Financial Performance Analysis of UK-Based Companies: A Report

VerifiedAdded on 2020/02/05

|16

|4302

|76

Report

AI Summary

This report provides a comprehensive financial performance analysis of Games Workshop Plc and Character Group Plc, two UK-based companies. It utilizes ratio analysis, including profitability, liquidity, efficiency, and solvency ratios, to assess their financial health and performance trends. The analysis covers the years 2015 and 2016, offering insights into gross profit margins, net profit margins, return on assets, and return on equity. The report also discusses the role of auditors and changes in audit reports according to UK standards. Furthermore, it applies investment appraisal techniques, specifically the Internal Rate of Return (IRR), to evaluate project viability for Trump Manufacturing, offering recommendations on whether to invest. The analysis includes stock market performance comparisons, highlighting share price fluctuations and investor sentiment for both companies.

ONLINE TEST

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ..........................................................................................................................3

Question 1........................................................................................................................................3

Internal and external financial performance analysis..................................................................3

Q2. Role of auditor and changes incorporated in the audit report.............................................11

Question 3: Computation of IRR ..............................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................15

INTRODUCTION ..........................................................................................................................3

Question 1........................................................................................................................................3

Internal and external financial performance analysis..................................................................3

Q2. Role of auditor and changes incorporated in the audit report.............................................11

Question 3: Computation of IRR ..............................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................15

INTRODUCTION

Looking at the changing market situations, it becomes important for all the managers to

measure their operational outcome and financial position so as to make solid decisions for the

future success. Strategic Financial Analysis (SFA) can be explained as a process of interpreting

financial results to identify reasons for poor performance so that better and effective decisions

can be made for meeting targets. The present assignment aims at analysing financial performance

of two British based companies that are Game Workshop Plc and Character Group Plc by using

ratio analysis methodology. It will be done on the basis of profitability measurement,

efficiency/activity ratios, liquidity performance and solvency position as well. Moreover, the

report will also describe the role of auditor and change in audit report as per recent UK auditing

and reporting standards. At the end, the report will apply investment appraisal techniques to

assess project viability for Trump Manufacturing to advice that whether they should invest

money or not.

Question 1

Internal and external financial performance analysis

Profitability ratios

Games workshop Plc Character Group plc

2015 (£000) 2016 (£000) 2014 (£000) 2015 (£000)

Turnover 119132 118069 97889 99054

Gross profit 82144 80631 29137 36655

Net profit 12257 13496 5945 10239

Gross profit margin 68.95% 68.29% 29.77% 37.01%

Net profit margin 10.29% 11.43% 6.07% 10.34%

Total assets 67441 69863 56541 57894

Return on assets 18.17% 19.32% 10.51% 17.69%

Total equity capital 51525 53163 9944 15241

Return on equity 23.79% 25.39% 59.78% 67.18%

Looking at the changing market situations, it becomes important for all the managers to

measure their operational outcome and financial position so as to make solid decisions for the

future success. Strategic Financial Analysis (SFA) can be explained as a process of interpreting

financial results to identify reasons for poor performance so that better and effective decisions

can be made for meeting targets. The present assignment aims at analysing financial performance

of two British based companies that are Game Workshop Plc and Character Group Plc by using

ratio analysis methodology. It will be done on the basis of profitability measurement,

efficiency/activity ratios, liquidity performance and solvency position as well. Moreover, the

report will also describe the role of auditor and change in audit report as per recent UK auditing

and reporting standards. At the end, the report will apply investment appraisal techniques to

assess project viability for Trump Manufacturing to advice that whether they should invest

money or not.

