Comprehensive Audit Report: DIPL Limited Financial Performance

VerifiedAdded on 2020/02/24

|11

|2503

|65

Report

AI Summary

This report is an audit of DIPL Limited, covering various aspects of financial analysis and risk management. The report begins by outlining the auditor's responsibilities, including understanding the business environment, applying professional skepticism, and assessing material misstatements. It then discusses the audit procedures undertaken, such as reviewing internal controls, inspecting financial records, and using analytical procedures. The report also addresses specific issues faced by DIPL Limited, including changes in IT systems, depreciation methods, and potential discrepancies in transaction recording. The analysis includes ratio analysis, comparing financial data over the last three years, and evaluating liquidity, debt, and profitability ratios. The report further delves into risk assessment and mitigation, identifying inherent, control, and detection risks, with a focus on the adoption of a new IT system and potential fraud risks due to lack of segregation of duties. The auditor's role in mitigating these risks through verifying documents, suggesting control improvements, and potentially qualifying the audit report is also highlighted. The report emphasizes the importance of proper control systems, surprise checks, and expert advice to ensure the accuracy and reliability of the financial statements.

By student name

Professor

University

Date: 25 August 2017.

Professor

University

Date: 25 August 2017.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Contents

Question no 1…………………………………………………………………...2

Question no 2…………………………………………………………………...6

Question no 3…………………………………………………………….....….8

Refrences.....……………………………………………………………….......10

1 | P a g e

Contents

Question no 1…………………………………………………………………...2

Question no 2…………………………………………………………………...6

Question no 3…………………………………………………………….....….8

Refrences.....……………………………………………………………….......10

1 | P a g e

2

Question no 1

While accepting the audit of the client, the auditor needs to understand the business, internal

and external business environment, the industry in which it is operating, the management and its

assertions. It is important that the auditor apply his professional skepticm and judgment before taking

major decisions. Audit is conducted with the objective of determining the risk of material misstatements

given the assumption that the management has tried to identify and mitigate all the types of risks. One

of the important aspects of auditing is studying and mitigating the risks posed by the related party

transactions by adequately disclosing the same in the financials (Raiborn, Butler & Martin 2016). The

auditor must also provide the reasonable assurance to both the internal and the external users, the

auditor needs to check the going concern assumption, consistency, etc. The various procedures which

the auditor undertakes for completion of the substantive audit includes observation of the key controls

in practice, inspection of the books of accounts and supporting and evidence on the basis of which

incomes and related expenditure are recorded in the books etc. It also includes using different

procedures to conclude on the existence of the asset and liabilities on the reporting date, whether the

same has been properly disclosed in the notes, whether proper valuation of the intangibles and

inventory has been done, and whether the completeness of the accounts is being ensured. An example

of the same would be to check the outflows of cash and bank from the bank statements and the cash

ledger book and reconciling the same at the period end (Knechel & Salterio 2016).

Once the substantive procedures are went through, the auditor also makes makes use of the

analytical procedures before making an audit plan. This generally includes comparison of the client’s

financial numbers with the industry data, the numbers in the previous period in the last year and just

previously ended quarter, analysis of key financial ratios, trend analysis, budgeted and forecasting

procedures and finally concluding with the trends of the non-financial data. Besides all this, the auditor

is also responsible to check the method and procedure being followed to book the expenses, recognition

of the revenue in the books, whether the same has been done on a reasonable basis or it is overstated

or understated. Based on all the above procedures and the effectiveness of the internal control existing

in the organization, the auditor plans the audit steps to be taken and the nature of the procedures to be

followed, the time to be allocated and extent to which the checking will be done by establishing the

audit materiality-planning threshold. In case the internal control is weak, the risk is more and therefore

less reliance can be placed on what is reported. Similarly, if the internal control being established and

practiced within the entity is strong, more reliance can be placed on it and therefore the audit plan need

