Assignment On Hypothetical company

VerifiedAdded on 2022/09/22

|10

|1932

|26

Assignment

AI Summary

my case company is HVN, please follow Harvard style. attempt only part 2 and part 3 please

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1

Finance

Finance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

Table of Contents

Question 2..................................................................................................................................3

a).............................................................................................................................................3

b)............................................................................................................................................3

Question 3..................................................................................................................................3

a).............................................................................................................................................3

References..................................................................................................................................6

Appendix....................................................................................................................................7

Table of Contents

Question 2..................................................................................................................................3

a).............................................................................................................................................3

b)............................................................................................................................................3

Question 3..................................................................................................................................3

a).............................................................................................................................................3

References..................................................................................................................................6

Appendix....................................................................................................................................7

3

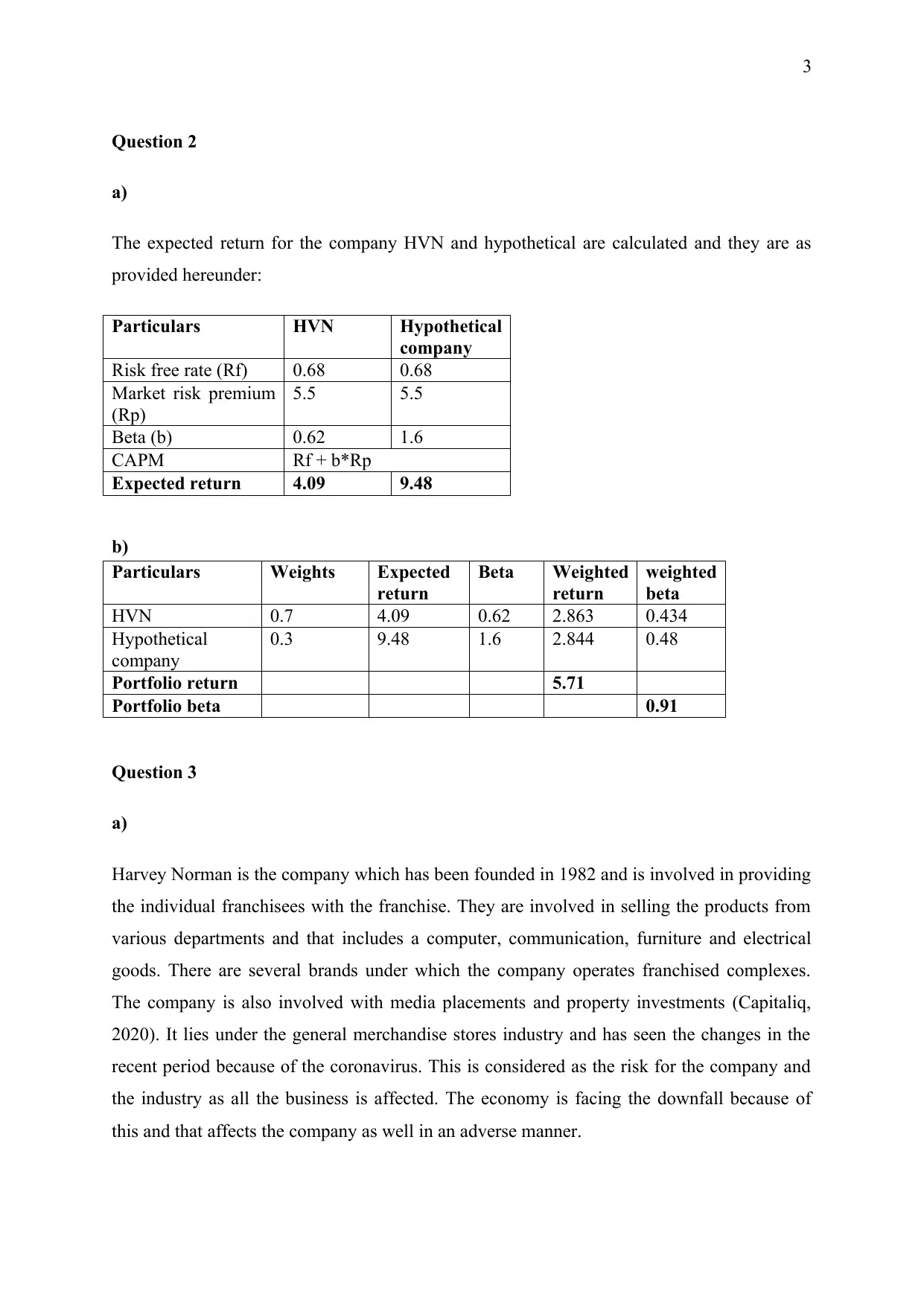

Question 2

a)

