Asset Impairment: A Study on MFRS136 and Denko Industrial Corporation Berhad

VerifiedAdded on 2023/06/10

|16

|3488

|485

AI Summary

This report discusses the standard MFRS136 related to asset impairment and how Denko Industrial Corporation Berhad, a Malaysian investment holding company, complies with the disclosure requirements. It also covers recognition and measurement of impairment losses. The report includes a description of the company, MFRS136 items of disclosure, disclosure compliance and format of the company, and recognition and measurement. The report concludes with a summary and references.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

RUNNING HEAD: ACCOUNTING

asset impairment

asset impairment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting 1

Contents

Introduction...........................................................................................................................................2

Description of the Company..................................................................................................................2

MFRS136 items of disclosure...............................................................................................................3

Disclosure compliance and format of the company...............................................................................5

Recognition and measurement...............................................................................................................9

Summary.............................................................................................................................................12

Conclusion...........................................................................................................................................13

References...........................................................................................................................................14

Contents

Introduction...........................................................................................................................................2

Description of the Company..................................................................................................................2

MFRS136 items of disclosure...............................................................................................................3

Disclosure compliance and format of the company...............................................................................5

Recognition and measurement...............................................................................................................9

Summary.............................................................................................................................................12

Conclusion...........................................................................................................................................13

References...........................................................................................................................................14

Accounting 2

Introduction

This report contains detail information about the standard MFRS136 which is related to

impairment of assets. It also shows the manner in which the impairment is been disclosed and

presented in the annual report of the selected company that operates in Malaysia. The

company is Denko Industrial which is listed on Bursa Malaysia and is an investment holding

company. The later part of the report discusses the requirements of disclosure and the format

followed by Denko for reporting its impairment exercise. In addition to that, the recognition

and measurement of MFRS136 is also discussed. All the findings of the report are then

presented in nutshell under the head summary, followed by the conclusion. The discussion

made in the report is been summarized in the last part of the report and is presented in a

concise manner.

Description of the Company

Denko Industrial Corporation Berhad is an investment holding company which operates in

the country named Malaysia. It was incorporated in 1989 under the name Ecodynamic (M)

Sdn Bhd. Later on it change the name to Denko Industrial and in 1990, it was transformed

into a public listed company and get listed on Second Board of Kuala Lumpur Stock

Exchange- Bursa Malaysia in 1991, the year when the history of expansion began for Denko

(Denko. 2018).

The segments of the company include snack food, plastic and moulding and others. Snack

food segment is involved in the trading of food stuff and consumer goods. The section

operates as a wholesaler and trader provide consumable food items across the country.

Another segment named as plastic and moulding is engaged in manufacturing or designing of

plastic moulded elements and products. These components are later sold in both domestic and

international markets (Reuters. 2018). The other divisions of the company deals with the

Introduction

This report contains detail information about the standard MFRS136 which is related to

impairment of assets. It also shows the manner in which the impairment is been disclosed and

presented in the annual report of the selected company that operates in Malaysia. The

company is Denko Industrial which is listed on Bursa Malaysia and is an investment holding

company. The later part of the report discusses the requirements of disclosure and the format

followed by Denko for reporting its impairment exercise. In addition to that, the recognition

and measurement of MFRS136 is also discussed. All the findings of the report are then

presented in nutshell under the head summary, followed by the conclusion. The discussion

made in the report is been summarized in the last part of the report and is presented in a

concise manner.

Description of the Company

Denko Industrial Corporation Berhad is an investment holding company which operates in

the country named Malaysia. It was incorporated in 1989 under the name Ecodynamic (M)

Sdn Bhd. Later on it change the name to Denko Industrial and in 1990, it was transformed

into a public listed company and get listed on Second Board of Kuala Lumpur Stock

Exchange- Bursa Malaysia in 1991, the year when the history of expansion began for Denko

(Denko. 2018).

The segments of the company include snack food, plastic and moulding and others. Snack

food segment is involved in the trading of food stuff and consumer goods. The section

operates as a wholesaler and trader provide consumable food items across the country.

Another segment named as plastic and moulding is engaged in manufacturing or designing of

plastic moulded elements and products. These components are later sold in both domestic and

international markets (Reuters. 2018). The other divisions of the company deals with the

Accounting 3

investment holding. Denko also provides management services to its customer and operates

in countries other than Malaysia, popularly known as United States of America, Asia –

Pacific and Europe. There are many subsidiaries of the company that are engaged in

providing food stuff and plastic parts. Winsheng Plastic Industry Sdn. Bhd., PT. Winsheng

Plastic and Tooling Industry and Lean Teik Soon Sdn. Bhd are the subsidiaries involved in

the manufacturing of plastic components and tooling fabrication along with the selling of

consumable goods (Bloomberg. 2018).

The key products of the firm are vacuum foams, packing materials, lease property, plastic

raw materials and pipes, garments made up of polyester, cotton and many other fabrics. It

also produces various types of chemicals and semi-finished products. Talking about the

financial highlights, the revenue of Denko has increased to RM 102 million in 2017 as

compare to the previous year. However, despite of an upsurge in sales, the company has

reported a net loss amounted to RM 11,289 thousands in year 2017 as compare to the profit

made prior to that (Bloomberg. 2018). This has eventually resulted in the deduction of

shareholders’ funds from RM 56 million to RM 45 million. In addition to that, the EPS of the

company was negative due to the loss and the amount of total assets has also reduced in 2017.

Overall, it can be said that Denko needs to improve its performance in order to enjoy growth

and success. As the company is publically listed on Bursa Malaysia, it is traded with a ticker

of DICM.KL (Reuters. 2018).

