Financial Management Homework: Budgeting, Make or Buy, Cash Flow

VerifiedAdded on 2020/04/01

|11

|2683

|30

Homework Assignment

AI Summary

This financial management assignment solution covers several key areas including budgeting, make or buy decisions, flexible budgeting, cash flow analysis, and capital investment decisions. The budgeting section includes the preparation of annual purchases, operating expenses, and abbreviated budgeted income statements under both sole proprietorship and limited liability scenarios, and a recommendation to change to limited liability. The make-or-buy decision analyzes whether a company should manufacture a component internally or purchase it from an external supplier, considering variable and fixed costs, and contribution margin. Flexible budgeting is explored through variance analysis, comparing budgeted and actual expenses, and determining the impact of increased sales. A detailed cash budget is presented, projecting cash receipts and disbursements, and evaluating the feasibility of a significant equipment purchase. Finally, capital investment decisions are analyzed using techniques such as payback period, discounted payback period, and net present value (NPV) to evaluate the profitability and viability of two mutually exclusive projects.

[Type the company name]

Financial Management

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

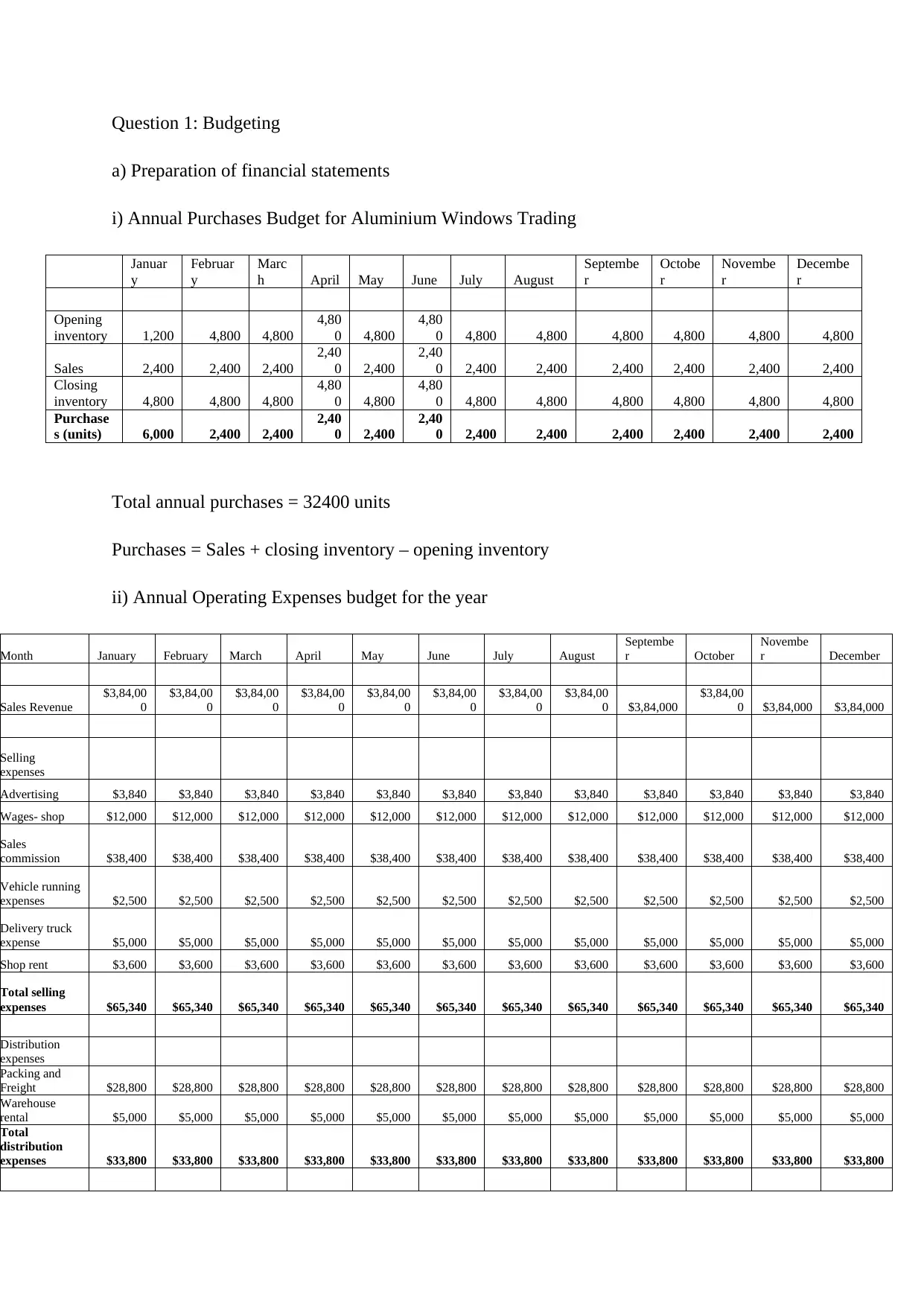

Question 1: Budgeting

a) Preparation of financial statements

i) Annual Purchases Budget for Aluminium Windows Trading

Januar

y

Februar

y

Marc

h April May June July August

Septembe

r

Octobe

r

Novembe

r

Decembe

r

Opening

inventory 1,200 4,800 4,800

4,80

0 4,800

4,80

0 4,800 4,800 4,800 4,800 4,800 4,800

Sales 2,400 2,400 2,400

2,40

0 2,400

2,40

0 2,400 2,400 2,400 2,400 2,400 2,400

Closing

inventory 4,800 4,800 4,800

4,80

0 4,800

4,80

0 4,800 4,800 4,800 4,800 4,800 4,800

Purchase

s (units) 6,000 2,400 2,400

2,40

0 2,400

2,40

0 2,400 2,400 2,400 2,400 2,400 2,400

Total annual purchases = 32400 units

Purchases = Sales + closing inventory – opening inventory

ii) Annual Operating Expenses budget for the year

Month January February March April May June July August

Septembe

r October

Novembe

r December

Sales Revenue

$3,84,00

0

$3,84,00

0

$3,84,00

0

$3,84,00

0

$3,84,00

0

$3,84,00

0

$3,84,00

0

$3,84,00

0 $3,84,000

$3,84,00

0 $3,84,000 $3,84,000

Selling

expenses

Advertising $3,840 $3,840 $3,840 $3,840 $3,840 $3,840 $3,840 $3,840 $3,840 $3,840 $3,840 $3,840

Wages- shop $12,000 $12,000 $12,000 $12,000 $12,000 $12,000 $12,000 $12,000 $12,000 $12,000 $12,000 $12,000

Sales

commission $38,400 $38,400 $38,400 $38,400 $38,400 $38,400 $38,400 $38,400 $38,400 $38,400 $38,400 $38,400

Vehicle running

expenses $2,500 $2,500 $2,500 $2,500 $2,500 $2,500 $2,500 $2,500 $2,500 $2,500 $2,500 $2,500

Delivery truck

expense $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000

Shop rent $3,600 $3,600 $3,600 $3,600 $3,600 $3,600 $3,600 $3,600 $3,600 $3,600 $3,600 $3,600

Total selling

expenses $65,340 $65,340 $65,340 $65,340 $65,340 $65,340 $65,340 $65,340 $65,340 $65,340 $65,340 $65,340

Distribution

expenses

Packing and

Freight $28,800 $28,800 $28,800 $28,800 $28,800 $28,800 $28,800 $28,800 $28,800 $28,800 $28,800 $28,800

Warehouse

rental $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000

Total

distribution

expenses $33,800 $33,800 $33,800 $33,800 $33,800 $33,800 $33,800 $33,800 $33,800 $33,800 $33,800 $33,800

a) Preparation of financial statements

i) Annual Purchases Budget for Aluminium Windows Trading

Januar

y

Februar

y

Marc

h April May June July August

Septembe

r

Octobe

r

Novembe

r

Decembe

r

Opening

inventory 1,200 4,800 4,800

4,80

0 4,800

4,80

0 4,800 4,800 4,800 4,800 4,800 4,800

Sales 2,400 2,400 2,400

2,40

0 2,400

2,40

0 2,400 2,400 2,400 2,400 2,400 2,400

Closing

inventory 4,800 4,800 4,800

4,80

0 4,800

4,80

0 4,800 4,800 4,800 4,800 4,800 4,800

Purchase

s (units) 6,000 2,400 2,400

2,40

0 2,400

2,40

0 2,400 2,400 2,400 2,400 2,400 2,400

Total annual purchases = 32400 units

Purchases = Sales + closing inventory – opening inventory

ii) Annual Operating Expenses budget for the year

Month January February March April May June July August

Septembe

r October

Novembe

r December

Sales Revenue

$3,84,00

0

$3,84,00

0

$3,84,00

0

$3,84,00

0

$3,84,00

0

$3,84,00

0

$3,84,00

0

$3,84,00

0 $3,84,000

$3,84,00

0 $3,84,000 $3,84,000

Selling

expenses

Advertising $3,840 $3,840 $3,840 $3,840 $3,840 $3,840 $3,840 $3,840 $3,840 $3,840 $3,840 $3,840

