Assessing Time-Driven Activity-Based Costing for Toyota Motors

VerifiedAdded on 2020/05/28

|13

|2533

|191

Report

AI Summary

This report assesses the suitability of Time-Driven Activity-Based Costing (TDABC) for Toyota Motor Corporation. It begins with an introduction to TDABC, explaining its principles and features, and then provides an overview of Toyota Motor Corporation, including its global vision and production system. The report details the differences between TDABC, Activity-Based Costing (ABC), and traditional costing systems, highlighting the advantages of TDABC in terms of accuracy and efficiency. It further analyzes the suitability of TDABC for Toyota, emphasizing the benefits such as time and cost savings, improved resource allocation, and enhanced process information within the company's complex operational structure. The report concludes that TDABC is a fitting method for Toyota, enabling it to streamline operations and enhance productivity. References to relevant academic sources are also included.

Accounting

Managerial Accounting

1/12/2018

Managerial Accounting

1/12/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 1

Contents

Introduction......................................................................................................................................2

About Toyota Motor Corporation....................................................................................................3

Toyota Global Vision..................................................................................................................3

Toyota production system............................................................................................................4

Time-Driven Activity-Based Costing..............................................................................................5

Time equations.............................................................................................................................5

Features of Time-Driven Activity-Based Costing.......................................................................6

Difference between TDABC and Activity- Based Costing and Traditional Costing System.........6

Suitability of TDABC for Toyota Motor Corporation....................................................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Contents

Introduction......................................................................................................................................2

About Toyota Motor Corporation....................................................................................................3

Toyota Global Vision..................................................................................................................3

Toyota production system............................................................................................................4

Time-Driven Activity-Based Costing..............................................................................................5

Time equations.............................................................................................................................5

Features of Time-Driven Activity-Based Costing.......................................................................6

Difference between TDABC and Activity- Based Costing and Traditional Costing System.........6

Suitability of TDABC for Toyota Motor Corporation....................................................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Managerial Accounting 2

Introduction

Time-Driven Activity-Based costing is an advanced method of ABC (Activity-Based costing).

The report shows whether Time-Driven Activity-Based costing is suitable for the Toyota Motor

Corporation or not. The report will talk about the Time-Driven Activity-Based costing concept

and its features. This is the fact that the TDABC is different than the ABC method and traditional

costing system. Furthermore, the report includes the suitability of TDABC costing method for

the Toyota Motor Corporation.

Introduction

Time-Driven Activity-Based costing is an advanced method of ABC (Activity-Based costing).

The report shows whether Time-Driven Activity-Based costing is suitable for the Toyota Motor

Corporation or not. The report will talk about the Time-Driven Activity-Based costing concept

and its features. This is the fact that the TDABC is different than the ABC method and traditional

costing system. Furthermore, the report includes the suitability of TDABC costing method for

the Toyota Motor Corporation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting 3

About Toyota Motor Corporation

Toyota Motor Corporation is a Japanese Multinational automotive manufacturing corporation

with the headquarters in Aichi. Since, the time when company came into the existence Toyota

has sought to contribute to a more prosperous society through manufacturing of vehicles

(Bloomberg, 2018). Toyota Motor Corporation manufactures, assembles, designs and sells

minivans, passenger vehicles, and commercial vehicles. Along with this the company sells the

related parts and accessories of the products. The company has completed 75 years and now the

company is celebrating its 75 years and showing its progress in the last three-quarter century

(Toyota, 2017). Toyota Industries Corporation came into the existence in the year 1926,

November. This was the time when the company started the manufacturing and deals of spinning

and weaving machines, industrial automobiles along with the logistics (Toyota, 2017).

Toyota is one of the world’ largest automobile manufacturer along with this the company is a

leading light in the sales of the hybrid electric automobiles. Toyota was the first company who

produce more than 10 million vehicles per year since 2012, at the same time the company

presented the production of the 200-million vehicles (Toyota, 2017). By the year 2009, the

company listed around 70 diverse models that are traded under its brand which include sedans,

coupes, vans, trucks, hybrids, and crossovers. By the end of December 2016, the company

operates its business operations with 53 foreign manufacturing organizations in 28 countries and

regions across the world. The company automobiles are traded in more than 170 regions and

countries (Toyota, 2017).

About Toyota Motor Corporation

Toyota Motor Corporation is a Japanese Multinational automotive manufacturing corporation

with the headquarters in Aichi. Since, the time when company came into the existence Toyota

has sought to contribute to a more prosperous society through manufacturing of vehicles

(Bloomberg, 2018). Toyota Motor Corporation manufactures, assembles, designs and sells

minivans, passenger vehicles, and commercial vehicles. Along with this the company sells the

related parts and accessories of the products. The company has completed 75 years and now the

company is celebrating its 75 years and showing its progress in the last three-quarter century

(Toyota, 2017). Toyota Industries Corporation came into the existence in the year 1926,

November. This was the time when the company started the manufacturing and deals of spinning

and weaving machines, industrial automobiles along with the logistics (Toyota, 2017).

