Identifying the Impact of Accounting Ethics on Banking Sector Finance

VerifiedAdded on 2023/01/11

|14

|4398

|20

Report

AI Summary

This report investigates the influence of accounting ethics on financial management and the auditing systems within the banking industry, with a specific focus on the Commonwealth Bank of Australia. The research explores the importance of ethical considerations in accounting, particularly concerning financial resource management and internal audit procedures. The study employs a descriptive research design, utilizing questionnaires to gather data and analyze the impact of accounting ethics on various aspects of the bank's operations, including financial planning, auditing, and overall productivity. The literature review highlights the significance of ethical behavior in accounting, the responsibilities of accountants, and the consequences of unethical practices, such as manipulation of financial records and conflicts of interest. The report also examines the role of accounting ethics in maintaining the integrity of financial statements and its impact on the bank's reputation and stakeholder relationships. Overall, the research aims to identify the relationship between accounting ethics and banking productivity, emphasizing the need for adherence to ethical standards to ensure transparency, accuracy, and reliability in financial reporting and auditing practices.

Research

(Project 3)

(Project 3)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Title page.......................................................................................................................................................................... 3

ABSTRACT.....................................................................................................................................................................4

Aim- Identifying the impact of accounting ethics on banking sector financial planning and internal audit framework:

a research project on the Commonwealth Bank Australia............................................................................................5

Objectives-....................................................................................................................................................................5

Literature review..............................................................................................................................................................5

Research Design and Methodology................................................................................................................................10

Data analysis..................................................................................................................................................................12

Ethical Consideration...................................................................................................................................................13

REFERENCES...............................................................................................................................................................14

Title page.......................................................................................................................................................................... 3

ABSTRACT.....................................................................................................................................................................4

Aim- Identifying the impact of accounting ethics on banking sector financial planning and internal audit framework:

a research project on the Commonwealth Bank Australia............................................................................................5

Objectives-....................................................................................................................................................................5

Literature review..............................................................................................................................................................5

Research Design and Methodology................................................................................................................................10

Data analysis..................................................................................................................................................................12

Ethical Consideration...................................................................................................................................................13

REFERENCES...............................................................................................................................................................14

Title page

Title: “To identify the influence of accounting ethics on financail management and auditing system

of Banking sector: A case study on Common Wealth Bank Asutralia”.

Title: “To identify the influence of accounting ethics on financail management and auditing system

of Banking sector: A case study on Common Wealth Bank Asutralia”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ABSTRACT

The respective research summarise the impact of accounting ethic rules and regulation over financial

management and the auditing procedure within banking industry. It is very important to consider each and

every ethical concept of accounting while managing financial resources and auditing the internal reports of

any bank. This particular work is focused solely around the legal concern of an organisation's auditing

framework. The Code of Ethics is important in banking industries for the accounting firm. The primary

objective behind this work is the recognition of the impact of business ethics mostly on financial markets and

the auditing method of banks. To complete the research descriptive research design has been selected. By

implementing this method researcher can enhance their project understanding, and outlines the final findings

equally. Method of research used is questionnaire which support in collecting data from a group of

candidates.

Research background

Accounting ethics is regarded as an important subject since, as accountants, is the main people

handling the persons and institutions' financial records. This control often provides the possibility and

consequences of knowledge misuse or number manipulating to improve client expectations or to implement

earnings management. Ethics, too, is completely important during an audit. Without satisfying the auditing

and financial ethics standards, an audit should be stopped immediately. Accountants have responsibilities

towards clients, investors, workers, customers, the state, the accounting community and the general public.

Accordingly, ethical behaviour is a necessary and anticipated trait; as a result, an auditor is responsible for

the implications of his moral decisions not just for his own life but also for the lives of company.

Australia's Commonwealth Bank (shortened CBA or CommBank) is an Independent investment bank

with operations throughout New Zealand, Europe, the U.S., as well as the U.K. It offers a variety of financial

services like private, corporate and investment finance, wealth management, pensions, retirement, savings,

and investment banking. As of August 2015 the Commonwealth Bank became Australia's biggest listed firm

on the Australian Stock Exchange. The CBA was created in 1911 under the act of Commonwealth Bank,

which was passed by the Andrew Fisher Labour Government, which advocated bank nationalization, with

effect from December 22, 1911. Good corporate governance means that CBA uphold the highest level of

ethics and behave with dignity throughout their commercial operations. The Code lays out assumptions for

how Commonwealth Bank is behaving with customer and other stakeholder, solving problems and making

decisions for the future improvement.

