IFRS 16: Financial Reporting Implications for Lessees, Lessors, & SIA

VerifiedAdded on 2020/04/21

|13

|2953

|84

Report

AI Summary

This report provides a detailed analysis of IFRS 16, the new lease accounting standard, and its implications for financial reporting. It covers the changes in accounting requirements for both lessees and lessors, highlighting the shift from operating and finance leases to a single lessee accounting model. The report examines the effects of IFRS 16 on key financial statements, including the balance sheet, income statement, and cash flow statement, with a specific focus on how these changes impact companies with significant off-balance-sheet leases. Furthermore, the report includes a case study of Singapore Airlines Limited, illustrating the practical application of IFRS 16 and its potential effects on the company's financial position and performance. The analysis considers the impact on reported profits, debts, gearing ratios, EBITDA, and return on capital employed, providing a comprehensive overview of the new lease standard's implications.

IFRS 16

Accounting and Financial Reporting

Running head: Accounting and financial reporting 0

Accounting and Financial Reporting

Running head: Accounting and financial reporting 0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Financial Reporting 1

Table of Contents

Table of Figure................................................................................................................................2

Introduction......................................................................................................................................3

Changes to Accounting Requirement..............................................................................................3

Implications for Lessee................................................................................................................4

Implication on Lessor...................................................................................................................5

Effects on Financial Statements.......................................................................................................5

Effects on Balance Sheet..............................................................................................................6

Effects on Income Statement.......................................................................................................7

Effects on Cash Flow Statement..................................................................................................8

Effect on Singapore Airlines Limited..............................................................................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Table of Contents

Table of Figure................................................................................................................................2

Introduction......................................................................................................................................3

Changes to Accounting Requirement..............................................................................................3

Implications for Lessee................................................................................................................4

Implication on Lessor...................................................................................................................5

Effects on Financial Statements.......................................................................................................5

Effects on Balance Sheet..............................................................................................................6

Effects on Income Statement.......................................................................................................7

Effects on Cash Flow Statement..................................................................................................8

Effect on Singapore Airlines Limited..............................................................................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Accounting and Financial Reporting 2

Table of Figure

Figure 1Implications of IFRS 16.....................................................................................................5

Figure 2 Effect on Balance Sheet....................................................................................................7

Figure 3 Effect on Income Statement..............................................................................................8

Figure 4 Financial Statements of Singapore Airline Ltd.................................................................9

Table of Figure

Figure 1Implications of IFRS 16.....................................................................................................5

Figure 2 Effect on Balance Sheet....................................................................................................7

Figure 3 Effect on Income Statement..............................................................................................8

Figure 4 Financial Statements of Singapore Airline Ltd.................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting and Financial Reporting 3

Introduction

A lease is a written agreement between owner of the property and a person or an entity who will

use the said property for a specified period of time on a specified payment. Leases can be of

shorter period and longer period as well where owner of the property is lessor and the person or

business who is using the property is the lessee. The lease contracts involves a series of

payments so the question arise that how the lease and its related payments or installments will be

accounted by the lessee and lessor. FASB and IASB are about to issue a common reporting

standard of financial accounting which will replace the US accounting rules (Cotter, 2012).

IFRS 16 introducing a single lessee accounting model and effective on or after 1 January 2019,

for annual reporting periods and permission for earlier application of IFRS 15 has been granted.

This lease standard is introduced with an objective to report the information which represents the

lease transactions and supports by providing the basis to financial statement users in order to

gage the value and vagueness of cash flows that arise from a lease. IFRS 16 has few transition

provisions in the existing finance leases and operating leases where the financial leases will

remain to be treated as finance leases and operating leases has the option for a full or a limited

reflective restatement in relation to fulfill the requirements of IFRS 16 (Iasplus.com, 2017).

In the following assignment the new requirements of lease standard for both lessee and lessor as

what changes it brings to the existing requirements. The effects on financial statement and a

company who is listed in Singapore exchange and the company chosen for the same is Singapore

Airline Ltd. Which is a world’s largest passenger aircraft.

Changes to Accounting Requirement

The introduction of IFRS 16 bring significant changes in lessee and lessor accounting but

comparatively the changes are more in lessee accounting which is of great importance. However

the changes in accounting for intermediate lessor, those who sublease assets through headlease

and those particular headlease act currently as operating lease. This is done because the assets

and liabilities come to the balance sheet and the classification of the sublease will be determined

by taking the reference of intermediate lessor’s rights on the use of asset. And the implications

for lessees are need to be discussed thoroughly as the percentage of change in accounting

requirement are more to the lessee (Byard, and 2011).

Introduction

A lease is a written agreement between owner of the property and a person or an entity who will

use the said property for a specified period of time on a specified payment. Leases can be of

shorter period and longer period as well where owner of the property is lessor and the person or

business who is using the property is the lessee. The lease contracts involves a series of

payments so the question arise that how the lease and its related payments or installments will be

accounted by the lessee and lessor. FASB and IASB are about to issue a common reporting

standard of financial accounting which will replace the US accounting rules (Cotter, 2012).

IFRS 16 introducing a single lessee accounting model and effective on or after 1 January 2019,

for annual reporting periods and permission for earlier application of IFRS 15 has been granted.

This lease standard is introduced with an objective to report the information which represents the

lease transactions and supports by providing the basis to financial statement users in order to

gage the value and vagueness of cash flows that arise from a lease. IFRS 16 has few transition

provisions in the existing finance leases and operating leases where the financial leases will

remain to be treated as finance leases and operating leases has the option for a full or a limited

reflective restatement in relation to fulfill the requirements of IFRS 16 (Iasplus.com, 2017).

