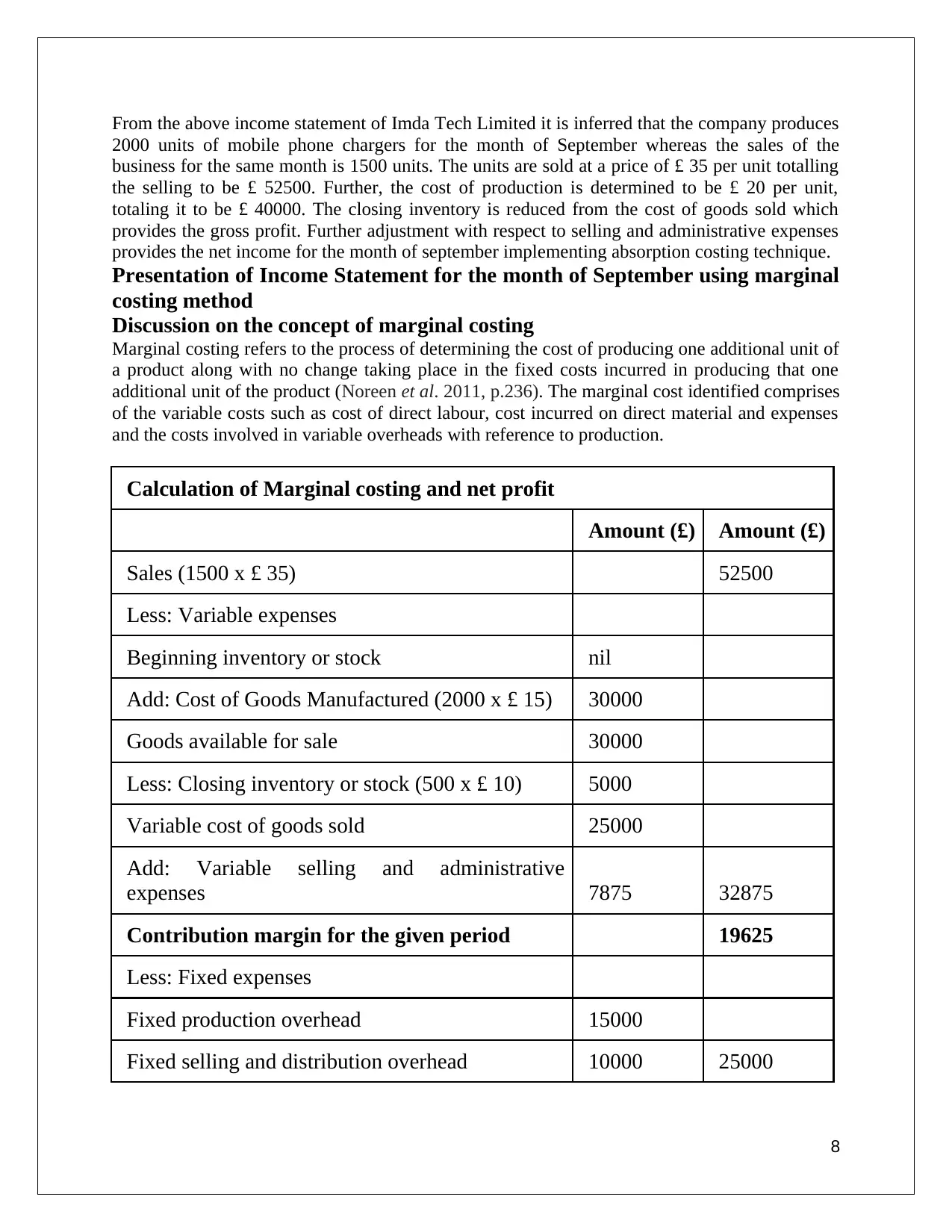

Management Accounting Report: Costing and Budgeting Analysis

VerifiedAdded on 2020/01/28

|15

|5268

|312

Report

AI Summary

This report provides a detailed analysis of management accounting principles, focusing on IMDA Tech (UK) Limited. It begins with an introduction to management accounting, contrasting it with financial accounting and highlighting its role in decision-making, planning, and performance measurement. The report then examines the functions of management accounting, including costing methods (absorption costing), budgeting techniques, and the use of the balanced scorecard to improve financial conditions. Task 1 defines management accounting and its differences from financial accounting, outlining its role in organizational decision-making. Task 2 presents an income statement using absorption costing. Task 3 explores different budgeting types, their advantages, disadvantages, and the strategies for price setting. Finally, Task 4 investigates the use of the balanced scorecard to address financial problems and improve performance. The report concludes with a summary of the findings and provides a reference list.

Assignment

Management Accounting

Student name:

Student ID:

College Name:

College ID:

1

Management Accounting

Student name:

Student ID:

College Name:

College ID:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of content

Introduction......................................................................................................................................3

Overview of the company................................................................................................................3

Task 1: a) Functions of management accounting (P1)....................................................................3

i) Definition of management accounting and the differences between the management accounting

and financial accounting..................................................................................................................3

ii) Role of management accounting to create some effective decisions in the organisation...........5

b) Types of management accounting system and the process that should be followed by the

organisations to improve their financial report (P2)........................................................................6

Task 2...............................................................................................................................................7

Presentation of Income Statement for the month of September using absorption costing..............7

Task 3: Preparation of different types of budgets [P4]....................................................................9

i) The advantages and disadvantages of different types of budgets................................................9

ii) The process that should be followed by the Company to prepare such budgets.......................11

iii) The strategies that should be adopt by the Company to set the price......................................11

Task 4: Use of balance scorecard to improve the financial condition of the organization [P5]....12

I) Use of balance scorecard to solve the financial problems.........................................................12

II) Implementation of Balanced scorecard can deliver a range of financial and non financial

performance measures...................................................................................................................12

Conclusion.....................................................................................................................................14

Reference list:................................................................................................................................15

2

Introduction......................................................................................................................................3

Overview of the company................................................................................................................3

Task 1: a) Functions of management accounting (P1)....................................................................3

i) Definition of management accounting and the differences between the management accounting

and financial accounting..................................................................................................................3

ii) Role of management accounting to create some effective decisions in the organisation...........5

b) Types of management accounting system and the process that should be followed by the

organisations to improve their financial report (P2)........................................................................6

Task 2...............................................................................................................................................7

Presentation of Income Statement for the month of September using absorption costing..............7

Task 3: Preparation of different types of budgets [P4]....................................................................9

i) The advantages and disadvantages of different types of budgets................................................9

ii) The process that should be followed by the Company to prepare such budgets.......................11

iii) The strategies that should be adopt by the Company to set the price......................................11

Task 4: Use of balance scorecard to improve the financial condition of the organization [P5]....12

I) Use of balance scorecard to solve the financial problems.........................................................12

II) Implementation of Balanced scorecard can deliver a range of financial and non financial

performance measures...................................................................................................................12

Conclusion.....................................................................................................................................14

Reference list:................................................................................................................................15

2

Introduction

Business organisations do their business activities both in the internal and external environment.