The problem statement of respective research is that in case if ethical standard of accounting are not

followed while managing and controlling financial resources and information overall functioning of

The respective research summarise the impact of accounting ethic rules and regulation over financial

management and the auditing procedure within banking industry. It is very important to consider each and

every ethical concept of accounting while managing financial resources and auditing the internal reports of

any bank. This particular work is focused solely around the legal concern of an organisation's auditing

framework. The Code of Ethics is important in banking industries for the accounting firm. The primary

objective behind this work is the recognition of the impact of business ethics mostly on financial markets and

the auditing method of banks. To complete the research descriptive research design has been selected. By

implementing this method researcher can enhance their project understanding, and outlines the final findings

equally. Method of research used is questionnaire which support in collecting data from a group of

candidates.

Research background

Accounting ethics is regarded as an important subject since, as accountants, is the main people

handling the persons and institutions' financial records. This control often provides the possibility and

consequences of knowledge misuse or number manipulating to improve client expectations or to implement

earnings management. Ethics, too, is completely important during an audit. Without satisfying the auditing

and financial ethics standards, an audit should be stopped immediately. Accountants have responsibilities

towards clients, investors, workers, customers, the state, the accounting community and the general public.

Accordingly, ethical behaviour is a necessary and anticipated trait; as a result, an auditor is responsible for

the implications of his moral decisions not just for his own life but also for the lives of company.

Australia's Commonwealth Bank (shortened CBA or CommBank) is an Independent investment bank

with operations throughout New Zealand, Europe, the U.S., as well as the U.K. It offers a variety of financial

services like private, corporate and investment finance, wealth management, pensions, retirement, savings,

and investment banking. As of August 2015 the Commonwealth Bank became Australia's biggest listed firm

on the Australian Stock Exchange. The CBA was created in 1911 under the act of Commonwealth Bank,

which was passed by the Andrew Fisher Labour Government, which advocated bank nationalization, with

effect from December 22, 1911. Good corporate governance means that CBA uphold the highest level of

ethics and behave with dignity throughout their commercial operations. The Code lays out assumptions for

how Commonwealth Bank is behaving with customer and other stakeholder, solving problems and making

decisions for the future improvement.

The problem statement of respective research is that in case if ethical standard of accounting are not

followed while managing and controlling financial resources and information overall functioning of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company or bank can be impacted in adverse manner. Moreover, if accounting ethics are not implemented

within auditing procedure than information audition can be manipulated and other problem financial

challenges may be faced by bank.

Research Questions and Research Objectives

Aim- Identifying the impact of accounting ethics on banking sector financial planning and internal

audit framework: a research project on the Commonwealth Bank Australia.

Objectives-

To identify the concept of accounting ethics.

To analyse the importance of accounting ethics in banking sector.

To understand the impact of accounting ethics on financial management and auditing system of

banking sector.

To determine the impact of accounting ethics on financial functioning of Common Wealth Bank

Australia.

To analyse the role of accounting ethics in management of auditing system of Banking industry.

To identify the relationship between accounting ethics and banking productivity.

Questions-

Explain the concept of accounting ethics?

What is the importance of accounting ethics in banking industry?

What are the impact of accounting ethics on financial management and auditing system of banking

sector?

Assess the influence of accounting ethics on financial functioning of Common Wealth Bank of

Australia?

Describe the role of accounting ethics in the management of banking auditing system?

What is the relationship between accounting ethics with banking productivity?

Literature review

Accounting ethical is, in Grama's view, (2015) a especially important subject as accountants, the key

individuals managing financial reports of entities and organizations. These authorities may have the

opportunity and data misuse situations or mathematical engineering to optimize market views or to enforce

revenue management. Nevertheless, throughout an audit, ethics is absolutely important. The inquiry will be

automatically halted without meeting the conditions for auditing and monitoring standards. Another

misunderstanding about accounting methods is the fact that several prospective practitioners believe that

adhering to the code of ethics of most respectable accounting organisations is nearly impossible. The

within auditing procedure than information audition can be manipulated and other problem financial

challenges may be faced by bank.

Research Questions and Research Objectives

Aim- Identifying the impact of accounting ethics on banking sector financial planning and internal

audit framework: a research project on the Commonwealth Bank Australia.

Objectives-

To identify the concept of accounting ethics.

To analyse the importance of accounting ethics in banking sector.

To understand the impact of accounting ethics on financial management and auditing system of

banking sector.

To determine the impact of accounting ethics on financial functioning of Common Wealth Bank

Australia.

To analyse the role of accounting ethics in management of auditing system of Banking industry.

To identify the relationship between accounting ethics and banking productivity.

Questions-

Explain the concept of accounting ethics?

What is the importance of accounting ethics in banking industry?

What are the impact of accounting ethics on financial management and auditing system of banking

sector?

Assess the influence of accounting ethics on financial functioning of Common Wealth Bank of

Australia?

Describe the role of accounting ethics in the management of banking auditing system?