In the following assignment the new requirements of lease standard for both lessee and lessor as

what changes it brings to the existing requirements. The effects on financial statement and a

company who is listed in Singapore exchange and the company chosen for the same is Singapore

Airline Ltd. Which is a world’s largest passenger aircraft.

Changes to Accounting Requirement

The introduction of IFRS 16 bring significant changes in lessee and lessor accounting but

comparatively the changes are more in lessee accounting which is of great importance. However

the changes in accounting for intermediate lessor, those who sublease assets through headlease

and those particular headlease act currently as operating lease. This is done because the assets

and liabilities come to the balance sheet and the classification of the sublease will be determined

by taking the reference of intermediate lessor’s rights on the use of asset. And the implications

for lessees are need to be discussed thoroughly as the percentage of change in accounting

requirement are more to the lessee (Byard, and 2011).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Financial Reporting 4

Implications for Lessee

Lessees who adopt IFRS 16 in their accounting have to make changes which are substantial in

nature, likewise there will be no more division in between finance leases and operating leases as

they are being eliminated and can adopt the current finance lease methodologies for all types of

leases. Basically a single method model for all accounting, there are no changes made in the

current rules about calculating the term of lease and it has decide by IASB whenever there are

extension and termination options available. IASB has also allowed leases for a term of not more

than 12 months and the exclusion has been made from the requirements of IFRS 16 for the leases

who are of low value. The “low value” carries no such definition to it but does indicate the

inclusion of tablet computers and laptops but cars are not included. The leases which are

currently treated as finance leases by lessees in their accounting will be the same there are such

changes made therein until and unless lessee guarantee the residual position of lessor (Ey.com.,

2017).

Nonetheless, currently the accounting for leases as operating leases will be changed for the

affected lessees and the changes are:

In the balance sheet of lessee there will be an asset and a liability;

Depreciation and interest will replace the current straight line rental expense.

Evidently, the asset of lessee represent their rights of use of the underlying leased asset and the

liabilities of the lessee will represent the obligation of lessee to pay future rentals for the

outstanding tenure of the lease.

The principles of accounting for finance leases will be the same, apparently the lease amount in

lessee’s initial balance sheet with a residual value position will be lower than the full payout

lease. The current operating leases experience the change in accounting where the acceleration of

lessee’s recognition of expense can be seen. The depreciation will be straight line and the interest

cost will be charged initially due to which the expense lines will be affected in the income

statement, the companies who are using EBITDA and related performance measures will

experiences changes. The real estate leases which are treated as operating leases currently will

have more impact in their accounting after the introduction of IFRS 16. The leasing companies

and banks will be positioned as lessees. The tangibility and intangibility of assets for capital

Implications for Lessee

Lessees who adopt IFRS 16 in their accounting have to make changes which are substantial in

nature, likewise there will be no more division in between finance leases and operating leases as

they are being eliminated and can adopt the current finance lease methodologies for all types of

leases. Basically a single method model for all accounting, there are no changes made in the

current rules about calculating the term of lease and it has decide by IASB whenever there are

extension and termination options available. IASB has also allowed leases for a term of not more

than 12 months and the exclusion has been made from the requirements of IFRS 16 for the leases

who are of low value. The “low value” carries no such definition to it but does indicate the

inclusion of tablet computers and laptops but cars are not included. The leases which are

currently treated as finance leases by lessees in their accounting will be the same there are such

changes made therein until and unless lessee guarantee the residual position of lessor (Ey.com.,

2017).

Nonetheless, currently the accounting for leases as operating leases will be changed for the

affected lessees and the changes are:

In the balance sheet of lessee there will be an asset and a liability;

Depreciation and interest will replace the current straight line rental expense.

Evidently, the asset of lessee represent their rights of use of the underlying leased asset and the

liabilities of the lessee will represent the obligation of lessee to pay future rentals for the

outstanding tenure of the lease.

The principles of accounting for finance leases will be the same, apparently the lease amount in

lessee’s initial balance sheet with a residual value position will be lower than the full payout

lease. The current operating leases experience the change in accounting where the acceleration of

lessee’s recognition of expense can be seen. The depreciation will be straight line and the interest

cost will be charged initially due to which the expense lines will be affected in the income

statement, the companies who are using EBITDA and related performance measures will

experiences changes. The real estate leases which are treated as operating leases currently will

have more impact in their accounting after the introduction of IFRS 16. The leasing companies

and banks will be positioned as lessees. The tangibility and intangibility of assets for capital

Accounting and Financial Reporting 5

adequacy purposes of the right of use asset on a bank’s balance sheet is still not resolved

(Öztürk, and Serçemeli, 2016).