Therefore, organisations have to prepare some strategies to achieve the objectives in both

internal and external environment. Basically, Organisations do their business activities to achieve

two major objectives the first one is profit maximization and the second one is wealth

maximization. Organisations have to conduct a good accounting system in the organisation

culture to achieve the profit maximization objective because financial accounting system has a

direct relationship with the profit of the organizations (Renz, 2016, p.209). As a good accounting

system keep all the records of the cost of activities of the organisation therefore,organisations

have to be depended on the accounting system to get the relevant information about the

expenditure of the organisation. The information provided by the accounting system also help the

organisation to prepare some strategies to reduces the cost of business activities and increase the

generation revenues from the activities. In this way accounting system help the organisations to

increase the differences between the revenue and expenditure to maximize the profit. The main

focus of the following thesis is to interpret the importance of the management accounting system

in the organisations which is a vital part of accounting system.

Overview of the company

The following study also focus on the accounting system of IMDA tech (UK) limited which is a

well known company for manufacturing special chargers of mobiles, telephones and other carry-

on gadgets. Company successfully generates their profit for the last few years but in the annual

meeting some of the department managers had some complaints about the accuracy of the

financial information system of the company. The managers cannot get the detail information

about the financial performance of the company. Company tries to include the management

accounting system in their accounting system to increase the accuracy of the financial

information system in the organisation.

Task 1: a) Functions of management accounting (P1)

i) Definition of management accounting and the differences between the

management accounting and financial accounting

Management accounting system help the organisations by providing some devices that can be

used to take some effective decisions, planning for the business activities, measuring the

performance of different business activities and management, preparing some financial report to

control the cost of the business activities, formulation and implementation of some strategies to

increase the efficiency of the business activities (Otley and Emmanuel, 2013, p.304). As

3

Business organisations do their business activities both in the internal and external environment.

Therefore, organisations have to prepare some strategies to achieve the objectives in both

internal and external environment. Basically, Organisations do their business activities to achieve

two major objectives the first one is profit maximization and the second one is wealth

maximization. Organisations have to conduct a good accounting system in the organisation

culture to achieve the profit maximization objective because financial accounting system has a

direct relationship with the profit of the organizations (Renz, 2016, p.209). As a good accounting

system keep all the records of the cost of activities of the organisation therefore,organisations

have to be depended on the accounting system to get the relevant information about the

expenditure of the organisation. The information provided by the accounting system also help the

organisation to prepare some strategies to reduces the cost of business activities and increase the

generation revenues from the activities. In this way accounting system help the organisations to

increase the differences between the revenue and expenditure to maximize the profit. The main

focus of the following thesis is to interpret the importance of the management accounting system

in the organisations which is a vital part of accounting system.

Overview of the company

The following study also focus on the accounting system of IMDA tech (UK) limited which is a

well known company for manufacturing special chargers of mobiles, telephones and other carry-

on gadgets. Company successfully generates their profit for the last few years but in the annual

meeting some of the department managers had some complaints about the accuracy of the

financial information system of the company. The managers cannot get the detail information

about the financial performance of the company. Company tries to include the management

accounting system in their accounting system to increase the accuracy of the financial

information system in the organisation.

Task 1: a) Functions of management accounting (P1)

i) Definition of management accounting and the differences between the

management accounting and financial accounting

Management accounting system help the organisations by providing some devices that can be

used to take some effective decisions, planning for the business activities, measuring the

performance of different business activities and management, preparing some financial report to

control the cost of the business activities, formulation and implementation of some strategies to

increase the efficiency of the business activities (Otley and Emmanuel, 2013, p.304). As

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

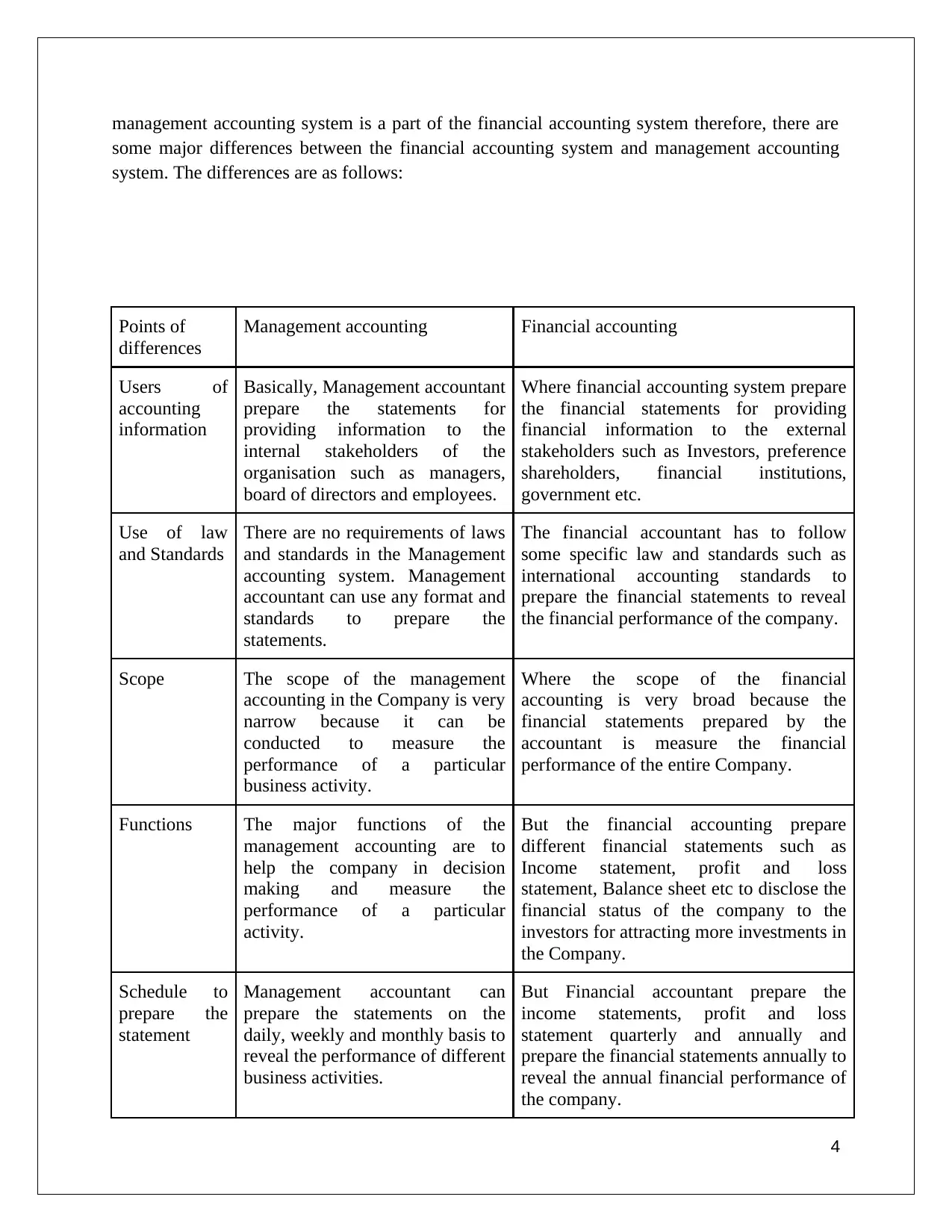

management accounting system is a part of the financial accounting system therefore, there are

some major differences between the financial accounting system and management accounting

system. The differences are as follows:

Points of

differences

Management accounting Financial accounting

Users of

accounting

information

Basically, Management accountant

prepare the statements for

providing information to the

internal stakeholders of the

organisation such as managers,

board of directors and employees.

