Advanced Financial Accounting Report: Sims Metal and Lease Standards

VerifiedAdded on 2020/05/16

|15

|3085

|91

Report

AI Summary

This report delves into advanced financial accounting, examining impairment testing practices at Sims Metal Management Limited and the application of IAS 17 lease standards. The report analyzes the impairment testing of goodwill and other intangible assets, including the methodologies, assumptions, and potential subjectivity involved. It assesses the impact of impairment charges and reversals, along with the valuation of financial assets and liabilities. The report also critiques IAS 17, highlighting its shortcomings in providing a true view of a company's financial position, particularly concerning operating leases. It discusses the incentives for lease classification, the impact on financial ratios, and the implications for comparability between companies. Furthermore, the report explores the complexities of lease accounting in specific industries, such as airlines, and discusses potential criticisms of new lease standards, including increased debt levels and administrative burdens. The report concludes by offering a comprehensive overview of the challenges and considerations in advanced financial accounting.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced financial accounting

Name of the university

Name of the student

Authors note

Advanced financial accounting

Name of the university

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Assessment Task Part A:.................................................................................................................2

Requirement i).................................................................................................................................2

Requirement ii)................................................................................................................................2

Requirement iii)...............................................................................................................................2

Requirement iv)...............................................................................................................................3

Requirement v)................................................................................................................................3

Requirement vi)...............................................................................................................................4

Requirement vii)..............................................................................................................................4

Requirement viii).............................................................................................................................5

Assessment Task Part B:.................................................................................................................5

Requirement i).................................................................................................................................5

Requirement ii)................................................................................................................................6

Requirement iii)...............................................................................................................................7

Requirement iv)...............................................................................................................................7

Requirement v)................................................................................................................................8

References list:...............................................................................................................................10

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Assessment Task Part A:.................................................................................................................2

Requirement i).................................................................................................................................2

Requirement ii)................................................................................................................................2

Requirement iii)...............................................................................................................................2

Requirement iv)...............................................................................................................................3

Requirement v)................................................................................................................................3

Requirement vi)...............................................................................................................................4

Requirement vii)..............................................................................................................................4

Requirement viii).............................................................................................................................5

Assessment Task Part B:.................................................................................................................5

Requirement i).................................................................................................................................5

Requirement ii)................................................................................................................................6

Requirement iii)...............................................................................................................................7

Requirement iv)...............................................................................................................................7

Requirement v)................................................................................................................................8

References list:...............................................................................................................................10

2

ADVANCED FINANCIAL ACCOUNTING

Assessment Task Part A:

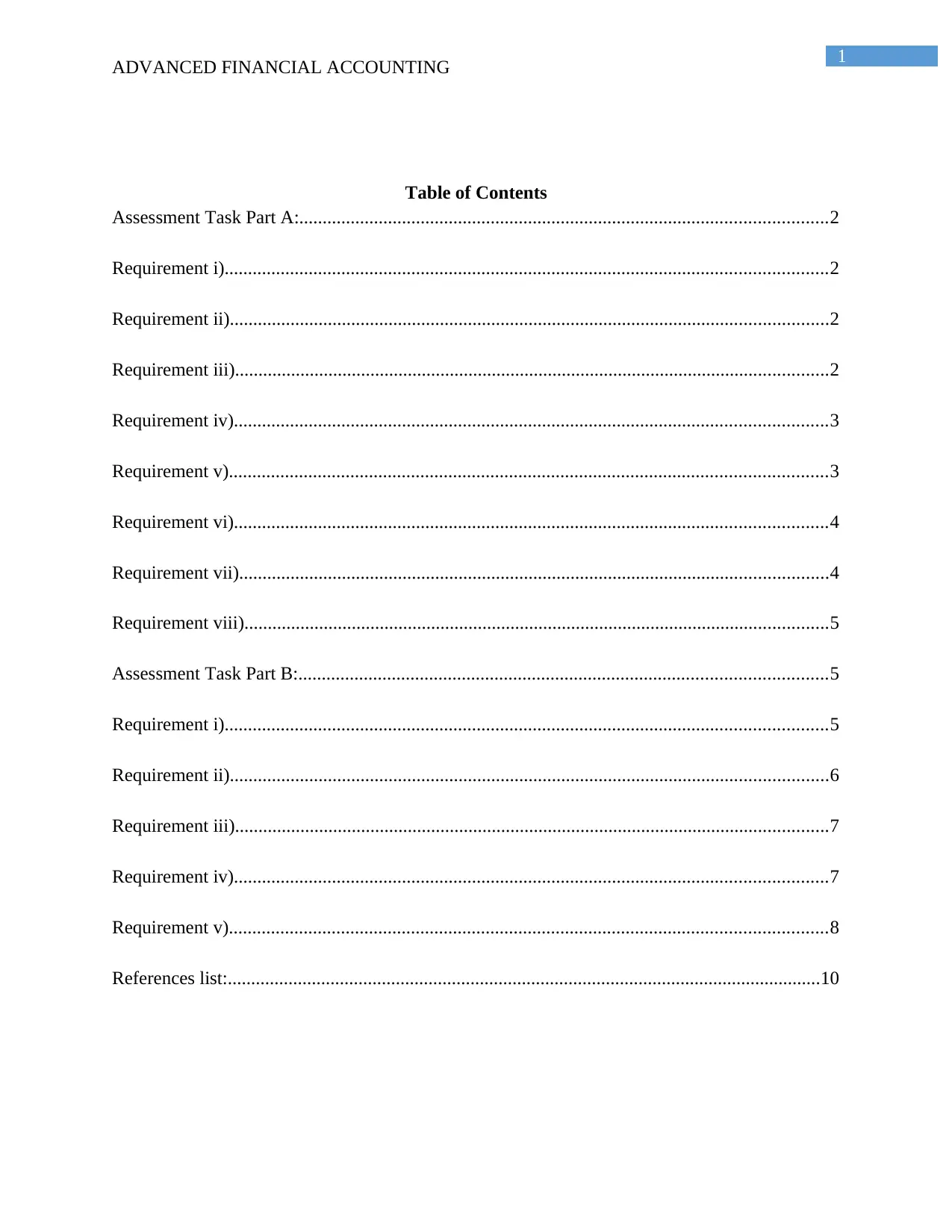

Requirement i)

Sims metal management limited conducts an impairment testing annually for goodwill

and other intangible assets. Testing of impairment is conducted when there is objective evidence

given by circumstance or happening of any events. Whenever there exists indication that it will

be difficult to recover the carrying amount of other definite lives intangible assets as indicated by

occurrence of some events and prevailing circumstances. Allocation of goodwill has been done

for impairment testing. The impairment testing for the cash-generating unit depicts excess

headroom of A$ 104.1 million for the year ending 30th June, 2016 (Simsmm.com 2018).

Requirement ii)

Sims metal management conducts the impairment testing of assets by reviewing the

amount of their carrying value and when there exists and indication that assts require

impairment. There is recognition of impairment loss when the estimated recoverable amount is

lower than the carrying amount of such assets. Recognition of trade and receivables is done at

fair value and measuring it subsequently at amortized cost by deducting any provision of

impairment. Trade receivables is written off against impairment account when it is identified by

organization such receivables become uncollectible. For impairment purpose, the carrying

amount of property, equipment and plant are reviewed and as indicated by existence of any

ADVANCED FINANCIAL ACCOUNTING

Assessment Task Part A:

Requirement i)

Sims metal management limited conducts an impairment testing annually for goodwill

and other intangible assets. Testing of impairment is conducted when there is objective evidence

given by circumstance or happening of any events. Whenever there exists indication that it will

be difficult to recover the carrying amount of other definite lives intangible assets as indicated by

occurrence of some events and prevailing circumstances. Allocation of goodwill has been done

for impairment testing. The impairment testing for the cash-generating unit depicts excess

headroom of A$ 104.1 million for the year ending 30th June, 2016 (Simsmm.com 2018).

Requirement ii)

Sims metal management conducts the impairment testing of assets by reviewing the

amount of their carrying value and when there exists and indication that assts require

impairment. There is recognition of impairment loss when the estimated recoverable amount is

lower than the carrying amount of such assets. Recognition of trade and receivables is done at

fair value and measuring it subsequently at amortized cost by deducting any provision of

impairment. Trade receivables is written off against impairment account when it is identified by

organization such receivables become uncollectible. For impairment purpose, the carrying

amount of property, equipment and plant are reviewed and as indicated by existence of any

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ADVANCED FINANCIAL ACCOUNTING

objective evidence and thereafter there is recognition of impairment loss. Intangible assets and

goodwill are tested annually for impairment as indicated by circumstances and occurrence of

events. Assessment of impairment of assets are done by grouping them at the lowest levels where

the cash flows have been separately identified and they are not dependant of cash flows

generating from other group of assets. Organization conducts annual testing of investment that is

made in joint ventures as indicated by the fact that their carrying value amount cannot be

recovered and there are any circumstances and events (Simsmm.com 2018).

