Accounting and Finance AAF044-6: Capital Investment Decisions Report

VerifiedAdded on 2022/02/17

|16

|4393

|46

Report

AI Summary

This report delves into capital investment decisions, exploring both discounted and non-discounted cash flow techniques. It provides detailed explanations of methods such as Payback Period, Accounting Rate of Return, Net Present Value (NPV), Internal Rate of Return (IRR), Profitability Index, and Discounted Payback Period. The report also examines the benefits of budgeting and planning within organizations, highlighting advantages and limitations. Furthermore, it addresses the concept of corporate governance, outlining the roles of shareholders and the board of directors. The report uses BHP Group as a case study to illustrate financial challenges and decision-making. The report concludes with a comprehensive analysis of capital investment strategies and their implications for corporate financial health.

Accounting and Finance AAF044-6

Main Assignment - Two

SAIMA SADIA SHEFA

STUDENT ID: 2016948

Main Assignment - Two

SAIMA SADIA SHEFA

STUDENT ID: 2016948

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1.0 Introduction

2.0 Capital investment decisions techniques

2.1 Discounted cash flow techniques

2.1.1 PayBack Period

2.1.2 Accounting rate of return

2.2 Non-discounted cash flow techniques

2.2.1 Net Present Value

2..2.2 Internal rate of return

2.2.3 Profitability Index

2.2.4 Discounted Payback Period

3.0 Benefits of budgeting and planning in organizations

3.1 Advantages of Capital Budgeting

3.2 Limitations of Capital Budgeting

4.0 The Concept Of Corporate Governance

4.1 Role of Shareholders in Corporate Governance

4.2 Board of directors in Corporate Governance

4.2.1 Role of Board of directors .............................................................12

4.3 Comply & Explain ............................................................................13

5.0 Conclusion

6.0 References

1 | Accounting and Finance (AAF044-6) Main Assignment two

1.0 Introduction

2.0 Capital investment decisions techniques

2.1 Discounted cash flow techniques

2.1.1 PayBack Period

2.1.2 Accounting rate of return

2.2 Non-discounted cash flow techniques

2.2.1 Net Present Value

2..2.2 Internal rate of return

2.2.3 Profitability Index

2.2.4 Discounted Payback Period

3.0 Benefits of budgeting and planning in organizations

3.1 Advantages of Capital Budgeting

3.2 Limitations of Capital Budgeting

4.0 The Concept Of Corporate Governance

4.1 Role of Shareholders in Corporate Governance

4.2 Board of directors in Corporate Governance

4.2.1 Role of Board of directors .............................................................12

4.3 Comply & Explain ............................................................................13

5.0 Conclusion

6.0 References

1 | Accounting and Finance (AAF044-6) Main Assignment two

1. Introduction

BHP Group (formerly BHP Billiton) is the Australian public corporation

along with BHP Group Plc based in the UK, form the BHP Group. It is the

largest mining company in the world and Australia's most valuable

company for its market capitalization. BHP was incorporated in 1885,

while Billiton roots trace back to 1851. In 2001, Billiton merged with the

Broken Hill Proprietary Company (BHP) to form BHP Billiton.

Company core objectives are - creating sustainable value for its

shareholders, employees, contractors, suppliers, customers, business

partners and host communities.

The company produces Iron ore and nickel in Western Australia,

metallurgical (steel-making) and energy coal in Queensland and New

South Wales, and copper in South Australia. It also operates projects in

Canada, Chile, Peru, the United States, Colombia and Brazil to produces

copper, iron ore, coal and potash. Its petroleum business operates in Gulf

of Mexico, Australia and Trinidad & Tobago.

BHP is a multinational company with operations on six continents and

offices in more than 100 countries (Dick, 2007). Company’s Global

headquarters is in Melbourne, Australia and Corporate office based in

London, UK.

BHP Group is operating as a Dual Listed Company, with two parent

companies: BHP Group Limited, which is listed on the ASX and the New

York Stock Exchange (NYSE) under the symbol BHP, and BHP Group Plc,

which is listed on the London Stock Exchange and the Johannesburg Stock

Exchange under the symbol BHP and on the NYSE under the symbol BBL.

Company’s Financial Challenges

BHP operates globally and company's main mission is to create long-term

shareholder value for natural resources around the world. The company

has a track record of providing significant shareholder returns by heavily

investing in mining projects for a long time. Apart from serving the needs

of its customers and rising economies, the company is devoted to

protecting the communities in which it operates as well as the

environment (Thompson and Macklin 2009).

The company faces significant financial difficulties because of its recent

decision to postpone expansion plans for some of its key projects and had

to put billions of dollars on hold. The issue emerged after the company

joined its competitors in delaying expansion plans due to the global

financial crisis.

2 | Accounting and Finance (AAF044-6) Main Assignment two

BHP Group (formerly BHP Billiton) is the Australian public corporation

along with BHP Group Plc based in the UK, form the BHP Group. It is the

largest mining company in the world and Australia's most valuable

company for its market capitalization. BHP was incorporated in 1885,

while Billiton roots trace back to 1851. In 2001, Billiton merged with the

Broken Hill Proprietary Company (BHP) to form BHP Billiton.

Company core objectives are - creating sustainable value for its

shareholders, employees, contractors, suppliers, customers, business

partners and host communities.

The company produces Iron ore and nickel in Western Australia,

metallurgical (steel-making) and energy coal in Queensland and New

South Wales, and copper in South Australia. It also operates projects in

Canada, Chile, Peru, the United States, Colombia and Brazil to produces

copper, iron ore, coal and potash. Its petroleum business operates in Gulf

of Mexico, Australia and Trinidad & Tobago.

BHP is a multinational company with operations on six continents and

offices in more than 100 countries (Dick, 2007). Company’s Global

headquarters is in Melbourne, Australia and Corporate office based in

London, UK.

BHP Group is operating as a Dual Listed Company, with two parent

companies: BHP Group Limited, which is listed on the ASX and the New

York Stock Exchange (NYSE) under the symbol BHP, and BHP Group Plc,

which is listed on the London Stock Exchange and the Johannesburg Stock

Exchange under the symbol BHP and on the NYSE under the symbol BBL.

