Accounting Assignment: Financial Accounting and Management Accounting

VerifiedAdded on 2022/10/11

|16

|2802

|40

Homework Assignment

AI Summary

This accounting assignment solution covers key concepts in financial and management accounting. It begins with an overview of accounting principles, scope, and the preparation of financial statements like income statements and balance sheets. The solution then delves into management accounting tools, including breakeven analysis, variance analysis, and budgeting techniques. The assignment further explores cost accounting principles, cost classification, and the relationship between accounting and finance. The solution provides detailed explanations, calculations, and examples to illustrate these concepts, offering a thorough understanding of accounting fundamentals and their practical applications. References are included for each concept covered, and a detailed analysis of each question is provided.

Running head: ACCOUNTING

Accounting

Name of the Student:

Name of the University:

Author’s Note:

Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING

Table of Contents

Answer to question 1:......................................................................................................................3

Part a:...........................................................................................................................................3

Part b:...........................................................................................................................................4

Answer to question 2:......................................................................................................................6

Part a:...........................................................................................................................................6

Subpart i:..................................................................................................................................6

Subpart ii:.................................................................................................................................7

Part b:...........................................................................................................................................7

Answer to question 3:......................................................................................................................8

Part a:...........................................................................................................................................9

Part b:...........................................................................................................................................9

Part c:.........................................................................................................................................10

Answer to question 4:....................................................................................................................10

Part a:.........................................................................................................................................10

Part b:.........................................................................................................................................11

Answer to question 5:....................................................................................................................12

Answer to question 6:....................................................................................................................13

Part a:.........................................................................................................................................13

Part b:.........................................................................................................................................13

Table of Contents

Answer to question 1:......................................................................................................................3

Part a:...........................................................................................................................................3

Part b:...........................................................................................................................................4

Answer to question 2:......................................................................................................................6

Part a:...........................................................................................................................................6

Subpart i:..................................................................................................................................6

Subpart ii:.................................................................................................................................7

Part b:...........................................................................................................................................7

Answer to question 3:......................................................................................................................8

Part a:...........................................................................................................................................9

Part b:...........................................................................................................................................9

Part c:.........................................................................................................................................10

Answer to question 4:....................................................................................................................10

Part a:.........................................................................................................................................10

Part b:.........................................................................................................................................11

Answer to question 5:....................................................................................................................12

Answer to question 6:....................................................................................................................13

Part a:.........................................................................................................................................13

Part b:.........................................................................................................................................13

2ACCOUNTING

References and bibliography:........................................................................................................14

References and bibliography:........................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING

Answer to question 1:

The first question focuses on the conceptual aspects of the financial accounting.

Accounting is an integrated and systematic process of recording transactions in the books of

accounts, classifying them, summarizing them based on relevancy and reporting transactions for

the financial information users. In the first part of this question, the concepts of accounting, its

scope and importance have been asked to describe. The second part of this question is aimed at

application of the knowledge of accounting and the knowledge of finalizing accounts and

preparing financial statements (Biereret al. 2015).

Part a:

Accounting can be defined as a continuous and systematic process of recording

transactions classifying them in according to their nature, summarizing them and preparing some

meaningful reports. Money is the common means of exchange, hence it can be converted into

anything. Therefore, there must be a track of cash inflows and outflows. Therefore, accounting is

the process, which keeps a track of all such inflows and outflows of money. It is also aimed at

comparing the inflows and outflows of money and money values and to ascertain the net result.

Accounting is not specifically meant for the business organization. Every such institutions or

happenings, where certain amount of money or money value is involved, the accounting process

can be applied to keep a proper track of all the inflow and outflow of money. Hence, the scope of

accounting is not a narrower one, rather it can be applied in each such contexts where some

monetary transactions are involved (Bobryshevet al. 2015).

In a business organization also in each segment of the business the accounting process

can be implemented as each process of a business organization involves certain monetary

Answer to question 1:

The first question focuses on the conceptual aspects of the financial accounting.

Accounting is an integrated and systematic process of recording transactions in the books of

accounts, classifying them, summarizing them based on relevancy and reporting transactions for

the financial information users. In the first part of this question, the concepts of accounting, its

scope and importance have been asked to describe. The second part of this question is aimed at

application of the knowledge of accounting and the knowledge of finalizing accounts and

preparing financial statements (Biereret al. 2015).