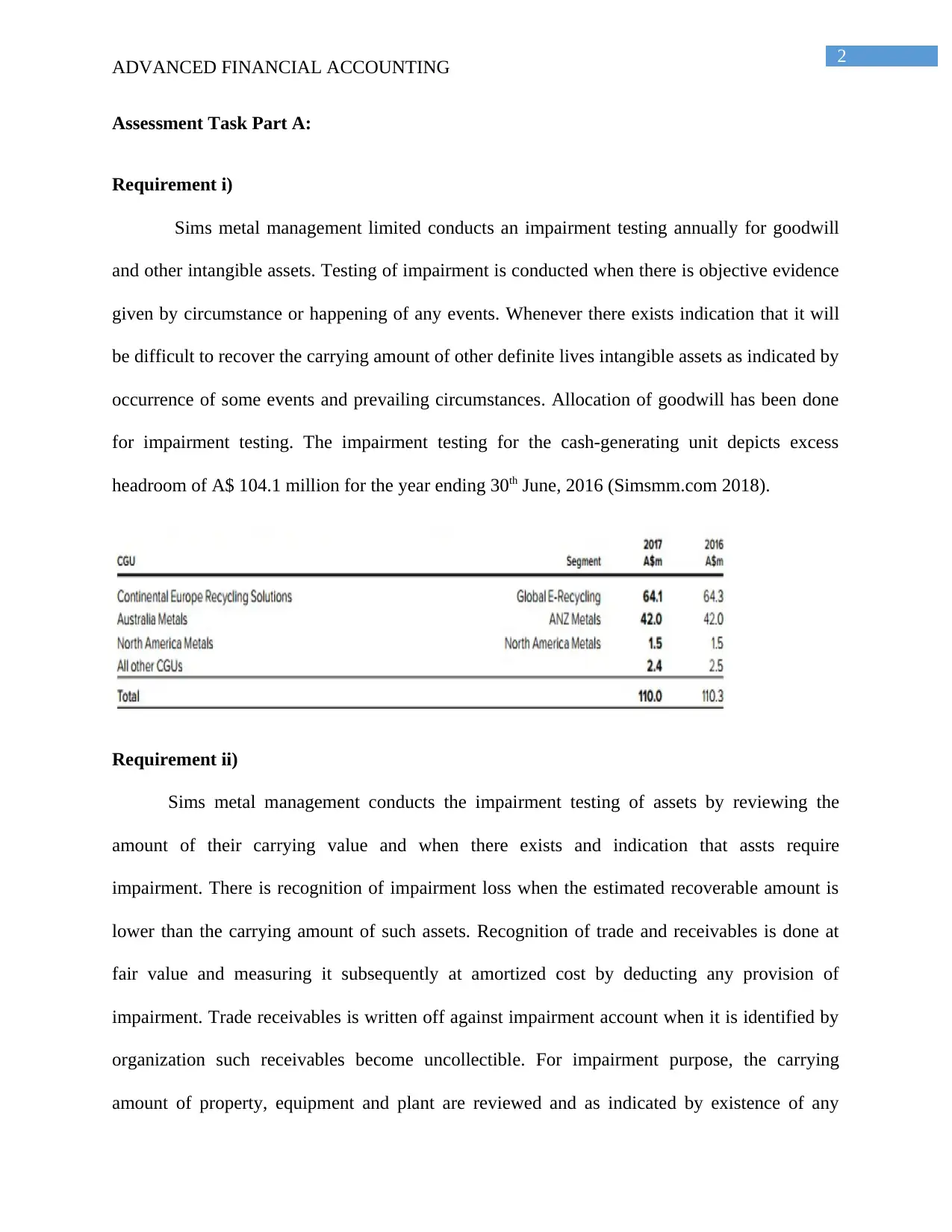

Requirement iii)

Impairment charge attributable to intangible assets and other goodwill for financial year

2016 stood at A $ 53 million. After the analysis of annual report of Sims metal management

limited, it has been ascertained that there has not been any impairment charge for the financial

year 2015 and 2017 in relation to assets and other goodwill (Simsmm.com 2018).

