Economics 23 Assignment: Market Analysis and Elasticity

VerifiedAdded on 2020/05/28

|24

|3778

|207

Homework Assignment

AI Summary

This economics assignment provides a comprehensive analysis of market dynamics, elasticity, and government interventions. Section A delves into market equilibrium, comparative advantage, and the impact of price controls. It examines the concepts of supply and demand, illustrating how various factors influence market prices and quantities. The assignment then explores market failures, discussing government tools such as subsidies, taxation, and price controls to address inefficiencies. Section B shifts the focus to production costs, the relationship between total, marginal, and average product, and optimization in production. The assignment also includes a discussion on how changes in input costs affect supply, and how external events influence demand. The assignment uses graphs and examples to illustrate key economic concepts and their practical applications.

Running Head: ASSIGNMENT FOR ECONOMICS

Assignment for economics

Name of the Student

Name of the University

Author Note

Assignment for economics

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ASSIGNMENT FOR ECONOMICS

Table of Contents

Section A:..................................................................................................................................2

Answer to question 1:................................................................................................................2

Answer to question 2:................................................................................................................3

Answer to question 3:................................................................................................................4

Answer to question 4:................................................................................................................6

Section B:...................................................................................................................................8

Answer to question 1:................................................................................................................8

Answer to question 2:..............................................................................................................12

Answer to question 3:..............................................................................................................18

ASSIGNMENT FOR ECONOMICS

Table of Contents

Section A:..................................................................................................................................2

Answer to question 1:................................................................................................................2

Answer to question 2:................................................................................................................3

Answer to question 3:................................................................................................................4

Answer to question 4:................................................................................................................6

Section B:...................................................................................................................................8

Answer to question 1:................................................................................................................8

Answer to question 2:..............................................................................................................12

Answer to question 3:..............................................................................................................18

2

ASSIGNMENT FOR ECONOMICS

Section A:

Answer to question 1:

a) Without international trade, there will be equilibrium in the domestic market. That is at

this level, quantity demanded of rise will be equal to quantity supplied. Quantity demanded of

rose is equal to quantity supplied at US $ 175 per container.

b) At price US $ 175, UAE has comparative advantage in producing roses compared to rest

of the world, as wholesaler can get roses at lowest price within their domestic country.

c) The lowest possible price cannot be less than $ 125 where roses can be purchased in

auction. Hence, if wholesalers buy rose at $ 125, then they will get only 2 million containers of

roses and they need to import 10 million containers.

Answer to question 2:

a) The supply curve will be a vertical line as blue period work of Picasso is not available

and hence supply cannot be increased. It will remain fixed at 1000 canvases.

ASSIGNMENT FOR ECONOMICS

Section A:

Answer to question 1:

a) Without international trade, there will be equilibrium in the domestic market. That is at

this level, quantity demanded of rise will be equal to quantity supplied. Quantity demanded of

rose is equal to quantity supplied at US $ 175 per container.

b) At price US $ 175, UAE has comparative advantage in producing roses compared to rest

of the world, as wholesaler can get roses at lowest price within their domestic country.

c) The lowest possible price cannot be less than $ 125 where roses can be purchased in

auction. Hence, if wholesalers buy rose at $ 125, then they will get only 2 million containers of

roses and they need to import 10 million containers.

Answer to question 2:

a) The supply curve will be a vertical line as blue period work of Picasso is not available

and hence supply cannot be increased. It will remain fixed at 1000 canvases.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ASSIGNMENT FOR ECONOMICS