Company’s Financial Challenges

BHP operates globally and company's main mission is to create long-term

shareholder value for natural resources around the world. The company

has a track record of providing significant shareholder returns by heavily

investing in mining projects for a long time. Apart from serving the needs

of its customers and rising economies, the company is devoted to

protecting the communities in which it operates as well as the

environment (Thompson and Macklin 2009).

The company faces significant financial difficulties because of its recent

decision to postpone expansion plans for some of its key projects and had

to put billions of dollars on hold. The issue emerged after the company

joined its competitors in delaying expansion plans due to the global

financial crisis.

2 | Accounting and Finance (AAF044-6) Main Assignment two

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Another strategy for overcoming these challenges is to reduce income-

expenditure and real wages. The company also chose to decrease prices

in order to manage commodity prices, which worsened the situation.

2.0 Capital investment decisions techniques

Companies across the world expand by launching new initiatives and

making investments in various industries and areas. The research and

subsequent appraisal of these initiatives mainly based on economic, cost,

and financial data. Investment appraisal techniques helps managers in

determining the financial sustainability of individual projects as well as

making decisions such as the purchase of land, machinery, buildings, or

equipment etc.

Feasibility of any project or decisions making process usually done by

using different techniques and each technique assesses the project from a

different perspective and delivers a different insight. These techniques

can be classified into two parts:

Non-discounted cash flow techniques.

Discounted cash flow techniques.

2.1 Non-Discounted cash flow techniques

This is the traditional method and it does not consider the time value of

money. To put it another way, all future dollars are presumed to have the

same value as today's money. Non-discounted cash flow strategies

include the following two techniques:

Payback period

Accounting rate of return

3 | Accounting and Finance (AAF044-6) Main Assignment two

expenditure and real wages. The company also chose to decrease prices

in order to manage commodity prices, which worsened the situation.

2.0 Capital investment decisions techniques

Companies across the world expand by launching new initiatives and

making investments in various industries and areas. The research and

subsequent appraisal of these initiatives mainly based on economic, cost,

and financial data. Investment appraisal techniques helps managers in

determining the financial sustainability of individual projects as well as

making decisions such as the purchase of land, machinery, buildings, or

equipment etc.

Feasibility of any project or decisions making process usually done by

using different techniques and each technique assesses the project from a

different perspective and delivers a different insight. These techniques

can be classified into two parts:

Non-discounted cash flow techniques.

Discounted cash flow techniques.

2.1 Non-Discounted cash flow techniques

This is the traditional method and it does not consider the time value of

money. To put it another way, all future dollars are presumed to have the

same value as today's money. Non-discounted cash flow strategies

include the following two techniques:

Payback period

Accounting rate of return

3 | Accounting and Finance (AAF044-6) Main Assignment two

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

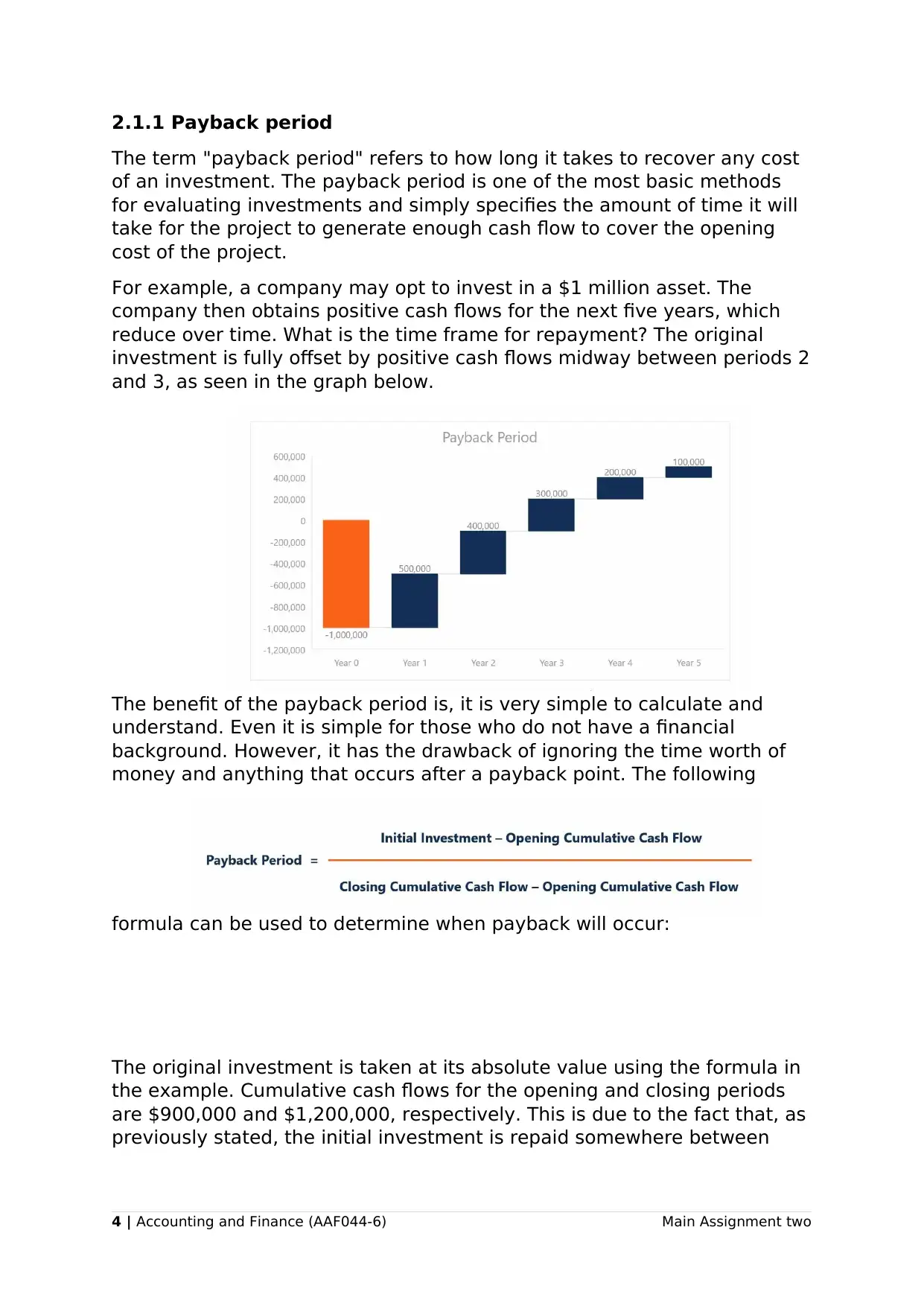

2.1.1 Payback period

The term "payback period" refers to how long it takes to recover any cost

of an investment. The payback period is one of the most basic methods

for evaluating investments and simply specifies the amount of time it will

take for the project to generate enough cash flow to cover the opening

cost of the project.