Where financial accounting system prepare

the financial statements for providing

financial information to the external

stakeholders such as Investors, preference

shareholders, financial institutions,

government etc.

Use of law

and Standards

There are no requirements of laws

and standards in the Management

accounting system. Management

accountant can use any format and

standards to prepare the

statements.

The financial accountant has to follow

some specific law and standards such as

international accounting standards to

prepare the financial statements to reveal

the financial performance of the company.

Scope The scope of the management

accounting in the Company is very

narrow because it can be

conducted to measure the

performance of a particular

business activity.

Where the scope of the financial

accounting is very broad because the

financial statements prepared by the

accountant is measure the financial

performance of the entire Company.

Functions The major functions of the

management accounting are to

help the company in decision

making and measure the

performance of a particular

activity.

But the financial accounting prepare

different financial statements such as

Income statement, profit and loss

statement, Balance sheet etc to disclose the

financial status of the company to the

investors for attracting more investments in

the Company.

Schedule to

prepare the

statement

Management accountant can

prepare the statements on the

daily, weekly and monthly basis to

reveal the performance of different

business activities.

But Financial accountant prepare the

income statements, profit and loss

statement quarterly and annually and

prepare the financial statements annually to

reveal the annual financial performance of

the company.

4

some major differences between the financial accounting system and management accounting

system. The differences are as follows:

Points of

differences

Management accounting Financial accounting

Users of

accounting

information

Basically, Management accountant

prepare the statements for

providing information to the

internal stakeholders of the

organisation such as managers,

board of directors and employees.

Where financial accounting system prepare

the financial statements for providing

financial information to the external

stakeholders such as Investors, preference

shareholders, financial institutions,

government etc.

Use of law

and Standards

There are no requirements of laws

and standards in the Management

accounting system. Management

accountant can use any format and

standards to prepare the

statements.

The financial accountant has to follow

some specific law and standards such as

international accounting standards to

prepare the financial statements to reveal

the financial performance of the company.

Scope The scope of the management

accounting in the Company is very

narrow because it can be

conducted to measure the

performance of a particular

business activity.

Where the scope of the financial

accounting is very broad because the

financial statements prepared by the

accountant is measure the financial

performance of the entire Company.

Functions The major functions of the

management accounting are to

help the company in decision

making and measure the

performance of a particular

activity.

But the financial accounting prepare

different financial statements such as

Income statement, profit and loss

statement, Balance sheet etc to disclose the

financial status of the company to the

investors for attracting more investments in

the Company.

Schedule to

prepare the

statement

Management accountant can

prepare the statements on the

daily, weekly and monthly basis to

reveal the performance of different

business activities.

But Financial accountant prepare the

income statements, profit and loss

statement quarterly and annually and

prepare the financial statements annually to

reveal the annual financial performance of

the company.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

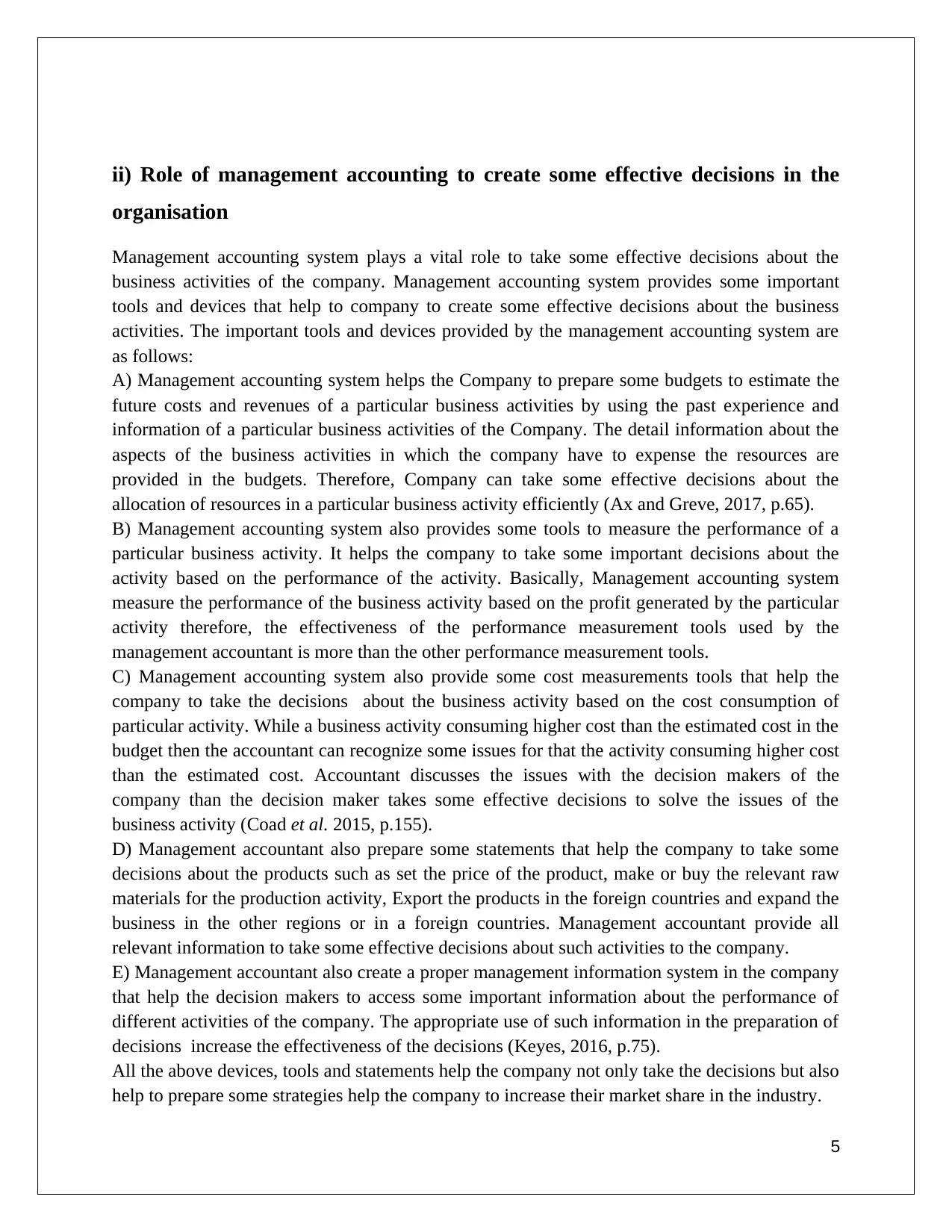

ii) Role of management accounting to create some effective decisions in the

organisation

Management accounting system plays a vital role to take some effective decisions about the

business activities of the company. Management accounting system provides some important

tools and devices that help to company to create some effective decisions about the business

activities. The important tools and devices provided by the management accounting system are

as follows:

A) Management accounting system helps the Company to prepare some budgets to estimate the

future costs and revenues of a particular business activities by using the past experience and

information of a particular business activities of the Company. The detail information about the

aspects of the business activities in which the company have to expense the resources are

provided in the budgets. Therefore, Company can take some effective decisions about the

allocation of resources in a particular business activity efficiently (Ax and Greve, 2017, p.65).

B) Management accounting system also provides some tools to measure the performance of a

particular business activity. It helps the company to take some important decisions about the

activity based on the performance of the activity. Basically, Management accounting system

measure the performance of the business activity based on the profit generated by the particular

activity therefore, the effectiveness of the performance measurement tools used by the

management accountant is more than the other performance measurement tools.

C) Management accounting system also provide some cost measurements tools that help the

company to take the decisions about the business activity based on the cost consumption of

particular activity. While a business activity consuming higher cost than the estimated cost in the

budget then the accountant can recognize some issues for that the activity consuming higher cost

than the estimated cost. Accountant discusses the issues with the decision makers of the

company than the decision maker takes some effective decisions to solve the issues of the

business activity (Coad et al. 2015, p.155).

D) Management accountant also prepare some statements that help the company to take some

decisions about the products such as set the price of the product, make or buy the relevant raw

materials for the production activity, Export the products in the foreign countries and expand the

business in the other regions or in a foreign countries. Management accountant provide all

relevant information to take some effective decisions about such activities to the company.

E) Management accountant also create a proper management information system in the company

that help the decision makers to access some important information about the performance of

different activities of the company. The appropriate use of such information in the preparation of

decisions increase the effectiveness of the decisions (Keyes, 2016, p.75).

All the above devices, tools and statements help the company not only take the decisions but also

help to prepare some strategies help the company to increase their market share in the industry.

5

organisation

Management accounting system plays a vital role to take some effective decisions about the

business activities of the company. Management accounting system provides some important

tools and devices that help to company to create some effective decisions about the business

activities. The important tools and devices provided by the management accounting system are

as follows:

A) Management accounting system helps the Company to prepare some budgets to estimate the

future costs and revenues of a particular business activities by using the past experience and

information of a particular business activities of the Company. The detail information about the

aspects of the business activities in which the company have to expense the resources are

provided in the budgets. Therefore, Company can take some effective decisions about the

allocation of resources in a particular business activity efficiently (Ax and Greve, 2017, p.65).

B) Management accounting system also provides some tools to measure the performance of a

particular business activity. It helps the company to take some important decisions about the

activity based on the performance of the activity. Basically, Management accounting system

measure the performance of the business activity based on the profit generated by the particular

activity therefore, the effectiveness of the performance measurement tools used by the

management accountant is more than the other performance measurement tools.

C) Management accounting system also provide some cost measurements tools that help the

company to take the decisions about the business activity based on the cost consumption of

particular activity. While a business activity consuming higher cost than the estimated cost in the

budget then the accountant can recognize some issues for that the activity consuming higher cost

than the estimated cost. Accountant discusses the issues with the decision makers of the

company than the decision maker takes some effective decisions to solve the issues of the

business activity (Coad et al. 2015, p.155).

D) Management accountant also prepare some statements that help the company to take some

decisions about the products such as set the price of the product, make or buy the relevant raw

materials for the production activity, Export the products in the foreign countries and expand the

business in the other regions or in a foreign countries. Management accountant provide all

relevant information to take some effective decisions about such activities to the company.

E) Management accountant also create a proper management information system in the company

that help the decision makers to access some important information about the performance of

different activities of the company. The appropriate use of such information in the preparation of

decisions increase the effectiveness of the decisions (Keyes, 2016, p.75).

All the above devices, tools and statements help the company not only take the decisions but also

help to prepare some strategies help the company to increase their market share in the industry.

5

b) Types of management accounting system and the process that should be

followed by the organisations to improve their financial report (P2)

There are different types of management accounting system that help the company to take the

decisions and measure the performance of the different business activities in the organisation.

The important types of about the management accounting system are as follows:

i) Cost accounting system

Cost accounting system provide some important information to the company about the cost of

production, cost of inventory and provide some effective measures to the company to control the

cost of the production. The important information provided by the cost accounting system not

only control the cost but also help the company to estimate the cost of production which is an

important operation of the company to increase the profit (Shields, 2015, p.130). Cost accounting

system also uses some devices to estimate the cost of production. The devices are as follows:

Activity based costing: In activity based costing system the rate of cost are applied in the

activity according to the usages of such activity.

Process costing: In this system of costing the cost of manufacturing of the products are

accumulated by the process involved in the production activity.

Traditional costing system: Traditional costing system uses a uniform rate for all departments

of a production activity of the company.

ii) System of inventory management: Inventory management system is a computer based

information system that keeps the record of the level of inventory, orders, sales and deliveries.

This system provide all relevant documents such as bill of materials, order invoices and other

production related documents that help the company to take some significant decisions about the

level of raw materials, closing stock of the finished products in the production process.

iii) Job costing system: Job costing system is a process by which company can accumulate the

relevant information about the costs associated with the production activity. Job costing system

generally collects the information about the direct materials, direct wages and overhead to

calculate the cost of production (Manyaeva et al. 2016, p.265).

iv) System of price optimization: Price optimization system help the company to set the price

according to the not only respond of the customers. Management accountant try to set ideal price

that meet the customer's utility maximization objectives and company’s profit maximization

objectives.

The IMDA ltd can adopt all the above system in the organisation to control the cost of the

activities and increase the generation of revenues in the company.

6

followed by the organisations to improve their financial report (P2)

There are different types of management accounting system that help the company to take the

decisions and measure the performance of the different business activities in the organisation.

The important types of about the management accounting system are as follows:

i) Cost accounting system

Cost accounting system provide some important information to the company about the cost of

production, cost of inventory and provide some effective measures to the company to control the

cost of the production. The important information provided by the cost accounting system not

only control the cost but also help the company to estimate the cost of production which is an

important operation of the company to increase the profit (Shields, 2015, p.130). Cost accounting

system also uses some devices to estimate the cost of production. The devices are as follows:

Activity based costing: In activity based costing system the rate of cost are applied in the

activity according to the usages of such activity.