MFRS136 items of disclosure

Malaysian Accounting Standards Board (MASB) developed and introduced a framework

which consists of certain standards which are required to be followed by every Malaysian

company listed on Bursa Malaysia. The framework is named as the Malaysian Financial

Reporting Standards (MFRS). Adopting such framework is considered as a significant

milestone in the capital market as it enables the companies to fully comply their financial

investment holding. Denko also provides management services to its customer and operates

in countries other than Malaysia, popularly known as United States of America, Asia –

Pacific and Europe. There are many subsidiaries of the company that are engaged in

providing food stuff and plastic parts. Winsheng Plastic Industry Sdn. Bhd., PT. Winsheng

Plastic and Tooling Industry and Lean Teik Soon Sdn. Bhd are the subsidiaries involved in

the manufacturing of plastic components and tooling fabrication along with the selling of

consumable goods (Bloomberg. 2018).

The key products of the firm are vacuum foams, packing materials, lease property, plastic

raw materials and pipes, garments made up of polyester, cotton and many other fabrics. It

also produces various types of chemicals and semi-finished products. Talking about the

financial highlights, the revenue of Denko has increased to RM 102 million in 2017 as

compare to the previous year. However, despite of an upsurge in sales, the company has

reported a net loss amounted to RM 11,289 thousands in year 2017 as compare to the profit

made prior to that (Bloomberg. 2018). This has eventually resulted in the deduction of

shareholders’ funds from RM 56 million to RM 45 million. In addition to that, the EPS of the

company was negative due to the loss and the amount of total assets has also reduced in 2017.

Overall, it can be said that Denko needs to improve its performance in order to enjoy growth

and success. As the company is publically listed on Bursa Malaysia, it is traded with a ticker

of DICM.KL (Reuters. 2018).

MFRS136 items of disclosure

Malaysian Accounting Standards Board (MASB) developed and introduced a framework

which consists of certain standards which are required to be followed by every Malaysian

company listed on Bursa Malaysia. The framework is named as the Malaysian Financial

Reporting Standards (MFRS). Adopting such framework is considered as a significant

milestone in the capital market as it enables the companies to fully comply their financial

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting 4

statements with the International Financial Reporting Standards (Lhaopadchan, 2010). From

the pool of guidelines, there is one standard named as MFRS136 which basically deals with

asset impairment. According to this standard, an asset is been impaired by the company when

its carrying amount is irrecoverable from its continuous use or sale. The entity is required to

report the impaired asset, if any. It has to compare the recoverable amount of that asset with

its carrying amount in order to determine the value of impairment (Reinstein and Lander,

2004).

The MFRS 136 states the recognition, disclosure and measurement for the impairment of

assets covered by MFRS 116 and 117 along with the PPE. In addition to that, intangible

assets covered in the standard MFRS 138 and goodwill (Devalle and Rizzato, 2017). The

items of disclosure requirements under MFRS136 that are represented in the annual report of

Denko Industrial Corporation are:

1. The amount of impairment losses is required to be disclosed which is documented in

the income statement of the company in its annual report.

2. Reversal of impairment loss is also recognized in the income statement of during the

period.

3. Another requirement is to recognize the nature of asset along with the amount of

impairment loss.

4. Disclosing the circumstances and situations that resulted in reversal and recognition

of loss on impairment.

5. Disclosure of the basis on which the net selling price, discount rate used and value in

use is determined (Ernst and Young. 2010).

The above items are the disclosure requirements of the Malaysian standards MFRS 136 and

all of them are been properly presented in the annual report of Denko for the year 2017. The

statements with the International Financial Reporting Standards (Lhaopadchan, 2010). From

the pool of guidelines, there is one standard named as MFRS136 which basically deals with

asset impairment. According to this standard, an asset is been impaired by the company when

its carrying amount is irrecoverable from its continuous use or sale. The entity is required to

report the impaired asset, if any. It has to compare the recoverable amount of that asset with

its carrying amount in order to determine the value of impairment (Reinstein and Lander,

2004).

The MFRS 136 states the recognition, disclosure and measurement for the impairment of

assets covered by MFRS 116 and 117 along with the PPE. In addition to that, intangible

assets covered in the standard MFRS 138 and goodwill (Devalle and Rizzato, 2017). The

items of disclosure requirements under MFRS136 that are represented in the annual report of

Denko Industrial Corporation are:

1. The amount of impairment losses is required to be disclosed which is documented in

the income statement of the company in its annual report.

2. Reversal of impairment loss is also recognized in the income statement of during the

period.

3. Another requirement is to recognize the nature of asset along with the amount of

impairment loss.

4. Disclosing the circumstances and situations that resulted in reversal and recognition

of loss on impairment.

5. Disclosure of the basis on which the net selling price, discount rate used and value in

use is determined (Ernst and Young. 2010).

The above items are the disclosure requirements of the Malaysian standards MFRS 136 and

all of them are been properly presented in the annual report of Denko for the year 2017. The

Accounting 5

company has reported impairment loss on trade and other receivables, property, plant and

equipment and on investment in subsidiaries (Abuaddous, Hanefah and Laili, 2014). In

addition to this the amount is been recognized in the statement of comprehensive income and

also if in future the value reduces will result in reversal of the previous loss shown in the

statement. Also while reporting the same, Denko has disclose about the nature of asset,

whether financial or non-financial. In investment in subsidiaries, the loss amount is equal to

RM 22,110,594 in 2017 and in 2016 it was RM 15,468,660. In PP&E, the loss amounted to

RM 4,168,596 and the reversal of loss on trade receivables was RM 176,418 was reported in

the financial year 2017. The total impairment of assets was amounted to RM 4.2 million in

2017 (Denko. 2017).