2 | P a g e

Question no 1

While accepting the audit of the client, the auditor needs to understand the business, internal

and external business environment, the industry in which it is operating, the management and its

assertions. It is important that the auditor apply his professional skepticm and judgment before taking

major decisions. Audit is conducted with the objective of determining the risk of material misstatements

given the assumption that the management has tried to identify and mitigate all the types of risks. One

of the important aspects of auditing is studying and mitigating the risks posed by the related party

transactions by adequately disclosing the same in the financials (Raiborn, Butler & Martin 2016). The

auditor must also provide the reasonable assurance to both the internal and the external users, the

auditor needs to check the going concern assumption, consistency, etc. The various procedures which

the auditor undertakes for completion of the substantive audit includes observation of the key controls

in practice, inspection of the books of accounts and supporting and evidence on the basis of which

incomes and related expenditure are recorded in the books etc. It also includes using different

procedures to conclude on the existence of the asset and liabilities on the reporting date, whether the

same has been properly disclosed in the notes, whether proper valuation of the intangibles and

inventory has been done, and whether the completeness of the accounts is being ensured. An example

of the same would be to check the outflows of cash and bank from the bank statements and the cash

ledger book and reconciling the same at the period end (Knechel & Salterio 2016).

Once the substantive procedures are went through, the auditor also makes makes use of the

analytical procedures before making an audit plan. This generally includes comparison of the client’s

financial numbers with the industry data, the numbers in the previous period in the last year and just

previously ended quarter, analysis of key financial ratios, trend analysis, budgeted and forecasting

procedures and finally concluding with the trends of the non-financial data. Besides all this, the auditor

is also responsible to check the method and procedure being followed to book the expenses, recognition

of the revenue in the books, whether the same has been done on a reasonable basis or it is overstated

or understated. Based on all the above procedures and the effectiveness of the internal control existing

in the organization, the auditor plans the audit steps to be taken and the nature of the procedures to be

followed, the time to be allocated and extent to which the checking will be done by establishing the

audit materiality-planning threshold. In case the internal control is weak, the risk is more and therefore

less reliance can be placed on what is reported. Similarly, if the internal control being established and

practiced within the entity is strong, more reliance can be placed on it and therefore the audit plan need