Wages- shop $12,000 $12,000 $12,000 $12,000 $12,000 $12,000 $12,000 $12,000 $12,000 $12,000 $12,000 $12,000

Sales

commission $38,400 $38,400 $38,400 $38,400 $38,400 $38,400 $38,400 $38,400 $38,400 $38,400 $38,400 $38,400

Vehicle running

expenses $2,500 $2,500 $2,500 $2,500 $2,500 $2,500 $2,500 $2,500 $2,500 $2,500 $2,500 $2,500

Delivery truck

expense $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000

Shop rent $3,600 $3,600 $3,600 $3,600 $3,600 $3,600 $3,600 $3,600 $3,600 $3,600 $3,600 $3,600

Total selling

expenses $65,340 $65,340 $65,340 $65,340 $65,340 $65,340 $65,340 $65,340 $65,340 $65,340 $65,340 $65,340

Distribution

expenses

Packing and

Freight $28,800 $28,800 $28,800 $28,800 $28,800 $28,800 $28,800 $28,800 $28,800 $28,800 $28,800 $28,800

Warehouse

rental $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000 $5,000

Total

distribution

expenses $33,800 $33,800 $33,800 $33,800 $33,800 $33,800 $33,800 $33,800 $33,800 $33,800 $33,800 $33,800

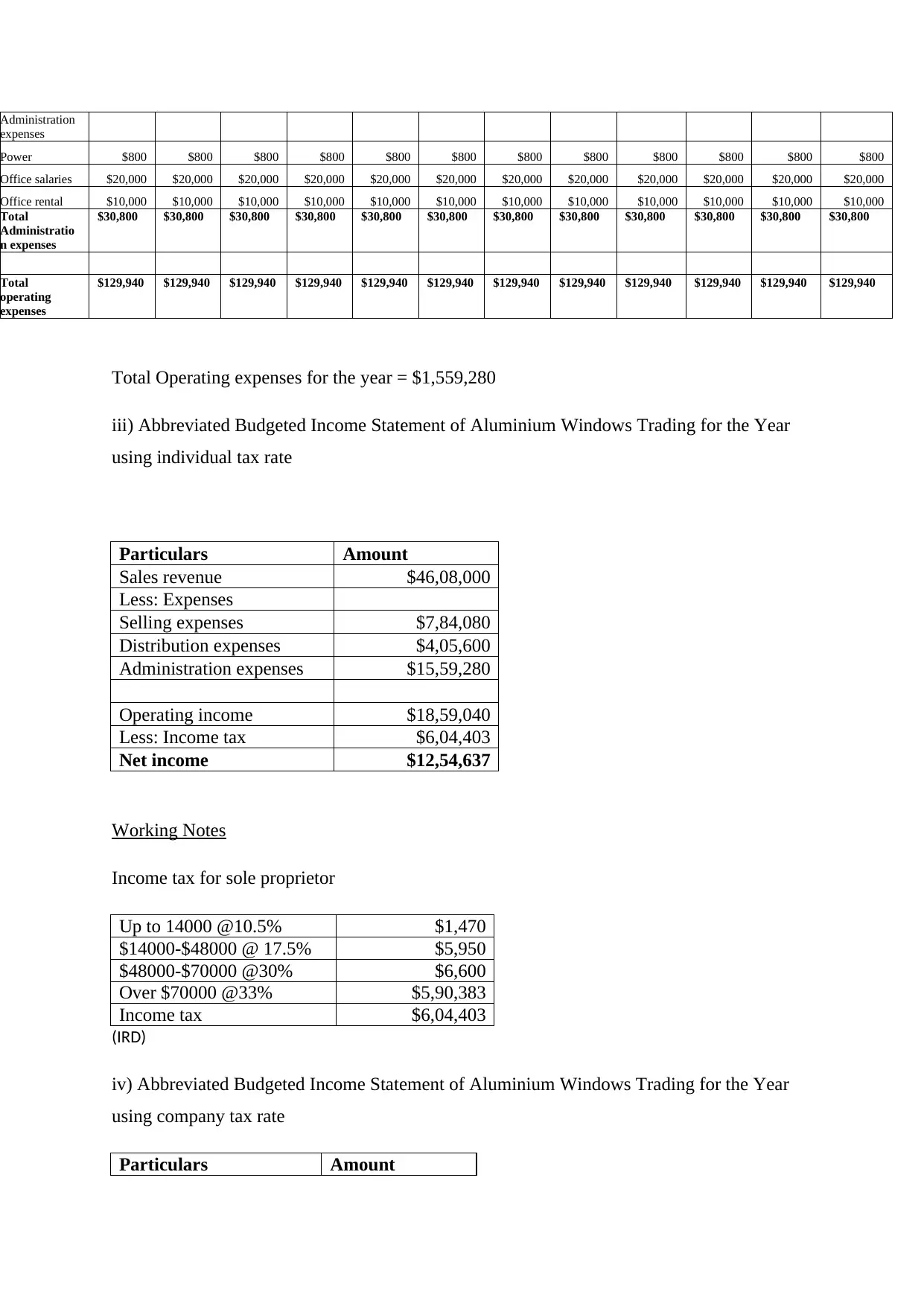

Administration

expenses

Power $800 $800 $800 $800 $800 $800 $800 $800 $800 $800 $800 $800

Office salaries $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000

Office rental $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000

Total

Administratio

n expenses

$30,800 $30,800 $30,800 $30,800 $30,800 $30,800 $30,800 $30,800 $30,800 $30,800 $30,800 $30,800

Total

operating

expenses

$129,940 $129,940 $129,940 $129,940 $129,940 $129,940 $129,940 $129,940 $129,940 $129,940 $129,940 $129,940

Total Operating expenses for the year = $1,559,280

iii) Abbreviated Budgeted Income Statement of Aluminium Windows Trading for the Year

using individual tax rate

Particulars Amount

Sales revenue $46,08,000

Less: Expenses

Selling expenses $7,84,080

Distribution expenses $4,05,600

Administration expenses $15,59,280

Operating income $18,59,040

Less: Income tax $6,04,403

Net income $12,54,637

Working Notes

Income tax for sole proprietor

Up to 14000 @10.5% $1,470

$14000-$48000 @ 17.5% $5,950

$48000-$70000 @30% $6,600

Over $70000 @33% $5,90,383

Income tax $6,04,403

(IRD)

iv) Abbreviated Budgeted Income Statement of Aluminium Windows Trading for the Year

using company tax rate

Particulars Amount

expenses

Power $800 $800 $800 $800 $800 $800 $800 $800 $800 $800 $800 $800

Office salaries $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000

Office rental $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000 $10,000

Total

Administratio

n expenses

$30,800 $30,800 $30,800 $30,800 $30,800 $30,800 $30,800 $30,800 $30,800 $30,800 $30,800 $30,800

Total

operating

expenses

$129,940 $129,940 $129,940 $129,940 $129,940 $129,940 $129,940 $129,940 $129,940 $129,940 $129,940 $129,940

Total Operating expenses for the year = $1,559,280

iii) Abbreviated Budgeted Income Statement of Aluminium Windows Trading for the Year

using individual tax rate

Particulars Amount

Sales revenue $46,08,000

Less: Expenses

Selling expenses $7,84,080

Distribution expenses $4,05,600

Administration expenses $15,59,280

Operating income $18,59,040

Less: Income tax $6,04,403

Net income $12,54,637

Working Notes

Income tax for sole proprietor

Up to 14000 @10.5% $1,470

$14000-$48000 @ 17.5% $5,950

$48000-$70000 @30% $6,600

Over $70000 @33% $5,90,383

Income tax $6,04,403

(IRD)

iv) Abbreviated Budgeted Income Statement of Aluminium Windows Trading for the Year

