Business Finance Report: Financial Statement Analysis and Budgeting

VerifiedAdded on 2023/01/03

|14

|3272

|96

Report

AI Summary

This report provides a comprehensive analysis of business finance, encompassing financial statement analysis, accounting methods, and budgeting techniques. The report begins with an examination of the statement of profit or loss, evaluating revenue, cost of sales, gross profit, operating expenses, and net profit. It then delves into the statement of financial position, analyzing current ratios, receivable turnover ratios, and payable turnover ratios to assess the company's liquidity and efficiency. The report further explores the concepts of accrual and cash accounting, comparing their benefits and limitations. It also differentiates between cash flow and profit, highlighting their significance in assessing a company's financial health. The report concludes by defining a budget and explaining its purposes, along with the benefits of forming a limited company and listing it on a stock exchange, providing a holistic overview of key financial concepts and their practical applications.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

MAIN BODY..............................................................................................................................................3

Part 1...........................................................................................................................................................3

Part 2...........................................................................................................................................................7

Part3............................................................................................................................................................8

REFERENCES..........................................................................................................................................12

APPENDIX...............................................................................................................................................13

MAIN BODY..............................................................................................................................................3

Part 1...........................................................................................................................................................3

Part 2...........................................................................................................................................................7

Part3............................................................................................................................................................8

REFERENCES..........................................................................................................................................12

APPENDIX...............................................................................................................................................13

MAIN BODY

Part 1

1.1 Statement of Profit or Loss

Revenue: Revenue is the benefit generated from periodic retail transactions, which involves caps

and discounts on the licensed stock. This would be the main line or calculation of the net

earnings from which losses are excluded to measure the gross pay (Adhikary and Kutsuna,

2016). Profits are cash placed into the corporation by an individual. A tender record is called

sales, an extension to the expenditure ratio and, as in the bargaining cost ratio, uses revenue

throughout the divisor.

There are different paths for estimating revenue depending on the option of accounting used.

Investments created using a loan as income for the products or managers supplied by the

consumer require collective accounting. It is important to evaluate the competitiveness of a

business that receives the money owing to analyze the independent financial. As the revenues

have declined by 35 percent since 2018, the revenues overall trend is falling. The reason may be

decline in government expenditure, either because of changes in popular taste or poor marketing

campaigns. As the Profit has also declined, price is not viewed as the variable in the decline in

Cost of Sales.

Cost of Sales-Since 2018, company sales costs have also dropped by 11 percent, but this decline

is lower than the income decline. This indicates the failure of a business to control its costs with

a decrease in revenue. It is suggested here that company should focus on cost-management

measures.

Gross Profit: Gross profit is reduced by 51 percent, as stated above. A rise in the cost of sales is

the source of the fall in profits. Owing to a 15 percent decrease in gross margin since 2018, sales

rates have increased by 24 percent. The corporation has three choices for rising gross profit:

raising revenue, growing selling rates and enhance the value of the commodity.

Part 1

1.1 Statement of Profit or Loss

Revenue: Revenue is the benefit generated from periodic retail transactions, which involves caps

and discounts on the licensed stock. This would be the main line or calculation of the net

earnings from which losses are excluded to measure the gross pay (Adhikary and Kutsuna,

2016). Profits are cash placed into the corporation by an individual. A tender record is called

sales, an extension to the expenditure ratio and, as in the bargaining cost ratio, uses revenue

throughout the divisor.

There are different paths for estimating revenue depending on the option of accounting used.

Investments created using a loan as income for the products or managers supplied by the

consumer require collective accounting. It is important to evaluate the competitiveness of a

business that receives the money owing to analyze the independent financial. As the revenues

have declined by 35 percent since 2018, the revenues overall trend is falling. The reason may be

decline in government expenditure, either because of changes in popular taste or poor marketing

campaigns. As the Profit has also declined, price is not viewed as the variable in the decline in

Cost of Sales.

Cost of Sales-Since 2018, company sales costs have also dropped by 11 percent, but this decline

is lower than the income decline. This indicates the failure of a business to control its costs with

a decrease in revenue. It is suggested here that company should focus on cost-management

measures.

