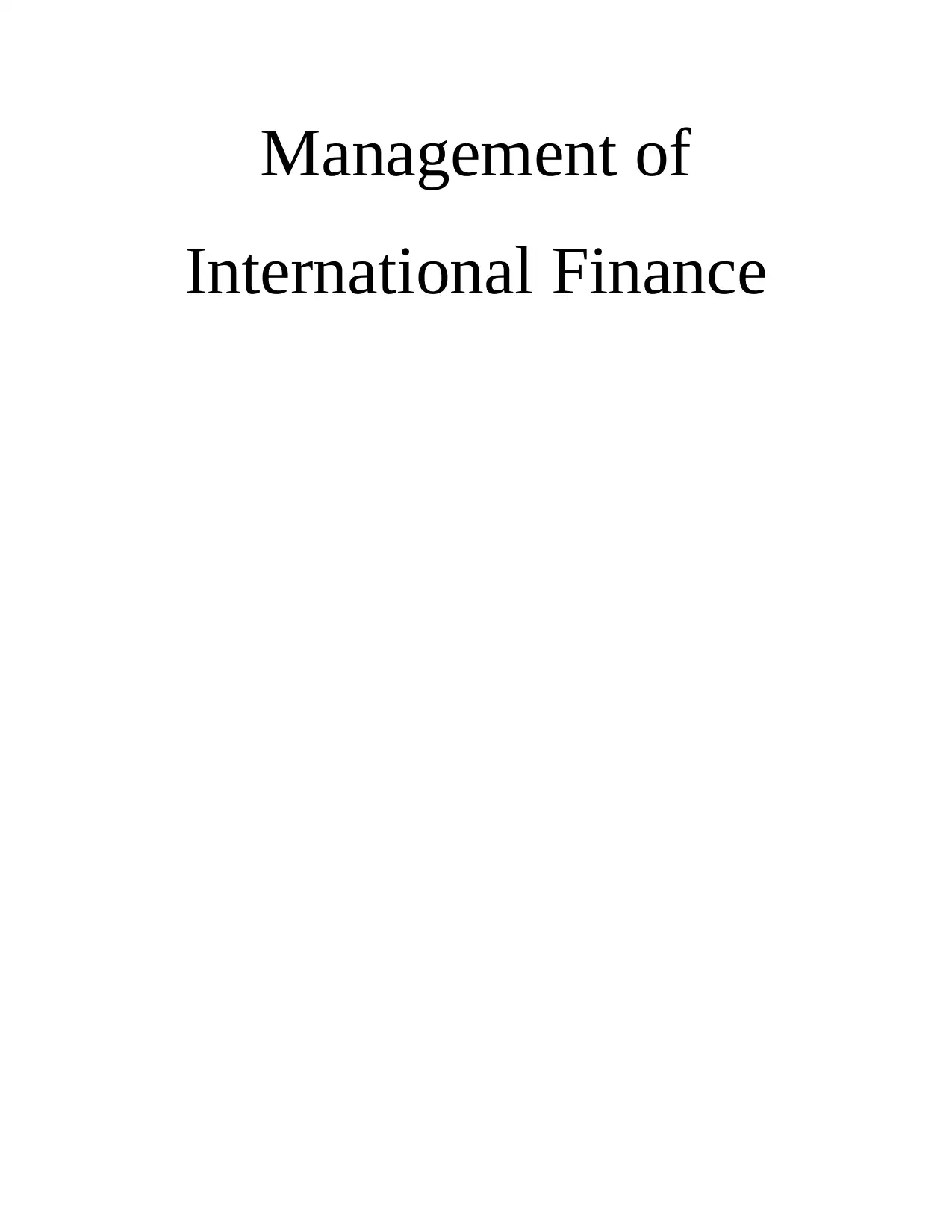

macroeconomic control. China's latest way out is the FPI path, said a representative. With the

advent of the COVID-19 disease outbreak, intelligence researches have described those Chinese

investments by Foreign Investment Portfolio Asset Finance Capital expenditure the real amount

could be a lot higher than that one, a representative confirmed (Sarsby, 2016). The FPI path is

really the latest road out embraced by China,” said about an official. With the advent of the

COVID-19 disease outbreak, declassified documents revealed that somewhere between

December 2019 through March 2020, Chinese investment throughout NSE-listed firms by

International Portfolio Investments (FPI) grew many fold. The real amount might be a lot higher

than that one, an official confirmed. Together to, Foreign Institutional Investments (FIIs) as well

as Eligible Foreign Contributions (QFIs) are regarded as FPIs, which are among the interested

parties of the Indian capital market that play a key role in forming the current account deficit and

volatility. Current laws make it a requirement for businesses to appoint an investor even then for

a professional trader, the stake in the company reaches one per cent. References said it was for

Chinese FPI buyers, private banks may have been enticing destination as a majority of them will

have a significant number of unidentified FPIs with much less for one investment terms. Figures

available from intelligence services reveal that at most Rs 622,95 crore stocks are held by

anonymous overseas companies in 19 private banks. High levels of growth by unidentified

investors throughout the financial system, official does can contribute to a reversal of RBI's bank

consolidation and could contribute to some other event like Yes Bank's (Van Horen and

Claessens, 2012).

