ACCT20075 Auditing and Ethics Report: BOQ Financial Analysis

VerifiedAdded on 2022/09/15

|13

|3014

|37

Report

AI Summary

This report provides a comprehensive analysis of auditing and ethics in relation to the Bank of Queensland (BOQ). It begins by determining the level of materiality, considering profit before tax as the benchmark and applying a 5% materiality percentage, resulting in a materiality level of $24.65 million. The report then performs a preliminary analytical review of BOQ's financial information from 2015 to 2018, utilizing ratio analysis to assess trends in Net Interest Margin, Cost to Income Ratio, Return on Equity, and Capital Adequacy Ratios. The analysis identifies potential areas for audit scrutiny, such as possible manipulation of interest income and overstatement of costs or capital. Furthermore, the report examines the cash flow statement, highlighting the dominance of operating activities in generating cash inflows and the implications for BOQ's going concern risk. Finally, the report reviews the independent auditor's report, noting the unqualified opinion and the emphasis on key audit matters related to loan provisions, goodwill valuation, and IT controls. The report concludes by recommending audit procedures to address the identified risks and ensure the accuracy and fairness of BOQ's financial statements.

Running head: AUDITING AND ETHIC

Auditing and Ethic

Name of the Student

Name of the University

Author’s Note

Auditing and Ethic

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ETHIC

Table of Contents

Introduction................................................................................................................................2

Section 1.....................................................................................................................................2

Section 2.....................................................................................................................................5

Section 3.....................................................................................................................................6

Conclusion..................................................................................................................................8

References..................................................................................................................................9

Table of Contents

Introduction................................................................................................................................2

Section 1.....................................................................................................................................2

Section 2.....................................................................................................................................5

Section 3.....................................................................................................................................6

Conclusion..................................................................................................................................8

References..................................................................................................................................9

2AUDITING AND ETHIC

Introduction

Auditing refers to the process to methodically examine as well as inspect the financial

statements of the companies in order to make sure that there is not any material misstatement

in them. In the auditing profession, the auditors are needed to take into consideration various

crucial aspects; such as use of appropriate materiality level, analytical review, appropriate

audit procedure, formation of the correct audit opinion and others. Consideration of all these

aspects leads to the carry out of a successful audit engagement program (Baker, Bédard &

Prat dit Hauret, 2014). The main aim of this report is to undertake the analysis of the above-

mentioned aspects of auditing in relation to the Bank of Queensland (BOQ). The first part

of the report involves in the determination of the level of materiality of BOQ. The aim of the

second part of the report is to undertake the preliminary analytical review of the financial

information of BOQ while considering the key ratios from the year 2015 to 2018. The last

part undertakes the analysis of the cash flow statement and audit report of the bank.

Section 1

Level of Materiality

Determination of the appropriate level of materiality is considered as paramount in the

audit engagement of a company and there is not any exception of this fact in case of BOQ.

Application of audit materiality can be seen in the audit planning stage along with the time

when the auditors assesses the impact of material misstatement on the clients’ financial

reports. It is the obligation on the auditors to follow three certain steps for the determination

of audit materiality level. They are 1) to select the appropriate benchmark or base, 2) to

determine a specific percentage that needs to be charged on the above-selected base, and 3) to

provide the required justification for the selections (Vîlsănoiu & Buzenche, 2014). It is

Introduction

Auditing refers to the process to methodically examine as well as inspect the financial

statements of the companies in order to make sure that there is not any material misstatement

in them. In the auditing profession, the auditors are needed to take into consideration various

crucial aspects; such as use of appropriate materiality level, analytical review, appropriate

audit procedure, formation of the correct audit opinion and others. Consideration of all these

aspects leads to the carry out of a successful audit engagement program (Baker, Bédard &

Prat dit Hauret, 2014). The main aim of this report is to undertake the analysis of the above-

mentioned aspects of auditing in relation to the Bank of Queensland (BOQ). The first part

of the report involves in the determination of the level of materiality of BOQ. The aim of the

second part of the report is to undertake the preliminary analytical review of the financial

information of BOQ while considering the key ratios from the year 2015 to 2018. The last

part undertakes the analysis of the cash flow statement and audit report of the bank.