Gross Profit: Gross profit is reduced by 51 percent, as stated above. A rise in the cost of sales is

the source of the fall in profits. Owing to a 15 percent decrease in gross margin since 2018, sales

rates have increased by 24 percent. The corporation has three choices for rising gross profit:

raising revenue, growing selling rates and enhance the value of the commodity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Operating expenses- It is increased by 23% due to investing on business model or recruiting new

sales staff employees. It is a bad indicator for the corporation and can be handled by eliminating

excessive publicity campaign investments and paying extra staff compensation.

Net Profit before tax- When it first appears in a firm's financial summary, the main point is

considered Net Profit before tax. Brief costs, often known as honesty, are included in maximum

compensation. There is a surplus as the profits exceed the expenses (Finance, 2015). In order to

maximize revenue, and therefore the income of each enterprise for owners, a corporation

increases revenues and reduces costs. Accounting consultants also independently consider an

individual's total income and benefits to measure tax cuts for the wealthy. Business expenses will

increase as long as revenues remain steady due to cost reductions. A very situation really doesn't

look good for the success of a company. When public agencies record quarterly earnings, sales

and net taxes, the two most notable figures regarded are ("profit" equals total). Being sure the

increased stock valuation is largely contingent on whether a corporation is substantially

outstripping or diminishing the sales and profit of each stock specialist.

Net Profit after tax: The Organization faces a deficit of £ 394,000; a significant 23 percent

growth in operational spending is the reason for this. The only option to profit in the next year is

either to increase net earnings or decrease running costs.

1.2 Statement of Financial Position

The balance sheet is often known as a mechanism for reporting all relevant information relating

to the company's financial situation (Babajide,, Olokoyo and Taiwo, 2016). It is simply a

representation of the financial position of an entity or a group. It could be a firm's sole trader,

company, corporate association, legal body, or some other structure. For all ways of being

prepared, this argument is necessary. That is beneficial because it gives an essential and equal

financial situation. The balance sheet will identify the various main elements of any company,

including currency, leverage, securities, etc.

