Analysis of New LifeTraining Plc's Operational and Regulatory Factors

VerifiedAdded on 2020/10/22

|13

|3920

|256

AI Summary

The assignment analyzes the income statement projections of New LifeTraining Plc for four years, considering alterations in tutor fees, hypothetical variable expenses, and source of capital. It provides clear evidence and descriptive statistics to understand issues and their applications in the business of giving training. The report also discusses various risk factors and the importance of proper consideration by the board of directors.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Managing Finance

and Operation

and Operation

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

a) Operational and regulatory factors considered by the board..............................................1

b) Income and expenditure projections for the first 4 years ..................................................3

c) Evaluation of financial worth for current proposal............................................................5

d) Conclusion and recommendation.......................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

a) Operational and regulatory factors considered by the board..............................................1

b) Income and expenditure projections for the first 4 years ..................................................3

c) Evaluation of financial worth for current proposal............................................................5

d) Conclusion and recommendation.......................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

In order to consider development of business, there are several elements included in it

that make important consideration to take decisions. In this way, proper cash needs to be

maintained to run short objectives in the financial management. Furthermore, it is important for

operations to consider proper attention and focus on day to day elements such as raw material,

electricity bills, rent, etc. In this context, present report is based on the New Life Training which

is growing business and authorised share capital to attain desired results in systematic manner.

They offer different kinds of core academic subjects to attain significant results in the business

environment. For gaining insight information of present report, it includes operational and

regulatory factors which are considered in the board. Furthermore, it focuses on income and

expenditure for 4 years incorporating to develop significant advantages. At last, conclusion and

recommendations have been implemented that help to attain significant advantages in the

business environment.

MAIN BODY

a) Operational and regulatory factors considered by the board

In order to focus on the board consideration, there are regulators that consider financial

focus on the business to analyse distinctive and greater level of insight and awareness. Therefore,

risk will be managed in a successful manner to ascertain and mitigate the significant results. In

addition to this, operational management involves managing process that helps to consider raw

material, labour, energy, etc. to produce goods and services. With this regard, different theories

are considered such as business process redesign, reconfigurable manufacturing system, lean, six

sigma, etc. In this context, Six Sigma is the main approach that helps to focus on the quality

which assists to maintain effectiveness at workplace with defined sequence and financial targets

as well. It assists to increase the profits and reduce costs to develop effective advantages

(Mizgier and et.al., 2015). Lean accounting is also a systematic method that helps to eliminate

waste material in the manufacturing process. It helps to seem resources to create value for

customers. As results, elimination of the negative elements could be considered in a systematic

manner.

Following are certain operational and regulatory factors exist that are considered by

board in New Life Training:

1

In order to consider development of business, there are several elements included in it

that make important consideration to take decisions. In this way, proper cash needs to be

maintained to run short objectives in the financial management. Furthermore, it is important for

operations to consider proper attention and focus on day to day elements such as raw material,

electricity bills, rent, etc. In this context, present report is based on the New Life Training which

is growing business and authorised share capital to attain desired results in systematic manner.

They offer different kinds of core academic subjects to attain significant results in the business

environment. For gaining insight information of present report, it includes operational and

regulatory factors which are considered in the board. Furthermore, it focuses on income and

expenditure for 4 years incorporating to develop significant advantages. At last, conclusion and

recommendations have been implemented that help to attain significant advantages in the

business environment.

MAIN BODY

a) Operational and regulatory factors considered by the board

In order to focus on the board consideration, there are regulators that consider financial

focus on the business to analyse distinctive and greater level of insight and awareness. Therefore,

risk will be managed in a successful manner to ascertain and mitigate the significant results. In

addition to this, operational management involves managing process that helps to consider raw

material, labour, energy, etc. to produce goods and services. With this regard, different theories

are considered such as business process redesign, reconfigurable manufacturing system, lean, six

sigma, etc. In this context, Six Sigma is the main approach that helps to focus on the quality

which assists to maintain effectiveness at workplace with defined sequence and financial targets

as well. It assists to increase the profits and reduce costs to develop effective advantages

(Mizgier and et.al., 2015). Lean accounting is also a systematic method that helps to eliminate

waste material in the manufacturing process. It helps to seem resources to create value for

customers. As results, elimination of the negative elements could be considered in a systematic

manner.

Following are certain operational and regulatory factors exist that are considered by

board in New Life Training:

1

Cyber risk and data security: In respect to work for the new operations and functions in

New Life Training, it is essential to look upon the cyber risk and data security. This is

because; number of risks ranked with threat from cyber-attack as the top operational risk

for last year. With the help of the proper management, they can reduce cyber-attack

which is not growing but also insidious forms by the risk practitioners (Chwieroth, 2015).

As the reputation damage, enough actions will be taken. Source of potential cyber threat

pins down and making building of appropriate control which is serious challenges and

attack in the world.

Regulations: Furthermore, there are several regulations considered as the risk

practitioner which denotes landmark regulations with capital adequacy frameworks,

widespread market structure reform, etc. It represents that changes to accounting

practices determine potential operational risks for New Life Training. In this regard, it is

essential for business to expose themselves in the operational risk and increasing their

return on equity. However, operational risk seems to one of the cause of regulators which

determines more concern in which they struggle. It creates a huge impact on the

operational risk capital and groups as well (Mousa, 2015). Hence, the chosen business

needs to make sure that all employees are fully aware with roles and responsibilities.

Ethical elements are also associated that create challenges that ensure proper business

practices exit around all products and services rendered by enterprise.

Outsourcing: Outsourcing consider three operational risks in New Life Training. For

instance: spurred by clear message from regulators, third party risk management and face

punitive sanctions. Hence, financial organisation must consider their reviews with

existing outsourcing arrangement. It helps to ensure that failure of third party service

providers will be reduced in a systematic way through focus on the systematic work

performances. GDPR compliance represents a significant burden so that managers need

to know exactly about the customer data that are held all times (Cambini and et.al.,

2016). Hence, it is important to understand complex web of relationship with different

outsource, practitioners, etc.

Geopolitical risk: In the business outcomes, geopolitical risk also ascertained due to

election of UK. The country withdrew from the European Union so that it combined to

push the geopolitical risk into 10 years. Along with this, direct costs occur against the

2

New Life Training, it is essential to look upon the cyber risk and data security. This is

because; number of risks ranked with threat from cyber-attack as the top operational risk

for last year. With the help of the proper management, they can reduce cyber-attack

which is not growing but also insidious forms by the risk practitioners (Chwieroth, 2015).

As the reputation damage, enough actions will be taken. Source of potential cyber threat

pins down and making building of appropriate control which is serious challenges and

attack in the world.