ADVANCED FINANCIAL ACCOUNTING

objective evidence and thereafter there is recognition of impairment loss. Intangible assets and

goodwill are tested annually for impairment as indicated by circumstances and occurrence of

events. Assessment of impairment of assets are done by grouping them at the lowest levels where

the cash flows have been separately identified and they are not dependant of cash flows

generating from other group of assets. Organization conducts annual testing of investment that is

made in joint ventures as indicated by the fact that their carrying value amount cannot be

recovered and there are any circumstances and events (Simsmm.com 2018).

Requirement iii)

Impairment charge attributable to intangible assets and other goodwill for financial year

2016 stood at A $ 53 million. After the analysis of annual report of Sims metal management

limited, it has been ascertained that there has not been any impairment charge for the financial

year 2015 and 2017 in relation to assets and other goodwill (Simsmm.com 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ADVANCED FINANCIAL ACCOUNTING

Requirement iv)

Sims metal management limited makes use of assumptions for conducting impairment

testing of goodwill and other intangible assets. Projection of five-year cash flow is done by

organization for computing the value in use and this is based on the budget after board approval

for the year 2017 and 2018 respectively. Historical average forms the basis of making four year

forecast and takes into account historical value for four years. Projections of five years

incorporates margin and price of commodity that are drawn from past experiences, estimates of

management relating to inherent impact on volume of future volatility and other factors relating

to current and expected future economic conditions. Organization also makes the application of

Gordon growth model for the determination of terminal value from the cash flow of final year.

Management makes best estimates in projecting the cash flow by referring to results that are

historical for determination of expense, income, cash flows for each cash generating unit and

capital expenditures (Simsmm.com 2018). Value in use of goodwill is determined by using

expected future cash flows. An estimation of CGU’s to intangible assets and goodwill

recoverable amount is required to be made for determining potential impairment relating to it.

Higher of any value in use and fair value less cost to sell helps in determining CGU recoverable

amount. Assumptions concerning growth rates and discount rates are to be made for the

calculations related to impairment testing.

ADVANCED FINANCIAL ACCOUNTING

Requirement iv)

Sims metal management limited makes use of assumptions for conducting impairment

testing of goodwill and other intangible assets. Projection of five-year cash flow is done by

organization for computing the value in use and this is based on the budget after board approval

for the year 2017 and 2018 respectively. Historical average forms the basis of making four year

forecast and takes into account historical value for four years. Projections of five years

incorporates margin and price of commodity that are drawn from past experiences, estimates of

management relating to inherent impact on volume of future volatility and other factors relating

to current and expected future economic conditions. Organization also makes the application of

Gordon growth model for the determination of terminal value from the cash flow of final year.

Management makes best estimates in projecting the cash flow by referring to results that are

historical for determination of expense, income, cash flows for each cash generating unit and

capital expenditures (Simsmm.com 2018). Value in use of goodwill is determined by using

expected future cash flows. An estimation of CGU’s to intangible assets and goodwill

recoverable amount is required to be made for determining potential impairment relating to it.

Higher of any value in use and fair value less cost to sell helps in determining CGU recoverable

amount. Assumptions concerning growth rates and discount rates are to be made for the

calculations related to impairment testing.