Process costing: In this system of costing the cost of manufacturing of the products are

accumulated by the process involved in the production activity.

Traditional costing system: Traditional costing system uses a uniform rate for all departments

of a production activity of the company.

ii) System of inventory management: Inventory management system is a computer based

information system that keeps the record of the level of inventory, orders, sales and deliveries.

This system provide all relevant documents such as bill of materials, order invoices and other

production related documents that help the company to take some significant decisions about the

level of raw materials, closing stock of the finished products in the production process.

iii) Job costing system: Job costing system is a process by which company can accumulate the

relevant information about the costs associated with the production activity. Job costing system

generally collects the information about the direct materials, direct wages and overhead to

calculate the cost of production (Manyaeva et al. 2016, p.265).

iv) System of price optimization: Price optimization system help the company to set the price

according to the not only respond of the customers. Management accountant try to set ideal price

that meet the customer's utility maximization objectives and company’s profit maximization

objectives.

The IMDA ltd can adopt all the above system in the organisation to control the cost of the

activities and increase the generation of revenues in the company.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

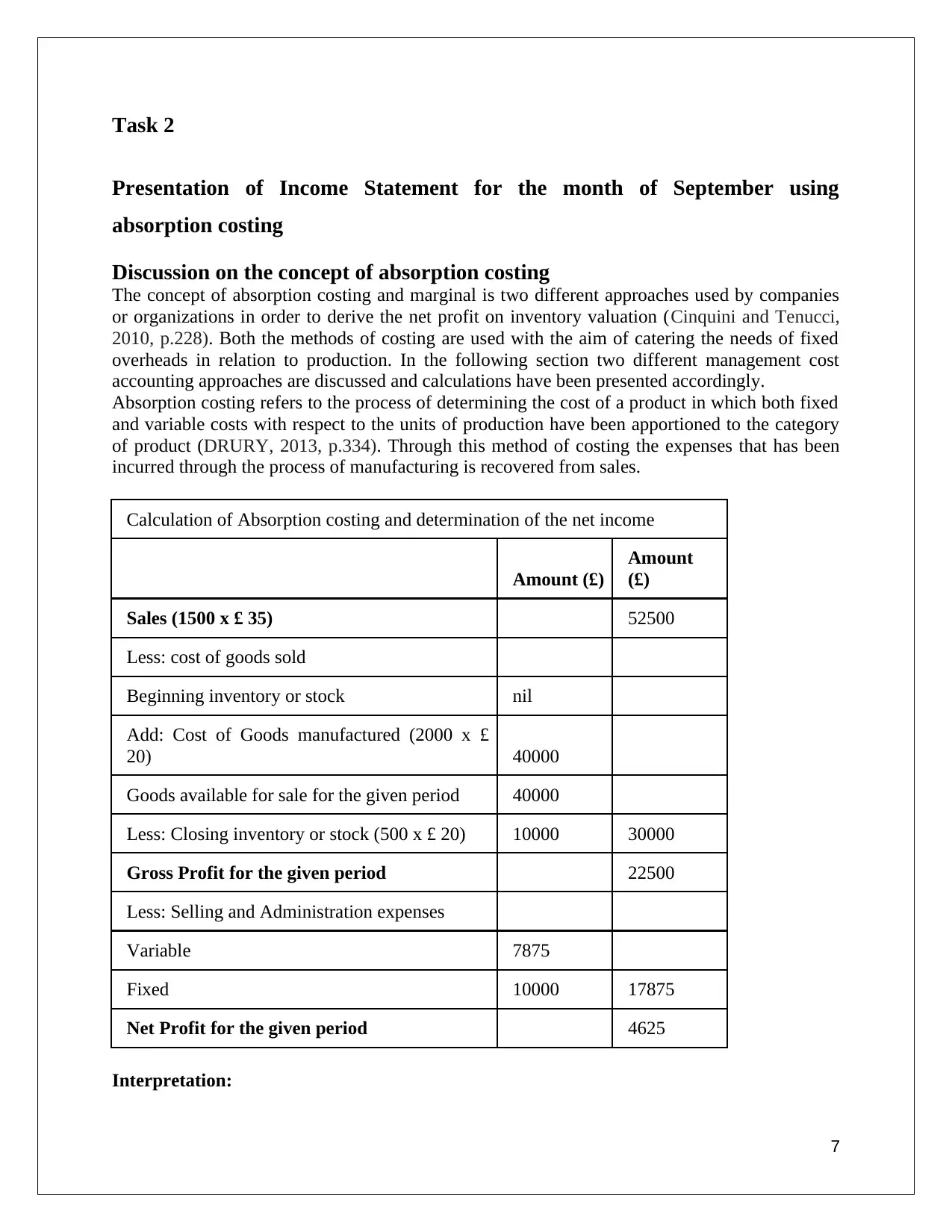

Task 2

Presentation of Income Statement for the month of September using

absorption costing

Discussion on the concept of absorption costing

The concept of absorption costing and marginal is two different approaches used by companies

or organizations in order to derive the net profit on inventory valuation (Cinquini and Tenucci,

2010, p.228). Both the methods of costing are used with the aim of catering the needs of fixed

overheads in relation to production. In the following section two different management cost

accounting approaches are discussed and calculations have been presented accordingly.

Absorption costing refers to the process of determining the cost of a product in which both fixed

and variable costs with respect to the units of production have been apportioned to the category

of product (DRURY, 2013, p.334). Through this method of costing the expenses that has been

incurred through the process of manufacturing is recovered from sales.

Calculation of Absorption costing and determination of the net income

Amount (£)

Amount

(£)

Sales (1500 x £ 35) 52500

Less: cost of goods sold

Beginning inventory or stock nil

Add: Cost of Goods manufactured (2000 x £

20) 40000

Goods available for sale for the given period 40000

Less: Closing inventory or stock (500 x £ 20) 10000 30000

Gross Profit for the given period 22500

Less: Selling and Administration expenses

Variable 7875

Fixed 10000 17875

Net Profit for the given period 4625

Interpretation:

7

Presentation of Income Statement for the month of September using

absorption costing

Discussion on the concept of absorption costing

The concept of absorption costing and marginal is two different approaches used by companies

or organizations in order to derive the net profit on inventory valuation (Cinquini and Tenucci,

2010, p.228). Both the methods of costing are used with the aim of catering the needs of fixed

overheads in relation to production. In the following section two different management cost

accounting approaches are discussed and calculations have been presented accordingly.

Absorption costing refers to the process of determining the cost of a product in which both fixed

and variable costs with respect to the units of production have been apportioned to the category

of product (DRURY, 2013, p.334). Through this method of costing the expenses that has been

incurred through the process of manufacturing is recovered from sales.