Question 1

Internal and external financial performance analysis

Profitability ratios

Games workshop Plc Character Group plc

2015 (£000) 2016 (£000) 2014 (£000) 2015 (£000)

Turnover 119132 118069 97889 99054

Gross profit 82144 80631 29137 36655

Net profit 12257 13496 5945 10239

Gross profit margin 68.95% 68.29% 29.77% 37.01%

Net profit margin 10.29% 11.43% 6.07% 10.34%

Total assets 67441 69863 56541 57894

Return on assets 18.17% 19.32% 10.51% 17.69%

Total equity capital 51525 53163 9944 15241

Return on equity 23.79% 25.39% 59.78% 67.18%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profitability narratives:

Profitability ratios measure that how efficiently an organization is generating return on

their total business revenue (Bhattacharjee and Moreno, 2013). Games workshop Plc (GWP) and

Character Group Plc’s (CGP) profit performance has been analyzed here using various

performance evaluation ratios, enumerated hereunder:

Profitability ratios measure that how efficiently an organization is generating return on

their total business revenue (Bhattacharjee and Moreno, 2013). Games workshop Plc (GWP) and

Character Group Plc’s (CGP) profit performance has been analyzed here using various

performance evaluation ratios, enumerated hereunder:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gross margin (GM): In 2016, GWP’s GM shows a little decline from 68.95% to 68.29%

however, CGP’s GM inclined from 29.77% to 37.01% in 2015. Decreased turnover by 0.89%

and rise in cost of sale by 1.22% are the reason for declined gross profit in GWP by 1.22% in

2016. It may be because of high rate of inflation resulted in lower demand, poor quality of

delivering and ineffective managerial control over cost. Although, rising trend is considered

good but still, high ratio of GWP indicates that it is generating greater return on their total

turnover as compare to that of CGP.

however, CGP’s GM inclined from 29.77% to 37.01% in 2015. Decreased turnover by 0.89%

and rise in cost of sale by 1.22% are the reason for declined gross profit in GWP by 1.22% in

2016. It may be because of high rate of inflation resulted in lower demand, poor quality of

delivering and ineffective managerial control over cost. Although, rising trend is considered

good but still, high ratio of GWP indicates that it is generating greater return on their total

turnover as compare to that of CGP.

Net margin: GWP’s NM got enhanced from 10.29% to 11.43% in 2016, whilst, CGP’s

ratio got increased from 6.07% to 10.34%. Although, both the company’s ratio got increased

which is a sign of improved performance, but still, it is comparatively greater in GBP shows that

it generated maximum yield on total turnover. High income from royalty worth £5,939,000 and

decreased taxation payment to £3,452,000 is the reason for high net yield of £13,496,000 in

2016. On the contrary to this, CWP’s tax payments got increased by 74.61% and administration

expenditures got increased by 16.24% in the year 2015. Moreover, its operational income got

declined by 9.35%. On the other hand, less selling and distribution cost, high interest earning and

decreased interest obligation resulted in increased profitability margin to 10.34%.

ratio got increased from 6.07% to 10.34%. Although, both the company’s ratio got increased

which is a sign of improved performance, but still, it is comparatively greater in GBP shows that

it generated maximum yield on total turnover. High income from royalty worth £5,939,000 and

decreased taxation payment to £3,452,000 is the reason for high net yield of £13,496,000 in

2016. On the contrary to this, CWP’s tax payments got increased by 74.61% and administration

expenditures got increased by 16.24% in the year 2015. Moreover, its operational income got

declined by 9.35%. On the other hand, less selling and distribution cost, high interest earning and

decreased interest obligation resulted in increased profitability margin to 10.34%.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Return on assets: GWP’s ROA got improved from 18.17% to 19.32% in the year 2016

which demonstrates that in this year, company generated better yield on their total assets.

However, on the other side, CGP’s ROA shows high rate of increase from 10.51% to 17.69%.

High percentage increase in net yield by 72.23% in CGP as compare to yield improvement in

GWP to 10.11% is the main reason behind high rate of ROE increase in CGP. But still,

comparatively it is higher in GWP to 19.32% is a sign of more profitability on total corporate

assets.

Return on equity: It indicates profit percentage on total equity capital invested in the

organization. With reference to GWP, ROE rose up from 23.79% to 25.39% whereas CGP’s ROE

depicts a high rate of increase from 59.78% to 67.18% which is more than twice to that of GWP.

It clearly reflects that this organization is generating more return on their total stockholders’

equity and delivering them better return. Excessive rate of increase in net earnings by 72.23% as

compare to percentage increase in invested equity capital by 53.27% is the reason behind

increased ROE to 67.18%.

