Assignment 1: Financial and Cost Accounting Analysis

VerifiedAdded on 2023/01/17

|10

|1468

|97

Homework Assignment

AI Summary

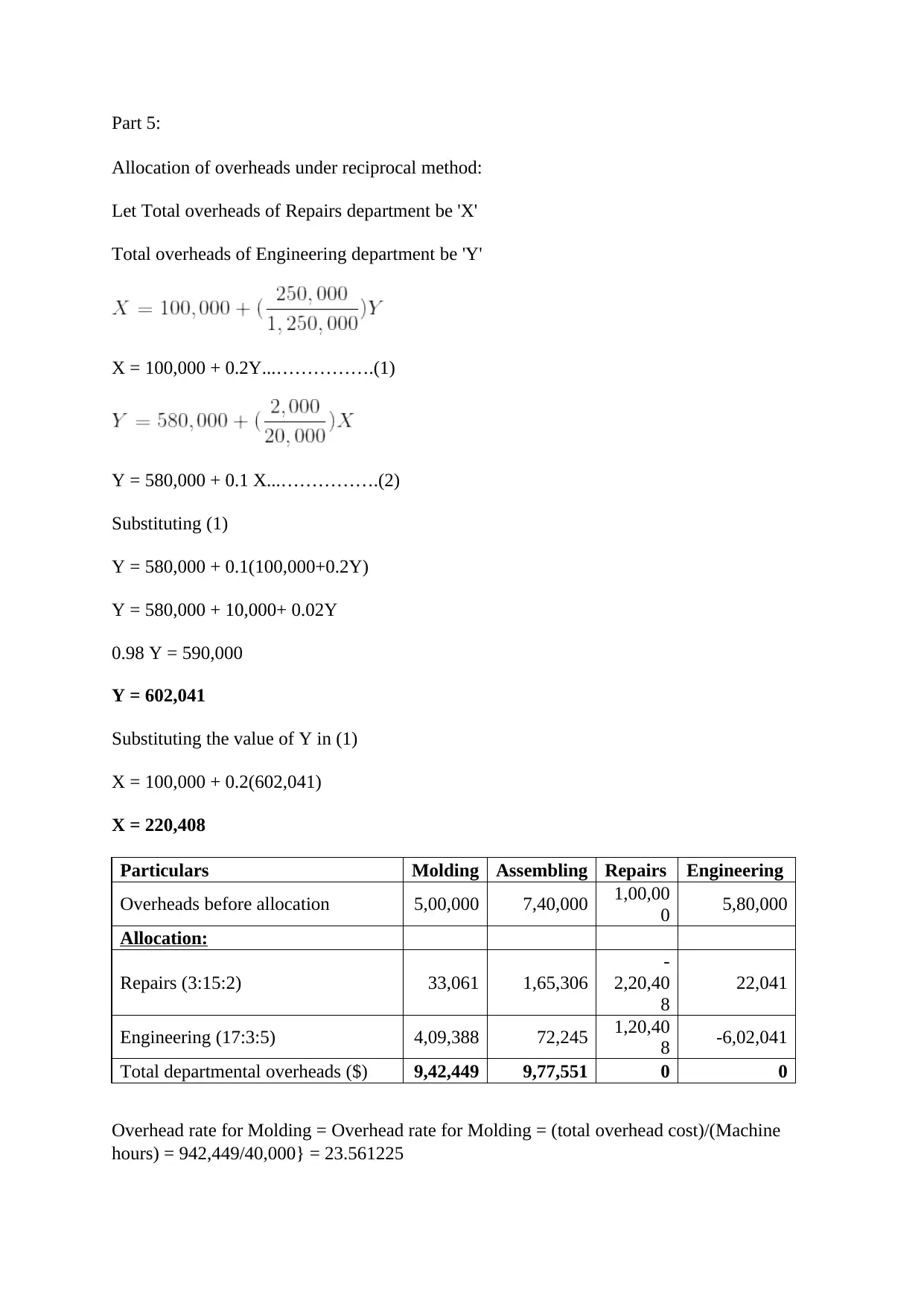

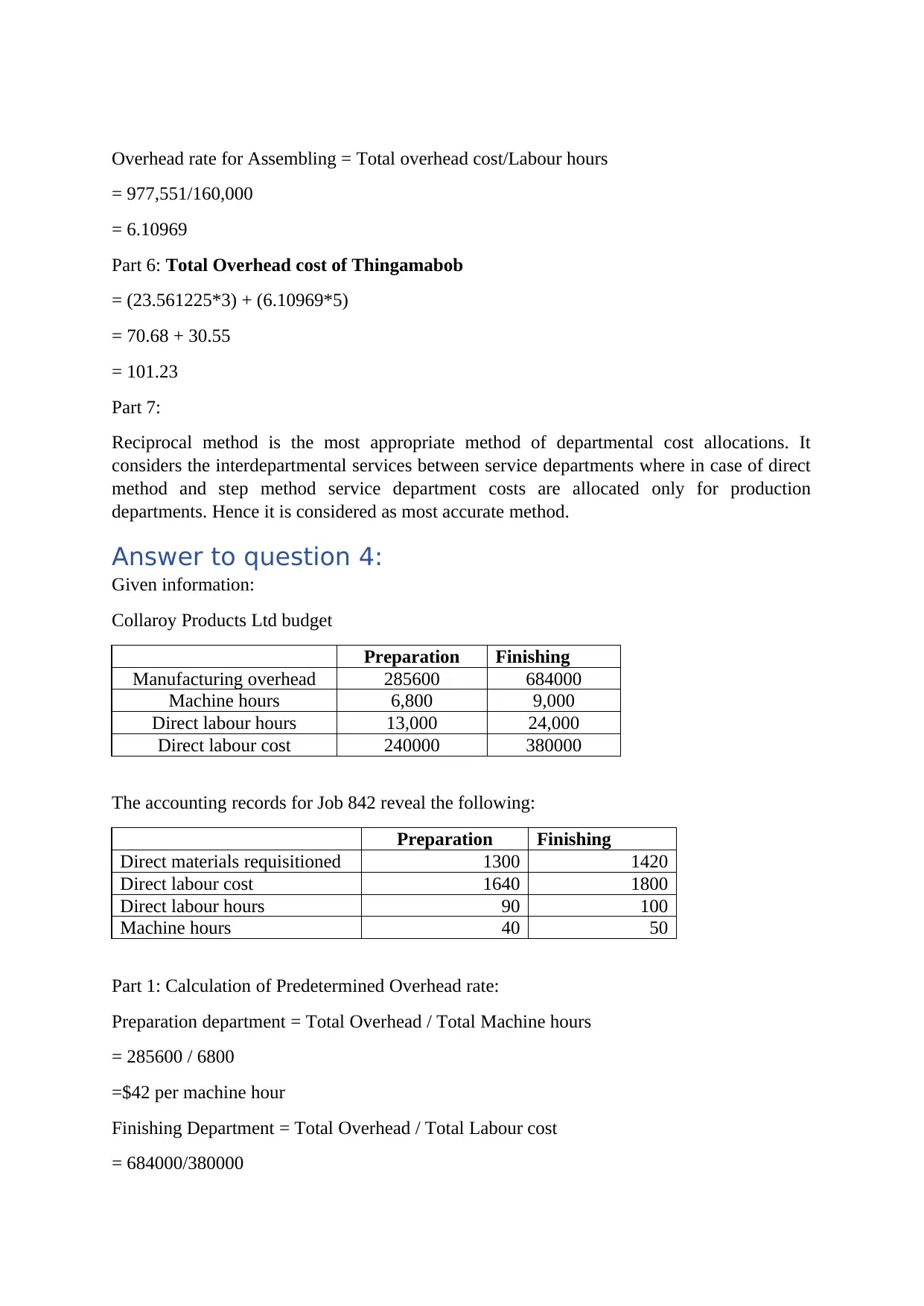

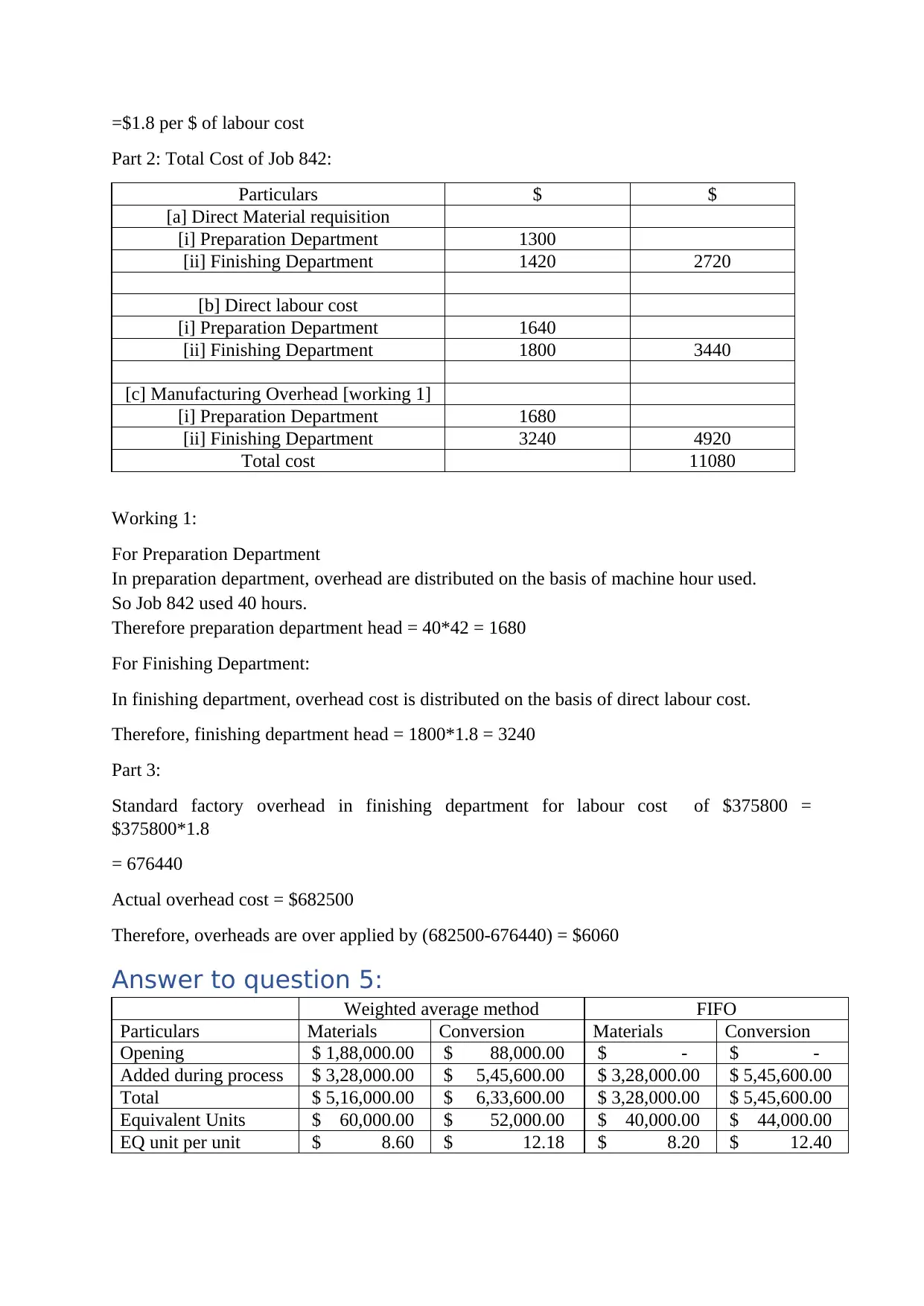

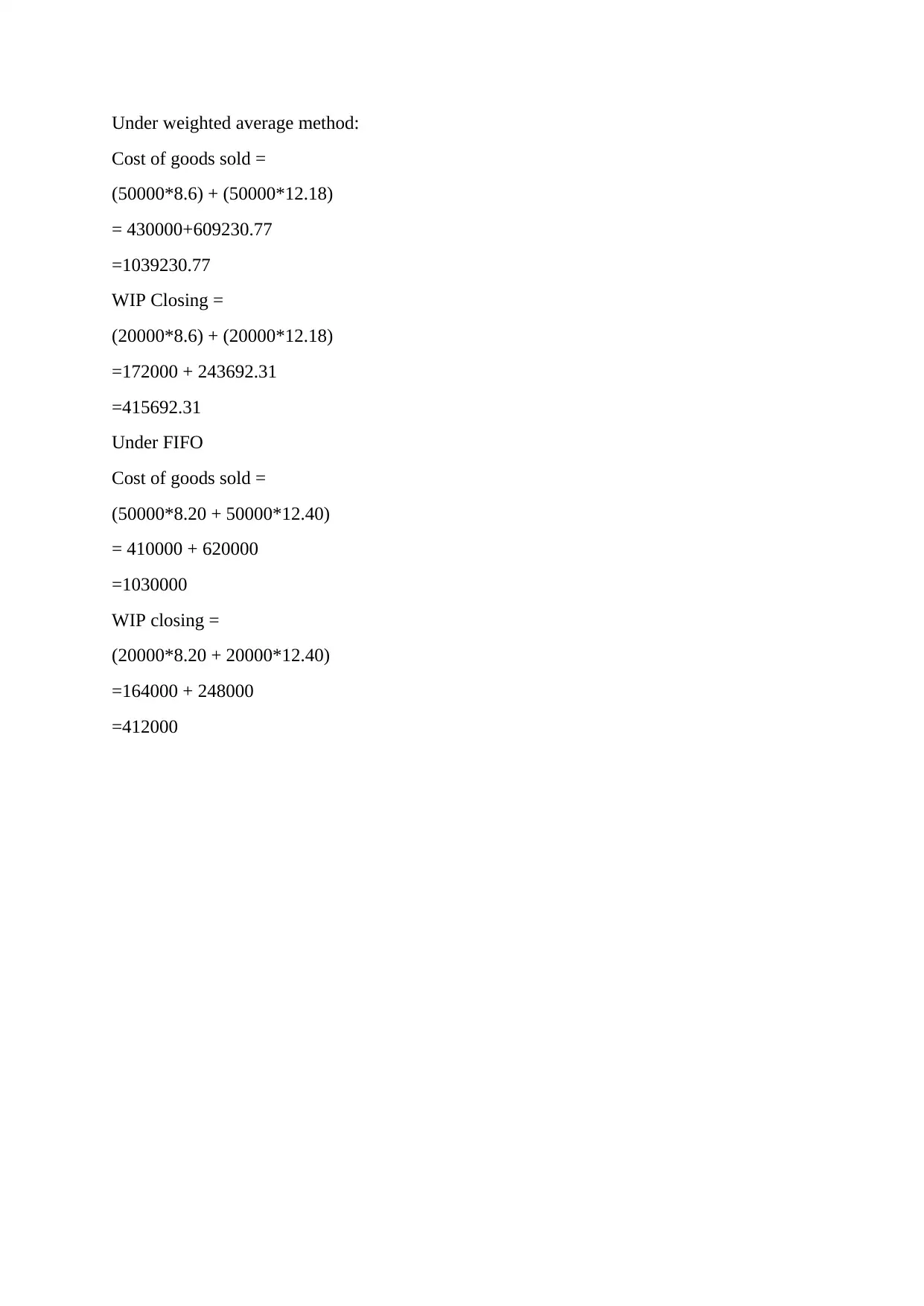

This assignment solution addresses several key concepts in cost and financial accounting. It begins with a value chain analysis, evaluating its framework for management accounting issues within an organization. The solution then delves into cost of manufacturing statements, detailing the calculation of the cost of goods manufactured, including direct materials, direct labor, and overhead costs. Further, the assignment explores departmental cost allocation using direct and step methods, along with the reciprocal method. The solution also covers the calculation of predetermined overhead rates and applying them to job costing, along with an analysis of over-applied overhead. Finally, the assignment concludes with a detailed analysis of process costing, comparing the weighted average and FIFO methods for cost of goods sold and work-in-progress inventory valuation.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.