Financial Ratio Analysis, Ethical Considerations, and System Adoption

VerifiedAdded on 2020/04/01

|9

|3280

|38

Homework Assignment

AI Summary

This assignment solution addresses key concepts in accounting for managers, focusing on financial ratio analysis, ethical dilemmas, and system implementation. The first part of the solution involves a detailed analysis of financial ratios, including liquidity, profitability, efficiency, and solvency ratios, with calculations and interpretations for three consecutive years. The second part delves into an ethical dilemma faced by an accountant, exploring the importance of ethical behavior and the consequences of financial reporting decisions. The third part examines the adoption of a computerized accounting system and the Just-In-Time (JIT) inventory strategy to improve operational efficiency and financial performance. The solution provides a comprehensive overview of these critical areas in accounting, offering practical insights and recommendations for effective financial management.

ACCOUNTING FOR MANAGERS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

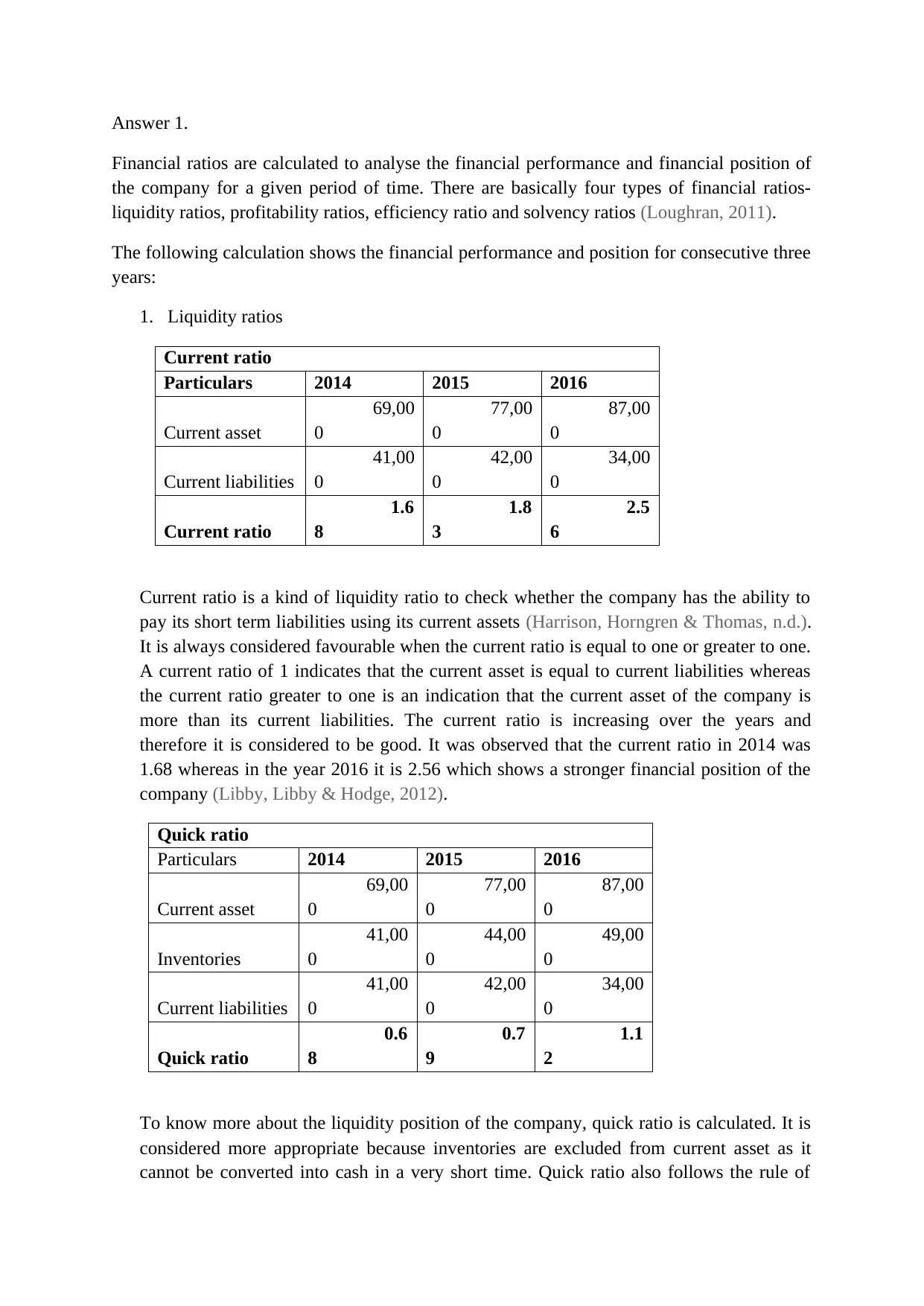

Answer 1.