using company tax rate

Particulars Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

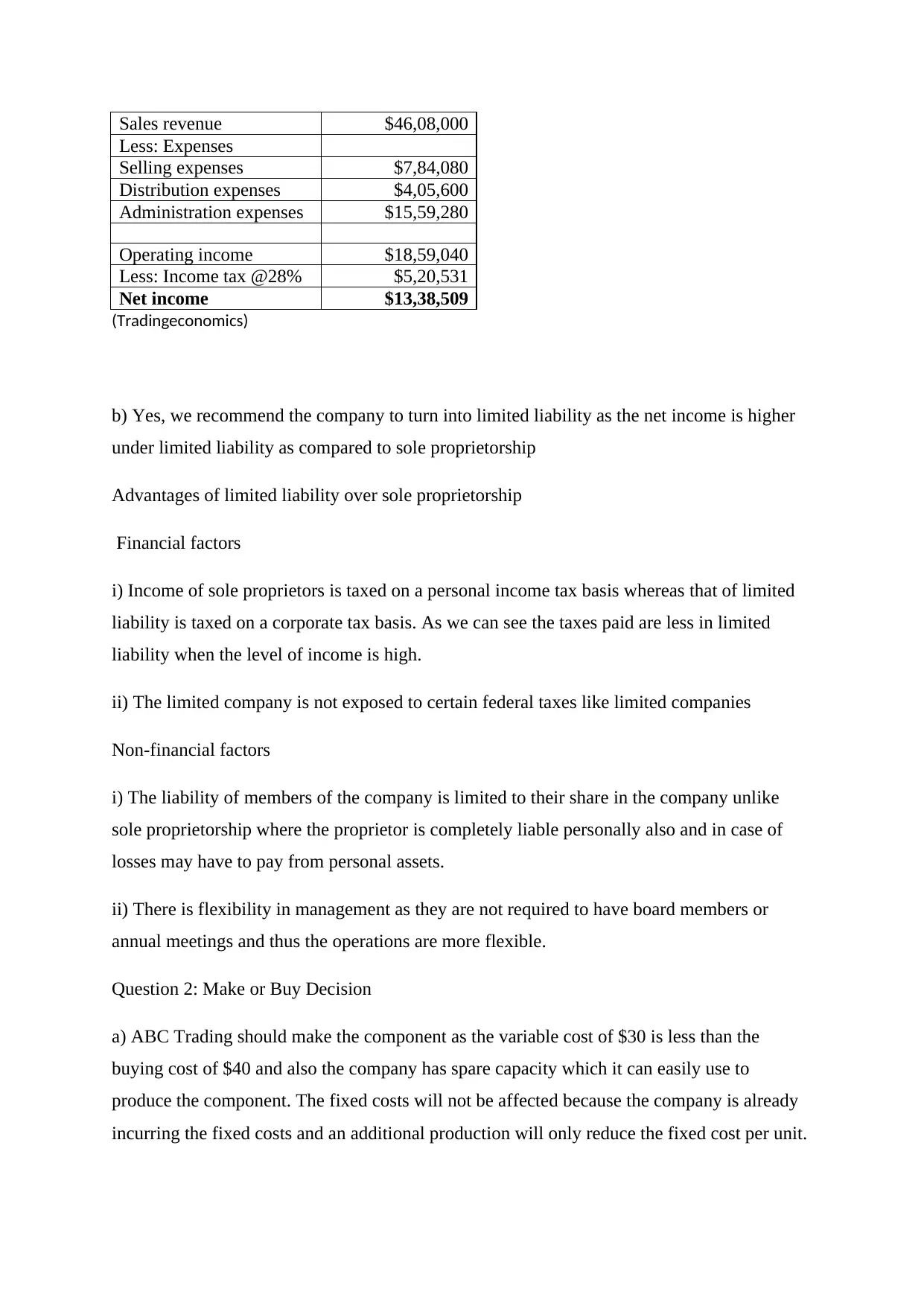

Sales revenue $46,08,000

Less: Expenses

Selling expenses $7,84,080

Distribution expenses $4,05,600

Administration expenses $15,59,280

Operating income $18,59,040

Less: Income tax @28% $5,20,531

Net income $13,38,509

(Tradingeconomics)

b) Yes, we recommend the company to turn into limited liability as the net income is higher

under limited liability as compared to sole proprietorship

Advantages of limited liability over sole proprietorship

Financial factors

i) Income of sole proprietors is taxed on a personal income tax basis whereas that of limited

liability is taxed on a corporate tax basis. As we can see the taxes paid are less in limited

liability when the level of income is high.

ii) The limited company is not exposed to certain federal taxes like limited companies

Non-financial factors

i) The liability of members of the company is limited to their share in the company unlike

sole proprietorship where the proprietor is completely liable personally also and in case of

losses may have to pay from personal assets.

ii) There is flexibility in management as they are not required to have board members or

annual meetings and thus the operations are more flexible.

Question 2: Make or Buy Decision

a) ABC Trading should make the component as the variable cost of $30 is less than the

buying cost of $40 and also the company has spare capacity which it can easily use to

produce the component. The fixed costs will not be affected because the company is already

incurring the fixed costs and an additional production will only reduce the fixed cost per unit.

Less: Expenses

Selling expenses $7,84,080

Distribution expenses $4,05,600

Administration expenses $15,59,280

Operating income $18,59,040

Less: Income tax @28% $5,20,531

Net income $13,38,509

(Tradingeconomics)

b) Yes, we recommend the company to turn into limited liability as the net income is higher

under limited liability as compared to sole proprietorship

Advantages of limited liability over sole proprietorship

Financial factors

i) Income of sole proprietors is taxed on a personal income tax basis whereas that of limited

liability is taxed on a corporate tax basis. As we can see the taxes paid are less in limited

liability when the level of income is high.

ii) The limited company is not exposed to certain federal taxes like limited companies

Non-financial factors

i) The liability of members of the company is limited to their share in the company unlike

sole proprietorship where the proprietor is completely liable personally also and in case of

losses may have to pay from personal assets.

ii) There is flexibility in management as they are not required to have board members or

annual meetings and thus the operations are more flexible.

Question 2: Make or Buy Decision

a) ABC Trading should make the component as the variable cost of $30 is less than the

buying cost of $40 and also the company has spare capacity which it can easily use to

produce the component. The fixed costs will not be affected because the company is already

incurring the fixed costs and an additional production will only reduce the fixed cost per unit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The company will save $10 by making the product. The use of spare capacity will not

increase the fixed costs.

b) If ABC Trading produced the component at a cost of $30, it will lose contribution margin

from another product of $25 so the total cost of manufacturing the component will be $55

which is more than the buying cost. Hence the company should buy at $40 rather than

making in this case.