The expected return for the company HVN and hypothetical are calculated and they are as

provided hereunder:

Particulars HVN Hypothetical

company

Risk free rate (Rf) 0.68 0.68

Market risk premium

(Rp)

5.5 5.5

Beta (b) 0.62 1.6

CAPM Rf + b*Rp

Expected return 4.09 9.48

b)

Particulars Weights Expected

return

Beta Weighted

return

weighted

beta

HVN 0.7 4.09 0.62 2.863 0.434

Hypothetical

company

0.3 9.48 1.6 2.844 0.48

Portfolio return 5.71

Portfolio beta 0.91

Question 3

a)

Harvey Norman is the company which has been founded in 1982 and is involved in providing

the individual franchisees with the franchise. They are involved in selling the products from

various departments and that includes a computer, communication, furniture and electrical

goods. There are several brands under which the company operates franchised complexes.

The company is also involved with media placements and property investments (Capitaliq,

2020). It lies under the general merchandise stores industry and has seen the changes in the

recent period because of the coronavirus. This is considered as the risk for the company and

the industry as all the business is affected. The economy is facing the downfall because of

this and that affects the company as well in an adverse manner.

Question 2

a)

The expected return for the company HVN and hypothetical are calculated and they are as

provided hereunder:

Particulars HVN Hypothetical

company

Risk free rate (Rf) 0.68 0.68

Market risk premium

(Rp)

5.5 5.5

Beta (b) 0.62 1.6

CAPM Rf + b*Rp

Expected return 4.09 9.48

b)

Particulars Weights Expected

return

Beta Weighted

return

weighted

beta

HVN 0.7 4.09 0.62 2.863 0.434

Hypothetical

company

0.3 9.48 1.6 2.844 0.48

Portfolio return 5.71

Portfolio beta 0.91

Question 3

a)

Harvey Norman is the company which has been founded in 1982 and is involved in providing

the individual franchisees with the franchise. They are involved in selling the products from

various departments and that includes a computer, communication, furniture and electrical

goods. There are several brands under which the company operates franchised complexes.

The company is also involved with media placements and property investments (Capitaliq,

2020). It lies under the general merchandise stores industry and has seen the changes in the

recent period because of the coronavirus. This is considered as the risk for the company and

the industry as all the business is affected. The economy is facing the downfall because of

this and that affects the company as well in an adverse manner.

4

There is a negative impact as all the businesses are temporarily closed and the trading is not

taking place which is affecting the profitability and cash flow of the business. The economy

is declining as the returns are not available and that will affect the business and the market in

the long-term as heavy losses are being made.

In the business, there are various stocks that are involved and in which the investment is

made by people. All of them consider various aspects before making the decision and in that

most important are the return and risk associated with them. The return which is expected by

the shareholders is required to be identified as that forms the base for all the decisions. This is

required to be calculated and for that various approaches are available. In the current case,

there is the use of the capital asset pricing model which is considered to be most appropriate

(Gagliardini and Gouriéroux, 2013). The method considers the risk free rate which is

prevailing in the market and then adjusts the market premium according to the involved risk

with the help of beta. The same is done and calculation for HVN and the hypothetical

company has been made. The return is calculated and it is derived to be 4.09% for the HVN

and 9.48% for the hypothetical company. It can be noted that the risk-free rate is a very low

level and with that, the beta of HVN is also low which provides with the lesser expected

returns. In comparison to this, the Hypothetical Company is making higher returns because

the beta of the same is at a high level of 1.60.