5

ADVANCED FINANCIAL ACCOUNTING

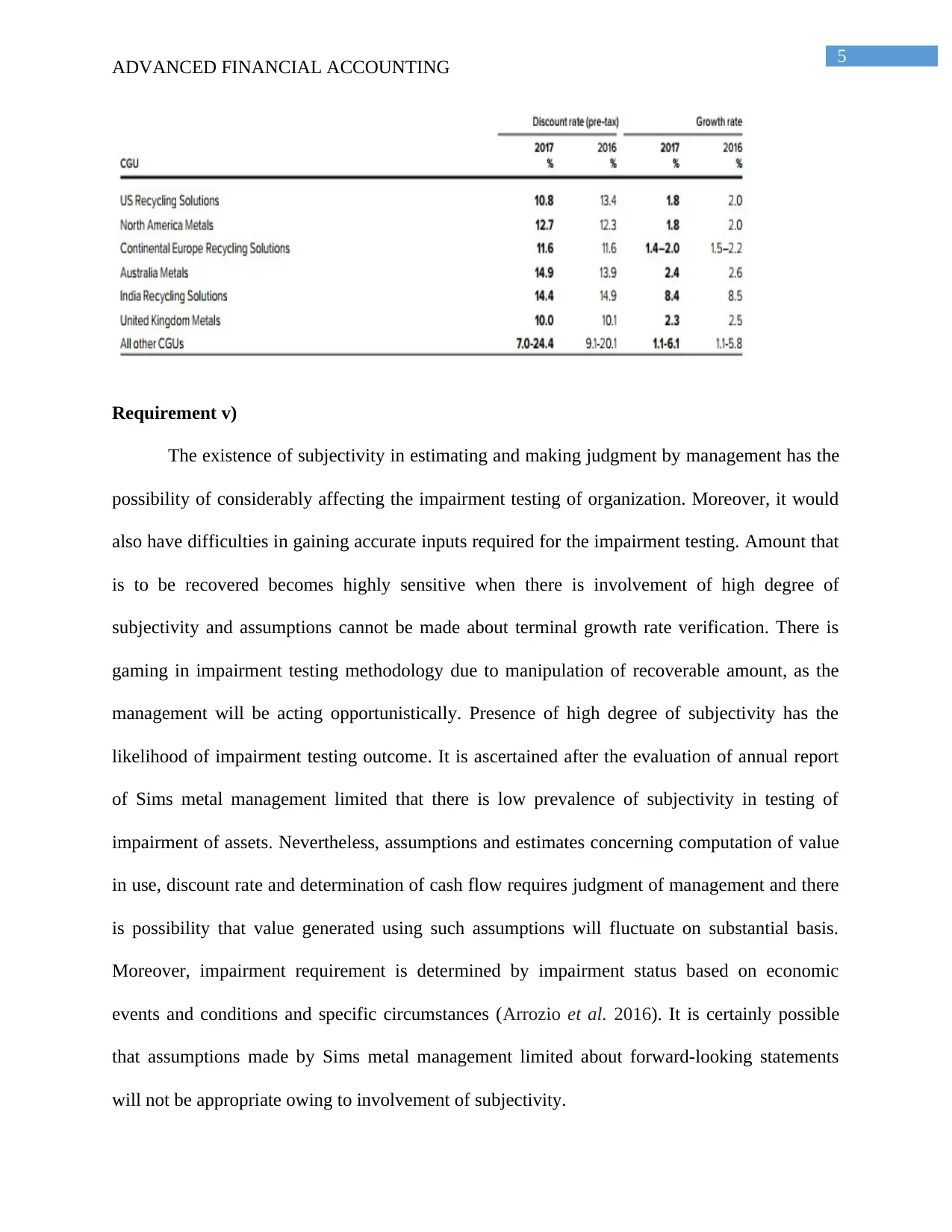

Requirement v)

The existence of subjectivity in estimating and making judgment by management has the

possibility of considerably affecting the impairment testing of organization. Moreover, it would

also have difficulties in gaining accurate inputs required for the impairment testing. Amount that

is to be recovered becomes highly sensitive when there is involvement of high degree of

subjectivity and assumptions cannot be made about terminal growth rate verification. There is

gaming in impairment testing methodology due to manipulation of recoverable amount, as the

management will be acting opportunistically. Presence of high degree of subjectivity has the

likelihood of impairment testing outcome. It is ascertained after the evaluation of annual report

of Sims metal management limited that there is low prevalence of subjectivity in testing of

impairment of assets. Nevertheless, assumptions and estimates concerning computation of value

in use, discount rate and determination of cash flow requires judgment of management and there

is possibility that value generated using such assumptions will fluctuate on substantial basis.

Moreover, impairment requirement is determined by impairment status based on economic

events and conditions and specific circumstances (Arrozio et al. 2016). It is certainly possible

that assumptions made by Sims metal management limited about forward-looking statements

will not be appropriate owing to involvement of subjectivity.

ADVANCED FINANCIAL ACCOUNTING

Requirement v)

The existence of subjectivity in estimating and making judgment by management has the

possibility of considerably affecting the impairment testing of organization. Moreover, it would

also have difficulties in gaining accurate inputs required for the impairment testing. Amount that

is to be recovered becomes highly sensitive when there is involvement of high degree of

subjectivity and assumptions cannot be made about terminal growth rate verification. There is

gaming in impairment testing methodology due to manipulation of recoverable amount, as the

management will be acting opportunistically. Presence of high degree of subjectivity has the

likelihood of impairment testing outcome. It is ascertained after the evaluation of annual report

of Sims metal management limited that there is low prevalence of subjectivity in testing of

impairment of assets. Nevertheless, assumptions and estimates concerning computation of value

in use, discount rate and determination of cash flow requires judgment of management and there

is possibility that value generated using such assumptions will fluctuate on substantial basis.

