Partnership Income and Expenses Calculation

VerifiedAdded on 2020/04/01

|11

|1690

|35

AI Summary

This assignment focuses on calculating the net profit of a partnership firm in Australia. It provides a detailed breakdown of various income and expense items, including interest expenses, travel costs, office fees, salaries, cost of goods sold, rent, bad debt losses, and pilferage. The calculation involves applying relevant tax regulations and setting off losses incurred in the previous year. Students need to analyze the provided data and accurately compute the partnership's net income for the income year.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................3

Answer to Question 3:.....................................................................................................................6

Answer to Question 4:.....................................................................................................................9

References:....................................................................................................................................12

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................3

Answer to Question 3:.....................................................................................................................6

Answer to Question 4:.....................................................................................................................9

References:....................................................................................................................................12

2TAXATION LAW

Answer to Question 1:

“Section 4-15 of the Income Tax Assessment Act 1997” states that in order to calculate

taxable income, the allowable expenses are deducted from assessable income. In addition, a

taxpayer is allowed in claiming deduction under “Section 8-1(1) of the ITAA 1997” for

expenditures incurred on gaining or developing assessable income along with conducting the

activities associated with the businesses1. Hence, the following points are discussed briefly as

follows:

1) According to “Section 8-1”, the amount spent on moving a machinery would be taken

into account for deduction only, if the machinery is utilised in earning an income, which

is taxable. In case of “Granite Supply Association Ltd v Kitton (1905) and Smith v

Westinghouse Brake Company (1888)”, the sum of money incurred for relocating

expenses and plant would not be allowed as deduction due to the capital nature of the

expenditures.

2) “Section 8-1 of ITAA 1997” denotes that the cost of revaluation related to an asset is not

considered as deductible expense2.

3) “Section 8-1 of ITAA 1997” represents that any expenditure related to lawful suits is

suffered in contrast to the closure of the company and this would be taken into account in

the form of deductible expenditure3.

1 Caldwell, R, Taxation for Australian businesses. in .

2 Morgan, A, C Mortimer, & D Pinto, A practical introduction to Australian taxation law. in .

Answer to Question 1:

“Section 4-15 of the Income Tax Assessment Act 1997” states that in order to calculate

taxable income, the allowable expenses are deducted from assessable income. In addition, a

taxpayer is allowed in claiming deduction under “Section 8-1(1) of the ITAA 1997” for

expenditures incurred on gaining or developing assessable income along with conducting the

activities associated with the businesses1. Hence, the following points are discussed briefly as

follows:

1) According to “Section 8-1”, the amount spent on moving a machinery would be taken

into account for deduction only, if the machinery is utilised in earning an income, which

is taxable. In case of “Granite Supply Association Ltd v Kitton (1905) and Smith v

Westinghouse Brake Company (1888)”, the sum of money incurred for relocating

expenses and plant would not be allowed as deduction due to the capital nature of the

expenditures.

2) “Section 8-1 of ITAA 1997” denotes that the cost of revaluation related to an asset is not

considered as deductible expense2.

3) “Section 8-1 of ITAA 1997” represents that any expenditure related to lawful suits is

suffered in contrast to the closure of the company and this would be taken into account in

the form of deductible expenditure3.

1 Caldwell, R, Taxation for Australian businesses. in .

2 Morgan, A, C Mortimer, & D Pinto, A practical introduction to Australian taxation law. in .

3TAXATION LAW

4) As laid out in “Section 8-1 of ITAA 1997”, in order to assure business income, with prior

experience of solicitor expense, it would be considered in the form of permissible

deduction4.

Answer to Question 2:

If a business organisation makes any purchase, the input credit of GST is permitted only,

in case; pertinent documents are stored properly in association with such transactions. According

to “GST Act 1999”, any organisation intending to make business income possesses the right to

obtain credit of input for payments related to GST involving material or asset purchase5.

Issue:

It has been identified from the provided case that Big Bank Limited has incurred

advertisement expenditure of $1,650,000 that includes GST as well. In the current scenario, the

bank intends to assure that the overall expenditures related to advertisement would be permitted

as credit of input or not, as the expenditures include GST6.

3 Woellner, R, S Barkoczy, S Murphy, C Evans, & D Pinto, Australian taxation law select 2014.

in .

4 Kenny, P, Australian tax 2013. in , Chatswood, N.S.W., LexisNexis Butterworths, 2013.

5 Woellner, R, R Woellner, S Barkoczy, S Murphy, C Evans, & D Pinto, Australian Taxation

Law 2015. in .

6 Krever, R, Australian taxation law cases 2013. in , Pyrmont, N.S.W., Thomson Reuters, 2013.

4) As laid out in “Section 8-1 of ITAA 1997”, in order to assure business income, with prior

experience of solicitor expense, it would be considered in the form of permissible

deduction4.

Answer to Question 2:

If a business organisation makes any purchase, the input credit of GST is permitted only,

in case; pertinent documents are stored properly in association with such transactions. According

to “GST Act 1999”, any organisation intending to make business income possesses the right to

obtain credit of input for payments related to GST involving material or asset purchase5.