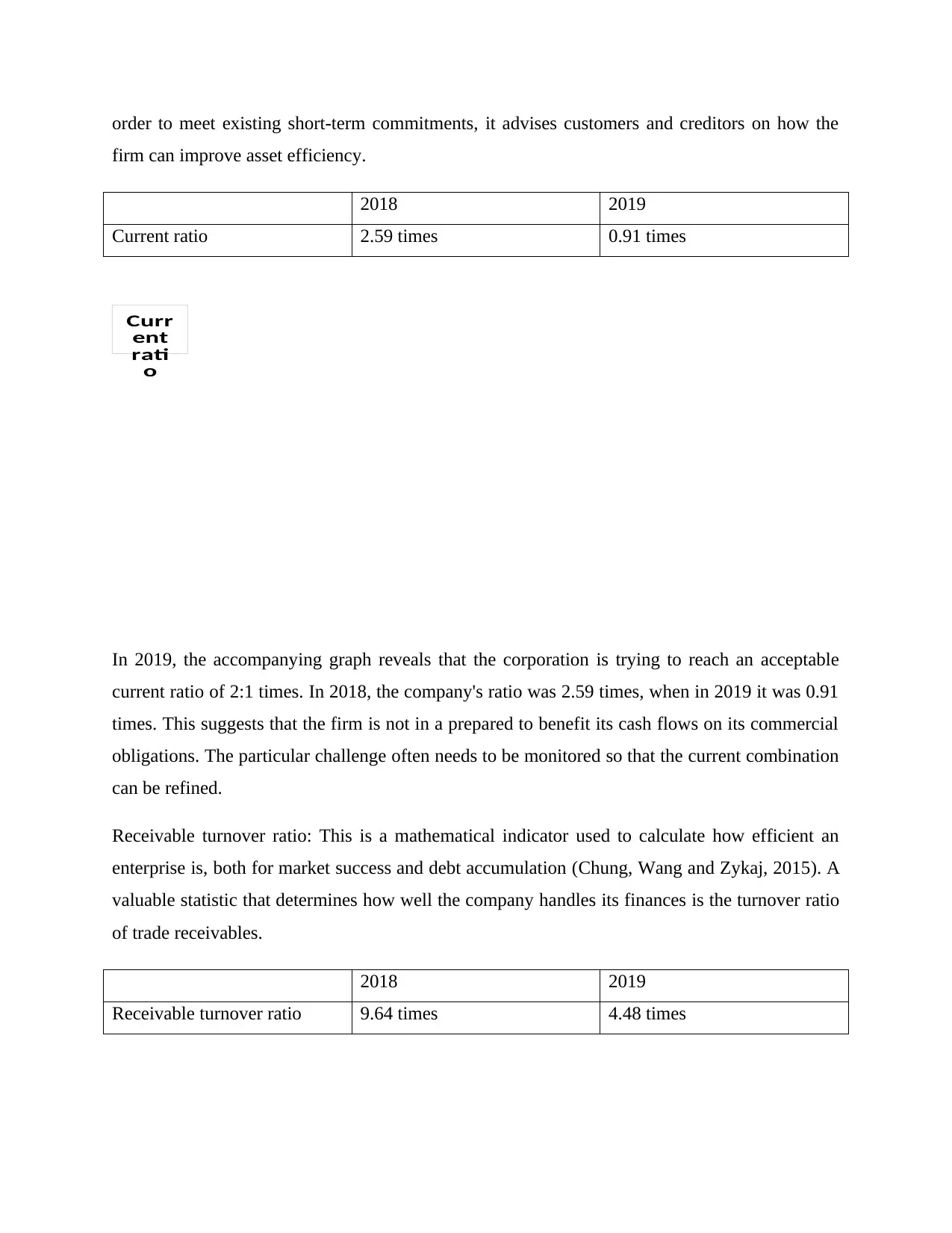

Current ratio: The current ratio is an accounting metric used to determine a company's readiness

to recognize fair or due commitments within one year (Jordà, Schularick and Taylor, 2016). In

sales staff employees. It is a bad indicator for the corporation and can be handled by eliminating

excessive publicity campaign investments and paying extra staff compensation.

Net Profit before tax- When it first appears in a firm's financial summary, the main point is

considered Net Profit before tax. Brief costs, often known as honesty, are included in maximum

compensation. There is a surplus as the profits exceed the expenses (Finance, 2015). In order to

maximize revenue, and therefore the income of each enterprise for owners, a corporation

increases revenues and reduces costs. Accounting consultants also independently consider an

individual's total income and benefits to measure tax cuts for the wealthy. Business expenses will

increase as long as revenues remain steady due to cost reductions. A very situation really doesn't

look good for the success of a company. When public agencies record quarterly earnings, sales

and net taxes, the two most notable figures regarded are ("profit" equals total). Being sure the

increased stock valuation is largely contingent on whether a corporation is substantially

outstripping or diminishing the sales and profit of each stock specialist.

Net Profit after tax: The Organization faces a deficit of £ 394,000; a significant 23 percent

growth in operational spending is the reason for this. The only option to profit in the next year is

either to increase net earnings or decrease running costs.

1.2 Statement of Financial Position

The balance sheet is often known as a mechanism for reporting all relevant information relating

to the company's financial situation (Babajide,, Olokoyo and Taiwo, 2016). It is simply a

representation of the financial position of an entity or a group. It could be a firm's sole trader,

company, corporate association, legal body, or some other structure. For all ways of being

prepared, this argument is necessary. That is beneficial because it gives an essential and equal

financial situation. The balance sheet will identify the various main elements of any company,

including currency, leverage, securities, etc.

Current ratio: The current ratio is an accounting metric used to determine a company's readiness

to recognize fair or due commitments within one year (Jordà, Schularick and Taylor, 2016). In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

order to meet existing short-term commitments, it advises customers and creditors on how the

firm can improve asset efficiency.

