Detailed Assessment of Taxation Including Medicare Levy and Income Tax

VerifiedAdded on 2020/03/07

|7

|997

|46

Homework Assignment

AI Summary

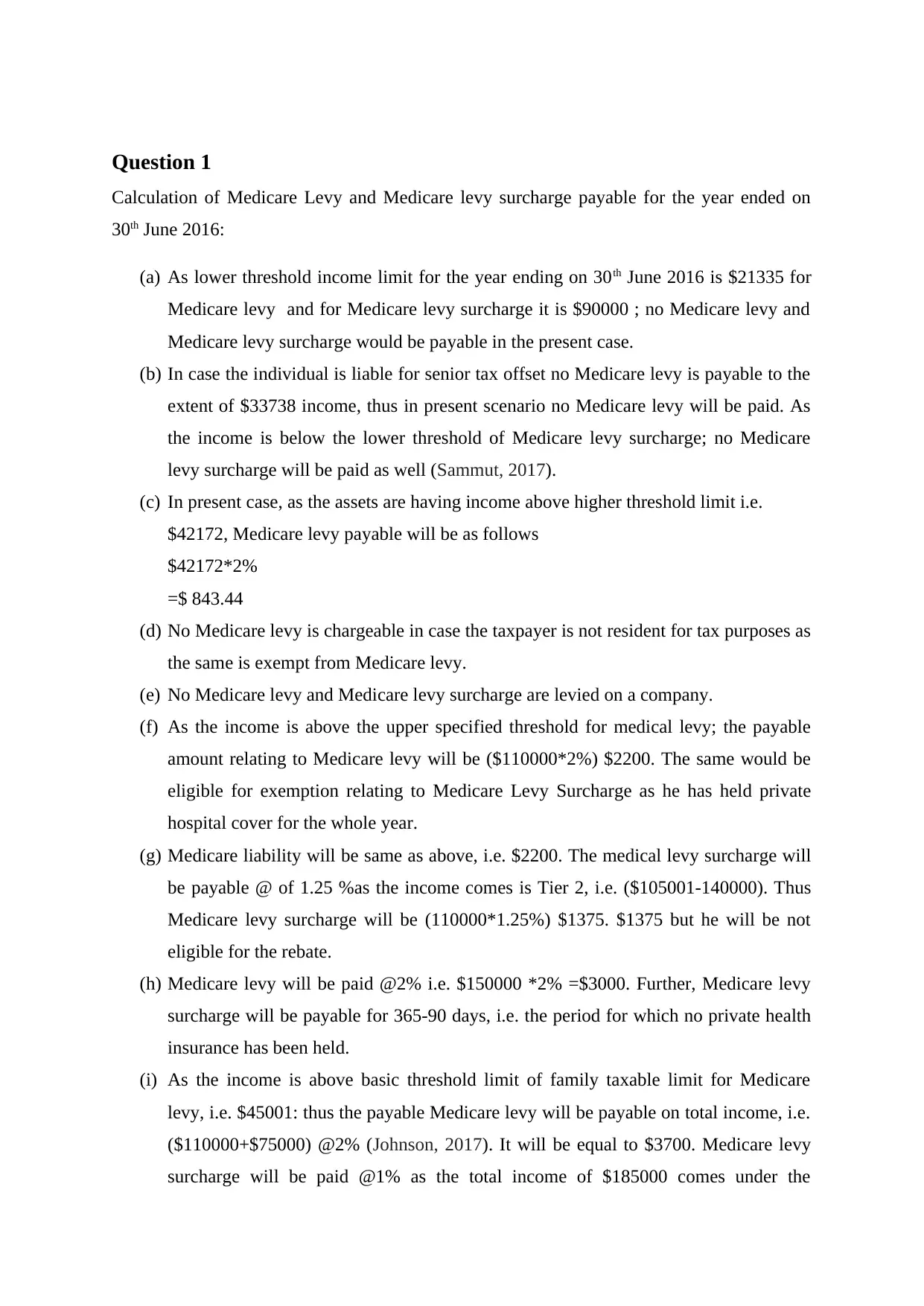

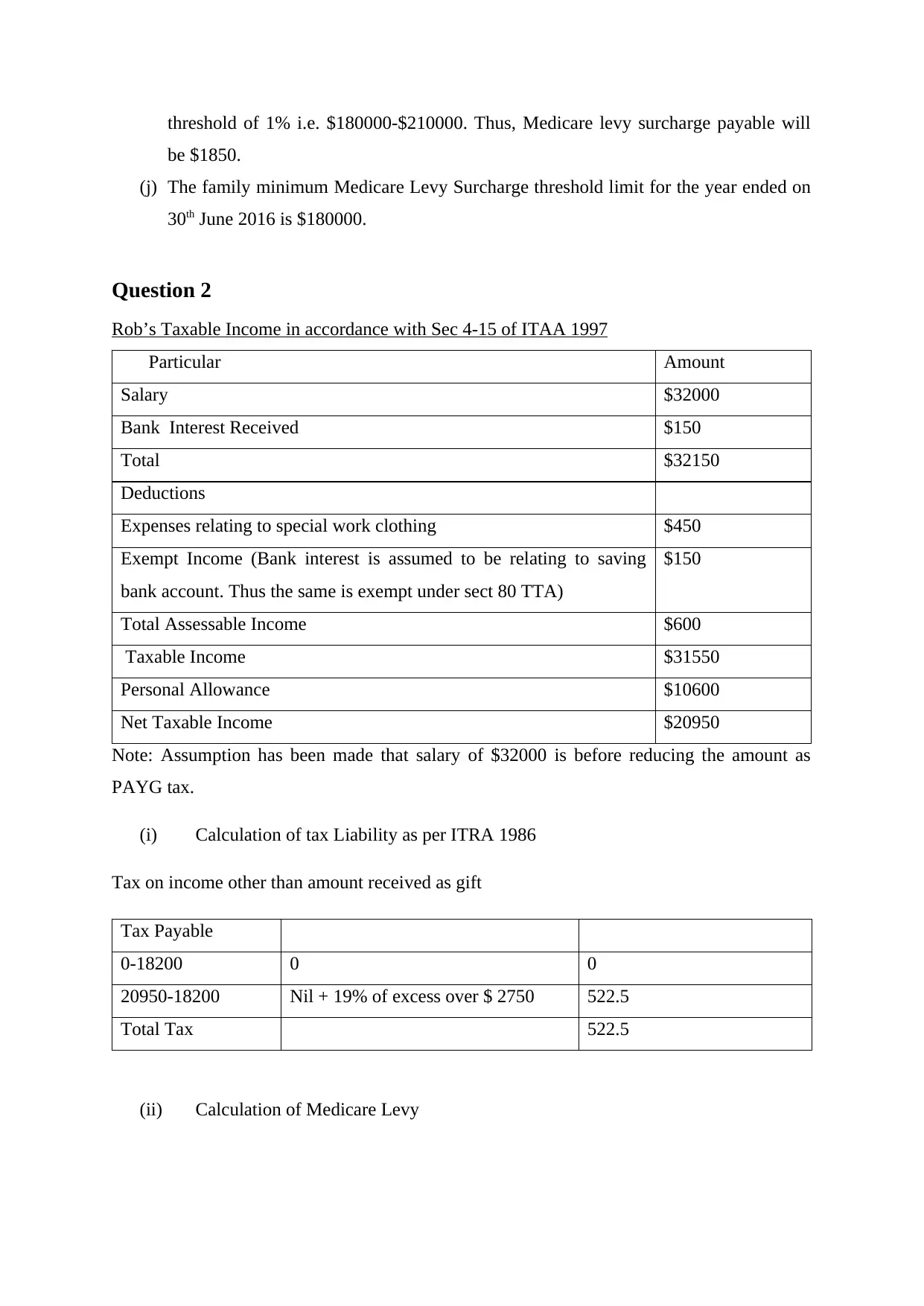

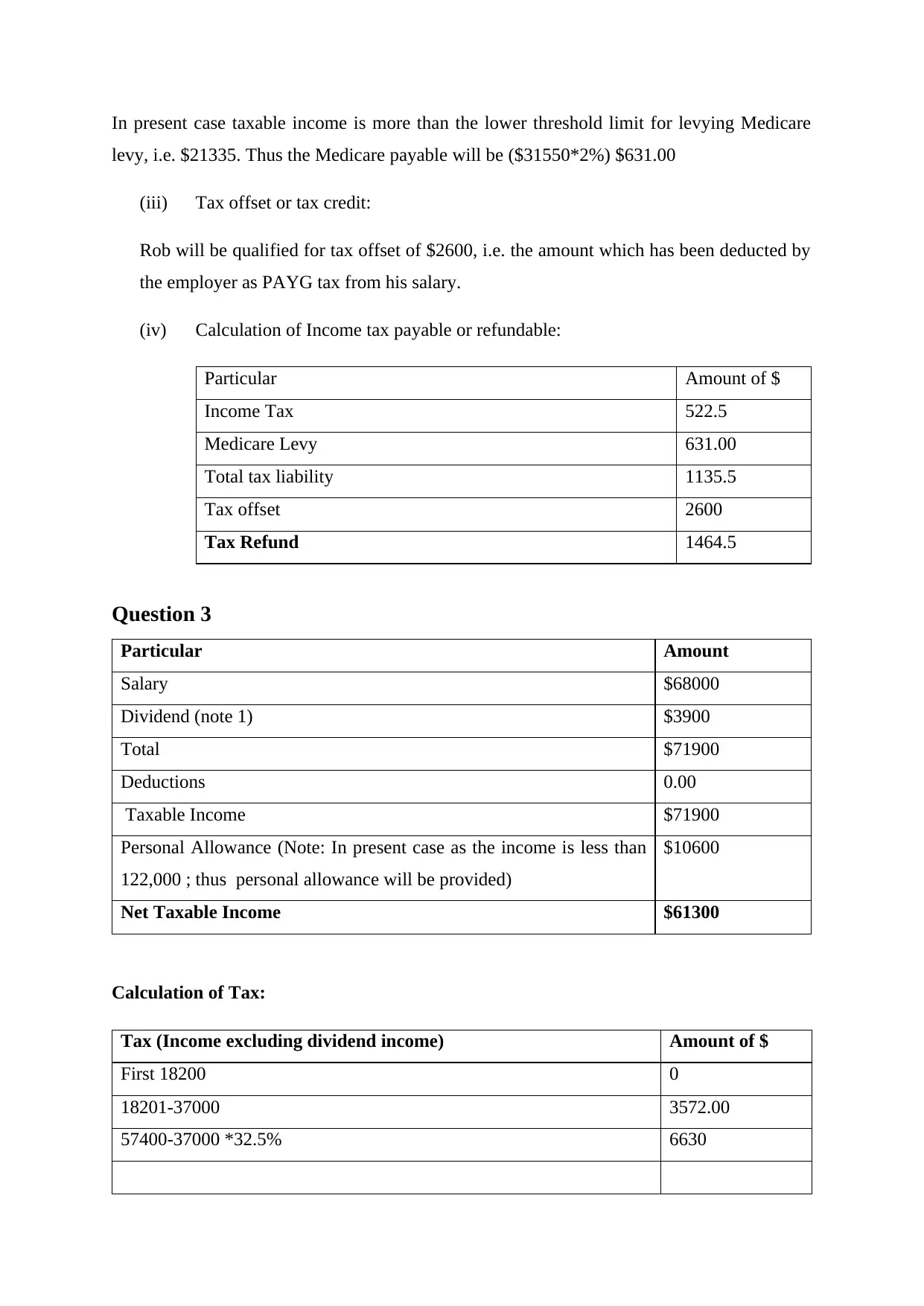