Toyota is one of the world’ largest automobile manufacturer along with this the company is a

leading light in the sales of the hybrid electric automobiles. Toyota was the first company who

produce more than 10 million vehicles per year since 2012, at the same time the company

presented the production of the 200-million vehicles (Toyota, 2017). By the year 2009, the

company listed around 70 diverse models that are traded under its brand which include sedans,

coupes, vans, trucks, hybrids, and crossovers. By the end of December 2016, the company

operates its business operations with 53 foreign manufacturing organizations in 28 countries and

regions across the world. The company automobiles are traded in more than 170 regions and

countries (Toyota, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 4

Toyota Global Vision

The vision of the company is to lead the way to the future of freedom of movement, enriching

lives globally with the harmless and accountable way of moving people. Toyota commits to

deliver the quality with the modernization and respect for the planet. The aim of the company is

to surpass expectations and be pleased with a smile (Toyota, 2017). The company believes that

they will meet the challenging objectives by involving talent and passion of people who have

faith in the fact that there is always a better way. Toyota has been guiding philosophies to

produce dependable automobiles and sustainable development of society by employing high-

quality innovative products (Toyota, 2017).

Toyota production system

Toyota production system is stepped in the philosophy of the comprehensive elimination of all

the waste. The production control system of the company has been founded based on several

years of constant developments. The aim of the Toyota is to make the vehicles ordered by the

customer’s ineffective and quickest way in order to supply the automobiles as soon as possible

(Toyota, 2017).

The production system of Toyota is created on two theories; “Jidoka” and “Just-in-Time”. Jidoka

means when a problem takes place when the equipment stops instantly that helps the business to

escape the manufacturing of the defective products. The concept of Just-in-time is the process in

which the production takes place in the continuous flow (Toyota, 2017). Through Just-in-Time,

the company can eliminate the complete waste, inconsistencies and unreasonable requirement in

the production line. The vehicles provided by the company to their customer are known for its

quality. The company is able to fulfill its commitment to quality. Toyota production system can

effectively and quickly produce vehicles of sound quality that helps the company in fulfilling and

Toyota Global Vision

The vision of the company is to lead the way to the future of freedom of movement, enriching

lives globally with the harmless and accountable way of moving people. Toyota commits to

deliver the quality with the modernization and respect for the planet. The aim of the company is

to surpass expectations and be pleased with a smile (Toyota, 2017). The company believes that

they will meet the challenging objectives by involving talent and passion of people who have

faith in the fact that there is always a better way. Toyota has been guiding philosophies to

produce dependable automobiles and sustainable development of society by employing high-

quality innovative products (Toyota, 2017).

Toyota production system

Toyota production system is stepped in the philosophy of the comprehensive elimination of all

the waste. The production control system of the company has been founded based on several

years of constant developments. The aim of the Toyota is to make the vehicles ordered by the

customer’s ineffective and quickest way in order to supply the automobiles as soon as possible

(Toyota, 2017).

The production system of Toyota is created on two theories; “Jidoka” and “Just-in-Time”. Jidoka

means when a problem takes place when the equipment stops instantly that helps the business to

escape the manufacturing of the defective products. The concept of Just-in-time is the process in

which the production takes place in the continuous flow (Toyota, 2017). Through Just-in-Time,

the company can eliminate the complete waste, inconsistencies and unreasonable requirement in

the production line. The vehicles provided by the company to their customer are known for its

quality. The company is able to fulfill its commitment to quality. Toyota production system can

effectively and quickly produce vehicles of sound quality that helps the company in fulfilling and

Managerial Accounting 5

meeting the expectations of the customers and ultimately leads to the customer’s satisfaction

(Toyota, 2017). This is possible due to the use of the simple philosophies of Just-in-Time and

Jidoka.

Time-Driven Activity-Based Costing

Activity-based costing is a costing practice that recognizes undertakings within an organization

and allocates the cost of every activity along with capitals to all products and services. ABC is

helping many companies in identifying the cost and profit enhancement opportunities through

lower-cost product designs, process improvement and rationalized product variety. To make this

process simpler there is a new approach of ABC that is TDABC (Time-Driven Activity-Based

Costing). The simplification is now possible because of the approach time-driven ABC. In the

year 2007, Rebert Kaplan, a Harvard Business School professor presented this concept of the

Time-Driven ABC (Kaplan and Anderson, 2017).

TDABC is a simpler way to estimate the resource demands considering the particular

transactions, product or the customers. For a particular group of resources, there is need of the

approximations of the two parameters which include the cost per time unity of Supplying

resource capacity and the unit times of consumption of resources capacity by customers,

products, services. Time-driven ABC offers more exact cost-driven rated by permitting unit

times to be predicted even for compound and focussed transactions (Dejnega, 2011). This new

ABC approach eliminated the required of time-consuming surveys and interviews process which

is defined as the resource pools. This method only relies on the direct observation of processes.