Issue:

It has been identified from the provided case that Big Bank Limited has incurred

advertisement expenditure of $1,650,000 that includes GST as well. In the current scenario, the

bank intends to assure that the overall expenditures related to advertisement would be permitted

as credit of input or not, as the expenditures include GST6.

3 Woellner, R, S Barkoczy, S Murphy, C Evans, & D Pinto, Australian taxation law select 2014.

in .

4 Kenny, P, Australian tax 2013. in , Chatswood, N.S.W., LexisNexis Butterworths, 2013.

5 Woellner, R, R Woellner, S Barkoczy, S Murphy, C Evans, & D Pinto, Australian Taxation

Law 2015. in .

6 Krever, R, Australian taxation law cases 2013. in , Pyrmont, N.S.W., Thomson Reuters, 2013.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

Rules:

As identified from the “Chapter 2 of the Goods and Services Act 1999”, input tax credit

including GST would be permitted to an organisation on the incurred expenditures at the time of

general course of the business. However, it is to be noted that such expenses include the amount

of GST.

Application:

Big Bank Limited is a financial organisation that provides services to the individuals

having more than 50 branches throughout the province of Australia. It has a 10-storied

apartment, in which its head office is situated. Along with, there has been the introduction of

home content and insurance policy in Australian market coupled with loan and deposit

provisions of the customers over the years7. In order to carry out advertising work, the bank has

kept apart a budget amounting to $1,650,000 from which $550,000 is invested for house

advertisement and insurance products. With the help of such investment, the organisation has

managed to generate 2% of its overall revenues. The leftover amount of $1,100,000 is for

promoting the other services of the organisation and it takes into consideration the GST as well8.

Therefore, it has been evaluated that $1,100,000 had been incurred for the promotion of

services for generation of maximum revenue, while the amount of $550,000 is to be considered

7 Woellner, R, Australian taxation law select 2013. in , North Ryde, N.S.W., CCH Australia,

2013.

8 Morgan, A, C Mortimer, & D Pinto, A practical introduction to Australian taxation law. in ,

North Ryde [N.S.W.], CCH Australia, 2013.

Rules:

As identified from the “Chapter 2 of the Goods and Services Act 1999”, input tax credit

including GST would be permitted to an organisation on the incurred expenditures at the time of

general course of the business. However, it is to be noted that such expenses include the amount

of GST.

Application:

Big Bank Limited is a financial organisation that provides services to the individuals

having more than 50 branches throughout the province of Australia. It has a 10-storied

apartment, in which its head office is situated. Along with, there has been the introduction of

home content and insurance policy in Australian market coupled with loan and deposit

provisions of the customers over the years7. In order to carry out advertising work, the bank has

kept apart a budget amounting to $1,650,000 from which $550,000 is invested for house

advertisement and insurance products. With the help of such investment, the organisation has

managed to generate 2% of its overall revenues. The leftover amount of $1,100,000 is for

promoting the other services of the organisation and it takes into consideration the GST as well8.

Therefore, it has been evaluated that $1,100,000 had been incurred for the promotion of

services for generation of maximum revenue, while the amount of $550,000 is to be considered

7 Woellner, R, Australian taxation law select 2013. in , North Ryde, N.S.W., CCH Australia,

2013.

8 Morgan, A, C Mortimer, & D Pinto, A practical introduction to Australian taxation law. in ,

North Ryde [N.S.W.], CCH Australia, 2013.