Liquidity ratio

This measure provides deeper insight to the information to which business unit has

enough amount of current assets to meet the financial obligations. Hence, by evaluating the

current and quick ratio stakeholders and organization itself would become able to assess the

extent to liquidity position of the firm is sound (Liquidity rations, 2016).

Liquidity ratio analysis of Games work shop and Character Plc

Games work shop Plc Character Plc

Particulars Formula 2015 2016 2014 2015

Current assets 30211 31160 50133 50537

Current

liabilities 15094 15591 46549 42486

Inventories 7625 8540 8854 8965

Current ratio

Current assets /

current

liabilities 2.0 2.0 1.1 1.2

which demonstrates that in this year, company generated better yield on their total assets.

However, on the other side, CGP’s ROA shows high rate of increase from 10.51% to 17.69%.

High percentage increase in net yield by 72.23% in CGP as compare to yield improvement in

GWP to 10.11% is the main reason behind high rate of ROE increase in CGP. But still,

comparatively it is higher in GWP to 19.32% is a sign of more profitability on total corporate

assets.

Return on equity: It indicates profit percentage on total equity capital invested in the

organization. With reference to GWP, ROE rose up from 23.79% to 25.39% whereas CGP’s ROE

depicts a high rate of increase from 59.78% to 67.18% which is more than twice to that of GWP.

It clearly reflects that this organization is generating more return on their total stockholders’

equity and delivering them better return. Excessive rate of increase in net earnings by 72.23% as

compare to percentage increase in invested equity capital by 53.27% is the reason behind

increased ROE to 67.18%.

Liquidity ratio

This measure provides deeper insight to the information to which business unit has

enough amount of current assets to meet the financial obligations. Hence, by evaluating the

current and quick ratio stakeholders and organization itself would become able to assess the

extent to liquidity position of the firm is sound (Liquidity rations, 2016).

Liquidity ratio analysis of Games work shop and Character Plc

Games work shop Plc Character Plc

Particulars Formula 2015 2016 2014 2015

Current assets 30211 31160 50133 50537

Current

liabilities 15094 15591 46549 42486

Inventories 7625 8540 8854 8965

Current ratio

Current assets /

current

liabilities 2.0 2.0 1.1 1.2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Quick ratio

Current assets

– inventories /

current

liabilities 1.50 1.45 0.89 0.98

Current ratio: From the above presented financial statement it has been analyzed that

current ratio of Games work shop Plc was 2 in both 2015 and 2016. On the other side,

current ratio of Character Plc inclined from 1.1 to 1.2 at the end of accounting year 2015.

Thus, by considering the ideal ratio such as 2:1 it can be said that Games work shop Plc

has enough amount to fulfil the financial obligations on time. Hence, company has 2

current assets to meet 1 liability. It shows that liquidity position of Games work shop Plc

is sound as compared to Character Plc. Further, it has been identified that Charcter Plc

needs to make focus on maintaining exert on cash and other current assets. This in turn

helps them in improving the liquidity position to the large extent.

Quick ratio: In the accounting year 2016 quick ratio of Games work shop Plc declined

from 1.50 to 1.45. Besides this, quick ratio of Character Plc inclined from .89 to .98 in

the financial period 2015. This aspect presents that quick ratio of Character Plc was good

during the period of 2015. Hence, it can be stated that company has ability to meet the

obligations more quickly by converting assets into cash. According to the ideal ratio

business unit must have 1 current asset to fulfil the 2 quick obligations. It reflects that

company has more current assets as compared to the needed. Thus, it is recommended to

both the organization to invest money in other productive activities rather than keeping

more money with themselves. Such strategy will provide assistance to the firms in

enhancing the profit or income to the large extent.

Efficiency ratio

It provides deeper insight about the level to which company has made effective use of

both current and non-current assets (Delen, Kuzey and Uyar, 2013). Such ratio assists company

in evaluating the effectinenes of strategies and potential of the personnel.