This approach precisely accounts for the difficulties of business transactions (like the variation in

the operational transactions) with the use of the time equation (Ozyurek and Dinç, 2014).

meeting the expectations of the customers and ultimately leads to the customer’s satisfaction

(Toyota, 2017). This is possible due to the use of the simple philosophies of Just-in-Time and

Jidoka.

Time-Driven Activity-Based Costing

Activity-based costing is a costing practice that recognizes undertakings within an organization

and allocates the cost of every activity along with capitals to all products and services. ABC is

helping many companies in identifying the cost and profit enhancement opportunities through

lower-cost product designs, process improvement and rationalized product variety. To make this

process simpler there is a new approach of ABC that is TDABC (Time-Driven Activity-Based

Costing). The simplification is now possible because of the approach time-driven ABC. In the

year 2007, Rebert Kaplan, a Harvard Business School professor presented this concept of the

Time-Driven ABC (Kaplan and Anderson, 2017).

TDABC is a simpler way to estimate the resource demands considering the particular

transactions, product or the customers. For a particular group of resources, there is need of the

approximations of the two parameters which include the cost per time unity of Supplying

resource capacity and the unit times of consumption of resources capacity by customers,

products, services. Time-driven ABC offers more exact cost-driven rated by permitting unit

times to be predicted even for compound and focussed transactions (Dejnega, 2011). This new

ABC approach eliminated the required of time-consuming surveys and interviews process which

is defined as the resource pools. This method only relies on the direct observation of processes.

This approach precisely accounts for the difficulties of business transactions (like the variation in

the operational transactions) with the use of the time equation (Ozyurek and Dinç, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting 6

Time equations

Time-driven ABC simply integrates variation in the time demands made by the various

categories of transactions. The time equation is beneficial for the organizations as with the use of

the time equation the company can precisely reflect the time comprises in a certain process. It

removes the requirement of tracking the various activities to account for the different costs

related to the single activity. TDABC model captures the accuracy of the resource demands from

various processes by adding extra terms to the departmental time equation from its ability (Adioti

and Valverde, 2013).

Features of Time-Driven Activity-Based Costing

TDABC system is stress-free to update and organise the use of the time equations that are

supported by the ERP system of today's (Kaplan and Anderson, 2017).

Managers of the companies find it easy to update the capacity cost rates and the unit-time

approximations as working state of affairs change.

Time-Driven Activity-Based Costing system is easily updated to show the variations in

processes of business, resource cost, and the ordered variety.

This model is one of the effective systems to handle millions of transactions in business,

real-time reporting and the fast processing time (Dejnega, 2011).

Difference between TDABC and Activity- Based Costing and Traditional

Costing System

Basis of

Difference

Traditional Costing

System

Activity-Based Costing Time-Driven Activity-

Based Costing

Time equations

Time-driven ABC simply integrates variation in the time demands made by the various

categories of transactions. The time equation is beneficial for the organizations as with the use of

the time equation the company can precisely reflect the time comprises in a certain process. It

removes the requirement of tracking the various activities to account for the different costs

related to the single activity. TDABC model captures the accuracy of the resource demands from

various processes by adding extra terms to the departmental time equation from its ability (Adioti

and Valverde, 2013).

Features of Time-Driven Activity-Based Costing

TDABC system is stress-free to update and organise the use of the time equations that are

supported by the ERP system of today's (Kaplan and Anderson, 2017).

Managers of the companies find it easy to update the capacity cost rates and the unit-time

approximations as working state of affairs change.

Time-Driven Activity-Based Costing system is easily updated to show the variations in

processes of business, resource cost, and the ordered variety.

This model is one of the effective systems to handle millions of transactions in business,

real-time reporting and the fast processing time (Dejnega, 2011).