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

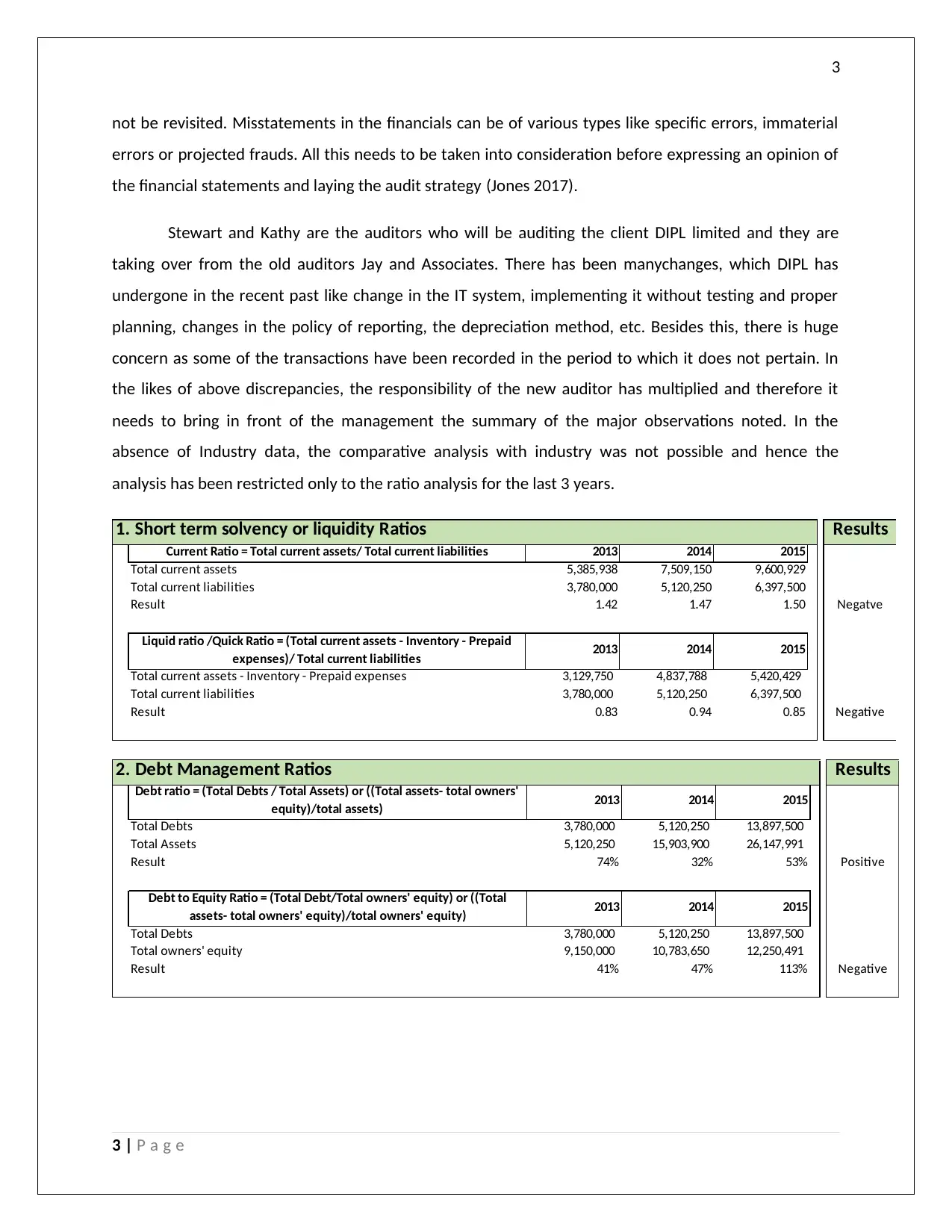

not be revisited. Misstatements in the financials can be of various types like specific errors, immaterial

errors or projected frauds. All this needs to be taken into consideration before expressing an opinion of

the financial statements and laying the audit strategy (Jones 2017).

Stewart and Kathy are the auditors who will be auditing the client DIPL limited and they are

taking over from the old auditors Jay and Associates. There has been manychanges, which DIPL has

undergone in the recent past like change in the IT system, implementing it without testing and proper

planning, changes in the policy of reporting, the depreciation method, etc. Besides this, there is huge

concern as some of the transactions have been recorded in the period to which it does not pertain. In

the likes of above discrepancies, the responsibility of the new auditor has multiplied and therefore it

needs to bring in front of the management the summary of the major observations noted. In the

absence of Industry data, the comparative analysis with industry was not possible and hence the

analysis has been restricted only to the ratio analysis for the last 3 years.

Results

2013 2014 2015

Total current assets 5,385,938 7,509,150 9,600,929

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 1.42 1.47 1.50 Negatve

2013 2014 2015

Total current assets - Inventory - Prepaid expenses 3,129,750 4,837,788 5,420,429

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 0.83 0.94 0.85 Negative

1. Short term solvency or liquidity Ratios

Current Ratio = Total current assets/ Total current liabilities

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities

Results

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total Assets 5,120,250 15,903,900 26,147,991

Result 74% 32% 53% Positive

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 41% 47% 113% Negative

2. Debt Management Ratios

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total owners'

equity)/total assets)

Debt to Equity Ratio = (Total Debt/Total owners' equity) or ((Total

assets- total owners' equity)/total owners' equity)

3 | P a g e

not be revisited. Misstatements in the financials can be of various types like specific errors, immaterial

errors or projected frauds. All this needs to be taken into consideration before expressing an opinion of

the financial statements and laying the audit strategy (Jones 2017).

Stewart and Kathy are the auditors who will be auditing the client DIPL limited and they are

taking over from the old auditors Jay and Associates. There has been manychanges, which DIPL has

undergone in the recent past like change in the IT system, implementing it without testing and proper

planning, changes in the policy of reporting, the depreciation method, etc. Besides this, there is huge

concern as some of the transactions have been recorded in the period to which it does not pertain. In

the likes of above discrepancies, the responsibility of the new auditor has multiplied and therefore it

needs to bring in front of the management the summary of the major observations noted. In the

absence of Industry data, the comparative analysis with industry was not possible and hence the

analysis has been restricted only to the ratio analysis for the last 3 years.

Results

2013 2014 2015

Total current assets 5,385,938 7,509,150 9,600,929

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 1.42 1.47 1.50 Negatve

2013 2014 2015

Total current assets - Inventory - Prepaid expenses 3,129,750 4,837,788 5,420,429

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 0.83 0.94 0.85 Negative

1. Short term solvency or liquidity Ratios

Current Ratio = Total current assets/ Total current liabilities

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities

Results

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total Assets 5,120,250 15,903,900 26,147,991

Result 74% 32% 53% Positive

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 41% 47% 113% Negative

2. Debt Management Ratios

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total owners'

equity)/total assets)