Calculation of Absorption costing and determination of the net income

Amount (£)

Amount

(£)

Sales (1500 x £ 35) 52500

Less: cost of goods sold

Beginning inventory or stock nil

Add: Cost of Goods manufactured (2000 x £

20) 40000

Goods available for sale for the given period 40000

Less: Closing inventory or stock (500 x £ 20) 10000 30000

Gross Profit for the given period 22500

Less: Selling and Administration expenses

Variable 7875

Fixed 10000 17875

Net Profit for the given period 4625

Interpretation:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above income statement of Imda Tech Limited it is inferred that the company produces

2000 units of mobile phone chargers for the month of September whereas the sales of the

business for the same month is 1500 units. The units are sold at a price of £ 35 per unit totalling

the selling to be £ 52500. Further, the cost of production is determined to be £ 20 per unit,

totaling it to be £ 40000. The closing inventory is reduced from the cost of goods sold which

provides the gross profit. Further adjustment with respect to selling and administrative expenses

provides the net income for the month of september implementing absorption costing technique.

Presentation of Income Statement for the month of September using marginal

costing method

Discussion on the concept of marginal costing

Marginal costing refers to the process of determining the cost of producing one additional unit of

a product along with no change taking place in the fixed costs incurred in producing that one

additional unit of the product (Noreen et al. 2011, p.236). The marginal cost identified comprises

of the variable costs such as cost of direct labour, cost incurred on direct material and expenses

and the costs involved in variable overheads with reference to production.

Calculation of Marginal costing and net profit

Amount (£) Amount (£)

Sales (1500 x £ 35) 52500

Less: Variable expenses

Beginning inventory or stock nil

Add: Cost of Goods Manufactured (2000 x £ 15) 30000

Goods available for sale 30000

Less: Closing inventory or stock (500 x £ 10) 5000

Variable cost of goods sold 25000

Add: Variable selling and administrative

expenses 7875 32875

Contribution margin for the given period 19625

Less: Fixed expenses

Fixed production overhead 15000

Fixed selling and distribution overhead 10000 25000

8

2000 units of mobile phone chargers for the month of September whereas the sales of the

business for the same month is 1500 units. The units are sold at a price of £ 35 per unit totalling

the selling to be £ 52500. Further, the cost of production is determined to be £ 20 per unit,

totaling it to be £ 40000. The closing inventory is reduced from the cost of goods sold which

provides the gross profit. Further adjustment with respect to selling and administrative expenses

provides the net income for the month of september implementing absorption costing technique.

Presentation of Income Statement for the month of September using marginal

costing method

Discussion on the concept of marginal costing

Marginal costing refers to the process of determining the cost of producing one additional unit of

a product along with no change taking place in the fixed costs incurred in producing that one

additional unit of the product (Noreen et al. 2011, p.236). The marginal cost identified comprises

of the variable costs such as cost of direct labour, cost incurred on direct material and expenses

and the costs involved in variable overheads with reference to production.

Calculation of Marginal costing and net profit

Amount (£) Amount (£)

Sales (1500 x £ 35) 52500

Less: Variable expenses

Beginning inventory or stock nil

Add: Cost of Goods Manufactured (2000 x £ 15) 30000

Goods available for sale 30000

Less: Closing inventory or stock (500 x £ 10) 5000

Variable cost of goods sold 25000

Add: Variable selling and administrative

expenses 7875 32875

Contribution margin for the given period 19625

Less: Fixed expenses

Fixed production overhead 15000

Fixed selling and distribution overhead 10000 25000

8

Net Profit/loss for the given period -5375

Interpretation:

From the above chart it is inferred that the organization appears to incur marginal loss in the

month September. Since fixed costs are considered to be period costs under the concept of

marginal costing therefore it is completely written off for the period and not carried forward.

Task 3: Preparation of different types of budgets [P4]

i) The advantages and disadvantages of different types of budgets

The company can use different types of budgets to estimate the cost of different activities and the

revenue generation from the activities. Budgets help the company to allocate the resources in an

efficient manner in the business activity. The proper allocation of resources helps the company to

minimize the use of the resources and maximize the assets and revenues of the company. IMDA

ltd can prepare the following budgets in the company:

Functional budget: Company prepares the functional budgets to estimate the future cost,

production and sales. Company prepare different types of the functional budgets such as sales

budget to estimate the sales of the company, production budget to estimate the numbers of

products for which the company can generate maximum revenues by using the minimum

resources (Li et al. 2013, p.454). Material budget is to increase the accuracy in the use of raw

materials and minimize the wastage of raw materials in the production process. Labor budget is

to use labor power efficiently and accurately. Apart from all budgets company also prepare some

other functional budgets to estimate the use of resources in different departments of the company

such as administrative budget, selling and distribution budget and cash budget. Company

sometime faces some problem with the implementation of such budgets in the activity. The use

of impractical estimation in the preparation of the budget always create problem for the

employees because higher expectations from the employees always create some additional

pressure for this reason the employees cannot perform their best and the quality of the product

also fall (Hill et al. 2017, p.235).

Master budget: Master budget is an aggregate of all budgets which are prepared in the

company. This budget helps the company to prepare a complete picture of the future financial

status of the company. Master budget is the combinations of all budgets such as sales, operating

profit and expenses, assets and income of the company. The advantages of this budget are to

provide clear information about the mission and vision of the company to the investors for

attracting more investments in the company. However, sometime inaccurate estimation in the

budget cannot provide expected earnings to the investors that decrease the goodwill of the

company in the market.

Operating budget: Operating budget help the company to forecast the future income and

expenditure of the company. Companies use the past experience of production, sales, labor cost

9

Interpretation:

From the above chart it is inferred that the organization appears to incur marginal loss in the

month September. Since fixed costs are considered to be period costs under the concept of

marginal costing therefore it is completely written off for the period and not carried forward.

Task 3: Preparation of different types of budgets [P4]

i) The advantages and disadvantages of different types of budgets

The company can use different types of budgets to estimate the cost of different activities and the

revenue generation from the activities. Budgets help the company to allocate the resources in an

efficient manner in the business activity. The proper allocation of resources helps the company to

minimize the use of the resources and maximize the assets and revenues of the company. IMDA

ltd can prepare the following budgets in the company:

Functional budget: Company prepares the functional budgets to estimate the future cost,

production and sales. Company prepare different types of the functional budgets such as sales

budget to estimate the sales of the company, production budget to estimate the numbers of

products for which the company can generate maximum revenues by using the minimum

resources (Li et al. 2013, p.454). Material budget is to increase the accuracy in the use of raw

materials and minimize the wastage of raw materials in the production process. Labor budget is

to use labor power efficiently and accurately. Apart from all budgets company also prepare some

other functional budgets to estimate the use of resources in different departments of the company

such as administrative budget, selling and distribution budget and cash budget. Company

sometime faces some problem with the implementation of such budgets in the activity. The use

of impractical estimation in the preparation of the budget always create problem for the

employees because higher expectations from the employees always create some additional

pressure for this reason the employees cannot perform their best and the quality of the product

also fall (Hill et al. 2017, p.235).