What is the relationship between accounting ethics with banking productivity?

Literature review

Accounting ethical is, in Grama's view, (2015) a especially important subject as accountants, the key

individuals managing financial reports of entities and organizations. These authorities may have the

opportunity and data misuse situations or mathematical engineering to optimize market views or to enforce

revenue management. Nevertheless, throughout an audit, ethics is absolutely important. The inquiry will be

automatically halted without meeting the conditions for auditing and monitoring standards. Another

misunderstanding about accounting methods is the fact that several prospective practitioners believe that

adhering to the code of ethics of most respectable accounting organisations is nearly impossible. The

principle of preventing theft from receiving integrated management inspections is the safest way of deterring

theft. Conflict of interest embraces the ethical code including the legal body but is concerned with making

things Australia of the Collective Wealth Bank much easier since these times are contrary.

In the Duska, Duska and Kury, (2018), accounting ethics involves financial declarations that were

important to customers in order to enable their path of financial strategic thinking. Business community

requires audit practitioners to conform with ethical standards to ensure timely, accurate, transparent

information is provided to all end-users. An ethics concern by an organization’s accountants is to minimize

the level of supervision and control by management, and allows auditors with incentives to engage in

deceptive behaviour and conceal evidence. It offers opportunities for major hacking of computers, leading to

criminal crimes such as avoiding tax and corruption. Unethical practices of accounting professionals

influence a firm's reputation and legitimacy with its stakeholders. Insecurity due to unethical actions damages

the credibility of the bank making it impossible for the Australian Common Wealth Bank. The corporate

report's basic goals are to convey economic statistics and details on the accounting entity's tool and results to

those with access to those details. It is also reported that financial statements help users evaluate ancient and

modern. The organization's success and its potential to optimize shareholders' capital, in turn, assesses the

company's capacity to produce profit and an unbiased evaluation of the income produced over period by the

firm's financial statement perspectives into these tools Krkač et al, (2011).

All the claims on these properties, including the company's duty to pass capital to other organizations

and stakeholders and the impact of sales, incidents and conditions that affect the properties and claims on

such services (Loeb, 2015). The author also mentioned that the essential methodological characteristics (i.e.,

importance and faithful representation) are most relevant and evaluate the meaning of knowledge on

financial statements. The improvement of qualitative attributes (that is, ability to interpret, comparability,

verifiability, and timeliness) will increase the effectiveness of decisions when the quantitative traits are

defined. Various ways of calculation to determine the consistency of the financial statements is beneficial for

the auditors. The most commonly used measure of the content of financial reporting in previous studies

involve accrual systems, value importance models, research focus on specific components in the financial

statement and techniques of quantifying the attributes of the financial reports.

According to Ogbonna (2010), when auditor speak about stuff they believe, that not actually contravene

the laws of the association or infringe the laws of the country or lead to overt criminality or

misconduct. They problem issues such as conflicts of interest, dealings with insiders, undermining

trustworthiness, Objectivity, transparency, anonymity, revealing of official secrets, and degradation of

official financial benefit records and other related activities according to fundamental principles and ethical

norms. Technical ethics gives account, as per Jenfa (2000) and Nwagboso (2008). Such advantages: it allows

the auditors to assess his performs wealth the accountant must retain a professional attitude if they wants to

theft. Conflict of interest embraces the ethical code including the legal body but is concerned with making

things Australia of the Collective Wealth Bank much easier since these times are contrary.

In the Duska, Duska and Kury, (2018), accounting ethics involves financial declarations that were

important to customers in order to enable their path of financial strategic thinking. Business community

requires audit practitioners to conform with ethical standards to ensure timely, accurate, transparent

information is provided to all end-users. An ethics concern by an organization’s accountants is to minimize

the level of supervision and control by management, and allows auditors with incentives to engage in

deceptive behaviour and conceal evidence. It offers opportunities for major hacking of computers, leading to

criminal crimes such as avoiding tax and corruption. Unethical practices of accounting professionals

influence a firm's reputation and legitimacy with its stakeholders. Insecurity due to unethical actions damages

the credibility of the bank making it impossible for the Australian Common Wealth Bank. The corporate

report's basic goals are to convey economic statistics and details on the accounting entity's tool and results to

those with access to those details. It is also reported that financial statements help users evaluate ancient and

modern. The organization's success and its potential to optimize shareholders' capital, in turn, assesses the

company's capacity to produce profit and an unbiased evaluation of the income produced over period by the

firm's financial statement perspectives into these tools Krkač et al, (2011).