For example, a company may opt to invest in a $1 million asset. The

company then obtains positive cash flows for the next five years, which

reduce over time. What is the time frame for repayment? The original

investment is fully offset by positive cash flows midway between periods 2

and 3, as seen in the graph below.

The benefit of the payback period is, it is very simple to calculate and

understand. Even it is simple for those who do not have a financial

background. However, it has the drawback of ignoring the time worth of

money and anything that occurs after a payback point. The following

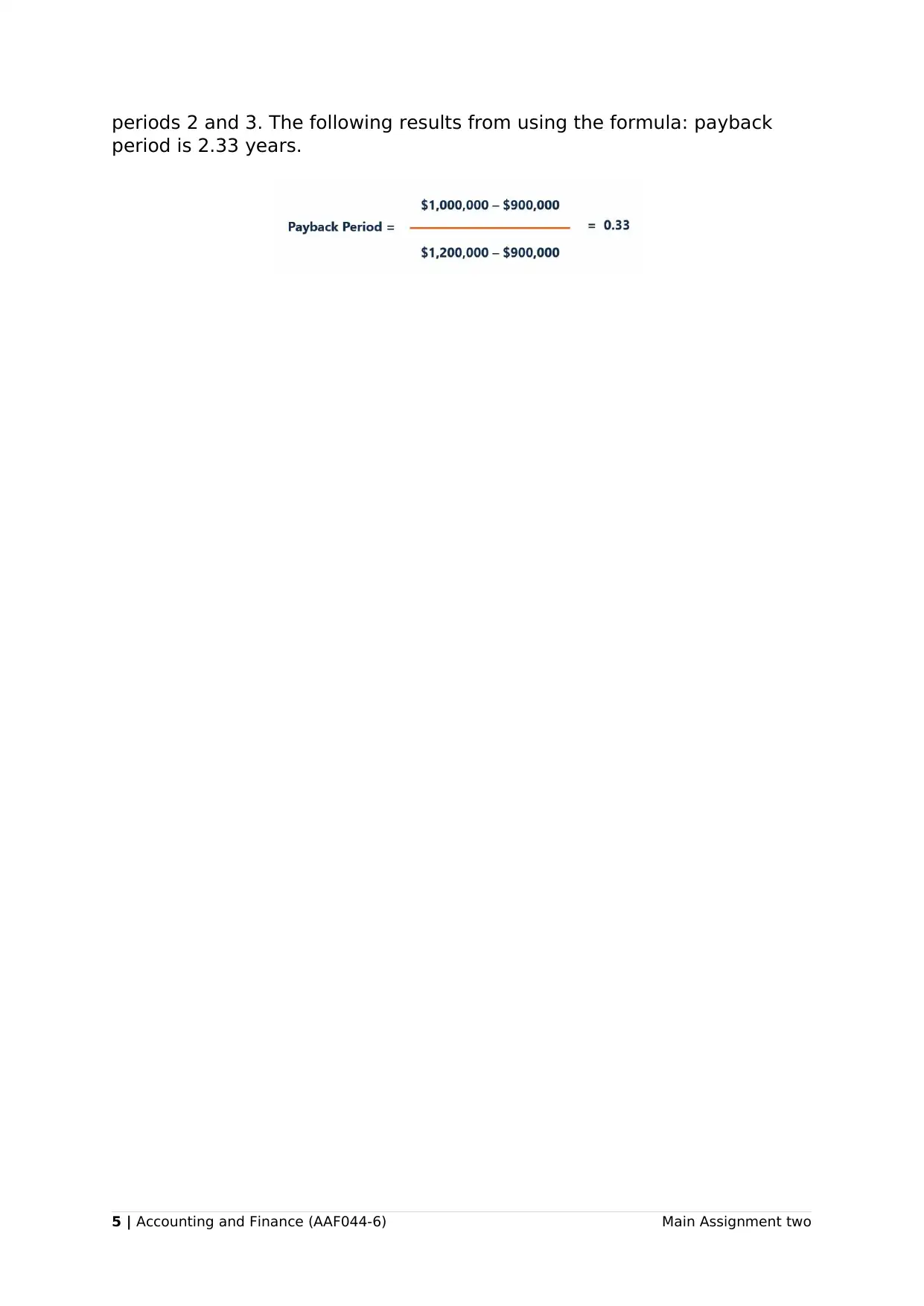

formula can be used to determine when payback will occur:

The original investment is taken at its absolute value using the formula in

the example. Cumulative cash flows for the opening and closing periods

are $900,000 and $1,200,000, respectively. This is due to the fact that, as

previously stated, the initial investment is repaid somewhere between

4 | Accounting and Finance (AAF044-6) Main Assignment two

The term "payback period" refers to how long it takes to recover any cost

of an investment. The payback period is one of the most basic methods

for evaluating investments and simply specifies the amount of time it will

take for the project to generate enough cash flow to cover the opening

cost of the project.

For example, a company may opt to invest in a $1 million asset. The

company then obtains positive cash flows for the next five years, which

reduce over time. What is the time frame for repayment? The original

investment is fully offset by positive cash flows midway between periods 2

and 3, as seen in the graph below.

The benefit of the payback period is, it is very simple to calculate and

understand. Even it is simple for those who do not have a financial

background. However, it has the drawback of ignoring the time worth of

money and anything that occurs after a payback point. The following

formula can be used to determine when payback will occur:

The original investment is taken at its absolute value using the formula in

the example. Cumulative cash flows for the opening and closing periods

are $900,000 and $1,200,000, respectively. This is due to the fact that, as

previously stated, the initial investment is repaid somewhere between

4 | Accounting and Finance (AAF044-6) Main Assignment two

periods 2 and 3. The following results from using the formula: payback

period is 2.33 years.

5 | Accounting and Finance (AAF044-6) Main Assignment two

period is 2.33 years.

