MAFI1A-8/S1 05/19: GTZ Group Finance and Accounting Assignment

VerifiedAdded on 2023/01/10

|11

|2554

|33

Homework Assignment

AI Summary

This assignment solution addresses various aspects of financial management and accounting, specifically within the context of the GTZ Business Group. It begins by analyzing the financial viability of opening a store on Sundays, considering incremental profit and loss, and evaluating the impact of e...

Assignment 1 (MAFI1A-8/S1 05/19)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1........................................................................................................................................3

Question 2........................................................................................................................................3

Question 3........................................................................................................................................4

Question 4........................................................................................................................................5

Question 5........................................................................................................................................5

Question 6........................................................................................................................................6

Question 7........................................................................................................................................7

Question 8........................................................................................................................................8

Question 9........................................................................................................................................9

Question 10....................................................................................................................................10

References......................................................................................................................................11

Question 1........................................................................................................................................3

Question 2........................................................................................................................................3

Question 3........................................................................................................................................4

Question 4........................................................................................................................................5

Question 5........................................................................................................................................5

Question 6........................................................................................................................................6

Question 7........................................................................................................................................7

Question 8........................................................................................................................................8

Question 9........................................................................................................................................9

Question 10....................................................................................................................................10

References......................................................................................................................................11

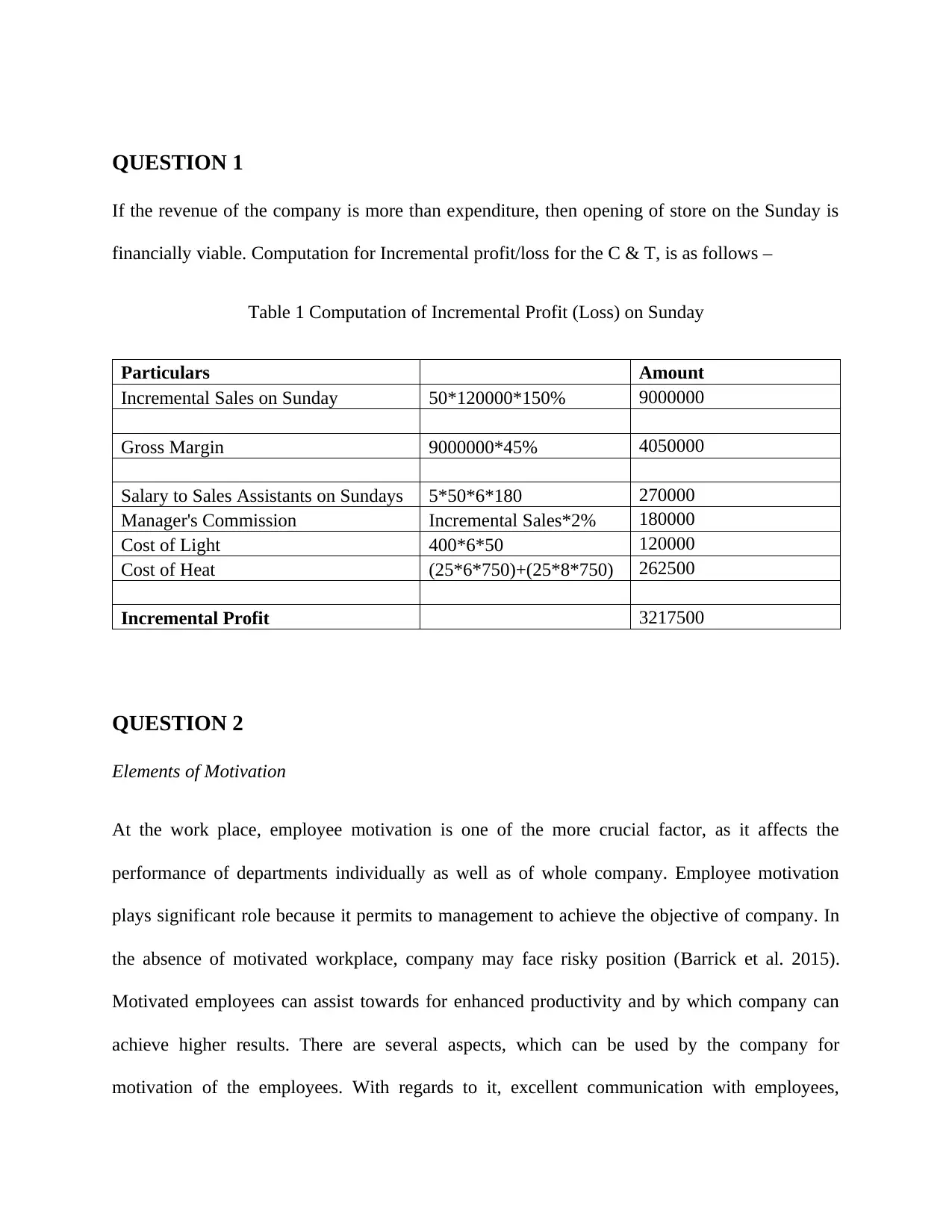

QUESTION 1

If the revenue of the company is more than expenditure, then opening of store on the Sunday is

financially viable. Computation for Incremental profit/loss for the C & T, is as follows –