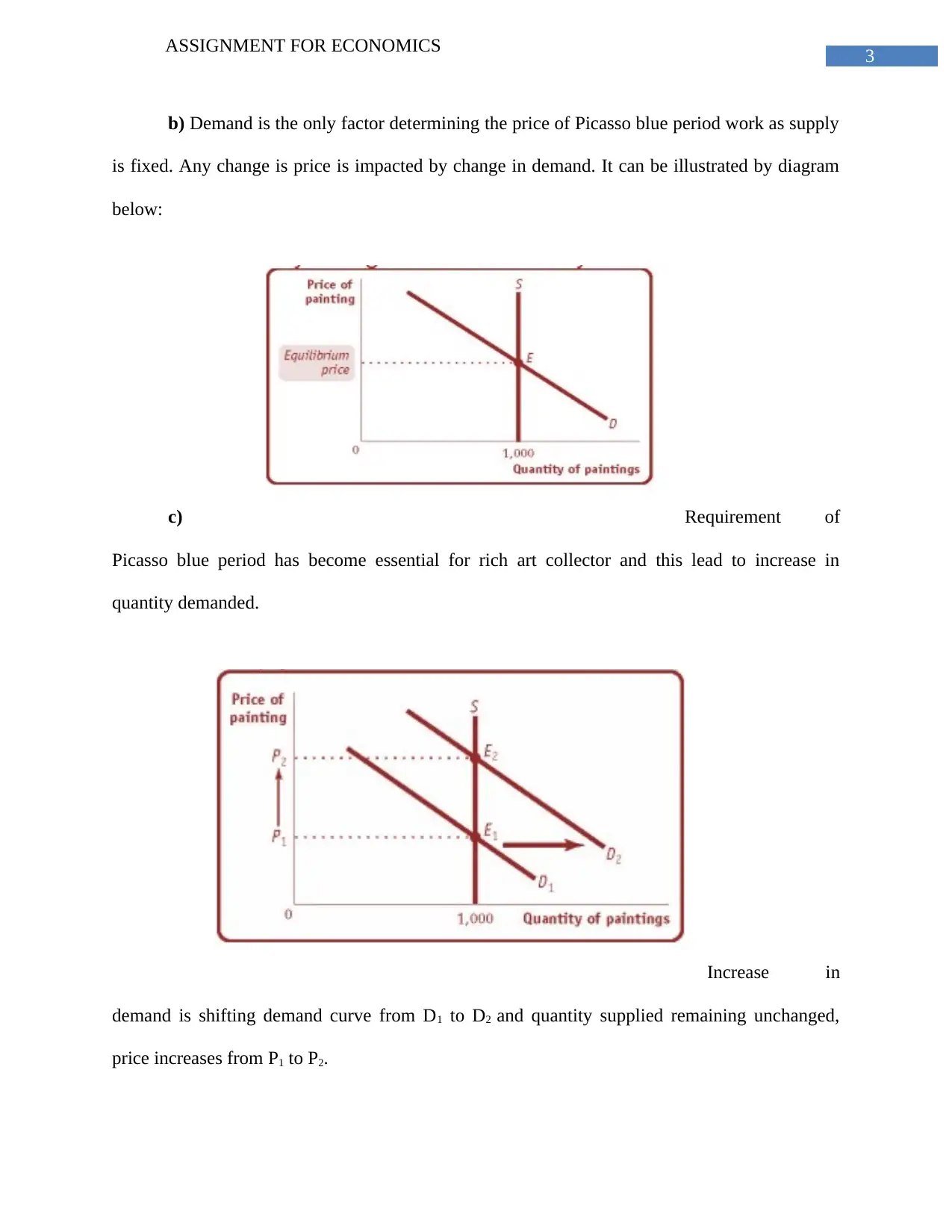

b) Demand is the only factor determining the price of Picasso blue period work as supply

is fixed. Any change is price is impacted by change in demand. It can be illustrated by diagram

below:

c) Requirement of

Picasso blue period has become essential for rich art collector and this lead to increase in

quantity demanded.

Increase in

demand is shifting demand curve from D1 to D2 and quantity supplied remaining unchanged,

price increases from P1 to P2.

ASSIGNMENT FOR ECONOMICS

b) Demand is the only factor determining the price of Picasso blue period work as supply

is fixed. Any change is price is impacted by change in demand. It can be illustrated by diagram

below:

c) Requirement of

Picasso blue period has become essential for rich art collector and this lead to increase in

quantity demanded.

Increase in

demand is shifting demand curve from D1 to D2 and quantity supplied remaining unchanged,

price increases from P1 to P2.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ASSIGNMENT FOR ECONOMICS

Answer to question 3:

Market failure occurs due to inefficient resources distribution that is dealt by government

through adoption of various tools and responding to market failures to varying degrees. Some of

the tools that are taken by government for dealing with market failures are as follows:

Direct provision of merit and public goods- Goods supply that have positive externalities

can be controlled by government by way of supplying high amounts of parks, education

and libraries to public. Community benefits of public goods can be maximized by

intervention of government in regulation, production, management and maintenance. It

would also help in congestion or over exploitation of resources. Allocative inefficiency

in allocation of resources of merit goods such as healthcare and education can be done by

government intervention by way of subsidization (Patterson 2015). This will help in

dealing with market inefficiency of such goods.