5 | Accounting and Finance (AAF044-6) Main Assignment two

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.1.2 Accounting rate of return

The accounting rate of return (ARR) is a capital budgeting ratio that

calculates the projected return on an investment in relation to the starting

cost. It represents the investment's net accounting profit as a proportion

of the capital investment. It's also referred to as return on capital or return

on investment. (Corporate Finance Institute, n.d.)

It is used when a company is selecting whether or not to invest in an asset

(a project, an acquisition, etc.) based on the predicted future net earnings

vs the capital cost.

The formula for ARR is:

ARR = Average Annual Profit / Average Investment

Where:

Average Annual Profit = Total profit over Investment Period /

Number of Years

Average Investment = (Book Value at Year 1 + Book Value at End

of Useful Life) / 2

For Example:

XYZ Inc. is looking to replace its present faulty machinery with new

equipment. The new machine, which costs $ 420,000, would bring in $

200,000 in yearly revenue and $ 50,000 in annual expenses. The

machine's useful life is anticipated to be 12 years.

Step 1: Calculate Average Annual Profit

Inflows, Years 1-12: (200,000*12) $2,400,000

Less: Annual Expenses: (50,000*12) -$600,000

Less: Depreciation -$420,000

Total Profit $1,380,000

Average Annual Profit (1,380,000/12) $115,000

Step 2: Calculate Average Investment

Average Investment ($420,000 + $0)/2 = $210,000

Step 3: Use ARR Formula

ARR = $115,000/$210,000 = 54.76%

Therefore, every dollar of investment will return a profit of around 54.76

cents.

2.2 Discounted cash flow techniques

6 | Accounting and Finance (AAF044-6) Main Assignment two

The accounting rate of return (ARR) is a capital budgeting ratio that

calculates the projected return on an investment in relation to the starting

cost. It represents the investment's net accounting profit as a proportion

of the capital investment. It's also referred to as return on capital or return

on investment. (Corporate Finance Institute, n.d.)

It is used when a company is selecting whether or not to invest in an asset

(a project, an acquisition, etc.) based on the predicted future net earnings

vs the capital cost.

The formula for ARR is:

ARR = Average Annual Profit / Average Investment

Where:

Average Annual Profit = Total profit over Investment Period /

Number of Years

Average Investment = (Book Value at Year 1 + Book Value at End

of Useful Life) / 2

For Example:

XYZ Inc. is looking to replace its present faulty machinery with new

equipment. The new machine, which costs $ 420,000, would bring in $

200,000 in yearly revenue and $ 50,000 in annual expenses. The

machine's useful life is anticipated to be 12 years.

Step 1: Calculate Average Annual Profit

Inflows, Years 1-12: (200,000*12) $2,400,000

Less: Annual Expenses: (50,000*12) -$600,000

Less: Depreciation -$420,000

Total Profit $1,380,000

Average Annual Profit (1,380,000/12) $115,000

Step 2: Calculate Average Investment

Average Investment ($420,000 + $0)/2 = $210,000

Step 3: Use ARR Formula

ARR = $115,000/$210,000 = 54.76%

Therefore, every dollar of investment will return a profit of around 54.76

cents.

2.2 Discounted cash flow techniques

6 | Accounting and Finance (AAF044-6) Main Assignment two

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is the method for reflecting the time value of money by discounting

future cash flows to the present. DCF analysis aims to determine the

current value of an investment based on forecasts of future earnings and

applies to decisions made by investors in firms or securities, such as

acquiring a company or purchasing a stock, as well as decisions made by

business owners and managers on capital budgeting and operating

expenses. (Corporate Finance Institute, n.d.) Discounted cash flow

techniques include the following:

Net present value

Internal rate of return

Profitability index

Discounted payback period

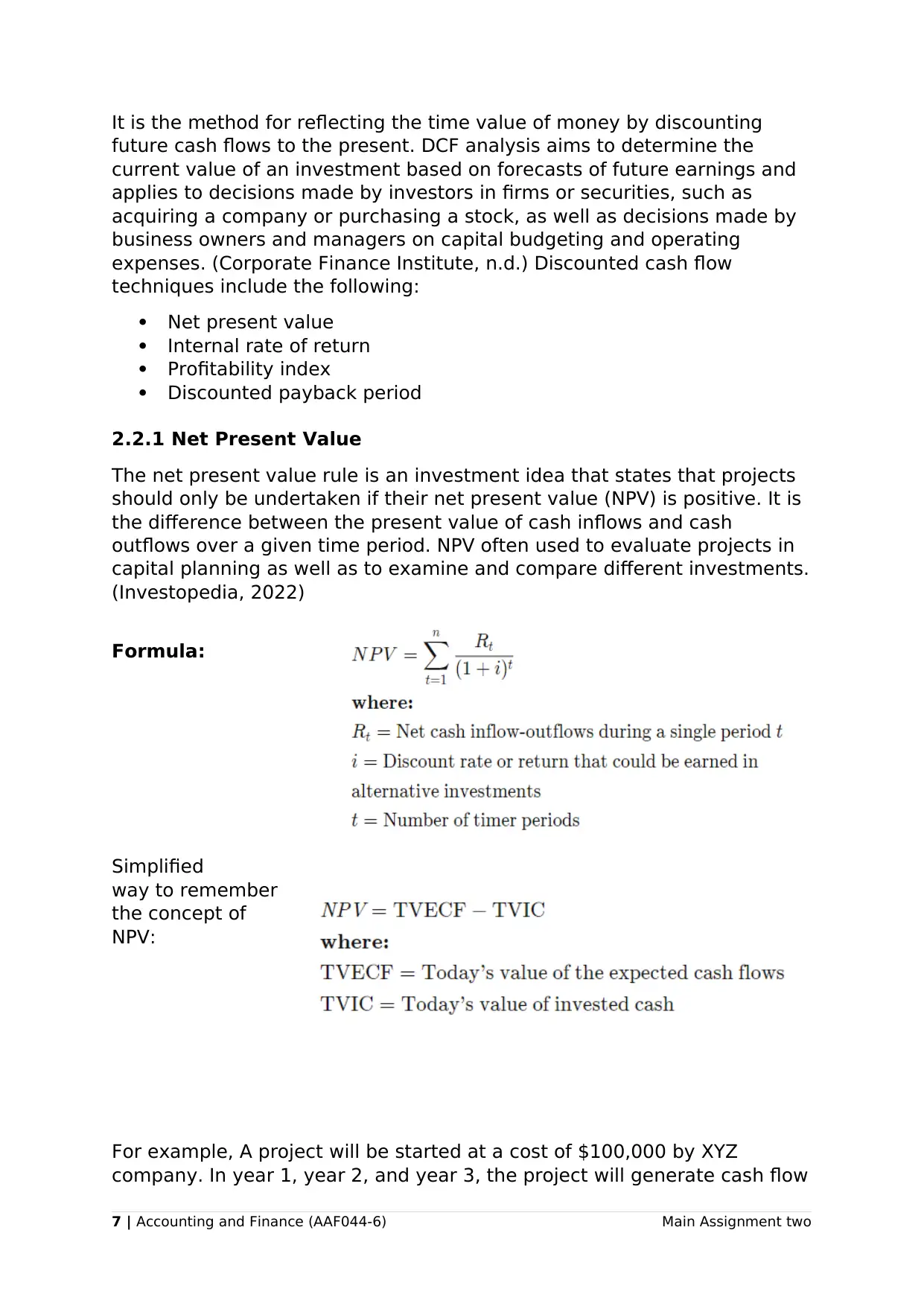

2.2.1 Net Present Value

The net present value rule is an investment idea that states that projects

should only be undertaken if their net present value (NPV) is positive. It is

the difference between the present value of cash inflows and cash

outflows over a given time period. NPV often used to evaluate projects in

capital planning as well as to examine and compare different investments.

(Investopedia, 2022)

Formula:

Simplified

way to remember

the concept of

NPV:

For example, A project will be started at a cost of $100,000 by XYZ

company. In year 1, year 2, and year 3, the project will generate cash flow

7 | Accounting and Finance (AAF044-6) Main Assignment two

future cash flows to the present. DCF analysis aims to determine the

current value of an investment based on forecasts of future earnings and

applies to decisions made by investors in firms or securities, such as

acquiring a company or purchasing a stock, as well as decisions made by

business owners and managers on capital budgeting and operating

expenses. (Corporate Finance Institute, n.d.) Discounted cash flow

techniques include the following:

Net present value

Internal rate of return

Profitability index

Discounted payback period

2.2.1 Net Present Value

The net present value rule is an investment idea that states that projects

should only be undertaken if their net present value (NPV) is positive. It is

the difference between the present value of cash inflows and cash

outflows over a given time period. NPV often used to evaluate projects in

capital planning as well as to examine and compare different investments.

(Investopedia, 2022)

Formula:

Simplified

way to remember

the concept of

NPV:

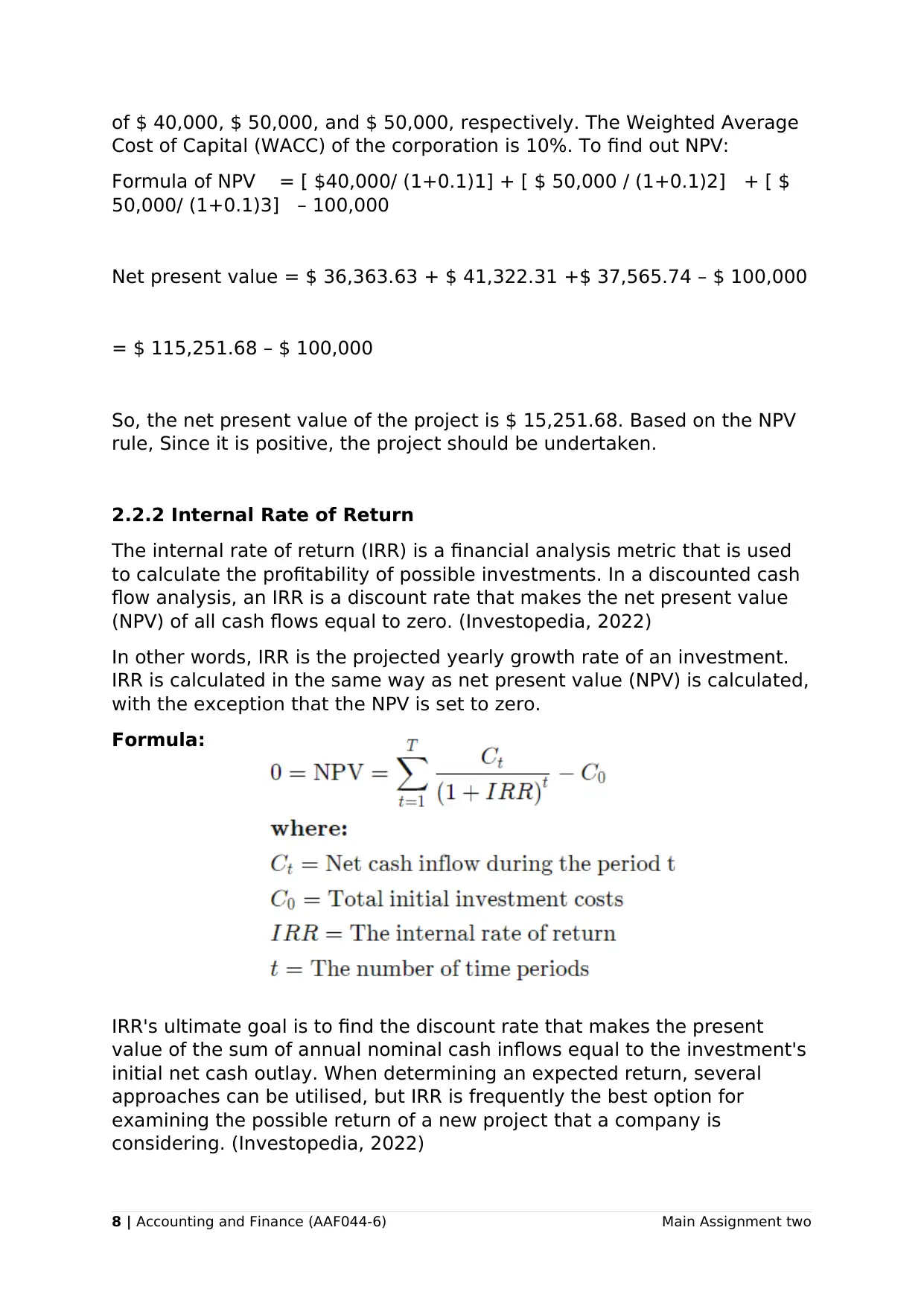

For example, A project will be started at a cost of $100,000 by XYZ

company. In year 1, year 2, and year 3, the project will generate cash flow

7 | Accounting and Finance (AAF044-6) Main Assignment two

of $ 40,000, $ 50,000, and $ 50,000, respectively. The Weighted Average

Cost of Capital (WACC) of the corporation is 10%. To find out NPV:

Formula of NPV = [ $40,000/ (1+0.1)1] + [ $ 50,000 / (1+0.1)2] + [ $

50,000/ (1+0.1)3] – 100,000

Net present value = $ 36,363.63 + $ 41,322.31 +$ 37,565.74 – $ 100,000

= $ 115,251.68 – $ 100,000

So, the net present value of the project is $ 15,251.68. Based on the NPV

rule, Since it is positive, the project should be undertaken.

2.2.2 Internal Rate of Return

The internal rate of return (IRR) is a financial analysis metric that is used

to calculate the profitability of possible investments. In a discounted cash

flow analysis, an IRR is a discount rate that makes the net present value

(NPV) of all cash flows equal to zero. (Investopedia, 2022)

In other words, IRR is the projected yearly growth rate of an investment.

IRR is calculated in the same way as net present value (NPV) is calculated,

with the exception that the NPV is set to zero.

Formula:

IRR's ultimate goal is to find the discount rate that makes the present

value of the sum of annual nominal cash inflows equal to the investment's

initial net cash outlay. When determining an expected return, several

approaches can be utilised, but IRR is frequently the best option for

examining the possible return of a new project that a company is

considering. (Investopedia, 2022)

8 | Accounting and Finance (AAF044-6) Main Assignment two

Cost of Capital (WACC) of the corporation is 10%. To find out NPV:

Formula of NPV = [ $40,000/ (1+0.1)1] + [ $ 50,000 / (1+0.1)2] + [ $

50,000/ (1+0.1)3] – 100,000

Net present value = $ 36,363.63 + $ 41,322.31 +$ 37,565.74 – $ 100,000

= $ 115,251.68 – $ 100,000

So, the net present value of the project is $ 15,251.68. Based on the NPV

rule, Since it is positive, the project should be undertaken.

2.2.2 Internal Rate of Return

The internal rate of return (IRR) is a financial analysis metric that is used

to calculate the profitability of possible investments. In a discounted cash

flow analysis, an IRR is a discount rate that makes the net present value

(NPV) of all cash flows equal to zero. (Investopedia, 2022)

In other words, IRR is the projected yearly growth rate of an investment.

IRR is calculated in the same way as net present value (NPV) is calculated,

with the exception that the NPV is set to zero.

Formula:

IRR's ultimate goal is to find the discount rate that makes the present

value of the sum of annual nominal cash inflows equal to the investment's

initial net cash outlay. When determining an expected return, several

approaches can be utilised, but IRR is frequently the best option for

examining the possible return of a new project that a company is

considering. (Investopedia, 2022)