As per current laws, most transferable equities, like bonds, stocks, savings accounts, alternate

institutional investors (AIFs) and financial products, are eligible for FPI of India. Actually, SEBI

advent of the COVID-19 disease outbreak, intelligence researches have described those Chinese

investments by Foreign Investment Portfolio Asset Finance Capital expenditure the real amount

could be a lot higher than that one, a representative confirmed (Sarsby, 2016). The FPI path is

really the latest road out embraced by China,” said about an official. With the advent of the

COVID-19 disease outbreak, declassified documents revealed that somewhere between

December 2019 through March 2020, Chinese investment throughout NSE-listed firms by

International Portfolio Investments (FPI) grew many fold. The real amount might be a lot higher

than that one, an official confirmed. Together to, Foreign Institutional Investments (FIIs) as well

as Eligible Foreign Contributions (QFIs) are regarded as FPIs, which are among the interested

parties of the Indian capital market that play a key role in forming the current account deficit and

volatility. Current laws make it a requirement for businesses to appoint an investor even then for

a professional trader, the stake in the company reaches one per cent. References said it was for

Chinese FPI buyers, private banks may have been enticing destination as a majority of them will

have a significant number of unidentified FPIs with much less for one investment terms. Figures

available from intelligence services reveal that at most Rs 622,95 crore stocks are held by

anonymous overseas companies in 19 private banks. High levels of growth by unidentified

investors throughout the financial system, official does can contribute to a reversal of RBI's bank

consolidation and could contribute to some other event like Yes Bank's (Van Horen and

Claessens, 2012).

As per current laws, most transferable equities, like bonds, stocks, savings accounts, alternate

institutional investors (AIFs) and financial products, are eligible for FPI of India. Actually, SEBI

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

has listed 111 Hong Kong firms and 16 Chinese companies. The amount of capital invested by

Sixteen Chinese businesses, the study noted, is about Rs 8,100 crore. Intelligence agents said it

should be for a tighter regulatory framework to monitor the influx of money from China since

Beijing has sought alternative things to create headway into Indian market. During the first

decades including its century, the fate of the Chinese and Indian share prices was closely

connected as international firms became gung-ho more about major companies which were rising

at a blazing hot rate. After 2015, once Stock markets first going on a raging bull-run, this

connection poorly drained, accompanied by a clear majority collapse, from not that they've

returned anymore. This connection seems to be being revived by that of the 2 nations (Argade,

2020).

Outperformance of India, China

If they compared with the results of the international accelerated vesting and during disease

outbreak, the into not were China and India. Though the Nifty 50 Indian average is strong to

exceeding the pre-Covid point, the Shanghai Composite Index of China is holding steady 4.7%

beyond this high point. The US business is also the only business which has been this thermally

conductive (Maulina and Raharja, 2018). The one to rebound again from original battle of sales

this year was the Beijing stock exchange. With documents provided either by Chinese

government signalling that the epidemic is now under command in the region, the Market

Capitalization had relocated to a different 52-week high through July. Through the uncertainty

surrounding corporate results and the economy, the Nifty 50 has still been rising heavily; it is

actually about 5 percent far below January high. Many US indexes, including the Axes (15

percent higher than the pre-Covid trough) as well as the S&P 500, which was 5 points greater

than its 2020 high at the beginning of September, too have continued to turn up well. This has

not been done well though, by stocks in several other economies. For eg, the CAC indexes of

France, that FTSE 100 of the United Kingdom, the RTS indexes of Russia, the Bovespa indexes

of Brazil as well as the Jakarta Weighted average of Indonesia are now at minimum 20% lower

than the pre-Covid levels.

Sixteen Chinese businesses, the study noted, is about Rs 8,100 crore. Intelligence agents said it

should be for a tighter regulatory framework to monitor the influx of money from China since

Beijing has sought alternative things to create headway into Indian market. During the first

decades including its century, the fate of the Chinese and Indian share prices was closely

connected as international firms became gung-ho more about major companies which were rising

at a blazing hot rate. After 2015, once Stock markets first going on a raging bull-run, this

connection poorly drained, accompanied by a clear majority collapse, from not that they've

returned anymore. This connection seems to be being revived by that of the 2 nations (Argade,

2020).

Outperformance of India, China

If they compared with the results of the international accelerated vesting and during disease

outbreak, the into not were China and India. Though the Nifty 50 Indian average is strong to

exceeding the pre-Covid point, the Shanghai Composite Index of China is holding steady 4.7%

beyond this high point. The US business is also the only business which has been this thermally

conductive (Maulina and Raharja, 2018). The one to rebound again from original battle of sales

this year was the Beijing stock exchange. With documents provided either by Chinese

government signalling that the epidemic is now under command in the region, the Market

Capitalization had relocated to a different 52-week high through July. Through the uncertainty

surrounding corporate results and the economy, the Nifty 50 has still been rising heavily; it is

actually about 5 percent far below January high. Many US indexes, including the Axes (15

percent higher than the pre-Covid trough) as well as the S&P 500, which was 5 points greater

than its 2020 high at the beginning of September, too have continued to turn up well. This has

not been done well though, by stocks in several other economies. For eg, the CAC indexes of

France, that FTSE 100 of the United Kingdom, the RTS indexes of Russia, the Bovespa indexes

of Brazil as well as the Jakarta Weighted average of Indonesia are now at minimum 20% lower

than the pre-Covid levels.