Disclosure compliance and format of the company

The accounting policies of Denko are in proper compliance with all the requirements and

provisions of international Financial Reporting Standards (IFRS), Malaysian Financial

Reporting Standards (MFRS) and the Companies Act 2016 applicable in Malaysia. The

company has applied various Malaysian standards for reporting their financial information.

Out of them, MFRS 136 is been applied for impairment of assets and MFRS 107 is applied

for disclosure initiative. Provided below is the sample of how Denko has disclosed the

impairment of assets.

company has reported impairment loss on trade and other receivables, property, plant and

equipment and on investment in subsidiaries (Abuaddous, Hanefah and Laili, 2014). In

addition to this the amount is been recognized in the statement of comprehensive income and

also if in future the value reduces will result in reversal of the previous loss shown in the

statement. Also while reporting the same, Denko has disclose about the nature of asset,

whether financial or non-financial. In investment in subsidiaries, the loss amount is equal to

RM 22,110,594 in 2017 and in 2016 it was RM 15,468,660. In PP&E, the loss amounted to

RM 4,168,596 and the reversal of loss on trade receivables was RM 176,418 was reported in

the financial year 2017. The total impairment of assets was amounted to RM 4.2 million in

2017 (Denko. 2017).

Disclosure compliance and format of the company

The accounting policies of Denko are in proper compliance with all the requirements and

provisions of international Financial Reporting Standards (IFRS), Malaysian Financial

Reporting Standards (MFRS) and the Companies Act 2016 applicable in Malaysia. The

company has applied various Malaysian standards for reporting their financial information.

Out of them, MFRS 136 is been applied for impairment of assets and MFRS 107 is applied

for disclosure initiative. Provided below is the sample of how Denko has disclosed the

impairment of assets.

Accounting 6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 7

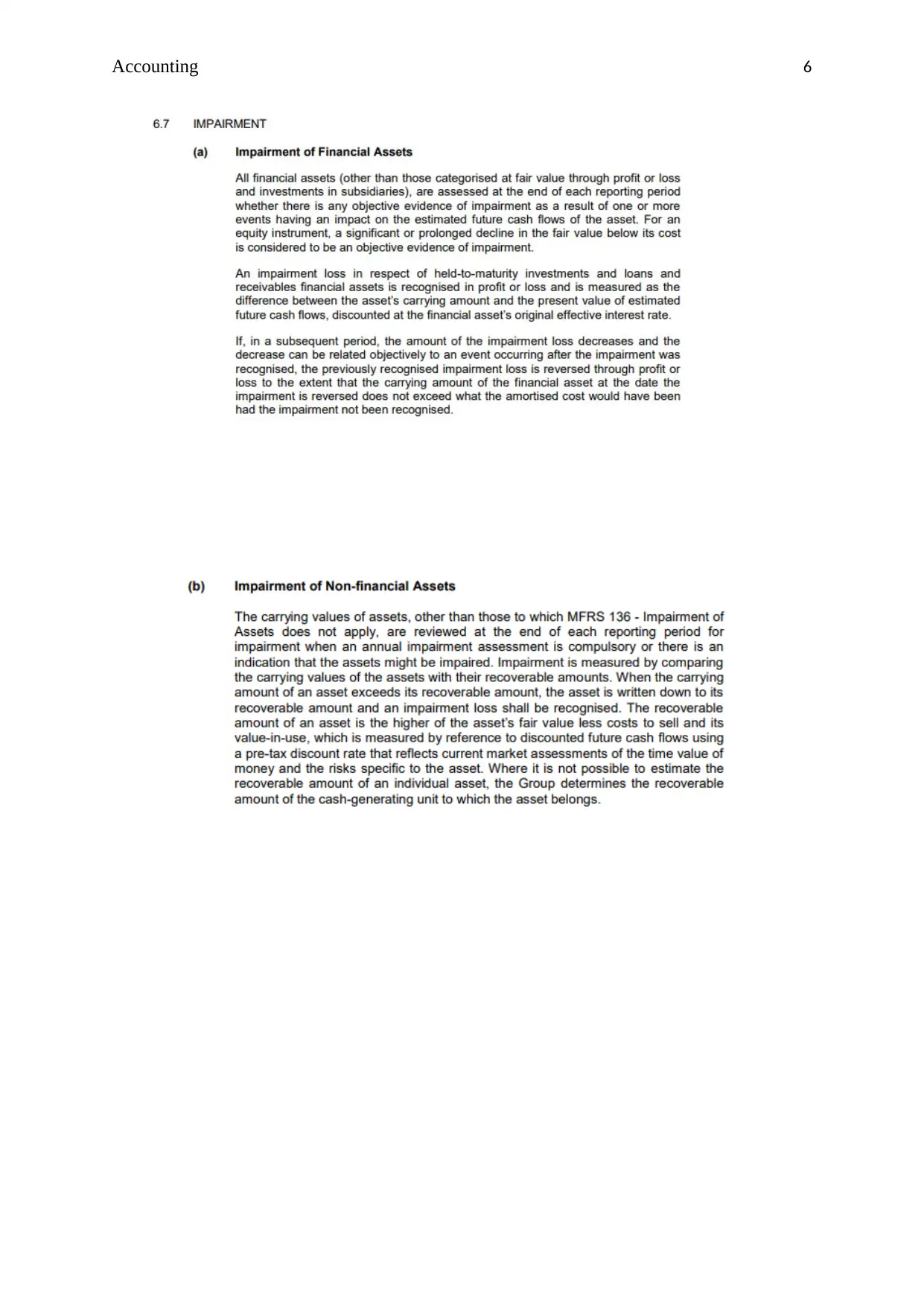

Above are the abstracts from the annual report of Denko Company and the sample showing

the format in which, the firm has represented or disclosed the information about the asset

impairment. Denko Industrial discloses all the information about impairment under the

section notes to financial statements. It contains the reasons identified for impairment, assets

that got impaired and their evaluation. According to the disclosure compliance, company is