8 | Accounting and Finance (AAF044-6) Main Assignment two

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

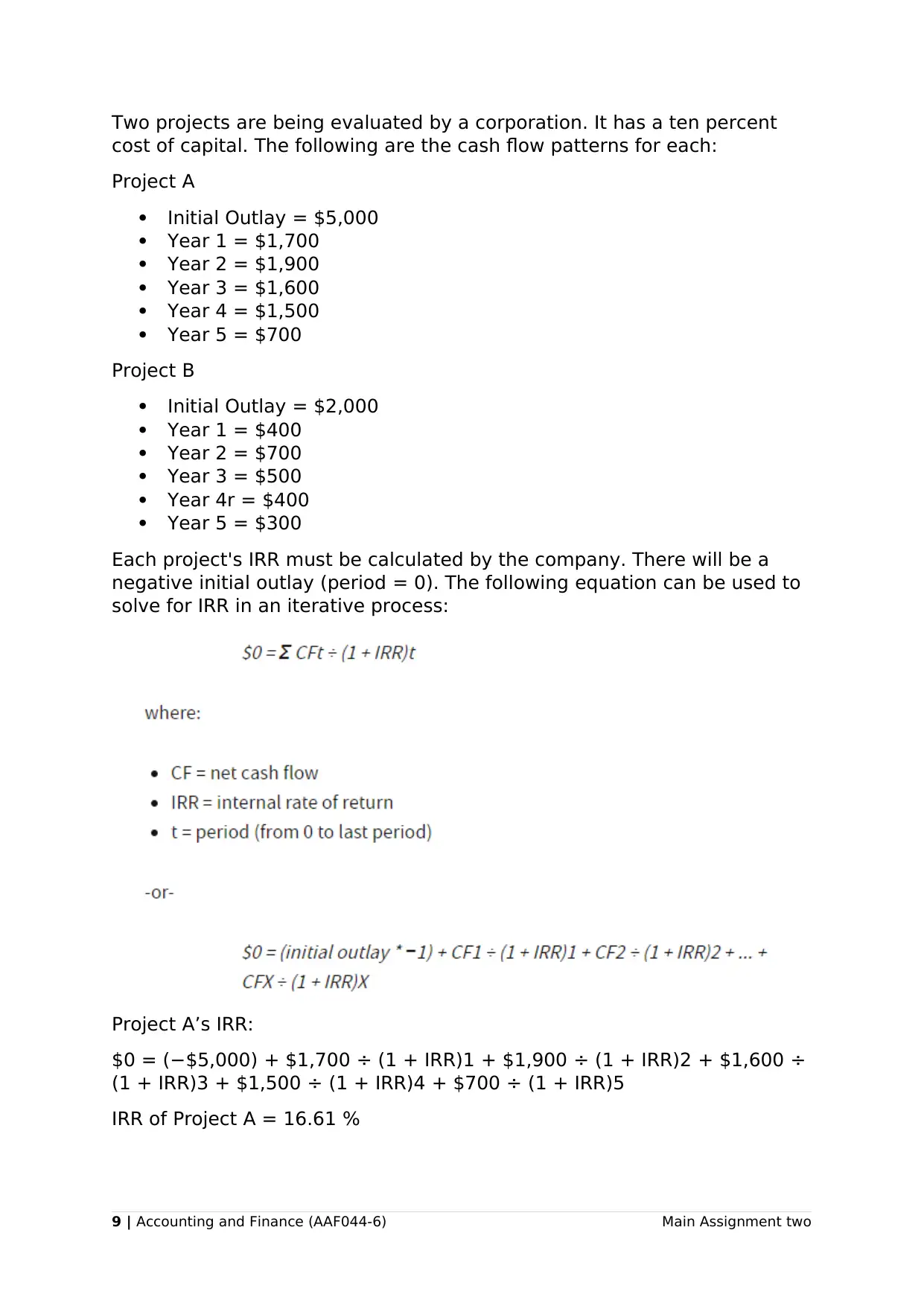

Two projects are being evaluated by a corporation. It has a ten percent

cost of capital. The following are the cash flow patterns for each:

Project A

Initial Outlay = $5,000

Year 1 = $1,700

Year 2 = $1,900

Year 3 = $1,600

Year 4 = $1,500

Year 5 = $700

Project B

Initial Outlay = $2,000

Year 1 = $400

Year 2 = $700

Year 3 = $500

Year 4r = $400

Year 5 = $300

Each project's IRR must be calculated by the company. There will be a

negative initial outlay (period = 0). The following equation can be used to

solve for IRR in an iterative process:

Project A’s IRR:

$0 = (−$5,000) + $1,700 ÷ (1 + IRR)1 + $1,900 ÷ (1 + IRR)2 + $1,600 ÷

(1 + IRR)3 + $1,500 ÷ (1 + IRR)4 + $700 ÷ (1 + IRR)5

IRR of Project A = 16.61 %

9 | Accounting and Finance (AAF044-6) Main Assignment two

cost of capital. The following are the cash flow patterns for each:

Project A

Initial Outlay = $5,000

Year 1 = $1,700

Year 2 = $1,900

Year 3 = $1,600

Year 4 = $1,500

Year 5 = $700

Project B

Initial Outlay = $2,000

Year 1 = $400

Year 2 = $700

Year 3 = $500

Year 4r = $400

Year 5 = $300

Each project's IRR must be calculated by the company. There will be a

negative initial outlay (period = 0). The following equation can be used to

solve for IRR in an iterative process:

Project A’s IRR:

$0 = (−$5,000) + $1,700 ÷ (1 + IRR)1 + $1,900 ÷ (1 + IRR)2 + $1,600 ÷

(1 + IRR)3 + $1,500 ÷ (1 + IRR)4 + $700 ÷ (1 + IRR)5

IRR of Project A = 16.61 %

9 | Accounting and Finance (AAF044-6) Main Assignment two

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Project B’s IRR:

$0 = (−$2,000) + $400 ÷ (1 + IRR)1 + $700 ÷ (1 + IRR)2 + $500 ÷ (1 +

IRR)3 + $400 ÷ (1 + IRR)4 + $300 ÷ (1 + IRR)5

IRR of Project B = 5.23 %

Management should proceed with Project A and reject Project B because

the company's cost of capital is 10%.

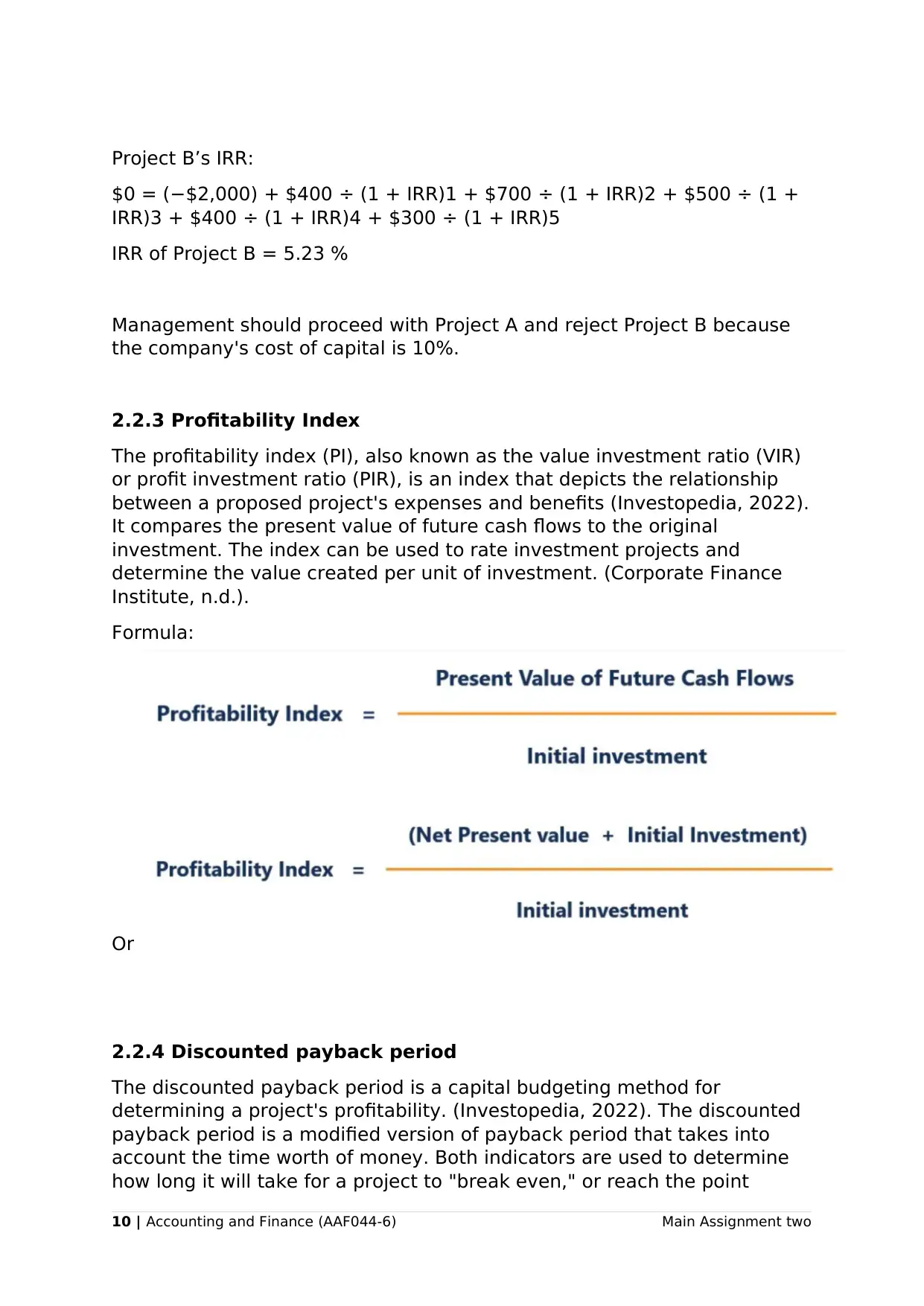

2.2.3 Profitability Index

The profitability index (PI), also known as the value investment ratio (VIR)