2018 2019

Current ratio 2.59 times 0.91 times

Curr

ent

rati

o

In 2019, the accompanying graph reveals that the corporation is trying to reach an acceptable

current ratio of 2:1 times. In 2018, the company's ratio was 2.59 times, when in 2019 it was 0.91

times. This suggests that the firm is not in a prepared to benefit its cash flows on its commercial

obligations. The particular challenge often needs to be monitored so that the current combination

can be refined.

Receivable turnover ratio: This is a mathematical indicator used to calculate how efficient an

enterprise is, both for market success and debt accumulation (Chung, Wang and Zykaj, 2015). A

valuable statistic that determines how well the company handles its finances is the turnover ratio

of trade receivables.

2018 2019

Receivable turnover ratio 9.64 times 4.48 times

firm can improve asset efficiency.

2018 2019

Current ratio 2.59 times 0.91 times

Curr

ent

rati

o

In 2019, the accompanying graph reveals that the corporation is trying to reach an acceptable

current ratio of 2:1 times. In 2018, the company's ratio was 2.59 times, when in 2019 it was 0.91

times. This suggests that the firm is not in a prepared to benefit its cash flows on its commercial

obligations. The particular challenge often needs to be monitored so that the current combination

can be refined.

Receivable turnover ratio: This is a mathematical indicator used to calculate how efficient an

enterprise is, both for market success and debt accumulation (Chung, Wang and Zykaj, 2015). A

valuable statistic that determines how well the company handles its finances is the turnover ratio

of trade receivables.

2018 2019

Receivable turnover ratio 9.64 times 4.48 times

Rec

eiva

ble

turn

over

rati

o

Above that the table suggests that while their percentage was 9.64 times, the company effectively

managed the commitments for the year 2018, which indicates that the expenses were earned at

discrete tables. It was reduced to 4.48 as it was during 2019, indicating that the company had

been unable to repay its debts in less years. Compared to 2018, the industry took more in fiscal

year 2019.

Payable turnover ratio- How quickly a business receives deposits from creditors and vendors that

grow new loans is determined by the turnover margin of paying earnings (Kapinos, Gurley-

Calvez and Kapinos, 2016). By estimating the total number of days, the auditors calculate the

amount of time the organization owes AP support over a given period of time.

2018 2019

Payable turnover ratio 15.45 times 9.05 times

eiva

ble

turn

over

rati

o

Above that the table suggests that while their percentage was 9.64 times, the company effectively

managed the commitments for the year 2018, which indicates that the expenses were earned at

discrete tables. It was reduced to 4.48 as it was during 2019, indicating that the company had

been unable to repay its debts in less years. Compared to 2018, the industry took more in fiscal

year 2019.

Payable turnover ratio- How quickly a business receives deposits from creditors and vendors that

grow new loans is determined by the turnover margin of paying earnings (Kapinos, Gurley-

Calvez and Kapinos, 2016). By estimating the total number of days, the auditors calculate the

amount of time the organization owes AP support over a given period of time.

2018 2019

Payable turnover ratio 15.45 times 9.05 times

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Pay

able

turn

over

rati

o

The above table showed that the company treated its obligations in a good manner for 2018,

while the average was 15.45 times, indicating that their debts were met at fewer periods. Even

though it dropped in 2019, in fewer years, it was 9.05 times when the business would not be able

to pay its debts. Compared to 2018, the business took longer in the period 2019.

Part 2

2.1. Explain the concept of accrual accounting versus cash accounting, including the benefits and

any limitations of each

There are mostly two accounting, financial planning and internal audit groups, since they are

properly regulated techniques that are very important to the group and are also analyzed in depth

below with respect to T Shirt plc.

Accrual accounting method- According to this financial accounting system, a charge is

reported if it can be measured in terms of revenue for the same period. Real cash transfers are a

change in leadership immediately following a time in the field of revenue. The transaction will

only be recorded in the cash position at the time that it is needed for the cash exchange (Burns

and Dewhurst, 2016). The sum will be reported in the tax documents for the next day if there is

an incentive for benefit or loss on some transaction. Since income and losses are reported hand-

to-hand instead of pending the payout period, it is very necessary and is often practiced by

able

turn

over

rati

o

The above table showed that the company treated its obligations in a good manner for 2018,

while the average was 15.45 times, indicating that their debts were met at fewer periods. Even

though it dropped in 2019, in fewer years, it was 9.05 times when the business would not be able

to pay its debts. Compared to 2018, the business took longer in the period 2019.

