ACCTG 101 Assignment 02: Financial Statement and Budgeting Analysis

VerifiedAdded on 2023/04/04

|10

|1643

|265

Homework Assignment

AI Summary

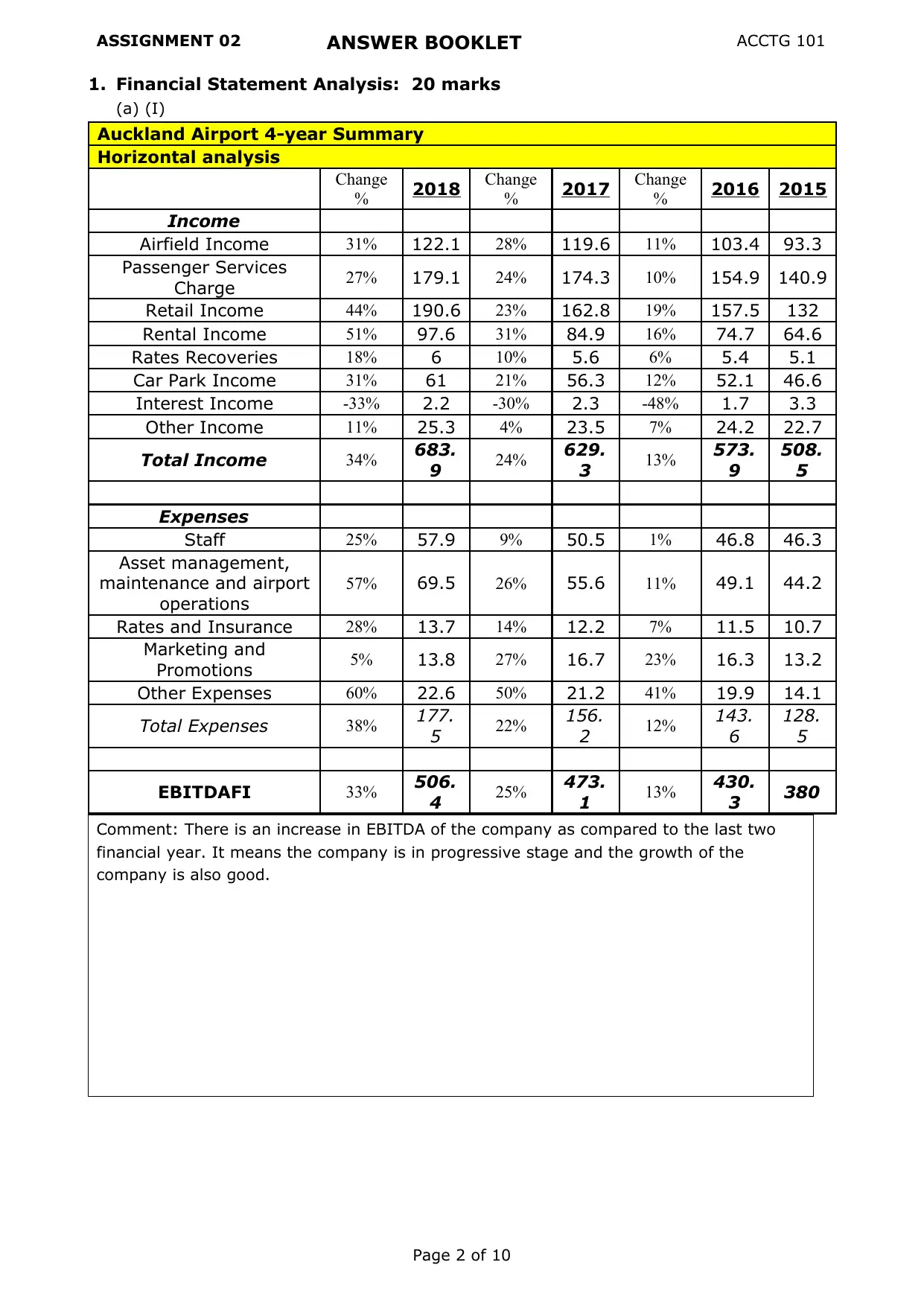

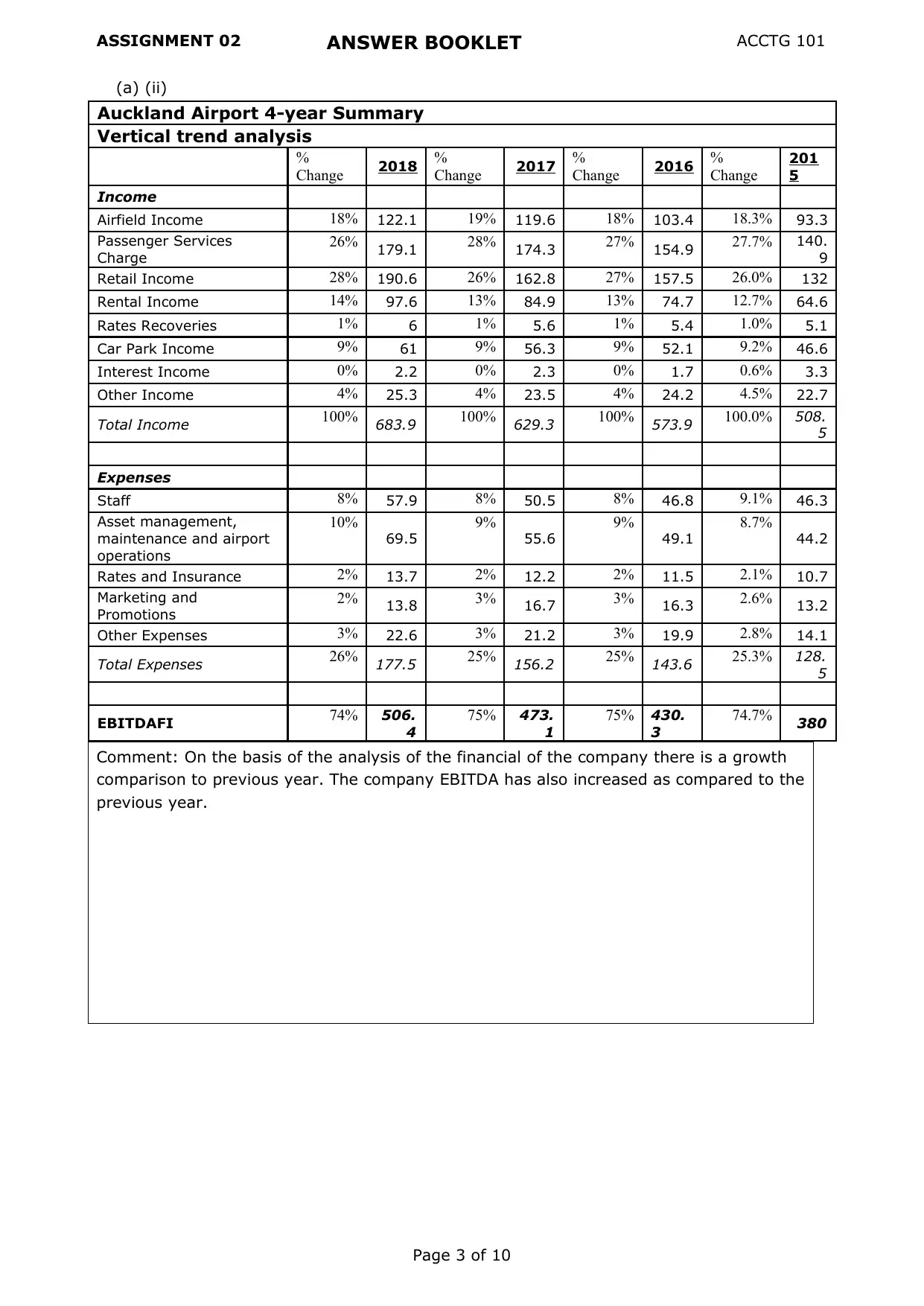

