Corporate Finance: Analyzing Investment Decisions with WACC and NPV

VerifiedAdded on 2020/05/28

|9

|1402

|28

Homework Assignment

AI Summary

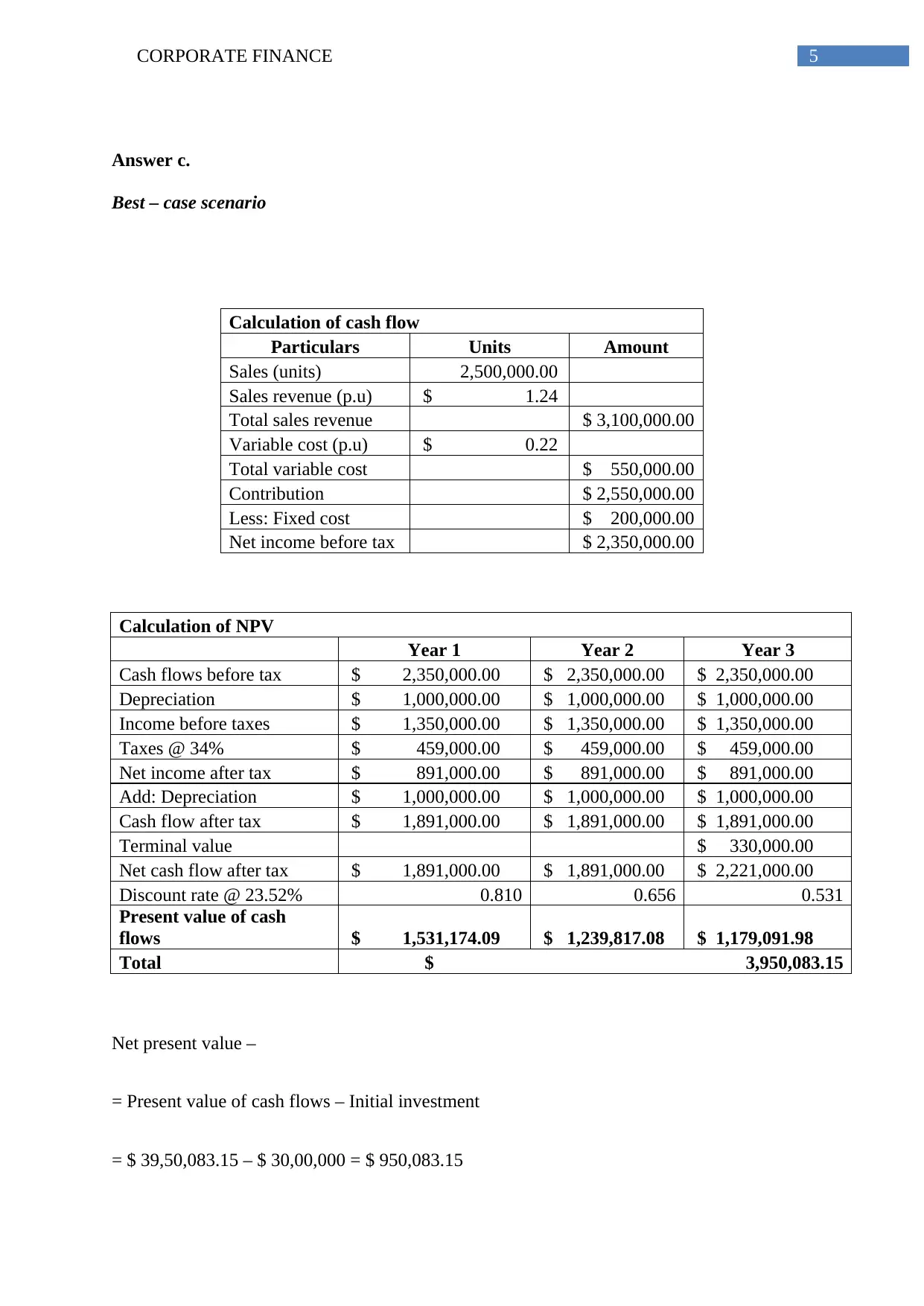

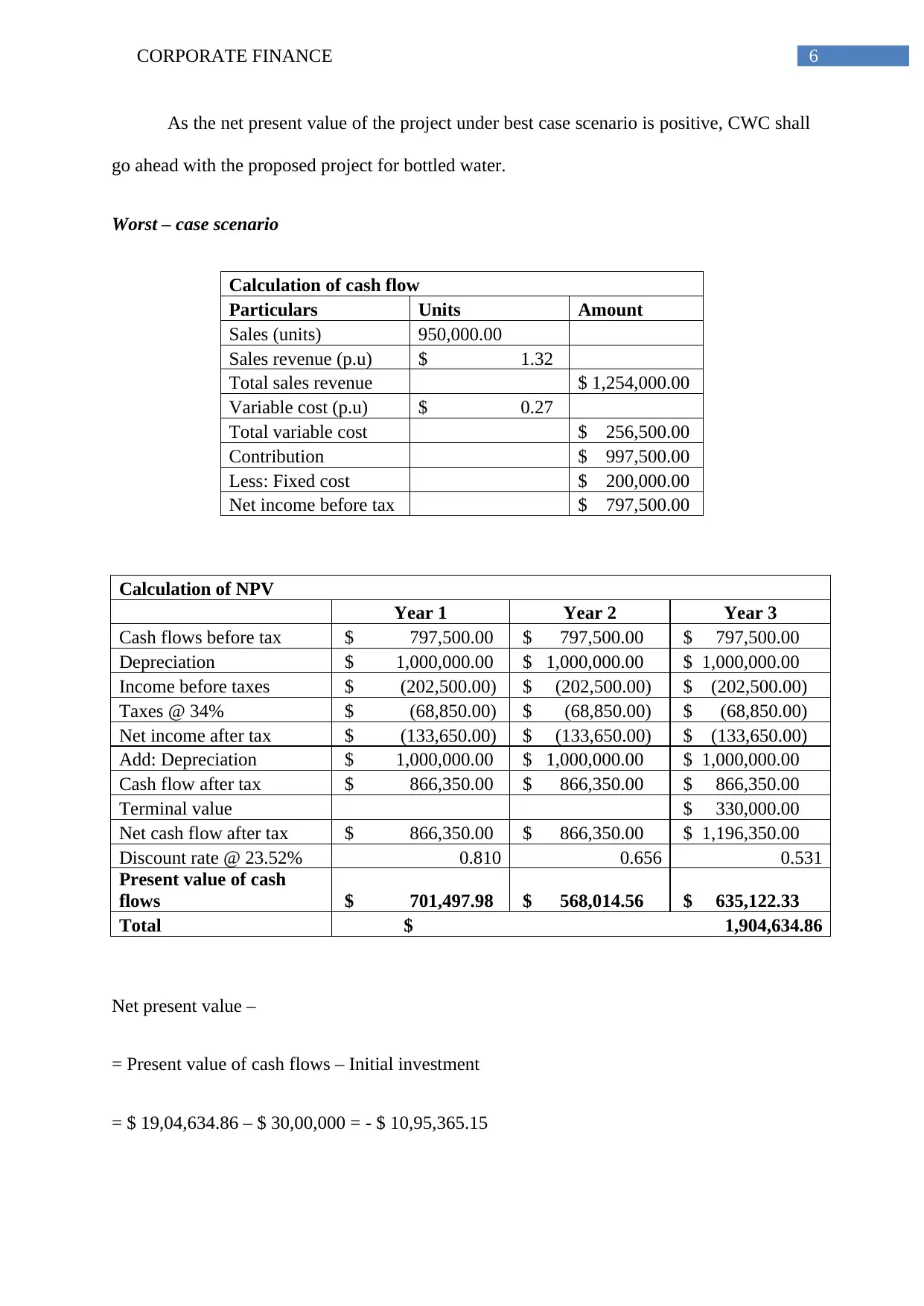

This corporate finance assignment delves into several key areas of financial analysis, including the calculation of Weighted Average Cost of Capital (WACC) and Net Present Value (NPV) for a hypothetical project. The assignment begins by calculating the WACC for a company, considering both the cost of equity and the cost of bonds. Subsequently, it proceeds to analyze a proposed project, determining its NPV under normal conditions, as well as under best-case and worst-case scenarios. The analysis involves detailed cash flow projections, including the consideration of depreciation, taxes, and terminal value. The student then provides recommendations based on the NPV results and discusses the factors that influence investment decisions, emphasizing the importance of financial analysis in determining project feasibility. The assignment concludes with a discussion on the importance of considering various scenarios and the role of a financial analyst in presenting the findings to management.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.