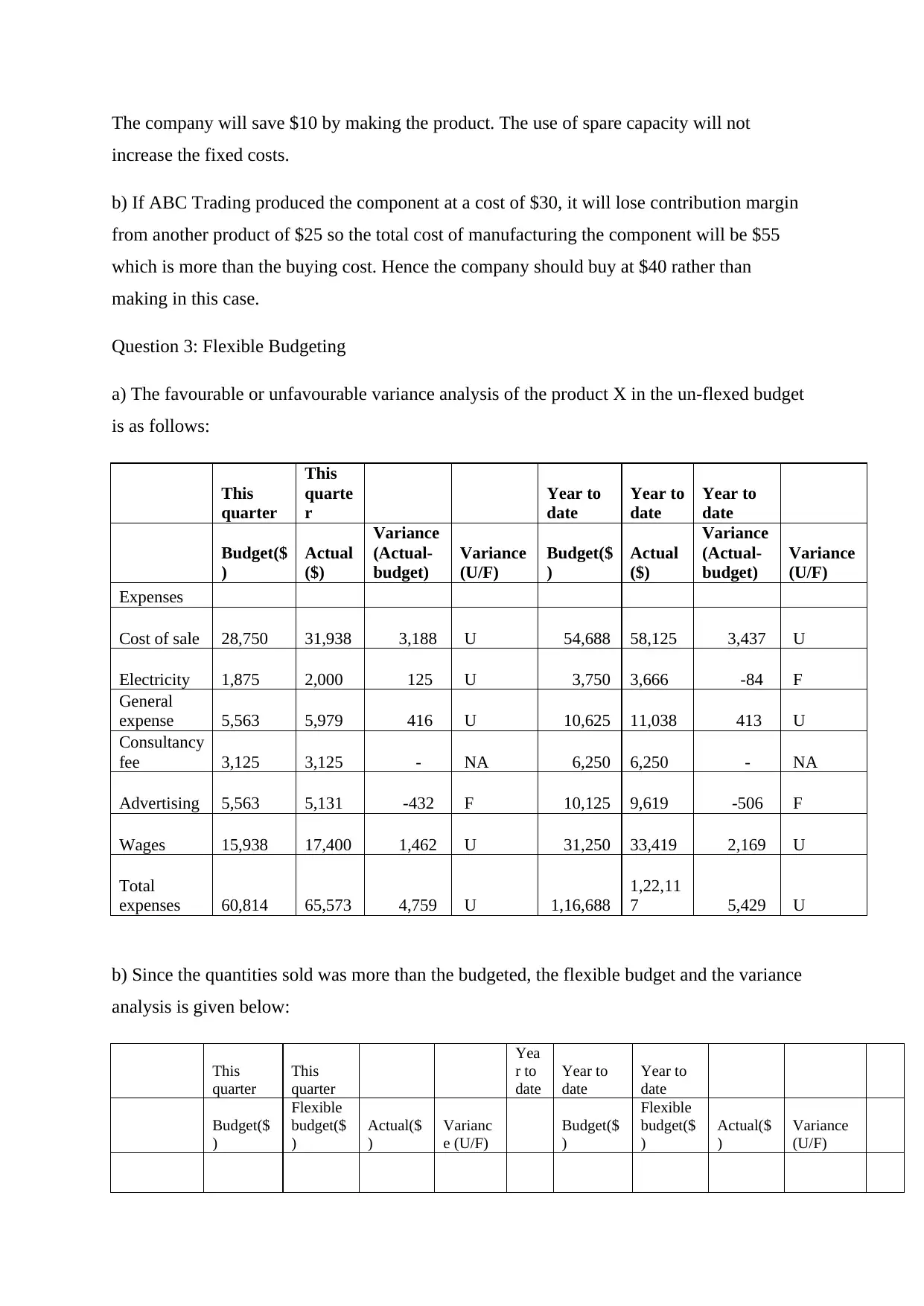

Question 3: Flexible Budgeting

a) The favourable or unfavourable variance analysis of the product X in the un-flexed budget

is as follows:

This

quarter

This

quarte

r

Year to

date

Year to

date

Year to

date

Budget($

)

Actual

($)

Variance

(Actual-

budget)

Variance

(U/F)

Budget($

)

Actual

($)

Variance

(Actual-

budget)

Variance

(U/F)

Expenses

Cost of sale 28,750 31,938 3,188 U 54,688 58,125 3,437 U

Electricity 1,875 2,000 125 U 3,750 3,666 -84 F

General

expense 5,563 5,979 416 U 10,625 11,038 413 U

Consultancy

fee 3,125 3,125 - NA 6,250 6,250 - NA

Advertising 5,563 5,131 -432 F 10,125 9,619 -506 F

Wages 15,938 17,400 1,462 U 31,250 33,419 2,169 U

Total

expenses 60,814 65,573 4,759 U 1,16,688

1,22,11

7 5,429 U

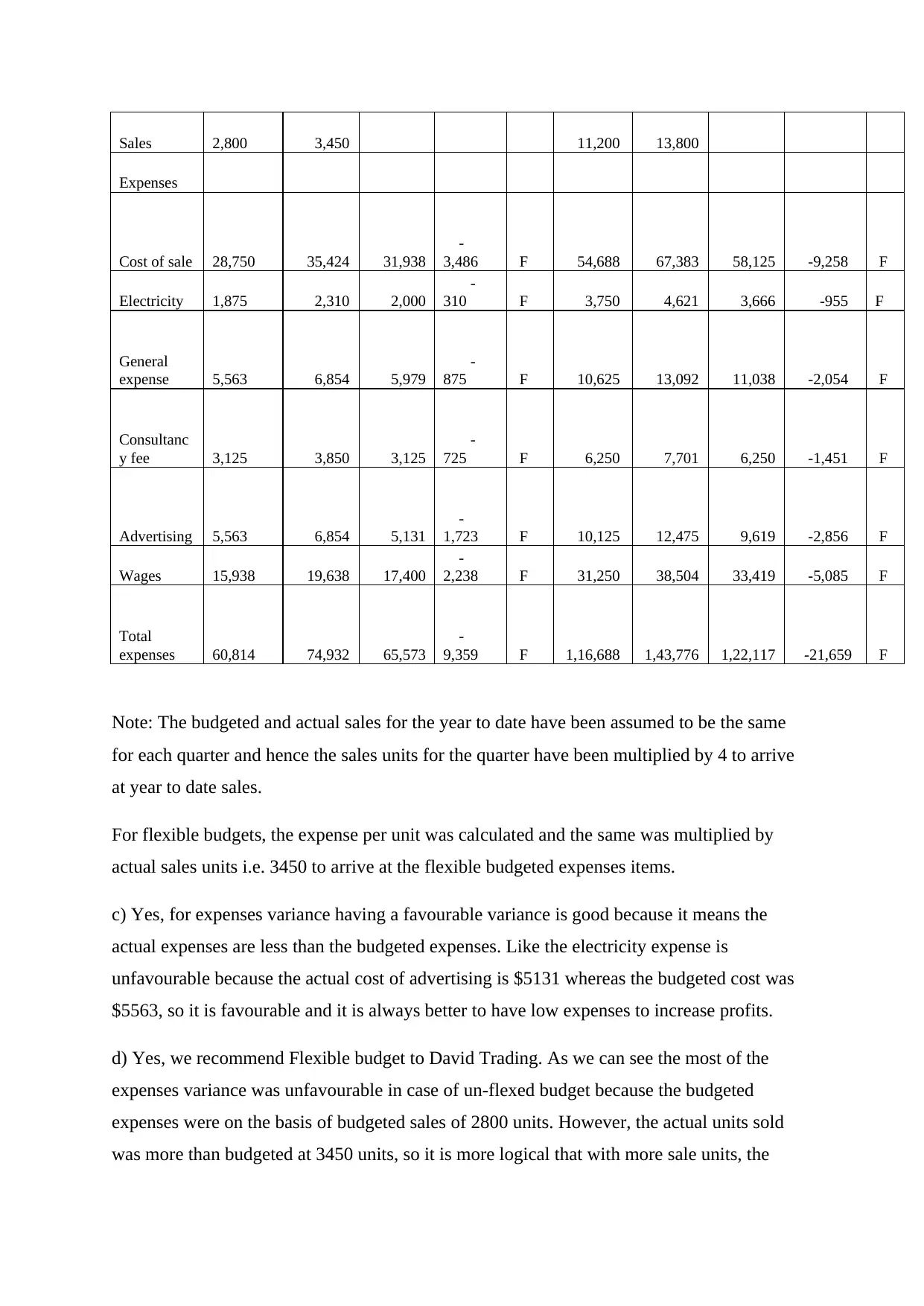

b) Since the quantities sold was more than the budgeted, the flexible budget and the variance

analysis is given below:

This

quarter

This

quarter

Yea

r to

date

Year to

date

Year to

date

Budget($

)

Flexible

budget($

)

Actual($

)

Varianc

e (U/F)

Budget($

)

Flexible

budget($

)

Actual($

)

Variance

(U/F)

increase the fixed costs.

b) If ABC Trading produced the component at a cost of $30, it will lose contribution margin

from another product of $25 so the total cost of manufacturing the component will be $55

which is more than the buying cost. Hence the company should buy at $40 rather than

making in this case.

Question 3: Flexible Budgeting

a) The favourable or unfavourable variance analysis of the product X in the un-flexed budget

is as follows:

This

quarter

This

quarte

r

Year to

date

Year to

date

Year to

date

Budget($

)

Actual

($)

Variance

(Actual-

budget)

Variance

(U/F)

Budget($

)

Actual

($)

Variance

(Actual-

budget)

Variance

(U/F)

Expenses

Cost of sale 28,750 31,938 3,188 U 54,688 58,125 3,437 U

Electricity 1,875 2,000 125 U 3,750 3,666 -84 F

General

expense 5,563 5,979 416 U 10,625 11,038 413 U

Consultancy

fee 3,125 3,125 - NA 6,250 6,250 - NA

Advertising 5,563 5,131 -432 F 10,125 9,619 -506 F

Wages 15,938 17,400 1,462 U 31,250 33,419 2,169 U

Total

expenses 60,814 65,573 4,759 U 1,16,688

1,22,11

7 5,429 U

b) Since the quantities sold was more than the budgeted, the flexible budget and the variance

analysis is given below:

This

quarter

This

quarter

Yea

r to

date

Year to

date

Year to

date

Budget($

)

Flexible

budget($

)

Actual($

)

Varianc

e (U/F)

Budget($

)

Flexible

budget($

)

Actual($

)

Variance

(U/F)

Sales 2,800 3,450 11,200 13,800

Expenses

Cost of sale 28,750 35,424 31,938

-

3,486 F 54,688 67,383 58,125 -9,258 F

Electricity 1,875 2,310 2,000

-

310 F 3,750 4,621 3,666 -955 F

General

expense 5,563 6,854 5,979

-

875 F 10,625 13,092 11,038 -2,054 F

Consultanc

y fee 3,125 3,850 3,125

-

725 F 6,250 7,701 6,250 -1,451 F

Advertising 5,563 6,854 5,131

-

1,723 F 10,125 12,475 9,619 -2,856 F

Wages 15,938 19,638 17,400

-

2,238 F 31,250 38,504 33,419 -5,085 F

Total

expenses 60,814 74,932 65,573

-

9,359 F 1,16,688 1,43,776 1,22,117 -21,659 F

Note: The budgeted and actual sales for the year to date have been assumed to be the same

for each quarter and hence the sales units for the quarter have been multiplied by 4 to arrive

at year to date sales.