Games work shop Plc Character Plc

Particulars Formula 2015 2016 2014 2015

Current assets

– inventories /

current

liabilities 1.50 1.45 0.89 0.98

Current ratio: From the above presented financial statement it has been analyzed that

current ratio of Games work shop Plc was 2 in both 2015 and 2016. On the other side,

current ratio of Character Plc inclined from 1.1 to 1.2 at the end of accounting year 2015.

Thus, by considering the ideal ratio such as 2:1 it can be said that Games work shop Plc

has enough amount to fulfil the financial obligations on time. Hence, company has 2

current assets to meet 1 liability. It shows that liquidity position of Games work shop Plc

is sound as compared to Character Plc. Further, it has been identified that Charcter Plc

needs to make focus on maintaining exert on cash and other current assets. This in turn

helps them in improving the liquidity position to the large extent.

Quick ratio: In the accounting year 2016 quick ratio of Games work shop Plc declined

from 1.50 to 1.45. Besides this, quick ratio of Character Plc inclined from .89 to .98 in

the financial period 2015. This aspect presents that quick ratio of Character Plc was good

during the period of 2015. Hence, it can be stated that company has ability to meet the

obligations more quickly by converting assets into cash. According to the ideal ratio

business unit must have 1 current asset to fulfil the 2 quick obligations. It reflects that

company has more current assets as compared to the needed. Thus, it is recommended to

both the organization to invest money in other productive activities rather than keeping

more money with themselves. Such strategy will provide assistance to the firms in

enhancing the profit or income to the large extent.

Efficiency ratio

It provides deeper insight about the level to which company has made effective use of

both current and non-current assets (Delen, Kuzey and Uyar, 2013). Such ratio assists company

in evaluating the effectinenes of strategies and potential of the personnel.