Table 1 Computation of Incremental Profit (Loss) on Sunday

Particulars Amount

Incremental Sales on Sunday 50*120000*150% 9000000

Gross Margin 9000000*45% 4050000

Salary to Sales Assistants on Sundays 5*50*6*180 270000

Manager's Commission Incremental Sales*2% 180000

Cost of Light 400*6*50 120000

Cost of Heat (25*6*750)+(25*8*750) 262500

Incremental Profit 3217500

QUESTION 2

Elements of Motivation

At the work place, employee motivation is one of the more crucial factor, as it affects the

performance of departments individually as well as of whole company. Employee motivation

plays significant role because it permits to management to achieve the objective of company. In

the absence of motivated workplace, company may face risky position (Barrick et al. 2015).

Motivated employees can assist towards for enhanced productivity and by which company can

achieve higher results. There are several aspects, which can be used by the company for

motivation of the employees. With regards to it, excellent communication with employees,

If the revenue of the company is more than expenditure, then opening of store on the Sunday is

financially viable. Computation for Incremental profit/loss for the C & T, is as follows –

Table 1 Computation of Incremental Profit (Loss) on Sunday

Particulars Amount

Incremental Sales on Sunday 50*120000*150% 9000000

Gross Margin 9000000*45% 4050000

Salary to Sales Assistants on Sundays 5*50*6*180 270000

Manager's Commission Incremental Sales*2% 180000

Cost of Light 400*6*50 120000

Cost of Heat (25*6*750)+(25*8*750) 262500

Incremental Profit 3217500

QUESTION 2

Elements of Motivation

At the work place, employee motivation is one of the more crucial factor, as it affects the

performance of departments individually as well as of whole company. Employee motivation

plays significant role because it permits to management to achieve the objective of company. In

the absence of motivated workplace, company may face risky position (Barrick et al. 2015).

Motivated employees can assist towards for enhanced productivity and by which company can

achieve higher results. There are several aspects, which can be used by the company for

motivation of the employees. With regards to it, excellent communication with employees,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

positive environment in company, rewards, promotion, bonus, value contribution of each

employee are some of the techniques that can increase the motivation of employees

(Kontoghiorghes, 2016).

In the present report, it is prescribed that, supervisor of the company will receive extra bonus of

2% on extra sales generated on Sunday project. It is definitely affect the motivational elements.

By this, supervisor will be motivated towards generation of the extra sales, so that he can receive

maximum monetary bonus. Along with this, he can also take equivalent time off during the week

day, if he works on Sunday as a non-monetary reward. By this, the working hours of the super

visor will not increase, even he gets extra benefit on Sunday. Therefore, on the basis of above

aspect, it can be said that manager’s pay deal at C&T regarding his bonus and time off is likely

to serve as a motivation.

QUESTION 3

Promotion means the activities carried out by the company, by which it can communicate about

its goods, services, products to its customers or users. It is planning to make society attract,

aware, and encourage for buy the products (Schmid, Grosche, and Mayrhofer, 2016). There are

several types of promotional activities, which assist the company for improvising its

performance. In this aspect, advertisements, trade discounts, incentives, schemes, and some other

tools helps the company to promote their product (Ryoo, Jeon, and Lee, 2016). In the given case,

the company offering significant price discount on Sunday as part of their promotional strategies.

Price discount is the general method, by which customers can easily be attracted. It is the right

thing, by which company can enhanced its sales on Sunday. But at the same time, it should

consider about its profitability. Further, significant discount leads to negative aspects regarding

employee are some of the techniques that can increase the motivation of employees

(Kontoghiorghes, 2016).

In the present report, it is prescribed that, supervisor of the company will receive extra bonus of

2% on extra sales generated on Sunday project. It is definitely affect the motivational elements.

By this, supervisor will be motivated towards generation of the extra sales, so that he can receive

maximum monetary bonus. Along with this, he can also take equivalent time off during the week

day, if he works on Sunday as a non-monetary reward. By this, the working hours of the super

visor will not increase, even he gets extra benefit on Sunday. Therefore, on the basis of above

aspect, it can be said that manager’s pay deal at C&T regarding his bonus and time off is likely

to serve as a motivation.

QUESTION 3

Promotion means the activities carried out by the company, by which it can communicate about

its goods, services, products to its customers or users. It is planning to make society attract,

aware, and encourage for buy the products (Schmid, Grosche, and Mayrhofer, 2016). There are

several types of promotional activities, which assist the company for improvising its

performance. In this aspect, advertisements, trade discounts, incentives, schemes, and some other

tools helps the company to promote their product (Ryoo, Jeon, and Lee, 2016). In the given case,

the company offering significant price discount on Sunday as part of their promotional strategies.