Subsidies- Government takes the measures of reducing goods price that is based on

benefits received by public. This particular tool is considered appropriate for encouraging

behavior generating positive externalities. Subsidy tool enables consumers paying the

price that is socially efficient comprising of external benefits and thereby leading to

greater social efficiency. Government efforts to subsidize public transport will motivate

people to use public transport and reducing negative externalities of private vehicles

(Feenstra 2015).

ASSIGNMENT FOR ECONOMICS

Answer to question 3:

Market failure occurs due to inefficient resources distribution that is dealt by government

through adoption of various tools and responding to market failures to varying degrees. Some of

the tools that are taken by government for dealing with market failures are as follows:

Direct provision of merit and public goods- Goods supply that have positive externalities

can be controlled by government by way of supplying high amounts of parks, education

and libraries to public. Community benefits of public goods can be maximized by

intervention of government in regulation, production, management and maintenance. It

would also help in congestion or over exploitation of resources. Allocative inefficiency

in allocation of resources of merit goods such as healthcare and education can be done by

government intervention by way of subsidization (Patterson 2015). This will help in

dealing with market inefficiency of such goods.

Subsidies- Government takes the measures of reducing goods price that is based on

benefits received by public. This particular tool is considered appropriate for encouraging

behavior generating positive externalities. Subsidy tool enables consumers paying the

price that is socially efficient comprising of external benefits and thereby leading to

greater social efficiency. Government efforts to subsidize public transport will motivate

people to use public transport and reducing negative externalities of private vehicles

(Feenstra 2015).

5

ASSIGNMENT FOR ECONOMICS

Taxation- Government to deal with inefficiency in market intends to place taxes on

certain goods that would assist in discouraging its usage and leading to external cost

internalization (Hursh and Roma 2016). This can be explained with the help of an

example, taxing tobacco products and this would have subsequent impact on tobacco

consumption cost that is leading to increase in consumption cost.

Property rights extension and tradable permits- Government take measures for creating

privatization of some public goods such as rivers, lakes and beaches and this is intended

to create market for pollution of these non private goods. Fines are imposed on

individuals for polluting these areas. Tradable permits is another considerable tool

intended to create market efficiency that gives firms permission to produce something

called pollution in association with goods production (Gwartney et al. 2014). In order to

increase or decrease the production, any one firm can trade permits with one another.

This helps in reducing pollution as it is the basis behind cap and trade.

Controlling domestic price movements (Maximum and Minimum price)- One of the

intervention measures of government to deal with market failure is imposition of price

control. Government might impose price ceiling if the market clearing price for services

and goods is considerably higher. Price ceiling imposition is the setting of maximum

legal limit price of goods and services. Such ceiling is imposed on merit and essential

goods and monopolist charging unusual higher price. Railway industry can increase the

tickets price to an unreasonable extent because of monopoly power. Imposition of

maximum price by government will assist in keeping tickets at reasonable level. In case

of minimum price, government takes the effort of setting minimum legal limit for

particular goods and services. This particular measure is undertaken by government to

ASSIGNMENT FOR ECONOMICS

Taxation- Government to deal with inefficiency in market intends to place taxes on

certain goods that would assist in discouraging its usage and leading to external cost

internalization (Hursh and Roma 2016). This can be explained with the help of an

example, taxing tobacco products and this would have subsequent impact on tobacco

consumption cost that is leading to increase in consumption cost.

Property rights extension and tradable permits- Government take measures for creating

privatization of some public goods such as rivers, lakes and beaches and this is intended

to create market for pollution of these non private goods. Fines are imposed on

individuals for polluting these areas. Tradable permits is another considerable tool

intended to create market efficiency that gives firms permission to produce something

called pollution in association with goods production (Gwartney et al. 2014). In order to

increase or decrease the production, any one firm can trade permits with one another.

This helps in reducing pollution as it is the basis behind cap and trade.