Difference between TDABC and Activity- Based Costing and Traditional

Costing System

Basis of

Difference

Traditional Costing

System

Activity-Based Costing Time-Driven Activity-

Based Costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 7

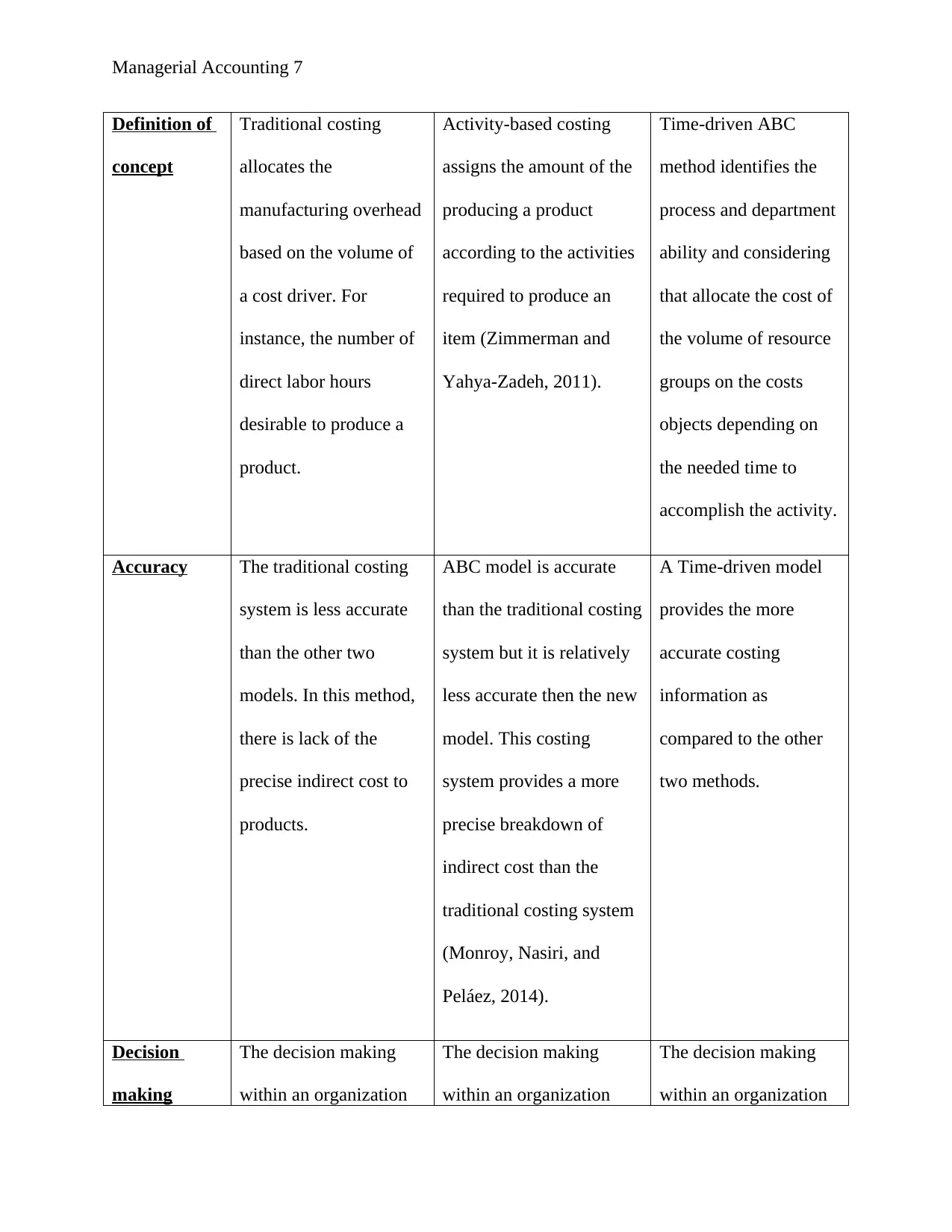

Definition of

concept

Traditional costing

allocates the

manufacturing overhead

based on the volume of

a cost driver. For

instance, the number of

direct labor hours

desirable to produce a

product.

Activity-based costing

assigns the amount of the

producing a product

according to the activities

required to produce an

item (Zimmerman and

Yahya-Zadeh, 2011).

Time-driven ABC

method identifies the

process and department

ability and considering

that allocate the cost of

the volume of resource

groups on the costs

objects depending on

the needed time to

accomplish the activity.

Accuracy The traditional costing

system is less accurate

than the other two

models. In this method,

there is lack of the

precise indirect cost to

products.

ABC model is accurate

than the traditional costing

system but it is relatively

less accurate then the new

model. This costing

system provides a more

precise breakdown of

indirect cost than the

traditional costing system

(Monroy, Nasiri, and

Peláez, 2014).

A Time-driven model

provides the more

accurate costing

information as

compared to the other

two methods.

Decision

making

The decision making

within an organization

The decision making

within an organization

The decision making

within an organization

Definition of

concept

Traditional costing

allocates the

manufacturing overhead

based on the volume of

a cost driver. For

instance, the number of

direct labor hours

desirable to produce a

product.

Activity-based costing

assigns the amount of the

producing a product

according to the activities

required to produce an

item (Zimmerman and

Yahya-Zadeh, 2011).

Time-driven ABC

method identifies the

process and department

ability and considering

that allocate the cost of

the volume of resource

groups on the costs

objects depending on

the needed time to

accomplish the activity.

Accuracy The traditional costing

system is less accurate

than the other two

models. In this method,

there is lack of the

precise indirect cost to

products.

ABC model is accurate

than the traditional costing

system but it is relatively

less accurate then the new

model. This costing

system provides a more

precise breakdown of

indirect cost than the

traditional costing system

(Monroy, Nasiri, and

Peláez, 2014).

A Time-driven model

provides the more

accurate costing

information as

compared to the other

two methods.