Section 1

Level of Materiality

Determination of the appropriate level of materiality is considered as paramount in the

audit engagement of a company and there is not any exception of this fact in case of BOQ.

Application of audit materiality can be seen in the audit planning stage along with the time

when the auditors assesses the impact of material misstatement on the clients’ financial

reports. It is the obligation on the auditors to follow three certain steps for the determination

of audit materiality level. They are 1) to select the appropriate benchmark or base, 2) to

determine a specific percentage that needs to be charged on the above-selected base, and 3) to

provide the required justification for the selections (Vîlsănoiu & Buzenche, 2014). It is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ETHIC

needed for the auditors of BOQ to undertake these three steps to determine the level of

materiality.

Step 1 – This step involves in the selection of the appropriate benchmark or base and the

auditors should consider certain aspects for the selection. Some of these aspects and the

characteristics of the industry in which the firm operates and the characteristics of the firm

itself. There are certain bases or benchmarks that are largely used such as profit before tax,

total expenses or income, total assets and others (Eilifsen & Messier Jr, 2014). Since BOQ

operates in the Australian banking industry, the chosen base or benchmark for BOQ is Profit

before Tax (PBT) due to its large use in the Australian banking industry which is $493

million (Cox, Dayanandan & Donker, 2014).

Step 2 – The aim of this step is to ascertain the relevant materiality percentage by the

auditors. The judgment of the auditors is a large factors in this case. In addition, the

principles and rules mentioned in AASB 1031 Materiality needs to be considered by the

auditors. AASB provides two quantitative thresholds for materiality determination and they

are as follows:

1. The auditor can select an amount that is more than or equal to 10% of the ascertained

base that is PBT.

2. The auditor can select an amount that is less than or equal to 5% of the ascertained

base that is PBT (aasb.gov.au, 2019).

It is totally dependent on the judgement of the auditors that which option they would

select while considering the relevant factors. Since BOQ operates in the Australian banking

industry, the selected percentage is 5.

Step 3 – This step involves in the determination of the level of materiality for BOQ and it is

shown below while considering the above-discussed factors.

needed for the auditors of BOQ to undertake these three steps to determine the level of

materiality.

Step 1 – This step involves in the selection of the appropriate benchmark or base and the

auditors should consider certain aspects for the selection. Some of these aspects and the

characteristics of the industry in which the firm operates and the characteristics of the firm

itself. There are certain bases or benchmarks that are largely used such as profit before tax,

total expenses or income, total assets and others (Eilifsen & Messier Jr, 2014). Since BOQ

operates in the Australian banking industry, the chosen base or benchmark for BOQ is Profit

before Tax (PBT) due to its large use in the Australian banking industry which is $493

million (Cox, Dayanandan & Donker, 2014).

Step 2 – The aim of this step is to ascertain the relevant materiality percentage by the

auditors. The judgment of the auditors is a large factors in this case. In addition, the

principles and rules mentioned in AASB 1031 Materiality needs to be considered by the

auditors. AASB provides two quantitative thresholds for materiality determination and they

are as follows:

1. The auditor can select an amount that is more than or equal to 10% of the ascertained

base that is PBT.

2. The auditor can select an amount that is less than or equal to 5% of the ascertained

base that is PBT (aasb.gov.au, 2019).

It is totally dependent on the judgement of the auditors that which option they would

select while considering the relevant factors. Since BOQ operates in the Australian banking

industry, the selected percentage is 5.

Step 3 – This step involves in the determination of the level of materiality for BOQ and it is

shown below while considering the above-discussed factors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ETHIC

Level of Materiality = PBT × 5% = $493 × 5% = $24.65 million.

Level of Materiality = PBT × 5% = $493 × 5% = $24.65 million.