Controlling domestic price movements (Maximum and Minimum price)- One of the

intervention measures of government to deal with market failure is imposition of price

control. Government might impose price ceiling if the market clearing price for services

and goods is considerably higher. Price ceiling imposition is the setting of maximum

legal limit price of goods and services. Such ceiling is imposed on merit and essential

goods and monopolist charging unusual higher price. Railway industry can increase the

tickets price to an unreasonable extent because of monopoly power. Imposition of

maximum price by government will assist in keeping tickets at reasonable level. In case

of minimum price, government takes the effort of setting minimum legal limit for

particular goods and services. This particular measure is undertaken by government to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ASSIGNMENT FOR ECONOMICS

provide assistance to some producers seeking assistance whose products are being sold at

significantly lower price in an unfair market. Goods surplus created in the market can be

eliminated by government efforts to buy excess supply at minimum price (Godelier

2014). This will help market in attaining equilibrium level by shifting of demand curve.

Example of setting minimum price is protecting workers by setting of minimum wages.

Setting of minimum wage would help in ensuring that enough is earned by workers that

would lead to their reasonable existence.

Answer to question 4:

Demand elasticity measures the responsiveness of change in quantity demanded of

products to alterations in any particular factor impacting demand of goods while keeping other

factors constant. There are three types of elasticity for demand that is price elasticity of demand,

income elasticity of demand and cross price elasticity of demand. When there is sensitivity of

changes in quantity demanded due to change in price, then demand change is said to be price

elastic. Change in quantity demanded resulting from change in income is income elasticity of

demand. Cross price elasticity is the change in demand of one product resulting from change in

price of another product.

Price elasticity of demand- Price elasticity of demand is the degree of responsiveness of

change in quantity demanded resulting from change in price of goods. Price elasticity of demand

is obtained by dividing ratio of percentage change in any goods quantity demanded by

percentage change in price of that particular good. The formulae for calculating price elasticity

of goods is

ASSIGNMENT FOR ECONOMICS

provide assistance to some producers seeking assistance whose products are being sold at

significantly lower price in an unfair market. Goods surplus created in the market can be

eliminated by government efforts to buy excess supply at minimum price (Godelier

2014). This will help market in attaining equilibrium level by shifting of demand curve.

Example of setting minimum price is protecting workers by setting of minimum wages.

Setting of minimum wage would help in ensuring that enough is earned by workers that

would lead to their reasonable existence.

Answer to question 4:

Demand elasticity measures the responsiveness of change in quantity demanded of

products to alterations in any particular factor impacting demand of goods while keeping other

factors constant. There are three types of elasticity for demand that is price elasticity of demand,

income elasticity of demand and cross price elasticity of demand. When there is sensitivity of

changes in quantity demanded due to change in price, then demand change is said to be price

elastic. Change in quantity demanded resulting from change in income is income elasticity of

demand. Cross price elasticity is the change in demand of one product resulting from change in

price of another product.

Price elasticity of demand- Price elasticity of demand is the degree of responsiveness of

change in quantity demanded resulting from change in price of goods. Price elasticity of demand

is obtained by dividing ratio of percentage change in any goods quantity demanded by

percentage change in price of that particular good. The formulae for calculating price elasticity

of goods is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ASSIGNMENT FOR ECONOMICS

Price elasticity of demand (Ed)= % age change in quantity of product demanded /% age

change in price of product

There are three types of price elasticity of goods that is elastic, unitary elastic and

inelastic. In elastic demand, value of elasticity is greater than one (Bowen et al. 2015). In case of

unit elastic demand, value of demand elasticity is equal to one. Inelastic demand has elasticity

value less than 1.

Income elasticity of demand- The change in quantity demanded of goods due to change

in income of consumers is income elasticity of demand. It is computed by dividing percentage

change in quantity demanded of goods by percentage change in income. Income elasticity is the

responsiveness of change in quantity demanded for products with respect to change income

while other factors remaining constant (Layson 2015). The formulae for computing income

elasticity of demand is

Income elasticity of demand (Ey)= % age change in quantity of product demanded /% age

change in consumer income

Depending upon categorization of goods whether it is normal or inferior, increase in

income influences change in demand for goods. Income elasticity value for normal goods is less

than one but greater than zero. For inferior goods, value of income elasticity is less than one.

Cross price elasticity of demand- Cross price elasticity of demand is the responsiveness

of change in quantity demanded for a product with respect to change in price of other products

that is related products whether substitutes goods or complementary goods. It is obtained by

dividing percentage change in quantity demanded of any particular good with respect to change

ASSIGNMENT FOR ECONOMICS

Price elasticity of demand (Ed)= % age change in quantity of product demanded /% age

change in price of product

There are three types of price elasticity of goods that is elastic, unitary elastic and

inelastic. In elastic demand, value of elasticity is greater than one (Bowen et al. 2015). In case of

unit elastic demand, value of demand elasticity is equal to one. Inelastic demand has elasticity

value less than 1.