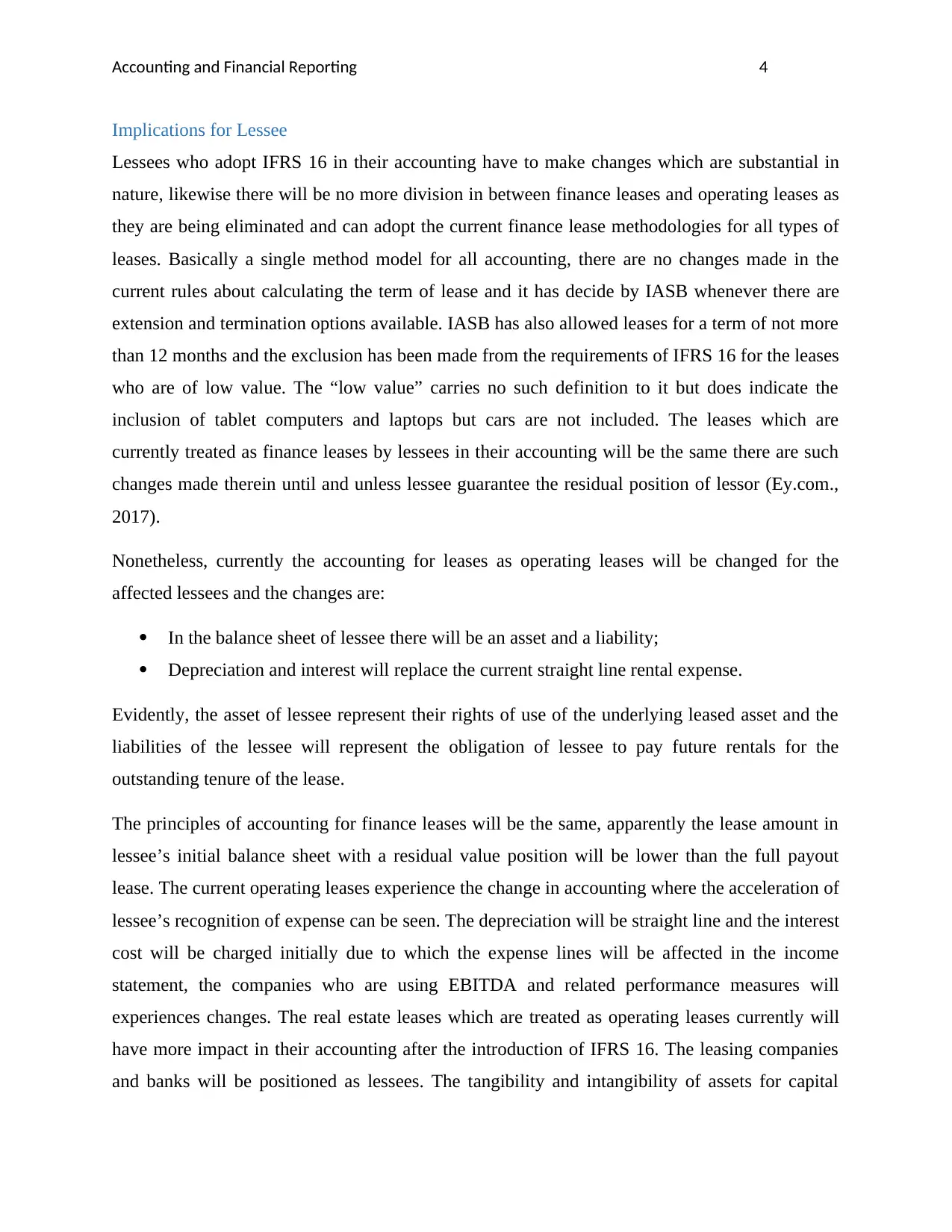

Implication on Lessor

There are no such changes seen in lessor accounting except the additional disclosures it will

require. For many of intermediate lessors there are few changes who subleases the asset taken

from headlease and that particular headlease is currently seen as operating lease. If the product

structures are transformed and lessors offers service contract in place of leases than lessor will

require accounting changes. From the point of view of lessor there is a minimum difference

between the accounting of hard asset service contracts and operating leases (Www2.deloitte.com,

2017). The changes in accounting for the service element of leases which was introduced by

IFRS 15 will be handled by lessors.

Figure 1Implications of IFRS 16

As shown in figure there is no such changes in lessor accounting and only the disclosures are

required.

Effects on Financial Statements

This newly launched lease standard IFRS 16 abolished the arrangement of leases for a lessee

namely operating leases or finance leases. Leases are to be capitalized after recognizing the net

present value of the lease payments by showing them as ROUA or may be together with the

property or plant and equipment. A company may recognize financial liability which represents

its compulsion to pay in future when the lease payment are made over time (Pwc.de, 2017).

The major impact of the new requirement in IFRS 16 in lease assets and financial liabilities are

the increases and for the companies having material off balance sheet leases the change occur

will be seen in key financial metrics which is consequent to the company’s assets and liabilities,

adequacy purposes of the right of use asset on a bank’s balance sheet is still not resolved

(Öztürk, and Serçemeli, 2016).

Implication on Lessor

There are no such changes seen in lessor accounting except the additional disclosures it will

require. For many of intermediate lessors there are few changes who subleases the asset taken

from headlease and that particular headlease is currently seen as operating lease. If the product

structures are transformed and lessors offers service contract in place of leases than lessor will

require accounting changes. From the point of view of lessor there is a minimum difference

between the accounting of hard asset service contracts and operating leases (Www2.deloitte.com,

2017). The changes in accounting for the service element of leases which was introduced by

IFRS 15 will be handled by lessors.

Figure 1Implications of IFRS 16

As shown in figure there is no such changes in lessor accounting and only the disclosures are

required.

Effects on Financial Statements

This newly launched lease standard IFRS 16 abolished the arrangement of leases for a lessee

namely operating leases or finance leases. Leases are to be capitalized after recognizing the net

present value of the lease payments by showing them as ROUA or may be together with the

property or plant and equipment. A company may recognize financial liability which represents

its compulsion to pay in future when the lease payment are made over time (Pwc.de, 2017).

The major impact of the new requirement in IFRS 16 in lease assets and financial liabilities are

the increases and for the companies having material off balance sheet leases the change occur

will be seen in key financial metrics which is consequent to the company’s assets and liabilities,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting and Financial Reporting 6

examples would be the leverage ratios. The key elements of the new standard and its effect on

financial statement will be the replacement of model ‘Risks and rewards’ to Right-of-use model

and at the inception of the lease, lessee is required to recognize the asset and liabilities (Ifrs.org,

2017).