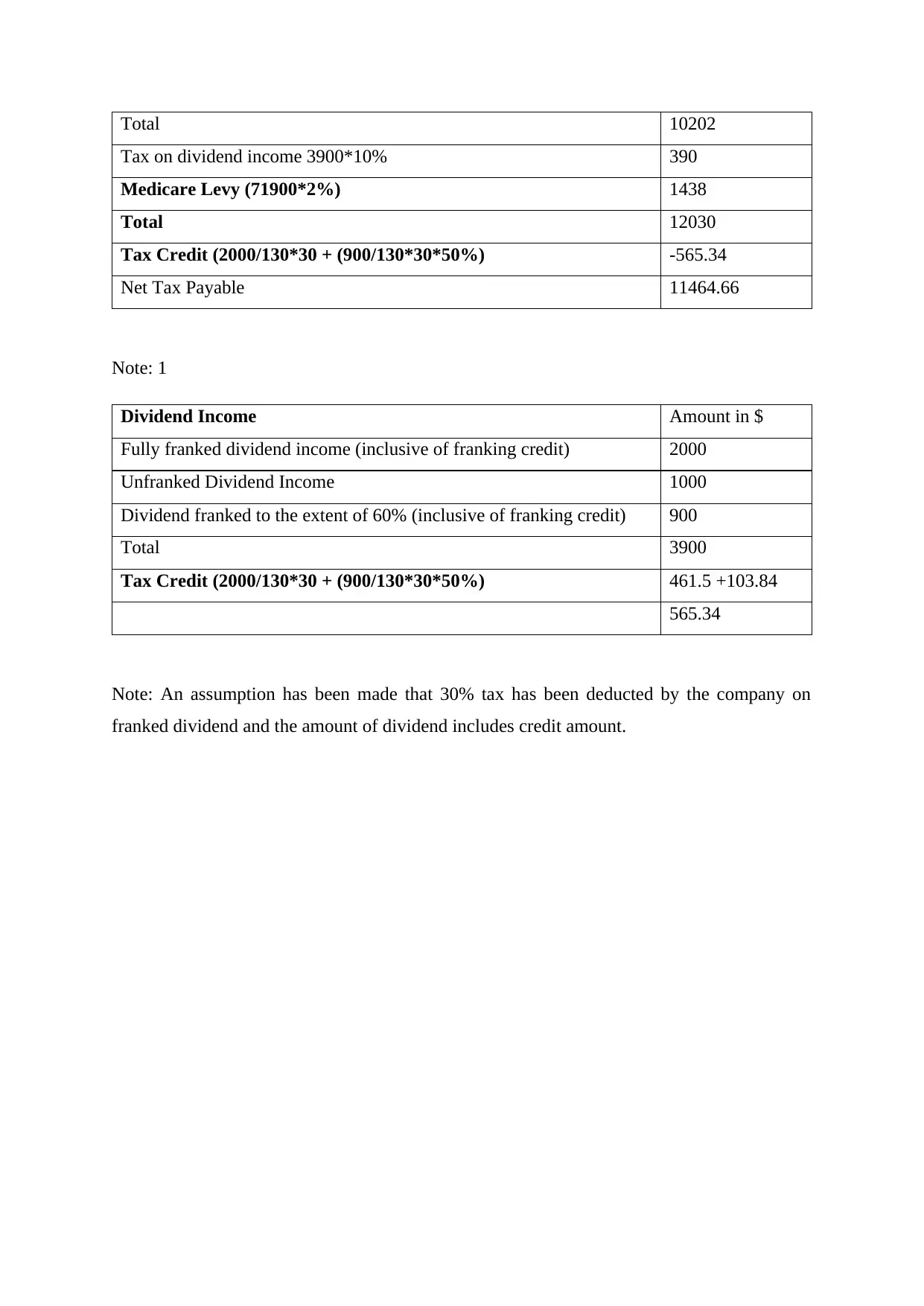

This homework assignment assesses various aspects of taxation, including the calculation of Medicare levy and Medicare levy surcharge under different scenarios, considering income thresholds and private health insurance. The assessment then delves into calculating taxable income, tax liability, and tax refunds for an individual, incorporating deductions for work clothing and the application of tax offsets. Finally, the assignment analyzes the taxation of dividend income, including fully franked, unfranked, and partially franked dividends, and determines the net tax payable after considering tax credits and personal allowances. The assignment utilizes relevant sections of the ITAA 1997 and ITRA 1986 to support its calculations.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.