Part a:

Accounting can be defined as a continuous and systematic process of recording

transactions classifying them in according to their nature, summarizing them and preparing some

meaningful reports. Money is the common means of exchange, hence it can be converted into

anything. Therefore, there must be a track of cash inflows and outflows. Therefore, accounting is

the process, which keeps a track of all such inflows and outflows of money. It is also aimed at

comparing the inflows and outflows of money and money values and to ascertain the net result.

Accounting is not specifically meant for the business organization. Every such institutions or

happenings, where certain amount of money or money value is involved, the accounting process

can be applied to keep a proper track of all the inflow and outflow of money. Hence, the scope of

accounting is not a narrower one, rather it can be applied in each such contexts where some

monetary transactions are involved (Bobryshevet al. 2015).

In a business organization also in each segment of the business the accounting process

can be implemented as each process of a business organization involves certain monetary

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING

transactions. Based on the department or the segment where the techniques of accounting is

implemented and applied it can be classified as financial accounting, management accounting,

cost accounting and corporate accounting (Brewer,Garrisonand Noreen2015).

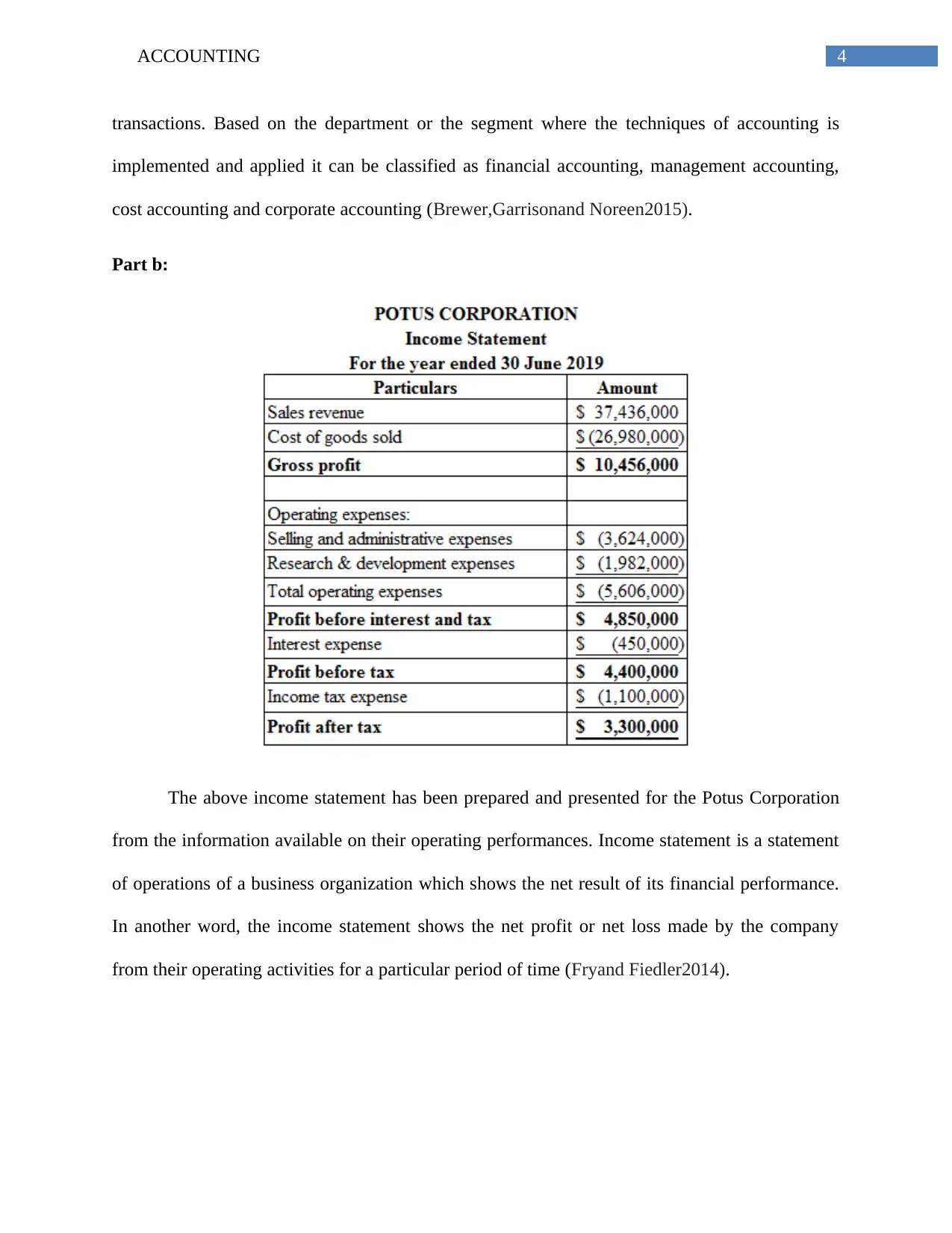

Part b:

The above income statement has been prepared and presented for the Potus Corporation

from the information available on their operating performances. Income statement is a statement

of operations of a business organization which shows the net result of its financial performance.

In another word, the income statement shows the net profit or net loss made by the company

from their operating activities for a particular period of time (Fryand Fiedler2014).

transactions. Based on the department or the segment where the techniques of accounting is

implemented and applied it can be classified as financial accounting, management accounting,

cost accounting and corporate accounting (Brewer,Garrisonand Noreen2015).

Part b:

The above income statement has been prepared and presented for the Potus Corporation

from the information available on their operating performances. Income statement is a statement

of operations of a business organization which shows the net result of its financial performance.

In another word, the income statement shows the net profit or net loss made by the company

from their operating activities for a particular period of time (Fryand Fiedler2014).

5ACCOUNTING

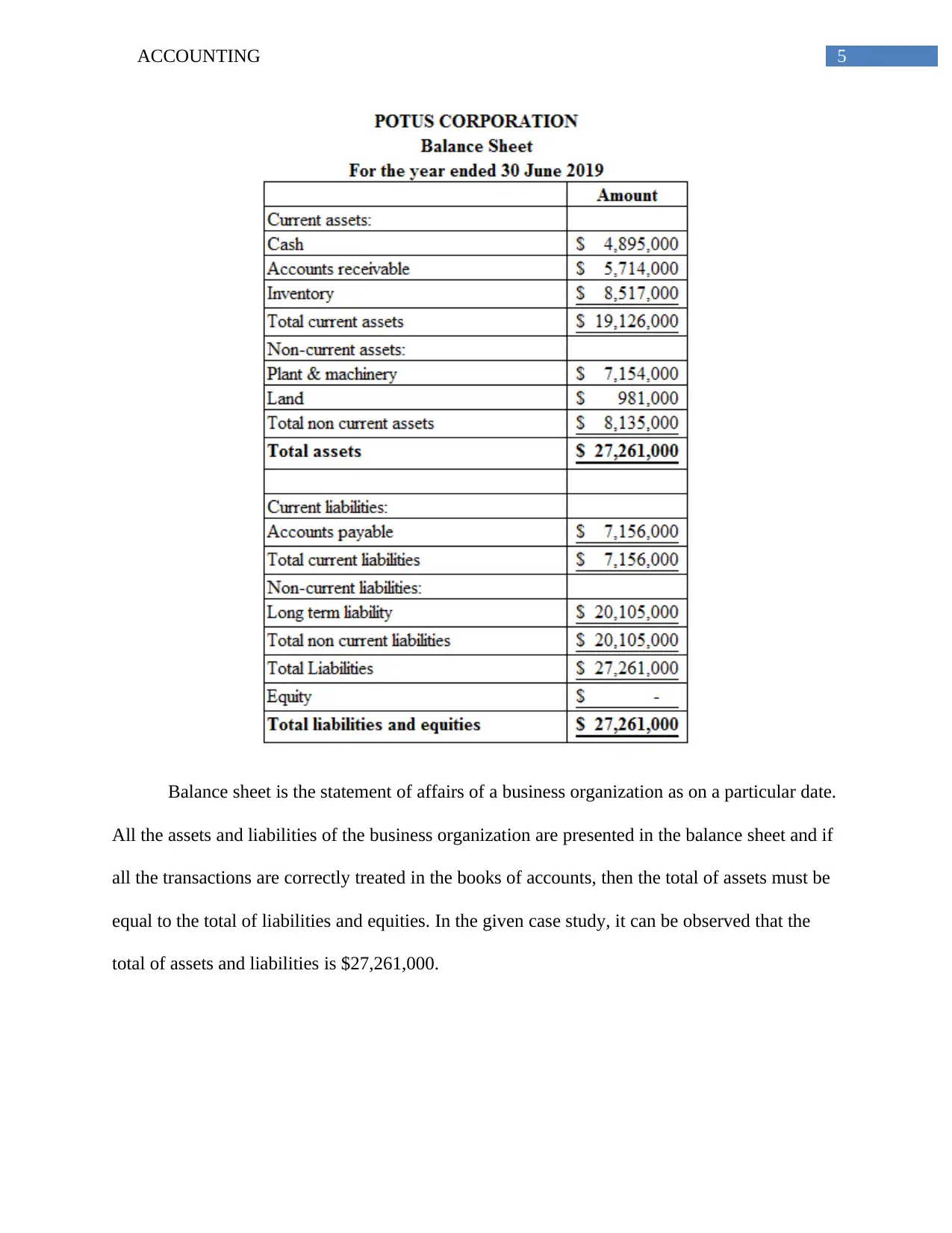

Balance sheet is the statement of affairs of a business organization as on a particular date.

All the assets and liabilities of the business organization are presented in the balance sheet and if

all the transactions are correctly treated in the books of accounts, then the total of assets must be

equal to the total of liabilities and equities. In the given case study, it can be observed that the

total of assets and liabilities is $27,261,000.

Balance sheet is the statement of affairs of a business organization as on a particular date.

All the assets and liabilities of the business organization are presented in the balance sheet and if

all the transactions are correctly treated in the books of accounts, then the total of assets must be

equal to the total of liabilities and equities. In the given case study, it can be observed that the

total of assets and liabilities is $27,261,000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING

Answer to question 2:

In this part knowledge of management accounting have been applied, and some of the

management accounting tools have been applied which help in analyzing and interpreting the

current operational performance of a business organization and to make necessary corrective

measures for improvement in the operational performance of the business (Glover2014).

Part a:

Breakeven point is nothing but that level of output at which the firm earns no profit and