The determination of lease term will require judgment, earlier it was not needed before an

operating lease. With the reference of the lease term estimated all the lease liabilities are

measured based on it. While measuring the lease assets and liabilities when these assets and

liabilities depend on the rate, or an index or on the fixed payment, the contingent rentals or

inconstant lease payments need to be included in it. A lessee must re-evaluate the lease terms

when they spot occurrence of any significant event or a change in such situations where the

lessee can have the control (Ifrs.org, 2017).

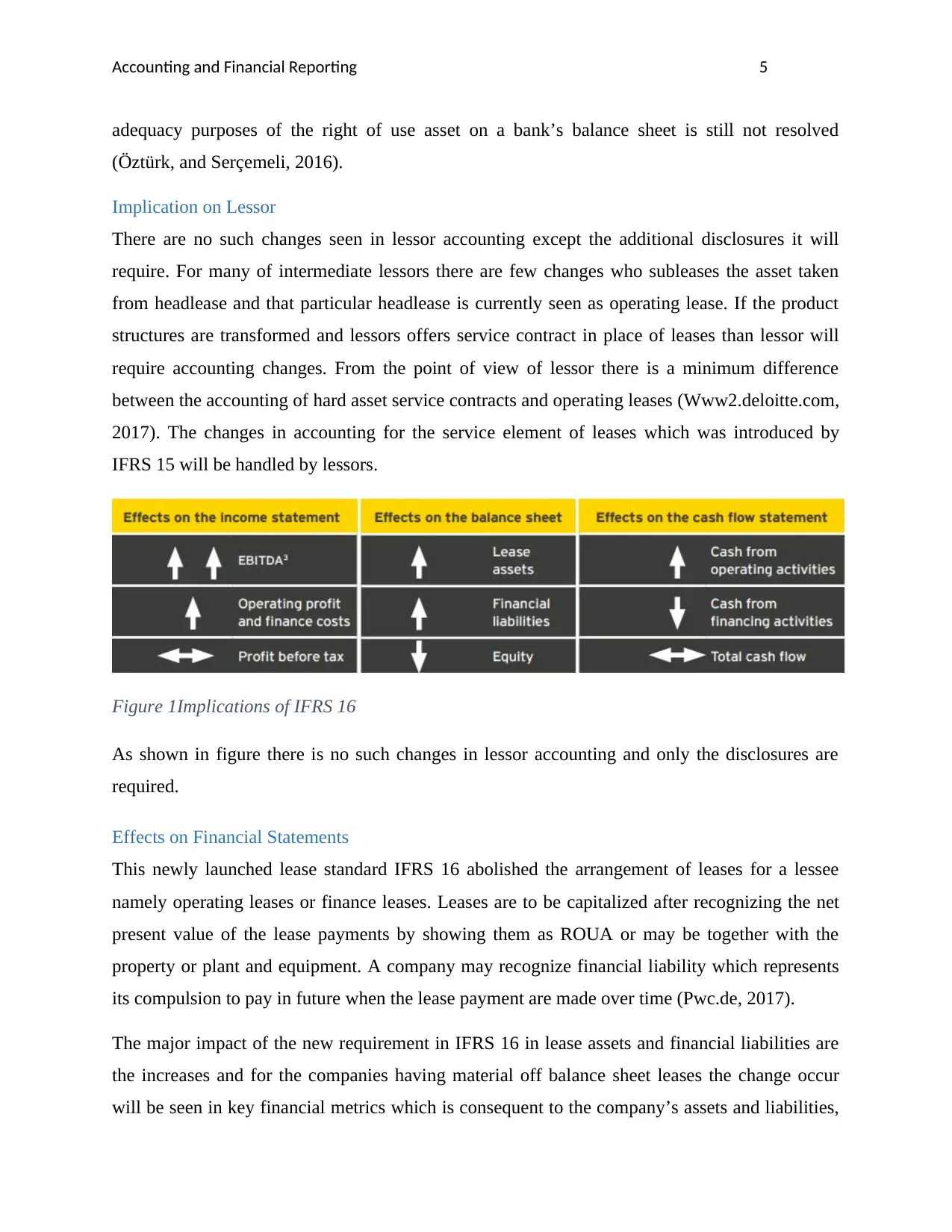

Effects on Balance Sheet

The consequence of IFRS 16 on company’s balance sheet is considered by IASB will be for

companies who have incognito leverage leases, the new-fangled lease standard will result into an

increase in the lease assets and financial liabilities. The carrying amount of lease assets will

reduce more than the carrying amount of lease liabilities. This ultimately result into decrease in

reported equity comparatively in IAS 17 for the companies having incognito leverage leases. It is

alike to the effect on equity that arise from financing the asset purchase and it can be from

balance sheet or a loan (Invigorsexecbriefings.com, 2017). The new standard requires company

to report on the balance sheet lease assets and liabilities but does not include short-term leases

and low value lease assets. IASB expects improvement in the comparability of financial

information by IFRS 16 with an intention to recognize assets and liabilities with importance of

all leases and measure those assets and liabilities in the way they are being recognized. Through

a lease the rights and liabilities are being recognized that re obtained and incurred respectively

(Home.kpmg.com, 2017).

examples would be the leverage ratios. The key elements of the new standard and its effect on

financial statement will be the replacement of model ‘Risks and rewards’ to Right-of-use model

and at the inception of the lease, lessee is required to recognize the asset and liabilities (Ifrs.org,

2017).

The determination of lease term will require judgment, earlier it was not needed before an

operating lease. With the reference of the lease term estimated all the lease liabilities are

measured based on it. While measuring the lease assets and liabilities when these assets and

liabilities depend on the rate, or an index or on the fixed payment, the contingent rentals or

inconstant lease payments need to be included in it. A lessee must re-evaluate the lease terms

when they spot occurrence of any significant event or a change in such situations where the

lessee can have the control (Ifrs.org, 2017).