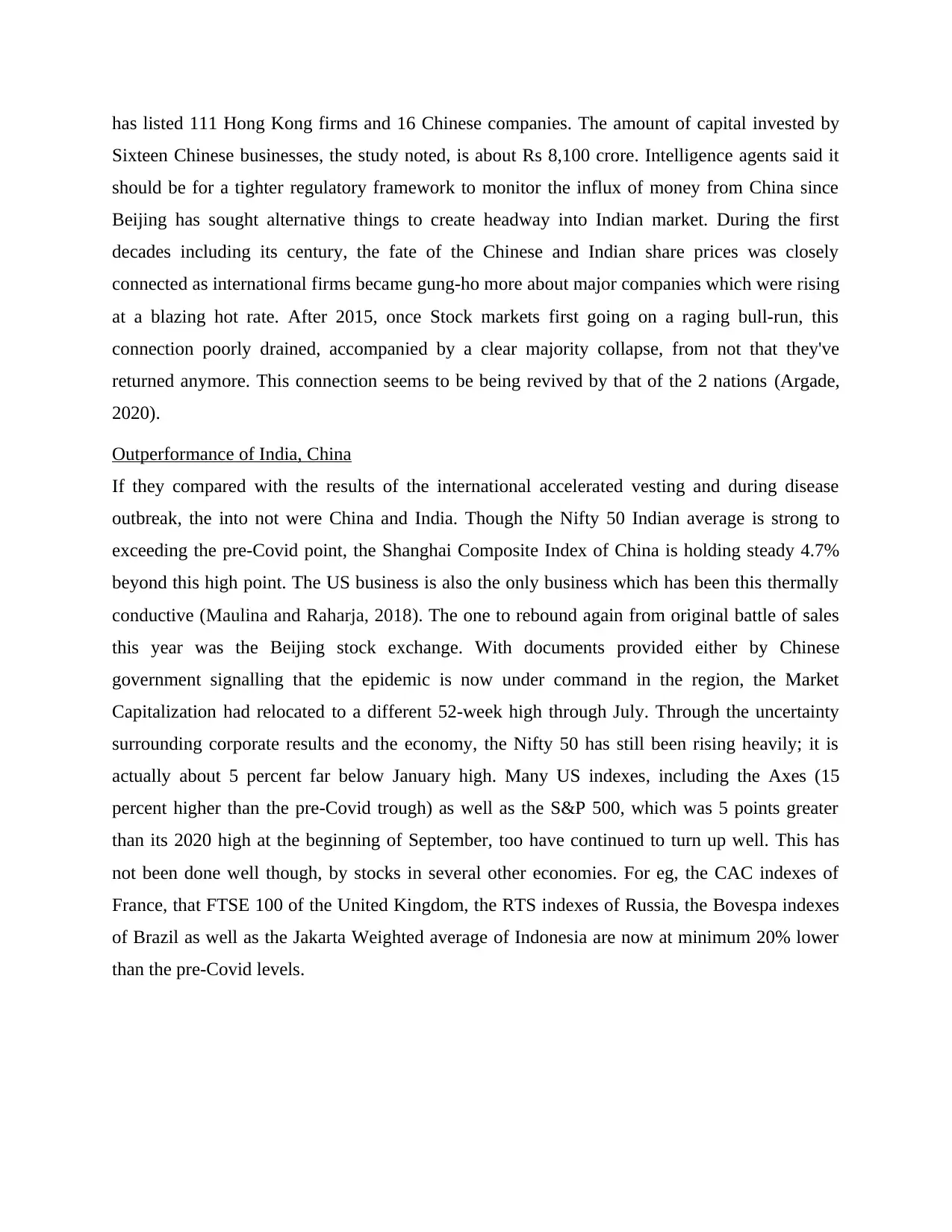

Driven by FPI flows

FPIs, based on the new data published by Forbes, has adopted a more positive approach

regarding India, China with the US. By February 29, 2020, these shareholders had acquired

Indian shares valued $4.07 billion decade, net. Of this, during July and September, about $6.5

billion was injected, nullifying the capital inflows reported in March. Data on the international

fund flows for China are only valid before June 30. Yet with the first 6 months of 2020, the

nation already has earned $47 billion (Drobyazko, Pavlova, Suhak, Kulyk and

Khodjimukhamedova, 2019).

Throughout the June 2020 quarter, almost $78 billion in outflows were reported, possibly since

in the early phases of the disease outbreak, international firms considered China's prospects good

comparison to other nations. Around January and July 2020, the US stock market earned total

FPI outflows of $135 billion. The growing confusion created by the disease outbreak may have

market advantages to transfer funds back to a safe refuge of shares priced in dollars. As the place

of residence of even more than 50 per quarter of total investment assets and the Us, the 'native

country bias' would also have kicked-in. This calendar has seen portfolio diversification outflows

in several other nations, like Indonesia, Taiwan, Thailand, the Indonesia, Saudi Arabia, Taiwan,

South africa and Australia. This indicates that throughout the pandemic, Foreign institutional

FPIs, based on the new data published by Forbes, has adopted a more positive approach

regarding India, China with the US. By February 29, 2020, these shareholders had acquired

Indian shares valued $4.07 billion decade, net. Of this, during July and September, about $6.5

billion was injected, nullifying the capital inflows reported in March. Data on the international

fund flows for China are only valid before June 30. Yet with the first 6 months of 2020, the

nation already has earned $47 billion (Drobyazko, Pavlova, Suhak, Kulyk and

Khodjimukhamedova, 2019).

Throughout the June 2020 quarter, almost $78 billion in outflows were reported, possibly since

in the early phases of the disease outbreak, international firms considered China's prospects good

comparison to other nations. Around January and July 2020, the US stock market earned total

FPI outflows of $135 billion. The growing confusion created by the disease outbreak may have

market advantages to transfer funds back to a safe refuge of shares priced in dollars. As the place

of residence of even more than 50 per quarter of total investment assets and the Us, the 'native

country bias' would also have kicked-in. This calendar has seen portfolio diversification outflows

in several other nations, like Indonesia, Taiwan, Thailand, the Indonesia, Saudi Arabia, Taiwan,

South africa and Australia. This indicates that throughout the pandemic, Foreign institutional