Regulations: Furthermore, there are several regulations considered as the risk

practitioner which denotes landmark regulations with capital adequacy frameworks,

widespread market structure reform, etc. It represents that changes to accounting

practices determine potential operational risks for New Life Training. In this regard, it is

essential for business to expose themselves in the operational risk and increasing their

return on equity. However, operational risk seems to one of the cause of regulators which

determines more concern in which they struggle. It creates a huge impact on the

operational risk capital and groups as well (Mousa, 2015). Hence, the chosen business

needs to make sure that all employees are fully aware with roles and responsibilities.

Ethical elements are also associated that create challenges that ensure proper business

practices exit around all products and services rendered by enterprise.

Outsourcing: Outsourcing consider three operational risks in New Life Training. For

instance: spurred by clear message from regulators, third party risk management and face

punitive sanctions. Hence, financial organisation must consider their reviews with

existing outsourcing arrangement. It helps to ensure that failure of third party service

providers will be reduced in a systematic way through focus on the systematic work

performances. GDPR compliance represents a significant burden so that managers need

to know exactly about the customer data that are held all times (Cambini and et.al.,

2016). Hence, it is important to understand complex web of relationship with different

outsource, practitioners, etc.

Geopolitical risk: In the business outcomes, geopolitical risk also ascertained due to

election of UK. The country withdrew from the European Union so that it combined to

push the geopolitical risk into 10 years. Along with this, direct costs occur against the

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

backdrop of significant economic, regulatory and business change. As results, it directly

impacts indirectly as operational risk with outsourcing, organisational and business

change, regulations, etc. in New Life Training (Cruz and et.al, 2016). Financial

legislations also create own risks to maintain new supplier relationship that are

heightened outsourcing the risk.

Conduct risk: In the UK, security and exchange commission take successful

enforcement that are entitled to provide reward up to 30%. Therefore, managers stated

that it seeks to codify culture of personality development. Individuals also input their

efforts to make systematic results in New Life Training. It assists the business to take

successful enforcement (Leyman and Vanhoucke, 2016). In this regard, Securities and

Exchange Commission imposed to the organisation with legislation which came into the

force and it is levied with related fines.

Organisational change: Organisational change comes in different forms. However, it

consider by the regulation, technological changes and corporate restructuring as well.

Results also consider upheaval which require changes to the top risk frameworks. It helps

to cope up with new and idiosyncratic source of risk (Ng and Beruvides, 2015). Changes

to desk structure and internal risk transfer processes helps to encounter under the

committee.

b) Income and expenditure projections for the first 4 years

Each and every transactions which are related to concerns which are not for profit such as

clubs, library etc. are usually tracked in the books of account according to the double entry

system and in the end of year all the interpretation is justified with the help of final accounts and

it comprises two steps, one is income and expenditure account and another one is a balance

sheet. Here the income statement is undertaken for observing the financial position or to justify

the net income and projections are done for consecutive four years (Caballero, Farhi and

Gourinchas, 2017). The main feature of income statement is all the revenue and income which

are properly concerned with current year whether the cash is received or not and even the

expenses which are paid or not are considered in this statement. But no expense or income of

next year is not included in it.

Projected Income statement for the years 2018, 2019, 2020 and 2021

2017-2018 2018-2019 2019-2020 2020-2021

3

impacts indirectly as operational risk with outsourcing, organisational and business

change, regulations, etc. in New Life Training (Cruz and et.al, 2016). Financial

legislations also create own risks to maintain new supplier relationship that are

heightened outsourcing the risk.

Conduct risk: In the UK, security and exchange commission take successful

enforcement that are entitled to provide reward up to 30%. Therefore, managers stated

that it seeks to codify culture of personality development. Individuals also input their

efforts to make systematic results in New Life Training. It assists the business to take

successful enforcement (Leyman and Vanhoucke, 2016). In this regard, Securities and

Exchange Commission imposed to the organisation with legislation which came into the

force and it is levied with related fines.

Organisational change: Organisational change comes in different forms. However, it

consider by the regulation, technological changes and corporate restructuring as well.

Results also consider upheaval which require changes to the top risk frameworks. It helps

to cope up with new and idiosyncratic source of risk (Ng and Beruvides, 2015). Changes

to desk structure and internal risk transfer processes helps to encounter under the

committee.

b) Income and expenditure projections for the first 4 years

Each and every transactions which are related to concerns which are not for profit such as

clubs, library etc. are usually tracked in the books of account according to the double entry

system and in the end of year all the interpretation is justified with the help of final accounts and

it comprises two steps, one is income and expenditure account and another one is a balance

sheet. Here the income statement is undertaken for observing the financial position or to justify

the net income and projections are done for consecutive four years (Caballero, Farhi and

Gourinchas, 2017). The main feature of income statement is all the revenue and income which

are properly concerned with current year whether the cash is received or not and even the

expenses which are paid or not are considered in this statement. But no expense or income of

next year is not included in it.