0 1 0.62 1.6

0

1

2

3

4

5

6

7

8

9

10

0.68

6.18

4.09

9.48

SML

CAPM

Beta

Return

The security market line is the line that represents the beta and the return which is made

under the capital asset pricing model. In the given case also there is the calculation of the

return with the help of CAPM and all of the returns which are made in respect of the risk-free

There is a negative impact as all the businesses are temporarily closed and the trading is not

taking place which is affecting the profitability and cash flow of the business. The economy

is declining as the returns are not available and that will affect the business and the market in

the long-term as heavy losses are being made.

In the business, there are various stocks that are involved and in which the investment is

made by people. All of them consider various aspects before making the decision and in that

most important are the return and risk associated with them. The return which is expected by

the shareholders is required to be identified as that forms the base for all the decisions. This is

required to be calculated and for that various approaches are available. In the current case,

there is the use of the capital asset pricing model which is considered to be most appropriate

(Gagliardini and Gouriéroux, 2013). The method considers the risk free rate which is

prevailing in the market and then adjusts the market premium according to the involved risk

with the help of beta. The same is done and calculation for HVN and the hypothetical

company has been made. The return is calculated and it is derived to be 4.09% for the HVN

and 9.48% for the hypothetical company. It can be noted that the risk-free rate is a very low

level and with that, the beta of HVN is also low which provides with the lesser expected

returns. In comparison to this, the Hypothetical Company is making higher returns because

the beta of the same is at a high level of 1.60.

0 1 0.62 1.6

0

1

2

3

4

5

6

7

8

9

10

0.68

6.18

4.09

9.48

SML

CAPM

Beta

Return

The security market line is the line that represents the beta and the return which is made

under the capital asset pricing model. In the given case also there is the calculation of the

return with the help of CAPM and all of the returns which are made in respect of the risk-free

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

asset, market and others are represented with the help of the graph. It can be noted that the

highest return is for the hypothetical company which is having a major risk. It shows the

relation between the risk and return and which demonstrates that with the higher risk there

will be more returns which will be earned. The risk-free asset is considered and in that the

beta is at zero as there is no risk which is involved. Due to this the return which is made on

the same is also limited to the risk-free rate and no other returns are available. Then the

market stock is taken into account with the beta of 1 which is perfect and in that situation, the

return which is available in the market is the total return which is made. There is a change in

the return corresponding to the change in the beta and this shows the relationships between

the risk and returns which is involved.

In the given case the two stocks are available which are for the company HVN and the

hypothetical company. In that, it can be noted that there is a higher risk under the

hypothetical company with the beta of 1.60 and HVN is having a beta of 0.62. There is a high

difference among them and due to that, the difference can also be noted in the return which is

made with the help of them. There is a higher return with the hypothetical stock and that is at

9.48% and the HVN is having a return of 4.09%. This shows that the company which is

having a higher beta is having a higher return and vice versa. The complete relationship can

be understood in an effective manner with the help of the calculation and the results that have

been derived.

According to this, the HVN is below the level of market premium which is involved at 5.50%

and this will be considered to be a negative factor for the same. The portfolio theory is

involved and according to that if the diversification is made then the risk which is involved in

the portfolio can be minimized (Teller, 2013). The risk which is involved in the company

comprises of two elements and they are systematic risk and unsystematic risk. The risk which

is due to unavoidable factors and that cannot be eliminated is considered as the systematic

risk and the remaining after this is an unsystematic risk. It is not possible for the company to

remove the systematic risk but the unsystematic can be reduced. This will be done with the

help of the creation of the portfolio by which the diversification will be made possible. In the

given case there is the portfolio that is designed with the HVN and hypothetical company.

The weights for the same have been decided and according to that HVN will comprise of

70% portion and the remaining 30% will be possessed by the hypothetical company.

asset, market and others are represented with the help of the graph. It can be noted that the

highest return is for the hypothetical company which is having a major risk. It shows the

relation between the risk and return and which demonstrates that with the higher risk there

will be more returns which will be earned. The risk-free asset is considered and in that the

beta is at zero as there is no risk which is involved. Due to this the return which is made on

the same is also limited to the risk-free rate and no other returns are available. Then the

market stock is taken into account with the beta of 1 which is perfect and in that situation, the

return which is available in the market is the total return which is made. There is a change in

the return corresponding to the change in the beta and this shows the relationships between

the risk and returns which is involved.