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

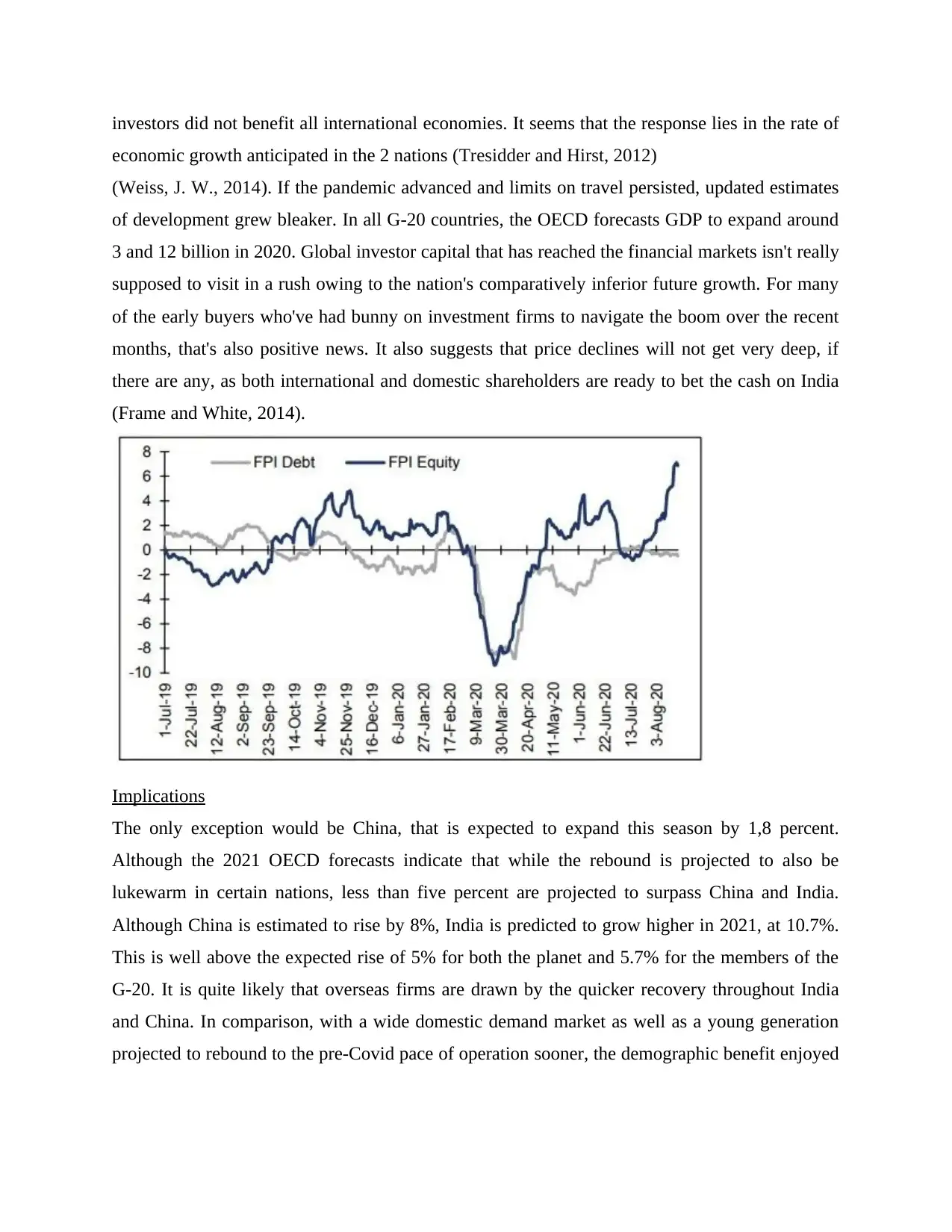

investors did not benefit all international economies. It seems that the response lies in the rate of

economic growth anticipated in the 2 nations (Tresidder and Hirst, 2012)

(Weiss, J. W., 2014). If the pandemic advanced and limits on travel persisted, updated estimates

of development grew bleaker. In all G-20 countries, the OECD forecasts GDP to expand around

3 and 12 billion in 2020. Global investor capital that has reached the financial markets isn't really

supposed to visit in a rush owing to the nation's comparatively inferior future growth. For many

of the early buyers who've had bunny on investment firms to navigate the boom over the recent

months, that's also positive news. It also suggests that price declines will not get very deep, if

there are any, as both international and domestic shareholders are ready to bet the cash on India

(Frame and White, 2014).

Implications

The only exception would be China, that is expected to expand this season by 1,8 percent.

Although the 2021 OECD forecasts indicate that while the rebound is projected to also be

lukewarm in certain nations, less than five percent are projected to surpass China and India.

Although China is estimated to rise by 8%, India is predicted to grow higher in 2021, at 10.7%.

This is well above the expected rise of 5% for both the planet and 5.7% for the members of the

G-20. It is quite likely that overseas firms are drawn by the quicker recovery throughout India

and China. In comparison, with a wide domestic demand market as well as a young generation

projected to rebound to the pre-Covid pace of operation sooner, the demographic benefit enjoyed

economic growth anticipated in the 2 nations (Tresidder and Hirst, 2012)

(Weiss, J. W., 2014). If the pandemic advanced and limits on travel persisted, updated estimates

of development grew bleaker. In all G-20 countries, the OECD forecasts GDP to expand around

3 and 12 billion in 2020. Global investor capital that has reached the financial markets isn't really

supposed to visit in a rush owing to the nation's comparatively inferior future growth. For many

of the early buyers who've had bunny on investment firms to navigate the boom over the recent

months, that's also positive news. It also suggests that price declines will not get very deep, if

there are any, as both international and domestic shareholders are ready to bet the cash on India

(Frame and White, 2014).

Implications

The only exception would be China, that is expected to expand this season by 1,8 percent.

Although the 2021 OECD forecasts indicate that while the rebound is projected to also be

lukewarm in certain nations, less than five percent are projected to surpass China and India.

Although China is estimated to rise by 8%, India is predicted to grow higher in 2021, at 10.7%.

This is well above the expected rise of 5% for both the planet and 5.7% for the members of the

G-20. It is quite likely that overseas firms are drawn by the quicker recovery throughout India

and China. In comparison, with a wide domestic demand market as well as a young generation

projected to rebound to the pre-Covid pace of operation sooner, the demographic benefit enjoyed

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

by both nations can also benefit the majority of the nations (Brooks, Heffner and Henderson,

2014).