Effects on Balance Sheet

The consequence of IFRS 16 on company’s balance sheet is considered by IASB will be for

companies who have incognito leverage leases, the new-fangled lease standard will result into an

increase in the lease assets and financial liabilities. The carrying amount of lease assets will

reduce more than the carrying amount of lease liabilities. This ultimately result into decrease in

reported equity comparatively in IAS 17 for the companies having incognito leverage leases. It is

alike to the effect on equity that arise from financing the asset purchase and it can be from

balance sheet or a loan (Invigorsexecbriefings.com, 2017). The new standard requires company

to report on the balance sheet lease assets and liabilities but does not include short-term leases

and low value lease assets. IASB expects improvement in the comparability of financial

information by IFRS 16 with an intention to recognize assets and liabilities with importance of

all leases and measure those assets and liabilities in the way they are being recognized. Through

a lease the rights and liabilities are being recognized that re obtained and incurred respectively

(Home.kpmg.com, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Financial Reporting 7

Figure 2 Effect on Balance Sheet

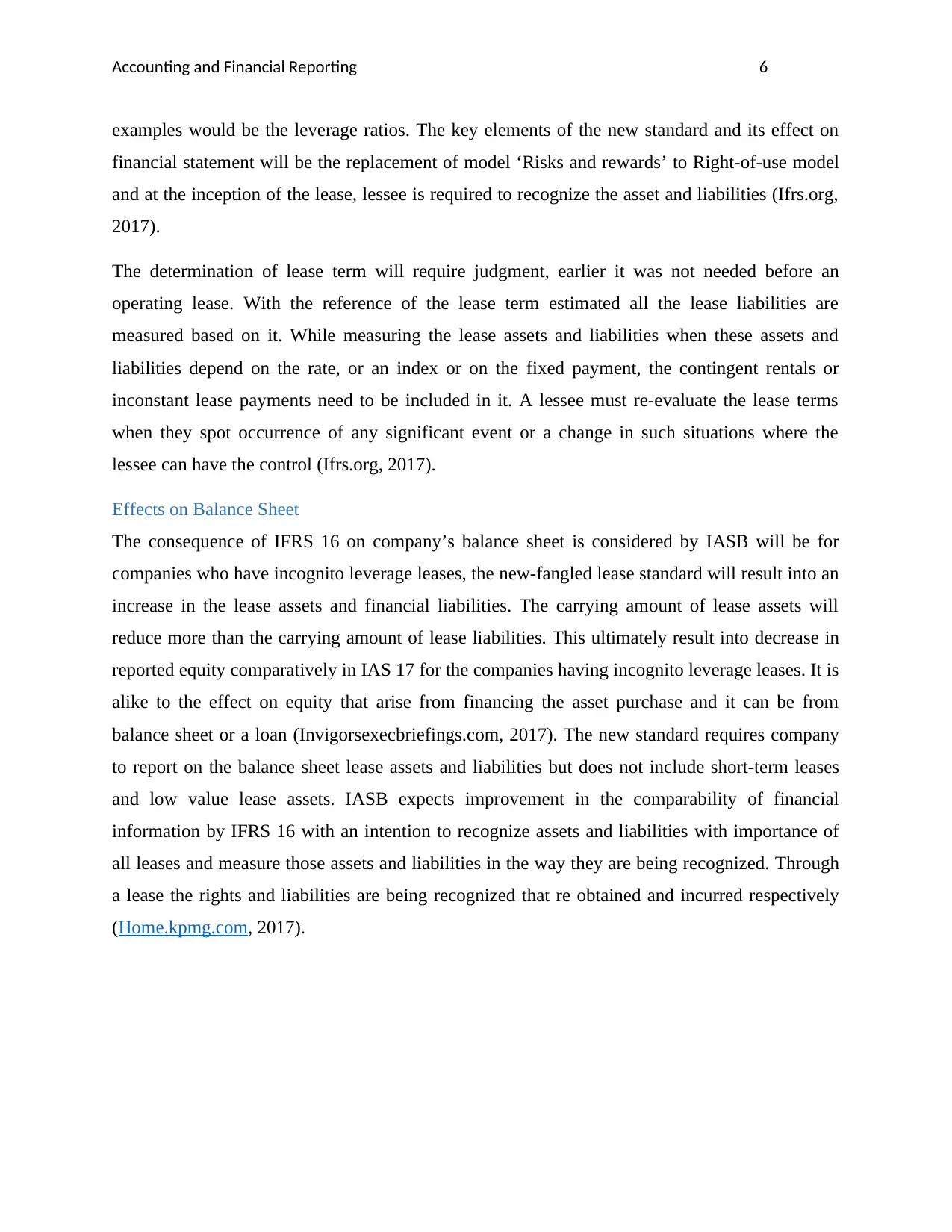

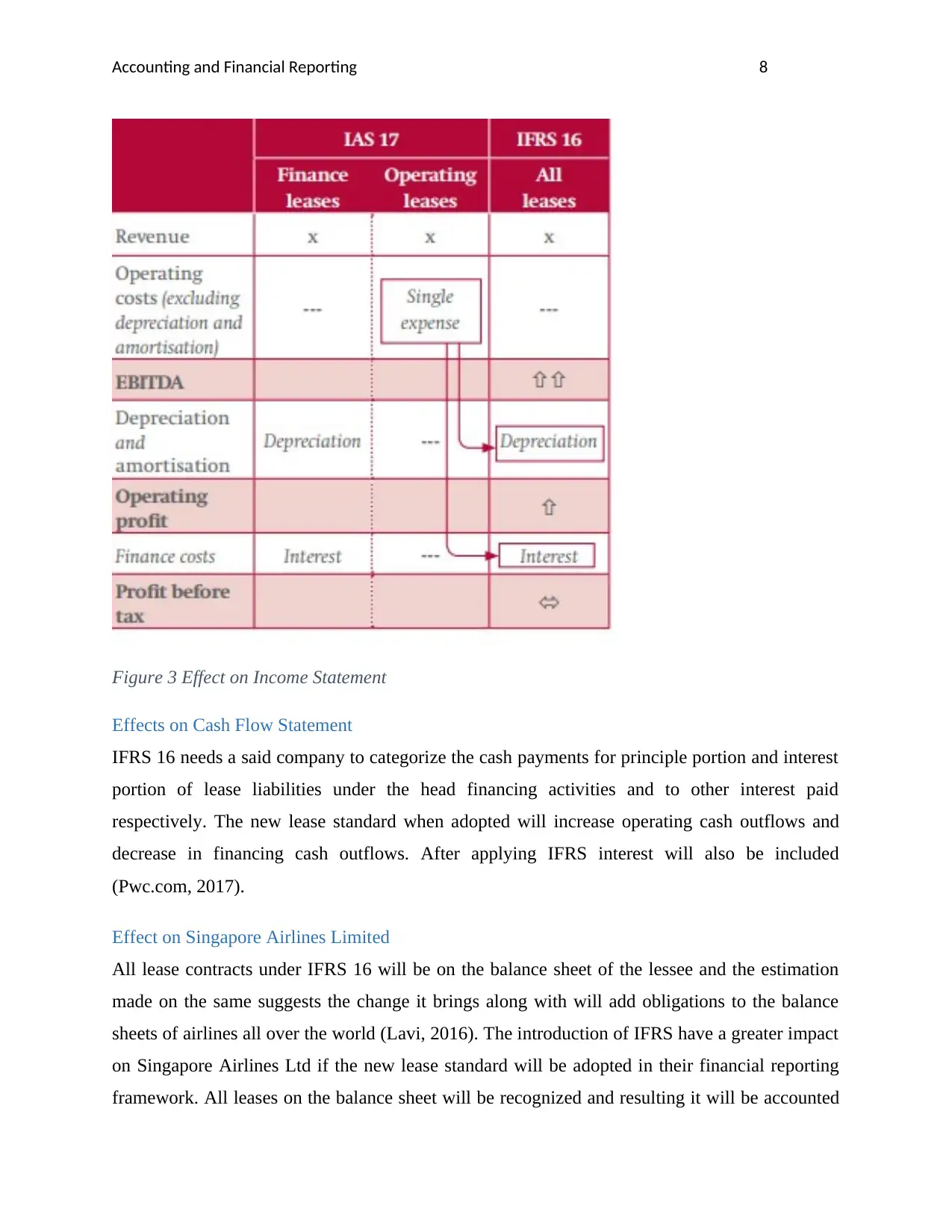

Effects on Income Statement

The effects that are considered by IASB by IFRS 16 will have on income statement of company

is the recognition of the expense which are related to individual as well as portfolios of leases,

the appearance of the expenses related to leases see the change and few other effects. The

companies who have assets and liabilities which does not appear on the company’s balance sheet

leases are expected to show the results in high profit before interest and tax, depreciation and

amortization (Hussey, 2017). Whereas operating profit and finance costs also increase but not

with the same percentage and profit before tax will be stable. As per new lease standard the

implicit interest in lease payments for material off balance sheet will form a part of finance cost

which was earlier was part of operating expenses. The figure hereunder shows the effect on

income statement:

Figure 2 Effect on Balance Sheet

Effects on Income Statement

