Financial Management Assignment: Project Analysis and Tax Liability

VerifiedAdded on 2022/08/26

|6

|908

|63

Homework Assignment

AI Summary

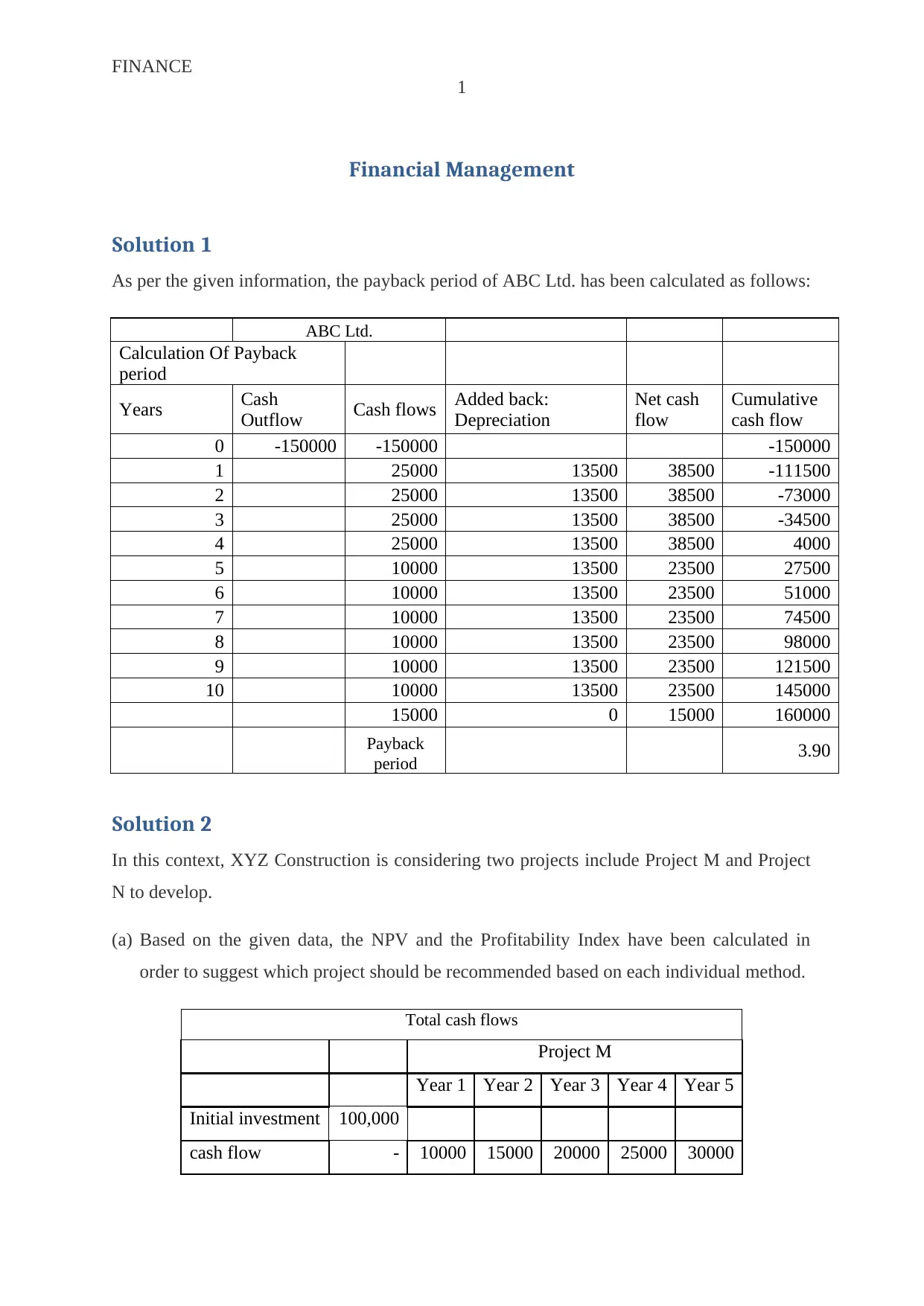

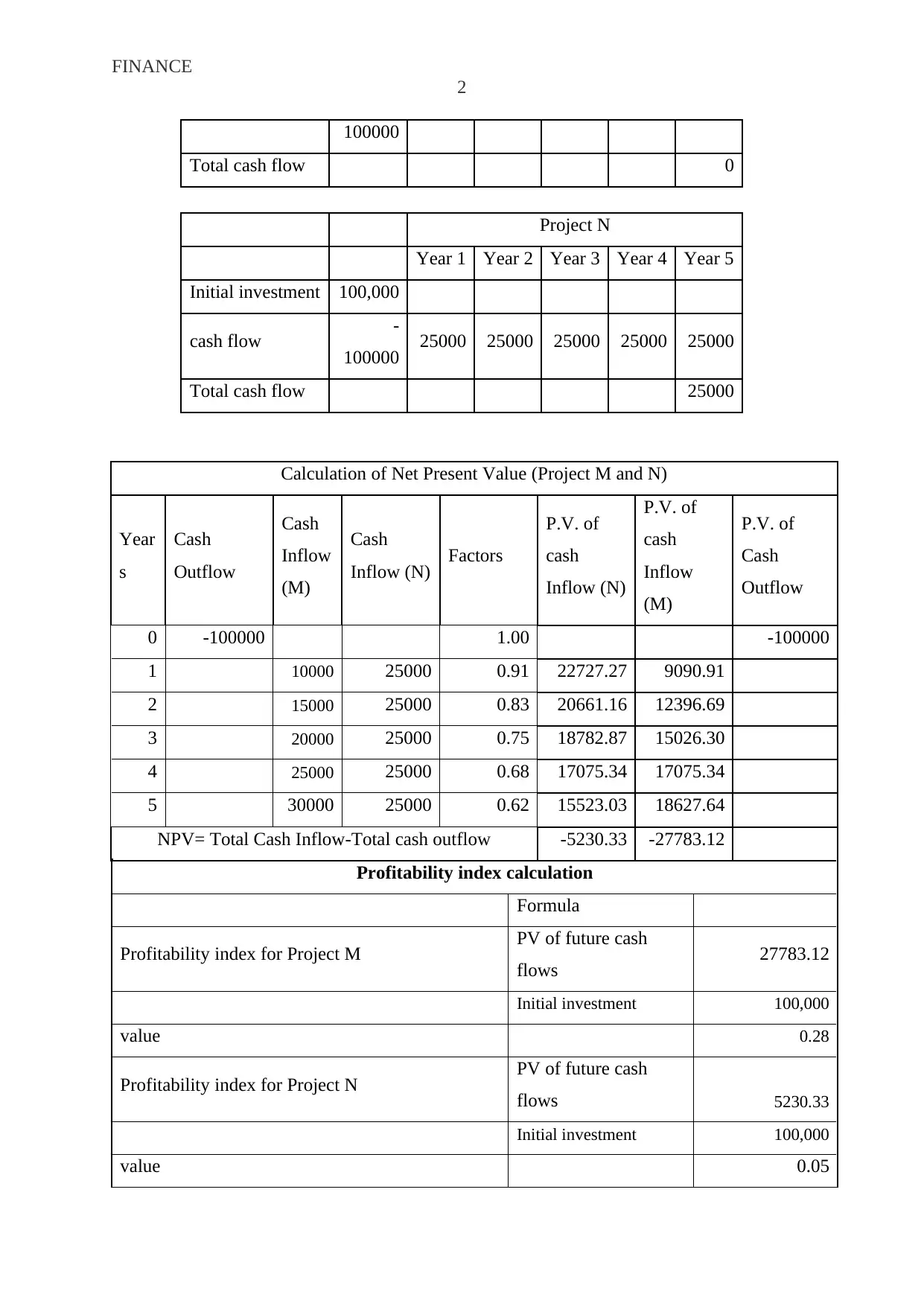

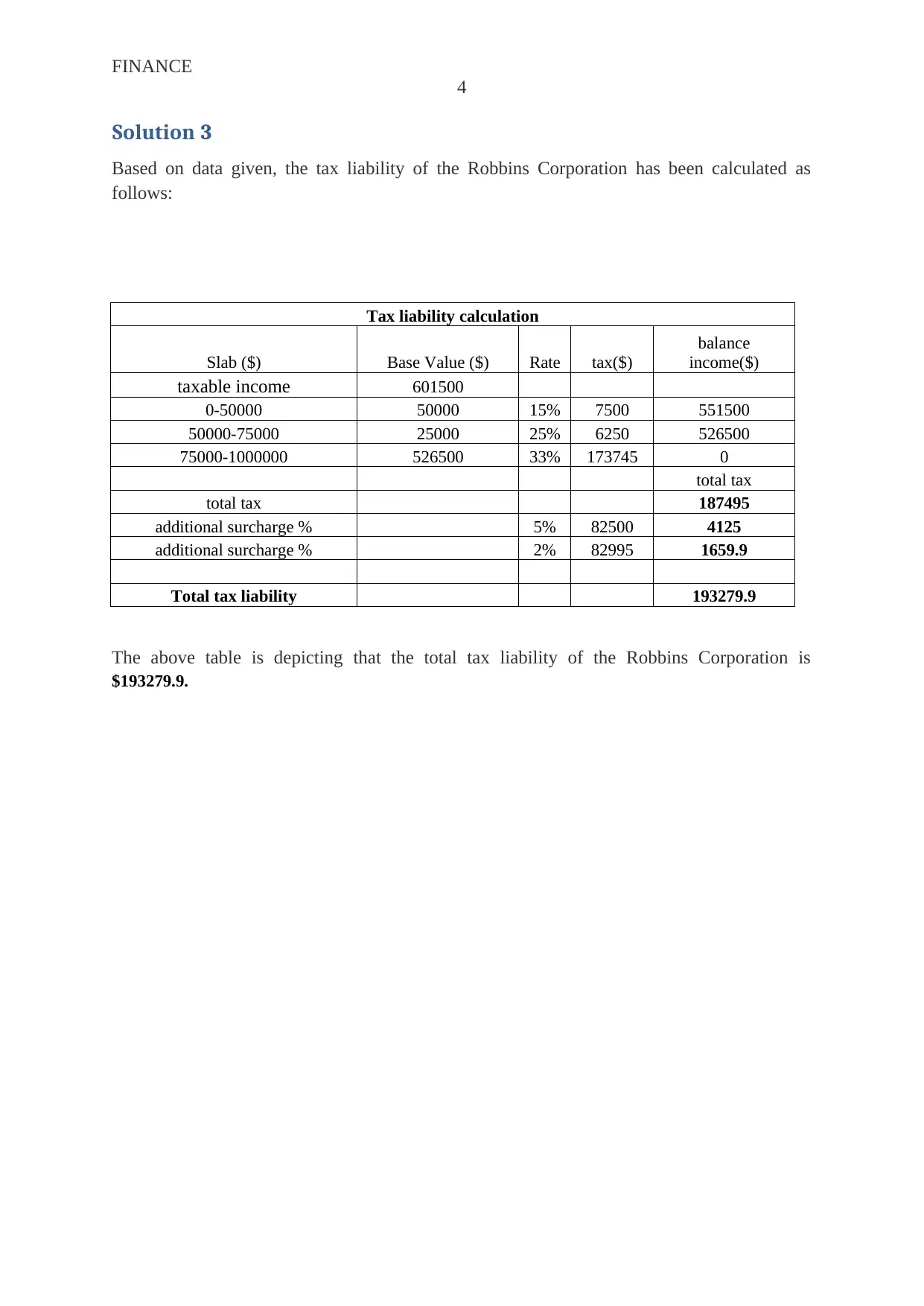

This financial management assignment solution provides detailed calculations and explanations for three key problems. The first problem calculates the payback period for ABC Ltd., considering cash outflows, inflows, and depreciation. The second problem analyzes two projects, M and N, using Net Present Value (NPV) and profitability index to determine the best investment. It also discusses the key decisions a finance manager must make, including working capital management, dividend policies, investment and financing decisions. The third problem calculates the tax liability of the Robbins Corporation based on its taxable income and the given corporate tax rates. The document includes the calculations, formulas, and relevant references.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.