University Event Management: Introduction, Budgeting, and Analysis

VerifiedAdded on 2020/05/03

|9

|1391

|85

Report

AI Summary

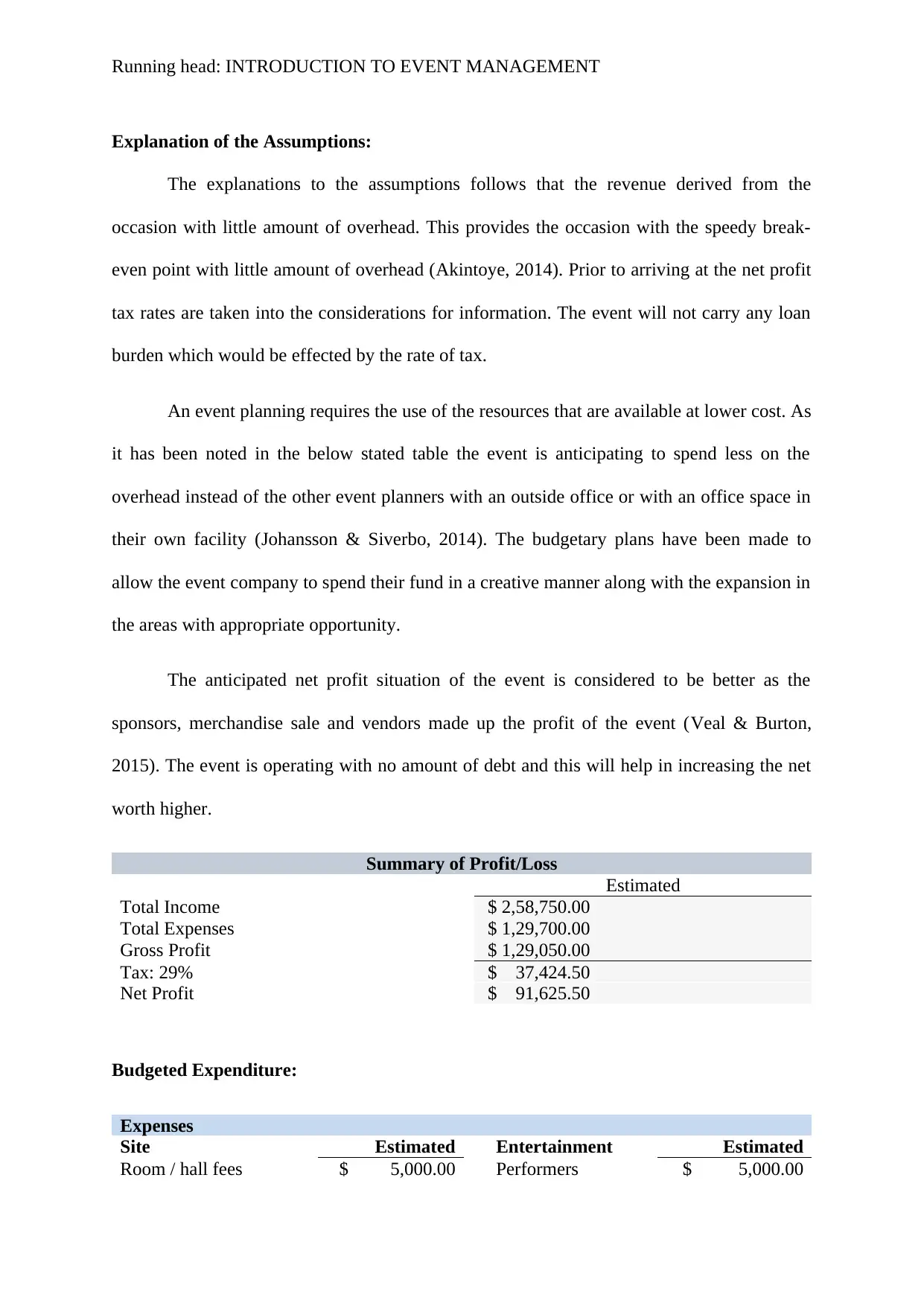

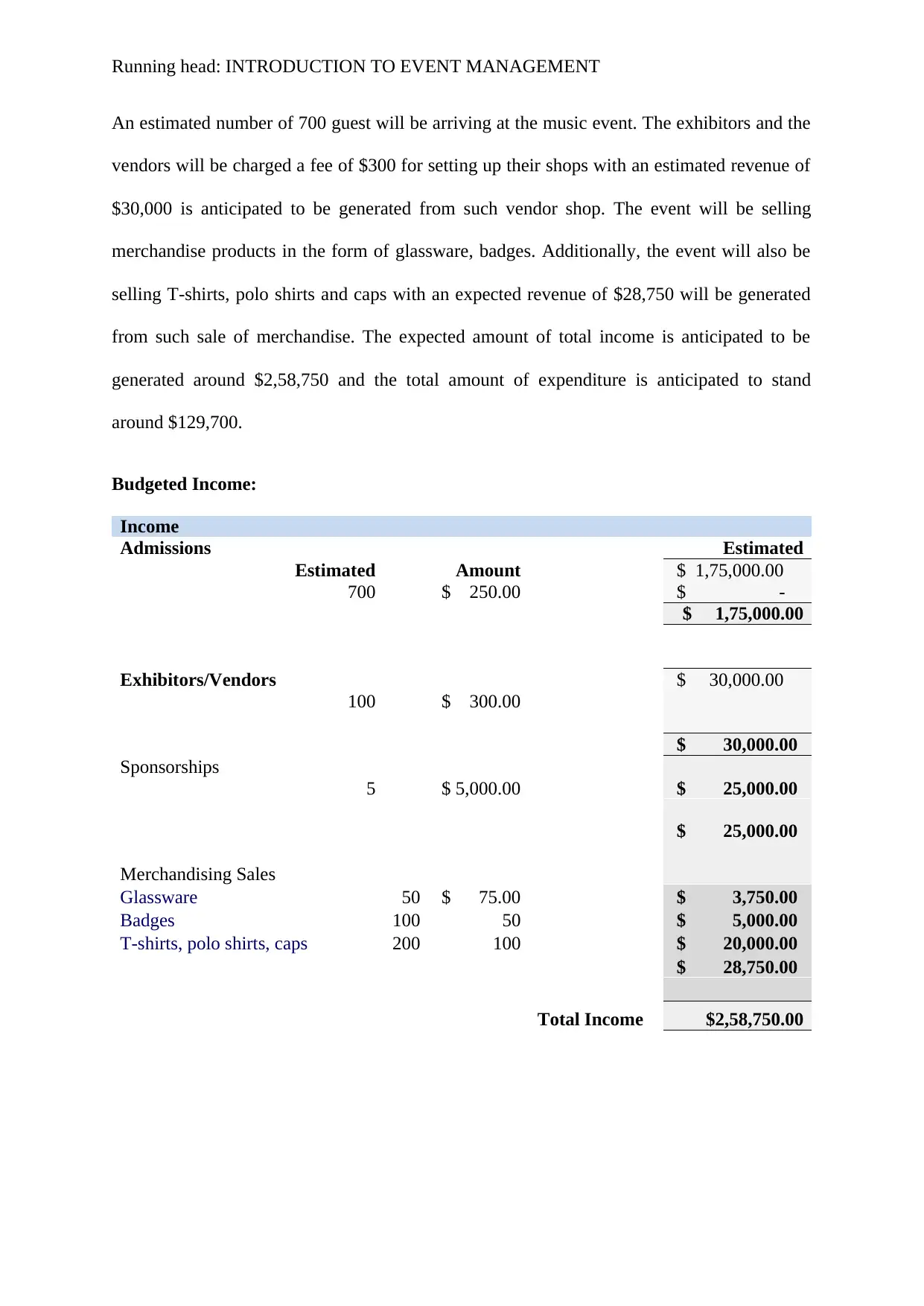

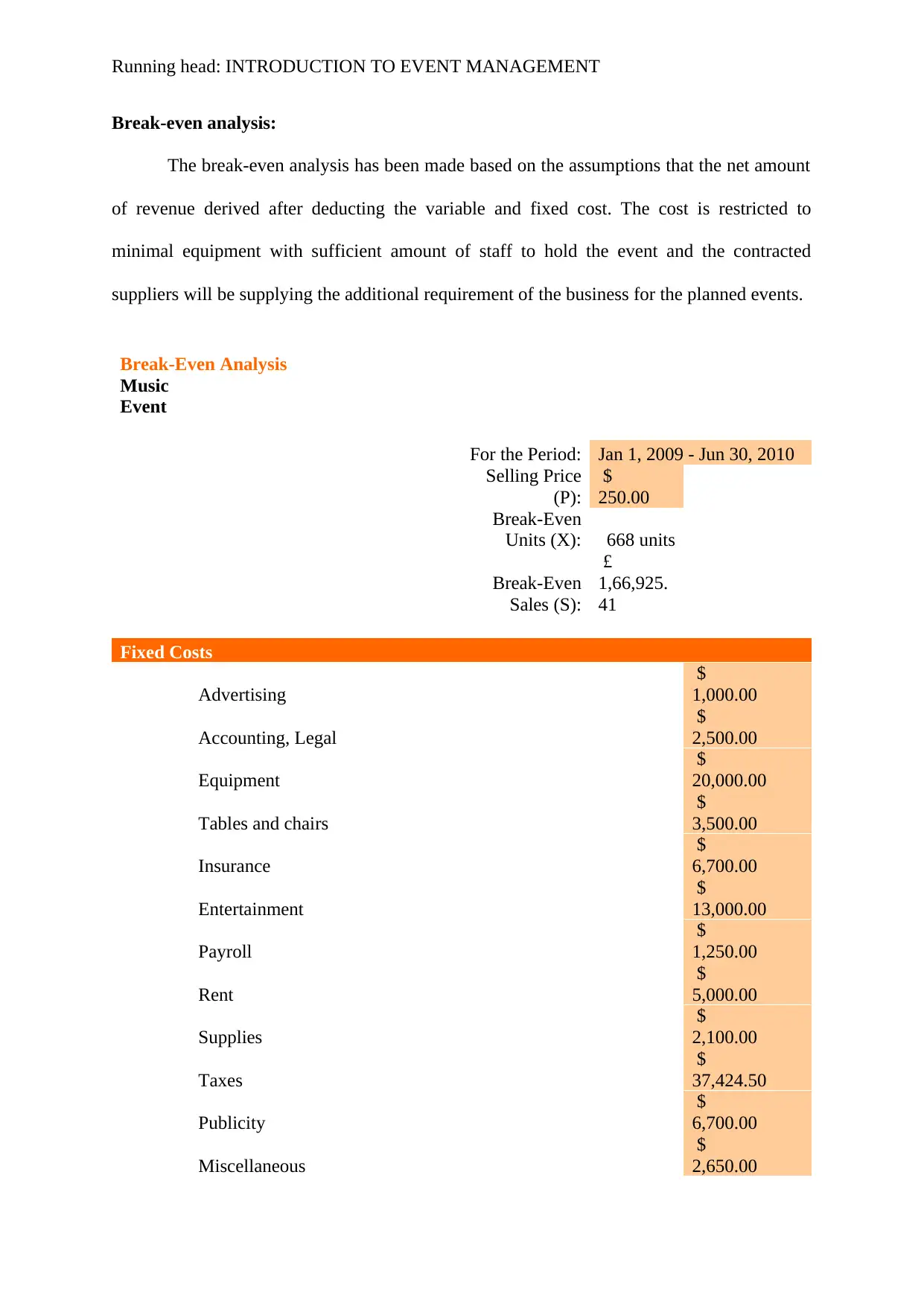