incurs no loss. It is a situation when the firm is able to extract the total costs, and nothing more or

less than the costs. The breakeven point analysis can be applied in various decision making such

as make or buy, outsourcing decision and so on (Hendersonet al. 2015).

Subpart i:

Breakeven analysis is the method of computation of minimum number of output that will

make the total cost equal to the total revenue there by leaving no profit and no loss. A firm must

produce the breakeven number of units to avoid any losses, otherwise there will be a capital

erosion. If the business is going to take up a new project, and if its costs are known then the

breakeven analysis can help to understand whether the expected demand for the output of the

proposed project is going to make profit for the company or loss. It can be applied for analysis of

the feasibility of the proposed project. Hence, in making various important business decisions

and management decisions, the breakeven point analysis is most important and helpful too

(Hoyle,Schaeferand Doupnik2015).

Answer to question 2:

In this part knowledge of management accounting have been applied, and some of the

management accounting tools have been applied which help in analyzing and interpreting the

current operational performance of a business organization and to make necessary corrective

measures for improvement in the operational performance of the business (Glover2014).

Part a:

Breakeven point is nothing but that level of output at which the firm earns no profit and

incurs no loss. It is a situation when the firm is able to extract the total costs, and nothing more or

less than the costs. The breakeven point analysis can be applied in various decision making such

as make or buy, outsourcing decision and so on (Hendersonet al. 2015).

Subpart i:

Breakeven analysis is the method of computation of minimum number of output that will

make the total cost equal to the total revenue there by leaving no profit and no loss. A firm must

produce the breakeven number of units to avoid any losses, otherwise there will be a capital

erosion. If the business is going to take up a new project, and if its costs are known then the

breakeven analysis can help to understand whether the expected demand for the output of the

proposed project is going to make profit for the company or loss. It can be applied for analysis of

the feasibility of the proposed project. Hence, in making various important business decisions

and management decisions, the breakeven point analysis is most important and helpful too

(Hoyle,Schaeferand Doupnik2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING

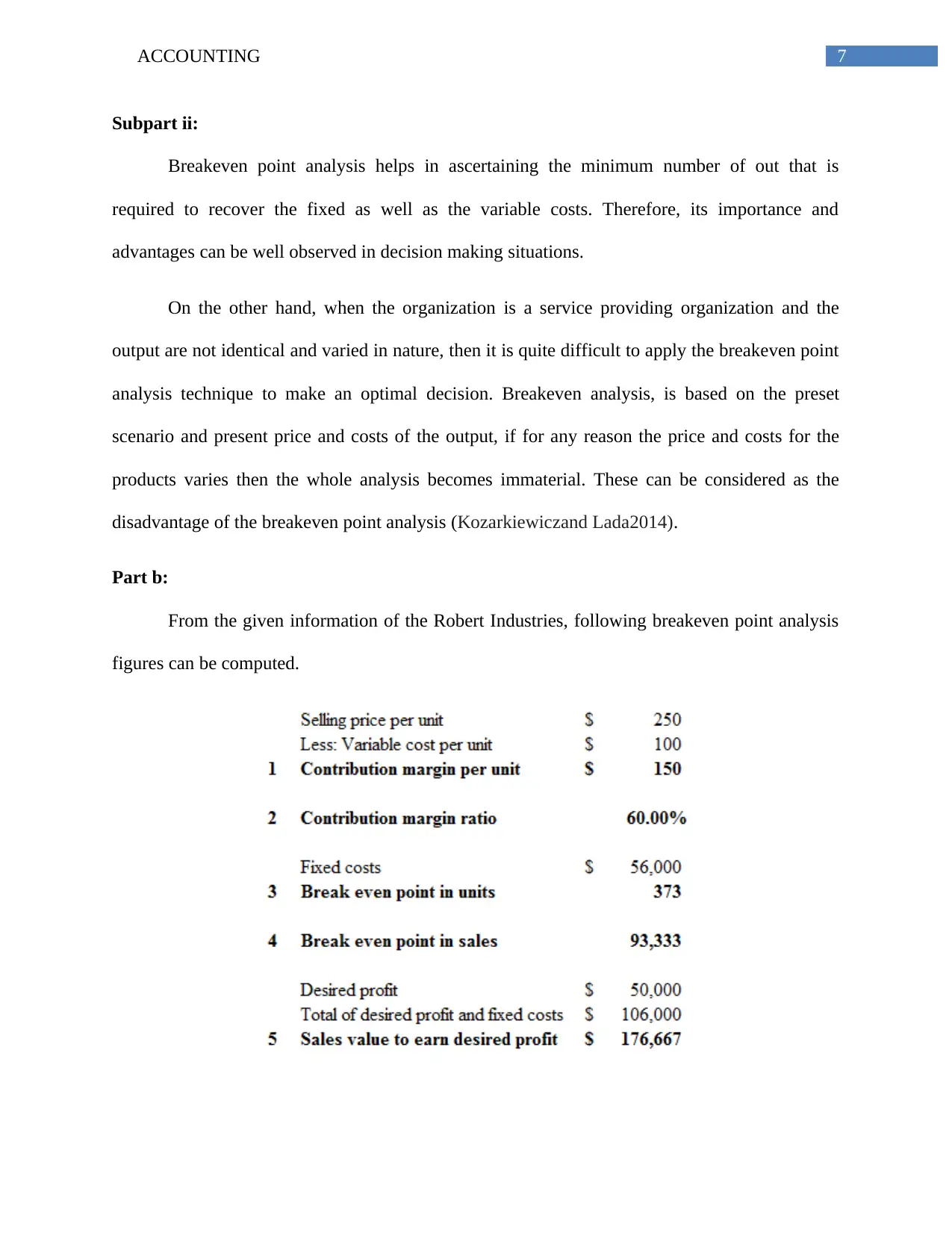

Subpart ii:

Breakeven point analysis helps in ascertaining the minimum number of out that is

required to recover the fixed as well as the variable costs. Therefore, its importance and

advantages can be well observed in decision making situations.

On the other hand, when the organization is a service providing organization and the

output are not identical and varied in nature, then it is quite difficult to apply the breakeven point

analysis technique to make an optimal decision. Breakeven analysis, is based on the preset

scenario and present price and costs of the output, if for any reason the price and costs for the

products varies then the whole analysis becomes immaterial. These can be considered as the

disadvantage of the breakeven point analysis (Kozarkiewiczand Lada2014).

Part b:

From the given information of the Robert Industries, following breakeven point analysis

figures can be computed.

Subpart ii:

Breakeven point analysis helps in ascertaining the minimum number of out that is

required to recover the fixed as well as the variable costs. Therefore, its importance and

advantages can be well observed in decision making situations.

On the other hand, when the organization is a service providing organization and the

output are not identical and varied in nature, then it is quite difficult to apply the breakeven point

analysis technique to make an optimal decision. Breakeven analysis, is based on the preset

scenario and present price and costs of the output, if for any reason the price and costs for the

products varies then the whole analysis becomes immaterial. These can be considered as the

disadvantage of the breakeven point analysis (Kozarkiewiczand Lada2014).