Part 2

2.1. Explain the concept of accrual accounting versus cash accounting, including the benefits and

any limitations of each

There are mostly two accounting, financial planning and internal audit groups, since they are

properly regulated techniques that are very important to the group and are also analyzed in depth

below with respect to T Shirt plc.

Accrual accounting method- According to this financial accounting system, a charge is

reported if it can be measured in terms of revenue for the same period. Real cash transfers are a

change in leadership immediately following a time in the field of revenue. The transaction will

only be recorded in the cash position at the time that it is needed for the cash exchange (Burns

and Dewhurst, 2016). The sum will be reported in the tax documents for the next day if there is

an incentive for benefit or loss on some transaction. Since income and losses are reported hand-

to-hand instead of pending the payout period, it is very necessary and is often practiced by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

international corporations and major companies. The main advantage is that it is very fast and

easy to run and very helpful with a great deal of flexibility in doing company. Although the

biggest downside of these financial reports is that reporting is needed and the section spending of

a consumer is not advantageous.

Cash basis accounting: According to this scheme, payments will only be listed in the financial

records if any cash purchase purchases or rights were created. In the accounting cycle, such as

depreciation, payments that do not have any money movements would not be listed. This

strategy is not used in large firms, but is suitable for large enterprises and their financial position,

where main source of exchange is considered to be currency. It is very meaningful for an

organization where trades are often made on the basis of pounds. The main benefit is that it

symbolizes the strategic plan and inclusive operations in the long run. The only drawback is that

it reduces the company's jobs and activities and therefore has a negative effect.

2.2

The major difference between cash flow and profit is that once all expenses have been paid, the

cash flow reflects net cash flow, even though income reflects the revenues and expenses.

Company organizations often find a metric to recognize the health of a company. They can see

what the exact sum will look towards that in order to see when they can invest or steer their

business strategy. The income source and benefit are still at odds as two critical and intertwined

indicators of profitability: who wants the most?

There is no straightforward solution to this issue; all income and working capital are relevant in

their own manner (Haldane, 2016). Profit and working capital is only a couple of the numerous

money opportunities, metrics, and metrics that can know in ways that will improve strategic

decisions. With a full understanding of core financial principles, it is possible to eventually

become a much more moderate entrepreneur or shareholder.

Part3: Budget techniques and Company Finance

3.1. Define Budget and explain purposes of preparing a budget.

easy to run and very helpful with a great deal of flexibility in doing company. Although the

biggest downside of these financial reports is that reporting is needed and the section spending of

a consumer is not advantageous.

Cash basis accounting: According to this scheme, payments will only be listed in the financial

records if any cash purchase purchases or rights were created. In the accounting cycle, such as

depreciation, payments that do not have any money movements would not be listed. This

strategy is not used in large firms, but is suitable for large enterprises and their financial position,

where main source of exchange is considered to be currency. It is very meaningful for an

organization where trades are often made on the basis of pounds. The main benefit is that it

symbolizes the strategic plan and inclusive operations in the long run. The only drawback is that

it reduces the company's jobs and activities and therefore has a negative effect.

2.2

The major difference between cash flow and profit is that once all expenses have been paid, the

cash flow reflects net cash flow, even though income reflects the revenues and expenses.

Company organizations often find a metric to recognize the health of a company. They can see

what the exact sum will look towards that in order to see when they can invest or steer their

business strategy. The income source and benefit are still at odds as two critical and intertwined

indicators of profitability: who wants the most?

There is no straightforward solution to this issue; all income and working capital are relevant in

their own manner (Haldane, 2016). Profit and working capital is only a couple of the numerous

money opportunities, metrics, and metrics that can know in ways that will improve strategic

decisions. With a full understanding of core financial principles, it is possible to eventually

become a much more moderate entrepreneur or shareholder.