All the claims on these properties, including the company's duty to pass capital to other organizations

and stakeholders and the impact of sales, incidents and conditions that affect the properties and claims on

such services (Loeb, 2015). The author also mentioned that the essential methodological characteristics (i.e.,

importance and faithful representation) are most relevant and evaluate the meaning of knowledge on

financial statements. The improvement of qualitative attributes (that is, ability to interpret, comparability,

verifiability, and timeliness) will increase the effectiveness of decisions when the quantitative traits are

defined. Various ways of calculation to determine the consistency of the financial statements is beneficial for

the auditors. The most commonly used measure of the content of financial reporting in previous studies

involve accrual systems, value importance models, research focus on specific components in the financial

statement and techniques of quantifying the attributes of the financial reports.

According to Ogbonna (2010), when auditor speak about stuff they believe, that not actually contravene

the laws of the association or infringe the laws of the country or lead to overt criminality or

misconduct. They problem issues such as conflicts of interest, dealings with insiders, undermining

trustworthiness, Objectivity, transparency, anonymity, revealing of official secrets, and degradation of

official financial benefit records and other related activities according to fundamental principles and ethical

norms. Technical ethics gives account, as per Jenfa (2000) and Nwagboso (2008). Such advantages: it allows

the auditors to assess his performs wealth the accountant must retain a professional attitude if they wants to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

achieve success; it gives future clients, a reason for feeling comfortable the specialist just wishes to represent

them well and places operation above cash reward; It ensures the consumer that competency requirements

are in place, determination and dignity remain the aim of regulatory authorities to meet their obligations,

responsibility to ensure that accounting professionals have the skills and expertise, the capabilities that staff,

customers and the public interest require of them are covered and the professional integrity is improved in

the whole accounting context. Throughout Brenkert (2004) perspective, the accuracy of financial reports

indicates a criterion for correctly representing Common Wealth Bank Australia financial reports, their

economic situation and activities, measured over time. Credibility and esteem in the billing system relies on

so much more to the system than perhaps human behaviour and events or complicated "procedures." Banking

industries and the professional associations of trained public accountants, and investment managers and

researchers have shaped the accuracy and faith of varying levels in financial statement systems. Throughout

the financial statement cycle, credibility and trust cannot merely be a matter of philosophical or institutional

ethics. The firms are related to the financial reports determined by their accountants to be having been

accurate and correct in addition to making good strategic decisions. Inaccurate financial statements caused by

the deceptive or fraudulent actions of a company's auditors may lead to a loss of revenue from an exposed

accounting scam, or worse, bankruptcy.

As per the view of Gitman, Juchau and Flanagan, (2015), ethical is a set of common principles or values

which the corporation uses to guide the activities of the CBA itself and its employees in both its internally

and externally corporate practices as well as in relation with the outside world. The principles of finance are

a code of conduct, which are implicit in financial conduct. Unlike the ethical behaviour of a bank, the

auditor's accounting compliance practices are a set of activities. As a member of a practice, accountants have

a responsibility not just to their employees and clients as well as to the society as a whole to follow the

highest moral values. That audit committee must adopt ethical guidelines and ensure its participants

understand their responsibilities as professional accountants. Accounting standards can also be perceived as

making a positive impact on reducing fraud, corruption, theft and diversion of funds by staff driven events.

As a result, no standard accepted audit quality concept may be used as a 'standard,' which can be measured

against real results. The impression of an auditor is difficult to assess if the financial results are "real and

equal." Various viewpoints may be taken as the audit proof required endorsing the claim to the point and

quality of it. As from the article struggled, the goal of supporting from financial management system and

holding confident in the audit phase is within the interim report as a core element corporate transparency and

accountability and successful business service financial markets business.

In the opinion of Lawton, Rayner and Lasthuizen, (2013), professional principles of accounting are

outlined in a written ethics code. Such guidelines provide instructions, but legal or behavioural practice

maintains a personal option. Companies will encounter legal dilemmas almost every day, many of which are

them well and places operation above cash reward; It ensures the consumer that competency requirements

are in place, determination and dignity remain the aim of regulatory authorities to meet their obligations,

responsibility to ensure that accounting professionals have the skills and expertise, the capabilities that staff,

customers and the public interest require of them are covered and the professional integrity is improved in

the whole accounting context. Throughout Brenkert (2004) perspective, the accuracy of financial reports

indicates a criterion for correctly representing Common Wealth Bank Australia financial reports, their

economic situation and activities, measured over time. Credibility and esteem in the billing system relies on

so much more to the system than perhaps human behaviour and events or complicated "procedures." Banking

industries and the professional associations of trained public accountants, and investment managers and

researchers have shaped the accuracy and faith of varying levels in financial statement systems. Throughout

the financial statement cycle, credibility and trust cannot merely be a matter of philosophical or institutional

ethics. The firms are related to the financial reports determined by their accountants to be having been

accurate and correct in addition to making good strategic decisions. Inaccurate financial statements caused by

the deceptive or fraudulent actions of a company's auditors may lead to a loss of revenue from an exposed

accounting scam, or worse, bankruptcy.