Appropriate financial concepts, theory, and practices

India has drawn up rules recommending closer oversight of China and Hong Kong's current

Foreign Investment Firms (FPIs), three presidency sources have told Foxnews.com, their latest

attempt during the coronavirus pandemic to monitor foreign inflows (Pagare, 2020). The

deliberations came days since India announced that all foreign investment (FDI) through places

in which it has a land boundary would be screened, a development had said was targeted at to

stave off mergers as asset values and during coronavirus disease outbreak are subdued. The

policy was described by the China as restrictive. FDIs were lengthier positive actions that usually

provide the management of a business with leverage (Zhou, 2012). The policy reform might

allow Chinese investors to start increasing their operations in Malaysia as investment firms,

buying business shares like equity markets to gain influence, authorities in New Delhi said and

that doubts had arisen throughout the government. Two top government sources have suggested

that India may established an agency to scrutinise new FPI registered members from economies

such as Germany, and that the guidelines would also extend to Hong Kong, this same separate

customs area from which major Chinese funding is being diverted. The officials claimed that in

coordination with the Department of Trading and the Stock Market Authority, the Securities and

Exchange Board of India (SEBI), a course of the narrative had been prepared and was intensely

scrutinized by the Central Finance ministry (Chavan, 2013.).

The Ministry of Finance as well as the Ministry of Trade refused to respond, although SEBI can't

respond instantly. The various sides continued that New Delhi also is exploring the prospect of

requiring such a "top secret clearance" for current FPI registered voters from such nation from

India's residential (interior) government. One representative who's had real experience of talks it

seems that are not suggesting that every investment will be halted and want to only add another

layer of screening to maintain the value among our enterprises. India was worried about Beijing

state-run firms purchasing stocks of Indian firms, a third defence official said. The statement

claimed that the FPI regulation is likely to be comparable to the recently implemented FDI

regulation that did not identify China but referred to nations at which a ground boundary is

shared by India. If the regulations would apply to other nations and whether current licenced

2014).

Appropriate financial concepts, theory, and practices

India has drawn up rules recommending closer oversight of China and Hong Kong's current

Foreign Investment Firms (FPIs), three presidency sources have told Foxnews.com, their latest

attempt during the coronavirus pandemic to monitor foreign inflows (Pagare, 2020). The

deliberations came days since India announced that all foreign investment (FDI) through places

in which it has a land boundary would be screened, a development had said was targeted at to

stave off mergers as asset values and during coronavirus disease outbreak are subdued. The

policy was described by the China as restrictive. FDIs were lengthier positive actions that usually

provide the management of a business with leverage (Zhou, 2012). The policy reform might

allow Chinese investors to start increasing their operations in Malaysia as investment firms,

buying business shares like equity markets to gain influence, authorities in New Delhi said and

that doubts had arisen throughout the government. Two top government sources have suggested

that India may established an agency to scrutinise new FPI registered members from economies

such as Germany, and that the guidelines would also extend to Hong Kong, this same separate

customs area from which major Chinese funding is being diverted. The officials claimed that in

coordination with the Department of Trading and the Stock Market Authority, the Securities and

Exchange Board of India (SEBI), a course of the narrative had been prepared and was intensely

scrutinized by the Central Finance ministry (Chavan, 2013.).

The Ministry of Finance as well as the Ministry of Trade refused to respond, although SEBI can't

respond instantly. The various sides continued that New Delhi also is exploring the prospect of

requiring such a "top secret clearance" for current FPI registered voters from such nation from

India's residential (interior) government. One representative who's had real experience of talks it

seems that are not suggesting that every investment will be halted and want to only add another

layer of screening to maintain the value among our enterprises. India was worried about Beijing

state-run firms purchasing stocks of Indian firms, a third defence official said. The statement

claimed that the FPI regulation is likely to be comparable to the recently implemented FDI

regulation that did not identify China but referred to nations at which a ground boundary is

shared by India. If the regulations would apply to other nations and whether current licenced

FPIs would face similar oversight was not readily evident. Actually, there have been 111

reported Hong Kong FPIs including 16 from China (Heaton and et.al, 2019).

Amongst these key drivers including its Indian capital markets were international

portfolio holders. Net FPI outflows in 2019 were $18 trillion, national statistics Securities

Depository shows. In particular questions about FPI investments have increased in last week

since Indian borrower HDFC's share capital disclosure in April revealed that Central bank have

marginally increased its interest in the project. An associate at Khaitan & Co., an Indian legal

firm, said policy testing could impact China as well as Hong Kong's fresh inflationary pressures

and disrupt new investments. Chinese investors have also been spooked by the FDI policy move,

including those who have placed their acquisition career on hold while they wait for clarification,

Reuters has stated.

India’s portfolio investment curbs on China signal bumpy road

India is allegedly cracking down on Beijing foreign direct investment (FPI) since putting curbs

on China's foreign investment (FDI) — a development observers have said will further worsen

reciprocal economic relations. The Government of India aims to limit Chinese equity investors'

entry to the sector as it tried to fill a potential loophole for investors to buy stock in the

mentioned Indian firms. As per a steps could include a compulsory 'approval path' for Beijing

FPI. The Government of India needed to ensure that shareholders barred by the newly revamped

FDI rules did not need the FPI choice to obtain a large shareholding in a business, the document

said. On April 22, the Cabinet approved adjustments to just the FDI strategy and directed prior

approval of acquisitions from nations in which India share a border crossing, a development that

is commonly viewed affecting China (Aliyu and Tasmin, 2012).

Sha Jun, senior associate of its Yingke Legal Firm's India International Financial services Hub,

informed that several international firms had portfolio interests in India, such as those from

China. "It must be to be anticipated that India will make a move towards china Capital flows." If

China's central bank increased its interest in Housing Construction Finance Corp, Country's

biggest mortgage company, on April 13, its Government of India was worried. It is assumed the

deal was the key cause that caused the reform in patent act. "As China-Indian monetary easing

has fallen due to various measures carried out along with the Indian border in blocking Private

companies, the reciprocal economic environment and collaboration facing a difficult journey,".

In India, the COVID-19 outbreak also raises safety problems for Chinese investors preparing to

reported Hong Kong FPIs including 16 from China (Heaton and et.al, 2019).