Part3: Budget techniques and Company Finance

3.1. Define Budget and explain purposes of preparing a budget.

The budget can be described as a structured calculation of a company's costs and income to

assess and quantify efficiency for this factor. The main aim of developing a budget is to develop

a strategy for the lengthy planning, control and development of the performance of an

organization so that, within a short amount of time, the corporation's priorities and targets can be

accomplished in an effective and reliable way.

Budget's Rationale:

A properly crafted budget helps a corporation to watch where they are going to be economically

in an ongoing phase (Fraser, Bhaumik and Wright, 2015). This facilitates real long preparation

for all, from actual operating costs to future growth. Realizing where the plan falls provides

opportunities for adding new workers, investing in better varieties of merchandise, and setting

targets for profits in line with the financial investment demands of the businesses.

An especially important aspect of corporate investment plan is budget control. Chief executives

and managers want to be able to identify whether or not a corporation is going to make a profit.

Essentially, the goal of budgeting is to provide a blueprint to how the organization will operate if

such policies, processes, strategies, got successfully, are followed.

The aim of a budget is to provide decision-making process with a financial basis i.e. the desired

way to proceed, is what businesses are preparing or not for. Spending should be closely regulated

when carefully operating an organization. Before the promotional expenditure has been

sufficiently spent, the assumption that businesses can expend money on marketing is likely to be

" is possibly to be no". The aim of financial planning is to enable actual operational efficiency,

i.e. the organization that achieves our targets, to be calculated against the planned financial

performance. The discrepancy among planned amounts and real expenditure is "variance" in the

inverse formula.

For regional administrators, who often work on a small budget, financial planning is incredibly

important. In a limited company, being marginally off on expense estimates or income may have

a devastating effect as well. It could be worth recruiting the in outside or auditor or a

professional analyst who has experience in business finance to ensure that budgetary control is

carried out effectively. This staff would aid with developing accounting, monitoring spending

assess and quantify efficiency for this factor. The main aim of developing a budget is to develop

a strategy for the lengthy planning, control and development of the performance of an

organization so that, within a short amount of time, the corporation's priorities and targets can be

accomplished in an effective and reliable way.

Budget's Rationale:

A properly crafted budget helps a corporation to watch where they are going to be economically

in an ongoing phase (Fraser, Bhaumik and Wright, 2015). This facilitates real long preparation

for all, from actual operating costs to future growth. Realizing where the plan falls provides

opportunities for adding new workers, investing in better varieties of merchandise, and setting

targets for profits in line with the financial investment demands of the businesses.

An especially important aspect of corporate investment plan is budget control. Chief executives

and managers want to be able to identify whether or not a corporation is going to make a profit.

Essentially, the goal of budgeting is to provide a blueprint to how the organization will operate if

such policies, processes, strategies, got successfully, are followed.

The aim of a budget is to provide decision-making process with a financial basis i.e. the desired

way to proceed, is what businesses are preparing or not for. Spending should be closely regulated

when carefully operating an organization. Before the promotional expenditure has been

sufficiently spent, the assumption that businesses can expend money on marketing is likely to be

" is possibly to be no". The aim of financial planning is to enable actual operational efficiency,

i.e. the organization that achieves our targets, to be calculated against the planned financial

performance. The discrepancy among planned amounts and real expenditure is "variance" in the

inverse formula.

For regional administrators, who often work on a small budget, financial planning is incredibly

important. In a limited company, being marginally off on expense estimates or income may have

a devastating effect as well. It could be worth recruiting the in outside or auditor or a

professional analyst who has experience in business finance to ensure that budgetary control is

carried out effectively. This staff would aid with developing accounting, monitoring spending

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and generating analyses that aid large companies in taking measured and informed key business

decisions.

3.2. What might be the main benefits of forming a limited company and listing it on a stock

exchange?