5TAXATION LAW

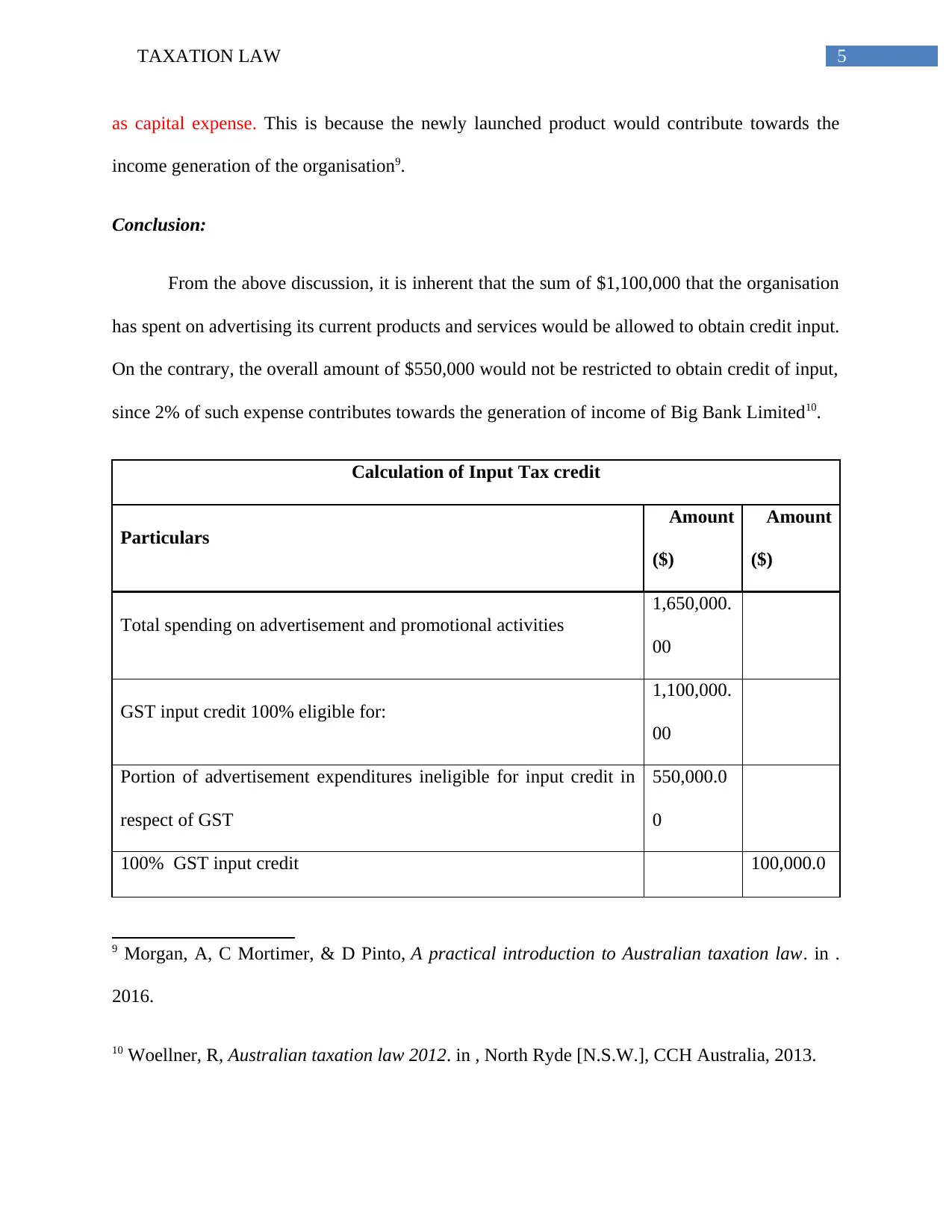

as capital expense. This is because the newly launched product would contribute towards the

income generation of the organisation9.

Conclusion:

From the above discussion, it is inherent that the sum of $1,100,000 that the organisation

has spent on advertising its current products and services would be allowed to obtain credit input.

On the contrary, the overall amount of $550,000 would not be restricted to obtain credit of input,

since 2% of such expense contributes towards the generation of income of Big Bank Limited10.

Calculation of Input Tax credit

Particulars

Amount

($)

Amount

($)

Total spending on advertisement and promotional activities

1,650,000.

00

GST input credit 100% eligible for:

1,100,000.

00

Portion of advertisement expenditures ineligible for input credit in

respect of GST

550,000.0

0

100% GST input credit 100,000.0

9 Morgan, A, C Mortimer, & D Pinto, A practical introduction to Australian taxation law. in .

2016.

10 Woellner, R, Australian taxation law 2012. in , North Ryde [N.S.W.], CCH Australia, 2013.

as capital expense. This is because the newly launched product would contribute towards the

income generation of the organisation9.

Conclusion:

From the above discussion, it is inherent that the sum of $1,100,000 that the organisation

has spent on advertising its current products and services would be allowed to obtain credit input.

On the contrary, the overall amount of $550,000 would not be restricted to obtain credit of input,

since 2% of such expense contributes towards the generation of income of Big Bank Limited10.

Calculation of Input Tax credit

Particulars

Amount

($)

Amount

($)

Total spending on advertisement and promotional activities

1,650,000.

00

GST input credit 100% eligible for:

1,100,000.

00

Portion of advertisement expenditures ineligible for input credit in

respect of GST

550,000.0

0

100% GST input credit 100,000.0

9 Morgan, A, C Mortimer, & D Pinto, A practical introduction to Australian taxation law. in .

2016.