Part b:

From the given information of the Robert Industries, following breakeven point analysis

figures can be computed.

8ACCOUNTING

From the above analysis and computation it can be observed that, the company need to

produce minimum of 373 units to reach the breakeven point and a sales amount of $176,667 to

earn a profit of $50,000.

Answer to question 3:

There are various tools and techniques in the cost and management accounting which can

be applied to analyze the operating performance of any department of the business and to

identify any variances from the budgeted one or from the standard benchmark. It helps in taking

various corrective measures and building strategies for improvement in the operating activities of

the business. Analysis of variance is one of such important management accounting tool which is

used to analyze variances for the actual performances with comparison to the standard

benchmarks. In the following part the variance analysis technique has been applied with a

practical example to understand it in better way (Laitinen2014).

From the above analysis and computation it can be observed that, the company need to

produce minimum of 373 units to reach the breakeven point and a sales amount of $176,667 to

earn a profit of $50,000.

Answer to question 3:

There are various tools and techniques in the cost and management accounting which can

be applied to analyze the operating performance of any department of the business and to

identify any variances from the budgeted one or from the standard benchmark. It helps in taking

various corrective measures and building strategies for improvement in the operating activities of

the business. Analysis of variance is one of such important management accounting tool which is

used to analyze variances for the actual performances with comparison to the standard

benchmarks. In the following part the variance analysis technique has been applied with a

practical example to understand it in better way (Laitinen2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING

Part a:

Part b:

Part a:

Part b:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING

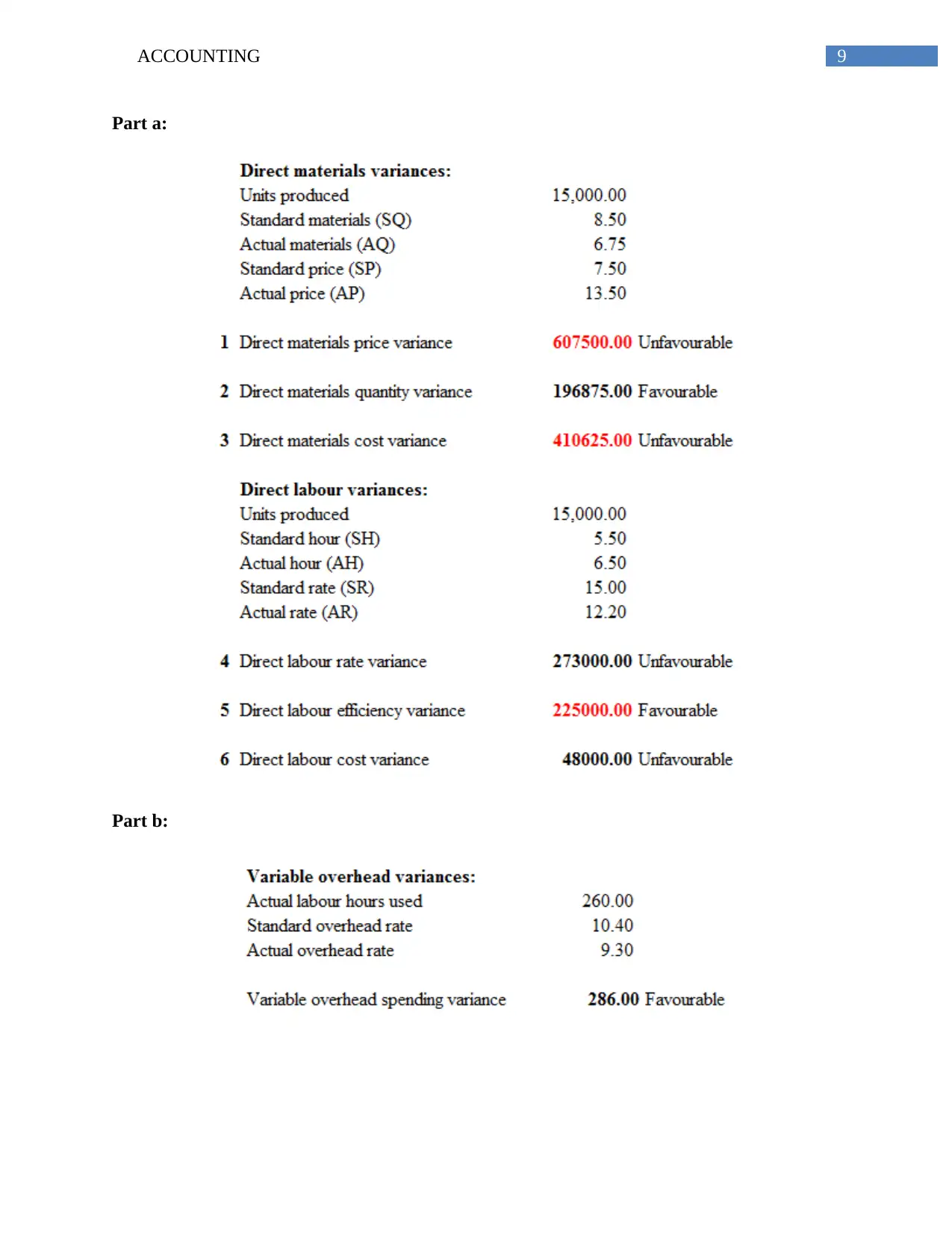

Part c:

Variance analysis is a cost and management accounting tool which is applied to ascertain

the difference between the budgeted or standards costs and the actual costs for the actual

production. Variance analysis not only means comparison and analysis of costs, it also applies

for the revenues. Therefore, comparison of the actual performance with the budgeted or

standards one and ascertainment of the differences between these two is known as the variance

analysis (Macve2015).

The most important advantage of the variance analysis is that, it helps in identifying the

cause behind the poor performance of any particular segment of the business and helps in taking

corrective measures. If the production process is unique in nature, where each of the production

requires different types of materials and process times the standards cannot be fixed before and

hence, the variance analysis cannot be applied. Hence, it is not applicable for tailor made works

which can be considered as the disadvantage of the variance analysis technique (Morden2016).

Answer to question 4:

Budget is another important tool of cost and management accounting. Budget is the

estimation of expenses of incomes for some future operating activities. Budget and forecasting is

different completely. Budget is the estimation of incomes and expenses based on the forecasted

demands for the products or services. Budget helps in planning activities and allocation of funds

for certain operational activities of the business (Nelsonand Miller2014).

Part a:

When preparing a budget, the main objective of the budget to ascertain the expected cash

inflows and the expected allocation of funds in expenses payments. Therefore, the main

Part c:

Variance analysis is a cost and management accounting tool which is applied to ascertain

the difference between the budgeted or standards costs and the actual costs for the actual

production. Variance analysis not only means comparison and analysis of costs, it also applies

for the revenues. Therefore, comparison of the actual performance with the budgeted or

standards one and ascertainment of the differences between these two is known as the variance

analysis (Macve2015).

The most important advantage of the variance analysis is that, it helps in identifying the

cause behind the poor performance of any particular segment of the business and helps in taking

corrective measures. If the production process is unique in nature, where each of the production

requires different types of materials and process times the standards cannot be fixed before and

hence, the variance analysis cannot be applied. Hence, it is not applicable for tailor made works

which can be considered as the disadvantage of the variance analysis technique (Morden2016).

Answer to question 4:

Budget is another important tool of cost and management accounting. Budget is the

estimation of expenses of incomes for some future operating activities. Budget and forecasting is

different completely. Budget is the estimation of incomes and expenses based on the forecasted

demands for the products or services. Budget helps in planning activities and allocation of funds

for certain operational activities of the business (Nelsonand Miller2014).

Part a:

When preparing a budget, the main objective of the budget to ascertain the expected cash

inflows and the expected allocation of funds in expenses payments. Therefore, the main

11ACCOUNTING

component of the budget is the receipts and payments. Based on functions, the budgeting can be

classified in functional budget, and cash budget. Functional budgets are prepared for every key

function in the supply chain of the business such as sales budget, production budget,

procurement budget, cash receipts budge and cash payment budget, expenses budget and so on.

On the other hand to sum up all the functional budgets, the master budget is prepared to make a

conclusion and to make a useful report to help in planning and managerial decision. Therefore,

forecasted demands, expected cash receipts and expenses payments and payment frequency is

the important factor that must be known while preparing the budget (Phillips,Libbyand

Libby2015).