Amongst these key drivers including its Indian capital markets were international

portfolio holders. Net FPI outflows in 2019 were $18 trillion, national statistics Securities

Depository shows. In particular questions about FPI investments have increased in last week

since Indian borrower HDFC's share capital disclosure in April revealed that Central bank have

marginally increased its interest in the project. An associate at Khaitan & Co., an Indian legal

firm, said policy testing could impact China as well as Hong Kong's fresh inflationary pressures

and disrupt new investments. Chinese investors have also been spooked by the FDI policy move,

including those who have placed their acquisition career on hold while they wait for clarification,

Reuters has stated.

India’s portfolio investment curbs on China signal bumpy road

India is allegedly cracking down on Beijing foreign direct investment (FPI) since putting curbs

on China's foreign investment (FDI) — a development observers have said will further worsen

reciprocal economic relations. The Government of India aims to limit Chinese equity investors'

entry to the sector as it tried to fill a potential loophole for investors to buy stock in the

mentioned Indian firms. As per a steps could include a compulsory 'approval path' for Beijing

FPI. The Government of India needed to ensure that shareholders barred by the newly revamped

FDI rules did not need the FPI choice to obtain a large shareholding in a business, the document

said. On April 22, the Cabinet approved adjustments to just the FDI strategy and directed prior

approval of acquisitions from nations in which India share a border crossing, a development that

is commonly viewed affecting China (Aliyu and Tasmin, 2012).

Sha Jun, senior associate of its Yingke Legal Firm's India International Financial services Hub,

informed that several international firms had portfolio interests in India, such as those from

China. "It must be to be anticipated that India will make a move towards china Capital flows." If

China's central bank increased its interest in Housing Construction Finance Corp, Country's

biggest mortgage company, on April 13, its Government of India was worried. It is assumed the

deal was the key cause that caused the reform in patent act. "As China-Indian monetary easing

has fallen due to various measures carried out along with the Indian border in blocking Private

companies, the reciprocal economic environment and collaboration facing a difficult journey,".

In India, the COVID-19 outbreak also raises safety problems for Chinese investors preparing to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

go on work trips to India. After the launching of the national FDI policy, Chinese policy of India

disappeared, a fast reversal compared to the growing excitement of investors last year. A Chinese

consultancy company is based on Indian financial products in recent time. Information from of

the Consulate General in India revealed as of December 2019, China's combined policy of India

have surpassed $8 billion, significantly more than the building support from many other nations

that share borders towards India. Due to the instability of Indian policy decisions as well as the

perception that Indian policy are affected by certain Western nations, especially the US, which

are restricting Private companies, many Chinese investors take a buy and hold approach (Tarpani

and Azapagic, 2018).

Indo-China Conflict: These 12 stocks are likely to be affected the most.

Political and economic concerns among India and China have been exacerbated by the latest

border dispute with China throughout the Galwan Region of Ladakh. Viewpoints throughout

India are rising clearer to reject Chinese goods across categories. Throughout terms of

procurement, sectors such as vehicles, consumer goods, medical devices, telecommunications,

pesticides and green energy (solar) have been most important to China. In certain cases, there is a

shortage of different sources at the very same size or expense. Although luxury goods rely on

China for parts, pharmaceuticals rely on API procurement (Awais and Samin, 2012). Mobile

Phone Company depends on China to networking gear and also 4G cellular phones, as China

meets upwards of 75% of India's request for devices. Vodafone as well as Bharti Airtel will

become the most impacted in the telecommunications domain in the event of tariff and

production bollards on suppliers of telecommunications networking gear (Verma and et.al.,

2014). It was of the opinion that throughout the present climate, any possible confrontation

between both the two countries may raise risk exposures, even when economies are looking to

rebound from the disease outbreak. Overall, it'd be expensive and time consuming for Indian

companies to find affordable instantly, it added. In the chemical room, stocks such as internal

network India, Dhanuka, Sumitomo India, as well as Insecticide Malaysia could have a greater

effect. A lower effect on PI Sectors, UPL, Identifying a potential, and Bayer can be seen. Info

Advantage will be influenced in the e-commerce field as its investor firms, Zomato but Policy

Bazaar, are exposed to China's investments (Nguyen, 2016). Chinese firms have major

investments among Indian software and e-commerce companies such as Byju, Paytm, Swiggy,

Ola, BigBasket and Snapdeal.

disappeared, a fast reversal compared to the growing excitement of investors last year. A Chinese

consultancy company is based on Indian financial products in recent time. Information from of

the Consulate General in India revealed as of December 2019, China's combined policy of India

have surpassed $8 billion, significantly more than the building support from many other nations

that share borders towards India. Due to the instability of Indian policy decisions as well as the

perception that Indian policy are affected by certain Western nations, especially the US, which

are restricting Private companies, many Chinese investors take a buy and hold approach (Tarpani

and Azapagic, 2018).

Indo-China Conflict: These 12 stocks are likely to be affected the most.

Political and economic concerns among India and China have been exacerbated by the latest

border dispute with China throughout the Galwan Region of Ladakh. Viewpoints throughout

India are rising clearer to reject Chinese goods across categories. Throughout terms of

procurement, sectors such as vehicles, consumer goods, medical devices, telecommunications,

pesticides and green energy (solar) have been most important to China. In certain cases, there is a

shortage of different sources at the very same size or expense. Although luxury goods rely on

China for parts, pharmaceuticals rely on API procurement (Awais and Samin, 2012). Mobile

Phone Company depends on China to networking gear and also 4G cellular phones, as China

meets upwards of 75% of India's request for devices. Vodafone as well as Bharti Airtel will

become the most impacted in the telecommunications domain in the event of tariff and

production bollards on suppliers of telecommunications networking gear (Verma and et.al.,