Moreover, impairment requirement is determined by impairment status based on economic

events and conditions and specific circumstances (Arrozio et al. 2016). It is certainly possible

that assumptions made by Sims metal management limited about forward-looking statements

will not be appropriate owing to involvement of subjectivity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ADVANCED FINANCIAL ACCOUNTING

Requirement vi)

Evaluation of annual report of Sims metal management limited indicates that impairment

testing methodology of is interesting. The impairment charge of cash generating unit was

impacted by margin pressure that arises from volatility in the prices of commodities and

landscape of competitive market. There were reassessment of US recycling solutions relating to

cash flows and this has indicated the fact that there is no recoverability of carrying amount of

goodwill. There would be fluctuation in the value of impairment charge recorded if the

assumptions about discount rate keep on changing. Calculations of value in use forms the basis

of estimating recoverable amount and it is performed independently by firm valuating the assets.

Impairment on investment is recognized by organization by assessing recoverable amount of

investments that are made in SA recycling (Simsmm.com 2018).

Requirement vii)

Analysis of annual report of Sims metal management limited concerning impairment

testing depicts that impairment that is recorded in the financial year 2016 involves impairment

that are recognized are offset closely by reversing the impairments that are recorded in the

previous year (Simsmm.com 2018). It has been ascertained from the annual report that there has

been impairment reversal in relation to property, plant and equipment. An insight that is gained

regarding impairment is that value of impairment charge fluctuates if there is any modification in

discount rate while all other assumptions remaining same.

ADVANCED FINANCIAL ACCOUNTING

Requirement vi)

Evaluation of annual report of Sims metal management limited indicates that impairment

testing methodology of is interesting. The impairment charge of cash generating unit was

impacted by margin pressure that arises from volatility in the prices of commodities and

landscape of competitive market. There were reassessment of US recycling solutions relating to

cash flows and this has indicated the fact that there is no recoverability of carrying amount of

goodwill. There would be fluctuation in the value of impairment charge recorded if the

assumptions about discount rate keep on changing. Calculations of value in use forms the basis

of estimating recoverable amount and it is performed independently by firm valuating the assets.

Impairment on investment is recognized by organization by assessing recoverable amount of

investments that are made in SA recycling (Simsmm.com 2018).

Requirement vii)

Analysis of annual report of Sims metal management limited concerning impairment

testing depicts that impairment that is recorded in the financial year 2016 involves impairment

that are recognized are offset closely by reversing the impairments that are recorded in the

previous year (Simsmm.com 2018). It has been ascertained from the annual report that there has

been impairment reversal in relation to property, plant and equipment. An insight that is gained

regarding impairment is that value of impairment charge fluctuates if there is any modification in

discount rate while all other assumptions remaining same.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ADVANCED FINANCIAL ACCOUNTING

Requirement viii)

Some of the financial liabilities and assets that are involves in the preparation of general

purpose financial report is based on fair value. Net loss generated by financial assets revaluation

is measured at fair value. Designations of investments in marketable securities are done as

financial assets that are at fair value. Last quoted price forms the basis of measurement of assets

fair value. Recognition of any alterations in fair value is accumulated in separate resources as

equity and done in the comprehensive income statement (Pavić et al. 2017). The estimated and

carrying amount of fair value of financial liabilities and assets of group is materially same.

Determination of financial instruments fair value that is not traded in active market is done using

broker quotes that are available readily. Organization makes use of valuation methodology for

classifying financial instruments that are measured at fair value by using hierarchy

(Simsmm.com 2018).

ADVANCED FINANCIAL ACCOUNTING

Requirement viii)

Some of the financial liabilities and assets that are involves in the preparation of general

purpose financial report is based on fair value. Net loss generated by financial assets revaluation

is measured at fair value. Designations of investments in marketable securities are done as

financial assets that are at fair value. Last quoted price forms the basis of measurement of assets

fair value. Recognition of any alterations in fair value is accumulated in separate resources as

equity and done in the comprehensive income statement (Pavić et al. 2017). The estimated and

carrying amount of fair value of financial liabilities and assets of group is materially same.

Determination of financial instruments fair value that is not traded in active market is done using

broker quotes that are available readily. Organization makes use of valuation methodology for

classifying financial instruments that are measured at fair value by using hierarchy

(Simsmm.com 2018).