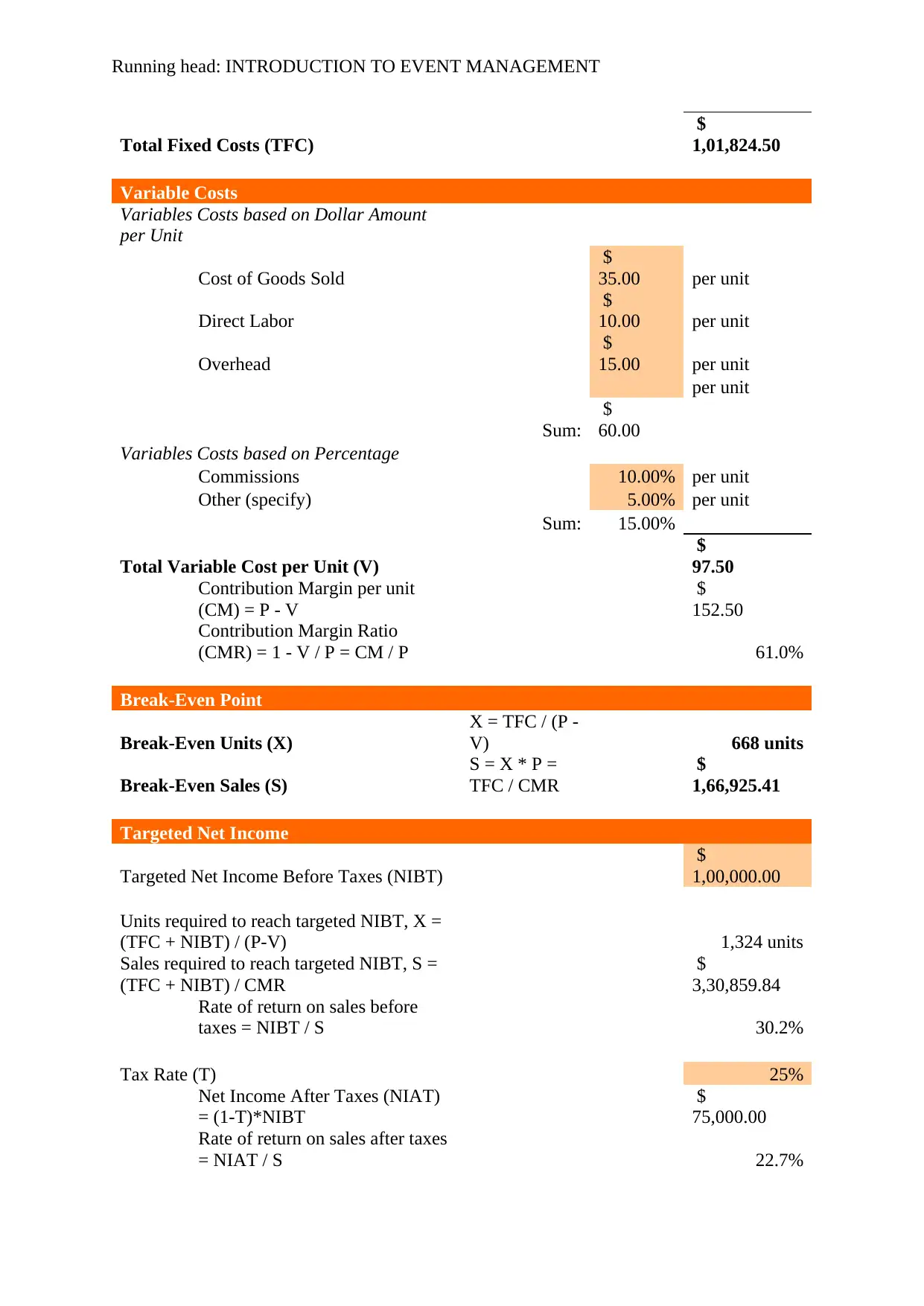

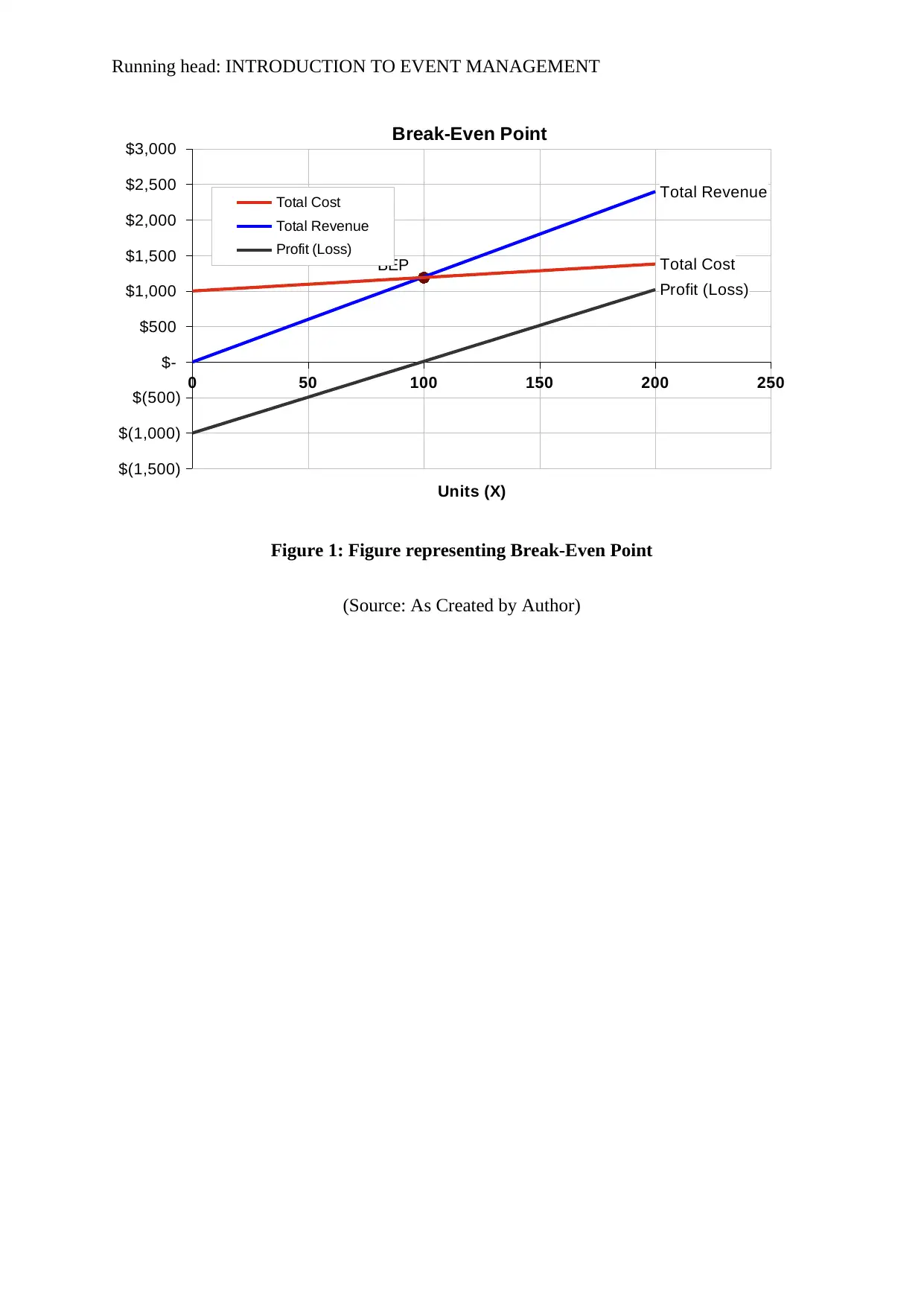

This report provides an introduction to event management, detailing the assumptions, budgeted income, and expenditure for a hypothetical music event. It outlines the financial aspects, including income from admissions, vendors, sponsorships, and merchandise sales, with a total expected income of $2,58,750. The report also includes a detailed breakdown of expenses, categorized by site, entertainment, refreshments, publicity, and other miscellaneous costs, totaling $129,700. A break-even analysis is presented, considering fixed and variable costs, to determine the number of units and sales required to break even and achieve targeted net income. The report emphasizes financial planning and control, offering insights into managing event budgets effectively. The report also mentions the importance of minimizing overhead costs and the use of resources to achieve profitability.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.