Income elasticity of demand- The change in quantity demanded of goods due to change

in income of consumers is income elasticity of demand. It is computed by dividing percentage

change in quantity demanded of goods by percentage change in income. Income elasticity is the

responsiveness of change in quantity demanded for products with respect to change income

while other factors remaining constant (Layson 2015). The formulae for computing income

elasticity of demand is

Income elasticity of demand (Ey)= % age change in quantity of product demanded /% age

change in consumer income

Depending upon categorization of goods whether it is normal or inferior, increase in

income influences change in demand for goods. Income elasticity value for normal goods is less

than one but greater than zero. For inferior goods, value of income elasticity is less than one.

Cross price elasticity of demand- Cross price elasticity of demand is the responsiveness

of change in quantity demanded for a product with respect to change in price of other products

that is related products whether substitutes goods or complementary goods. It is obtained by

dividing percentage change in quantity demanded of any particular good with respect to change

8

ASSIGNMENT FOR ECONOMICS

in price of other goods that is related goods. The formula for measuring cross price elasticity of

demand is

Income elasticity of demand (Emn)= % age change in quantity demanded of product m /%

age change in quantity demanded of product n.

Value of cross price elasticity of demand is positive when two goods are substitutes. This

is so because demand for good will increase due to increase in price of its substitutes. For

example, coffee and tea, demand for tea will increase if price of coffee increases at the same

time. When two goods are complementary goods, then value of cross price elasticity of demand

is negative (Edmond et al. 2014). It can be explained with the help of an example, car and petrol

are two complementary goods and demand for cars will fall if there is an increase in price of

petrol.

Section B:

Answer to question 1:

a)

Optimization point of both the countries are different is machine intensive and other is labor

intensive. The relationship between total product, marginal product and average product can be

explained with the help of graph drawn below:

ASSIGNMENT FOR ECONOMICS

in price of other goods that is related goods. The formula for measuring cross price elasticity of

demand is

Income elasticity of demand (Emn)= % age change in quantity demanded of product m /%

age change in quantity demanded of product n.

Value of cross price elasticity of demand is positive when two goods are substitutes. This

is so because demand for good will increase due to increase in price of its substitutes. For

example, coffee and tea, demand for tea will increase if price of coffee increases at the same

time. When two goods are complementary goods, then value of cross price elasticity of demand

is negative (Edmond et al. 2014). It can be explained with the help of an example, car and petrol

are two complementary goods and demand for cars will fall if there is an increase in price of

petrol.

Section B:

Answer to question 1:

a)

Optimization point of both the countries are different is machine intensive and other is labor

intensive. The relationship between total product, marginal product and average product can be

explained with the help of graph drawn below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