8

ADVANCED FINANCIAL ACCOUNTING

Assessment Task Part B:

Requirement i)

The existing lease standard that is IAS 17 is associated with several criticisms that make

investors difficulties in having a true and fair view of financial position of reporting entities. For

the classification of lease as operating or finance, the standard allows lesser and lessees to

evaluate the transactions. One of the major flaws that are associated with the existing standard is

that organizations have incentives to make the classification of lease as operating lease. This has

the major consequence of key financial ratios of companies and classifying lease contracts as

operating lease finance is more favorable for companies. Financial ratios such as return on assets

and debt to equity ratios will get worsen if the lease contract is classified, as finance lease as

against operating lease and this does not affect the two ratios (Czajor and Michalak 2017). If the

positive income is generated by operating lease might improve the return on assets. It is

noteworthy to take into account that costs and benefits of both the lease whether financial and

operating leases are equal. However, the benefits provided by operating lease in terms of

financial ratios are purely an accounting illusion that is created in the investor’s eyes. IASB has

made the estimation that 85% of total amount of lease commitments out of US $ 3.3 million does

not appear on balance sheets (Brouwer et al. 2015). Therefore, actual liabilities of organization

might be less than what is presented on balance sheet and this is the reason why the existing

standard did not reflect true economic reality.

Requirement ii)

Providing user with information about entities that helps them in making economic

decisions is the objective of financial report that is prepared under the current lease standard.

Leasing transactions are likely to be classified unfaithfully under the existing standard. The rue

ADVANCED FINANCIAL ACCOUNTING

Assessment Task Part B:

Requirement i)

The existing lease standard that is IAS 17 is associated with several criticisms that make

investors difficulties in having a true and fair view of financial position of reporting entities. For

the classification of lease as operating or finance, the standard allows lesser and lessees to

evaluate the transactions. One of the major flaws that are associated with the existing standard is

that organizations have incentives to make the classification of lease as operating lease. This has

the major consequence of key financial ratios of companies and classifying lease contracts as

operating lease finance is more favorable for companies. Financial ratios such as return on assets

and debt to equity ratios will get worsen if the lease contract is classified, as finance lease as

against operating lease and this does not affect the two ratios (Czajor and Michalak 2017). If the

positive income is generated by operating lease might improve the return on assets. It is

noteworthy to take into account that costs and benefits of both the lease whether financial and

operating leases are equal. However, the benefits provided by operating lease in terms of

financial ratios are purely an accounting illusion that is created in the investor’s eyes. IASB has

made the estimation that 85% of total amount of lease commitments out of US $ 3.3 million does

not appear on balance sheets (Brouwer et al. 2015). Therefore, actual liabilities of organization

might be less than what is presented on balance sheet and this is the reason why the existing

standard did not reflect true economic reality.

Requirement ii)

Providing user with information about entities that helps them in making economic

decisions is the objective of financial report that is prepared under the current lease standard.

Leasing transactions are likely to be classified unfaithfully under the existing standard. The rue

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ADVANCED FINANCIAL ACCOUNTING

debt structure of companies is not provided on the balance sheets because of absence of value of

operating leases. Information that is presented in the balance sheets concerning leased assets and

liabilities is not sufficient and making accurate calculations for bringing some of lease

commitments back to balance sheet is difficult. Absence of operating lease on balance sheets for

impoverishing comparability between companies requires users to make the adjustments in the

balance sheets for operating leases (Nobes 2015). For ascertaining true debt structure,

discounted amount concerning leases is added back to balance sheet, which is not appropriate.

This explains why the off balance sheet liabilities were up to 66 times more than debt that is

reported on balance sheets.

Requirement iii)

The balance sheet of airline companies is formed under different accounting model and

there do not exist difference between operating lease and financing lease. Complications in

creating difference between financing and operating leases are one of the controversies that are

associated with affecting financial position of airline companies. It is so because either airline

companies buy aircraft fleets or they lease the fleets. This difference in lease accounting

illustrates financial position of such companies would be different. However, in reality, there

exists possibility that financial position of some airline companies is similar and identical.

Leasing structures and particular method of financing will affect the individual airline companies

(Karwowski 2016). Therefore, it can be said that there were no level playing field between some

airline companies.

Requirement iv)

The reason why the new lease standard will be unpopular is attributable to several

criticism associated with it. Debt structure and balance sheets of companies would increase due

ADVANCED FINANCIAL ACCOUNTING

debt structure of companies is not provided on the balance sheets because of absence of value of

operating leases. Information that is presented in the balance sheets concerning leased assets and

liabilities is not sufficient and making accurate calculations for bringing some of lease

commitments back to balance sheet is difficult. Absence of operating lease on balance sheets for

impoverishing comparability between companies requires users to make the adjustments in the

balance sheets for operating leases (Nobes 2015). For ascertaining true debt structure,

discounted amount concerning leases is added back to balance sheet, which is not appropriate.