Debt to Equity Ratio = (Total Debt/Total owners' equity) or ((Total

assets- total owners' equity)/total owners' equity)

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Results

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Accounts Receivable 2,482,500 4,320,000 5,073,309

Result 13.78 8.73 8.57 Negative

2013 2014 2015

No. of days 365 365 365

Receivable turnover 13.78 8.73 8.57

Result 26.49 41.83 42.61 Negative

2013 2014 2015

COGS 28,207,500 31,620,000 36,855,000

Inventory 2,256,188 2,671,362 4,180,500

Result 12.50 11.84 8.82 Negative

2013 2014 2015

No. of days 365 365 365

Inventory turnover 12.50 11.84 8.82

Result 29.19 30.84 41.40 Negative

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Net Fixed Assets 7,544,062 8,394,750 15,572,062

Result 4.53 4.49 2.79 Negative

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Total Assets 12,930,000 15,903,900 26,147,991 Negative

Results 2.65 2.37 1.66

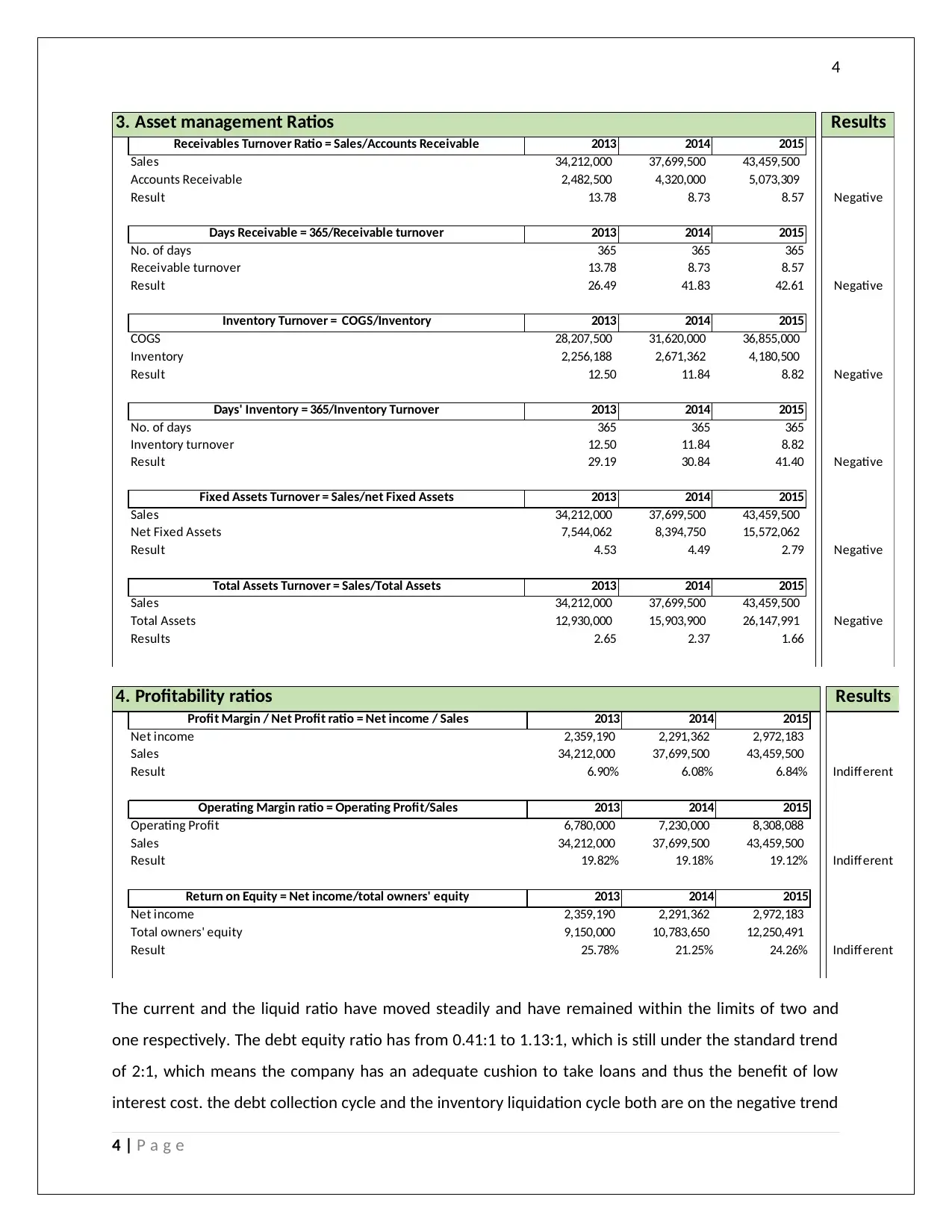

3. Asset management Ratios

Inventory Turnover = COGS/Inventory

Days' Inventory = 365/Inventory Turnover

Fixed Assets Turnover = Sales/net Fixed Assets

Total Assets Turnover = Sales/Total Assets

Receivables Turnover Ratio = Sales/Accounts Receivable

Days Receivable = 365/Receivable turnover

Results

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Sales 34,212,000 37,699,500 43,459,500

Result 6.90% 6.08% 6.84% Indifferent

2013 2014 2015

Operating Profit 6,780,000 7,230,000 8,308,088

Sales 34,212,000 37,699,500 43,459,500

Result 19.82% 19.18% 19.12% Indifferent

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 25.78% 21.25% 24.26% Indifferent

4. Profitability ratios

Profit Margin / Net Profit ratio = Net income / Sales

Operating Margin ratio = Operating Profit/Sales

Return on Equity = Net income/total owners' equity

The current and the liquid ratio have moved steadily and have remained within the limits of two and

one respectively. The debt equity ratio has from 0.41:1 to 1.13:1, which is still under the standard trend

of 2:1, which means the company has an adequate cushion to take loans and thus the benefit of low

interest cost. the debt collection cycle and the inventory liquidation cycle both are on the negative trend

4 | P a g e

Results

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Accounts Receivable 2,482,500 4,320,000 5,073,309

Result 13.78 8.73 8.57 Negative

2013 2014 2015

No. of days 365 365 365

Receivable turnover 13.78 8.73 8.57

Result 26.49 41.83 42.61 Negative

2013 2014 2015

COGS 28,207,500 31,620,000 36,855,000

Inventory 2,256,188 2,671,362 4,180,500

Result 12.50 11.84 8.82 Negative