Financial ratios are calculated to analyse the financial performance and financial position of

the company for a given period of time. There are basically four types of financial ratios-

liquidity ratios, profitability ratios, efficiency ratio and solvency ratios (Loughran, 2011).

The following calculation shows the financial performance and position for consecutive three

years:

1. Liquidity ratios

Current ratio

Particulars 2014 2015 2016

Current asset

69,00

0

77,00

0

87,00

0

Current liabilities

41,00

0

42,00

0

34,00

0

Current ratio

1.6

8

1.8

3

2.5

6

Current ratio is a kind of liquidity ratio to check whether the company has the ability to

pay its short term liabilities using its current assets (Harrison, Horngren & Thomas, n.d.).

It is always considered favourable when the current ratio is equal to one or greater to one.

A current ratio of 1 indicates that the current asset is equal to current liabilities whereas

the current ratio greater to one is an indication that the current asset of the company is

more than its current liabilities. The current ratio is increasing over the years and

therefore it is considered to be good. It was observed that the current ratio in 2014 was

1.68 whereas in the year 2016 it is 2.56 which shows a stronger financial position of the

company (Libby, Libby & Hodge, 2012).

Quick ratio

Particulars 2014 2015 2016

Current asset

69,00

0

77,00

0

87,00

0

Inventories

41,00

0

44,00

0

49,00

0

Current liabilities

41,00

0

42,00

0

34,00

0

Quick ratio

0.6

8

0.7

9

1.1

2

To know more about the liquidity position of the company, quick ratio is calculated. It is

considered more appropriate because inventories are excluded from current asset as it

cannot be converted into cash in a very short time. Quick ratio also follows the rule of

Financial ratios are calculated to analyse the financial performance and financial position of

the company for a given period of time. There are basically four types of financial ratios-

liquidity ratios, profitability ratios, efficiency ratio and solvency ratios (Loughran, 2011).

The following calculation shows the financial performance and position for consecutive three

years:

1. Liquidity ratios

Current ratio

Particulars 2014 2015 2016

Current asset

69,00

0

77,00

0

87,00

0

Current liabilities

41,00

0

42,00

0

34,00

0

Current ratio

1.6

8

1.8

3

2.5

6

Current ratio is a kind of liquidity ratio to check whether the company has the ability to

pay its short term liabilities using its current assets (Harrison, Horngren & Thomas, n.d.).

It is always considered favourable when the current ratio is equal to one or greater to one.

A current ratio of 1 indicates that the current asset is equal to current liabilities whereas

the current ratio greater to one is an indication that the current asset of the company is

more than its current liabilities. The current ratio is increasing over the years and

therefore it is considered to be good. It was observed that the current ratio in 2014 was

1.68 whereas in the year 2016 it is 2.56 which shows a stronger financial position of the

company (Libby, Libby & Hodge, 2012).

Quick ratio

Particulars 2014 2015 2016

Current asset

69,00

0

77,00

0

87,00

0

Inventories

41,00

0

44,00

0

49,00

0

Current liabilities

41,00

0

42,00

0

34,00

0

Quick ratio

0.6

8

0.7

9

1.1

2

To know more about the liquidity position of the company, quick ratio is calculated. It is

considered more appropriate because inventories are excluded from current asset as it

cannot be converted into cash in a very short time. Quick ratio also follows the rule of

higher the better, it has also increased over the years. Overall we can comment that the

liquidity position of the company is quite good (Spiceland, Thomas & Herrmann, 2010).

2. Profitability ratio.

Operating profit margin

Particulars 2014 2015 2016

Operating profit

20,

000

11,

000

3,

500

Sales

2,00,0

00

1,80,0

00

1,65,

000

Operating profit margin

ratio 10% 6% 2%

The main motive of every company is to earn profits. If the company’s financial

performance is not good it is expected that it will not survive in the long run. Therefore,

in order to see the expected survival of the company operating margin ratio is calculated.

It has been seen that the operating profit margin is falling over the years which is adverse.

Therefore, we can conclude that there is a decline in the financial performance of the

company (Kimmel, Weygandt & Kieso, 2012).

3.Efficiency ratio.

The most important financial ratio that helps to analyse the financial position of the

company is called efficiency ratio. Efficiency is based on the assets and liabilities of the

company which reflects a true picture of financial position of the company. The data used in

the calculation of efficiency ratio is usually taken from the balance sheet of the company.

The few efficiency ratios that are calculated by me are inventory turnover ratio, total asset

turnover ratio, fixed asset turnover ratio, return on asset and return on equity ratio

(Weygandt, Kimmel & Kieso, n.d.).