In the given case the two stocks are available which are for the company HVN and the

hypothetical company. In that, it can be noted that there is a higher risk under the

hypothetical company with the beta of 1.60 and HVN is having a beta of 0.62. There is a high

difference among them and due to that, the difference can also be noted in the return which is

made with the help of them. There is a higher return with the hypothetical stock and that is at

9.48% and the HVN is having a return of 4.09%. This shows that the company which is

having a higher beta is having a higher return and vice versa. The complete relationship can

be understood in an effective manner with the help of the calculation and the results that have

been derived.

According to this, the HVN is below the level of market premium which is involved at 5.50%

and this will be considered to be a negative factor for the same. The portfolio theory is

involved and according to that if the diversification is made then the risk which is involved in

the portfolio can be minimized (Teller, 2013). The risk which is involved in the company

comprises of two elements and they are systematic risk and unsystematic risk. The risk which

is due to unavoidable factors and that cannot be eliminated is considered as the systematic

risk and the remaining after this is an unsystematic risk. It is not possible for the company to

remove the systematic risk but the unsystematic can be reduced. This will be done with the

help of the creation of the portfolio by which the diversification will be made possible. In the

given case there is the portfolio that is designed with the HVN and hypothetical company.

The weights for the same have been decided and according to that HVN will comprise of

70% portion and the remaining 30% will be possessed by the hypothetical company.

6

The same has been considered and with the help of available information calculation for the

portfolio has been made. The expected return of the portfolio is ascertained and that is

derived at 5.71%. This is the rate that will be made by the portfolio and is higher than the

market premium. This is beneficial and can be considered. The portfolio beta is also

considered and as the higher share is of HVN with the lower beta so by that the risk is also

reduced. The portfolio beta is ascertained at 0.91 which comprises both the stocks (Capitaliq,

2020). The individual betas have been considered and to evaluate the beta it is defined that if

the beta is less than 1 then the stock is less risky and defensive whereas the beta of more than

1 reflects the higher risk and aggressive stock. The Beta for HVN has been identified to be

0.62 which is less than one and this shows that there is less risk which is involved with the

HVN and the investments which are made by it. The hypothetical company, on the other

hand, has a higher beta of 1.6 which shows its high level of aggressiveness and the risk that is

involved with making the investment in the same. It can be said with this that the more

investment will be made in a hypothetical company then the overall beta will be more and

there will be more risk which will be involved with the same.

The systematic risk is denoted with the help of beta and so in case of HVN the expected

return is 4.09% and the beta is 0.62 so in this, the 0.62 portions of the return will be the

systematic risk which will not be eliminated and rest is the unsystematic risk (Prather, 2012).

The same can be applied for the hypothetical company and in that the systematic risk is

denoted by 1.60 part of the expected return which is 9.48%. This shows that the systematic

risk is higher in the case of the hypothetical company and that will have to be borne by the

investor as there is no aspect by which it can be avoided. For the same evaluation the

portfolio return and beta are also calculated and they show the return of 5.71% and a beta of

0.91. The systematic risk in this will be up to the level of beta and after that, there will be an

unsystematic risk.

In the beta, there are the involvements of various elements such as operational and financial

risk. The risk which is related to the operational position of the business is considered as the

operational risk and that which is in relation to the financial leverage is the financial risk

(Hofman, Spalek and Grela, 2017). They both are important and shall be considered. from

this evaluation, it can be said that the portfolio will be of advantage as by this the risk is

brought to below 1 which shows that the portfolio will not be much aggressive and also the

return which is lower than the market premium for HVN is brought above them. This reflects

The same has been considered and with the help of available information calculation for the

portfolio has been made. The expected return of the portfolio is ascertained and that is

derived at 5.71%. This is the rate that will be made by the portfolio and is higher than the

market premium. This is beneficial and can be considered. The portfolio beta is also

considered and as the higher share is of HVN with the lower beta so by that the risk is also

reduced. The portfolio beta is ascertained at 0.91 which comprises both the stocks (Capitaliq,

2020). The individual betas have been considered and to evaluate the beta it is defined that if

the beta is less than 1 then the stock is less risky and defensive whereas the beta of more than

1 reflects the higher risk and aggressive stock. The Beta for HVN has been identified to be

0.62 which is less than one and this shows that there is less risk which is involved with the

HVN and the investments which are made by it. The hypothetical company, on the other

hand, has a higher beta of 1.6 which shows its high level of aggressiveness and the risk that is

involved with making the investment in the same. It can be said with this that the more

investment will be made in a hypothetical company then the overall beta will be more and

there will be more risk which will be involved with the same.