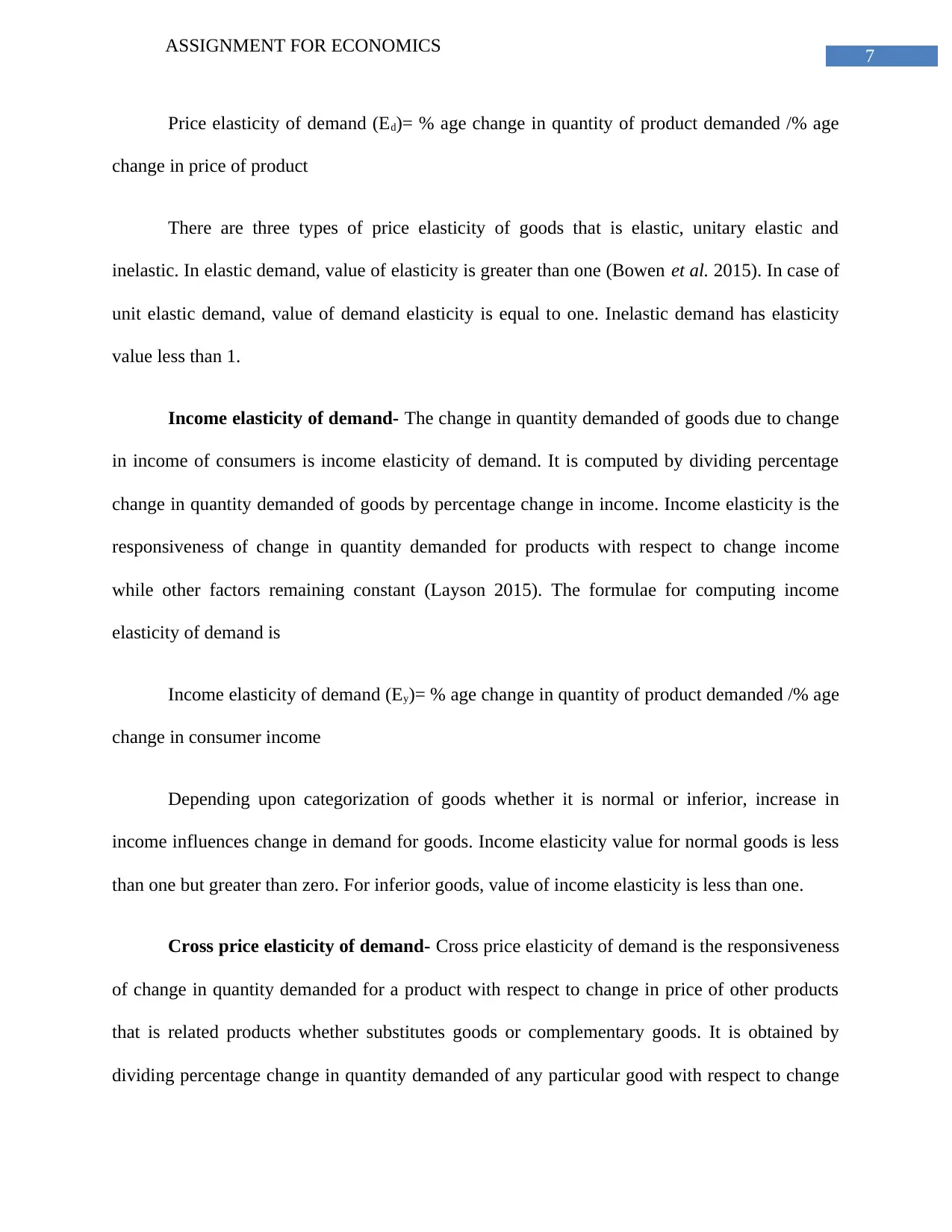

ASSIGNMENT FOR ECONOMICS

Labor is plotted on x axis and output is plotted on y axis. It can be depicted from graph

that total product (TP) increases at an increasing rate initially. Increase in TP is associated with

increase in Average product (AP) initially. When TP is increasing at increasing rate, AP is rising

TP is at its highest at point M where AP is also maximum. Later on, TP increases at a decreasing

rate where AP is rising continuously. Nonetheless, AP never reaches zero level.

Relationship between TP and Marginal product (MP) can be explained as an increase in

TP at increasing rates also increases MP as indicated at point C. When TP increases at

decreasing rate, MP starts declining, however, it remains positive. Furthermore, when TP is at its

highest level, MP reaches zero. MP becomes negative when TP starts falling.

ASSIGNMENT FOR ECONOMICS

Labor is plotted on x axis and output is plotted on y axis. It can be depicted from graph

that total product (TP) increases at an increasing rate initially. Increase in TP is associated with

increase in Average product (AP) initially. When TP is increasing at increasing rate, AP is rising

TP is at its highest at point M where AP is also maximum. Later on, TP increases at a decreasing

rate where AP is rising continuously. Nonetheless, AP never reaches zero level.

Relationship between TP and Marginal product (MP) can be explained as an increase in

TP at increasing rates also increases MP as indicated at point C. When TP increases at

decreasing rate, MP starts declining, however, it remains positive. Furthermore, when TP is at its

highest level, MP reaches zero. MP becomes negative when TP starts falling.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ASSIGNMENT FOR ECONOMICS