Price discount is the general method, by which customers can easily be attracted. It is the right

thing, by which company can enhanced its sales on Sunday. But at the same time, it should

consider about its profitability. Further, significant discount leads to negative aspects regarding

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the quality of products, as customer may think adverse if the price of product is very low. By

considering all the above aspect, the company should offer substantial price discount and

promotions on Sunday.

QUESTION 4

Pricing strategies is related with the determination of the price of product. The price of the

product is not same trough out the entire life cycle of the product. In the present case, subsidiary

company of the GTZ, PAX is launching a new product in the market. It is the new product and

has several features. This product will enhance the effectiveness of the garages; therefore it is

likely that, the demand of the product gradually increase. Further, at present there is no

competitor of this product in the market, and it is predicted that, at least six month will require

for the development of this product by competitors. On the basis of the facts, it is recommended

that, PAX should adopt the price skimming policy for its new product. In this case, the company

keep the price of product high, because of its uniqueness (Kireyev, Kumar,and Ofek, 2017). By

this, company can maximize its profit. After passing of time, as the competitor will enter,

company should decrease the price for capturing market. On the other hand, due to experience

curve, cost will reduce to some extent; therefore even by reduction of price, company can earn

good return (Wu, Deng, and Jiang, 2018).

QUESTION 5

Computation of the profit maximizing selling price per unit, using the data supplied by the

Finance Director at PAX

Table 2 Computation of selling price

considering all the above aspect, the company should offer substantial price discount and

promotions on Sunday.

QUESTION 4

Pricing strategies is related with the determination of the price of product. The price of the

product is not same trough out the entire life cycle of the product. In the present case, subsidiary

company of the GTZ, PAX is launching a new product in the market. It is the new product and

has several features. This product will enhance the effectiveness of the garages; therefore it is

likely that, the demand of the product gradually increase. Further, at present there is no

competitor of this product in the market, and it is predicted that, at least six month will require

for the development of this product by competitors. On the basis of the facts, it is recommended

that, PAX should adopt the price skimming policy for its new product. In this case, the company

keep the price of product high, because of its uniqueness (Kireyev, Kumar,and Ofek, 2017). By

this, company can maximize its profit. After passing of time, as the competitor will enter,

company should decrease the price for capturing market. On the other hand, due to experience

curve, cost will reduce to some extent; therefore even by reduction of price, company can earn

good return (Wu, Deng, and Jiang, 2018).

QUESTION 5

Computation of the profit maximizing selling price per unit, using the data supplied by the

Finance Director at PAX

Table 2 Computation of selling price

Given that,

P=a-bx

Mr=a-2bx

P denotes the selling price

X is the total demand at this selling price

a is the maximum price

b is the proportionate change in price as the demand of product changes

Thus,

b= change in price/Change in demand

Change in Price 5

Change in Demand 250

B 0.02

Similarly

A 48

p=48-0.02d

By addition of 0.02 and –p both side

0.02d= 48 – p

Apply multiplication of 100 both side

d = 4800-200p

If

MR=MC

then, profit will be maximized

MR = a-2bx

MR= 48- 0.04d

Long term variable cost 320

Put this value in above equation, we get

320= 48-0.04d

By solving above equation,

d=6800units

thus,

p= 48-0.02d

p= 88 per unit

QUESTION 6

In the present report, it is stated that competitor will require at least six month for development

of the new product. At the introduction phase of the product, the company adopt price skimming

policy as there is no competitor, however, after six month company should reconsider its price

P=a-bx

Mr=a-2bx

P denotes the selling price

X is the total demand at this selling price

a is the maximum price

b is the proportionate change in price as the demand of product changes

Thus,

b= change in price/Change in demand

Change in Price 5

Change in Demand 250

B 0.02

Similarly

A 48

p=48-0.02d

By addition of 0.02 and –p both side

0.02d= 48 – p

Apply multiplication of 100 both side

d = 4800-200p

If

MR=MC

then, profit will be maximized

MR = a-2bx

MR= 48- 0.04d

Long term variable cost 320

Put this value in above equation, we get

320= 48-0.04d

By solving above equation,

d=6800units

thus,

p= 48-0.02d

p= 88 per unit

QUESTION 6

In the present report, it is stated that competitor will require at least six month for development

of the new product. At the introduction phase of the product, the company adopt price skimming

policy as there is no competitor, however, after six month company should reconsider its price

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

policy, because if the company still charge higher price as compare with the competitor’s price,

then the customer will shifted towards the other sellers. Therefore, it is advisable for the

company to decrease its selling price, to maintain their customers. Therefore for hitting

competitor, profit maximization, and holding consumers are the possible reason for the PAX to

reconsider its pricing policy, that the circuit board has been available in the market for six

months.