10 Woellner, R, Australian taxation law 2012. in , North Ryde [N.S.W.], CCH Australia, 2013.

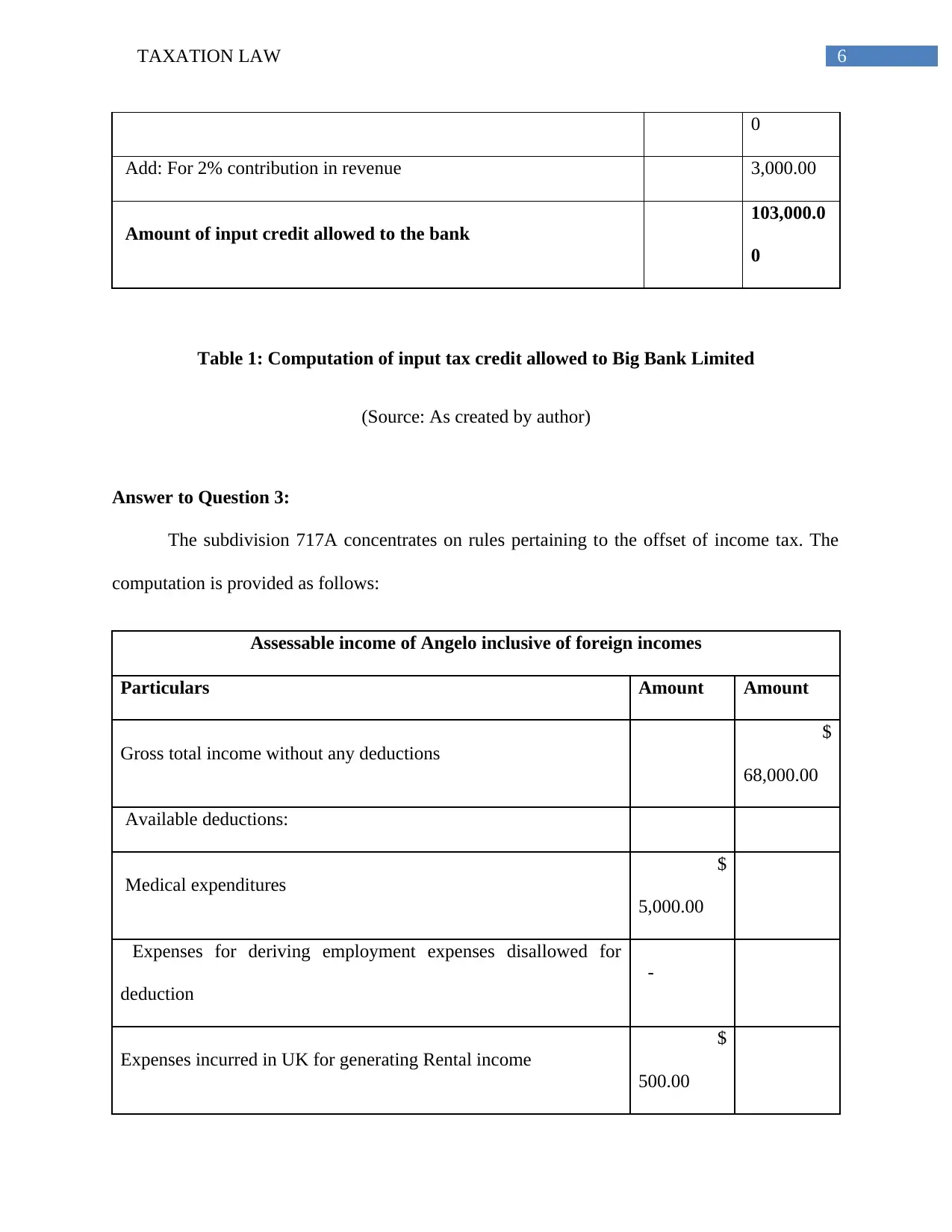

6TAXATION LAW

0

Add: For 2% contribution in revenue 3,000.00

Amount of input credit allowed to the bank

103,000.0

0

Table 1: Computation of input tax credit allowed to Big Bank Limited

(Source: As created by author)