Above are the abstracts from the annual report of Denko Company and the sample showing

the format in which, the firm has represented or disclosed the information about the asset

impairment. Denko Industrial discloses all the information about impairment under the

section notes to financial statements. It contains the reasons identified for impairment, assets

that got impaired and their evaluation. According to the disclosure compliance, company is

Accounting 8

required to assess the factors that indicates the chances of impairment and should report the

same in its annual reports. Following indications are there as prescribed by the standard,

which requires impairment.

External sources

1. The decrease in the market value of the asset during a specific period is more than the

estimated reduction due to normal usage.

2. When market capitalization of an asset is more than its carrying amount.

3. The significant changes affecting the legal, technological, economic environment and

market, to which a particular asset is associated.

Internal sources

1. Availability of evidence related to the damage or obsolescence of a physical asset.

2. The presence of the evidence that the asset’s economic performance will get worse

than its current performance in the near future.

3. When the recoverable amount is higher than value in use and fair value net of selling

expenses.

4. Changes in the operational plans or strategy of the organization such as discontinuing

an operation or disposing an asset.

All the above indications do call for asset impairment and are required to be disclosed by the

companies in their annual report. Denko Industrial discloses the assets impaired by it during

the financial year 2017. It also shows the reasons for doing in the same in the section named

as impairment. Apart from the indications, the loss on impairment recognized by Denko is

also explained in the above abstracts of the company. The above listed five items of

disclosure are been clearly disclosed in the annual report of Denko Industrial for the year

required to assess the factors that indicates the chances of impairment and should report the

same in its annual reports. Following indications are there as prescribed by the standard,

which requires impairment.

External sources

1. The decrease in the market value of the asset during a specific period is more than the

estimated reduction due to normal usage.

2. When market capitalization of an asset is more than its carrying amount.

3. The significant changes affecting the legal, technological, economic environment and

market, to which a particular asset is associated.

Internal sources

1. Availability of evidence related to the damage or obsolescence of a physical asset.

2. The presence of the evidence that the asset’s economic performance will get worse

than its current performance in the near future.

3. When the recoverable amount is higher than value in use and fair value net of selling

expenses.

4. Changes in the operational plans or strategy of the organization such as discontinuing

an operation or disposing an asset.

All the above indications do call for asset impairment and are required to be disclosed by the

companies in their annual report. Denko Industrial discloses the assets impaired by it during

the financial year 2017. It also shows the reasons for doing in the same in the section named

as impairment. Apart from the indications, the loss on impairment recognized by Denko is

also explained in the above abstracts of the company. The above listed five items of

disclosure are been clearly disclosed in the annual report of Denko Industrial for the year

Accounting 9

2017. Apart from the items, the reasons for recognizing the impairment losses is also clearly

represented in the report of the company.