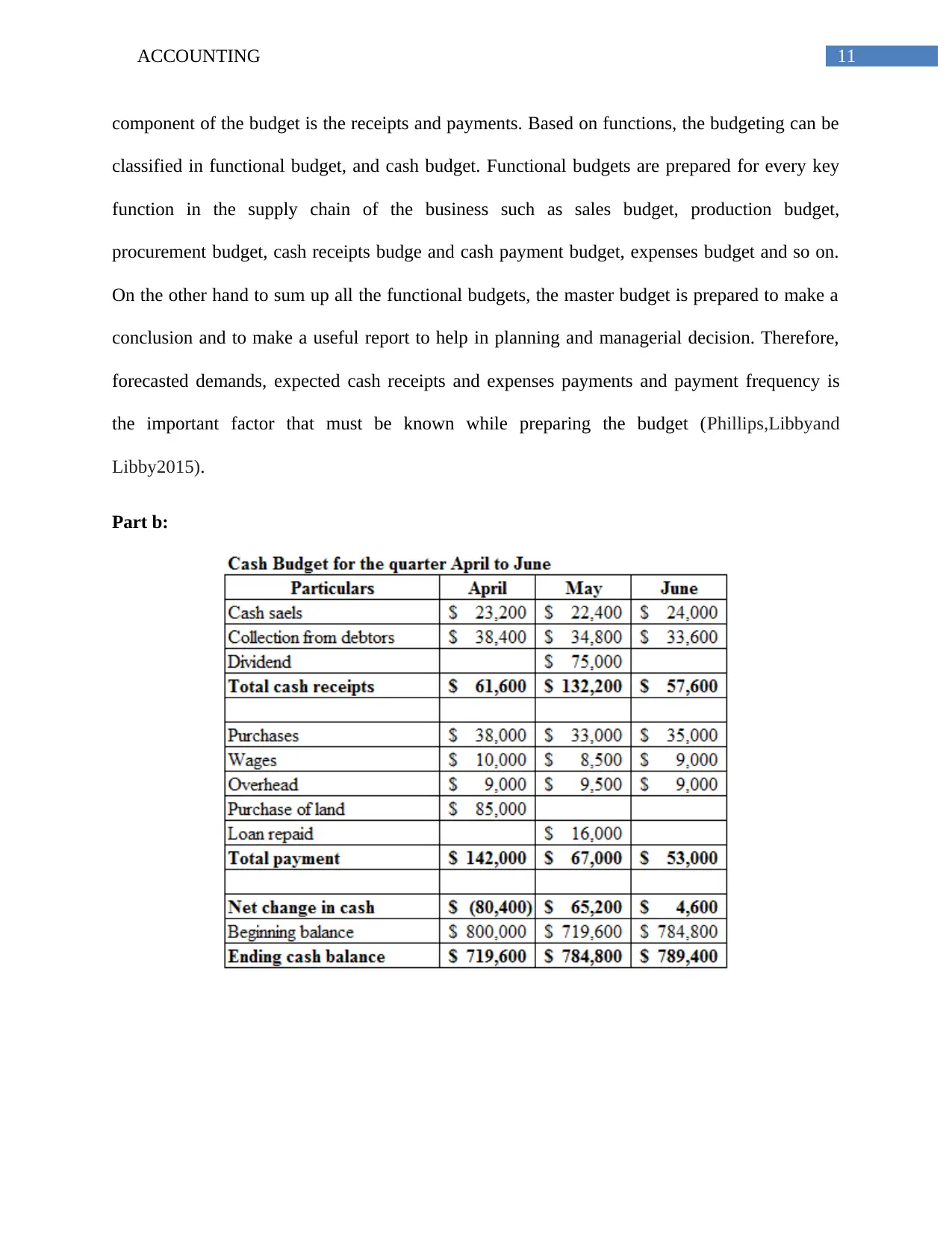

Part b:

component of the budget is the receipts and payments. Based on functions, the budgeting can be

classified in functional budget, and cash budget. Functional budgets are prepared for every key

function in the supply chain of the business such as sales budget, production budget,

procurement budget, cash receipts budge and cash payment budget, expenses budget and so on.

On the other hand to sum up all the functional budgets, the master budget is prepared to make a

conclusion and to make a useful report to help in planning and managerial decision. Therefore,

forecasted demands, expected cash receipts and expenses payments and payment frequency is

the important factor that must be known while preparing the budget (Phillips,Libbyand

Libby2015).

Part b:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.