For flexible budgets, the expense per unit was calculated and the same was multiplied by

actual sales units i.e. 3450 to arrive at the flexible budgeted expenses items.

c) Yes, for expenses variance having a favourable variance is good because it means the

actual expenses are less than the budgeted expenses. Like the electricity expense is

unfavourable because the actual cost of advertising is $5131 whereas the budgeted cost was

$5563, so it is favourable and it is always better to have low expenses to increase profits.

d) Yes, we recommend Flexible budget to David Trading. As we can see the most of the

expenses variance was unfavourable in case of un-flexed budget because the budgeted

expenses were on the basis of budgeted sales of 2800 units. However, the actual units sold

was more than budgeted at 3450 units, so it is more logical that with more sale units, the

Expenses

Cost of sale 28,750 35,424 31,938

-

3,486 F 54,688 67,383 58,125 -9,258 F

Electricity 1,875 2,310 2,000

-

310 F 3,750 4,621 3,666 -955 F

General

expense 5,563 6,854 5,979

-

875 F 10,625 13,092 11,038 -2,054 F

Consultanc

y fee 3,125 3,850 3,125

-

725 F 6,250 7,701 6,250 -1,451 F

Advertising 5,563 6,854 5,131

-

1,723 F 10,125 12,475 9,619 -2,856 F

Wages 15,938 19,638 17,400

-

2,238 F 31,250 38,504 33,419 -5,085 F

Total

expenses 60,814 74,932 65,573

-

9,359 F 1,16,688 1,43,776 1,22,117 -21,659 F

Note: The budgeted and actual sales for the year to date have been assumed to be the same

for each quarter and hence the sales units for the quarter have been multiplied by 4 to arrive

at year to date sales.

For flexible budgets, the expense per unit was calculated and the same was multiplied by

actual sales units i.e. 3450 to arrive at the flexible budgeted expenses items.

c) Yes, for expenses variance having a favourable variance is good because it means the

actual expenses are less than the budgeted expenses. Like the electricity expense is

unfavourable because the actual cost of advertising is $5131 whereas the budgeted cost was

$5563, so it is favourable and it is always better to have low expenses to increase profits.

d) Yes, we recommend Flexible budget to David Trading. As we can see the most of the

expenses variance was unfavourable in case of un-flexed budget because the budgeted

expenses were on the basis of budgeted sales of 2800 units. However, the actual units sold

was more than budgeted at 3450 units, so it is more logical that with more sale units, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

budgeted expenses should also increase according to the increased sales. Then the flexible

budgeted expenses should be compared to the actual expenses which are at 3450 units’ level

of sales. Under flexible budget, all the expenses variances have become positive or

favourable.

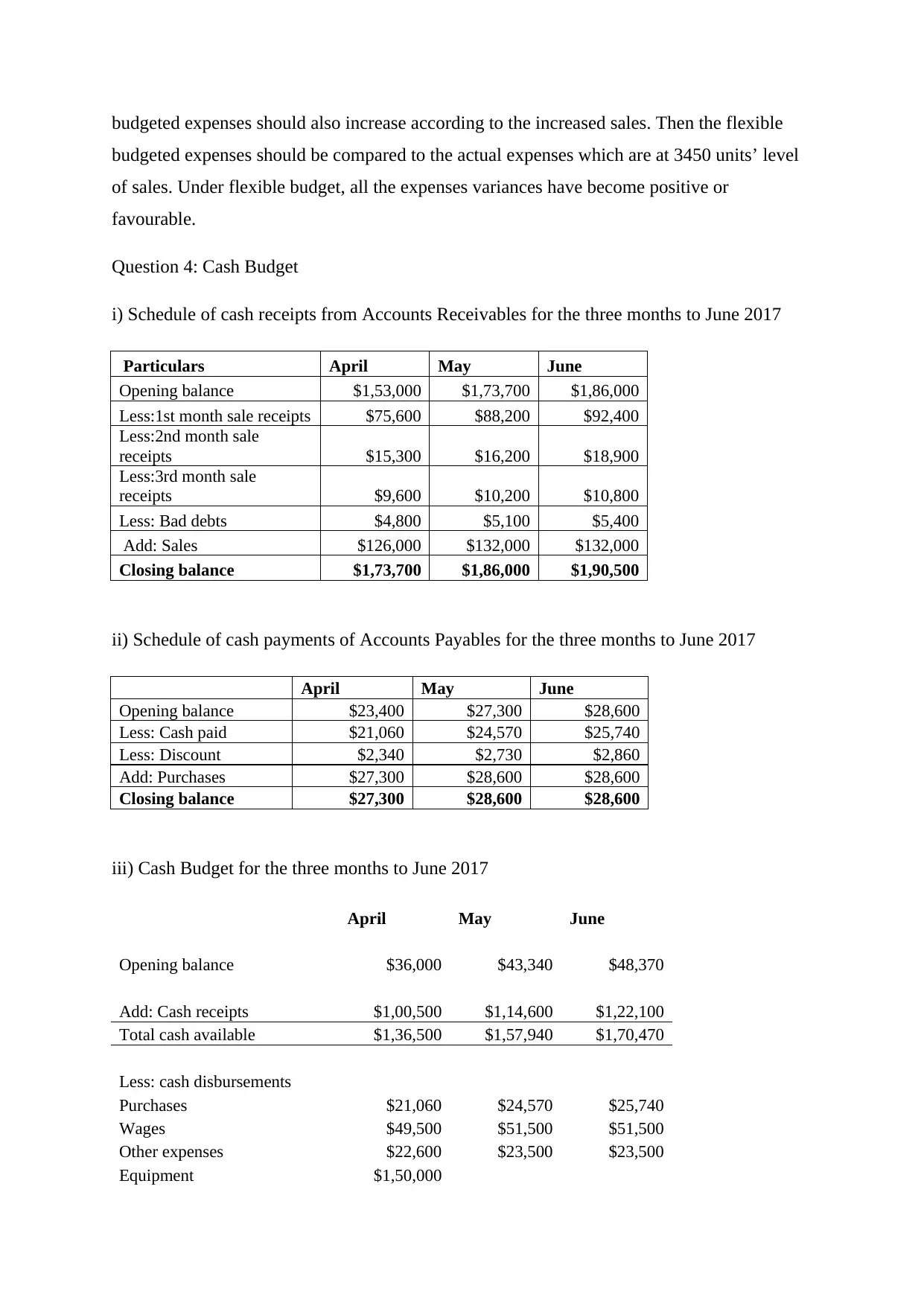

Question 4: Cash Budget

i) Schedule of cash receipts from Accounts Receivables for the three months to June 2017

Particulars April May June

Opening balance $1,53,000 $1,73,700 $1,86,000

Less:1st month sale receipts $75,600 $88,200 $92,400

Less:2nd month sale

receipts $15,300 $16,200 $18,900

Less:3rd month sale

receipts $9,600 $10,200 $10,800

Less: Bad debts $4,800 $5,100 $5,400

Add: Sales $126,000 $132,000 $132,000

Closing balance $1,73,700 $1,86,000 $1,90,500

ii) Schedule of cash payments of Accounts Payables for the three months to June 2017

April May June

Opening balance $23,400 $27,300 $28,600

Less: Cash paid $21,060 $24,570 $25,740

Less: Discount $2,340 $2,730 $2,860

Add: Purchases $27,300 $28,600 $28,600

Closing balance $27,300 $28,600 $28,600

iii) Cash Budget for the three months to June 2017

April May June

Opening balance $36,000 $43,340 $48,370

Add: Cash receipts $1,00,500 $1,14,600 $1,22,100

Total cash available $1,36,500 $1,57,940 $1,70,470

Less: cash disbursements

Purchases $21,060 $24,570 $25,740

Wages $49,500 $51,500 $51,500

Other expenses $22,600 $23,500 $23,500

Equipment $1,50,000

budgeted expenses should be compared to the actual expenses which are at 3450 units’ level

of sales. Under flexible budget, all the expenses variances have become positive or

favourable.