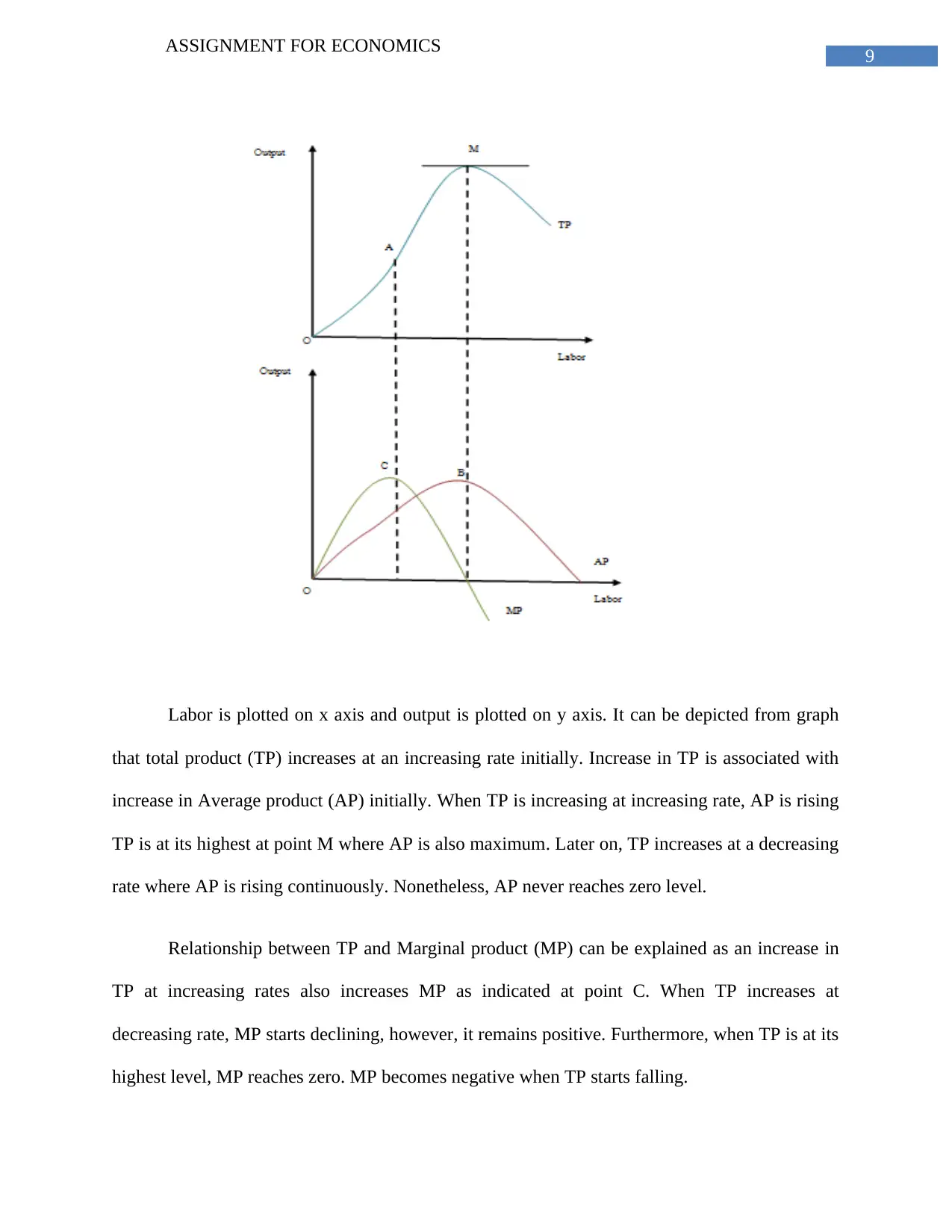

China being a developing country has relatively lower wages and therefore they can

employ more labor for cleaning streets. China can attain maximum productivity at point M

where TP is at its maximum, AP is beginning to fall and MP is zero. Hiring of additional labors

by China will help in increasing productivity at lower cost compared to US where hiring labor

would incur additional costs (Assous et al. 2014). Hence, UK can achieve optimization at point

A, where MP is maximum and AP is rising.

ASSIGNMENT FOR ECONOMICS

China being a developing country has relatively lower wages and therefore they can

employ more labor for cleaning streets. China can attain maximum productivity at point M

where TP is at its maximum, AP is beginning to fall and MP is zero. Hiring of additional labors

by China will help in increasing productivity at lower cost compared to US where hiring labor

would incur additional costs (Assous et al. 2014). Hence, UK can achieve optimization at point

A, where MP is maximum and AP is rising.