2013 2014 2015

No. of days 365 365 365

Inventory turnover 12.50 11.84 8.82

Result 29.19 30.84 41.40 Negative

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Net Fixed Assets 7,544,062 8,394,750 15,572,062

Result 4.53 4.49 2.79 Negative

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Total Assets 12,930,000 15,903,900 26,147,991 Negative

Results 2.65 2.37 1.66

3. Asset management Ratios

Inventory Turnover = COGS/Inventory

Days' Inventory = 365/Inventory Turnover

Fixed Assets Turnover = Sales/net Fixed Assets

Total Assets Turnover = Sales/Total Assets

Receivables Turnover Ratio = Sales/Accounts Receivable

Days Receivable = 365/Receivable turnover

Results

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Sales 34,212,000 37,699,500 43,459,500

Result 6.90% 6.08% 6.84% Indifferent

2013 2014 2015

Operating Profit 6,780,000 7,230,000 8,308,088

Sales 34,212,000 37,699,500 43,459,500

Result 19.82% 19.18% 19.12% Indifferent

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 25.78% 21.25% 24.26% Indifferent

4. Profitability ratios

Profit Margin / Net Profit ratio = Net income / Sales

Operating Margin ratio = Operating Profit/Sales

Return on Equity = Net income/total owners' equity

The current and the liquid ratio have moved steadily and have remained within the limits of two and

one respectively. The debt equity ratio has from 0.41:1 to 1.13:1, which is still under the standard trend

of 2:1, which means the company has an adequate cushion to take loans and thus the benefit of low

interest cost. the debt collection cycle and the inventory liquidation cycle both are on the negative trend

4 | P a g e

5

which have increased from 26 to 42 days and 29 to 41 days respectively. This shows the loss of control

over these areas such that the funding is not coming at the right time to the company The profitability

ratio of DIPL over last 3 years is evident of the fact that the profits has not increased and has remained

constant at around 6.5-7%. In addition, the company is failing to give increased returns to the

shareholders (calculated through ROE), even after increasing the mix of debt in the capital structure.

The financial viability of the company can be easily judged on the basic of these nalyticals that may be

applied to the overall accounts of the company. It helps in asserting the liquidity position of the

company and also helps the investors in taking important decisions. In case of DIPL, the ratio analysis

shows that the books of account are prepared ina correct manner showing the overall financial

prospects of the company (Grenier 2017).