The effects that are considered by IASB by IFRS 16 will have on income statement of company

is the recognition of the expense which are related to individual as well as portfolios of leases,

the appearance of the expenses related to leases see the change and few other effects. The

companies who have assets and liabilities which does not appear on the company’s balance sheet

leases are expected to show the results in high profit before interest and tax, depreciation and

amortization (Hussey, 2017). Whereas operating profit and finance costs also increase but not

with the same percentage and profit before tax will be stable. As per new lease standard the

implicit interest in lease payments for material off balance sheet will form a part of finance cost

which was earlier was part of operating expenses. The figure hereunder shows the effect on

income statement:

Accounting and Financial Reporting 8

Figure 3 Effect on Income Statement

Effects on Cash Flow Statement

IFRS 16 needs a said company to categorize the cash payments for principle portion and interest

portion of lease liabilities under the head financing activities and to other interest paid

respectively. The new lease standard when adopted will increase operating cash outflows and

decrease in financing cash outflows. After applying IFRS interest will also be included

(Pwc.com, 2017).

Effect on Singapore Airlines Limited

All lease contracts under IFRS 16 will be on the balance sheet of the lessee and the estimation

made on the same suggests the change it brings along with will add obligations to the balance

sheets of airlines all over the world (Lavi, 2016). The introduction of IFRS have a greater impact

on Singapore Airlines Ltd if the new lease standard will be adopted in their financial reporting

framework. All leases on the balance sheet will be recognized and resulting it will be accounted

Figure 3 Effect on Income Statement

Effects on Cash Flow Statement

IFRS 16 needs a said company to categorize the cash payments for principle portion and interest

portion of lease liabilities under the head financing activities and to other interest paid

respectively. The new lease standard when adopted will increase operating cash outflows and

decrease in financing cash outflows. After applying IFRS interest will also be included

(Pwc.com, 2017).