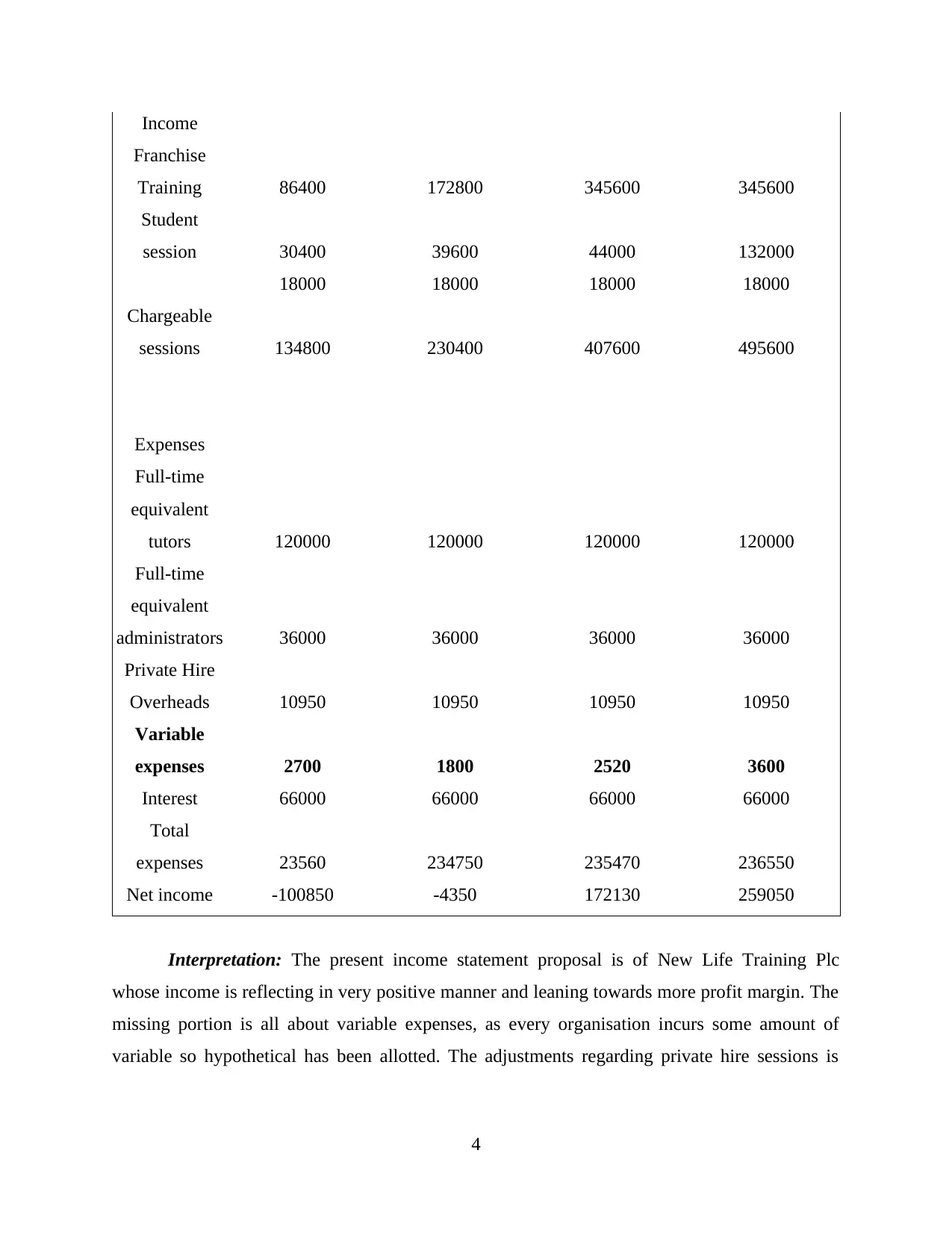

Projected Income statement for the years 2018, 2019, 2020 and 2021

2017-2018 2018-2019 2019-2020 2020-2021

3

Income

Franchise

Training 86400 172800 345600 345600

Student

session 30400 39600 44000 132000

18000 18000 18000 18000

Chargeable

sessions 134800 230400 407600 495600

Expenses

Full-time

equivalent

tutors 120000 120000 120000 120000

Full-time

equivalent

administrators 36000 36000 36000 36000

Private Hire

Overheads 10950 10950 10950 10950

Variable

expenses 2700 1800 2520 3600

Interest 66000 66000 66000 66000

Total

expenses 23560 234750 235470 236550

Net income -100850 -4350 172130 259050

Interpretation: The present income statement proposal is of New Life Training Plc

whose income is reflecting in very positive manner and leaning towards more profit margin. The

missing portion is all about variable expenses, as every organisation incurs some amount of

variable so hypothetical has been allotted. The adjustments regarding private hire sessions is

4

Franchise

Training 86400 172800 345600 345600

Student

session 30400 39600 44000 132000

18000 18000 18000 18000

Chargeable

sessions 134800 230400 407600 495600

Expenses

Full-time

equivalent

tutors 120000 120000 120000 120000

Full-time

equivalent

administrators 36000 36000 36000 36000

Private Hire

Overheads 10950 10950 10950 10950

Variable

expenses 2700 1800 2520 3600

Interest 66000 66000 66000 66000

Total

expenses 23560 234750 235470 236550

Net income -100850 -4350 172130 259050

Interpretation: The present income statement proposal is of New Life Training Plc

whose income is reflecting in very positive manner and leaning towards more profit margin. The

missing portion is all about variable expenses, as every organisation incurs some amount of

variable so hypothetical has been allotted. The adjustments regarding private hire sessions is

4

been altered that for six years then want to be stable from previous year. In the first two year it

generated loss but that is also decreasing after that it started raising its net income in four years.

The combination of debt and equity is been presenting the whole company as in the

present company it has equity of 10% and debt of 6% and gearing ratio was 50% before taking

debt of additional capital for the building. According to the given information company has

given more focus on equity but it should give priority to debt base to improve the performance of

organizations. But the building will be debt financed so company must be able to balance debt

and equity both but with properly payment of instalment.