5 | P a g e

which have increased from 26 to 42 days and 29 to 41 days respectively. This shows the loss of control

over these areas such that the funding is not coming at the right time to the company The profitability

ratio of DIPL over last 3 years is evident of the fact that the profits has not increased and has remained

constant at around 6.5-7%. In addition, the company is failing to give increased returns to the

shareholders (calculated through ROE), even after increasing the mix of debt in the capital structure.

The financial viability of the company can be easily judged on the basic of these nalyticals that may be

applied to the overall accounts of the company. It helps in asserting the liquidity position of the

company and also helps the investors in taking important decisions. In case of DIPL, the ratio analysis

shows that the books of account are prepared ina correct manner showing the overall financial

prospects of the company (Grenier 2017).

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Solution 2

Risk assessment and mitigation, is an important aspect of auditing. It is important that any

auditor must check all the possible sources that may have any risk associated with them and mitigate

the same. The three main type of risk that is associated with an audit is inherent risk, control risk and

detection risk. Inherent risks are the type of risks that are present even if the management has ensured

proper control measures. These risks are not in the hands of the management and it is important that

the auditor must apply all types of substantive and analytical process to mitigate the overall risk. Control

risks are the type of risks that occur when the company has low internal control established; it is

because of mismanagement that often leads to materiality in the financial statements. Detection risks

occur in case the auditor fails to establish enough professional skepticm and fails to detect major errors

that might affect the overall profitability of the company. As an auditor of the given company, it is the

duty to conduct its audit in such manner that major risks are properly identified and mitigated. In the

case of DIPL, these are the few types of risk that the company may be exposed to given its nature of

business and operations (Sonu, Ahn & Choi 2017).

The first type of inherent risk that is the company might face is in the deviation from the routine

transactional and adoption of non-routine transaction that might affect the overall profitability of the

company. The management of the company are considering new methods for calculation of

depreciation, considering the life of asset to be twenty years where as in general policy as per the

standard the life is thirty years. The Ceo of the company is taking such a decision based just on his

knowledge and not on any kind of research that has been undertaken in this regard. This might lead to

material misstatement and affect the overall profitability of the company. It is important that before

taking such steps the management must take expert guidance so that chances of risk are reduced (Fay &

Negangard 2017).

The second type of risk is associated in the adoption of the new IT system by the company

without any proper scrutiny and research. The management is adopting the same without reconciling

the cost and the profit. There are high chances that the system might fail and might not work as

stipulated. The management needs to conduct proper research before taking such an important step. It

is important that the auditor verify all the documents related, so that there are no discrepancies in the

future. In case the auditor feels that, the system is not functioning as needed it might ask the

management to replace the same. Whenever a new system is adopted in place of an old system, proper

training must be provided to the staff so that they do not manhandle it. The auditor must also reduce

6 | P a g e

Solution 2

Risk assessment and mitigation, is an important aspect of auditing. It is important that any

auditor must check all the possible sources that may have any risk associated with them and mitigate

the same. The three main type of risk that is associated with an audit is inherent risk, control risk and

detection risk. Inherent risks are the type of risks that are present even if the management has ensured

proper control measures. These risks are not in the hands of the management and it is important that

the auditor must apply all types of substantive and analytical process to mitigate the overall risk. Control

risks are the type of risks that occur when the company has low internal control established; it is

because of mismanagement that often leads to materiality in the financial statements. Detection risks

occur in case the auditor fails to establish enough professional skepticm and fails to detect major errors

that might affect the overall profitability of the company. As an auditor of the given company, it is the

duty to conduct its audit in such manner that major risks are properly identified and mitigated. In the

case of DIPL, these are the few types of risk that the company may be exposed to given its nature of

business and operations (Sonu, Ahn & Choi 2017).

The first type of inherent risk that is the company might face is in the deviation from the routine

transactional and adoption of non-routine transaction that might affect the overall profitability of the

company. The management of the company are considering new methods for calculation of

depreciation, considering the life of asset to be twenty years where as in general policy as per the

standard the life is thirty years. The Ceo of the company is taking such a decision based just on his

knowledge and not on any kind of research that has been undertaken in this regard. This might lead to

material misstatement and affect the overall profitability of the company. It is important that before

taking such steps the management must take expert guidance so that chances of risk are reduced (Fay &

Negangard 2017).