11

ASSIGNMENT FOR ECONOMICS

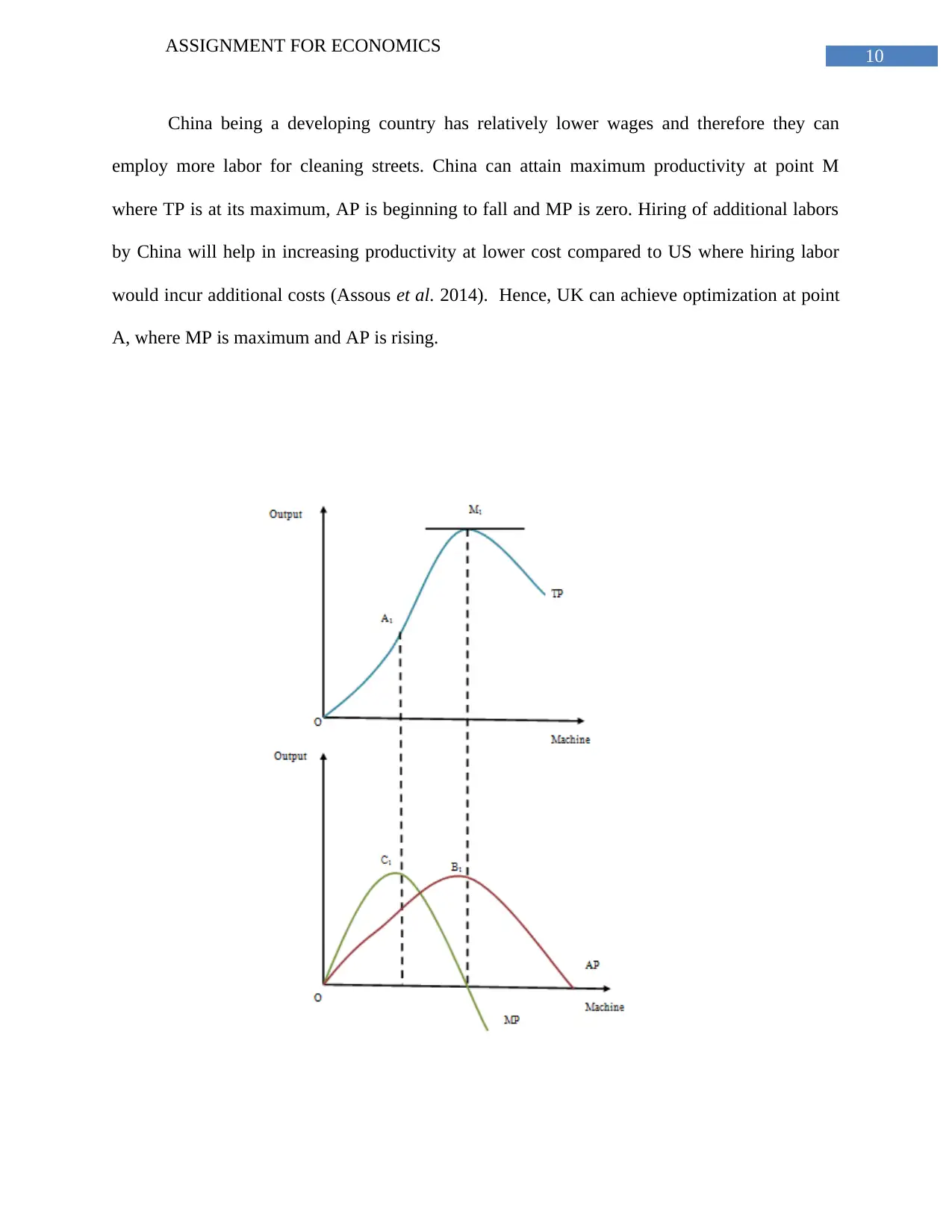

Machines employed is plotted on x axis and output is plotted on y axis. US would achieve

optimization point at M1 as it can increase its production by using additional machineries unlike

China that has to incur additional cost in order to employ machineries (Moseley 2014). At this

point, AP of US has started to fall with zero MP. On other hand, China can achieve optimization

at point A1 where MP is at its maximum and AP is rising continuously.

b):

ASSIGNMENT FOR ECONOMICS

Machines employed is plotted on x axis and output is plotted on y axis. US would achieve

optimization point at M1 as it can increase its production by using additional machineries unlike

China that has to incur additional cost in order to employ machineries (Moseley 2014). At this

point, AP of US has started to fall with zero MP. On other hand, China can achieve optimization

at point A1 where MP is at its maximum and AP is rising continuously.

b):

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.