Decision

making

The decision making

within an organization

The decision making

within an organization

The decision making

within an organization

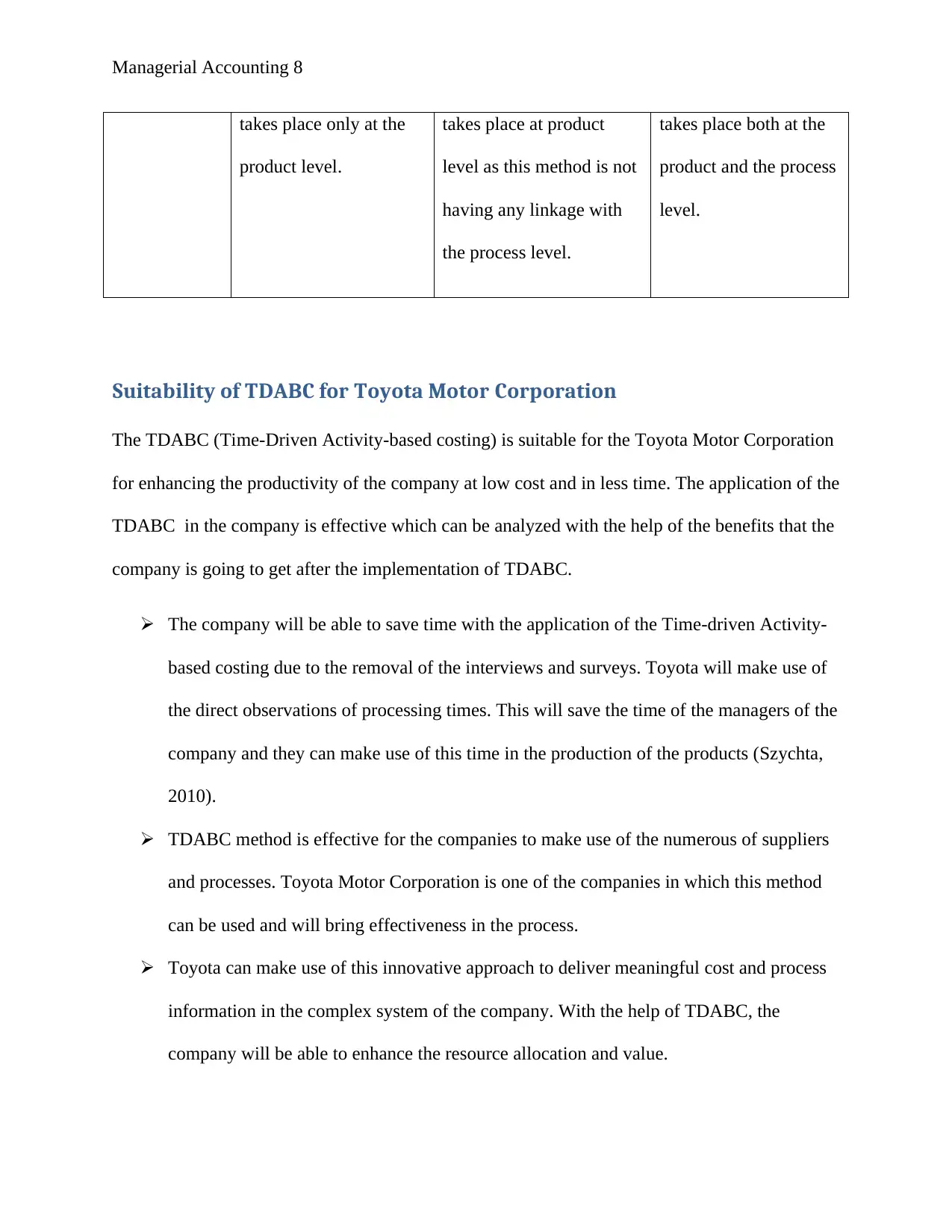

Managerial Accounting 8

takes place only at the

product level.

takes place at product

level as this method is not

having any linkage with

the process level.

takes place both at the

product and the process

level.

Suitability of TDABC for Toyota Motor Corporation

The TDABC (Time-Driven Activity-based costing) is suitable for the Toyota Motor Corporation

for enhancing the productivity of the company at low cost and in less time. The application of the

TDABC in the company is effective which can be analyzed with the help of the benefits that the

company is going to get after the implementation of TDABC.

The company will be able to save time with the application of the Time-driven Activity-

based costing due to the removal of the interviews and surveys. Toyota will make use of

the direct observations of processing times. This will save the time of the managers of the

company and they can make use of this time in the production of the products (Szychta,

2010).

TDABC method is effective for the companies to make use of the numerous of suppliers

and processes. Toyota Motor Corporation is one of the companies in which this method

can be used and will bring effectiveness in the process.