The second type of risk is associated in the adoption of the new IT system by the company

without any proper scrutiny and research. The management is adopting the same without reconciling

the cost and the profit. There are high chances that the system might fail and might not work as

stipulated. The management needs to conduct proper research before taking such an important step. It

is important that the auditor verify all the documents related, so that there are no discrepancies in the

future. In case the auditor feels that, the system is not functioning as needed it might ask the

management to replace the same. Whenever a new system is adopted in place of an old system, proper

training must be provided to the staff so that they do not manhandle it. The auditor must also reduce

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

any kind of risk of material misstatement that it might come across while verifying the validity of the

system. The management must also ensure that strong control measures are undertaken so that any

kind of inherent risk can be counter attacked. It makes the work of the auditor easy and ensures that the

system work efficiently without any kind of problem. The auditor along with the support of the

management mitigates the inherent risks that the company faces in these few ways (DeZoort & Harrison

2016).

7 | P a g e

any kind of risk of material misstatement that it might come across while verifying the validity of the

system. The management must also ensure that strong control measures are undertaken so that any

kind of inherent risk can be counter attacked. It makes the work of the auditor easy and ensures that the

system work efficiently without any kind of problem. The auditor along with the support of the

management mitigates the inherent risks that the company faces in these few ways (DeZoort & Harrison

2016).

7 | P a g e

8

Solution 3

Fraud occurs when the management or the employees of the company indulges in certain

activity like manipulation or records or defalcation of cash, for their own benefits. The work of the

auditor is to verify the records of the company and to make sure that any kind of fraud risk factor is

mitigated and removed. Fraud occurs because of the negligence of the management and it is important

that proper control be established to prevent the same. Identification of fraud risk factor is the work of

the management of the company and the auditor can help in mitigation of the same. While conducting

the audit, the auditor must apply such methods that help in identification of major fraud risk factors.

Often the management might be the culprit, the auditor should not rely on what the management

portrays and should apply his own research techniques before reaching a conclusion (Bae 2017).

In case of DIPL, the major fraud risk factor that the company faces is in the non-segregation of

important work departments. There is lack of authority and delegation of work systematically. In the

company, the accounts receivable department is handles by a single person, who manages all the work.

A single clerk does the verification of the books, making the payments, reconciling the amount and

asserting the validity of the records. A single person also handles the cash receivable department. A

single person does all the work from downloading the e receipts, making the collection, updating and

reconciling the book. All these leads to lack of establishment of duty and responsibility. If the power is

given in one hands, he can easily manipulate the accounts, as per his own preference and it will be hard

for the management to ascertain the same easily. It is thus important for the auditor to make sure that

the management has installed proper control systems. Work must be properly divided and it must be

authorised. Surprise checks of accounts must be done, so that any kind of error can be easily identified.

The second area where there might be fraud is in the installation of the new IT system. The

management installed the same in allot of haste, without undertaking nay precaution. There are high

chances that some personal motive of the management was involved in this case. The management had

done the same to save cost the wrong way or to manipulate the books. It is important on part of the

auditor to properly investigate into the matter; the auditor can also take expert advice to know the

poorer value of the system. Proper reconciliation of the cost and results must be done. In any case, if the

auditor feels that the magemnt is not giving the required level of support, the auditor can qualify the

audit report. It is the duty of the management, to provide the auditor with all the necessary information

that he might need to verify the viability of the accounts. All the important documents regarding the

8 | P a g e

Solution 3

Fraud occurs when the management or the employees of the company indulges in certain

activity like manipulation or records or defalcation of cash, for their own benefits. The work of the

auditor is to verify the records of the company and to make sure that any kind of fraud risk factor is

mitigated and removed. Fraud occurs because of the negligence of the management and it is important

that proper control be established to prevent the same. Identification of fraud risk factor is the work of

the management of the company and the auditor can help in mitigation of the same. While conducting

the audit, the auditor must apply such methods that help in identification of major fraud risk factors.

Often the management might be the culprit, the auditor should not rely on what the management

portrays and should apply his own research techniques before reaching a conclusion (Bae 2017).

In case of DIPL, the major fraud risk factor that the company faces is in the non-segregation of

important work departments. There is lack of authority and delegation of work systematically. In the

company, the accounts receivable department is handles by a single person, who manages all the work.