Inventory turnover ratio

Particulars 2014 2015 2016

Sales

2,00,0

00

1,80,0

00

1,65,0

00

Inventories

41,0

00

44,0

00

49,0

00

Inventory turnover

ratio

4

.88

4

.09

3

.37

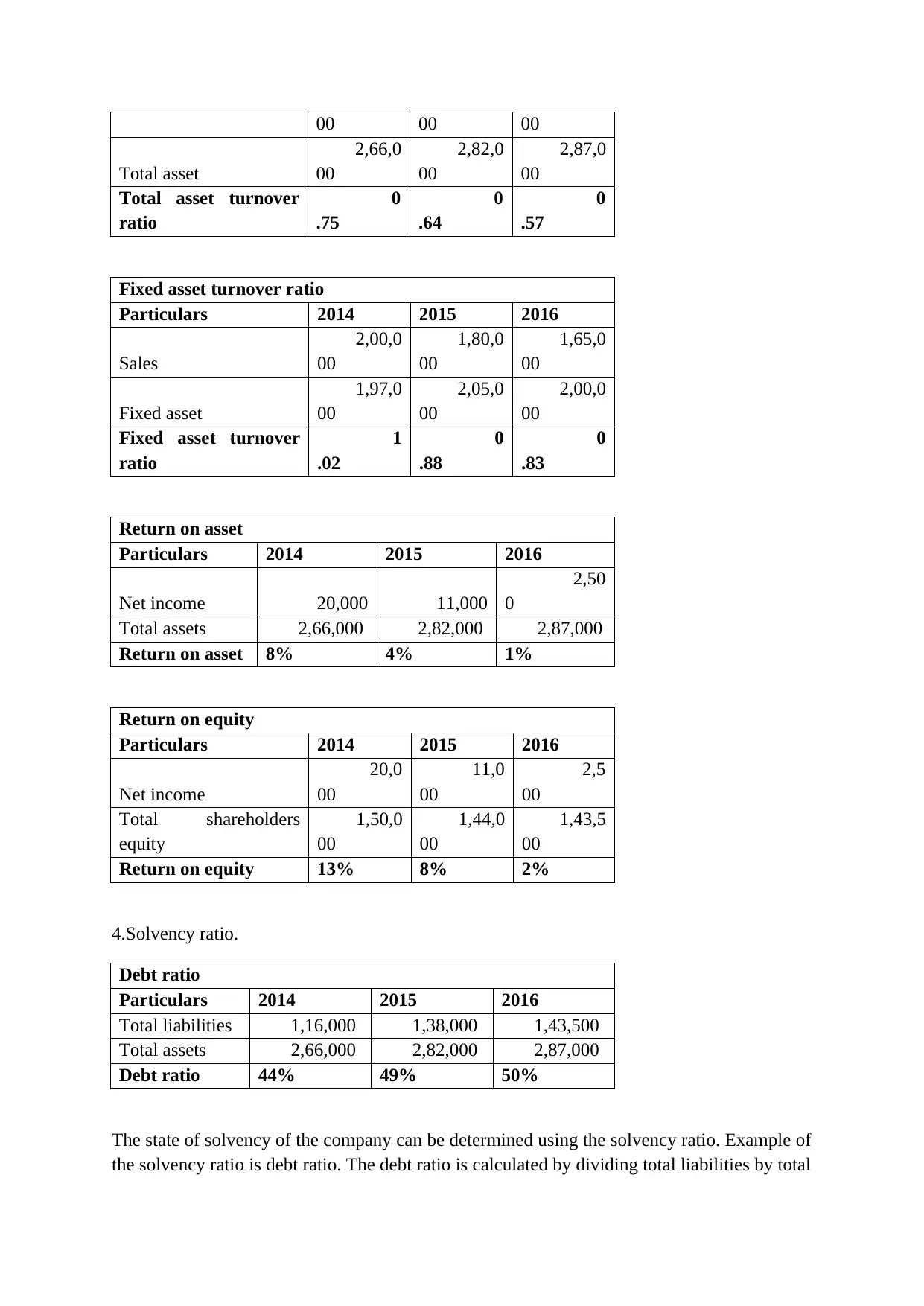

Total asset turnover ratio

Particulars 2014 2015 2016

Sales 2,00,0 1,80,0 1,65,0

liquidity position of the company is quite good (Spiceland, Thomas & Herrmann, 2010).

2. Profitability ratio.

Operating profit margin

Particulars 2014 2015 2016

Operating profit

20,

000

11,

000

3,

500

Sales

2,00,0

00

1,80,0

00

1,65,

000

Operating profit margin

ratio 10% 6% 2%

The main motive of every company is to earn profits. If the company’s financial

performance is not good it is expected that it will not survive in the long run. Therefore,

in order to see the expected survival of the company operating margin ratio is calculated.

It has been seen that the operating profit margin is falling over the years which is adverse.

Therefore, we can conclude that there is a decline in the financial performance of the

company (Kimmel, Weygandt & Kieso, 2012).

3.Efficiency ratio.