Effect on Singapore Airlines Limited

All lease contracts under IFRS 16 will be on the balance sheet of the lessee and the estimation

made on the same suggests the change it brings along with will add obligations to the balance

sheets of airlines all over the world (Lavi, 2016). The introduction of IFRS have a greater impact

on Singapore Airlines Ltd if the new lease standard will be adopted in their financial reporting

framework. All leases on the balance sheet will be recognized and resulting it will be accounted

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

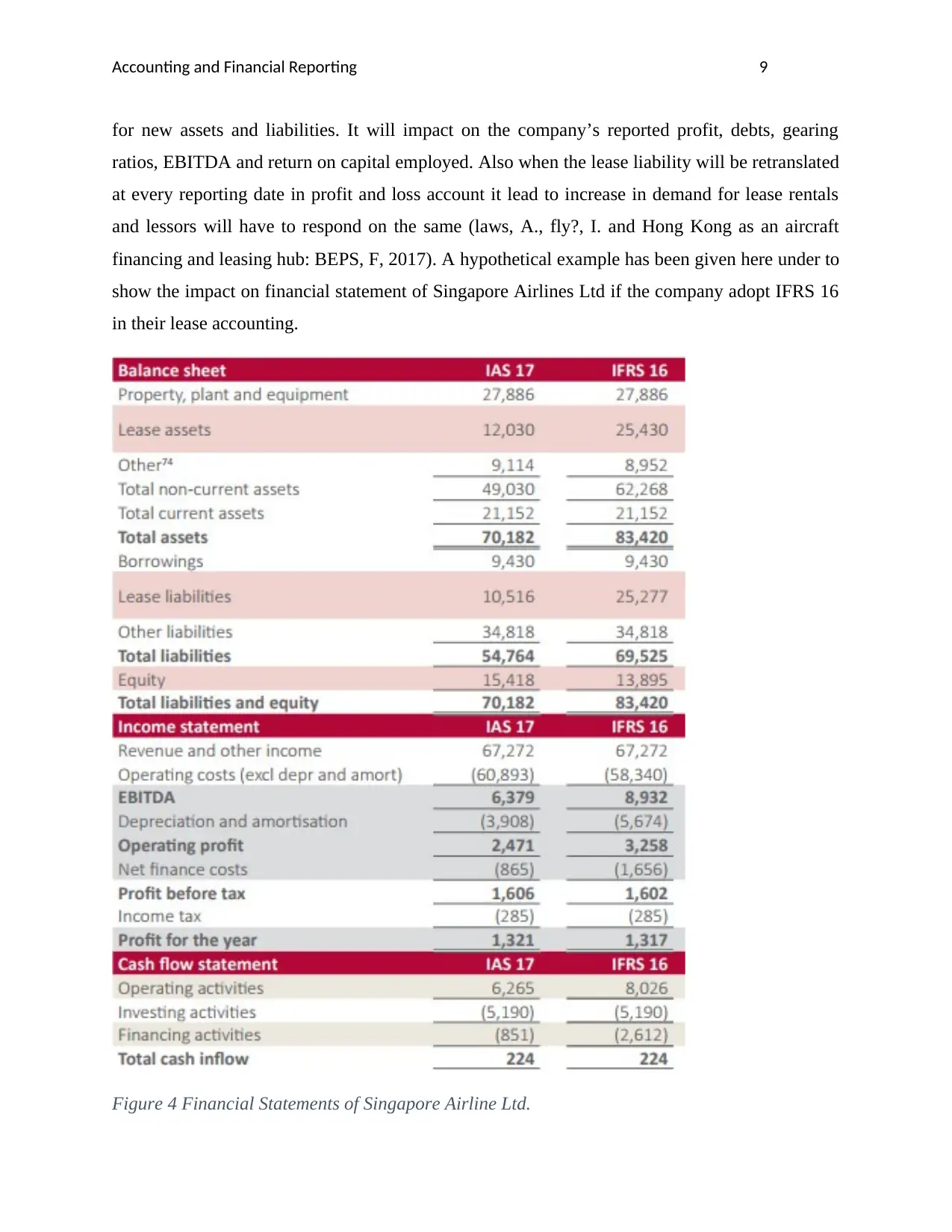

Accounting and Financial Reporting 9

for new assets and liabilities. It will impact on the company’s reported profit, debts, gearing

ratios, EBITDA and return on capital employed. Also when the lease liability will be retranslated

at every reporting date in profit and loss account it lead to increase in demand for lease rentals

and lessors will have to respond on the same (laws, A., fly?, I. and Hong Kong as an aircraft

financing and leasing hub: BEPS, F, 2017). A hypothetical example has been given here under to

show the impact on financial statement of Singapore Airlines Ltd if the company adopt IFRS 16

in their lease accounting.

Figure 4 Financial Statements of Singapore Airline Ltd.

for new assets and liabilities. It will impact on the company’s reported profit, debts, gearing

ratios, EBITDA and return on capital employed. Also when the lease liability will be retranslated

at every reporting date in profit and loss account it lead to increase in demand for lease rentals

and lessors will have to respond on the same (laws, A., fly?, I. and Hong Kong as an aircraft

financing and leasing hub: BEPS, F, 2017). A hypothetical example has been given here under to

show the impact on financial statement of Singapore Airlines Ltd if the company adopt IFRS 16

in their lease accounting.

Figure 4 Financial Statements of Singapore Airline Ltd.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and Financial Reporting 10

As per the given financial statements the comparability has been shown in between IAS 17 and

IFRS 16. There is an instant increase in lease assets and lease liabilities of the company after

adopting the new lease standard whereas equity has seen a drop after applying IFRS 16 in their

financial reporting. IFRS 16 does not require the presentation of lease assets and liabilities on the

balance sheet. In income statement after applying the lease standard the company sees higher

EBITDA because no expense related to lease are included and operating profit also shown an

increase due to the inclusion of the portion of expenses only. Looking at the profits for the year

there is a slight decrease found out as company hold a portfolio of leases which does not have a

starting and ending in the same year. The impact on cash flow statement is not on the total cash

flows but on the net cash flows from operating activities and financing activities which are

showing an increase after applying IFRS 16. The company has reports interest within the

operating activities (Chen, and Khurana, 2017).