2014). It was of the opinion that throughout the present climate, any possible confrontation

between both the two countries may raise risk exposures, even when economies are looking to

rebound from the disease outbreak. Overall, it'd be expensive and time consuming for Indian

companies to find affordable instantly, it added. In the chemical room, stocks such as internal

network India, Dhanuka, Sumitomo India, as well as Insecticide Malaysia could have a greater

effect. A lower effect on PI Sectors, UPL, Identifying a potential, and Bayer can be seen. Info

Advantage will be influenced in the e-commerce field as its investor firms, Zomato but Policy

Bazaar, are exposed to China's investments (Nguyen, 2016). Chinese firms have major

investments among Indian software and e-commerce companies such as Byju, Paytm, Swiggy,

Ola, BigBasket and Snapdeal.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tata Group has access to the installation and configuration of power plants throughout the utility

space within our reporting domain. It also means that the company has been requested by the

Government of India to compile a list of Chinese imports. In addition, several individual states

have revoked company finally approved to Chinese companies (Maharashtra and Haryana). The

continuing conflict between two nations may have a larger economic influence than a physical

one (Lemmens, 2016). India-China boundary dispute is a century’s tussle. It is an incredibly

significant issue strategically and can have broader implications on the global politics of the

South Asia throughout the longer term. India had a trade surplus of USD48.6b (1.7 percent of

GDP) with China in FY20 from hardly any surplus in FY 2000. India's Chinese imports grew

sharply from just 2.6% of overall exports in FY00 to the all high to 16.4% in FY18 until slipping

to 14% (USD65.3b) in FY20. The continued boundary disputes are subject to fluctuate mutual

bilateral trade throughout the potential. Throughout the post-COVID environment, a big change

could occur. A border dispute could contribute in the past to a shift in trade relations. India has a

significant trade deficits and imports are in most situations, an integral part of the economy.

Industries such as vehicles, electronics, bulk medicines, chemicals, imports from China and

manufacturing. At the very same time, if they actually develop alternative inside India and from

other nations, China might also meet the threat of decreased shipments to India over moment.

There may be a shift in the way multinational firms outsource from China after Covid-19. Here,

India does have a chance to draw foreign businesses to set up its industries would attract further

FDI (Akhlaq and Ahmed, 2013).

Cost Basis

Unrealized

Gain/Loss

Unrealize

d

Gain/Loss

% XIRR

Realized

Gain/Loss

Dividend

s

Collected

Total

Gain/Loss

$62133.74 $-62133.74 -100.00% -9.12% $0 $0 $-62133.74

26,000.00 (26,000.00) -100.00% -28.38% 0.00 0.00 -26,000.00

15,000.00 (15,000.00) -100.00% 10.44% 0.00 0.00 -15,000.00

6,380.00 (6,380.00) -100.00% 0.11% 0.00 0.00 -6,380.00

12,500.00 (12,500.00) -100.00% 32.61% 0.00 0.00 -12,500.00

7,250.00 (7,250.00) -100.00% 3.29% 0.00 0.00 -7,250.00

Response because of an expectations beating in financial statements, resources, and

health the beat proportion (net earnings reward separated by a full group of securities) increased

to 50 percent QoQ. On the basis of rising prices of raw materials and operating costs, the

space within our reporting domain. It also means that the company has been requested by the

Government of India to compile a list of Chinese imports. In addition, several individual states

have revoked company finally approved to Chinese companies (Maharashtra and Haryana). The

continuing conflict between two nations may have a larger economic influence than a physical

one (Lemmens, 2016). India-China boundary dispute is a century’s tussle. It is an incredibly

significant issue strategically and can have broader implications on the global politics of the

South Asia throughout the longer term. India had a trade surplus of USD48.6b (1.7 percent of

GDP) with China in FY20 from hardly any surplus in FY 2000. India's Chinese imports grew

sharply from just 2.6% of overall exports in FY00 to the all high to 16.4% in FY18 until slipping

to 14% (USD65.3b) in FY20. The continued boundary disputes are subject to fluctuate mutual

bilateral trade throughout the potential. Throughout the post-COVID environment, a big change

could occur. A border dispute could contribute in the past to a shift in trade relations. India has a

significant trade deficits and imports are in most situations, an integral part of the economy.

Industries such as vehicles, electronics, bulk medicines, chemicals, imports from China and

manufacturing. At the very same time, if they actually develop alternative inside India and from

other nations, China might also meet the threat of decreased shipments to India over moment.

There may be a shift in the way multinational firms outsource from China after Covid-19. Here,

India does have a chance to draw foreign businesses to set up its industries would attract further

FDI (Akhlaq and Ahmed, 2013).

Cost Basis

Unrealized

Gain/Loss

Unrealize

d

Gain/Loss

% XIRR

Realized

Gain/Loss

Dividend

s

Collected

Total

Gain/Loss

$62133.74 $-62133.74 -100.00% -9.12% $0 $0 $-62133.74

26,000.00 (26,000.00) -100.00% -28.38% 0.00 0.00 -26,000.00

15,000.00 (15,000.00) -100.00% 10.44% 0.00 0.00 -15,000.00

6,380.00 (6,380.00) -100.00% 0.11% 0.00 0.00 -6,380.00

12,500.00 (12,500.00) -100.00% 32.61% 0.00 0.00 -12,500.00

7,250.00 (7,250.00) -100.00% 3.29% 0.00 0.00 -7,250.00

Response because of an expectations beating in financial statements, resources, and

health the beat proportion (net earnings reward separated by a full group of securities) increased