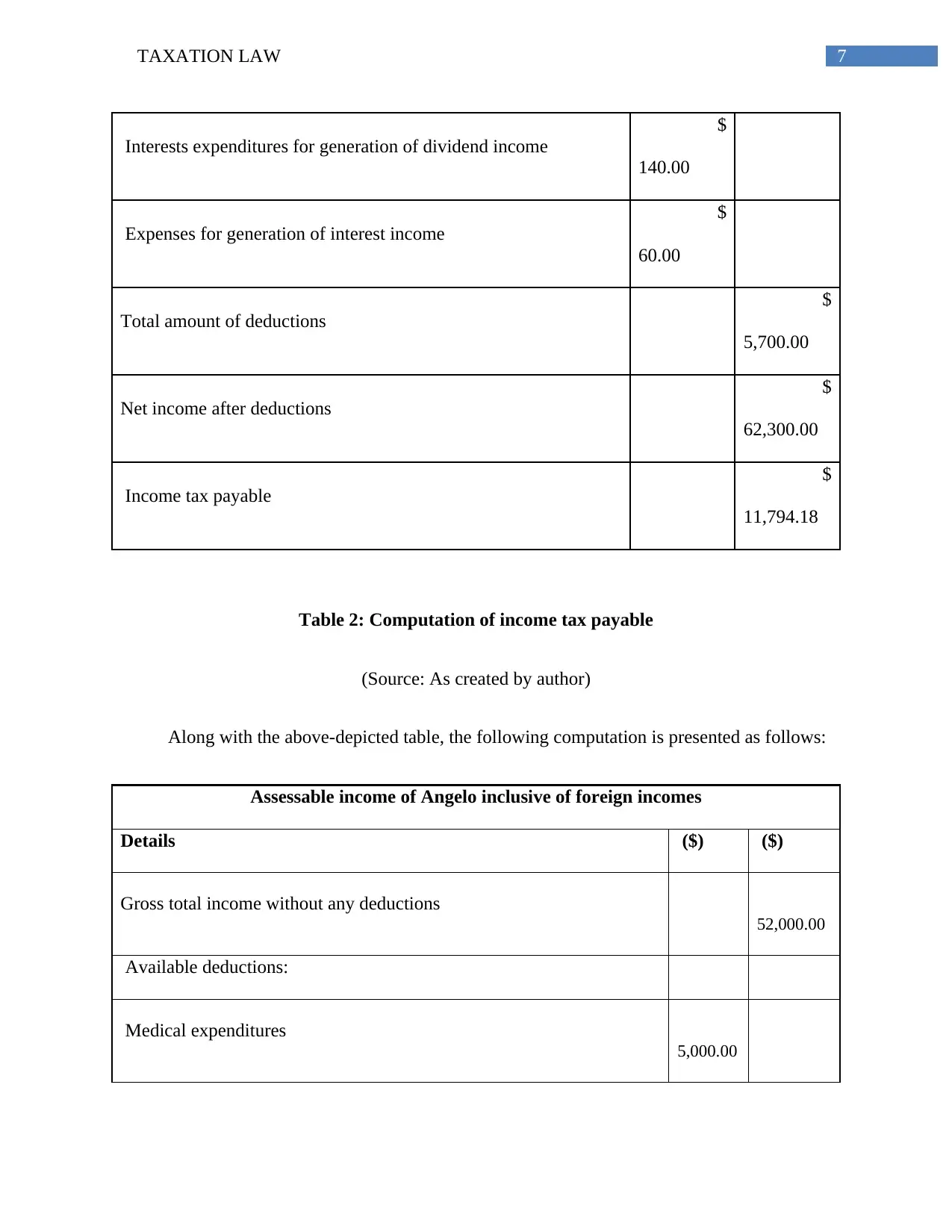

Answer to Question 3:

The subdivision 717A concentrates on rules pertaining to the offset of income tax. The

computation is provided as follows:

Assessable income of Angelo inclusive of foreign incomes

Particulars Amount Amount

Gross total income without any deductions

$

68,000.00

Available deductions:

Medical expenditures

$

5,000.00

Expenses for deriving employment expenses disallowed for

deduction

-

Expenses incurred in UK for generating Rental income

$

500.00

0

Add: For 2% contribution in revenue 3,000.00

Amount of input credit allowed to the bank

103,000.0

0

Table 1: Computation of input tax credit allowed to Big Bank Limited

(Source: As created by author)

Answer to Question 3:

The subdivision 717A concentrates on rules pertaining to the offset of income tax. The

computation is provided as follows:

Assessable income of Angelo inclusive of foreign incomes

Particulars Amount Amount

Gross total income without any deductions

$

68,000.00

Available deductions:

Medical expenditures

$

5,000.00

Expenses for deriving employment expenses disallowed for

deduction

-

Expenses incurred in UK for generating Rental income

$

500.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Interests expenditures for generation of dividend income

$

140.00

Expenses for generation of interest income

$

60.00

Total amount of deductions

$

5,700.00

Net income after deductions

$

62,300.00

Income tax payable

$

11,794.18

Table 2: Computation of income tax payable

(Source: As created by author)

Along with the above-depicted table, the following computation is presented as follows:

Assessable income of Angelo inclusive of foreign incomes

Details ($) ($)

Gross total income without any deductions

52,000.00

Available deductions:

Medical expenditures

5,000.00

Interests expenditures for generation of dividend income

$

140.00

Expenses for generation of interest income

$

60.00

Total amount of deductions

$

5,700.00

Net income after deductions

$

62,300.00

Income tax payable

$

11,794.18

Table 2: Computation of income tax payable

(Source: As created by author)