Master budget: Master budget is an aggregate of all budgets which are prepared in the

company. This budget helps the company to prepare a complete picture of the future financial

status of the company. Master budget is the combinations of all budgets such as sales, operating

profit and expenses, assets and income of the company. The advantages of this budget are to

provide clear information about the mission and vision of the company to the investors for

attracting more investments in the company. However, sometime inaccurate estimation in the

budget cannot provide expected earnings to the investors that decrease the goodwill of the

company in the market.

Operating budget: Operating budget help the company to forecast the future income and

expenditure of the company. Companies use the past experience of production, sales, labor cost

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and other expenses to the operating budgets. This budget can be prepared weekly, monthly,

quarterly or annually in the company. The disadvantages of this budget are ignorance of market

condition in the preparation of such budget (Oriekhova, 2016, p.45).

Cash flow budget: The function of this budget is to provide a clear picture of generation of cash

in the company and outflow of cash from the company. This budget basically focuses on the

sources from which the company can generate cash in future and the aspects in which company

can expense their cash in future. Company can use the account receivables and account payables

as factors to prepare the budgets.

Apart for all the advantages of the budgets the company sometime faces some serious problems

with the budgets:

A) Inaccuracy of the budget always creates some problems for the company. Basically, the

budgets are prepared based on some assumptions which have no relation with the practical

condition of the company. The ignorance of changes in the business environment increase the

accuracy of the budget. Company never achieves their expected earnings with an inaccurate

budget (Ambrosini et al. 2015, P.372).

B) The budgets are prepared by the management of the company therefore, they some ignore the

inclusion of market shift in the budget. However, this is advisable to the company to run the

business according to market to achieve success in long run.

C) The preparation of the budgets always consume a lot of time of the company. The company

can invest the time in the other activity to earn more profit.

D) While the company cannot achieve the result according to the budget then the company

blame the managers for such failure this incident demotivates the managers to provide their best

effort in the company.

ii) The process that should be followed by the Company to prepare such

budgets

Company can use some process to prepare the budget in an efficient manner. The inclusion of

the detriments in the budget increase the efficiency of the budget. The process are as follows:

A) Company has to prepare the budget based on the fiscal target and try to estimate the

expenditure which can comply with the targets.

B) Company also makes some expenditure strategies to prepare such budgets. The appropriate

inclusion of expenditure strategies helps the company to control the cost in the budget.

C) Company has to allocate the resources in the company according to the expenditure strategies

and fiscal target. The proper allocation of resources reduces the wastages of the resources and

increases the revenues of the company (Morden, 2016, p.255).

D) Management can also include some production process, plan and procedures to increase the

efficiency of the production process and performance of the employees.

E) Company also can increase the efficiency of the organisational structure and concentrate on

the achievement of long term objectives of the company while preparing the budget.

10

quarterly or annually in the company. The disadvantages of this budget are ignorance of market

condition in the preparation of such budget (Oriekhova, 2016, p.45).

Cash flow budget: The function of this budget is to provide a clear picture of generation of cash

in the company and outflow of cash from the company. This budget basically focuses on the

sources from which the company can generate cash in future and the aspects in which company

can expense their cash in future. Company can use the account receivables and account payables

as factors to prepare the budgets.

Apart for all the advantages of the budgets the company sometime faces some serious problems

with the budgets:

A) Inaccuracy of the budget always creates some problems for the company. Basically, the

budgets are prepared based on some assumptions which have no relation with the practical

condition of the company. The ignorance of changes in the business environment increase the

accuracy of the budget. Company never achieves their expected earnings with an inaccurate

budget (Ambrosini et al. 2015, P.372).

B) The budgets are prepared by the management of the company therefore, they some ignore the

inclusion of market shift in the budget. However, this is advisable to the company to run the

business according to market to achieve success in long run.

C) The preparation of the budgets always consume a lot of time of the company. The company

can invest the time in the other activity to earn more profit.

D) While the company cannot achieve the result according to the budget then the company

blame the managers for such failure this incident demotivates the managers to provide their best

effort in the company.

ii) The process that should be followed by the Company to prepare such

budgets

Company can use some process to prepare the budget in an efficient manner. The inclusion of

the detriments in the budget increase the efficiency of the budget. The process are as follows:

A) Company has to prepare the budget based on the fiscal target and try to estimate the

expenditure which can comply with the targets.

B) Company also makes some expenditure strategies to prepare such budgets. The appropriate

inclusion of expenditure strategies helps the company to control the cost in the budget.

C) Company has to allocate the resources in the company according to the expenditure strategies

and fiscal target. The proper allocation of resources reduces the wastages of the resources and

increases the revenues of the company (Morden, 2016, p.255).

D) Management can also include some production process, plan and procedures to increase the

efficiency of the production process and performance of the employees.

E) Company also can increase the efficiency of the organisational structure and concentrate on

the achievement of long term objectives of the company while preparing the budget.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

F) Company can share the information about the budget with the employees and try to get some

feedback from them to increase the accuracy of the budget. Company also can motivate the

employees to improve their performance by achieving the target set by the budget (Coe and

Letza, 2014, p. 226).

iii) The strategies that should be adopt by the Company to set the price

Company can use different pricing strategies to set the price of the product. However, the

appropriate pricing strategies for the company are as follows:

Price penetration: Company can set a lower price of their products from the other competitors

in the market to increase the awareness about their products among the customers. Price

penetration is also a part of the marketing strategies of the company. By applying this strategy

company tries to attract more customers to buy the product.

Economy pricing: Company tries to reduce the marketing and production of the products to set

a lower price of the products. As IMDA ltd is a well known company in the mobile accessories

industry in UK they can follow this strategy to increase the demand of the customers for the

products and increase the market share of the products in the industry (DRURY, 2013, p.52).

Psychology pricing: Company can use these techniques to encourage the customer emotionally

to buy the products at a price which was set by the company.

Premium pricing: In this technique company try to set a higher price of their product than the

products of their competitors. By using this technique company tries to prove the superiority of

their products from the products of the competitors.

Task 4: Use of balance scorecard to improve the financial condition of the

organization [P5]

I) Use of balance scorecard to solve the financial problems

IMDA ltd can use the balanced scorecard to solve financial problems. The following measures

provided by the balance scorecard help the company to solve the financial problems:

A) Balanced scorecard helps the company to take some strategic initiatives to solve the financial

problems.

B) Balanced scorecard also provides some creative and innovative ideas to the company to solve

the financial problem.

C) As balance scorecard is a performance measurement tool therefore, it can help the company to

determine the issues that create the financial problem in the company by measuring the financial

performance (Cooper et al. 2017, p.135).

D) Balance scorecard can provide a transparent and comprehensive picture of the financial

problems to the company by providing some relevant information about the problem.

11

feedback from them to increase the accuracy of the budget. Company also can motivate the

employees to improve their performance by achieving the target set by the budget (Coe and

Letza, 2014, p. 226).

iii) The strategies that should be adopt by the Company to set the price

Company can use different pricing strategies to set the price of the product. However, the

appropriate pricing strategies for the company are as follows:

Price penetration: Company can set a lower price of their products from the other competitors

in the market to increase the awareness about their products among the customers. Price

penetration is also a part of the marketing strategies of the company. By applying this strategy

company tries to attract more customers to buy the product.