A single clerk does the verification of the books, making the payments, reconciling the amount and

asserting the validity of the records. A single person also handles the cash receivable department. A

single person does all the work from downloading the e receipts, making the collection, updating and

reconciling the book. All these leads to lack of establishment of duty and responsibility. If the power is

given in one hands, he can easily manipulate the accounts, as per his own preference and it will be hard

for the management to ascertain the same easily. It is thus important for the auditor to make sure that

the management has installed proper control systems. Work must be properly divided and it must be

authorised. Surprise checks of accounts must be done, so that any kind of error can be easily identified.

The second area where there might be fraud is in the installation of the new IT system. The

management installed the same in allot of haste, without undertaking nay precaution. There are high

chances that some personal motive of the management was involved in this case. The management had

done the same to save cost the wrong way or to manipulate the books. It is important on part of the

auditor to properly investigate into the matter; the auditor can also take expert advice to know the

poorer value of the system. Proper reconciliation of the cost and results must be done. In any case, if the

auditor feels that the magemnt is not giving the required level of support, the auditor can qualify the

audit report. It is the duty of the management, to provide the auditor with all the necessary information

that he might need to verify the viability of the accounts. All the important documents regarding the

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

project must be given to the auditor. The auditor can mitigate the major risks that the organisation

might face in these few ways (Sonu, Ahn & Choi 2017).

9 | P a g e

project must be given to the auditor. The auditor can mitigate the major risks that the organisation

might face in these few ways (Sonu, Ahn & Choi 2017).

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

References

Bae, SH 2017, 'The Association Between Corporate Tax Avoidance And Audit Efforts: Evidence From

Korea', Journal of Applied Business Research, vol 33, no. 1, pp. 153-172.

DeZoort, FT & Harrison, PD 2016, 'Understanding Auditors sense of Responsibility for detecting fraud

within organization', Journal of Business Ethics, pp. 1-18.

Fay, R & Negangard, EM 2017, 'Manual journal entry testing : Data analytics and the risk of fraud',

Journal of Accounting Education, vol 38, pp. 37-49.

Grenier, J 2017, 'Encouraging Professional Skepticism in the Industry Specialization Era', Journal of

Business Ethics, vol 142, no. 2, pp. 241-256.

Jones, P 2017, Statistical Sampling and Risk Analysis in Auditing, Routledge, NY.

Knechel, WB & Salterio, SE 2016, Auditing:Assurance and Risk, 4th edn, Routledge, New York.

Raiborn, C, Butler, JB & Martin, K 2016, 'The internal audit function: A prerequisite for Good

Governance', Journal of Corporate Accounting and Finance, vol 28, no. 2, pp. 10-21.

Sonu, CH, Ahn, H & Choi, A 2017, 'Audit fee pressure and audit risk: evidence from the financial crisis of

2008', Asia-Pacific Journal of Accounting & Economics , vol 24, no. 1-2, pp. 127-144.

10 | P a g e

References

Bae, SH 2017, 'The Association Between Corporate Tax Avoidance And Audit Efforts: Evidence From

Korea', Journal of Applied Business Research, vol 33, no. 1, pp. 153-172.

DeZoort, FT & Harrison, PD 2016, 'Understanding Auditors sense of Responsibility for detecting fraud

within organization', Journal of Business Ethics, pp. 1-18.

Fay, R & Negangard, EM 2017, 'Manual journal entry testing : Data analytics and the risk of fraud',

Journal of Accounting Education, vol 38, pp. 37-49.

Grenier, J 2017, 'Encouraging Professional Skepticism in the Industry Specialization Era', Journal of

Business Ethics, vol 142, no. 2, pp. 241-256.

Jones, P 2017, Statistical Sampling and Risk Analysis in Auditing, Routledge, NY.

Knechel, WB & Salterio, SE 2016, Auditing:Assurance and Risk, 4th edn, Routledge, New York.

Raiborn, C, Butler, JB & Martin, K 2016, 'The internal audit function: A prerequisite for Good

Governance', Journal of Corporate Accounting and Finance, vol 28, no. 2, pp. 10-21.

Sonu, CH, Ahn, H & Choi, A 2017, 'Audit fee pressure and audit risk: evidence from the financial crisis of

2008', Asia-Pacific Journal of Accounting & Economics , vol 24, no. 1-2, pp. 127-144.

10 | P a g e

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.