Toyota can make use of this innovative approach to deliver meaningful cost and process

information in the complex system of the company. With the help of TDABC, the

company will be able to enhance the resource allocation and value.

takes place only at the

product level.

takes place at product

level as this method is not

having any linkage with

the process level.

takes place both at the

product and the process

level.

Suitability of TDABC for Toyota Motor Corporation

The TDABC (Time-Driven Activity-based costing) is suitable for the Toyota Motor Corporation

for enhancing the productivity of the company at low cost and in less time. The application of the

TDABC in the company is effective which can be analyzed with the help of the benefits that the

company is going to get after the implementation of TDABC.

The company will be able to save time with the application of the Time-driven Activity-

based costing due to the removal of the interviews and surveys. Toyota will make use of

the direct observations of processing times. This will save the time of the managers of the

company and they can make use of this time in the production of the products (Szychta,

2010).

TDABC method is effective for the companies to make use of the numerous of suppliers

and processes. Toyota Motor Corporation is one of the companies in which this method

can be used and will bring effectiveness in the process.

Toyota can make use of this innovative approach to deliver meaningful cost and process

information in the complex system of the company. With the help of TDABC, the

company will be able to enhance the resource allocation and value.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managerial Accounting 9

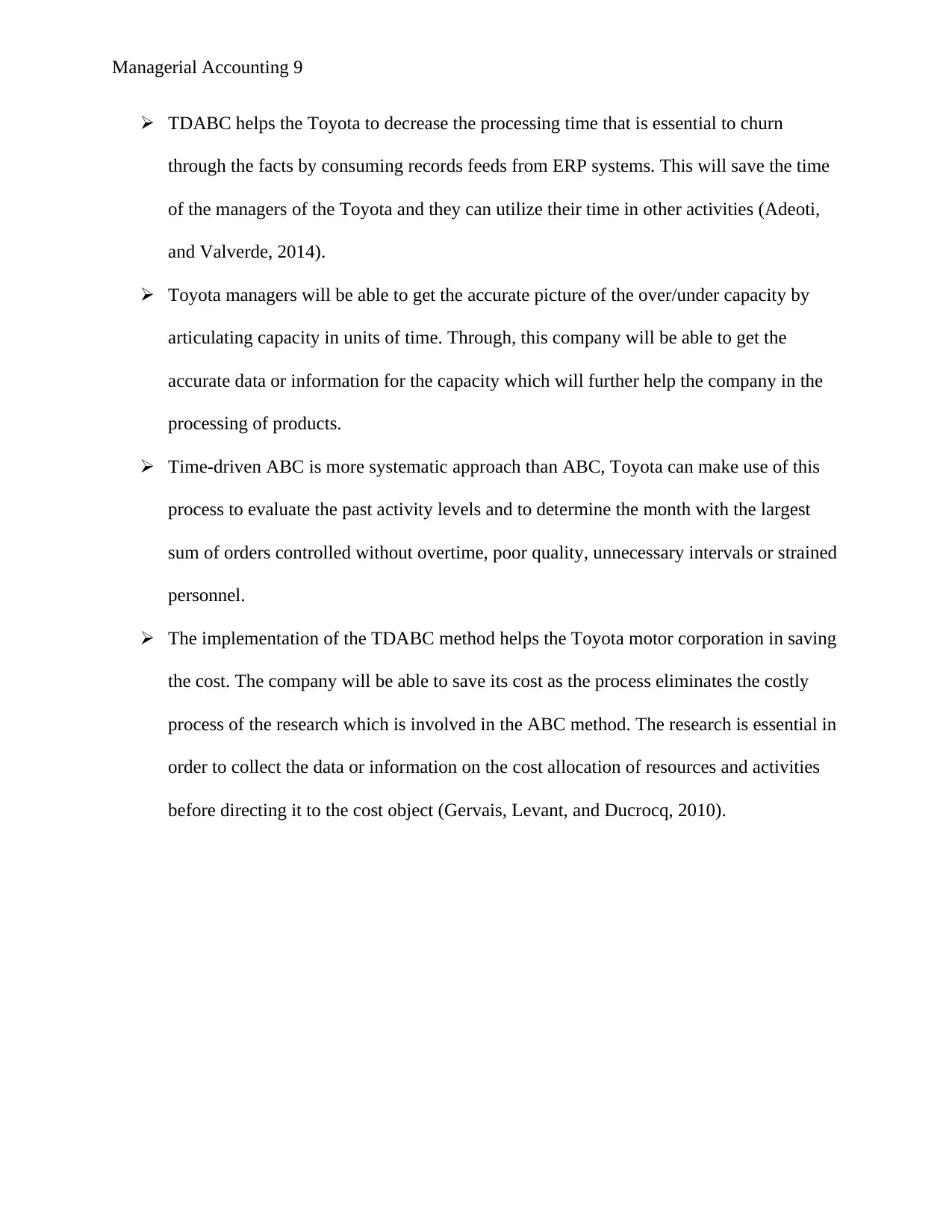

TDABC helps the Toyota to decrease the processing time that is essential to churn

through the facts by consuming records feeds from ERP systems. This will save the time

of the managers of the Toyota and they can utilize their time in other activities (Adeoti,

and Valverde, 2014).