As per the view of Gitman, Juchau and Flanagan, (2015), ethical is a set of common principles or values

which the corporation uses to guide the activities of the CBA itself and its employees in both its internally

and externally corporate practices as well as in relation with the outside world. The principles of finance are

a code of conduct, which are implicit in financial conduct. Unlike the ethical behaviour of a bank, the

auditor's accounting compliance practices are a set of activities. As a member of a practice, accountants have

a responsibility not just to their employees and clients as well as to the society as a whole to follow the

highest moral values. That audit committee must adopt ethical guidelines and ensure its participants

understand their responsibilities as professional accountants. Accounting standards can also be perceived as

making a positive impact on reducing fraud, corruption, theft and diversion of funds by staff driven events.

As a result, no standard accepted audit quality concept may be used as a 'standard,' which can be measured

against real results. The impression of an auditor is difficult to assess if the financial results are "real and

equal." Various viewpoints may be taken as the audit proof required endorsing the claim to the point and

quality of it. As from the article struggled, the goal of supporting from financial management system and

holding confident in the audit phase is within the interim report as a core element corporate transparency and

accountability and successful business service financial markets business.

In the opinion of Lawton, Rayner and Lasthuizen, (2013), professional principles of accounting are

outlined in a written ethics code. Such guidelines provide instructions, but legal or behavioural practice

maintains a personal option. Companies will encounter legal dilemmas almost every day, many of which are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

challenging and impossible to overcome, as those working in the corporate environment. This is why the law

implementation is as clear as the quality of the laws themselves guaranteeing that the procedure is legitimate

and comparisons arising out of everything. The principles of the law here is focused on the importance of a

particular reporting or audit program and its aims thus the significance of an auditor testing the accounting

processes are developed regularly categories of their financial status portrayal. That is what makes

everything possible. Obviously, audit companies have the same socially responsible responsibilities as

practitioners With regard to compliance with accounting standards which help to make audits beneficial to

end-users. Companies, however, have added mutual duty to provide independent auditors with assistance and

advice in carrying out their duties and collaborating with the accountants. Even amongst the way individuals

of audit committees are the availability of basic skills and support, the creation of a system that values

auditor credibility and the subservience of increasing profits to the repair work of audit report. Unable to

maintain ethical activity in the industry is a result of managers, personnel auditors and intermediate

stakeholders.

Based on the review strategy established by the director of the internal auditor and approved by the

executive committee, Ramos (2010) believes that the auditing system must be allowed to perform its duties

on its own account in all areas of operations of the bank. It must be able to debate its findings and

assessments internally across straight reporting columns. The Manager of CBA should display strong

leadership and have the skills necessary to serve the banking obligation to uphold the credibility and

objectivity of the banking services. A stable corporate management system with an effective and productive

corporate auditing process is a component of good financial regulation. Banking managers ought to focus on

the efficacy of the bank's internal control position, the execution of procedures and regulations, and the

introduction of appropriate and timely corrective steps in response to internal audit deficiency. The audit role

offers vital assurance for the board of directors and the senior managers and bank managers of the business

of the quality of the internal management system. The role of this enables the bank to be more likely to fail

and lose its reputation. The common assumption that the law in auditing has played an essential role in

maintaining continuity in independent auditors' services by defining responsibilities, spelling out minimum

standards, proposing reporting guidelines, and recognizing, amongst other items, technical references.

As per the view of Chen, Kelly and Salterio, (2012) the continued improvement of audits is anticipated

to contribute to a stronger and more comprehensive regulatory structure, perhaps because regulator

regulation has been more transparent or because accountant roles are more specifically defined about what

should be anticipated in financial products. The correlation between audit oversight and regulation and the

level of output and income, but no substantive partnership of the Australia Common Wealth Bank, had also

been examined. Similarly no statistically significant results were found for groups of nations when making a

detailed review of the internal audit criteria. The possibility of reporting is influenced by the independence of

implementation is as clear as the quality of the laws themselves guaranteeing that the procedure is legitimate

and comparisons arising out of everything. The principles of the law here is focused on the importance of a

particular reporting or audit program and its aims thus the significance of an auditor testing the accounting

processes are developed regularly categories of their financial status portrayal. That is what makes

everything possible. Obviously, audit companies have the same socially responsible responsibilities as

practitioners With regard to compliance with accounting standards which help to make audits beneficial to

end-users. Companies, however, have added mutual duty to provide independent auditors with assistance and

advice in carrying out their duties and collaborating with the accountants. Even amongst the way individuals

of audit committees are the availability of basic skills and support, the creation of a system that values

auditor credibility and the subservience of increasing profits to the repair work of audit report. Unable to

maintain ethical activity in the industry is a result of managers, personnel auditors and intermediate

stakeholders.