5AUDITING AND ETHIC

Draft Notes Review and Audit Procedures

1. It can be seen from the 2018 Annual Report of BOQ that the bank has applied certain

new accounting standards for the purpose of financial reporting in the current year;

they are AASB 2016-1 Amendments to Australian Accounting Standards –

Recognition of Deferred Tax Assets for Unrealised Losses, AASB 2016-2

Amendments to Australian Accounting Standards - Disclosure Initiative:

Amendments to AASB 107, AASB 2017-2 Amendments to Australian Accounting

Standards – Further Annual Improvements 2014-2016 Cycle; and AASB 1048

Interpretation of Standards (boq.com.au, 2019). It needs to be mentioned that the

application of these amended standards would change the financial outcome of the

bank and therefore, this significant for the audit of BOQ. The audit procedure that will

be required to perform is to calculate and ascertain the impact of these amended

standards on the financial reports of BOQ.

Draft Notes Review and Audit Procedures

1. It can be seen from the 2018 Annual Report of BOQ that the bank has applied certain

new accounting standards for the purpose of financial reporting in the current year;

they are AASB 2016-1 Amendments to Australian Accounting Standards –

Recognition of Deferred Tax Assets for Unrealised Losses, AASB 2016-2

Amendments to Australian Accounting Standards - Disclosure Initiative:

Amendments to AASB 107, AASB 2017-2 Amendments to Australian Accounting

Standards – Further Annual Improvements 2014-2016 Cycle; and AASB 1048

Interpretation of Standards (boq.com.au, 2019). It needs to be mentioned that the

application of these amended standards would change the financial outcome of the

bank and therefore, this significant for the audit of BOQ. The audit procedure that will

be required to perform is to calculate and ascertain the impact of these amended

standards on the financial reports of BOQ.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ETHIC