Toyota managers will be able to get the accurate picture of the over/under capacity by

articulating capacity in units of time. Through, this company will be able to get the

accurate data or information for the capacity which will further help the company in the

processing of products.

Time-driven ABC is more systematic approach than ABC, Toyota can make use of this

process to evaluate the past activity levels and to determine the month with the largest

sum of orders controlled without overtime, poor quality, unnecessary intervals or strained

personnel.

The implementation of the TDABC method helps the Toyota motor corporation in saving

the cost. The company will be able to save its cost as the process eliminates the costly

process of the research which is involved in the ABC method. The research is essential in

order to collect the data or information on the cost allocation of resources and activities

before directing it to the cost object (Gervais, Levant, and Ducrocq, 2010).

TDABC helps the Toyota to decrease the processing time that is essential to churn

through the facts by consuming records feeds from ERP systems. This will save the time

of the managers of the Toyota and they can utilize their time in other activities (Adeoti,

and Valverde, 2014).

Toyota managers will be able to get the accurate picture of the over/under capacity by

articulating capacity in units of time. Through, this company will be able to get the

accurate data or information for the capacity which will further help the company in the

processing of products.

Time-driven ABC is more systematic approach than ABC, Toyota can make use of this

process to evaluate the past activity levels and to determine the month with the largest

sum of orders controlled without overtime, poor quality, unnecessary intervals or strained

personnel.

The implementation of the TDABC method helps the Toyota motor corporation in saving

the cost. The company will be able to save its cost as the process eliminates the costly

process of the research which is involved in the ABC method. The research is essential in

order to collect the data or information on the cost allocation of resources and activities

before directing it to the cost object (Gervais, Levant, and Ducrocq, 2010).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Managerial Accounting 10