Games work shop Plc Character Plc

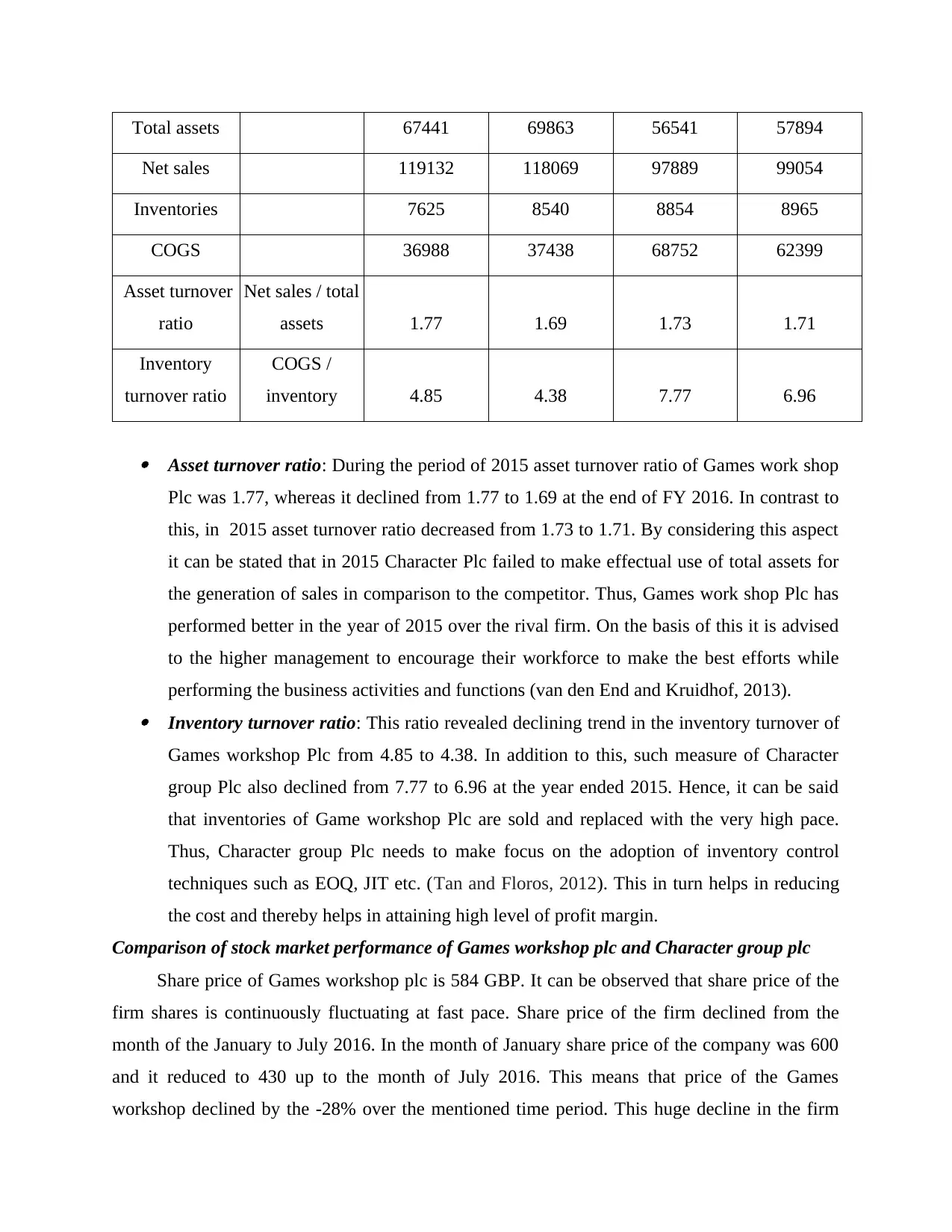

Particulars Formula 2015 2016 2014 2015

Total assets 67441 69863 56541 57894

Net sales 119132 118069 97889 99054

Inventories 7625 8540 8854 8965

COGS 36988 37438 68752 62399

Asset turnover

ratio

Net sales / total

assets 1.77 1.69 1.73 1.71

Inventory

turnover ratio

COGS /

inventory 4.85 4.38 7.77 6.96

Asset turnover ratio: During the period of 2015 asset turnover ratio of Games work shop

Plc was 1.77, whereas it declined from 1.77 to 1.69 at the end of FY 2016. In contrast to

this, in 2015 asset turnover ratio decreased from 1.73 to 1.71. By considering this aspect

it can be stated that in 2015 Character Plc failed to make effectual use of total assets for

the generation of sales in comparison to the competitor. Thus, Games work shop Plc has

performed better in the year of 2015 over the rival firm. On the basis of this it is advised

to the higher management to encourage their workforce to make the best efforts while

performing the business activities and functions (van den End and Kruidhof, 2013). Inventory turnover ratio: This ratio revealed declining trend in the inventory turnover of

Games workshop Plc from 4.85 to 4.38. In addition to this, such measure of Character

group Plc also declined from 7.77 to 6.96 at the year ended 2015. Hence, it can be said

that inventories of Game workshop Plc are sold and replaced with the very high pace.

Thus, Character group Plc needs to make focus on the adoption of inventory control

techniques such as EOQ, JIT etc. (Tan and Floros, 2012). This in turn helps in reducing

the cost and thereby helps in attaining high level of profit margin.

Comparison of stock market performance of Games workshop plc and Character group plc

Share price of Games workshop plc is 584 GBP. It can be observed that share price of the

firm shares is continuously fluctuating at fast pace. Share price of the firm declined from the

month of the January to July 2016. In the month of January share price of the company was 600

and it reduced to 430 up to the month of July 2016. This means that price of the Games

workshop declined by the -28% over the mentioned time period. This huge decline in the firm

Net sales 119132 118069 97889 99054

Inventories 7625 8540 8854 8965

COGS 36988 37438 68752 62399

Asset turnover

ratio

Net sales / total

assets 1.77 1.69 1.73 1.71

Inventory

turnover ratio

COGS /

inventory 4.85 4.38 7.77 6.96

Asset turnover ratio: During the period of 2015 asset turnover ratio of Games work shop

Plc was 1.77, whereas it declined from 1.77 to 1.69 at the end of FY 2016. In contrast to

this, in 2015 asset turnover ratio decreased from 1.73 to 1.71. By considering this aspect

it can be stated that in 2015 Character Plc failed to make effectual use of total assets for

the generation of sales in comparison to the competitor. Thus, Games work shop Plc has

performed better in the year of 2015 over the rival firm. On the basis of this it is advised

to the higher management to encourage their workforce to make the best efforts while

performing the business activities and functions (van den End and Kruidhof, 2013). Inventory turnover ratio: This ratio revealed declining trend in the inventory turnover of

Games workshop Plc from 4.85 to 4.38. In addition to this, such measure of Character

group Plc also declined from 7.77 to 6.96 at the year ended 2015. Hence, it can be said

that inventories of Game workshop Plc are sold and replaced with the very high pace.