Conclusion

The introduction of IFRS 16 has given a scale of changes in the financial instruments, lease

accounting and the revenues to the listed companies. It has been observed that the new

requirements of the standard brings major changes in the lease accounting requirements and for

those companies who lease their most of the assets in their operations will experience the

increase in their reported assets and liabilities. It affects variety of sectors and in this report the

effect on Singapore Airlines limited has been shown as they have a larger portfolio so the impact

on their financial metrics are greater too.

As per the given financial statements the comparability has been shown in between IAS 17 and

IFRS 16. There is an instant increase in lease assets and lease liabilities of the company after

adopting the new lease standard whereas equity has seen a drop after applying IFRS 16 in their

financial reporting. IFRS 16 does not require the presentation of lease assets and liabilities on the

balance sheet. In income statement after applying the lease standard the company sees higher

EBITDA because no expense related to lease are included and operating profit also shown an

increase due to the inclusion of the portion of expenses only. Looking at the profits for the year

there is a slight decrease found out as company hold a portfolio of leases which does not have a

starting and ending in the same year. The impact on cash flow statement is not on the total cash

flows but on the net cash flows from operating activities and financing activities which are

showing an increase after applying IFRS 16. The company has reports interest within the

operating activities (Chen, and Khurana, 2017).

Conclusion

The introduction of IFRS 16 has given a scale of changes in the financial instruments, lease

accounting and the revenues to the listed companies. It has been observed that the new

requirements of the standard brings major changes in the lease accounting requirements and for

those companies who lease their most of the assets in their operations will experience the

increase in their reported assets and liabilities. It affects variety of sectors and in this report the

effect on Singapore Airlines limited has been shown as they have a larger portfolio so the impact

on their financial metrics are greater too.

Accounting and Financial Reporting 11

References

Byard, D., Li, Y., & Yu, Y. (2011). The effect of mandatory IFRS adoption on financial

analysts’ information environment. Journal of accounting research, 49(1), 69-96.

Chen, L. H., & Khurana, I. K. (2017). The Impact of IFRS versus US GAAP on Audit Fees and

Going Concern Opinions: Evidence from US-Listed Foreign Firms.

Cotter, D. (2012). Advanced financial reporting: A complete guide to IFRS. Financial

Times/Prentice Hall.

Ey.com. (2017). Cite a Website - Cite This For Me. Available at:

http://www.ey.com/Publication/vwLUAssets/ey-leases-a-summary-of-ifrs-16/$FILE/ey-

leases-a-summary-of-ifrs-16.pdf [Accessed 15 Nov. 2017].

Home.kpmg.com. (2017). Cite a Website - Cite This For Me. Available at:

https://home.kpmg.com/content/dam/kpmg/pdf/2016/05/SG-Issue54-april2016.pdf

[Accessed 15 Nov. 2017].

Hussey, R. (2017, May). Leasing of Assets: A Content Analysis of Comment. In GAI

International Academic Conferences Proceedings (p. 23).

Iasplus.com. (2017). IFRS 16 — Leases. Available at:

https://www.iasplus.com/en/standards/ifrs/ifrs-16 [Accessed 15 Nov. 2017].

Ifrs.org. (2017). Cite a Website - Cite This For Me. Available at:

http://www.ifrs.org/-/media/project/leases/ifrs/published-documents/ifrs16-project-

summary.pdf [Accessed 15 Nov. 2017].

Ifrs.org. (2017). Cite a Website - Cite This For Me. Available at:

http://www.ifrs.org/-/media/project/leases/ifrs/published-documents/ifrs16-effects-

analysis.pdf [Accessed 15 Nov. 2017].

References

Byard, D., Li, Y., & Yu, Y. (2011). The effect of mandatory IFRS adoption on financial

analysts’ information environment. Journal of accounting research, 49(1), 69-96.

Chen, L. H., & Khurana, I. K. (2017). The Impact of IFRS versus US GAAP on Audit Fees and

Going Concern Opinions: Evidence from US-Listed Foreign Firms.

Cotter, D. (2012). Advanced financial reporting: A complete guide to IFRS. Financial

Times/Prentice Hall.

Ey.com. (2017). Cite a Website - Cite This For Me. Available at:

http://www.ey.com/Publication/vwLUAssets/ey-leases-a-summary-of-ifrs-16/$FILE/ey-

leases-a-summary-of-ifrs-16.pdf [Accessed 15 Nov. 2017].

Home.kpmg.com. (2017). Cite a Website - Cite This For Me. Available at:

https://home.kpmg.com/content/dam/kpmg/pdf/2016/05/SG-Issue54-april2016.pdf

[Accessed 15 Nov. 2017].

Hussey, R. (2017, May). Leasing of Assets: A Content Analysis of Comment. In GAI

International Academic Conferences Proceedings (p. 23).

Iasplus.com. (2017). IFRS 16 — Leases. Available at:

https://www.iasplus.com/en/standards/ifrs/ifrs-16 [Accessed 15 Nov. 2017].

Ifrs.org. (2017). Cite a Website - Cite This For Me. Available at:

http://www.ifrs.org/-/media/project/leases/ifrs/published-documents/ifrs16-project-

summary.pdf [Accessed 15 Nov. 2017].

Ifrs.org. (2017). Cite a Website - Cite This For Me. Available at:

http://www.ifrs.org/-/media/project/leases/ifrs/published-documents/ifrs16-effects-

analysis.pdf [Accessed 15 Nov. 2017].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.