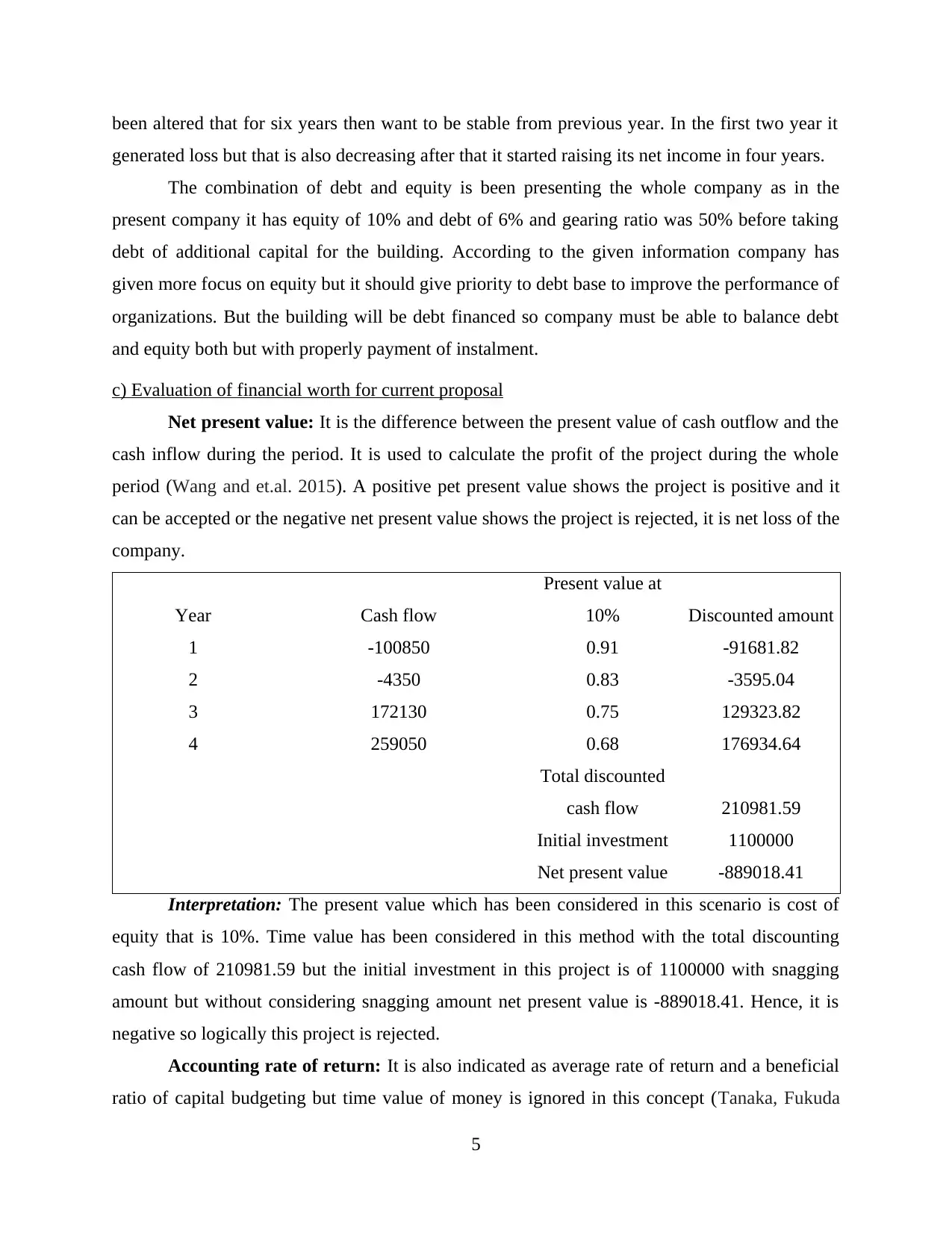

c) Evaluation of financial worth for current proposal

Net present value: It is the difference between the present value of cash outflow and the

cash inflow during the period. It is used to calculate the profit of the project during the whole

period (Wang and et.al. 2015). A positive pet present value shows the project is positive and it

can be accepted or the negative net present value shows the project is rejected, it is net loss of the

company.

Year Cash flow

Present value at

10% Discounted amount

1 -100850 0.91 -91681.82

2 -4350 0.83 -3595.04

3 172130 0.75 129323.82

4 259050 0.68 176934.64

Total discounted

cash flow 210981.59

Initial investment 1100000

Net present value -889018.41

Interpretation: The present value which has been considered in this scenario is cost of

equity that is 10%. Time value has been considered in this method with the total discounting

cash flow of 210981.59 but the initial investment in this project is of 1100000 with snagging

amount but without considering snagging amount net present value is -889018.41. Hence, it is

negative so logically this project is rejected.

Accounting rate of return: It is also indicated as average rate of return and a beneficial

ratio of capital budgeting but time value of money is ignored in this concept (Tanaka, Fukuda

5

generated loss but that is also decreasing after that it started raising its net income in four years.

The combination of debt and equity is been presenting the whole company as in the

present company it has equity of 10% and debt of 6% and gearing ratio was 50% before taking

debt of additional capital for the building. According to the given information company has

given more focus on equity but it should give priority to debt base to improve the performance of

organizations. But the building will be debt financed so company must be able to balance debt

and equity both but with properly payment of instalment.

c) Evaluation of financial worth for current proposal

Net present value: It is the difference between the present value of cash outflow and the

cash inflow during the period. It is used to calculate the profit of the project during the whole

period (Wang and et.al. 2015). A positive pet present value shows the project is positive and it

can be accepted or the negative net present value shows the project is rejected, it is net loss of the

company.

Year Cash flow

Present value at

10% Discounted amount

1 -100850 0.91 -91681.82

2 -4350 0.83 -3595.04

3 172130 0.75 129323.82

4 259050 0.68 176934.64

Total discounted

cash flow 210981.59

Initial investment 1100000

Net present value -889018.41

Interpretation: The present value which has been considered in this scenario is cost of

equity that is 10%. Time value has been considered in this method with the total discounting

cash flow of 210981.59 but the initial investment in this project is of 1100000 with snagging

amount but without considering snagging amount net present value is -889018.41. Hence, it is

negative so logically this project is rejected.

Accounting rate of return: It is also indicated as average rate of return and a beneficial

ratio of capital budgeting but time value of money is ignored in this concept (Tanaka, Fukuda