The most important financial ratio that helps to analyse the financial position of the

company is called efficiency ratio. Efficiency is based on the assets and liabilities of the

company which reflects a true picture of financial position of the company. The data used in

the calculation of efficiency ratio is usually taken from the balance sheet of the company.

The few efficiency ratios that are calculated by me are inventory turnover ratio, total asset

turnover ratio, fixed asset turnover ratio, return on asset and return on equity ratio

(Weygandt, Kimmel & Kieso, n.d.).

Inventory turnover ratio

Particulars 2014 2015 2016

Sales

2,00,0

00

1,80,0

00

1,65,0

00

Inventories

41,0

00

44,0

00

49,0

00

Inventory turnover

ratio

4

.88

4

.09

3

.37

Total asset turnover ratio

Particulars 2014 2015 2016

Sales 2,00,0 1,80,0 1,65,0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

00 00 00

Total asset

2,66,0

00

2,82,0

00

2,87,0

00

Total asset turnover

ratio

0

.75

0

.64

0

.57

Fixed asset turnover ratio

Particulars 2014 2015 2016

Sales

2,00,0

00

1,80,0

00

1,65,0

00

Fixed asset

1,97,0

00

2,05,0

00

2,00,0

00

Fixed asset turnover

ratio

1

.02

0

.88

0

.83

Return on asset

Particulars 2014 2015 2016

Net income 20,000 11,000

2,50

0

Total assets 2,66,000 2,82,000 2,87,000

Return on asset 8% 4% 1%

Return on equity

Particulars 2014 2015 2016

Net income

20,0

00

11,0

00

2,5

00

Total shareholders

equity

1,50,0

00

1,44,0

00

1,43,5

00

Return on equity 13% 8% 2%

4.Solvency ratio.

Debt ratio

Particulars 2014 2015 2016

Total liabilities 1,16,000 1,38,000 1,43,500

Total assets 2,66,000 2,82,000 2,87,000

Debt ratio 44% 49% 50%

The state of solvency of the company can be determined using the solvency ratio. Example of

the solvency ratio is debt ratio. The debt ratio is calculated by dividing total liabilities by total

Total asset

2,66,0

00

2,82,0

00

2,87,0

00

Total asset turnover

ratio

0

.75

0

.64

0

.57

Fixed asset turnover ratio

Particulars 2014 2015 2016

Sales

2,00,0

00

1,80,0

00

1,65,0

00

Fixed asset

1,97,0

00

2,05,0

00

2,00,0

00

Fixed asset turnover

ratio

1

.02

0

.88

0

.83

Return on asset

Particulars 2014 2015 2016

Net income 20,000 11,000

2,50

0

Total assets 2,66,000 2,82,000 2,87,000

Return on asset 8% 4% 1%

Return on equity

Particulars 2014 2015 2016

Net income

20,0

00

11,0

00

2,5

00

Total shareholders

equity

1,50,0

00

1,44,0

00

1,43,5

00

Return on equity 13% 8% 2%

4.Solvency ratio.

Debt ratio

Particulars 2014 2015 2016

Total liabilities 1,16,000 1,38,000 1,43,500

Total assets 2,66,000 2,82,000 2,87,000

Debt ratio 44% 49% 50%

The state of solvency of the company can be determined using the solvency ratio. Example of

the solvency ratio is debt ratio. The debt ratio is calculated by dividing total liabilities by total

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

asset. Lower the ratio better it is, it is seen that the debt ratio is increasing over the years

which is a negative aspect of the company (Ittelson, 2009).

(b) Financial ratios are used by a wide range of users to take certain economic decisions.

These financial ratios give the users the idea of the financial position and performance of the

company so the non financial aspect is ignored which may lead to wrong decisions.

There are also other limitations of these financial ratios (Harrison, Horngren & Thomas,

2015). They are-

There are various types of financial ratios. Some may show that the company has a

good overall performance and is strong whereas some ratios may show a weak

position.

The accounting is based on certain estimates, assumptions and different accounting

policies and therefore, the ratios may not be reliable enough to take important

decisions.

The analysis may be distorted due to various seasonal factors, therefore it is

important to understand such factors as it will lead to reduction of chances of

misinterpretation.

The financial statement may have been affected due to inflation or other market

conditions. Therefore, there always lies a confusion in the minds of the investors.

Apart from earning profits, it is the duty of the company to satisfy the customers of

the company and fulfil the social obligations also. Therefore, the users should also

check whether the company is taking part in fulfilling its social responsibilities or

not.

©

The financial ratios is just a tool that helps in the process of decision making but the in

the practical world it is important to collect the non financial information also along with

the financial ratios. It is also important to look at the capital structure of the company. If

there is a huge proportion of debt in the company then it is dangerous for the existence of

the company. There arises a doubt in the mind of the investors regarding the going

concern of the company. the users of the financial statements that include creditors,

lenders, investors and others must take decisions only after taking into consideration all

the various other factors. It has been observed that the retained earnings of the company

is also falling because of the falling profits.

which is a negative aspect of the company (Ittelson, 2009).