This explains why the off balance sheet liabilities were up to 66 times more than debt that is

reported on balance sheets.

Requirement iii)

The balance sheet of airline companies is formed under different accounting model and

there do not exist difference between operating lease and financing lease. Complications in

creating difference between financing and operating leases are one of the controversies that are

associated with affecting financial position of airline companies. It is so because either airline

companies buy aircraft fleets or they lease the fleets. This difference in lease accounting

illustrates financial position of such companies would be different. However, in reality, there

exists possibility that financial position of some airline companies is similar and identical.

Leasing structures and particular method of financing will affect the individual airline companies

(Karwowski 2016). Therefore, it can be said that there were no level playing field between some

airline companies.

Requirement iv)

The reason why the new lease standard will be unpopular is attributable to several

criticism associated with it. Debt structure and balance sheets of companies would increase due

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ADVANCED FINANCIAL ACCOUNTING

to focus on operating lease capitalization. There is a possibility of violating existing debt

covenants of business due to 100% increase in balance sheets. It is indicative of the fact that

companies will be required to make renegotiation of debt covenants and this excludes

agreements concerning leases (Joubert et al. 2017). Furthermore, companies in receiving credits

have raised concerns. The impact of short-term leases would have absurd consequences on their

financial statements due to the implementation of the standard. Criticism of lease burden is also

because of considerable increase in administrative burden and some of the common examples in

relation to this are new IT systems, educational efforts, and increased expenditures in the

consultation fees and changes in process and control systems. Complications and increased cost

of reporting is another criticism of new lease standard because organizations having lot of lease

agreement will need to invest time in management information and investment in large amount

of new IT systems (Osei 2017). It is so because, there will be need of making estimations in

detail relating to right to use assets and lease liability.

Requirement v)

The implementation of new lease standard will make financial reports of organizations

useful to investors and financial analysts and will facilitate enhancement of comparison between

them. However, benefit of enhanced comparability will be achieved at the expense of

organizations recognizing all lease agreements on their balance sheets. Lease accountings that

are classified unfaithfully will be addressed under this standard. Implementation of the standard

will no longer require investors to make rough estimations and rough calculations for bringing

back lease commitments on balance sheets by computing substantial lease obligations.

Facilitation of transparency regarding the lease obligations will lead to better-informed decisions

among investors (Edeigba and Amenkhienan 2017). There will be more balanced lease versus

ADVANCED FINANCIAL ACCOUNTING

to focus on operating lease capitalization. There is a possibility of violating existing debt

covenants of business due to 100% increase in balance sheets. It is indicative of the fact that

companies will be required to make renegotiation of debt covenants and this excludes

agreements concerning leases (Joubert et al. 2017). Furthermore, companies in receiving credits

have raised concerns. The impact of short-term leases would have absurd consequences on their

financial statements due to the implementation of the standard. Criticism of lease burden is also

because of considerable increase in administrative burden and some of the common examples in

relation to this are new IT systems, educational efforts, and increased expenditures in the

consultation fees and changes in process and control systems. Complications and increased cost

of reporting is another criticism of new lease standard because organizations having lot of lease

agreement will need to invest time in management information and investment in large amount

of new IT systems (Osei 2017). It is so because, there will be need of making estimations in

detail relating to right to use assets and lease liability.

Requirement v)

The implementation of new lease standard will make financial reports of organizations

useful to investors and financial analysts and will facilitate enhancement of comparison between

them. However, benefit of enhanced comparability will be achieved at the expense of

organizations recognizing all lease agreements on their balance sheets. Lease accountings that

are classified unfaithfully will be addressed under this standard. Implementation of the standard

will no longer require investors to make rough estimations and rough calculations for bringing

back lease commitments on balance sheets by computing substantial lease obligations.

Facilitation of transparency regarding the lease obligations will lead to better-informed decisions

among investors (Edeigba and Amenkhienan 2017). There will be more balanced lease versus

11

ADVANCED FINANCIAL ACCOUNTING

buy decisions as adoption of standard will lead to efficient allocation of capital and better

decisions on part of management.

References list:

ADVANCED FINANCIAL ACCOUNTING

buy decisions as adoption of standard will lead to efficient allocation of capital and better

decisions on part of management.

References list:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.