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

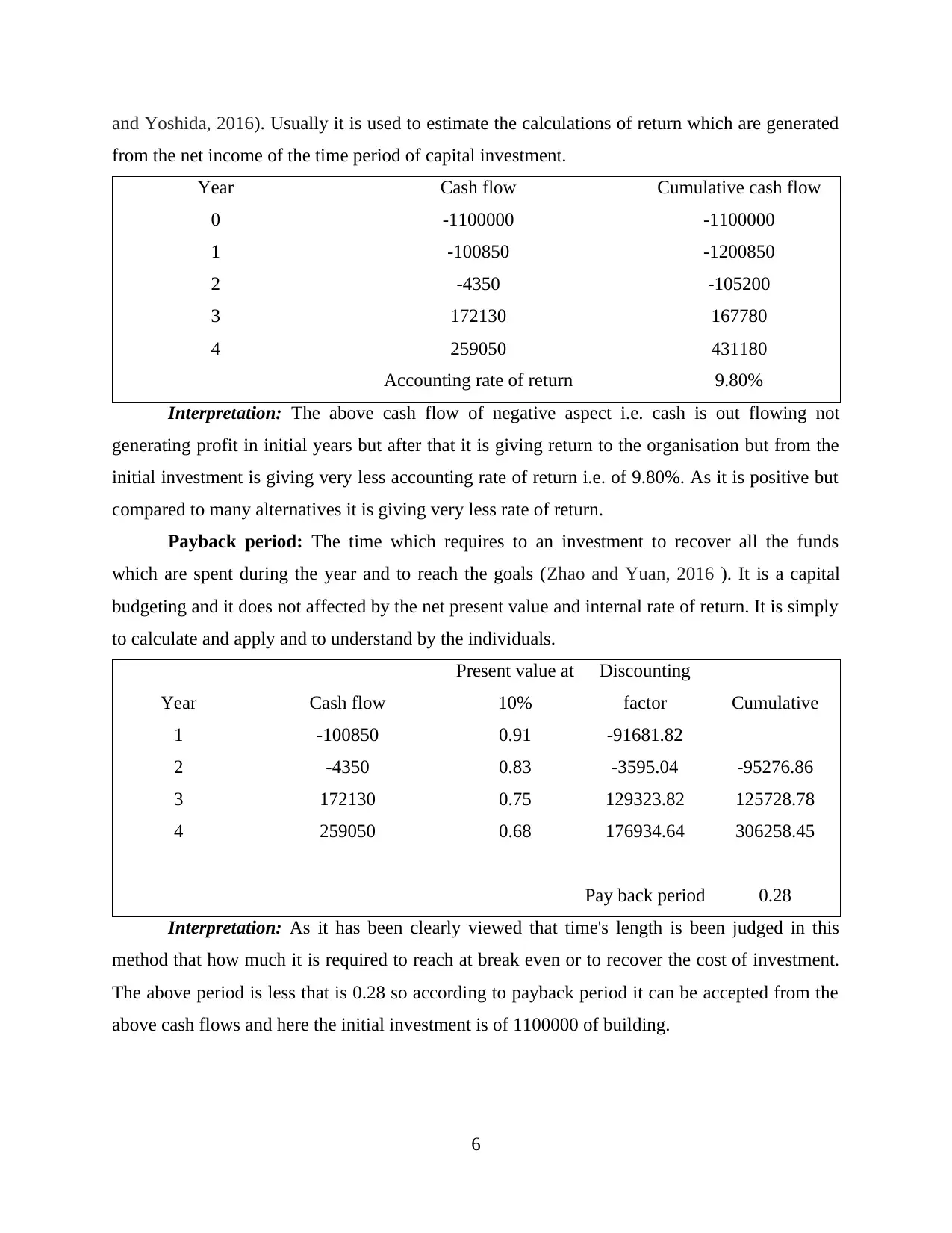

and Yoshida, 2016). Usually it is used to estimate the calculations of return which are generated

from the net income of the time period of capital investment.

Year Cash flow Cumulative cash flow

0 -1100000 -1100000

1 -100850 -1200850

2 -4350 -105200

3 172130 167780

4 259050 431180

Accounting rate of return 9.80%

Interpretation: The above cash flow of negative aspect i.e. cash is out flowing not

generating profit in initial years but after that it is giving return to the organisation but from the

initial investment is giving very less accounting rate of return i.e. of 9.80%. As it is positive but

compared to many alternatives it is giving very less rate of return.

Payback period: The time which requires to an investment to recover all the funds

which are spent during the year and to reach the goals (Zhao and Yuan, 2016 ). It is a capital

budgeting and it does not affected by the net present value and internal rate of return. It is simply

to calculate and apply and to understand by the individuals.

Year Cash flow

Present value at

10%

Discounting

factor Cumulative

1 -100850 0.91 -91681.82

2 -4350 0.83 -3595.04 -95276.86

3 172130 0.75 129323.82 125728.78

4 259050 0.68 176934.64 306258.45

Pay back period 0.28

Interpretation: As it has been clearly viewed that time's length is been judged in this

method that how much it is required to reach at break even or to recover the cost of investment.

The above period is less that is 0.28 so according to payback period it can be accepted from the

above cash flows and here the initial investment is of 1100000 of building.

6

from the net income of the time period of capital investment.

Year Cash flow Cumulative cash flow

0 -1100000 -1100000

1 -100850 -1200850

2 -4350 -105200

3 172130 167780

4 259050 431180

Accounting rate of return 9.80%

Interpretation: The above cash flow of negative aspect i.e. cash is out flowing not

generating profit in initial years but after that it is giving return to the organisation but from the

initial investment is giving very less accounting rate of return i.e. of 9.80%. As it is positive but

compared to many alternatives it is giving very less rate of return.

Payback period: The time which requires to an investment to recover all the funds

which are spent during the year and to reach the goals (Zhao and Yuan, 2016 ). It is a capital

budgeting and it does not affected by the net present value and internal rate of return. It is simply

to calculate and apply and to understand by the individuals.

Year Cash flow

Present value at

10%

Discounting

factor Cumulative

1 -100850 0.91 -91681.82

2 -4350 0.83 -3595.04 -95276.86

3 172130 0.75 129323.82 125728.78

4 259050 0.68 176934.64 306258.45

Pay back period 0.28

Interpretation: As it has been clearly viewed that time's length is been judged in this

method that how much it is required to reach at break even or to recover the cost of investment.

The above period is less that is 0.28 so according to payback period it can be accepted from the

above cash flows and here the initial investment is of 1100000 of building.