or profit investment ratio (PIR), is an index that depicts the relationship

between a proposed project's expenses and benefits (Investopedia, 2022).

It compares the present value of future cash flows to the original

investment. The index can be used to rate investment projects and

determine the value created per unit of investment. (Corporate Finance

Institute, n.d.).

Formula:

Or

2.2.4 Discounted payback period

The discounted payback period is a capital budgeting method for

determining a project's profitability. (Investopedia, 2022). The discounted

payback period is a modified version of payback period that takes into

account the time worth of money. Both indicators are used to determine

how long it will take for a project to "break even," or reach the point

10 | Accounting and Finance (AAF044-6) Main Assignment two

$0 = (−$2,000) + $400 ÷ (1 + IRR)1 + $700 ÷ (1 + IRR)2 + $500 ÷ (1 +

IRR)3 + $400 ÷ (1 + IRR)4 + $300 ÷ (1 + IRR)5

IRR of Project B = 5.23 %

Management should proceed with Project A and reject Project B because

the company's cost of capital is 10%.

2.2.3 Profitability Index

The profitability index (PI), also known as the value investment ratio (VIR)

or profit investment ratio (PIR), is an index that depicts the relationship

between a proposed project's expenses and benefits (Investopedia, 2022).

It compares the present value of future cash flows to the original

investment. The index can be used to rate investment projects and

determine the value created per unit of investment. (Corporate Finance

Institute, n.d.).

Formula:

Or

2.2.4 Discounted payback period

The discounted payback period is a capital budgeting method for

determining a project's profitability. (Investopedia, 2022). The discounted

payback period is a modified version of payback period that takes into

account the time worth of money. Both indicators are used to determine

how long it will take for a project to "break even," or reach the point

10 | Accounting and Finance (AAF044-6) Main Assignment two

where the net cash flows generated exceed the project's starting cost.

(Corporate Finance Institute, n.d.)

3.0 Benefits of budgeting and planning in organizations

A budget is an estimate of future revenues and expenses that aids in the

planning of future expenses or resource allocation for a specific period. A

corporate budget is based on a set of assumptions and is in line with the

company's business strategy and goals. (Corporate Finance Institute, n.d.)

Capital budgeting (also called investment appraisal) is the most significant

tool in corporate finance for determining whether or not a company's

long-term investments are worthwhile. As stated in Corporate Finance by

Ehrhardt and Brigham, capital implies long-term assets that are utilized in

production and a budget is a plan that outlines anticipated expenditures

during a coming period (p 381). Forecasting and identifying cash flows,

performing scenario and sensitivity analysis, and using capital budgeting

tools are all part of the capital budgeting process. (Kwok & Rabe, 2010).

Capital budgeting is critical for manufacturing businesses of all sizes. Any

company that invests in a project without considering the risks and

rewards will lose money and have no chance of surviving in a competitive

market. Capital budgeting decisions helps in the making of two important

decisions: financial decisions and investment decisions.

3.1 Advantages of Capital Budgeting

It provides adequate project spending control.

It helps organisation to refrain from over investing and under-

investing.

Helps a company to understand the numerous risks associated with

an investment opportunity and how these risks affect the company's

returns.

A company can choose from a variety of capital budgeting

approaches and methods to determine whether or not a project is

financially viable.

All capital budgeting techniques/methods aim to generate

shareholder wealth and offer the organisation a competitive

advantage.

3.2 Limitations of Capital Budgeting

A poor capital budgeting decision might jeopardise the company's

long-term viability, thus it must be handled with care by

professionals who are familiar with the project.

11 | Accounting and Finance (AAF044-6) Main Assignment two

(Corporate Finance Institute, n.d.)

3.0 Benefits of budgeting and planning in organizations

A budget is an estimate of future revenues and expenses that aids in the

planning of future expenses or resource allocation for a specific period. A

corporate budget is based on a set of assumptions and is in line with the

company's business strategy and goals. (Corporate Finance Institute, n.d.)

Capital budgeting (also called investment appraisal) is the most significant

tool in corporate finance for determining whether or not a company's

long-term investments are worthwhile. As stated in Corporate Finance by

Ehrhardt and Brigham, capital implies long-term assets that are utilized in

production and a budget is a plan that outlines anticipated expenditures

during a coming period (p 381). Forecasting and identifying cash flows,

performing scenario and sensitivity analysis, and using capital budgeting

tools are all part of the capital budgeting process. (Kwok & Rabe, 2010).

Capital budgeting is critical for manufacturing businesses of all sizes. Any

company that invests in a project without considering the risks and

rewards will lose money and have no chance of surviving in a competitive

market. Capital budgeting decisions helps in the making of two important

decisions: financial decisions and investment decisions.

3.1 Advantages of Capital Budgeting

It provides adequate project spending control.

It helps organisation to refrain from over investing and under-

investing.

Helps a company to understand the numerous risks associated with

an investment opportunity and how these risks affect the company's

returns.

A company can choose from a variety of capital budgeting

approaches and methods to determine whether or not a project is

financially viable.

All capital budgeting techniques/methods aim to generate

shareholder wealth and offer the organisation a competitive

advantage.

3.2 Limitations of Capital Budgeting

A poor capital budgeting decision might jeopardise the company's

long-term viability, thus it must be handled with care by

professionals who are familiar with the project.

11 | Accounting and Finance (AAF044-6) Main Assignment two

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.