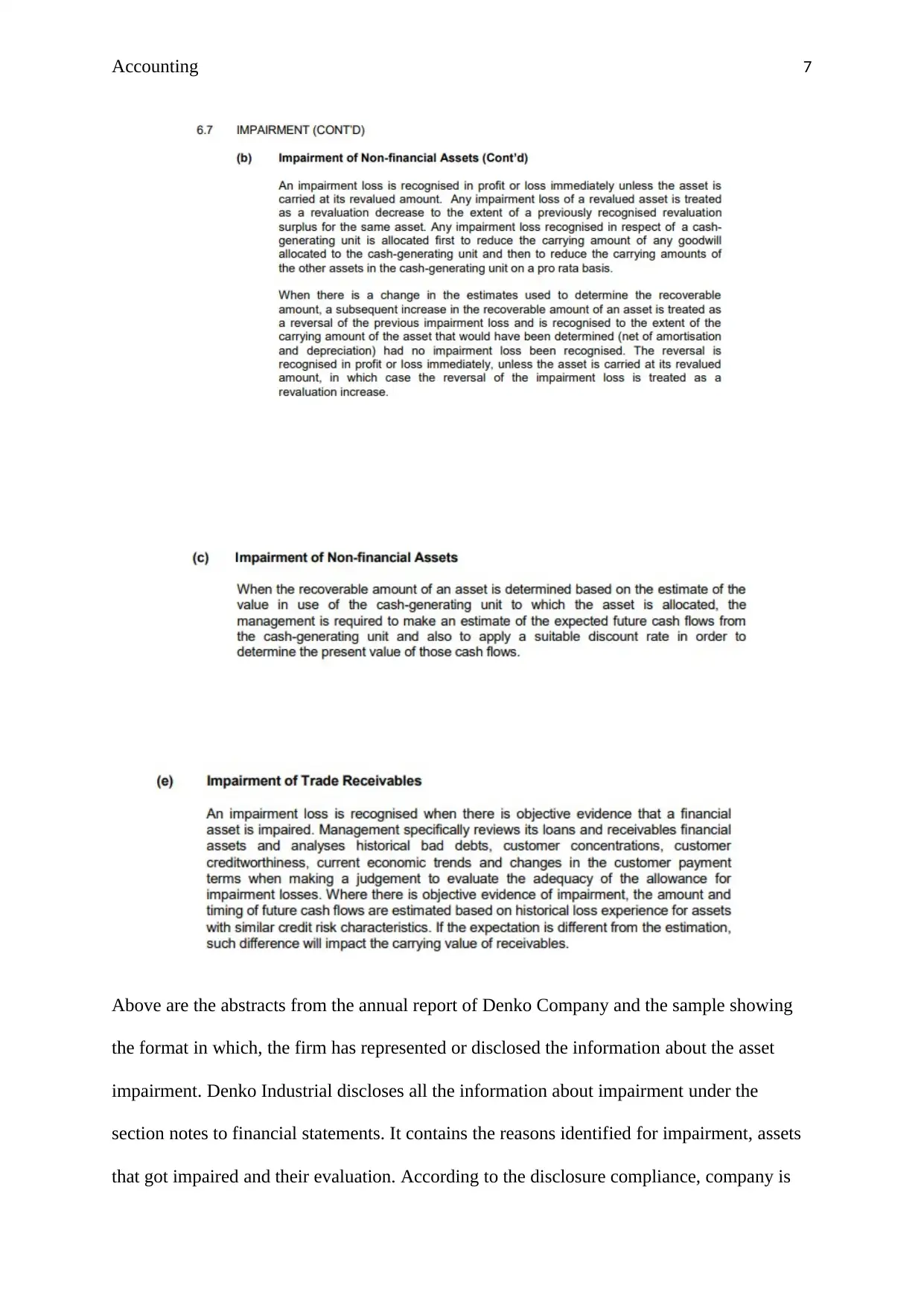

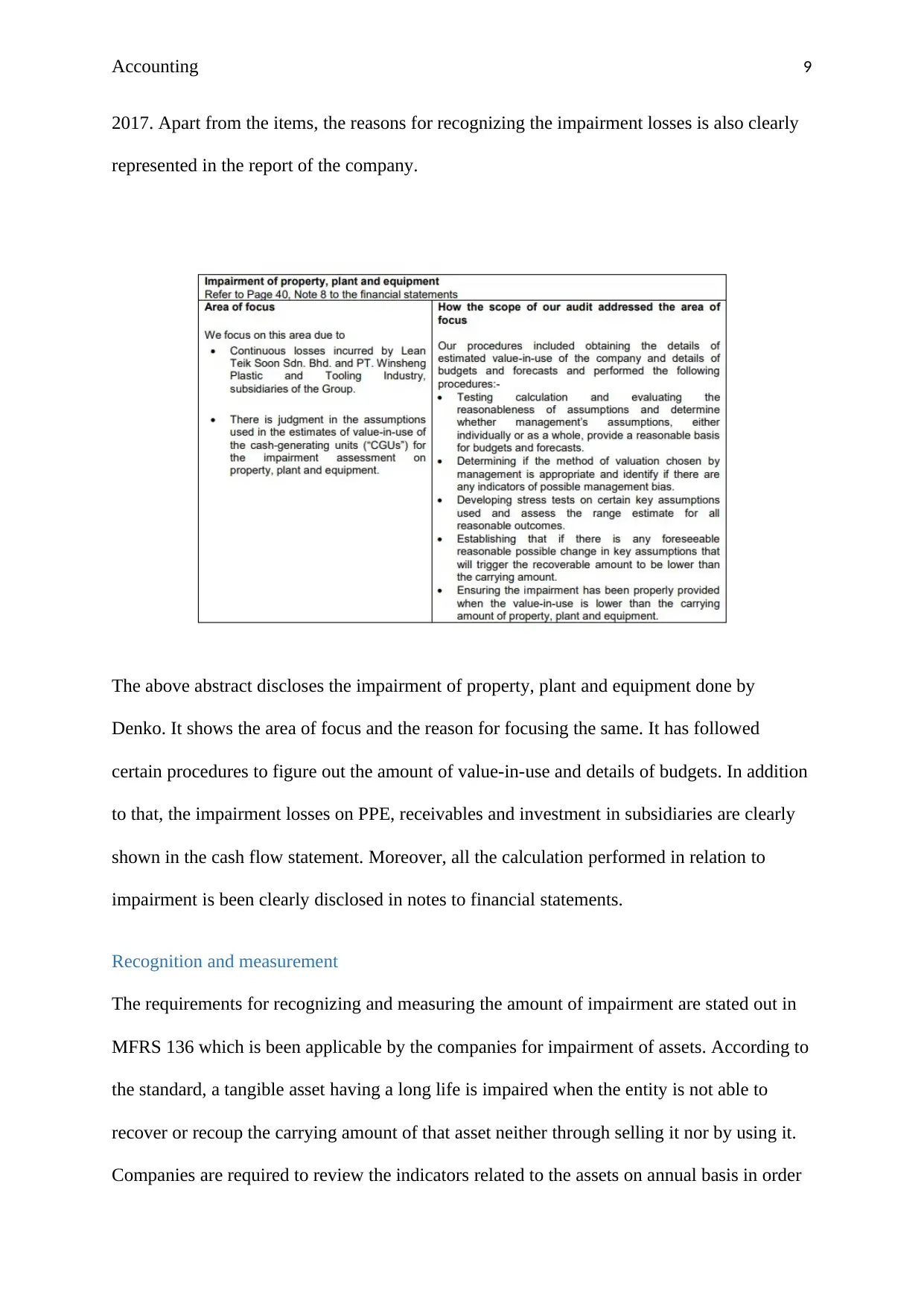

The above abstract discloses the impairment of property, plant and equipment done by

Denko. It shows the area of focus and the reason for focusing the same. It has followed

certain procedures to figure out the amount of value-in-use and details of budgets. In addition

to that, the impairment losses on PPE, receivables and investment in subsidiaries are clearly

shown in the cash flow statement. Moreover, all the calculation performed in relation to

impairment is been clearly disclosed in notes to financial statements.