6

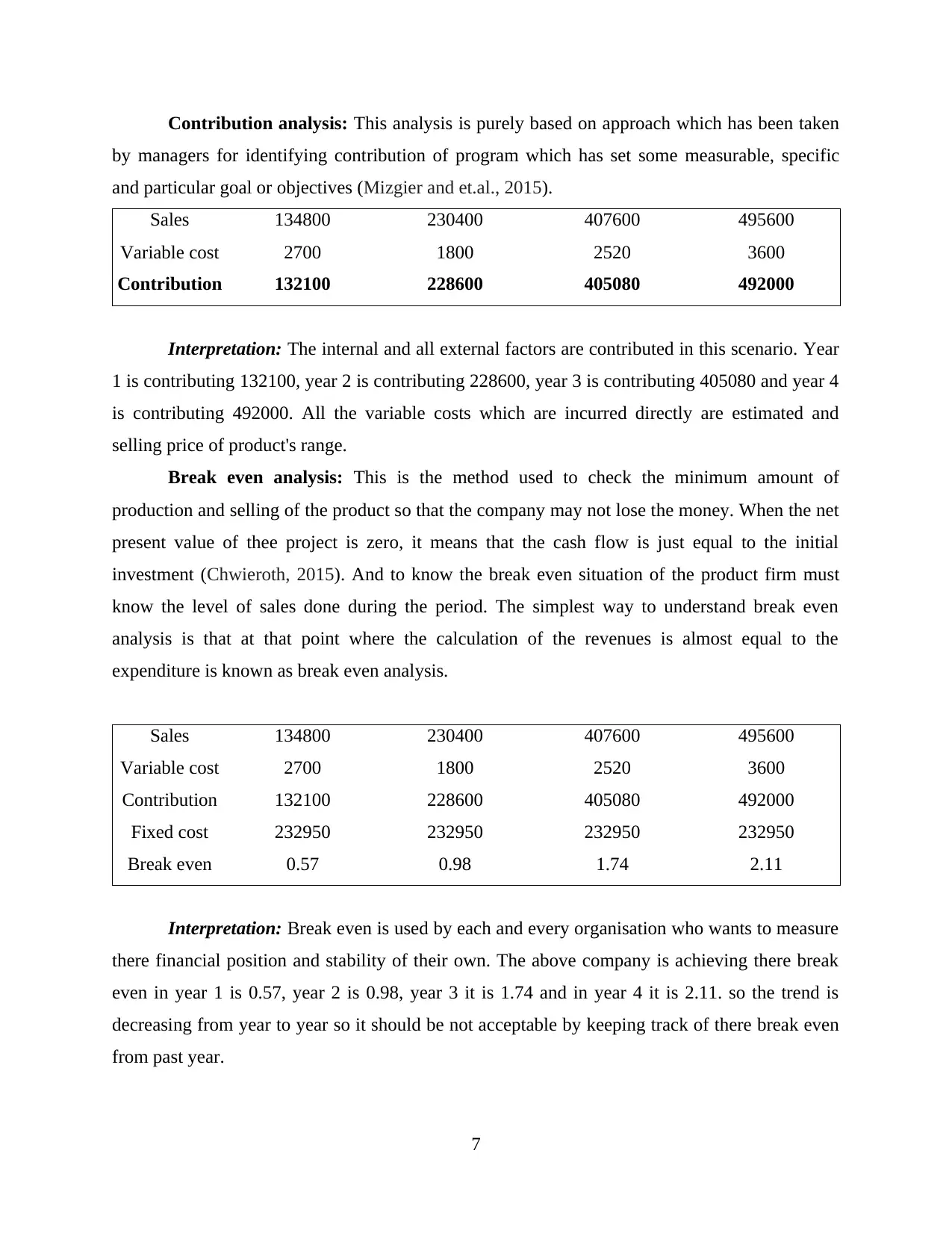

Contribution analysis: This analysis is purely based on approach which has been taken

by managers for identifying contribution of program which has set some measurable, specific

and particular goal or objectives (Mizgier and et.al., 2015).

Sales 134800 230400 407600 495600

Variable cost 2700 1800 2520 3600

Contribution 132100 228600 405080 492000

Interpretation: The internal and all external factors are contributed in this scenario. Year

1 is contributing 132100, year 2 is contributing 228600, year 3 is contributing 405080 and year 4

is contributing 492000. All the variable costs which are incurred directly are estimated and

selling price of product's range.

Break even analysis: This is the method used to check the minimum amount of

production and selling of the product so that the company may not lose the money. When the net

present value of thee project is zero, it means that the cash flow is just equal to the initial

investment (Chwieroth, 2015). And to know the break even situation of the product firm must

know the level of sales done during the period. The simplest way to understand break even

analysis is that at that point where the calculation of the revenues is almost equal to the

expenditure is known as break even analysis.

Sales 134800 230400 407600 495600

Variable cost 2700 1800 2520 3600

Contribution 132100 228600 405080 492000

Fixed cost 232950 232950 232950 232950

Break even 0.57 0.98 1.74 2.11

Interpretation: Break even is used by each and every organisation who wants to measure

there financial position and stability of their own. The above company is achieving there break

even in year 1 is 0.57, year 2 is 0.98, year 3 it is 1.74 and in year 4 it is 2.11. so the trend is

decreasing from year to year so it should be not acceptable by keeping track of there break even

from past year.

7

by managers for identifying contribution of program which has set some measurable, specific

and particular goal or objectives (Mizgier and et.al., 2015).

Sales 134800 230400 407600 495600

Variable cost 2700 1800 2520 3600

Contribution 132100 228600 405080 492000

Interpretation: The internal and all external factors are contributed in this scenario. Year

1 is contributing 132100, year 2 is contributing 228600, year 3 is contributing 405080 and year 4

is contributing 492000. All the variable costs which are incurred directly are estimated and

selling price of product's range.

Break even analysis: This is the method used to check the minimum amount of

production and selling of the product so that the company may not lose the money. When the net

present value of thee project is zero, it means that the cash flow is just equal to the initial

investment (Chwieroth, 2015). And to know the break even situation of the product firm must

know the level of sales done during the period. The simplest way to understand break even

analysis is that at that point where the calculation of the revenues is almost equal to the

expenditure is known as break even analysis.

Sales 134800 230400 407600 495600

Variable cost 2700 1800 2520 3600

Contribution 132100 228600 405080 492000

Fixed cost 232950 232950 232950 232950

Break even 0.57 0.98 1.74 2.11

Interpretation: Break even is used by each and every organisation who wants to measure

there financial position and stability of their own. The above company is achieving there break

even in year 1 is 0.57, year 2 is 0.98, year 3 it is 1.74 and in year 4 it is 2.11. so the trend is

decreasing from year to year so it should be not acceptable by keeping track of there break even

from past year.