Based on the review strategy established by the director of the internal auditor and approved by the

executive committee, Ramos (2010) believes that the auditing system must be allowed to perform its duties

on its own account in all areas of operations of the bank. It must be able to debate its findings and

assessments internally across straight reporting columns. The Manager of CBA should display strong

leadership and have the skills necessary to serve the banking obligation to uphold the credibility and

objectivity of the banking services. A stable corporate management system with an effective and productive

corporate auditing process is a component of good financial regulation. Banking managers ought to focus on

the efficacy of the bank's internal control position, the execution of procedures and regulations, and the

introduction of appropriate and timely corrective steps in response to internal audit deficiency. The audit role

offers vital assurance for the board of directors and the senior managers and bank managers of the business

of the quality of the internal management system. The role of this enables the bank to be more likely to fail

and lose its reputation. The common assumption that the law in auditing has played an essential role in

maintaining continuity in independent auditors' services by defining responsibilities, spelling out minimum

standards, proposing reporting guidelines, and recognizing, amongst other items, technical references.

As per the view of Chen, Kelly and Salterio, (2012) the continued improvement of audits is anticipated

to contribute to a stronger and more comprehensive regulatory structure, perhaps because regulator

regulation has been more transparent or because accountant roles are more specifically defined about what

should be anticipated in financial products. The correlation between audit oversight and regulation and the

level of output and income, but no substantive partnership of the Australia Common Wealth Bank, had also

been examined. Similarly no statistically significant results were found for groups of nations when making a

detailed review of the internal audit criteria. The possibility of reporting is influenced by the independence of

the auditor. Supreme freedom ensures that a content error or irregularity needs to be announced openly.

Freedom concerns include selection and firing processes, limited or forbidden practices (e.g., corporate

relationships) and required behaviours (e.g., auditors' communication). The explanation that technology

transfer happens is due to the needs that both sides have for technology transfer. Although there are major

gaps in the technical standard between the developed and the technically backward, and depending on banks

resources to improve own standard of technology is often challenging, those who are small and irrelevant

must work with advanced technology organizations. Hence, the industry should be considered as an industry

where unfair competition persists. The substance and the production process have their own specific features;

insofar that each of them has separate protections.

Freedom concerns include selection and firing processes, limited or forbidden practices (e.g., corporate

relationships) and required behaviours (e.g., auditors' communication). The explanation that technology

transfer happens is due to the needs that both sides have for technology transfer. Although there are major

gaps in the technical standard between the developed and the technically backward, and depending on banks

resources to improve own standard of technology is often challenging, those who are small and irrelevant

must work with advanced technology organizations. Hence, the industry should be considered as an industry

where unfair competition persists. The substance and the production process have their own specific features;

insofar that each of them has separate protections.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Research Design and Methodology

The research methodology is the basic procedures or techniques for defining, collecting, interpreting and

evaluating subject knowledge. The analysis segment helps readers to assess the general quality and durability

of a report in a scientific report objectively.

Research Design: Description research is described as a technique of studies that defines the population

features or the concept under consideration. The emphasis of this approach is mostly on the "why" than on

the "what" of the topic of study. Descriptive research could be used in several ways so for a variety of

reasons. However, the questionnaire objectives and survey specification are very essential before having into

some kind of questionnaire. However, despite following such steps, there really is no way of knowing

whether the results of the study will be approached. This seeks to draw real conclusions about the

interviewees using descriptive method. This may be appropriate to extract respondent’s habits,

characteristics. The participant can therefore acknowledge their role or opinions on the phenomena in

question.

Research Approach: Descriptive analysis is a systematic testing approach aimed at gathering

quantifiable knowledge for longitudinal sample study. This is a common market research method that

enables the demographic section to be gathered and represented. Quantitative evaluation is the analytical

compilation of data based solely on quantities and values it implies that it is linked with or described in terms

of quantity. Quantitative analytical findings are obtained using techniques of mathematical and statistical

analysis.

Research data: In order to collect the data regarding the particular research primary data collection

method is used which help to gather the direct information from the respondent selected for the research. A

primary source offers additional or life experiences proof of an event, object, person or art work. Historical

and legal records, eyewitness reports, trial findings, scientific evidence, fine arts pieces, audio and video

interviews, statements, and works of art are reliable sources.

Research sample: In context of particular research, a sample is a collection of people, items or property

taken for measure by a greater population. The survey will be reflective of the community to insure that the

outcomes of the test study can be applied to the whole community. The total sample size for this research is

30 respondents to who question are asked to gather information regarding the topic.