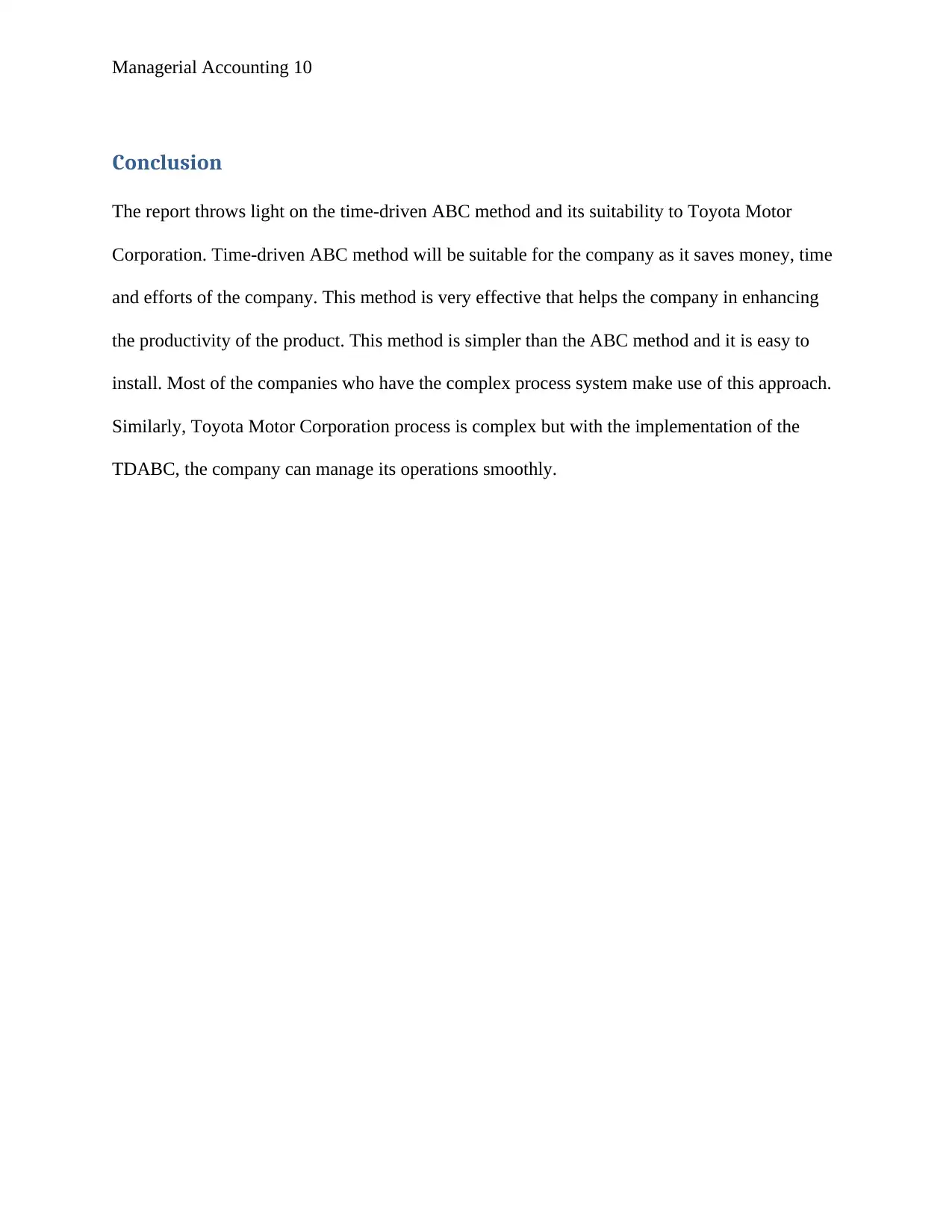

Conclusion

The report throws light on the time-driven ABC method and its suitability to Toyota Motor

Corporation. Time-driven ABC method will be suitable for the company as it saves money, time

and efforts of the company. This method is very effective that helps the company in enhancing

the productivity of the product. This method is simpler than the ABC method and it is easy to

install. Most of the companies who have the complex process system make use of this approach.

Similarly, Toyota Motor Corporation process is complex but with the implementation of the

TDABC, the company can manage its operations smoothly.

Conclusion

The report throws light on the time-driven ABC method and its suitability to Toyota Motor

Corporation. Time-driven ABC method will be suitable for the company as it saves money, time

and efforts of the company. This method is very effective that helps the company in enhancing

the productivity of the product. This method is simpler than the ABC method and it is easy to

install. Most of the companies who have the complex process system make use of this approach.

Similarly, Toyota Motor Corporation process is complex but with the implementation of the

TDABC, the company can manage its operations smoothly.

Managerial Accounting 11

References

Adeoti, A.A. and Valverde, R., 2014. Time-Driven Activity Based Costing for the Improvement

of IT Service Operations. International Journal of Business and Management, 9(1).

Bloomberg, 2018, Company Overview of Toyota Motor Corporation, Accessed on; 13th January

2018, Accessed from https://www.bloomberg.com/research/stocks/private/snapshot.asp?

privcapId=319676

Dejnega, O., 2011. Method Time Driven Activity Based Costing. Journal of Applied.

Gervais, M., Levant, Y. and Ducrocq, C., 2010. Time-driven activity-based costing (TDABC):

An initial appraisal through a longitudinal case study. Journal of Applied Management

Accounting Research, 8(2), p.1.

Kaplan, R.S. and Anderson, S.R., 2017, Time Driven Activity Based Costing, Accessed on; 13th

January 2018, Accessed from https://hbr.org/2004/11/time-driven-activity-based-costing

Monroy, C.R., Nasiri, A. and Peláez, M.Á., 2014. Activity Based Costing, Time-Driven Activity

Based Costing and Lean Accounting: Differences among three accounting systems’ approach to

manufacturing. In Annals of Industrial Engineering 2012 (pp. 11-17). Springer London.

Ozyurek, H. and Dinç, Y., 2014. Time-Driven Activity Based Costing. International Journal of

Business and Management Studies, 6(1), pp.97-117.

Szychta, A., 2010. Time-Driven Activity-Based Costing in Service Industries. Social Sciences

(1392-0758), 67(1).

References

Adeoti, A.A. and Valverde, R., 2014. Time-Driven Activity Based Costing for the Improvement

of IT Service Operations. International Journal of Business and Management, 9(1).

Bloomberg, 2018, Company Overview of Toyota Motor Corporation, Accessed on; 13th January

2018, Accessed from https://www.bloomberg.com/research/stocks/private/snapshot.asp?

privcapId=319676

Dejnega, O., 2011. Method Time Driven Activity Based Costing. Journal of Applied.

Gervais, M., Levant, Y. and Ducrocq, C., 2010. Time-driven activity-based costing (TDABC):

An initial appraisal through a longitudinal case study. Journal of Applied Management

Accounting Research, 8(2), p.1.

Kaplan, R.S. and Anderson, S.R., 2017, Time Driven Activity Based Costing, Accessed on; 13th

January 2018, Accessed from https://hbr.org/2004/11/time-driven-activity-based-costing

Monroy, C.R., Nasiri, A. and Peláez, M.Á., 2014. Activity Based Costing, Time-Driven Activity

Based Costing and Lean Accounting: Differences among three accounting systems’ approach to

manufacturing. In Annals of Industrial Engineering 2012 (pp. 11-17). Springer London.

Ozyurek, H. and Dinç, Y., 2014. Time-Driven Activity Based Costing. International Journal of

Business and Management Studies, 6(1), pp.97-117.

Szychta, A., 2010. Time-Driven Activity-Based Costing in Service Industries. Social Sciences

(1392-0758), 67(1).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13