Thus, Character group Plc needs to make focus on the adoption of inventory control

techniques such as EOQ, JIT etc. (Tan and Floros, 2012). This in turn helps in reducing

the cost and thereby helps in attaining high level of profit margin.

Comparison of stock market performance of Games workshop plc and Character group plc

Share price of Games workshop plc is 584 GBP. It can be observed that share price of the

firm shares is continuously fluctuating at fast pace. Share price of the firm declined from the

month of the January to July 2016. In the month of January share price of the company was 600

and it reduced to 430 up to the month of July 2016. This means that price of the Games

workshop declined by the -28% over the mentioned time period. This huge decline in the firm

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

share price revealed that it lose confidence among the investors (Patel, 2016). However, after

time period rebound is observed in the firm shares. As share price increase from 430 to 584 GBP

in the December month. This means that company share price increased by 26% from the month

August to December 2016. This entire story makes it clear that firm shares are highly volatile.

Price of same never remain stable in the specific range. Hence, there is heavy risk on the

investment if made in the Games workshop plc. In case shares price will increase huge amount

of profit can earned on same. Contrary to this, if shares price get declined then big amount of

loss can be faced on the investment amount. Hence, investor need to follow a cautious approach

before taking final decisions.

In case of Character group plc current share price is 460 GBP. In case of the mentioned

firm trend is different. In case of the mentioned firm it can be seen that share price increase at

rapid pace from 470 to 650 from the month of the January to June 2016. This reflects that share

price increased by 28% between this 6 month duration or half year. After the month of June 2016

trend get changed and many times large ups and down are observed in the firm shares price. It

must be noted that from the month of June to July share price declined sharply. During the

mentioned time period shares price decline by -18%. This is the huge decline in the any company

share price. Those who make heavy investment in the Character group plc face a big loss on

investment. After this decline again upward movement comes in existence in the mentioned firm

share price (Malik, Awais and Khursheed, 2016). In July month share price was 428 which

increase to 523 GBP in the month of the September. This means that 18% plunge was observed

in the firm shares price in the three months’ time period. After the month of September small up

and down are observed in the firm shares price.

If comparison is made between both firms share price then it can be observed that price of

both company shares keeps on fluctuating consistently. However, in case of the Game workshop

group plc higher fluctuation is observed in comparison to the other company. As for long time

nearby to 6 months consistently share price declined. Due to this reason investors face huge loss

in the investment that they made in the Game workshop group plc. In case of Character group plc

also fluctuation is observed but that same trend does not persist for long time in the stock market.

It can be said that investors does not losing their money on the investment that they made in the

Character group plc shares. Investors are getting earning opportunity more in case of Character

group plc relative to Games workshop plc. Hence, it can be said that former firm perform better

time period rebound is observed in the firm shares. As share price increase from 430 to 584 GBP

in the December month. This means that company share price increased by 26% from the month

August to December 2016. This entire story makes it clear that firm shares are highly volatile.

Price of same never remain stable in the specific range. Hence, there is heavy risk on the

investment if made in the Games workshop plc. In case shares price will increase huge amount

of profit can earned on same. Contrary to this, if shares price get declined then big amount of

loss can be faced on the investment amount. Hence, investor need to follow a cautious approach

before taking final decisions.