The research methodology is the basic procedures or techniques for defining, collecting, interpreting and

evaluating subject knowledge. The analysis segment helps readers to assess the general quality and durability

of a report in a scientific report objectively.

Research Design: Description research is described as a technique of studies that defines the population

features or the concept under consideration. The emphasis of this approach is mostly on the "why" than on

the "what" of the topic of study. Descriptive research could be used in several ways so for a variety of

reasons. However, the questionnaire objectives and survey specification are very essential before having into

some kind of questionnaire. However, despite following such steps, there really is no way of knowing

whether the results of the study will be approached. This seeks to draw real conclusions about the

interviewees using descriptive method. This may be appropriate to extract respondent’s habits,

characteristics. The participant can therefore acknowledge their role or opinions on the phenomena in

question.

Research Approach: Descriptive analysis is a systematic testing approach aimed at gathering

quantifiable knowledge for longitudinal sample study. This is a common market research method that

enables the demographic section to be gathered and represented. Quantitative evaluation is the analytical

compilation of data based solely on quantities and values it implies that it is linked with or described in terms

of quantity. Quantitative analytical findings are obtained using techniques of mathematical and statistical

analysis.

Research data: In order to collect the data regarding the particular research primary data collection

method is used which help to gather the direct information from the respondent selected for the research. A

primary source offers additional or life experiences proof of an event, object, person or art work. Historical

and legal records, eyewitness reports, trial findings, scientific evidence, fine arts pieces, audio and video

interviews, statements, and works of art are reliable sources.

Research sample: In context of particular research, a sample is a collection of people, items or property

taken for measure by a greater population. The survey will be reflective of the community to insure that the

outcomes of the test study can be applied to the whole community. The total sample size for this research is

30 respondents to who question are asked to gather information regarding the topic.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Questionnaire

1. Did you know about concept of accounting ethics?

Yes

No

2. What is the importance of accounting ethics in banking industry?

Better banking operation

Transparency in services

Expansion of branches

What are the impact of accounting ethics on financial management and auditing system of banking

sector?

Managing of financial resources

Accuracy in accounting reports

Reliable annual statements

What is the influence of accounting ethics on financial functioning of Common Wealth Bank of

Australia?

Quality in banking services

More satisfied customer base

Highest level of return on investment and shares.

Is accounting ethics in the management of banking auditing system?

Yes

No

What is the relationship between accounting ethics with banking productivity?

Better control over banking records.

Maintaining the customer accounts.

1. Did you know about concept of accounting ethics?

Yes

No

2. What is the importance of accounting ethics in banking industry?

Better banking operation

Transparency in services

Expansion of branches

What are the impact of accounting ethics on financial management and auditing system of banking

sector?

Managing of financial resources

Accuracy in accounting reports

Reliable annual statements

What is the influence of accounting ethics on financial functioning of Common Wealth Bank of

Australia?

Quality in banking services

More satisfied customer base

Highest level of return on investment and shares.

Is accounting ethics in the management of banking auditing system?

Yes

No

What is the relationship between accounting ethics with banking productivity?

Better control over banking records.

Maintaining the customer accounts.