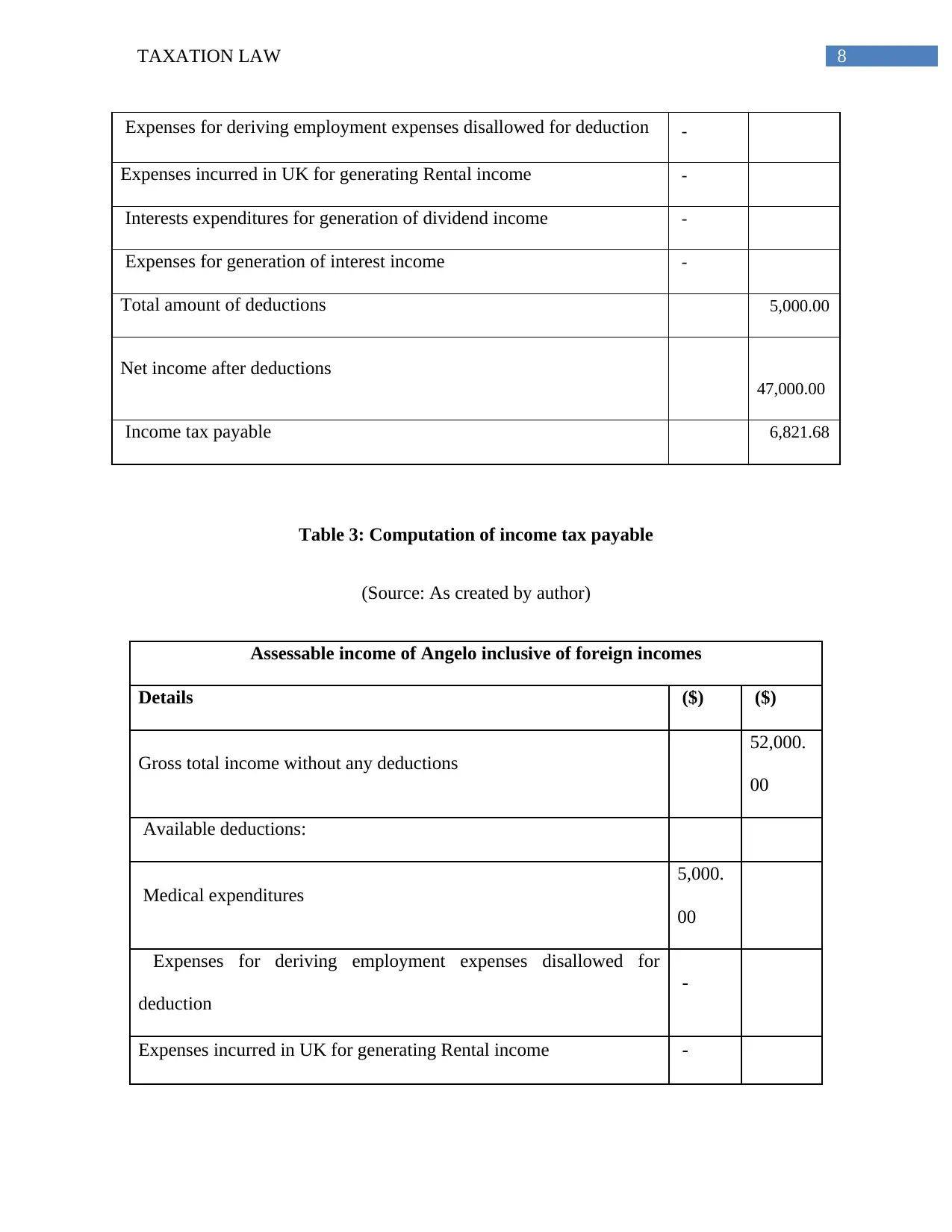

Along with the above-depicted table, the following computation is presented as follows:

Assessable income of Angelo inclusive of foreign incomes

Details ($) ($)

Gross total income without any deductions

52,000.00

Available deductions:

Medical expenditures

5,000.00

8TAXATION LAW

Expenses for deriving employment expenses disallowed for deduction -

Expenses incurred in UK for generating Rental income -

Interests expenditures for generation of dividend income -

Expenses for generation of interest income -

Total amount of deductions 5,000.00

Net income after deductions

47,000.00

Income tax payable 6,821.68

Table 3: Computation of income tax payable

(Source: As created by author)

Assessable income of Angelo inclusive of foreign incomes

Details ($) ($)

Gross total income without any deductions

52,000.

00

Available deductions:

Medical expenditures

5,000.

00

Expenses for deriving employment expenses disallowed for

deduction

-

Expenses incurred in UK for generating Rental income -

Expenses for deriving employment expenses disallowed for deduction -

Expenses incurred in UK for generating Rental income -

Interests expenditures for generation of dividend income -

Expenses for generation of interest income -

Total amount of deductions 5,000.00

Net income after deductions

47,000.00

Income tax payable 6,821.68

Table 3: Computation of income tax payable

(Source: As created by author)