7

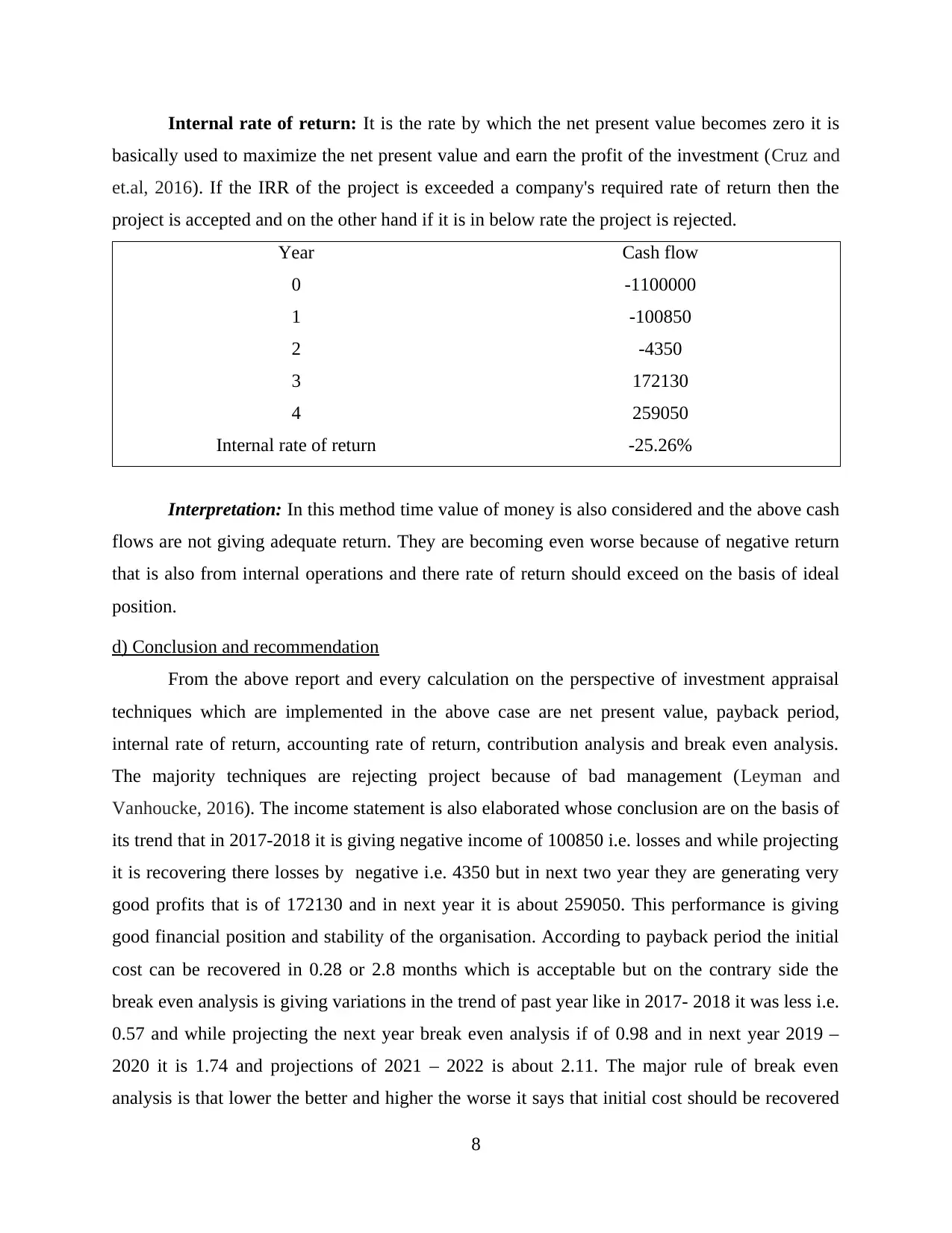

Internal rate of return: It is the rate by which the net present value becomes zero it is

basically used to maximize the net present value and earn the profit of the investment (Cruz and

et.al, 2016). If the IRR of the project is exceeded a company's required rate of return then the

project is accepted and on the other hand if it is in below rate the project is rejected.

Year Cash flow

0 -1100000

1 -100850

2 -4350

3 172130

4 259050

Internal rate of return -25.26%

Interpretation: In this method time value of money is also considered and the above cash

flows are not giving adequate return. They are becoming even worse because of negative return

that is also from internal operations and there rate of return should exceed on the basis of ideal

position.

d) Conclusion and recommendation

From the above report and every calculation on the perspective of investment appraisal

techniques which are implemented in the above case are net present value, payback period,

internal rate of return, accounting rate of return, contribution analysis and break even analysis.

The majority techniques are rejecting project because of bad management (Leyman and

Vanhoucke, 2016). The income statement is also elaborated whose conclusion are on the basis of

its trend that in 2017-2018 it is giving negative income of 100850 i.e. losses and while projecting

it is recovering there losses by negative i.e. 4350 but in next two year they are generating very

good profits that is of 172130 and in next year it is about 259050. This performance is giving

good financial position and stability of the organisation. According to payback period the initial

cost can be recovered in 0.28 or 2.8 months which is acceptable but on the contrary side the

break even analysis is giving variations in the trend of past year like in 2017- 2018 it was less i.e.

0.57 and while projecting the next year break even analysis if of 0.98 and in next year 2019 –

2020 it is 1.74 and projections of 2021 – 2022 is about 2.11. The major rule of break even

analysis is that lower the better and higher the worse it says that initial cost should be recovered

8

basically used to maximize the net present value and earn the profit of the investment (Cruz and

et.al, 2016). If the IRR of the project is exceeded a company's required rate of return then the

project is accepted and on the other hand if it is in below rate the project is rejected.

Year Cash flow

0 -1100000

1 -100850

2 -4350

3 172130

4 259050

Internal rate of return -25.26%

Interpretation: In this method time value of money is also considered and the above cash

flows are not giving adequate return. They are becoming even worse because of negative return

that is also from internal operations and there rate of return should exceed on the basis of ideal

position.

d) Conclusion and recommendation

From the above report and every calculation on the perspective of investment appraisal

techniques which are implemented in the above case are net present value, payback period,

internal rate of return, accounting rate of return, contribution analysis and break even analysis.

The majority techniques are rejecting project because of bad management (Leyman and

Vanhoucke, 2016). The income statement is also elaborated whose conclusion are on the basis of

its trend that in 2017-2018 it is giving negative income of 100850 i.e. losses and while projecting

it is recovering there losses by negative i.e. 4350 but in next two year they are generating very

good profits that is of 172130 and in next year it is about 259050. This performance is giving

good financial position and stability of the organisation. According to payback period the initial

cost can be recovered in 0.28 or 2.8 months which is acceptable but on the contrary side the

break even analysis is giving variations in the trend of past year like in 2017- 2018 it was less i.e.

0.57 and while projecting the next year break even analysis if of 0.98 and in next year 2019 –

2020 it is 1.74 and projections of 2021 – 2022 is about 2.11. The major rule of break even

analysis is that lower the better and higher the worse it says that initial cost should be recovered

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

as soon as possible. The past performance is more good as compared to the projections. The

accounting rate of return of the project is giving 9.80% return from the project which is giving

not very good significance from the organisation perspective, it should give more return, there

goal should be big and it should be achieved. As it is giving return but it always ignores time

value of money, there is the presence of constraint and there analysis and it is always giving

impact on company's output and there operations. This measure is not adequate for doing

comparisons between another projects and many other factors rate of return is purely considered

but are not able to express them quantitatively. The project's internal rate of return is about

25.26% but that is negative so it is rejected without observing the factors because in this overall

rate of returns instead of net present value and by rule highest is better and logically through the

operations of the factory is transformed and how much return they are able to make internally. It

can be best suited for doing brief analysis of venture capital and investments of private equity

which does the entailing various cash investments over the life span of business (Ng and

Beruvides, 2015). By summing up the analysis company should reject the proposal because by

observing investment appraisal technique the majority of them are giving negative prospective so

it should properly focus on balance of equity and debt, its internal operations and should try to

reduce the expenses because this will directly reflecting the financial performance and stability

of the organization.

CONCLUSION

From the above report it should be concluded that operational and regulatory factors are

very essential for the organisation and it should give proper consideration by the board of

directors. The major risk should be undertaken very carefully along with the process of training

that are geopolitical risk, cyber risk and data security, outsourcing and regulations should be

conducted very properly and risk should be conducted in appropriate manner. The present report

has mentioned various projections of the income statement of New LifeTraining Plc has been

done for the four years and in that alterations like stable fees of tutor, hypothetical variable

expenses and source of capital has been also identified above with its important. Further it is

concluded not with only descriptive statistics but clear evidence has been provided for

understanding issues and how they are applied for the business of giving training.