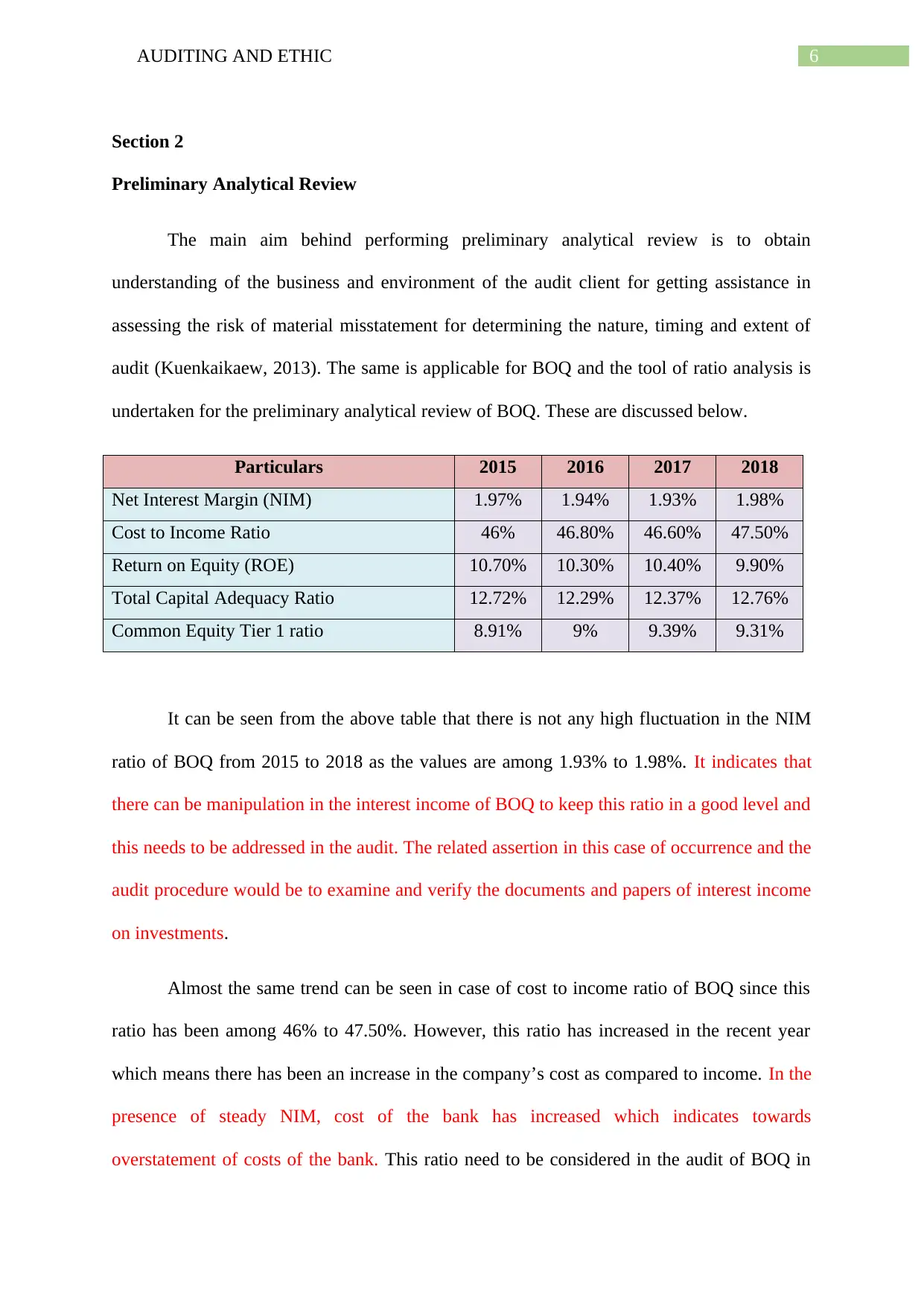

Section 2

Preliminary Analytical Review

The main aim behind performing preliminary analytical review is to obtain

understanding of the business and environment of the audit client for getting assistance in

assessing the risk of material misstatement for determining the nature, timing and extent of

audit (Kuenkaikaew, 2013). The same is applicable for BOQ and the tool of ratio analysis is

undertaken for the preliminary analytical review of BOQ. These are discussed below.

Particulars 2015 2016 2017 2018

Net Interest Margin (NIM) 1.97% 1.94% 1.93% 1.98%

Cost to Income Ratio 46% 46.80% 46.60% 47.50%

Return on Equity (ROE) 10.70% 10.30% 10.40% 9.90%

Total Capital Adequacy Ratio 12.72% 12.29% 12.37% 12.76%

Common Equity Tier 1 ratio 8.91% 9% 9.39% 9.31%

It can be seen from the above table that there is not any high fluctuation in the NIM

ratio of BOQ from 2015 to 2018 as the values are among 1.93% to 1.98%. It indicates that

there can be manipulation in the interest income of BOQ to keep this ratio in a good level and

this needs to be addressed in the audit. The related assertion in this case of occurrence and the

audit procedure would be to examine and verify the documents and papers of interest income

on investments.

Almost the same trend can be seen in case of cost to income ratio of BOQ since this

ratio has been among 46% to 47.50%. However, this ratio has increased in the recent year

which means there has been an increase in the company’s cost as compared to income. In the

presence of steady NIM, cost of the bank has increased which indicates towards

overstatement of costs of the bank. This ratio need to be considered in the audit of BOQ in

Section 2

Preliminary Analytical Review

The main aim behind performing preliminary analytical review is to obtain

understanding of the business and environment of the audit client for getting assistance in

assessing the risk of material misstatement for determining the nature, timing and extent of

audit (Kuenkaikaew, 2013). The same is applicable for BOQ and the tool of ratio analysis is

undertaken for the preliminary analytical review of BOQ. These are discussed below.

Particulars 2015 2016 2017 2018

Net Interest Margin (NIM) 1.97% 1.94% 1.93% 1.98%

Cost to Income Ratio 46% 46.80% 46.60% 47.50%

Return on Equity (ROE) 10.70% 10.30% 10.40% 9.90%

Total Capital Adequacy Ratio 12.72% 12.29% 12.37% 12.76%

Common Equity Tier 1 ratio 8.91% 9% 9.39% 9.31%

It can be seen from the above table that there is not any high fluctuation in the NIM

ratio of BOQ from 2015 to 2018 as the values are among 1.93% to 1.98%. It indicates that

there can be manipulation in the interest income of BOQ to keep this ratio in a good level and

this needs to be addressed in the audit. The related assertion in this case of occurrence and the

audit procedure would be to examine and verify the documents and papers of interest income

on investments.