(b) Financial ratios are used by a wide range of users to take certain economic decisions.

These financial ratios give the users the idea of the financial position and performance of the

company so the non financial aspect is ignored which may lead to wrong decisions.

There are also other limitations of these financial ratios (Harrison, Horngren & Thomas,

2015). They are-

There are various types of financial ratios. Some may show that the company has a

good overall performance and is strong whereas some ratios may show a weak

position.

The accounting is based on certain estimates, assumptions and different accounting

policies and therefore, the ratios may not be reliable enough to take important

decisions.

The analysis may be distorted due to various seasonal factors, therefore it is

important to understand such factors as it will lead to reduction of chances of

misinterpretation.

The financial statement may have been affected due to inflation or other market

conditions. Therefore, there always lies a confusion in the minds of the investors.

Apart from earning profits, it is the duty of the company to satisfy the customers of

the company and fulfil the social obligations also. Therefore, the users should also

check whether the company is taking part in fulfilling its social responsibilities or

not.

©

The financial ratios is just a tool that helps in the process of decision making but the in

the practical world it is important to collect the non financial information also along with

the financial ratios. It is also important to look at the capital structure of the company. If

there is a huge proportion of debt in the company then it is dangerous for the existence of

the company. There arises a doubt in the mind of the investors regarding the going

concern of the company. the users of the financial statements that include creditors,

lenders, investors and others must take decisions only after taking into consideration all

the various other factors. It has been observed that the retained earnings of the company

is also falling because of the falling profits.

Answer 2.

(a) Ethics are the moral values & principles that govern a person's behavior or an activity.

Working in ways that would go hand in hand with the societies & individuals thinking is

what considered to be good values. A business's key element to success is behaving ethically

that involves respect for the major key principles such as fairness, honesty, diversity, dignity,

equality and individual rights (Piper, 2015).

In the given case, Tom Lyons, the accountant of Allandale Ltd, has been in a big ethical

dilemma. The mortgage loan that the company took of $20 millions demanded two conditions

of maintaining current ratio of 2:1 & after tax return on assets as 10% minimum. However,

there is a boat valued at $500000 in the balance sheet that would have a net realizable value

as $350000. Also, a customer who was liable to pay $10 million could only pay half of the

amount due to severe financial troubles (Atrill & McLaney, 2009). Thus the provision

regarding the two amounting to $150000 and $200000 respectively meets all the three

conditions and are supposed to be recognized as provisions. However, this would lead to

falling of current ratio to 1.6:1 and the return on assets ratio to be 2% which was previously

stated at 2.1:1 and 11% respectively. Such making of provisions would fail to meet the

mortgage lender’s conditions and would lead to an immediate call of repayment of loan

amount. Thus, the dilemma arises here to recognize an expense which has in actuality not

occurred and by doing so, asking the situations itself to arise such issues that would take them

to bankruptcy as well as losing of their jobs.

(b) Tom should go for the following steps so as to deal with this ethical dilemma:

The accounting standards states that a provision should be recognized only if three

conditions are met, that is, there must be a present obligation as an outcome of a past

event; the outflow of economic benefits to satisfy the obligation must be at least more

than 50% probable and the amount required for satisfaction of the obligation must be

estimated reliably. Thus, since all the three conditions are met, the provisions shall be

recognized.

The presentation and preparation of financial statements are based on certain

assumptions one of which includes the concept of 'prudence'. This concept states that

such estimates and policies should be adopted that the incomes and assets are not

overstated as well as liabilities & expenses are not understated. It states that an asset

shouldn't be recognized at a value higher than what it is expected to be recovered in

the future and a liability shouldn't be recognized at a lesser value than what it is

expected to be paid in future. Thus, it is important for the company to go for this

recognition so as to behave ethically (Hart, Wilson & Fergus, 2012).

The company, to avoid future bankruptcy, can write to the bank lender for some time

instead of immediate repayment so as to be able to cope up with the circumstances

and improve their present ratios.

(a) Ethics are the moral values & principles that govern a person's behavior or an activity.

Working in ways that would go hand in hand with the societies & individuals thinking is

what considered to be good values. A business's key element to success is behaving ethically

that involves respect for the major key principles such as fairness, honesty, diversity, dignity,

equality and individual rights (Piper, 2015).