Recognition and measurement

The requirements for recognizing and measuring the amount of impairment are stated out in

MFRS 136 which is been applicable by the companies for impairment of assets. According to

the standard, a tangible asset having a long life is impaired when the entity is not able to

recover or recoup the carrying amount of that asset neither through selling it nor by using it.

Companies are required to review the indicators related to the assets on annual basis in order

2017. Apart from the items, the reasons for recognizing the impairment losses is also clearly

represented in the report of the company.

The above abstract discloses the impairment of property, plant and equipment done by

Denko. It shows the area of focus and the reason for focusing the same. It has followed

certain procedures to figure out the amount of value-in-use and details of budgets. In addition

to that, the impairment losses on PPE, receivables and investment in subsidiaries are clearly

shown in the cash flow statement. Moreover, all the calculation performed in relation to

impairment is been clearly disclosed in notes to financial statements.

Recognition and measurement

The requirements for recognizing and measuring the amount of impairment are stated out in

MFRS 136 which is been applicable by the companies for impairment of assets. According to

the standard, a tangible asset having a long life is impaired when the entity is not able to

recover or recoup the carrying amount of that asset neither through selling it nor by using it.

Companies are required to review the indicators related to the assets on annual basis in order

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accounting 10

to know about the probability or chances of impairment (Rahman and Mohamed, 2018). This

is how the entities recognize the assets which are required to be impaired. The above

discussed internal and external sources of indications are been kept in mind during the

process of review. In case if any of the indications is present, then the company is required to

figure out the estimate of recoverable amount. Also the assessment of each asset is required at

the end of each reporting period. In case of intangible assets, their ability to generate future

economic benefits is highly subject to the uncertainty. In that case, the standard allow the

entities to conduct an impairment test on an annual basis (Che Azmi and English, 2016)

Apart from the above discussed internal and external sources, the indication by which

company can recognize impairment for the investment in subsidiary is by recognizing the

amount of dividend received from that investment with the following evidence:

Investments’ carrying amount in separate financial statements is more than the

carrying amount in the consolidated financial statements of net assets; or

The amount of dividend is more than the total comprehensive income of the

subsidiary company, in the period when the dividend is declared (IFRS. 2017).

Talking about impairment loss of individual asset, it is recognized in the income statement of

the company only when the recoverable value is less than the carrying amount. The entity

must immediately recognize the loss in income statement. However, previously if the asset is

evaluated and there is a credit balance of the same in the revaluation account, then the

amount of loss on impairment must be taken to revaluation amount (Lobo, et. al., 2017).

After recognition, the same is been calculated by subtracting the recoverable amount of the

asset from its carrying amount. The recoverable amount of the asset is higher of the

following:

Value-in-use.

to know about the probability or chances of impairment (Rahman and Mohamed, 2018). This

is how the entities recognize the assets which are required to be impaired. The above

discussed internal and external sources of indications are been kept in mind during the

process of review. In case if any of the indications is present, then the company is required to

figure out the estimate of recoverable amount. Also the assessment of each asset is required at

the end of each reporting period. In case of intangible assets, their ability to generate future

economic benefits is highly subject to the uncertainty. In that case, the standard allow the

entities to conduct an impairment test on an annual basis (Che Azmi and English, 2016)

Apart from the above discussed internal and external sources, the indication by which

company can recognize impairment for the investment in subsidiary is by recognizing the

amount of dividend received from that investment with the following evidence:

Investments’ carrying amount in separate financial statements is more than the

carrying amount in the consolidated financial statements of net assets; or

The amount of dividend is more than the total comprehensive income of the

subsidiary company, in the period when the dividend is declared (IFRS. 2017).

Talking about impairment loss of individual asset, it is recognized in the income statement of

the company only when the recoverable value is less than the carrying amount. The entity

must immediately recognize the loss in income statement. However, previously if the asset is

evaluated and there is a credit balance of the same in the revaluation account, then the

amount of loss on impairment must be taken to revaluation amount (Lobo, et. al., 2017).

After recognition, the same is been calculated by subtracting the recoverable amount of the

asset from its carrying amount. The recoverable amount of the asset is higher of the

following:

Value-in-use.

Accounting 11

Net selling price

Value in use is calculated by aggregating the present values of the cash flows that are

estimated by making a continuous use of asset or from its disposal. NSP is equal to the

amount at which the particular asset is been sold in the market. The asset’s value carried out

by the balance sheet of the firm is known as the carrying amount. However, the value of

impaired loss can be reversed in the cases where the recoverable amount is more than the

carrying amount (Schwarzbichler, Steiner and Turnheim, 2018). The reversal amount must be

recognized in the statement of financial performance of the company. However, if the loss on

impairment is already charged to revaluation account, then such reversal income should also

be recognized in the revaluation reserves by writing back the loss which was earlier

recognized. In addition to that, after the reversal, the amount of depreciation and amortization

should be readjusted for the future periods (Shaari, Cao and Donnelly, 2017). According to

the standard, the guidelines for measurement and recognition of impairment loss of individual

asset is same for cash generating units also. It prescribes the manner in which the carrying

amount of CGUs can be identified and the loss of impairment can be allocated between the

assets of unit.