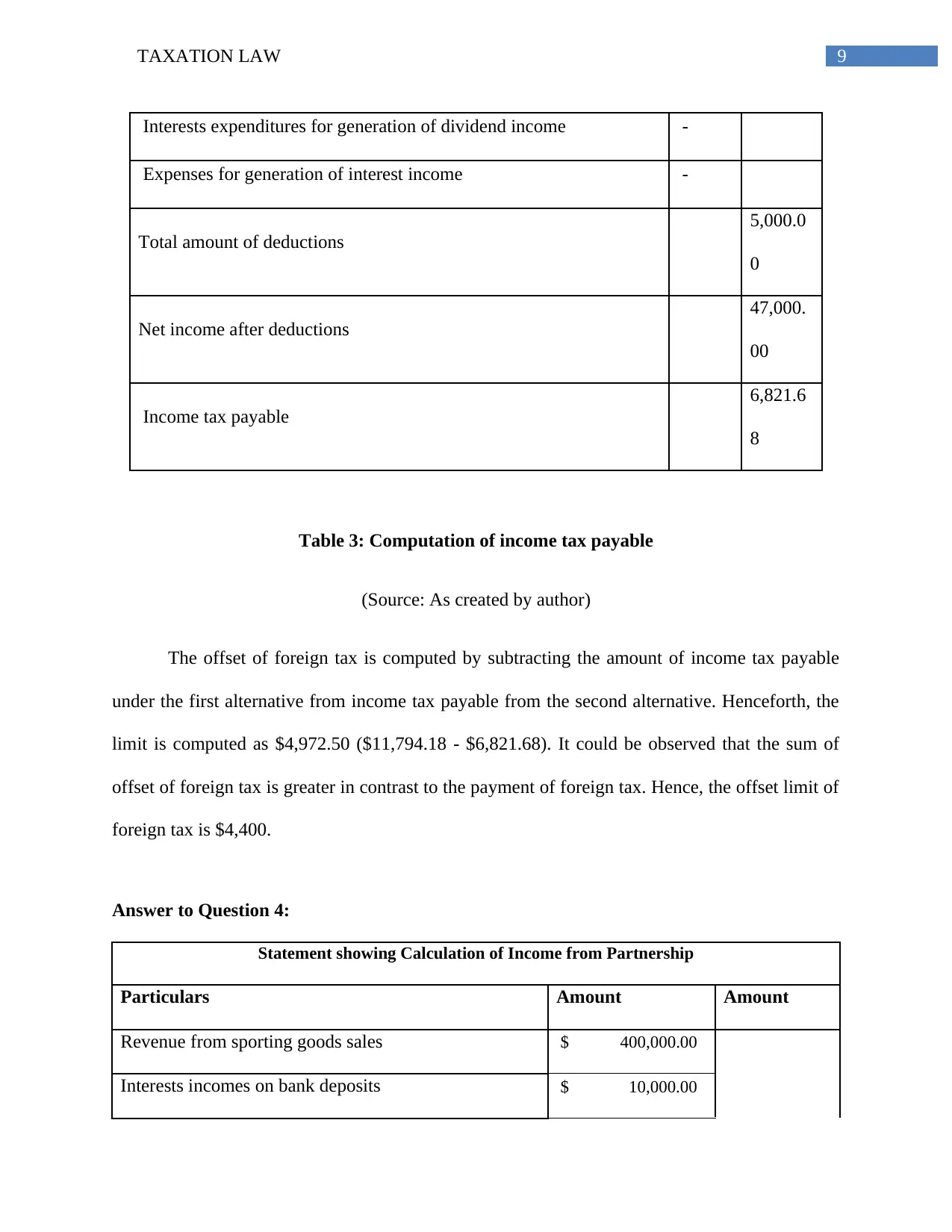

Assessable income of Angelo inclusive of foreign incomes

Details ($) ($)

Gross total income without any deductions

52,000.

00

Available deductions:

Medical expenditures

5,000.

00

Expenses for deriving employment expenses disallowed for

deduction

-

Expenses incurred in UK for generating Rental income -

9TAXATION LAW

Interests expenditures for generation of dividend income -

Expenses for generation of interest income -

Total amount of deductions

5,000.0

0

Net income after deductions

47,000.

00

Income tax payable

6,821.6

8

Table 3: Computation of income tax payable

(Source: As created by author)

The offset of foreign tax is computed by subtracting the amount of income tax payable

under the first alternative from income tax payable from the second alternative. Henceforth, the

limit is computed as $4,972.50 ($11,794.18 - $6,821.68). It could be observed that the sum of

offset of foreign tax is greater in contrast to the payment of foreign tax. Hence, the offset limit of

foreign tax is $4,400.