In the given case, Tom Lyons, the accountant of Allandale Ltd, has been in a big ethical

dilemma. The mortgage loan that the company took of $20 millions demanded two conditions

of maintaining current ratio of 2:1 & after tax return on assets as 10% minimum. However,

there is a boat valued at $500000 in the balance sheet that would have a net realizable value

as $350000. Also, a customer who was liable to pay $10 million could only pay half of the

amount due to severe financial troubles (Atrill & McLaney, 2009). Thus the provision

regarding the two amounting to $150000 and $200000 respectively meets all the three

conditions and are supposed to be recognized as provisions. However, this would lead to

falling of current ratio to 1.6:1 and the return on assets ratio to be 2% which was previously

stated at 2.1:1 and 11% respectively. Such making of provisions would fail to meet the

mortgage lender’s conditions and would lead to an immediate call of repayment of loan

amount. Thus, the dilemma arises here to recognize an expense which has in actuality not

occurred and by doing so, asking the situations itself to arise such issues that would take them

to bankruptcy as well as losing of their jobs.

(b) Tom should go for the following steps so as to deal with this ethical dilemma:

The accounting standards states that a provision should be recognized only if three

conditions are met, that is, there must be a present obligation as an outcome of a past

event; the outflow of economic benefits to satisfy the obligation must be at least more

than 50% probable and the amount required for satisfaction of the obligation must be

estimated reliably. Thus, since all the three conditions are met, the provisions shall be

recognized.

The presentation and preparation of financial statements are based on certain

assumptions one of which includes the concept of 'prudence'. This concept states that

such estimates and policies should be adopted that the incomes and assets are not

overstated as well as liabilities & expenses are not understated. It states that an asset

shouldn't be recognized at a value higher than what it is expected to be recovered in

the future and a liability shouldn't be recognized at a lesser value than what it is

expected to be paid in future. Thus, it is important for the company to go for this

recognition so as to behave ethically (Hart, Wilson & Fergus, 2012).

The company, to avoid future bankruptcy, can write to the bank lender for some time

instead of immediate repayment so as to be able to cope up with the circumstances

and improve their present ratios.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Answer 3.

(a) Considering the management's difficulties and continuous negative cash flows, Giggling

Brothers should now replace their manual accounting system with computerized system and

should go for the adoption of Just-In-Time (JIT) system as their major problems revolves

around the mismanagement of inventory and therefore, excessive purchases are made at times

or lower sales are made sometimes. Just In Time inventory is a strategy to increase efficiency

as well as decrease waste as the goods are being brought into the production process only

when their requirement arises. Thus, reduces the inventory costs (Berry & Jarvis, 2007). This

is a strategy of having stock ready instantly to meet the demand of customers, but not to a

point when the company would again face the burden of heavy stock extra units.

The JIT strategy helps a company to trace its demand accurately and then accordingly go for

the purchase of materials required. In this manner, the purchase department of thr could make

an appropriate purchase of materials (Shim, Siegel & Shim, 2013). The computerized

software should be such adopted that when the credit balance of any customer goes below the

defined amount, it notifies the accounting department and further sales should be delay to that

particular customer until the previous debts are cleared.

(b) The adoption of JIT strategy along with the computerized system would serve a number

of advantages to the company as stated below (Lalli, 2012) :

The company would be notified about the demand of their products and then, could

accordingly order input materials. In this way, it would be able to meet the customers

in a timely manner with high quality products at a possible low costs.

JIT helps in reduction of overhead costs, material handling costs, storage costs, etc

and also, helps in early detection of defective goods so as to make an early correction

with at minimum costing (Loganathan, 1997).

It frees up the funds as only required purchases would be made and such funds could

be used for some other purposes. Also, it will free up the warehousing space as

appropriate purchases wouldn't give rise to situations of storing excessive stock in the

warehouse.

Such adoption demands the coordination between the departments as failure of one

department would lead to the failure of other department which is already happening

in thr company.Thus, with such adoption, the departments would work as a team

which would be indirectly good for the entire business (Izhar & Hontoir, 2001).

The computerized system would lead to better maintenance of accounts and would

highlight the major weaknesses whether the company is making unnecessary

expenditures or whether the revenues are not being recognized but have been received

long before. Such problems occurring in the manual system would be eliminated.

The computerized accounting system wouldn't be much time consuming in

comparison to previous system and therefore, the time saved could be used by the

accounting department in further tracing of better options and planning purposes for

the betterment of the company (Bhattacharyya, 2011).

(a) Considering the management's difficulties and continuous negative cash flows, Giggling

Brothers should now replace their manual accounting system with computerized system and

should go for the adoption of Just-In-Time (JIT) system as their major problems revolves

around the mismanagement of inventory and therefore, excessive purchases are made at times

or lower sales are made sometimes. Just In Time inventory is a strategy to increase efficiency

as well as decrease waste as the goods are being brought into the production process only

when their requirement arises. Thus, reduces the inventory costs (Berry & Jarvis, 2007). This

is a strategy of having stock ready instantly to meet the demand of customers, but not to a

point when the company would again face the burden of heavy stock extra units.