Almost the same trend can be seen in case of cost to income ratio of BOQ since this

ratio has been among 46% to 47.50%. However, this ratio has increased in the recent year

which means there has been an increase in the company’s cost as compared to income. In the

presence of steady NIM, cost of the bank has increased which indicates towards

overstatement of costs of the bank. This ratio need to be considered in the audit of BOQ in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ETHIC

order to test the assertion of occurrence and the audit procedure is to inquire the transactions

related to expenses in order to assess the occurrence of these expenses for gaining the

appropriate audit evidence (Quadackers, Groot & Wright, 2014).

The above table shows a fluctuation in the ROE of BOQ such as it decreases from

2015 to 2016, then increases in 2017 and lastly, again decreases in 2018. This situation

implies that the ROE of BOQ has decreased in the presence of steady NIM which makes it

essential to check the return on equity investment of the bank. This needs to be considered in

the audit of BOQ in order to test the accuracy and occurrence assertions (Badara & Saidin,

2014). The audit procedure includes checking the documents and papers of equity investment

in the bank for assessing the actual return on equity.

It can be seen that there has been slight fluctuation in the capital adequacy ratio of

BOQ which indicates towards the fact that there could be overstatement in the values of

capital. This needs to be considered in the audit process and the relevant assertion is

existence. The relevant audit procedure is to check the balance of capital with the aim to

assess its existence (Brazel, Jones & Prawitt, 2013).

There has been fluctuation in the common equity tier 1 ratio that increases in 2016,

then decreases in 2017 and lastly increases in 2018. This indicates towards the

understatement of the equity capital of the bank. This ratio needs be tested in the audit

process in order to assess the assertions of existence. The relevant audit procedure is to check

the balance of equity capital with the aim to assess whether there has been any

understatement of this capital (Pinho, 2014).

Section 3

Statement of Cash Flows

order to test the assertion of occurrence and the audit procedure is to inquire the transactions

related to expenses in order to assess the occurrence of these expenses for gaining the

appropriate audit evidence (Quadackers, Groot & Wright, 2014).

The above table shows a fluctuation in the ROE of BOQ such as it decreases from

2015 to 2016, then increases in 2017 and lastly, again decreases in 2018. This situation

implies that the ROE of BOQ has decreased in the presence of steady NIM which makes it

essential to check the return on equity investment of the bank. This needs to be considered in

the audit of BOQ in order to test the accuracy and occurrence assertions (Badara & Saidin,

2014). The audit procedure includes checking the documents and papers of equity investment

in the bank for assessing the actual return on equity.

It can be seen that there has been slight fluctuation in the capital adequacy ratio of

BOQ which indicates towards the fact that there could be overstatement in the values of

capital. This needs to be considered in the audit process and the relevant assertion is

existence. The relevant audit procedure is to check the balance of capital with the aim to

assess its existence (Brazel, Jones & Prawitt, 2013).

There has been fluctuation in the common equity tier 1 ratio that increases in 2016,

then decreases in 2017 and lastly increases in 2018. This indicates towards the

understatement of the equity capital of the bank. This ratio needs be tested in the audit

process in order to assess the assertions of existence. The relevant audit procedure is to check

the balance of equity capital with the aim to assess whether there has been any

understatement of this capital (Pinho, 2014).

Section 3

Statement of Cash Flows

8AUDITING AND ETHIC

According to the 2019 Statement of Cash Flows of BOQ, the majority of cash inflows

is provided by the operating activities that is $317 million in 2018; and the greater

cash outflow is provided by investing activities that is $79 million in 2018

(boq.com.au, 2019).

In the cash flow of BOQ, the primary cash receipts are interest received and fees and

other income received that is $2,085 million and $160 million respectively. After that,

the primary cash payments are interest payment of $1,102 million, cash paid to

suppliers and employees of $500 million and income tax payment of $147 million

(boq.com.au, 2019).

Non-cash financing and investing activities are crucial that do not have direct effects

on cash. The cash flow statement of BOQ does not have any non-cash investing or

financing activities (boq.com.au, 2019).