9

accounting rate of return of the project is giving 9.80% return from the project which is giving

not very good significance from the organisation perspective, it should give more return, there

goal should be big and it should be achieved. As it is giving return but it always ignores time

value of money, there is the presence of constraint and there analysis and it is always giving

impact on company's output and there operations. This measure is not adequate for doing

comparisons between another projects and many other factors rate of return is purely considered

but are not able to express them quantitatively. The project's internal rate of return is about

25.26% but that is negative so it is rejected without observing the factors because in this overall

rate of returns instead of net present value and by rule highest is better and logically through the

operations of the factory is transformed and how much return they are able to make internally. It

can be best suited for doing brief analysis of venture capital and investments of private equity

which does the entailing various cash investments over the life span of business (Ng and

Beruvides, 2015). By summing up the analysis company should reject the proposal because by

observing investment appraisal technique the majority of them are giving negative prospective so

it should properly focus on balance of equity and debt, its internal operations and should try to

reduce the expenses because this will directly reflecting the financial performance and stability

of the organization.

CONCLUSION

From the above report it should be concluded that operational and regulatory factors are

very essential for the organisation and it should give proper consideration by the board of

directors. The major risk should be undertaken very carefully along with the process of training

that are geopolitical risk, cyber risk and data security, outsourcing and regulations should be

conducted very properly and risk should be conducted in appropriate manner. The present report

has mentioned various projections of the income statement of New LifeTraining Plc has been

done for the four years and in that alterations like stable fees of tutor, hypothetical variable

expenses and source of capital has been also identified above with its important. Further it is

concluded not with only descriptive statistics but clear evidence has been provided for

understanding issues and how they are applied for the business of giving training.

9

REFERENCES

Books and Journals

Caballero, R. J., Farhi, E. and Gourinchas, P. O., 2017. Rents, technical change, and risk premia

accounting for secular trends in interest rates, returns on capital, earning yields, and factor

shares. American Economic Review. 107(5). pp.614-20.

Cambini, C. and et.al., 2016. Market and regulatory factors influencing smart-grid investment in

Europe: Evidence from pilot projects and implications for reform. Utilities Policy. 40.

pp.36-47.

Chwieroth, J. M., 2015. Managing and transforming policy stigmas in international finance:

Emerging markets and controlling capital inflows after the crisis. Review of International

Political Economy. 22(1). pp.44-76.

Cruz, T. and et.al, 2016. A cybersecurity detection framework for supervisory control and data

acquisition systems. IEEE Transactions on Industrial Informatics. 12(6). pp.2236-2246.

Leyman, P. and Vanhoucke, M., 2016. Payment models and net present value optimization for

resource-constrained project scheduling. Computers & Industrial Engineering. 91. pp.139-

153.

Mizgier, K.J. And et.al., 2015. Managing operational disruptions through capital adequacy and

process improvement. European Journal of Operational Research. 245(1). pp.320-332.

Mousa, G. A., 2015. Financial Ratios versus Data Envelopment Analysis: The Efficiency

Assessment of Banking Sector in Bahrain Bourse. International Journal of Business and

Statistical Analysis. 2(2). pp.75-84.

Ng, E. H. and Beruvides, M. G., 2015. Multiple internal rate of return revisited: Frequency of

occurrences. The Engineering Economist. 60(1). pp.75-87.

Tanaka, K., Fukuda, J. Y. D. S. and Yoshida, J., 2016. Vibration mode contribution analysis for

construction machines utilizing operational TPA. Proc 23rd ICSV, pp.10-14.

Wang, X. Q. And et.al. 2015. Payback period estimation and parameter optimization of

subcritical organic Rankine cycle system for waste heat recovery. Energy. 88. pp.734-745.

Zhao, D. and Yuan, S., 2016. Critical result on the break-even concentration in a single-species

stochastic chemostat model. Journal of Mathematical Analysis and Applications. 434(2).

pp.1336-1345.

10

Books and Journals

Caballero, R. J., Farhi, E. and Gourinchas, P. O., 2017. Rents, technical change, and risk premia

accounting for secular trends in interest rates, returns on capital, earning yields, and factor

shares. American Economic Review. 107(5). pp.614-20.

Cambini, C. and et.al., 2016. Market and regulatory factors influencing smart-grid investment in

Europe: Evidence from pilot projects and implications for reform. Utilities Policy. 40.

pp.36-47.

Chwieroth, J. M., 2015. Managing and transforming policy stigmas in international finance:

Emerging markets and controlling capital inflows after the crisis. Review of International

Political Economy. 22(1). pp.44-76.

Cruz, T. and et.al, 2016. A cybersecurity detection framework for supervisory control and data

acquisition systems. IEEE Transactions on Industrial Informatics. 12(6). pp.2236-2246.

Leyman, P. and Vanhoucke, M., 2016. Payment models and net present value optimization for

resource-constrained project scheduling. Computers & Industrial Engineering. 91. pp.139-

153.

Mizgier, K.J. And et.al., 2015. Managing operational disruptions through capital adequacy and

process improvement. European Journal of Operational Research. 245(1). pp.320-332.

Mousa, G. A., 2015. Financial Ratios versus Data Envelopment Analysis: The Efficiency

Assessment of Banking Sector in Bahrain Bourse. International Journal of Business and

Statistical Analysis. 2(2). pp.75-84.

Ng, E. H. and Beruvides, M. G., 2015. Multiple internal rate of return revisited: Frequency of

occurrences. The Engineering Economist. 60(1). pp.75-87.

Tanaka, K., Fukuda, J. Y. D. S. and Yoshida, J., 2016. Vibration mode contribution analysis for

construction machines utilizing operational TPA. Proc 23rd ICSV, pp.10-14.

Wang, X. Q. And et.al. 2015. Payback period estimation and parameter optimization of

subcritical organic Rankine cycle system for waste heat recovery. Energy. 88. pp.734-745.

Zhao, D. and Yuan, S., 2016. Critical result on the break-even concentration in a single-species

stochastic chemostat model. Journal of Mathematical Analysis and Applications. 434(2).

pp.1336-1345.

10

ONLINE

Income and Expenditure account, 2013. [Online]. Available through

:<http://www.accountingexplanation.com/income_and_expenditure_account.html>.

11

Income and Expenditure account, 2013. [Online]. Available through

:<http://www.accountingexplanation.com/income_and_expenditure_account.html>.

11

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.