The JIT strategy helps a company to trace its demand accurately and then accordingly go for

the purchase of materials required. In this manner, the purchase department of thr could make

an appropriate purchase of materials (Shim, Siegel & Shim, 2013). The computerized

software should be such adopted that when the credit balance of any customer goes below the

defined amount, it notifies the accounting department and further sales should be delay to that

particular customer until the previous debts are cleared.

(b) The adoption of JIT strategy along with the computerized system would serve a number

of advantages to the company as stated below (Lalli, 2012) :

The company would be notified about the demand of their products and then, could

accordingly order input materials. In this way, it would be able to meet the customers

in a timely manner with high quality products at a possible low costs.

JIT helps in reduction of overhead costs, material handling costs, storage costs, etc

and also, helps in early detection of defective goods so as to make an early correction

with at minimum costing (Loganathan, 1997).

It frees up the funds as only required purchases would be made and such funds could

be used for some other purposes. Also, it will free up the warehousing space as

appropriate purchases wouldn't give rise to situations of storing excessive stock in the

warehouse.

Such adoption demands the coordination between the departments as failure of one

department would lead to the failure of other department which is already happening

in thr company.Thus, with such adoption, the departments would work as a team

which would be indirectly good for the entire business (Izhar & Hontoir, 2001).

The computerized system would lead to better maintenance of accounts and would

highlight the major weaknesses whether the company is making unnecessary

expenditures or whether the revenues are not being recognized but have been received

long before. Such problems occurring in the manual system would be eliminated.

The computerized accounting system wouldn't be much time consuming in

comparison to previous system and therefore, the time saved could be used by the

accounting department in further tracing of better options and planning purposes for

the betterment of the company (Bhattacharyya, 2011).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(c) The cost of implementation of new computerized system would cost heavily to the

company. Thus, it is important for them to evaluate their other costs so against such

implementation of new system (Epstein & Lee, 2012). The company, as we know, is adopting

JIT strategy that would help them in reducing both inventory & overhead costs. Such funds

could be used elsewhere for further revenue or could be given as loan so as to earn an interest

income. In a similar way, the warehousing space that would be then free could be rented to

some other party so as to earn a rental income. The company can even go the replacement or

termination of employees as the computerized system wouldn't be requiring too much of

workers and a group of two or three members with expertise knowledge in that field would

work.

Thus, such steps would lead to a cost reduction in the company's expenses.

(d) While designing and developing the operating specifications of the new system of the

company, there are some more things that should be involved in that :

The system should be representing the monthly cash flows as the company has been

facing severe negative cash flows in every 6 months so as to take immediate steps if

even after new adoptions, the same thing continues.

The system should be presenting a quarterly report regarding every case be it

purchases made, sales made or accounts receivables account so as to avoid

mismanagement or loss of unnecessary cash.

The accounting department should keep an eye on the unusual sales made if

exceeding certain limit and make an enquiry about that as maximum fraud occurs if

the company has poor management of accounting records. Thus, to avoid the

advantages that can be taken, the accounting department should be either trained or

replaced with experts of the field.

An accounting of funds should be made separately so as to actually analyze all those

activities where the funds are being used and whether it was worth enough or not and

the benefits reached or the costs incurred if in case.

(e) Giggling Brothers has been trading profitability in the past years but is suffering from

negative cash flows currently. In the generation of computerized system, where the company

is already late in adopting it, the competitors of it would have adopted it long before and is

now with different targets. Thus, there is a difference of level, that is, the company under

question is at that level where its competitors have already been long before. The competitors

might have faced the difficulties too initially and might have then adopted such strategies so

as to enjoy benefits. The competitors must have made a number of approaches for having the

best and to arrive at the most profitable level. Thus, Giggling Brothers should make use of

such information to avoid these difficulties in advance. It is rightly said that we learn from

mistakes and experience. Thus, evaluating the approcahes adopted and the experience of the

competitors would work in the betterment of the company under question. Thus, such an

examination would be definitely serving benefits to Giggling Brothers.

company. Thus, it is important for them to evaluate their other costs so against such

implementation of new system (Epstein & Lee, 2012). The company, as we know, is adopting

JIT strategy that would help them in reducing both inventory & overhead costs. Such funds

could be used elsewhere for further revenue or could be given as loan so as to earn an interest

income. In a similar way, the warehousing space that would be then free could be rented to

some other party so as to earn a rental income. The company can even go the replacement or

termination of employees as the computerized system wouldn't be requiring too much of

workers and a group of two or three members with expertise knowledge in that field would

work.

Thus, such steps would lead to a cost reduction in the company's expenses.

(d) While designing and developing the operating specifications of the new system of the

company, there are some more things that should be involved in that :

The system should be representing the monthly cash flows as the company has been

facing severe negative cash flows in every 6 months so as to take immediate steps if

even after new adoptions, the same thing continues.

The system should be presenting a quarterly report regarding every case be it

purchases made, sales made or accounts receivables account so as to avoid

mismanagement or loss of unnecessary cash.