QUESTION 7

A Life cycle of the product is consisting with the four stages, namely, introduction, growth,

maturity, and decline. Introduction stage, starts from launching the new product in the market,

when the sales of product increasing at the faster rate, then it is known as growth stage. Further,

when the sales reach at their highest point, but the rate of growth low dawn because of the

market saturation, then it is maturity stage of product. Moreover, when the sales begin to

decrease, then it is the declining and last stage of product life cycle (Restuccia et al. 2016).

In the product life cycle of PLAYY product, at the introduction phase, the selling price of the

product high, production cost is high, and selling and marketing cost is also high. The reason

behind the same is the product is unique, and at the introduction stage the competition is less.

Further in the growth stage the selling price of the product should be reduces, production cost

also reduced, and marketing and advertising cost may remain same. This was due to the

competition in market, and reduction of production cost is because of the learning curve effect.

For promotion of product, company should spend on marketing and advertising techniques. In

the maturity stage, the selling price decreased, production cost may remain same, and rise in the

advertising and marketing cost for enhancing the product in new market. At the last stage, that is

then the customer will shifted towards the other sellers. Therefore, it is advisable for the

company to decrease its selling price, to maintain their customers. Therefore for hitting

competitor, profit maximization, and holding consumers are the possible reason for the PAX to

reconsider its pricing policy, that the circuit board has been available in the market for six

months.

QUESTION 7

A Life cycle of the product is consisting with the four stages, namely, introduction, growth,

maturity, and decline. Introduction stage, starts from launching the new product in the market,

when the sales of product increasing at the faster rate, then it is known as growth stage. Further,

when the sales reach at their highest point, but the rate of growth low dawn because of the

market saturation, then it is maturity stage of product. Moreover, when the sales begin to

decrease, then it is the declining and last stage of product life cycle (Restuccia et al. 2016).

In the product life cycle of PLAYY product, at the introduction phase, the selling price of the

product high, production cost is high, and selling and marketing cost is also high. The reason

behind the same is the product is unique, and at the introduction stage the competition is less.

Further in the growth stage the selling price of the product should be reduces, production cost

also reduced, and marketing and advertising cost may remain same. This was due to the

competition in market, and reduction of production cost is because of the learning curve effect.

For promotion of product, company should spend on marketing and advertising techniques. In

the maturity stage, the selling price decreased, production cost may remain same, and rise in the

advertising and marketing cost for enhancing the product in new market. At the last stage, that is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

declining stage, the selling price reduced, production cost remain same, and rise in the marketing

and selling cost (Wu et al. 2017).