Economy pricing: Company tries to reduce the marketing and production of the products to set

a lower price of the products. As IMDA ltd is a well known company in the mobile accessories

industry in UK they can follow this strategy to increase the demand of the customers for the

products and increase the market share of the products in the industry (DRURY, 2013, p.52).

Psychology pricing: Company can use these techniques to encourage the customer emotionally

to buy the products at a price which was set by the company.

Premium pricing: In this technique company try to set a higher price of their product than the

products of their competitors. By using this technique company tries to prove the superiority of

their products from the products of the competitors.

Task 4: Use of balance scorecard to improve the financial condition of the

organization [P5]

I) Use of balance scorecard to solve the financial problems

IMDA ltd can use the balanced scorecard to solve financial problems. The following measures

provided by the balance scorecard help the company to solve the financial problems:

A) Balanced scorecard helps the company to take some strategic initiatives to solve the financial

problems.

B) Balanced scorecard also provides some creative and innovative ideas to the company to solve

the financial problem.

C) As balance scorecard is a performance measurement tool therefore, it can help the company to

determine the issues that create the financial problem in the company by measuring the financial

performance (Cooper et al. 2017, p.135).

D) Balance scorecard can provide a transparent and comprehensive picture of the financial

problems to the company by providing some relevant information about the problem.

11

E) Balance scorecard also provide some relevant results quickly that help the company to solve

the problem quickly.

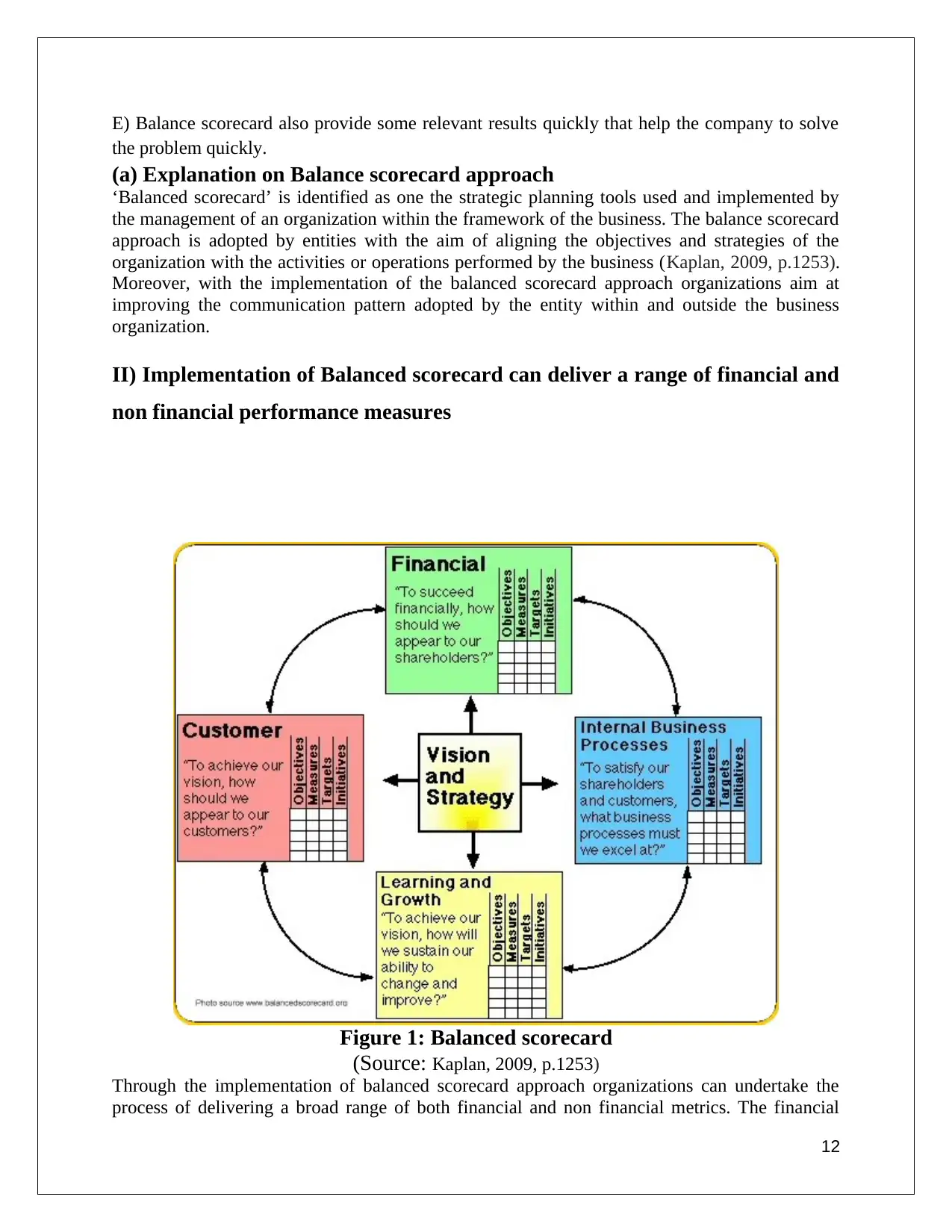

(a) Explanation on Balance scorecard approach

‘Balanced scorecard’ is identified as one the strategic planning tools used and implemented by

the management of an organization within the framework of the business. The balance scorecard

approach is adopted by entities with the aim of aligning the objectives and strategies of the

organization with the activities or operations performed by the business (Kaplan, 2009, p.1253).

Moreover, with the implementation of the balanced scorecard approach organizations aim at

improving the communication pattern adopted by the entity within and outside the business

organization.

II) Implementation of Balanced scorecard can deliver a range of financial and

non financial performance measures

Figure 1: Balanced scorecard

(Source: Kaplan, 2009, p.1253)

Through the implementation of balanced scorecard approach organizations can undertake the

process of delivering a broad range of both financial and non financial metrics. The financial

12

the problem quickly.

(a) Explanation on Balance scorecard approach

‘Balanced scorecard’ is identified as one the strategic planning tools used and implemented by

the management of an organization within the framework of the business. The balance scorecard

approach is adopted by entities with the aim of aligning the objectives and strategies of the

organization with the activities or operations performed by the business (Kaplan, 2009, p.1253).

Moreover, with the implementation of the balanced scorecard approach organizations aim at

improving the communication pattern adopted by the entity within and outside the business

organization.

II) Implementation of Balanced scorecard can deliver a range of financial and

non financial performance measures

Figure 1: Balanced scorecard

(Source: Kaplan, 2009, p.1253)

Through the implementation of balanced scorecard approach organizations can undertake the

process of delivering a broad range of both financial and non financial metrics. The financial

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.