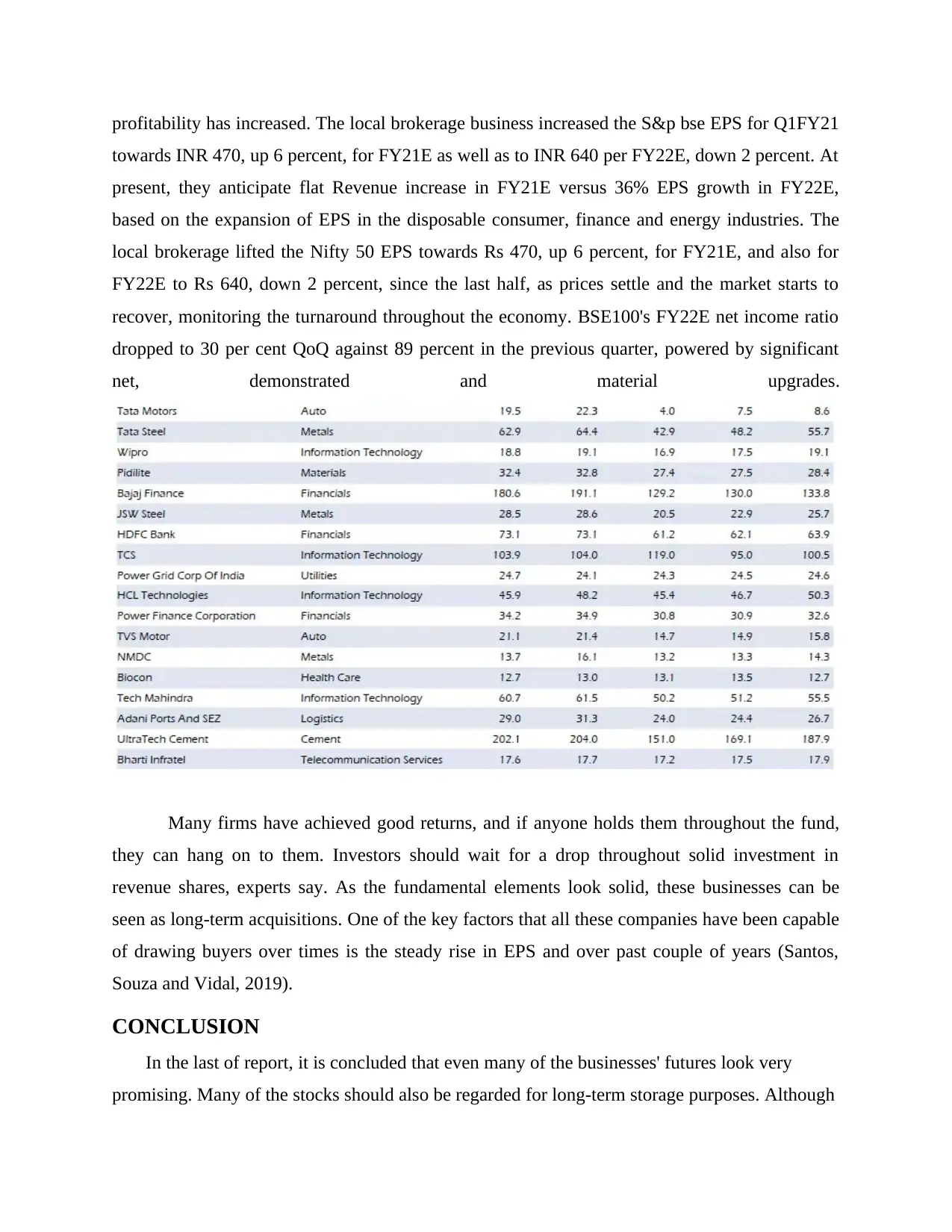

to 50 percent QoQ. On the basis of rising prices of raw materials and operating costs, the

profitability has increased. The local brokerage business increased the S&p bse EPS for Q1FY21

towards INR 470, up 6 percent, for FY21E as well as to INR 640 per FY22E, down 2 percent. At

present, they anticipate flat Revenue increase in FY21E versus 36% EPS growth in FY22E,

based on the expansion of EPS in the disposable consumer, finance and energy industries. The

local brokerage lifted the Nifty 50 EPS towards Rs 470, up 6 percent, for FY21E, and also for

FY22E to Rs 640, down 2 percent, since the last half, as prices settle and the market starts to

recover, monitoring the turnaround throughout the economy. BSE100's FY22E net income ratio

dropped to 30 per cent QoQ against 89 percent in the previous quarter, powered by significant

net, demonstrated and material upgrades.

Many firms have achieved good returns, and if anyone holds them throughout the fund,

they can hang on to them. Investors should wait for a drop throughout solid investment in

revenue shares, experts say. As the fundamental elements look solid, these businesses can be

seen as long-term acquisitions. One of the key factors that all these companies have been capable

of drawing buyers over times is the steady rise in EPS and over past couple of years (Santos,

Souza and Vidal, 2019).

CONCLUSION

In the last of report, it is concluded that even many of the businesses' futures look very

promising. Many of the stocks should also be regarded for long-term storage purposes. Although

towards INR 470, up 6 percent, for FY21E as well as to INR 640 per FY22E, down 2 percent. At

present, they anticipate flat Revenue increase in FY21E versus 36% EPS growth in FY22E,

based on the expansion of EPS in the disposable consumer, finance and energy industries. The

local brokerage lifted the Nifty 50 EPS towards Rs 470, up 6 percent, for FY21E, and also for

FY22E to Rs 640, down 2 percent, since the last half, as prices settle and the market starts to

recover, monitoring the turnaround throughout the economy. BSE100's FY22E net income ratio

dropped to 30 per cent QoQ against 89 percent in the previous quarter, powered by significant

net, demonstrated and material upgrades.

Many firms have achieved good returns, and if anyone holds them throughout the fund,

they can hang on to them. Investors should wait for a drop throughout solid investment in

revenue shares, experts say. As the fundamental elements look solid, these businesses can be

seen as long-term acquisitions. One of the key factors that all these companies have been capable

of drawing buyers over times is the steady rise in EPS and over past couple of years (Santos,

Souza and Vidal, 2019).

CONCLUSION

In the last of report, it is concluded that even many of the businesses' futures look very

promising. Many of the stocks should also be regarded for long-term storage purposes. Although

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.