The above discussion shows that the operating activities of BOQ are responsible for

generating the majority of the cash inflows which is a good indicator that the main

business operations of BOQ has been able in generating adequate cash inflows for the

overall business. Moreover, the primary cash receipts are greater than the primary

cash payments (Amin, Krishnan & Yang, 2014). The main investing activities involve

purchase of fixed assets, acquisition of business, payment of loan and others which

are indications that BOQ is investing in its future. Moreover, the amount of proceed

from borrowings is greater than repayment of borrowings which shows sting liquidity

position of BOQ. In the presence of all these reason, it can be said that the going

concern risk of BOQ is low (Geiger, Raghunandan & Riccardi, 2013).

The recommended audit procedures for going concern includes acquiring adequate

audit evidence on how effectively the management of BOQ is using the going concern

basis of accounting. After that, it is recommended to the auditors to ensure the

According to the 2019 Statement of Cash Flows of BOQ, the majority of cash inflows

is provided by the operating activities that is $317 million in 2018; and the greater

cash outflow is provided by investing activities that is $79 million in 2018

(boq.com.au, 2019).

In the cash flow of BOQ, the primary cash receipts are interest received and fees and

other income received that is $2,085 million and $160 million respectively. After that,

the primary cash payments are interest payment of $1,102 million, cash paid to

suppliers and employees of $500 million and income tax payment of $147 million

(boq.com.au, 2019).

Non-cash financing and investing activities are crucial that do not have direct effects

on cash. The cash flow statement of BOQ does not have any non-cash investing or

financing activities (boq.com.au, 2019).

The above discussion shows that the operating activities of BOQ are responsible for

generating the majority of the cash inflows which is a good indicator that the main

business operations of BOQ has been able in generating adequate cash inflows for the

overall business. Moreover, the primary cash receipts are greater than the primary

cash payments (Amin, Krishnan & Yang, 2014). The main investing activities involve

purchase of fixed assets, acquisition of business, payment of loan and others which

are indications that BOQ is investing in its future. Moreover, the amount of proceed

from borrowings is greater than repayment of borrowings which shows sting liquidity

position of BOQ. In the presence of all these reason, it can be said that the going

concern risk of BOQ is low (Geiger, Raghunandan & Riccardi, 2013).

The recommended audit procedures for going concern includes acquiring adequate

audit evidence on how effectively the management of BOQ is using the going concern

basis of accounting. After that, it is recommended to the auditors to ensure the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ETHIC

assessment of the presence of any key uncertainties that pose major threat to the

capability of BOQ to continue its going concern status. In case there is any threat, the

auditor is needed to mention that in the appropriate section of the audit report (Gallizo

Larraz & Saladrigues Solé, 2016).

Audit Report

As per the independent auditor’s report of BOQ, the auditors have expressed the

opinion that the consolidated financial statements of the bank are in accordance with

the Corporations Act 2001 that provides a true and fair view of the bank’s and the

consolidated entities’ financial position and financial performance; and they adheres

to the Australian Accounting Standards and the Corporations Regulations 2001

(boq.com.au, 2019). This implies that the auditors have provided the bank with

unqualified audit opinion. Unqualified audit opinion is the kind of opinion where the

auditors have expressed an opinion that the financial statements are presented as per

the applicable financial reporting framework; and attaches an emphasis on the matter

paragraph. The same aspect can be seen in case of BOQ as the auditors of the bank

has stated that the financial statements have been prepared as per the required

financial reporting framework; and they have emphasized on certain matters or issues

faced in the audit called “key audit matters” in separate paragraph. All these supports

the unqualified audit opinion.

The presence of “Key Audit Matter” section can be seen in the independent auditor’s

report of BOQ which discusses about five specific audit issues in the areas of Specific

and collective impairment provisions for loans and advances at amortised cost,

goodwill valuation, intangible computer software valuation, fair value measurement

of financial instruments and systems as well as control related to Information

Technology (IT) and control environment (boq.com.au, 2019). The main reason

assessment of the presence of any key uncertainties that pose major threat to the

capability of BOQ to continue its going concern status. In case there is any threat, the

auditor is needed to mention that in the appropriate section of the audit report (Gallizo

Larraz & Saladrigues Solé, 2016).