Question 4: Cash Budget

i) Schedule of cash receipts from Accounts Receivables for the three months to June 2017

Particulars April May June

Opening balance $1,53,000 $1,73,700 $1,86,000

Less:1st month sale receipts $75,600 $88,200 $92,400

Less:2nd month sale

receipts $15,300 $16,200 $18,900

Less:3rd month sale

receipts $9,600 $10,200 $10,800

Less: Bad debts $4,800 $5,100 $5,400

Add: Sales $126,000 $132,000 $132,000

Closing balance $1,73,700 $1,86,000 $1,90,500

ii) Schedule of cash payments of Accounts Payables for the three months to June 2017

April May June

Opening balance $23,400 $27,300 $28,600

Less: Cash paid $21,060 $24,570 $25,740

Less: Discount $2,340 $2,730 $2,860

Add: Purchases $27,300 $28,600 $28,600

Closing balance $27,300 $28,600 $28,600

iii) Cash Budget for the three months to June 2017

April May June

Opening balance $36,000 $43,340 $48,370

Add: Cash receipts $1,00,500 $1,14,600 $1,22,100

Total cash available $1,36,500 $1,57,940 $1,70,470

Less: cash disbursements

Purchases $21,060 $24,570 $25,740

Wages $49,500 $51,500 $51,500

Other expenses $22,600 $23,500 $23,500

Equipment $1,50,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

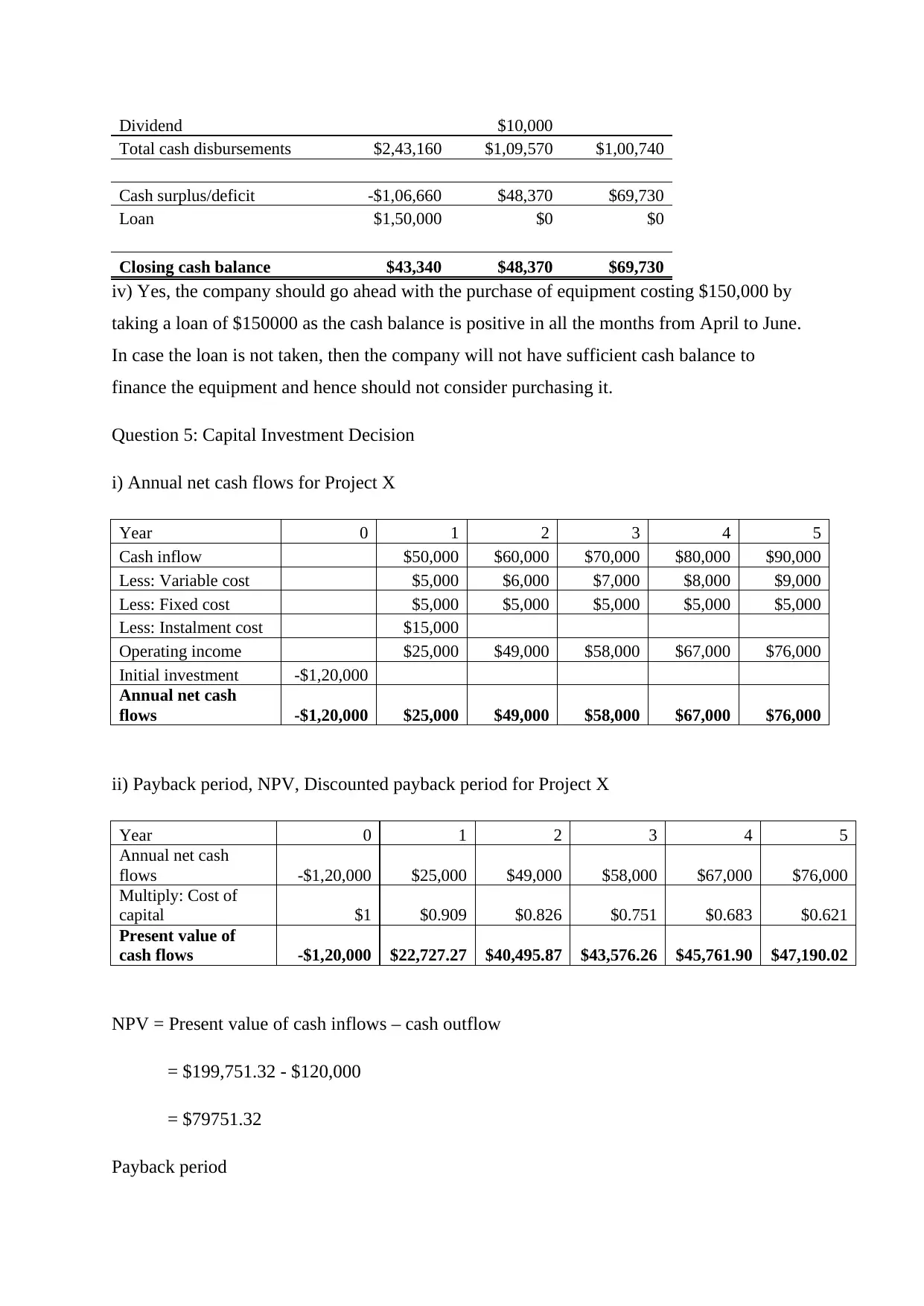

Dividend $10,000

Total cash disbursements $2,43,160 $1,09,570 $1,00,740

Cash surplus/deficit -$1,06,660 $48,370 $69,730

Loan $1,50,000 $0 $0

Closing cash balance $43,340 $48,370 $69,730

iv) Yes, the company should go ahead with the purchase of equipment costing $150,000 by

taking a loan of $150000 as the cash balance is positive in all the months from April to June.

In case the loan is not taken, then the company will not have sufficient cash balance to

finance the equipment and hence should not consider purchasing it.

Question 5: Capital Investment Decision

i) Annual net cash flows for Project X

Year 0 1 2 3 4 5

Cash inflow $50,000 $60,000 $70,000 $80,000 $90,000

Less: Variable cost $5,000 $6,000 $7,000 $8,000 $9,000

Less: Fixed cost $5,000 $5,000 $5,000 $5,000 $5,000

Less: Instalment cost $15,000

Operating income $25,000 $49,000 $58,000 $67,000 $76,000

Initial investment -$1,20,000

Annual net cash

flows -$1,20,000 $25,000 $49,000 $58,000 $67,000 $76,000

ii) Payback period, NPV, Discounted payback period for Project X

Year 0 1 2 3 4 5

Annual net cash

flows -$1,20,000 $25,000 $49,000 $58,000 $67,000 $76,000

Multiply: Cost of

capital $1 $0.909 $0.826 $0.751 $0.683 $0.621

Present value of

cash flows -$1,20,000 $22,727.27 $40,495.87 $43,576.26 $45,761.90 $47,190.02

NPV = Present value of cash inflows – cash outflow

= $199,751.32 - $120,000

= $79751.32

Payback period

Total cash disbursements $2,43,160 $1,09,570 $1,00,740

Cash surplus/deficit -$1,06,660 $48,370 $69,730

Loan $1,50,000 $0 $0

Closing cash balance $43,340 $48,370 $69,730

iv) Yes, the company should go ahead with the purchase of equipment costing $150,000 by

taking a loan of $150000 as the cash balance is positive in all the months from April to June.

In case the loan is not taken, then the company will not have sufficient cash balance to

finance the equipment and hence should not consider purchasing it.