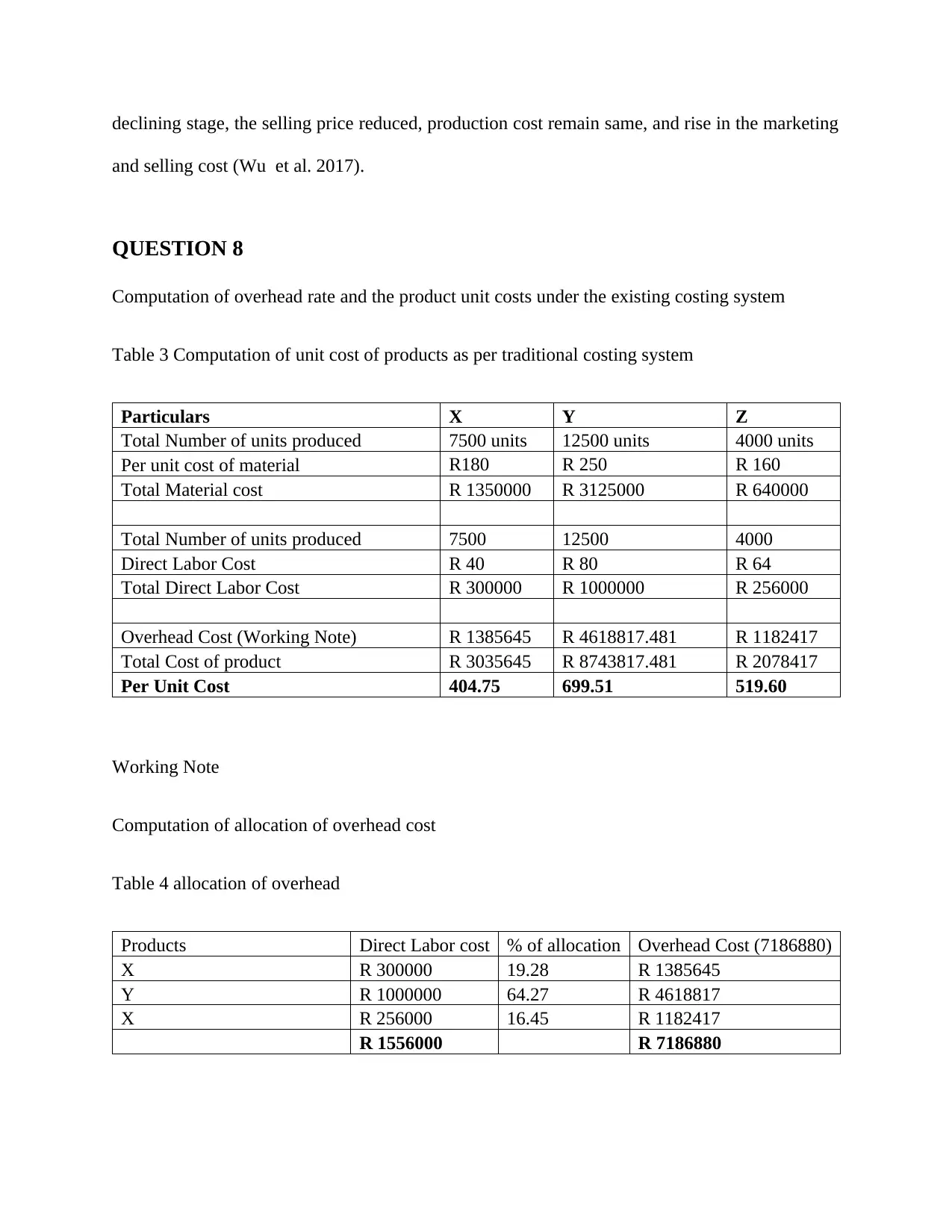

QUESTION 8

Computation of overhead rate and the product unit costs under the existing costing system

Table 3 Computation of unit cost of products as per traditional costing system

Particulars X Y Z

Total Number of units produced 7500 units 12500 units 4000 units

Per unit cost of material R180 R 250 R 160

Total Material cost R 1350000 R 3125000 R 640000

Total Number of units produced 7500 12500 4000

Direct Labor Cost R 40 R 80 R 64

Total Direct Labor Cost R 300000 R 1000000 R 256000

Overhead Cost (Working Note) R 1385645 R 4618817.481 R 1182417

Total Cost of product R 3035645 R 8743817.481 R 2078417

Per Unit Cost 404.75 699.51 519.60

Working Note

Computation of allocation of overhead cost

Table 4 allocation of overhead

Products Direct Labor cost % of allocation Overhead Cost (7186880)

X R 300000 19.28 R 1385645

Y R 1000000 64.27 R 4618817

X R 256000 16.45 R 1182417

R 1556000 R 7186880

and selling cost (Wu et al. 2017).

QUESTION 8

Computation of overhead rate and the product unit costs under the existing costing system

Table 3 Computation of unit cost of products as per traditional costing system

Particulars X Y Z

Total Number of units produced 7500 units 12500 units 4000 units

Per unit cost of material R180 R 250 R 160

Total Material cost R 1350000 R 3125000 R 640000

Total Number of units produced 7500 12500 4000

Direct Labor Cost R 40 R 80 R 64

Total Direct Labor Cost R 300000 R 1000000 R 256000

Overhead Cost (Working Note) R 1385645 R 4618817.481 R 1182417

Total Cost of product R 3035645 R 8743817.481 R 2078417

Per Unit Cost 404.75 699.51 519.60

Working Note

Computation of allocation of overhead cost

Table 4 allocation of overhead

Products Direct Labor cost % of allocation Overhead Cost (7186880)