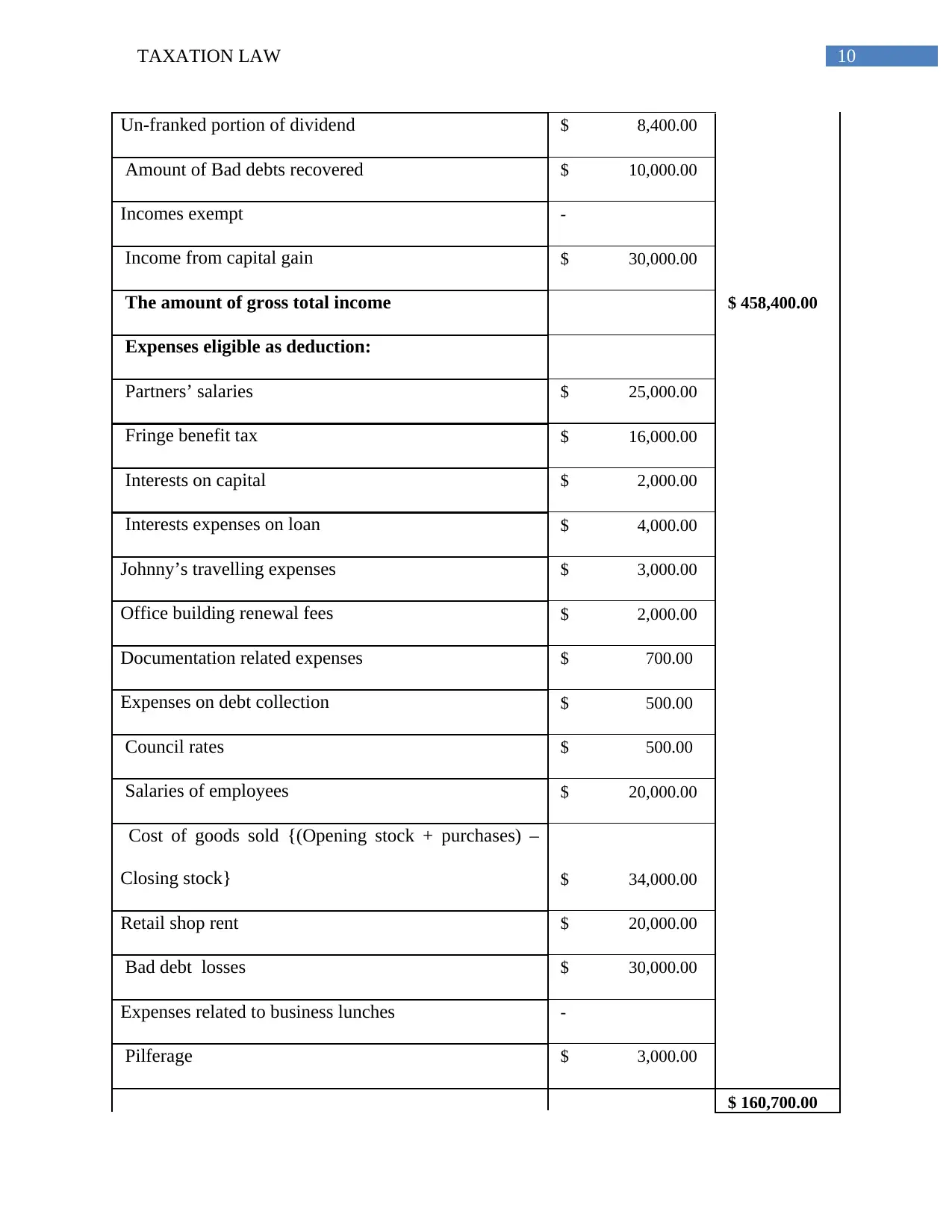

Answer to Question 4:

Statement showing Calculation of Income from Partnership

Particulars Amount Amount

Revenue from sporting goods sales $ 400,000.00

Interests incomes on bank deposits $ 10,000.00

Interests expenditures for generation of dividend income -

Expenses for generation of interest income -

Total amount of deductions

5,000.0

0

Net income after deductions

47,000.

00

Income tax payable

6,821.6

8

Table 3: Computation of income tax payable

(Source: As created by author)

The offset of foreign tax is computed by subtracting the amount of income tax payable

under the first alternative from income tax payable from the second alternative. Henceforth, the

limit is computed as $4,972.50 ($11,794.18 - $6,821.68). It could be observed that the sum of

offset of foreign tax is greater in contrast to the payment of foreign tax. Hence, the offset limit of

foreign tax is $4,400.

Answer to Question 4:

Statement showing Calculation of Income from Partnership

Particulars Amount Amount

Revenue from sporting goods sales $ 400,000.00

Interests incomes on bank deposits $ 10,000.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

Un-franked portion of dividend $ 8,400.00

Amount of Bad debts recovered $ 10,000.00

Incomes exempt -

Income from capital gain $ 30,000.00

The amount of gross total income $ 458,400.00

Expenses eligible as deduction:

Partners’ salaries $ 25,000.00

Fringe benefit tax $ 16,000.00

Interests on capital $ 2,000.00

Interests expenses on loan $ 4,000.00

Johnny’s travelling expenses $ 3,000.00

Office building renewal fees $ 2,000.00

Documentation related expenses $ 700.00

Expenses on debt collection $ 500.00

Council rates $ 500.00

Salaries of employees $ 20,000.00

Cost of goods sold {(Opening stock + purchases) –

Closing stock} $ 34,000.00

Retail shop rent $ 20,000.00

Bad debt losses $ 30,000.00

Expenses related to business lunches -

Pilferage $ 3,000.00

$ 160,700.00

Un-franked portion of dividend $ 8,400.00

Amount of Bad debts recovered $ 10,000.00

Incomes exempt -

Income from capital gain $ 30,000.00

The amount of gross total income $ 458,400.00

Expenses eligible as deduction:

Partners’ salaries $ 25,000.00

Fringe benefit tax $ 16,000.00

Interests on capital $ 2,000.00

Interests expenses on loan $ 4,000.00

Johnny’s travelling expenses $ 3,000.00

Office building renewal fees $ 2,000.00

Documentation related expenses $ 700.00

Expenses on debt collection $ 500.00

Council rates $ 500.00

Salaries of employees $ 20,000.00

Cost of goods sold {(Opening stock + purchases) –

Closing stock} $ 34,000.00

Retail shop rent $ 20,000.00

Bad debt losses $ 30,000.00

Expenses related to business lunches -

Pilferage $ 3,000.00

$ 160,700.00

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.