In case of Character group plc current share price is 460 GBP. In case of the mentioned

firm trend is different. In case of the mentioned firm it can be seen that share price increase at

rapid pace from 470 to 650 from the month of the January to June 2016. This reflects that share

price increased by 28% between this 6 month duration or half year. After the month of June 2016

trend get changed and many times large ups and down are observed in the firm shares price. It

must be noted that from the month of June to July share price declined sharply. During the

mentioned time period shares price decline by -18%. This is the huge decline in the any company

share price. Those who make heavy investment in the Character group plc face a big loss on

investment. After this decline again upward movement comes in existence in the mentioned firm

share price (Malik, Awais and Khursheed, 2016). In July month share price was 428 which

increase to 523 GBP in the month of the September. This means that 18% plunge was observed

in the firm shares price in the three months’ time period. After the month of September small up

and down are observed in the firm shares price.

If comparison is made between both firms share price then it can be observed that price of

both company shares keeps on fluctuating consistently. However, in case of the Game workshop

group plc higher fluctuation is observed in comparison to the other company. As for long time

nearby to 6 months consistently share price declined. Due to this reason investors face huge loss

in the investment that they made in the Game workshop group plc. In case of Character group plc

also fluctuation is observed but that same trend does not persist for long time in the stock market.

It can be said that investors does not losing their money on the investment that they made in the

Character group plc shares. Investors are getting earning opportunity more in case of Character

group plc relative to Games workshop plc. Hence, it can be said that former firm perform better

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in the stock market relative to the latter firm (Luo and et.al., 2015). In other words it can be said

that investors have more confidence on the Character group plc then Games workshop plc. Both

firms can be compared on the basis of price earnings ratio. It is the ratio which reflects valuation

of company shares. This method help in identifying whether firm shares are overvalued or

undervalued (Lartey, Antwi and Boadi, 2013). Price earnings ratio of Character group plc is

10.66 and same of the Games workshop groups is 13.93. This means that shares of the Games

workshop plc are available at a higher price than Character group plc. This means that on the

basis of consideration of the stock market performance investment must be made in the latter

firm relative to former firm.

Q2. Role of auditor and changes incorporated in the audit report

Auditing standards are framed in order to guide all the auditors by handling their primary

duty of observing the financial statements. These standards are prepared by an entity which

emphasizes on the financial statements of the business which includes objectives for the auditors

and all the business requirement which needs to be followed by the auditors in fulfilling its basic

responsibilities towards an entity (Keune and Johnstone, 2012). The role of the auditors to assess

the authenticity of the financial statement by expressing their opinions on the truth and fairness

of the financial statements by commenting upon the efficiency of the business.

The international standards of auditing of UK has been framed in order to cater the

external needs and aspirations by changes takes places in the external environment which will

created direct impact on the internal business entity (Dwivedi and et.al., 2013). The financial

reporting standards will come into existence in order to help an entity by improving the financial

errors by checking their statements by appointing auditors in their organizations (Gul, Zhou and

Zhu, 2013). The roles and responsibilities of all the auditors appointed in an entity need to

comply with the rules framed bey the external legal authority. There are various roles and

responsibilities of auditors in assessing the accuracy of all the financial statements which are

given as follows:

It helps in identifying the areas of material mi statement occurred in an enterprise which

helps in improving the current efficiency of all the financial statements. This poliucies will need

to define all the prospective errors discovered in assessing the financial statements such as

frauds, errors, default in the designing of internal control.

that investors have more confidence on the Character group plc then Games workshop plc. Both

firms can be compared on the basis of price earnings ratio. It is the ratio which reflects valuation

of company shares. This method help in identifying whether firm shares are overvalued or

undervalued (Lartey, Antwi and Boadi, 2013). Price earnings ratio of Character group plc is

10.66 and same of the Games workshop groups is 13.93. This means that shares of the Games

workshop plc are available at a higher price than Character group plc. This means that on the

basis of consideration of the stock market performance investment must be made in the latter

firm relative to former firm.

Q2. Role of auditor and changes incorporated in the audit report

Auditing standards are framed in order to guide all the auditors by handling their primary

duty of observing the financial statements. These standards are prepared by an entity which

emphasizes on the financial statements of the business which includes objectives for the auditors

and all the business requirement which needs to be followed by the auditors in fulfilling its basic

responsibilities towards an entity (Keune and Johnstone, 2012). The role of the auditors to assess

the authenticity of the financial statement by expressing their opinions on the truth and fairness

of the financial statements by commenting upon the efficiency of the business.