X R 300000 19.28 R 1385645

Y R 1000000 64.27 R 4618817

X R 256000 16.45 R 1182417

R 1556000 R 7186880

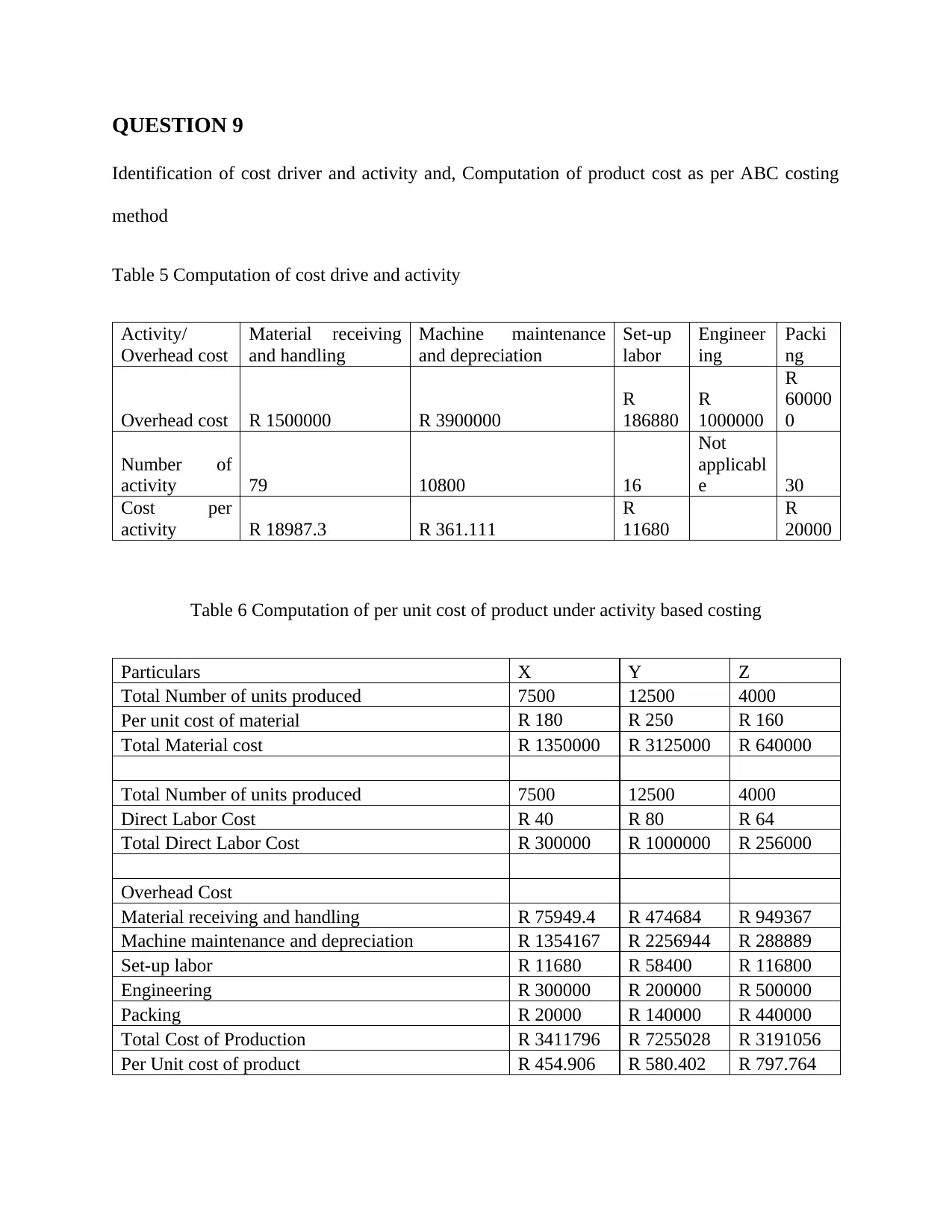

QUESTION 9

Identification of cost driver and activity and, Computation of product cost as per ABC costing

method

Table 5 Computation of cost drive and activity

Activity/

Overhead cost

Material receiving

and handling

Machine maintenance

and depreciation

Set-up

labor

Engineer

ing

Packi

ng

Overhead cost R 1500000 R 3900000

R

186880

R

1000000

R

60000

0

Number of

activity 79 10800 16

Not

applicabl

e 30

Cost per

activity R 18987.3 R 361.111

R

11680

R

20000

Table 6 Computation of per unit cost of product under activity based costing

Particulars X Y Z

Total Number of units produced 7500 12500 4000

Per unit cost of material R 180 R 250 R 160

Total Material cost R 1350000 R 3125000 R 640000

Total Number of units produced 7500 12500 4000

Direct Labor Cost R 40 R 80 R 64

Total Direct Labor Cost R 300000 R 1000000 R 256000

Overhead Cost

Material receiving and handling R 75949.4 R 474684 R 949367

Machine maintenance and depreciation R 1354167 R 2256944 R 288889

Set-up labor R 11680 R 58400 R 116800

Engineering R 300000 R 200000 R 500000

Packing R 20000 R 140000 R 440000

Total Cost of Production R 3411796 R 7255028 R 3191056

Per Unit cost of product R 454.906 R 580.402 R 797.764

Identification of cost driver and activity and, Computation of product cost as per ABC costing