There is no particular amount of money spent and it is always possible to enter low amounts of

business and leisure time is always viable and one of the most significant facets of it the main

advantage of creating a limited company is that there is no real quantity of cash involving

(Gitman, Juchau and Flanagan, 2015). It also allows certain kinds of businesses, in comparison

to this simplicity of collecting money. While the key benefit of owning a general company listed

on the stock market will be because by using various types of machinery available on the market,

more resources can be applied to the venture, and therefore the company would gain greater

sustainability and efficiency in the potential. Below, certain key advantages are addressed in

such a manner:

There is no particular amount of money spent because it is still possible to target a low amounts

in business and land ownership is still viable among the most significant facets of that The main

advantage of creating a limited partnership is that there is no real amount of money involving. It

also allows certain kinds of firms, in comparison to this simplicity of collecting funds. Whereas

the key benefit of owning a general company publicly traded companies will be that by using

various types of machinery available on the market, more resources can be applied to the

venture, and therefore the company would gain greater sustainability and efficiency in the

potential. Below, certain key advantages are addressed in such a manner:

Many corporations have reached a stage where it is necessary to infuse increased cash to support

potential growth/expansion planning. However, making it official is a way to solve these

limitations. By selling on a stock market and enhancing its brand, the company improves the

customer base. By selling, liquidity is increased, giving owners the ability to consider the

valuation of their property. It enables unpaid earnings members to swap, exchange risks, and

benefit from organizational revenue growth.

decisions.

3.2. What might be the main benefits of forming a limited company and listing it on a stock

exchange?

There is no particular amount of money spent and it is always possible to enter low amounts of

business and leisure time is always viable and one of the most significant facets of it the main

advantage of creating a limited company is that there is no real quantity of cash involving

(Gitman, Juchau and Flanagan, 2015). It also allows certain kinds of businesses, in comparison

to this simplicity of collecting money. While the key benefit of owning a general company listed

on the stock market will be because by using various types of machinery available on the market,

more resources can be applied to the venture, and therefore the company would gain greater

sustainability and efficiency in the potential. Below, certain key advantages are addressed in

such a manner:

There is no particular amount of money spent because it is still possible to target a low amounts

in business and land ownership is still viable among the most significant facets of that The main

advantage of creating a limited partnership is that there is no real amount of money involving. It

also allows certain kinds of firms, in comparison to this simplicity of collecting funds. Whereas

the key benefit of owning a general company publicly traded companies will be that by using

various types of machinery available on the market, more resources can be applied to the

venture, and therefore the company would gain greater sustainability and efficiency in the

potential. Below, certain key advantages are addressed in such a manner:

Many corporations have reached a stage where it is necessary to infuse increased cash to support

potential growth/expansion planning. However, making it official is a way to solve these

limitations. By selling on a stock market and enhancing its brand, the company improves the

customer base. By selling, liquidity is increased, giving owners the ability to consider the

valuation of their property. It enables unpaid earnings members to swap, exchange risks, and

benefit from organizational revenue growth.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Listing brings accountability and utility to the corporate activities of the organization.

Going public increases the visibility and reputation of the union within businesses and the buying

public as it follows various levels of enforcement and ensures transparency during operations.

A democratic company's board and executive team are responsible to the owners. In specific, the

members of the Board will need to enable characteristics that apply to the Exchange/shareholders

as set out in the Listing Agreement or in the relevant Instructions to be rapidly complied with.

Going public raises visibility and improves the public image of the organization, thus continuing

to grow workers' cost - efficiency. This can also contribute to new personnel selection and enable

securities sales like ESOPs, etc.

The lack of abundance of labor assets is one of the main challenges to growth strategy. By

introducing different shareholdings to customers, many firms listed on the stock market are able

to increase more appealing capital more rapidly. To expand their companies to pay for

operational costs, they will use the funds they collect by bond issuance.

Stocks frequently defer the taxation of capital profits. There is no requirement to file a claim on

profits after spending capital if the portfolio value rises. Until selling the stock, the retailer also

wants to monitor the stock updates. In addition, if the lender makes a loss on the sale of the

securities, the loss will be used by taxation, to fund any other investment rise.

Going public increases the visibility and reputation of the union within businesses and the buying

public as it follows various levels of enforcement and ensures transparency during operations.