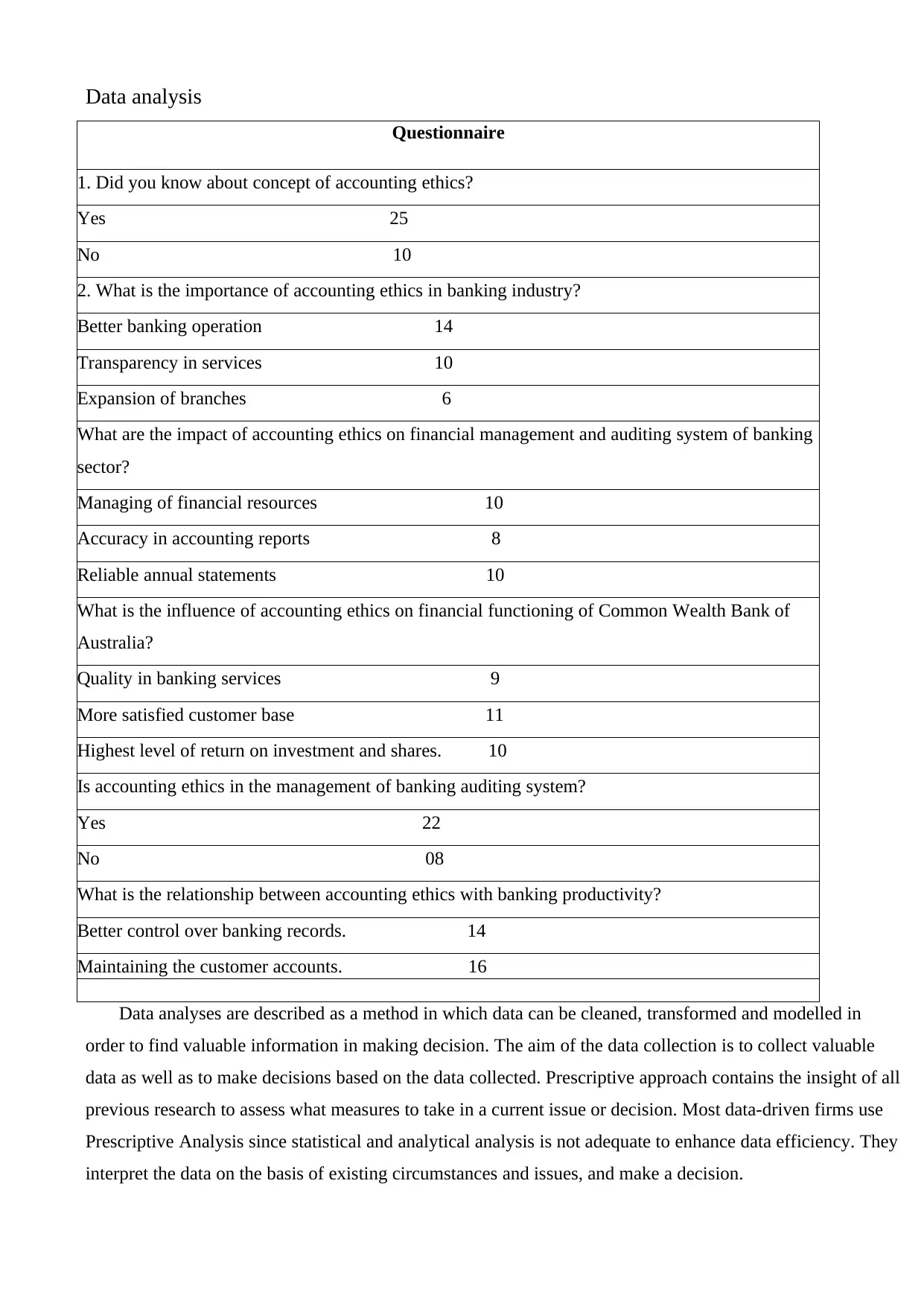

Data analysis

Questionnaire

1. Did you know about concept of accounting ethics?

Yes 25

No 10

2. What is the importance of accounting ethics in banking industry?

Better banking operation 14

Transparency in services 10

Expansion of branches 6

What are the impact of accounting ethics on financial management and auditing system of banking

sector?

Managing of financial resources 10

Accuracy in accounting reports 8

Reliable annual statements 10

What is the influence of accounting ethics on financial functioning of Common Wealth Bank of

Australia?

Quality in banking services 9

More satisfied customer base 11

Highest level of return on investment and shares. 10

Is accounting ethics in the management of banking auditing system?

Yes 22

No 08

What is the relationship between accounting ethics with banking productivity?

Better control over banking records. 14

Maintaining the customer accounts. 16

Data analyses are described as a method in which data can be cleaned, transformed and modelled in

order to find valuable information in making decision. The aim of the data collection is to collect valuable

data as well as to make decisions based on the data collected. Prescriptive approach contains the insight of all

previous research to assess what measures to take in a current issue or decision. Most data-driven firms use

Prescriptive Analysis since statistical and analytical analysis is not adequate to enhance data efficiency. They

interpret the data on the basis of existing circumstances and issues, and make a decision.

Questionnaire

1. Did you know about concept of accounting ethics?

Yes 25

No 10

2. What is the importance of accounting ethics in banking industry?

Better banking operation 14

Transparency in services 10

Expansion of branches 6

What are the impact of accounting ethics on financial management and auditing system of banking

sector?

Managing of financial resources 10

Accuracy in accounting reports 8

Reliable annual statements 10

What is the influence of accounting ethics on financial functioning of Common Wealth Bank of

Australia?

Quality in banking services 9

More satisfied customer base 11

Highest level of return on investment and shares. 10

Is accounting ethics in the management of banking auditing system?

Yes 22

No 08

What is the relationship between accounting ethics with banking productivity?

Better control over banking records. 14

Maintaining the customer accounts. 16

Data analyses are described as a method in which data can be cleaned, transformed and modelled in

order to find valuable information in making decision. The aim of the data collection is to collect valuable

data as well as to make decisions based on the data collected. Prescriptive approach contains the insight of all

previous research to assess what measures to take in a current issue or decision. Most data-driven firms use

Prescriptive Analysis since statistical and analytical analysis is not adequate to enhance data efficiency. They

interpret the data on the basis of existing circumstances and issues, and make a decision.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.