method

Table 5 Computation of cost drive and activity

Activity/

Overhead cost

Material receiving

and handling

Machine maintenance

and depreciation

Set-up

labor

Engineer

ing

Packi

ng

Overhead cost R 1500000 R 3900000

R

186880

R

1000000

R

60000

0

Number of

activity 79 10800 16

Not

applicabl

e 30

Cost per

activity R 18987.3 R 361.111

R

11680

R

20000

Table 6 Computation of per unit cost of product under activity based costing

Particulars X Y Z

Total Number of units produced 7500 12500 4000

Per unit cost of material R 180 R 250 R 160

Total Material cost R 1350000 R 3125000 R 640000

Total Number of units produced 7500 12500 4000

Direct Labor Cost R 40 R 80 R 64

Total Direct Labor Cost R 300000 R 1000000 R 256000

Overhead Cost

Material receiving and handling R 75949.4 R 474684 R 949367

Machine maintenance and depreciation R 1354167 R 2256944 R 288889

Set-up labor R 11680 R 58400 R 116800

Engineering R 300000 R 200000 R 500000

Packing R 20000 R 140000 R 440000

Total Cost of Production R 3411796 R 7255028 R 3191056

Per Unit cost of product R 454.906 R 580.402 R 797.764

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

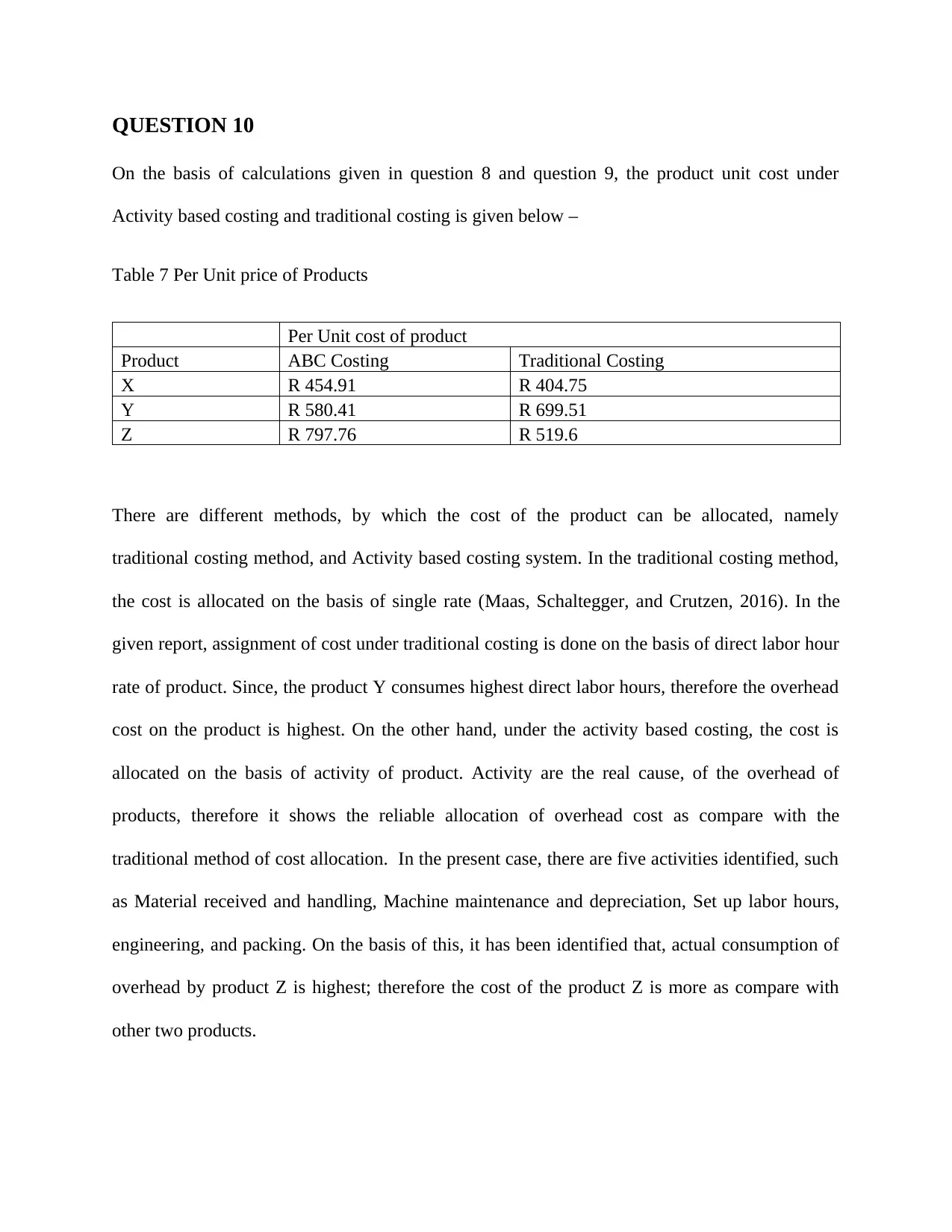

QUESTION 10

On the basis of calculations given in question 8 and question 9, the product unit cost under

Activity based costing and traditional costing is given below –

Table 7 Per Unit price of Products

Per Unit cost of product

Product ABC Costing Traditional Costing

X R 454.91 R 404.75

Y R 580.41 R 699.51

Z R 797.76 R 519.6

There are different methods, by which the cost of the product can be allocated, namely

traditional costing method, and Activity based costing system. In the traditional costing method,

the cost is allocated on the basis of single rate (Maas, Schaltegger, and Crutzen, 2016). In the

given report, assignment of cost under traditional costing is done on the basis of direct labor hour

rate of product. Since, the product Y consumes highest direct labor hours, therefore the overhead

cost on the product is highest. On the other hand, under the activity based costing, the cost is

allocated on the basis of activity of product. Activity are the real cause, of the overhead of

products, therefore it shows the reliable allocation of overhead cost as compare with the

traditional method of cost allocation. In the present case, there are five activities identified, such

as Material received and handling, Machine maintenance and depreciation, Set up labor hours,

engineering, and packing. On the basis of this, it has been identified that, actual consumption of

overhead by product Z is highest; therefore the cost of the product Z is more as compare with

other two products.