A democratic company's board and executive team are responsible to the owners. In specific, the

members of the Board will need to enable characteristics that apply to the Exchange/shareholders

as set out in the Listing Agreement or in the relevant Instructions to be rapidly complied with.

Going public raises visibility and improves the public image of the organization, thus continuing

to grow workers' cost - efficiency. This can also contribute to new personnel selection and enable

securities sales like ESOPs, etc.

The lack of abundance of labor assets is one of the main challenges to growth strategy. By

introducing different shareholdings to customers, many firms listed on the stock market are able

to increase more appealing capital more rapidly. To expand their companies to pay for

operational costs, they will use the funds they collect by bond issuance.

Stocks frequently defer the taxation of capital profits. There is no requirement to file a claim on

profits after spending capital if the portfolio value rises. Until selling the stock, the retailer also

wants to monitor the stock updates. In addition, if the lender makes a loss on the sale of the

securities, the loss will be used by taxation, to fund any other investment rise.

REFERENCES

Adhikary, B. and Kutsuna, K., 2016. Small Business Finance in Bangladesh:

Can'Crowdfunding'Be an Alternative?. Review of Integrative Business and Economics

Research, 4, pp.1-21.

Finance, B., 2015. Business Finance.

Babajide, A.A., Olokoyo, F.O. and Taiwo, J.N., 2016. Evaluation of effects of banking

consolidation on small business finance in Nigeria. In Proceedings of the 23rd

International Business Information Management Association Conference (pp. 12522-

12540).

Jordà, Ò., Schularick, M. and Taylor, A.M., 2016. The great mortgaging: housing finance, crises

and business cycles. Economic policy, 31(85), pp.107-152.

Chung, C.Y., Liu, C., Wang, K. and Zykaj, B.B., 2015. Institutional monitoring: Evidence from

the F‐score. Journal of Business Finance & Accounting, 42(7-8), pp.885-914.

Kapinos, P., Gurley-Calvez, T. and Kapinos, K., 2016. (Un) expected housing price changes:

Identifying the drivers of small business finance. Journal of Economics and Business, 84,

pp.79-94.

Burns, P. and Dewhurst, J. eds., 2016. Small business and entrepreneurship. Macmillan

International Higher Education.

Haldane, A., 2016. Finance Version 2.0. Speech. Bank of England, 7.

Fraser, S., Bhaumik, S.K. and Wright, M., 2015. What do we know about entrepreneurial finance

and its relationship with growth?. International Small Business Journal, 33(1), pp.70-88.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Adhikary, B. and Kutsuna, K., 2016. Small Business Finance in Bangladesh:

Can'Crowdfunding'Be an Alternative?. Review of Integrative Business and Economics

Research, 4, pp.1-21.

Finance, B., 2015. Business Finance.

Babajide, A.A., Olokoyo, F.O. and Taiwo, J.N., 2016. Evaluation of effects of banking

consolidation on small business finance in Nigeria. In Proceedings of the 23rd

International Business Information Management Association Conference (pp. 12522-

12540).

Jordà, Ò., Schularick, M. and Taylor, A.M., 2016. The great mortgaging: housing finance, crises

and business cycles. Economic policy, 31(85), pp.107-152.

Chung, C.Y., Liu, C., Wang, K. and Zykaj, B.B., 2015. Institutional monitoring: Evidence from

the F‐score. Journal of Business Finance & Accounting, 42(7-8), pp.885-914.

Kapinos, P., Gurley-Calvez, T. and Kapinos, K., 2016. (Un) expected housing price changes:

Identifying the drivers of small business finance. Journal of Economics and Business, 84,

pp.79-94.

Burns, P. and Dewhurst, J. eds., 2016. Small business and entrepreneurship. Macmillan

International Higher Education.

Haldane, A., 2016. Finance Version 2.0. Speech. Bank of England, 7.

Fraser, S., Bhaumik, S.K. and Wright, M., 2015. What do we know about entrepreneurial finance

and its relationship with growth?. International Small Business Journal, 33(1), pp.70-88.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.