Above discussion shows the standards of recognizing and measuring the impairment value of

the assets. It shows how companies calculate the amount of impairment losses, recoverable

figure and carrying amount of an asset which is to be impaired. Denko Industrial has

considered all the requirements of measurement and recognition of impairment as prescribed

by MFRS 136 in its annual report.

Summary

From the above discussion, following are the key points which explains the whole

information discussed above in a nutshell.

Net selling price

Value in use is calculated by aggregating the present values of the cash flows that are

estimated by making a continuous use of asset or from its disposal. NSP is equal to the

amount at which the particular asset is been sold in the market. The asset’s value carried out

by the balance sheet of the firm is known as the carrying amount. However, the value of

impaired loss can be reversed in the cases where the recoverable amount is more than the

carrying amount (Schwarzbichler, Steiner and Turnheim, 2018). The reversal amount must be

recognized in the statement of financial performance of the company. However, if the loss on

impairment is already charged to revaluation account, then such reversal income should also

be recognized in the revaluation reserves by writing back the loss which was earlier

recognized. In addition to that, after the reversal, the amount of depreciation and amortization

should be readjusted for the future periods (Shaari, Cao and Donnelly, 2017). According to

the standard, the guidelines for measurement and recognition of impairment loss of individual

asset is same for cash generating units also. It prescribes the manner in which the carrying

amount of CGUs can be identified and the loss of impairment can be allocated between the

assets of unit.

Above discussion shows the standards of recognizing and measuring the impairment value of

the assets. It shows how companies calculate the amount of impairment losses, recoverable

figure and carrying amount of an asset which is to be impaired. Denko Industrial has

considered all the requirements of measurement and recognition of impairment as prescribed

by MFRS 136 in its annual report.

Summary

From the above discussion, following are the key points which explains the whole

information discussed above in a nutshell.

Accounting 12

Malaysian companies operating their business in Malaysia are required to comply

with all the requirements of the Malaysian standard named as MFRS 136 –

Impairment of assets for the purpose of getting their assets impaired.

All the items of disclosure, measurement and recognition must be properly presented

in the annual report of the companies.

Denko Industrial Corporation is the one which has applied MFRS 136 in its financial

reporting and has followed all the requirements of the standard.

The company operates through various segments which are related to making and

moulding plastic materials, offering snack food and one segment operates as an

investment holding company.

The key products of the company are packing materials, vacuum foams, garments

made up of cotton and other fibres.

Denko properly presents all the items of disclosure in its recent annual report. It

shows all the information in its notes to financial statements.

The amount of impairment losses and the circumstances that causes impairment are

disclosed in the annual report.

Recognition and measurement requirements of MFRS 136 are discussed above.

The loss on impairment is measured only when the assets’ recoverable amount is less

than its carrying amount.

Higher of value in use and net selling price determines the recoverable amount of the

asset.

Carrying value means the figure at which the asset is been carried out in the balance

sheet of the company.

Overall, it is very important for Denko to comply with all the requirements of MFRS

136.

Malaysian companies operating their business in Malaysia are required to comply

with all the requirements of the Malaysian standard named as MFRS 136 –

Impairment of assets for the purpose of getting their assets impaired.

All the items of disclosure, measurement and recognition must be properly presented

in the annual report of the companies.

Denko Industrial Corporation is the one which has applied MFRS 136 in its financial

reporting and has followed all the requirements of the standard.

The company operates through various segments which are related to making and

moulding plastic materials, offering snack food and one segment operates as an

investment holding company.

The key products of the company are packing materials, vacuum foams, garments

made up of cotton and other fibres.

Denko properly presents all the items of disclosure in its recent annual report. It

shows all the information in its notes to financial statements.

The amount of impairment losses and the circumstances that causes impairment are

disclosed in the annual report.

Recognition and measurement requirements of MFRS 136 are discussed above.

The loss on impairment is measured only when the assets’ recoverable amount is less

than its carrying amount.

Higher of value in use and net selling price determines the recoverable amount of the

asset.

Carrying value means the figure at which the asset is been carried out in the balance

sheet of the company.

Overall, it is very important for Denko to comply with all the requirements of MFRS

136.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 13

Conclusion

The above report concludes that it is very much necessary for the Malaysian companies to

follow all the guidelines and requirements described by the standard which is applicable for

impairment of assets. The amount of impairment loss and other values must be calculated as

per MFRS 136 and should be disclosed in the annual report of the company. The treatment of

the same must also be presented.

References

Abuaddous, M., Hanefah, M.M. and Laili, N.H., (2014) Accounting standards, goodwill

impairment and earnings management in Malaysia. International Journal of Economics and

Finance, 6(12), p.201.

Conclusion

The above report concludes that it is very much necessary for the Malaysian companies to

follow all the guidelines and requirements described by the standard which is applicable for

impairment of assets. The amount of impairment loss and other values must be calculated as

per MFRS 136 and should be disclosed in the annual report of the company. The treatment of

the same must also be presented.

References

Abuaddous, M., Hanefah, M.M. and Laili, N.H., (2014) Accounting standards, goodwill

impairment and earnings management in Malaysia. International Journal of Economics and

Finance, 6(12), p.201.

Accounting 14

Bloomberg. (2018). Denko Industrial Corporation Bhd. [Online]. Available at:

https://www.bloomberg.com/quote/DEN:MK [Accessed 16 July 2018].

Che Azmi, A. and English, L.M., (2016) IFRS Disclosure Compliance in Malaysia: Insights

from a Small‐sample Analytical Study. Australian Accounting Review, 26(4), pp.390-414.