Question 5: Capital Investment Decision

i) Annual net cash flows for Project X

Year 0 1 2 3 4 5

Cash inflow $50,000 $60,000 $70,000 $80,000 $90,000

Less: Variable cost $5,000 $6,000 $7,000 $8,000 $9,000

Less: Fixed cost $5,000 $5,000 $5,000 $5,000 $5,000

Less: Instalment cost $15,000

Operating income $25,000 $49,000 $58,000 $67,000 $76,000

Initial investment -$1,20,000

Annual net cash

flows -$1,20,000 $25,000 $49,000 $58,000 $67,000 $76,000

ii) Payback period, NPV, Discounted payback period for Project X

Year 0 1 2 3 4 5

Annual net cash

flows -$1,20,000 $25,000 $49,000 $58,000 $67,000 $76,000

Multiply: Cost of

capital $1 $0.909 $0.826 $0.751 $0.683 $0.621

Present value of

cash flows -$1,20,000 $22,727.27 $40,495.87 $43,576.26 $45,761.90 $47,190.02

NPV = Present value of cash inflows – cash outflow

= $199,751.32 - $120,000

= $79751.32

Payback period

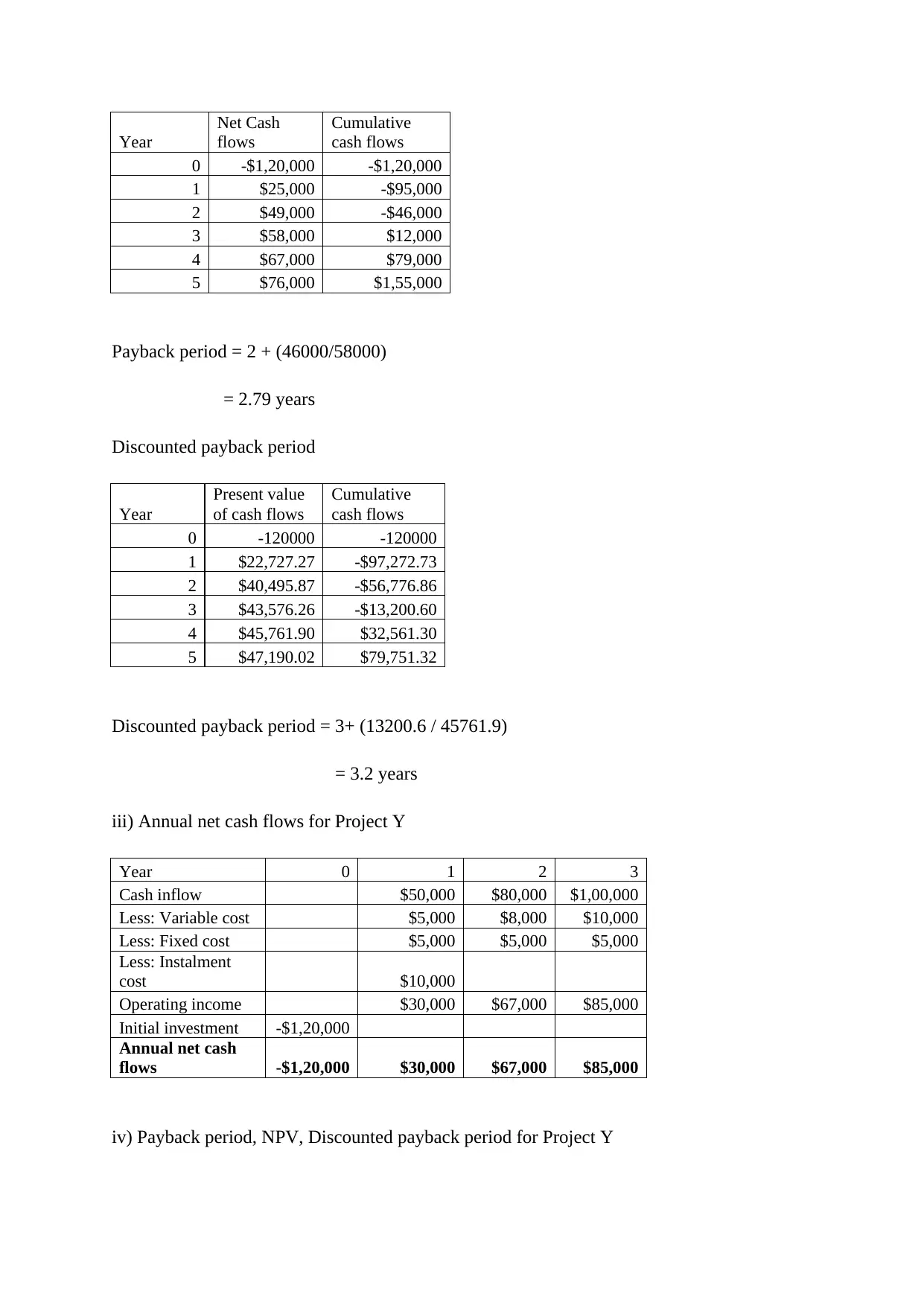

Year

Net Cash

flows

Cumulative

cash flows

0 -$1,20,000 -$1,20,000

1 $25,000 -$95,000

2 $49,000 -$46,000

3 $58,000 $12,000

4 $67,000 $79,000

5 $76,000 $1,55,000

Payback period = 2 + (46000/58000)

= 2.79 years

Discounted payback period

Year

Present value

of cash flows

Cumulative

cash flows

0 -120000 -120000

1 $22,727.27 -$97,272.73

2 $40,495.87 -$56,776.86

3 $43,576.26 -$13,200.60

4 $45,761.90 $32,561.30

5 $47,190.02 $79,751.32

Discounted payback period = 3+ (13200.6 / 45761.9)

= 3.2 years

iii) Annual net cash flows for Project Y

Year 0 1 2 3

Cash inflow $50,000 $80,000 $1,00,000

Less: Variable cost $5,000 $8,000 $10,000

Less: Fixed cost $5,000 $5,000 $5,000

Less: Instalment

cost $10,000

Operating income $30,000 $67,000 $85,000

Initial investment -$1,20,000

Annual net cash

flows -$1,20,000 $30,000 $67,000 $85,000

iv) Payback period, NPV, Discounted payback period for Project Y

Net Cash

flows

Cumulative

cash flows

0 -$1,20,000 -$1,20,000

1 $25,000 -$95,000

2 $49,000 -$46,000

3 $58,000 $12,000

4 $67,000 $79,000

5 $76,000 $1,55,000

Payback period = 2 + (46000/58000)

= 2.79 years

Discounted payback period

Year

Present value

of cash flows

Cumulative

cash flows

0 -120000 -120000

1 $22,727.27 -$97,272.73

2 $40,495.87 -$56,776.86

3 $43,576.26 -$13,200.60

4 $45,761.90 $32,561.30

5 $47,190.02 $79,751.32

Discounted payback period = 3+ (13200.6 / 45761.9)