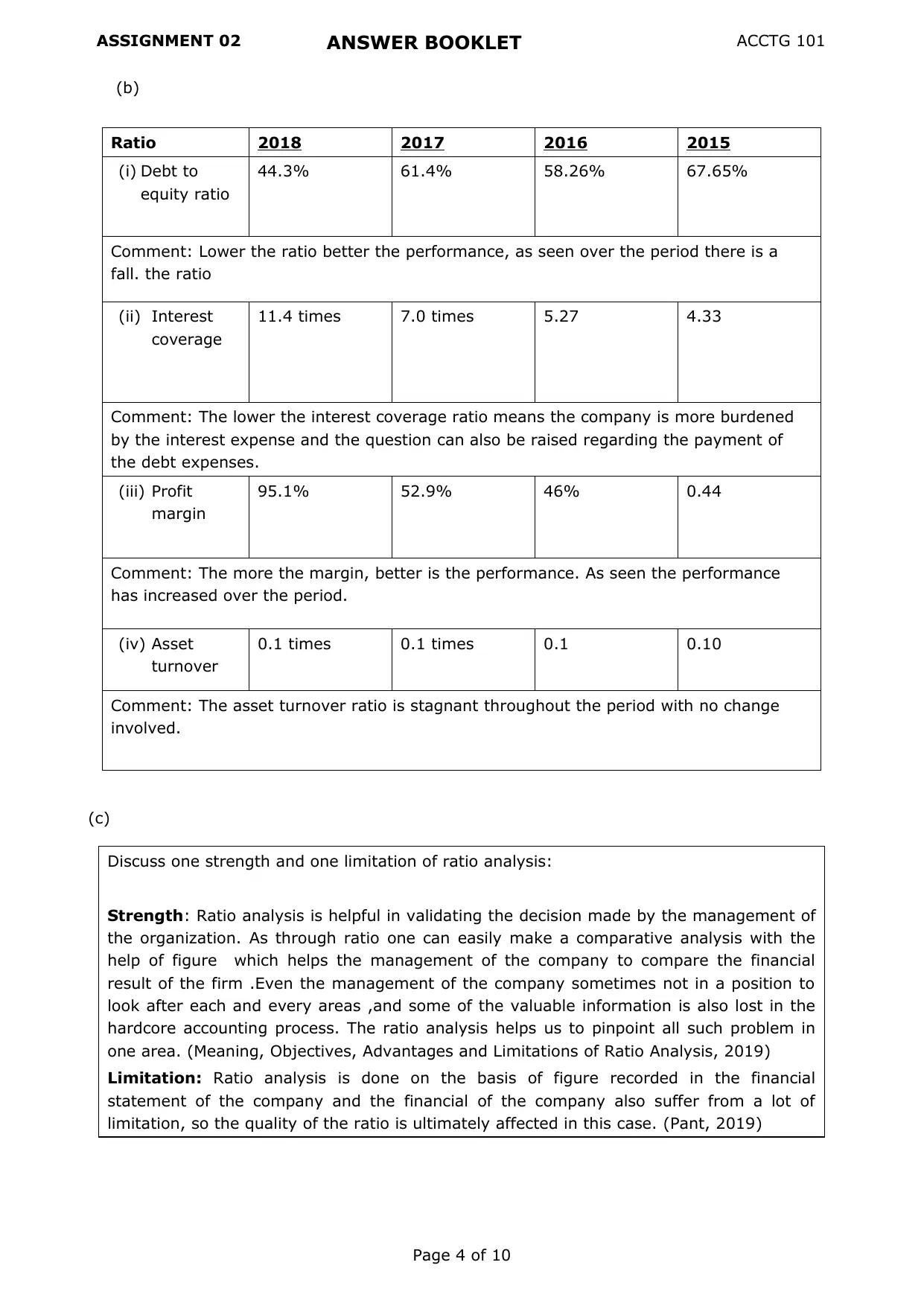

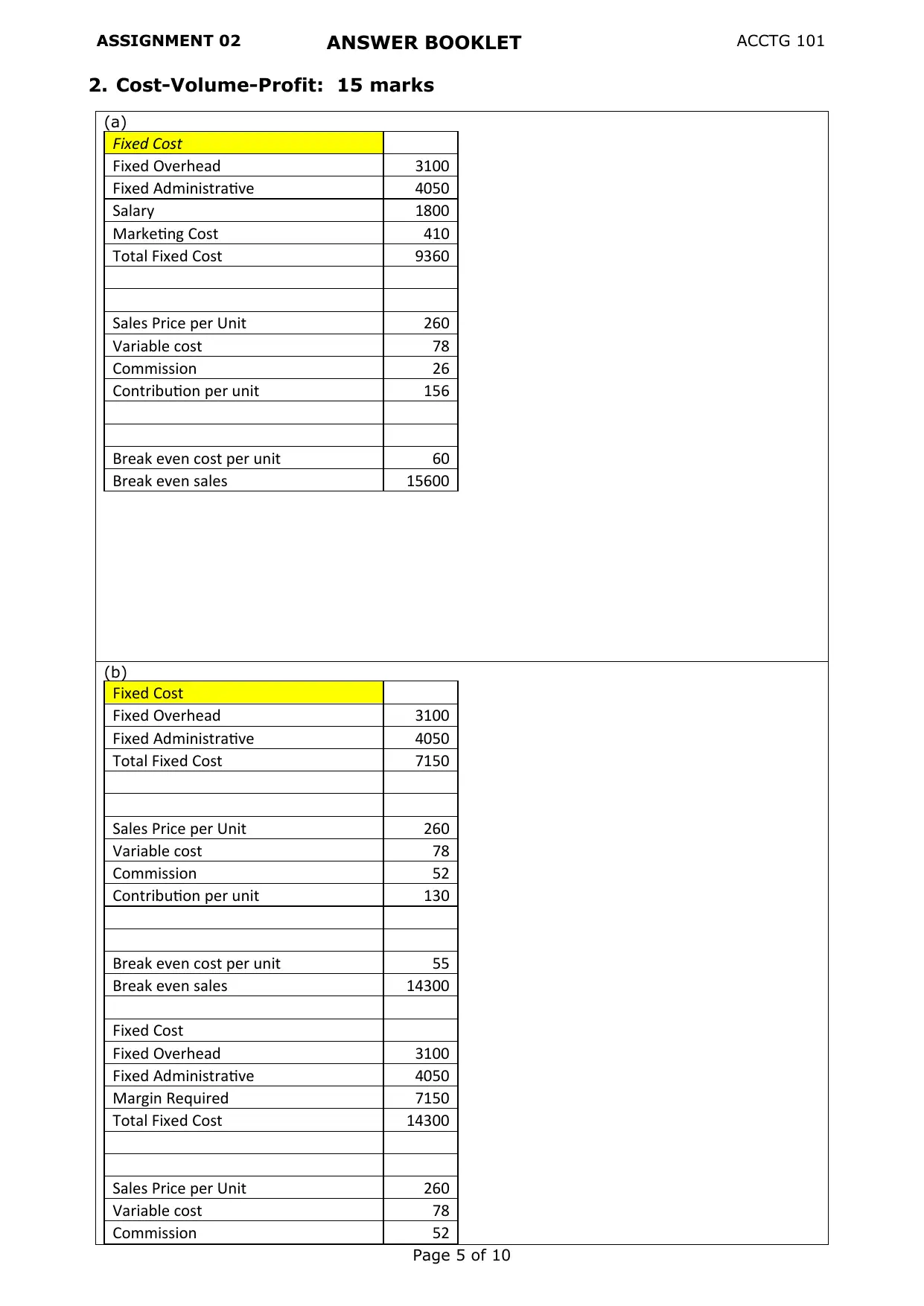

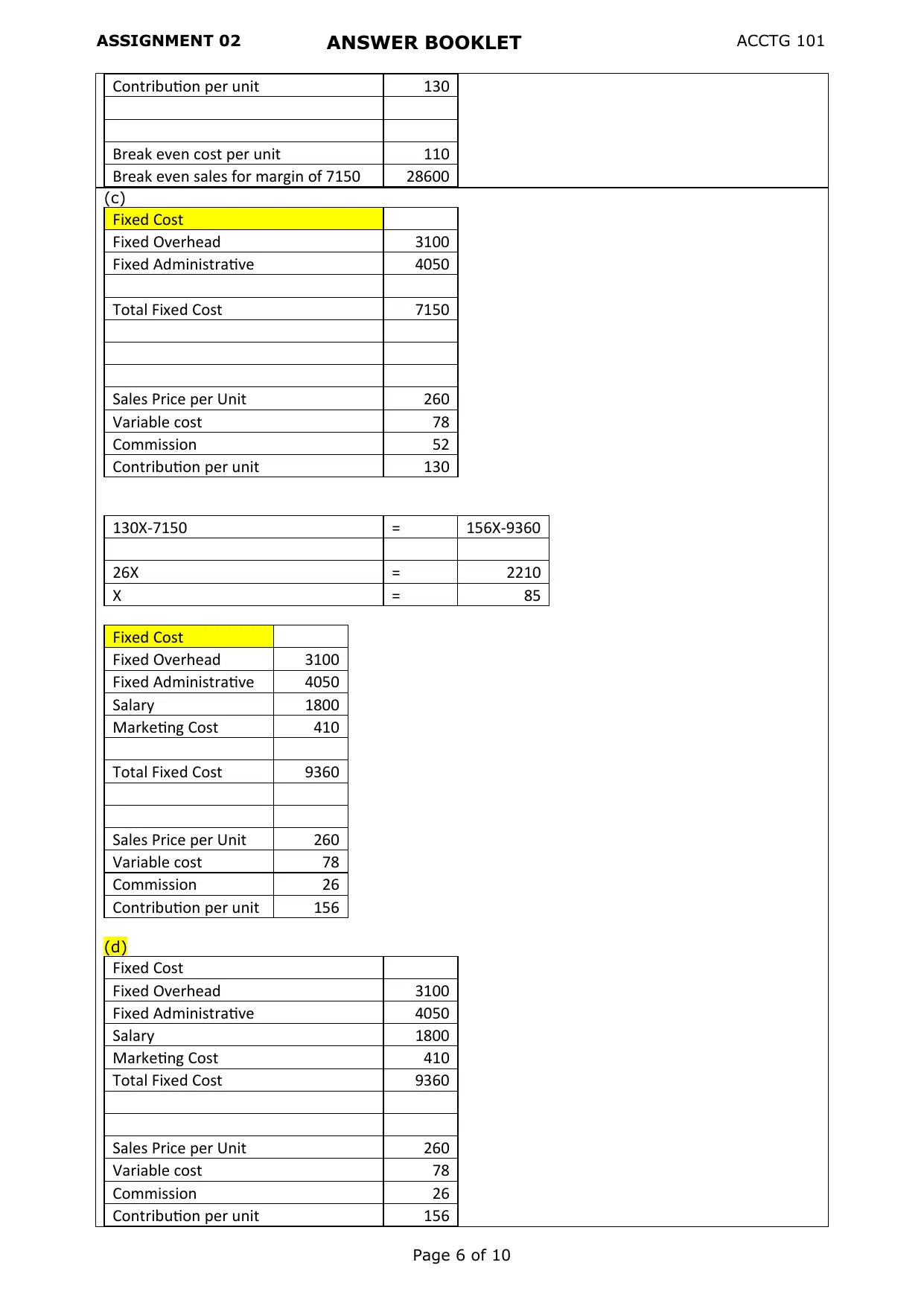

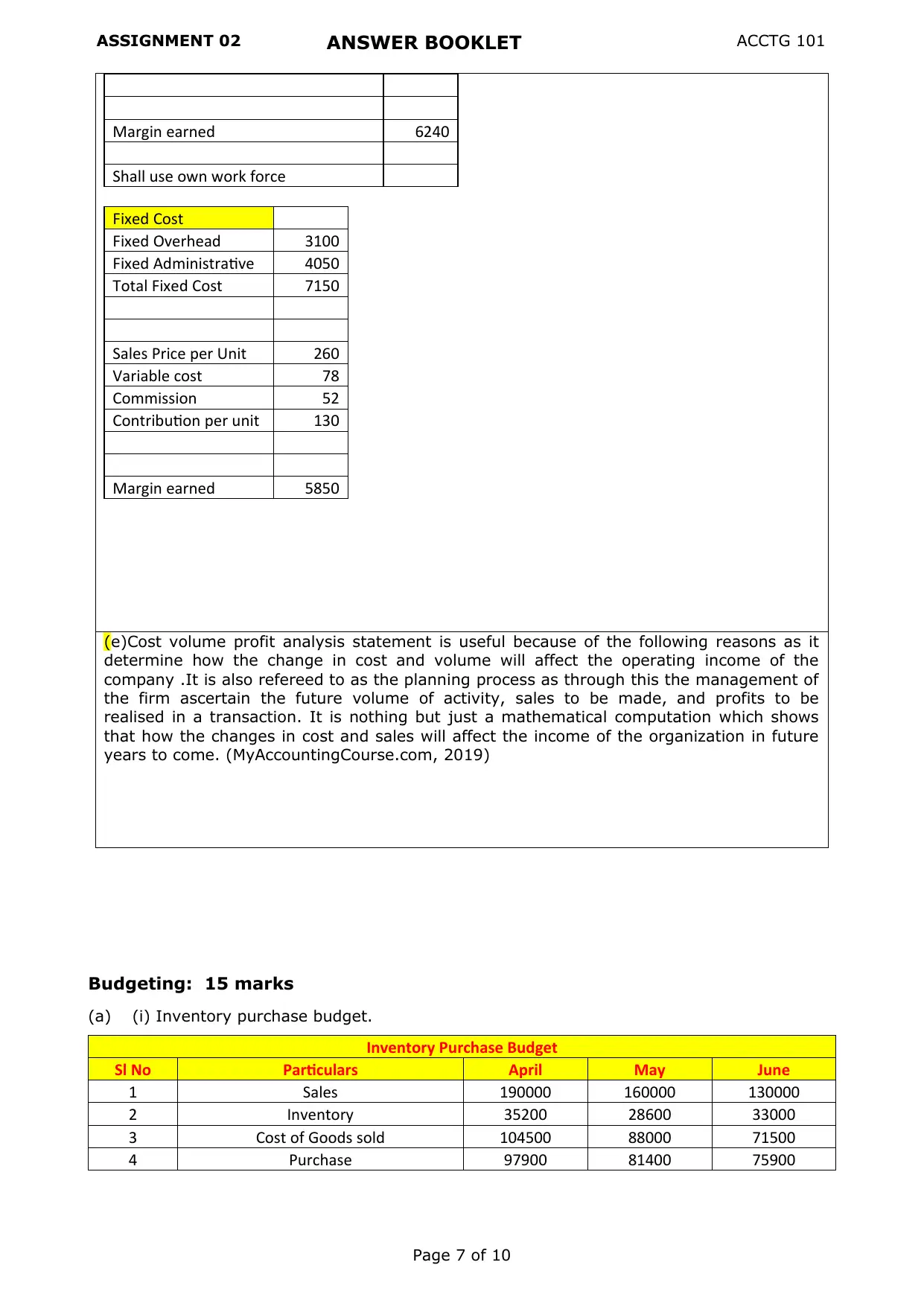

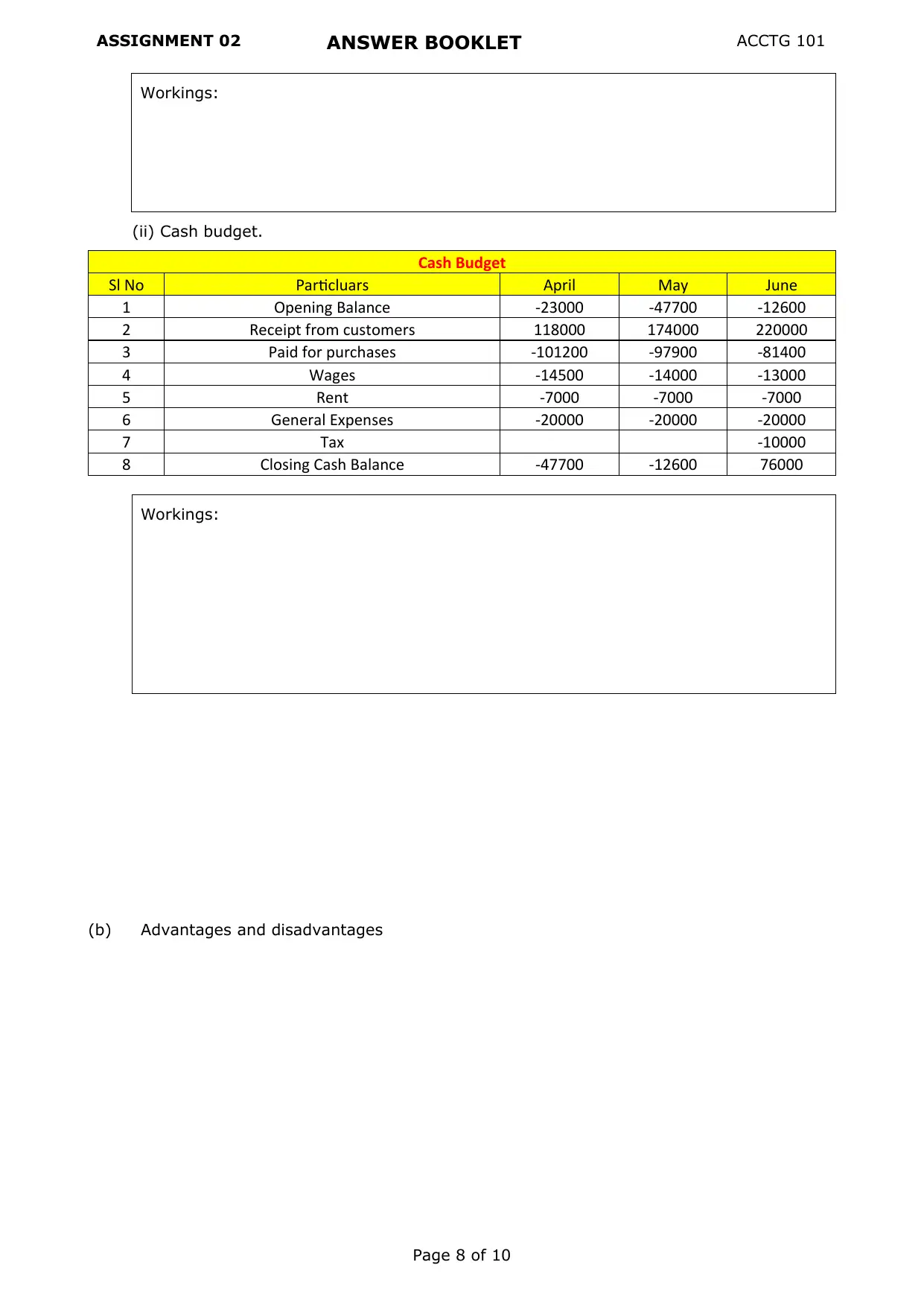

This document provides a detailed solution for ACCTG 101 Assignment 02, a homework assignment from the University of Auckland's first semester of 2019. The assignment covers three main areas: financial statement analysis, cost-volume-profit (CVP) analysis, and budgeting. The financial statement analysis includes horizontal and vertical analysis of Auckland Airport's income and expenses over a four-year period, along with the calculation and interpretation of key financial ratios like debt-to-equity, interest coverage, profit margin, and asset turnover. The CVP analysis involves calculating break-even points and determining the impact of different cost structures on profitability. The budgeting section includes creating an inventory purchase budget and a cash budget, along with a discussion of the advantages and disadvantages of just-in-time inventory management. The solution provides clear workings and explanations for each question, demonstrating a strong understanding of accounting principles and financial analysis techniques. The assignment is a comprehensive assessment of fundamental accounting concepts and their practical application.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.