The accounting department should keep an eye on the unusual sales made if

exceeding certain limit and make an enquiry about that as maximum fraud occurs if

the company has poor management of accounting records. Thus, to avoid the

advantages that can be taken, the accounting department should be either trained or

replaced with experts of the field.

An accounting of funds should be made separately so as to actually analyze all those

activities where the funds are being used and whether it was worth enough or not and

the benefits reached or the costs incurred if in case.

(e) Giggling Brothers has been trading profitability in the past years but is suffering from

negative cash flows currently. In the generation of computerized system, where the company

is already late in adopting it, the competitors of it would have adopted it long before and is

now with different targets. Thus, there is a difference of level, that is, the company under

question is at that level where its competitors have already been long before. The competitors

might have faced the difficulties too initially and might have then adopted such strategies so

as to enjoy benefits. The competitors must have made a number of approaches for having the

best and to arrive at the most profitable level. Thus, Giggling Brothers should make use of

such information to avoid these difficulties in advance. It is rightly said that we learn from

mistakes and experience. Thus, evaluating the approcahes adopted and the experience of the

competitors would work in the betterment of the company under question. Thus, such an

examination would be definitely serving benefits to Giggling Brothers.

References:

Atrill, P., & McLaney, E. (2009). Management accounting for decision makers. Harlow,

England: Financial Times/Prentice Hall.

Berry, A., & Jarvis, R. (2007). Accounting in a business context. London: Thomson Learning.

Bhattacharyya, D. (2011). Management accounting. Noida, India: Pearson.

Epstein, M., & Lee, J. (2012). Advances in management accounting. Bingley: Emerald.

Harrison, W., Horngren, C., & Thomas, C. (2015). Financial accounting. Upper Saddle

River: Prentice Hall.

Harrison, W., Horngren, C., & Thomas, C. Financial accounting.

Hart, J., Wilson, C., & Fergus, C. (2012). Management accounting. Frenchs Forest, N.S.W.:

Pearson Australia.

Ittelson, T. (2009). Financial statements. Franklin Lakes, N.J.: Career Press.

Izhar, R., & Hontoir, J. (2001). Accounting, costing and management. Oxford: Oxford

University Press.

Kimmel, P., Weygandt, J., & Kieso, D. (2012). Financial Accounting.

Lalli, W. (2012). Handbook of budgeting. Hoboken, N.J: Wiley.

Libby, R., Libby, P., & Hodge, F. (2012). Financial accounting.

Loganathan, N. (1997). Foundations of budgeting. Sydney: UNSW Press.

Loughran, M. (2011). Financial accounting for dummies. Hoboken (NJ): Wiley.

Piper, M. (2015). Accounting made simple. [United States]: [CreateSpace Pub.].

Shim, A., Siegel, J., & Shim, J. (2013). Budgeting basics and beyond. Hoboken, N.J.: Wiley.

Spiceland, J., Thomas, W., & Herrmann, D. (2010). Financial accounting.

Weygandt, J., Kimmel, P., & Kieso, D. Financial accounting.

Atrill, P., & McLaney, E. (2009). Management accounting for decision makers. Harlow,

England: Financial Times/Prentice Hall.

Berry, A., & Jarvis, R. (2007). Accounting in a business context. London: Thomson Learning.

Bhattacharyya, D. (2011). Management accounting. Noida, India: Pearson.

Epstein, M., & Lee, J. (2012). Advances in management accounting. Bingley: Emerald.

Harrison, W., Horngren, C., & Thomas, C. (2015). Financial accounting. Upper Saddle

River: Prentice Hall.

Harrison, W., Horngren, C., & Thomas, C. Financial accounting.

Hart, J., Wilson, C., & Fergus, C. (2012). Management accounting. Frenchs Forest, N.S.W.:

Pearson Australia.

Ittelson, T. (2009). Financial statements. Franklin Lakes, N.J.: Career Press.

Izhar, R., & Hontoir, J. (2001). Accounting, costing and management. Oxford: Oxford

University Press.

Kimmel, P., Weygandt, J., & Kieso, D. (2012). Financial Accounting.

Lalli, W. (2012). Handbook of budgeting. Hoboken, N.J: Wiley.

Libby, R., Libby, P., & Hodge, F. (2012). Financial accounting.

Loganathan, N. (1997). Foundations of budgeting. Sydney: UNSW Press.

Loughran, M. (2011). Financial accounting for dummies. Hoboken (NJ): Wiley.

Piper, M. (2015). Accounting made simple. [United States]: [CreateSpace Pub.].

Shim, A., Siegel, J., & Shim, J. (2013). Budgeting basics and beyond. Hoboken, N.J.: Wiley.

Spiceland, J., Thomas, W., & Herrmann, D. (2010). Financial accounting.

Weygandt, J., Kimmel, P., & Kieso, D. Financial accounting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.