= 3.2 years

iii) Annual net cash flows for Project Y

Year 0 1 2 3

Cash inflow $50,000 $80,000 $1,00,000

Less: Variable cost $5,000 $8,000 $10,000

Less: Fixed cost $5,000 $5,000 $5,000

Less: Instalment

cost $10,000

Operating income $30,000 $67,000 $85,000

Initial investment -$1,20,000

Annual net cash

flows -$1,20,000 $30,000 $67,000 $85,000

iv) Payback period, NPV, Discounted payback period for Project Y

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

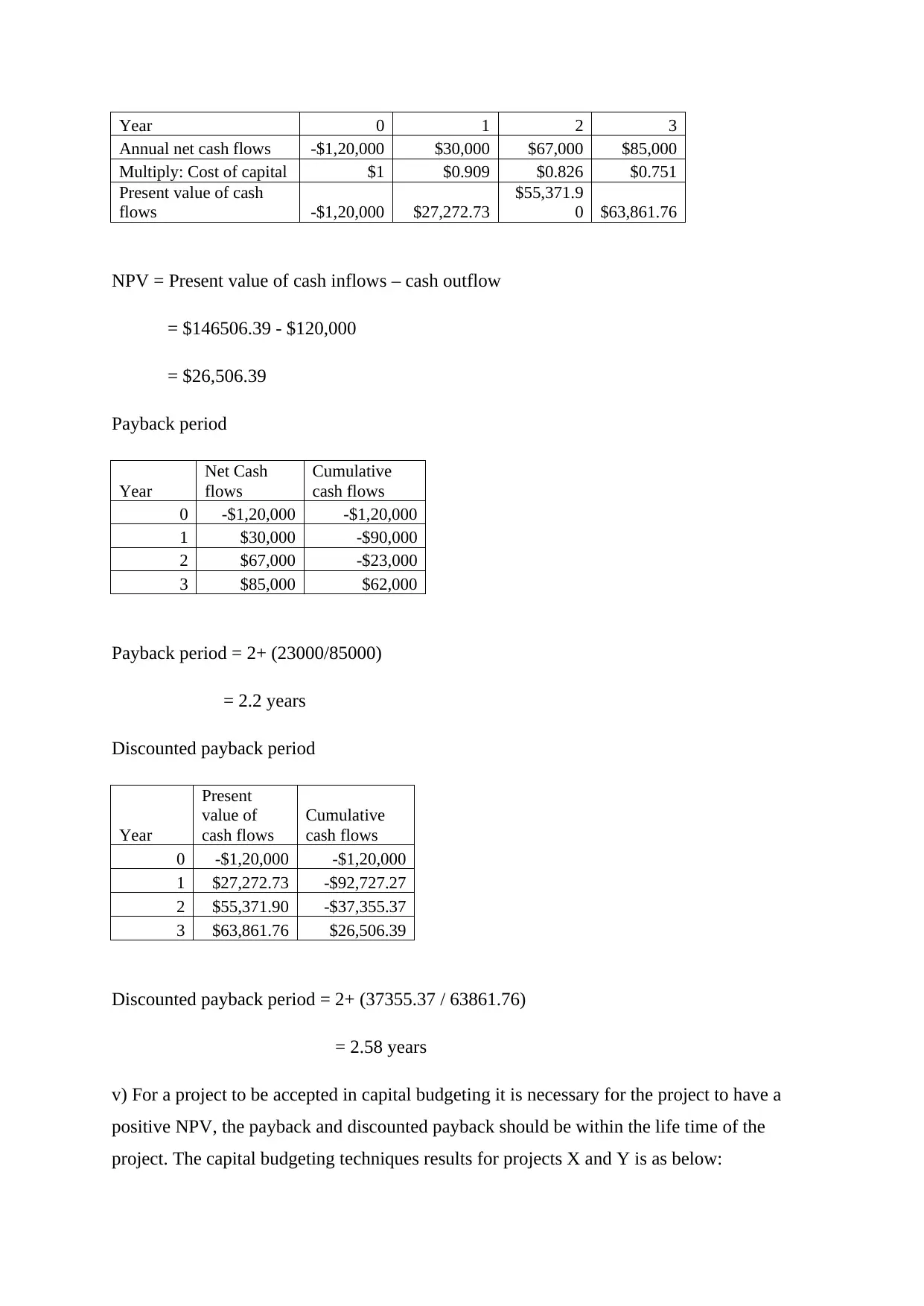

Year 0 1 2 3

Annual net cash flows -$1,20,000 $30,000 $67,000 $85,000

Multiply: Cost of capital $1 $0.909 $0.826 $0.751

Present value of cash

flows -$1,20,000 $27,272.73

$55,371.9

0 $63,861.76

NPV = Present value of cash inflows – cash outflow

= $146506.39 - $120,000

= $26,506.39

Payback period

Year

Net Cash

flows

Cumulative

cash flows

0 -$1,20,000 -$1,20,000

1 $30,000 -$90,000

2 $67,000 -$23,000

3 $85,000 $62,000

Payback period = 2+ (23000/85000)

= 2.2 years

Discounted payback period

Year

Present

value of

cash flows

Cumulative

cash flows

0 -$1,20,000 -$1,20,000

1 $27,272.73 -$92,727.27

2 $55,371.90 -$37,355.37

3 $63,861.76 $26,506.39

Discounted payback period = 2+ (37355.37 / 63861.76)

= 2.58 years

v) For a project to be accepted in capital budgeting it is necessary for the project to have a

positive NPV, the payback and discounted payback should be within the life time of the

project. The capital budgeting techniques results for projects X and Y is as below:

Annual net cash flows -$1,20,000 $30,000 $67,000 $85,000

Multiply: Cost of capital $1 $0.909 $0.826 $0.751

Present value of cash

flows -$1,20,000 $27,272.73

$55,371.9

0 $63,861.76

NPV = Present value of cash inflows – cash outflow

= $146506.39 - $120,000

= $26,506.39

Payback period

Year

Net Cash

flows

Cumulative

cash flows

0 -$1,20,000 -$1,20,000

1 $30,000 -$90,000

2 $67,000 -$23,000

3 $85,000 $62,000

Payback period = 2+ (23000/85000)

= 2.2 years

Discounted payback period

Year

Present

value of

cash flows

Cumulative

cash flows

0 -$1,20,000 -$1,20,000

1 $27,272.73 -$92,727.27

2 $55,371.90 -$37,355.37

3 $63,861.76 $26,506.39

Discounted payback period = 2+ (37355.37 / 63861.76)

= 2.58 years

v) For a project to be accepted in capital budgeting it is necessary for the project to have a

positive NPV, the payback and discounted payback should be within the life time of the

project. The capital budgeting techniques results for projects X and Y is as below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

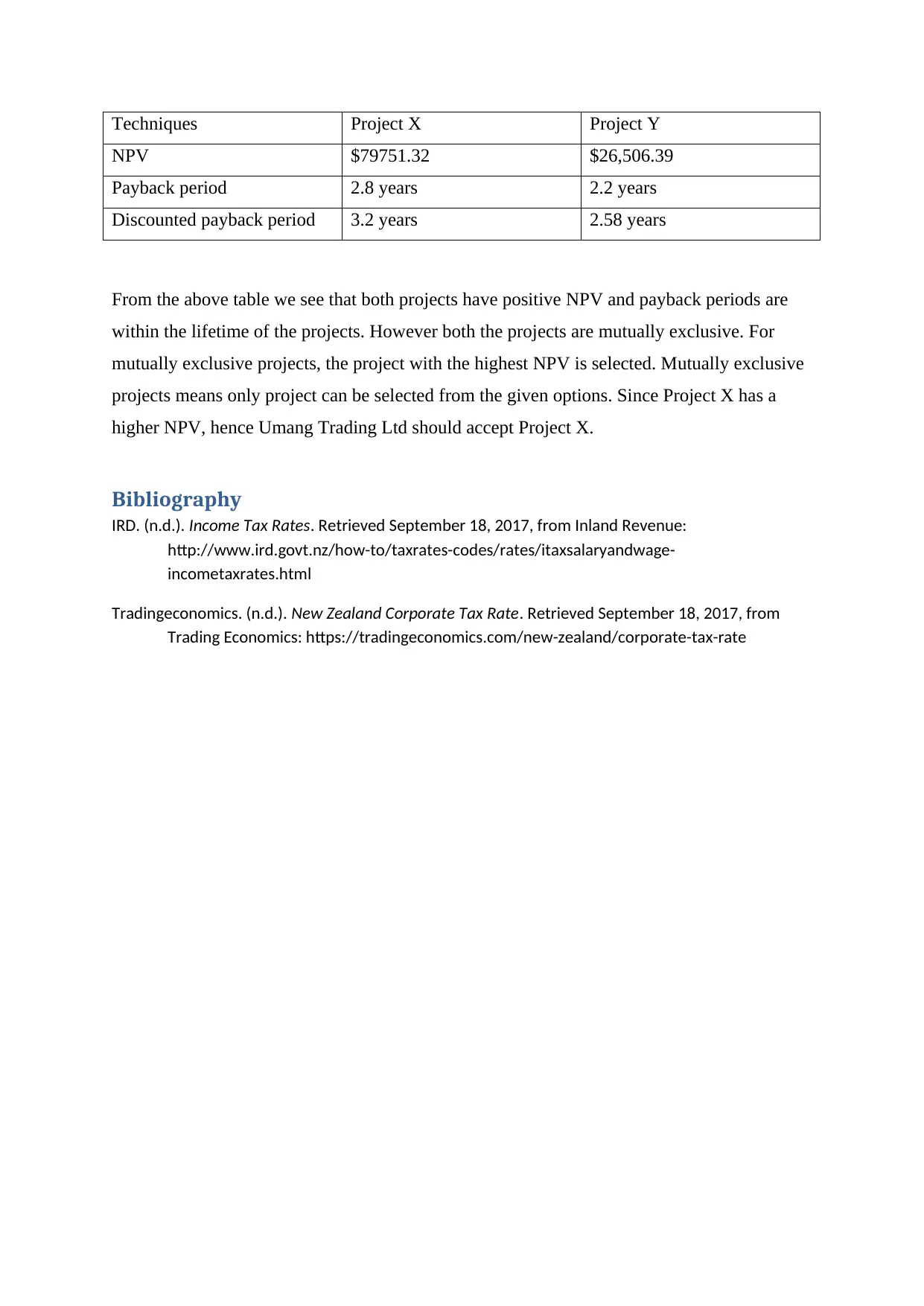

Techniques Project X Project Y

NPV $79751.32 $26,506.39

Payback period 2.8 years 2.2 years

Discounted payback period 3.2 years 2.58 years

From the above table we see that both projects have positive NPV and payback periods are

within the lifetime of the projects. However both the projects are mutually exclusive. For

mutually exclusive projects, the project with the highest NPV is selected. Mutually exclusive

projects means only project can be selected from the given options. Since Project X has a

higher NPV, hence Umang Trading Ltd should accept Project X.

Bibliography

IRD. (n.d.). Income Tax Rates. Retrieved September 18, 2017, from Inland Revenue:

http://www.ird.govt.nz/how-to/taxrates-codes/rates/itaxsalaryandwage-

incometaxrates.html

Tradingeconomics. (n.d.). New Zealand Corporate Tax Rate. Retrieved September 18, 2017, from

Trading Economics: https://tradingeconomics.com/new-zealand/corporate-tax-rate

NPV $79751.32 $26,506.39

Payback period 2.8 years 2.2 years

Discounted payback period 3.2 years 2.58 years

From the above table we see that both projects have positive NPV and payback periods are

within the lifetime of the projects. However both the projects are mutually exclusive. For

mutually exclusive projects, the project with the highest NPV is selected. Mutually exclusive

projects means only project can be selected from the given options. Since Project X has a

higher NPV, hence Umang Trading Ltd should accept Project X.

Bibliography

IRD. (n.d.). Income Tax Rates. Retrieved September 18, 2017, from Inland Revenue:

http://www.ird.govt.nz/how-to/taxrates-codes/rates/itaxsalaryandwage-

incometaxrates.html

Tradingeconomics. (n.d.). New Zealand Corporate Tax Rate. Retrieved September 18, 2017, from

Trading Economics: https://tradingeconomics.com/new-zealand/corporate-tax-rate

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.