The international standards of auditing of UK has been framed in order to cater the

external needs and aspirations by changes takes places in the external environment which will

created direct impact on the internal business entity (Dwivedi and et.al., 2013). The financial

reporting standards will come into existence in order to help an entity by improving the financial

errors by checking their statements by appointing auditors in their organizations (Gul, Zhou and

Zhu, 2013). The roles and responsibilities of all the auditors appointed in an entity need to

comply with the rules framed bey the external legal authority. There are various roles and

responsibilities of auditors in assessing the accuracy of all the financial statements which are

given as follows:

It helps in identifying the areas of material mi statement occurred in an enterprise which

helps in improving the current efficiency of all the financial statements. This poliucies will need

to define all the prospective errors discovered in assessing the financial statements such as

frauds, errors, default in the designing of internal control.

The internal control are also observed as this also assess the weakness of the internal control

which shows the deficiency of the management in assigning responsibilities and designing

various kinds of procedures. The changes need to be incorporate by the auditors as they can

modify their opinion in case of any kind of evidence discovered on a later stage. The opinion of

the auditors can be altered due to ascertain of material misstatements on later year (Eliasson and

Börjesson, 2014). The duty of an enterprise is to make significant changes in the already

prepared audit report by incorporating changes in the existing held audit report. In the case of

lack of evidences obtained by the auditors then in that case auditor can make disclaimer of

opinion.

The changes can be in the form of legal regulations which are constantly changes which

needs to be complied by all auditors as their appointment is affected by the regulations (Guerra,

Magni and Stefanini, 2012). The disclosures are the basic thing which needs to be prepared by

the auditors as the changes occurred in an enterprise which have material effect on the financial

statements should be incorporated into the current business efficiency. This needs to be taken

into consideration as this can affect an enterprise's efficiency by achieving all the targets of

seeking opportunities in the external market by reflecting accurate financial statements. The

audited statements are regarded as one of the important statements that can be negotiated for

taking loans.

Question 3: Computation of IRR

Internal rate of return is that rate which indicates that rate at which both the total

discounted cash flows and initial investment are equal indicates zero value of net present value

(Fahmi and Saputra, 2013).

Initial investment 100000

Machinery 440000

Total investment 540000

Items 1 2 3 4

Selling units 20000 21000 22050 16000

Sales price 40 40 40 40

Expected sales 800000 840000 882000 640000

which shows the deficiency of the management in assigning responsibilities and designing

various kinds of procedures. The changes need to be incorporate by the auditors as they can

modify their opinion in case of any kind of evidence discovered on a later stage. The opinion of

the auditors can be altered due to ascertain of material misstatements on later year (Eliasson and

Börjesson, 2014). The duty of an enterprise is to make significant changes in the already

prepared audit report by incorporating changes in the existing held audit report. In the case of

lack of evidences obtained by the auditors then in that case auditor can make disclaimer of

opinion.

The changes can be in the form of legal regulations which are constantly changes which

needs to be complied by all auditors as their appointment is affected by the regulations (Guerra,

Magni and Stefanini, 2012). The disclosures are the basic thing which needs to be prepared by

the auditors as the changes occurred in an enterprise which have material effect on the financial

statements should be incorporated into the current business efficiency. This needs to be taken

into consideration as this can affect an enterprise's efficiency by achieving all the targets of

seeking opportunities in the external market by reflecting accurate financial statements. The

audited statements are regarded as one of the important statements that can be negotiated for

taking loans.

Question 3: Computation of IRR

Internal rate of return is that rate which indicates that rate at which both the total

discounted cash flows and initial investment are equal indicates zero value of net present value

(Fahmi and Saputra, 2013).

Initial investment 100000

Machinery 440000

Total investment 540000

Items 1 2 3 4

Selling units 20000 21000 22050 16000

Sales price 40 40 40 40

Expected sales 800000 840000 882000 640000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.