The systematic risk is denoted with the help of beta and so in case of HVN the expected

return is 4.09% and the beta is 0.62 so in this, the 0.62 portions of the return will be the

systematic risk which will not be eliminated and rest is the unsystematic risk (Prather, 2012).

The same can be applied for the hypothetical company and in that the systematic risk is

denoted by 1.60 part of the expected return which is 9.48%. This shows that the systematic

risk is higher in the case of the hypothetical company and that will have to be borne by the

investor as there is no aspect by which it can be avoided. For the same evaluation the

portfolio return and beta are also calculated and they show the return of 5.71% and a beta of

0.91. The systematic risk in this will be up to the level of beta and after that, there will be an

unsystematic risk.

In the beta, there are the involvements of various elements such as operational and financial

risk. The risk which is related to the operational position of the business is considered as the

operational risk and that which is in relation to the financial leverage is the financial risk

(Hofman, Spalek and Grela, 2017). They both are important and shall be considered. from

this evaluation, it can be said that the portfolio will be of advantage as by this the risk is

brought to below 1 which shows that the portfolio will not be much aggressive and also the

return which is lower than the market premium for HVN is brought above them. This reflects

7

the portfolio with moderate risk and return. Certain other factors will be considered and will

help in eliminating the risk further so the return can be increased.

the portfolio with moderate risk and return. Certain other factors will be considered and will

help in eliminating the risk further so the return can be increased.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

References

Capitaliq. (2020) Australia Government Debt Interest Rate Profile. [Online] Available at:

https://www.capitaliq.com/CIQDotNet/MacroEconomics/InterestRate.aspx?

companyId=50027527 [Accessed 13 April 2020]

Capitaliq. (2020) Harvey Norman Holdings Limited (ASX:HVN) Public Company Profile.

[Online] Available at: https://www.capitaliq.com/CIQDotNet/company.aspx?

companyId=6478902 [Accessed 13 April 2020]

Gagliardini, P. and Gouriéroux, C. (2013) Granularity adjustment for risk measures:

Systematic vs unsystematic risks. International journal of approximate reasoning, 54(6),

pp.717-747.

Hofman, M., Spalek, S. and Grela, G. (2017) Shedding new light on project portfolio risk

management. Sustainability, 9(10), p.1798.

Prather, L.J. (2012) Portfolio risk management implications of mutual fund investment

objective classifications. Journal of Financial Risk Management, 1(03), p.33.

Teller, J. (2013) Portfolio risk management and its contribution to project portfolio success:

An investigation of organization, process, and culture. Project Management Journal, 44(2),

pp.36-51.

References

Capitaliq. (2020) Australia Government Debt Interest Rate Profile. [Online] Available at:

https://www.capitaliq.com/CIQDotNet/MacroEconomics/InterestRate.aspx?

companyId=50027527 [Accessed 13 April 2020]

Capitaliq. (2020) Harvey Norman Holdings Limited (ASX:HVN) Public Company Profile.

[Online] Available at: https://www.capitaliq.com/CIQDotNet/company.aspx?

companyId=6478902 [Accessed 13 April 2020]

Gagliardini, P. and Gouriéroux, C. (2013) Granularity adjustment for risk measures:

Systematic vs unsystematic risks. International journal of approximate reasoning, 54(6),

pp.717-747.

Hofman, M., Spalek, S. and Grela, G. (2017) Shedding new light on project portfolio risk

management. Sustainability, 9(10), p.1798.

Prather, L.J. (2012) Portfolio risk management implications of mutual fund investment

objective classifications. Journal of Financial Risk Management, 1(03), p.33.

Teller, J. (2013) Portfolio risk management and its contribution to project portfolio success:

An investigation of organization, process, and culture. Project Management Journal, 44(2),

pp.36-51.

9

Appendix

Appendix

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.