On the basis of calculations given in question 8 and question 9, the product unit cost under

Activity based costing and traditional costing is given below –

Table 7 Per Unit price of Products

Per Unit cost of product

Product ABC Costing Traditional Costing

X R 454.91 R 404.75

Y R 580.41 R 699.51

Z R 797.76 R 519.6

There are different methods, by which the cost of the product can be allocated, namely

traditional costing method, and Activity based costing system. In the traditional costing method,

the cost is allocated on the basis of single rate (Maas, Schaltegger, and Crutzen, 2016). In the

given report, assignment of cost under traditional costing is done on the basis of direct labor hour

rate of product. Since, the product Y consumes highest direct labor hours, therefore the overhead

cost on the product is highest. On the other hand, under the activity based costing, the cost is

allocated on the basis of activity of product. Activity are the real cause, of the overhead of

products, therefore it shows the reliable allocation of overhead cost as compare with the

traditional method of cost allocation. In the present case, there are five activities identified, such

as Material received and handling, Machine maintenance and depreciation, Set up labor hours,

engineering, and packing. On the basis of this, it has been identified that, actual consumption of

overhead by product Z is highest; therefore the cost of the product Z is more as compare with

other two products.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Barrick, M.R., Thurgood, G.R., Smith, T.A. and Courtright, S.H., 2015. Collective

organizational engagement: Linking motivational antecedents, strategic implementation, and

firm performance. Academy of Management journal, 58(1), pp.111-135.

Kireyev, P., Kumar, V. and Ofek, E., 2017. Match your own price? self-matching as a retailer’s

multichannel pricing strategy. Marketing Science, 36(6), pp.908-930.

Kontoghiorghes, C., 2016. Linking high performance organizational culture and talent

management: satisfaction/motivation and organizational commitment as mediators. The

International Journal of Human Resource Management, 27(16), pp.1833-1853.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production, 136, pp.237-

248.

Restuccia, M., de Brentani, U., Legoux, R. and Ouellet, J.F., 2016. Product Life‐Cycle

Management and Distributor Contribution to New Product Development. Journal of Product

Innovation Management, 33(1), pp.69-89.

Ryoo, J., Jeon, J.Q. and Lee, C., 2016. Do marketing activities enhance firm value? Evidence

from M&A transactions. European Management Journal, 34(3), pp.243-257.

Schmid, S., Grosche, P. and Mayrhofer, U., 2016. Configuration and coordination of

international marketing activities. International Business Review, 25(2), pp.535-547.

Wu, J., Chang, C.T., Teng, J.T. and Lai, K.K., 2017. Optimal order quantity and selling price

over a product life cycle with deterioration rate linked to expiration date. International Journal

of Production Economics, 193, pp.343-351.

Wu, L., Deng, S. and Jiang, X., 2018. Sampling and pricing strategy under

competition. Omega, 80, pp.192-208.

Barrick, M.R., Thurgood, G.R., Smith, T.A. and Courtright, S.H., 2015. Collective

organizational engagement: Linking motivational antecedents, strategic implementation, and

firm performance. Academy of Management journal, 58(1), pp.111-135.

Kireyev, P., Kumar, V. and Ofek, E., 2017. Match your own price? self-matching as a retailer’s

multichannel pricing strategy. Marketing Science, 36(6), pp.908-930.

Kontoghiorghes, C., 2016. Linking high performance organizational culture and talent

management: satisfaction/motivation and organizational commitment as mediators. The

International Journal of Human Resource Management, 27(16), pp.1833-1853.

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production, 136, pp.237-

248.

Restuccia, M., de Brentani, U., Legoux, R. and Ouellet, J.F., 2016. Product Life‐Cycle

Management and Distributor Contribution to New Product Development. Journal of Product

Innovation Management, 33(1), pp.69-89.

Ryoo, J., Jeon, J.Q. and Lee, C., 2016. Do marketing activities enhance firm value? Evidence

from M&A transactions. European Management Journal, 34(3), pp.243-257.

Schmid, S., Grosche, P. and Mayrhofer, U., 2016. Configuration and coordination of

international marketing activities. International Business Review, 25(2), pp.535-547.

Wu, J., Chang, C.T., Teng, J.T. and Lai, K.K., 2017. Optimal order quantity and selling price

over a product life cycle with deterioration rate linked to expiration date. International Journal

of Production Economics, 193, pp.343-351.

Wu, L., Deng, S. and Jiang, X., 2018. Sampling and pricing strategy under

competition. Omega, 80, pp.192-208.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.