Denko. (2017). Denko industrial corporation Berhad Annual Report. [Online]. Available at:

http://www.denko.com.my/data/cms/images/1502779902_denko%20annual%20report

%202017.pdf [Accessed 16 July 2018].

Denko. (2018). Corporate History. [Online]. Available at:

http://www.denko.com.my/usr/pagesub.aspx?pgid=29 [Accessed 16 July 2018].

Devalle, A. and Rizzato, F., (2017) IFRS 3, IAS 36 and disclosure: The determinants of the

quality of disclosure. GSTF Journal on Business Review (GBR), 2(4).

Ernst and Young. (2010). Impairment accounting – the basics of IAS 36 Impairment of

Assets. [Online]. Available at:

http://www.ey.com/Publication/vwLUAssets/Impairment_accounting_the_basics_of_IAS_36

_Impairment_of_Assets/$FILE/Impairment_accounting_IAS_36.pdf [Accessed 16 July

2018].

IFRS. (2017). IAS 36 Impairment of Assets. [Online]. Available at:

http://www.ifrs.org/issued-standards/list-of-standards/ias-36-impairment-of-assets [Accessed

16 July 2018].

Lhaopadchan, S. (2010). Fair value accounting and intangible assets: Goodwill impairment

and managerial choice. Journal of Financial Regulation and Compliance, 18(2), 120-130.

Bloomberg. (2018). Denko Industrial Corporation Bhd. [Online]. Available at:

https://www.bloomberg.com/quote/DEN:MK [Accessed 16 July 2018].

Che Azmi, A. and English, L.M., (2016) IFRS Disclosure Compliance in Malaysia: Insights

from a Small‐sample Analytical Study. Australian Accounting Review, 26(4), pp.390-414.

Denko. (2017). Denko industrial corporation Berhad Annual Report. [Online]. Available at:

http://www.denko.com.my/data/cms/images/1502779902_denko%20annual%20report

%202017.pdf [Accessed 16 July 2018].

Denko. (2018). Corporate History. [Online]. Available at:

http://www.denko.com.my/usr/pagesub.aspx?pgid=29 [Accessed 16 July 2018].

Devalle, A. and Rizzato, F., (2017) IFRS 3, IAS 36 and disclosure: The determinants of the

quality of disclosure. GSTF Journal on Business Review (GBR), 2(4).

Ernst and Young. (2010). Impairment accounting – the basics of IAS 36 Impairment of

Assets. [Online]. Available at:

http://www.ey.com/Publication/vwLUAssets/Impairment_accounting_the_basics_of_IAS_36

_Impairment_of_Assets/$FILE/Impairment_accounting_IAS_36.pdf [Accessed 16 July

2018].

IFRS. (2017). IAS 36 Impairment of Assets. [Online]. Available at:

http://www.ifrs.org/issued-standards/list-of-standards/ias-36-impairment-of-assets [Accessed

16 July 2018].

Lhaopadchan, S. (2010). Fair value accounting and intangible assets: Goodwill impairment

and managerial choice. Journal of Financial Regulation and Compliance, 18(2), 120-130.

Accounting 15

Lobo, G.J., Paugam, L., Zhang, D. and Casta, J.F., (2017) The effect of joint auditor pair

composition on audit quality: Evidence from impairment tests. Contemporary Accounting

Research, 34(1), pp.118-153.

Rahman, A.A. and Mohamed, A.S., (2018) Investigating the Early Implementation of MFRS

136 Disclosure among Top 50 Firms in Malaysia. Asian Journal of Accounting and

Governance, 8, pp.59-76.

Reinstein, A., & Lander, G. H. (2004). Implementing the impairment of assets requirements

of SFAS No. 144: An empirical analysis. Managerial Auditing Journal, 19(3), 400-411.

Reuters. (2018). Denko Industrial Corporation Bhd (DICM.KL). [Online]. Available at:

https://www.reuters.com/finance/stocks/companyProfile/DICM.KL [Accessed 16 July 2018].

Schwarzbichler, M., Steiner, C. and Turnheim, D., (2018) Impairment of Assets (Fixed

Assets and Goodwill). In Financial Steering (pp. 343-370). Springer, Cham.

Shaari, H., Cao, T. and Donnelly, R., (2017) Reversals of impairment charges under IAS 36:

evidence from Malaysia. International Journal of Disclosure and Governance, 14(3), pp.224-

240.

Lobo, G.J., Paugam, L., Zhang, D. and Casta, J.F., (2017) The effect of joint auditor pair

composition on audit quality: Evidence from impairment tests. Contemporary Accounting

Research, 34(1), pp.118-153.

Rahman, A.A. and Mohamed, A.S., (2018) Investigating the Early Implementation of MFRS

136 Disclosure among Top 50 Firms in Malaysia. Asian Journal of Accounting and

Governance, 8, pp.59-76.

Reinstein, A., & Lander, G. H. (2004). Implementing the impairment of assets requirements

of SFAS No. 144: An empirical analysis. Managerial Auditing Journal, 19(3), 400-411.

Reuters. (2018). Denko Industrial Corporation Bhd (DICM.KL). [Online]. Available at:

https://www.reuters.com/finance/stocks/companyProfile/DICM.KL [Accessed 16 July 2018].

Schwarzbichler, M., Steiner, C. and Turnheim, D., (2018) Impairment of Assets (Fixed

Assets and Goodwill). In Financial Steering (pp. 343-370). Springer, Cham.

Shaari, H., Cao, T. and Donnelly, R., (2017) Reversals of impairment charges under IAS 36:

evidence from Malaysia. International Journal of Disclosure and Governance, 14(3), pp.224-

240.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.