Audit Report

As per the independent auditor’s report of BOQ, the auditors have expressed the

opinion that the consolidated financial statements of the bank are in accordance with

the Corporations Act 2001 that provides a true and fair view of the bank’s and the

consolidated entities’ financial position and financial performance; and they adheres

to the Australian Accounting Standards and the Corporations Regulations 2001

(boq.com.au, 2019). This implies that the auditors have provided the bank with

unqualified audit opinion. Unqualified audit opinion is the kind of opinion where the

auditors have expressed an opinion that the financial statements are presented as per

the applicable financial reporting framework; and attaches an emphasis on the matter

paragraph. The same aspect can be seen in case of BOQ as the auditors of the bank

has stated that the financial statements have been prepared as per the required

financial reporting framework; and they have emphasized on certain matters or issues

faced in the audit called “key audit matters” in separate paragraph. All these supports

the unqualified audit opinion.

The presence of “Key Audit Matter” section can be seen in the independent auditor’s

report of BOQ which discusses about five specific audit issues in the areas of Specific

and collective impairment provisions for loans and advances at amortised cost,

goodwill valuation, intangible computer software valuation, fair value measurement

of financial instruments and systems as well as control related to Information

Technology (IT) and control environment (boq.com.au, 2019). The main reason

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ETHIC

behind considering these key audit matters as audit issues because these matters were

most important in the respective audits of the financial statements of BOQ as per the

professional judgments of the auditors. The auditors have addressed these matters as a

whole for the development of audit opinion (Council, 2013).

Conclusion

The above discussion provides crucial insight on the audit issues like materiality level

determination, preliminary analytical review, analysis of going concern risk through cash

flow analysis and others. As per the above analysis, the selection of appropriate base as well

as relevant percentage is paramount for the determination of materiality level. For example,

the materiality of BOQ is determined charging 5% on the base of PBT as this is acceptable in

the Australian banking industry. Another significant aspect is that the preliminary analytical

review provides the auditors with the insight about the areas in the financial statements that

need specific consideration in the final audit of the company; and the auditors become able in

designing the appropriate audit strategies based on the outcome of the preliminary analytical

procedures. As per the above discussion, cash flow statement analysis provides the insight on

the going concern risk of the companies. Lastly, as per the above discussion, the section of

“Key Audit Matters” is important since this portrays the areas that were significant in the

audit of the financial statements of the company.

behind considering these key audit matters as audit issues because these matters were

most important in the respective audits of the financial statements of BOQ as per the

professional judgments of the auditors. The auditors have addressed these matters as a

whole for the development of audit opinion (Council, 2013).

Conclusion

The above discussion provides crucial insight on the audit issues like materiality level

determination, preliminary analytical review, analysis of going concern risk through cash

flow analysis and others. As per the above analysis, the selection of appropriate base as well

as relevant percentage is paramount for the determination of materiality level. For example,

the materiality of BOQ is determined charging 5% on the base of PBT as this is acceptable in

the Australian banking industry. Another significant aspect is that the preliminary analytical

review provides the auditors with the insight about the areas in the financial statements that

need specific consideration in the final audit of the company; and the auditors become able in

designing the appropriate audit strategies based on the outcome of the preliminary analytical

procedures. As per the above discussion, cash flow statement analysis provides the insight on

the going concern risk of the companies. Lastly, as per the above discussion, the section of

“Key Audit Matters” is important since this portrays the areas that were significant in the

audit of the financial statements of the company.

11AUDITING AND ETHIC

References

Aasb.gov.au. (2019). Materiality. Retrieved 27 August 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB1031_12-13.pdf

Amin, K., Krishnan, J., & Yang, J. S. (2014). Going concern opinion and cost of

equity. Auditing: A Journal of Practice & Theory, 33(4), 1-39.

Badara, M. A. S., & Saidin, S. Z. (2014). Internal audit effectiveness: Data screening and

preliminary analysis. Asian Social Science, 10(10), 76-85.

Baker, C. R., Bédard, J., & Prat dit Hauret, C. (2014). The regulation of statutory auditing: an

institutional theory approach. Managerial Auditing Journal, 29(5), 371-394.

Boq.com.au. (2019). 2018 ANNUAL REPORT. Retrieved 27 August 2019, from

https://www.boq.com.au/content/dam/boq/files/shareholder-centre/financial-results/

2018/FY2018_Annual_Report.pdf

Brazel, J. F., Jones, K. L., & Prawitt, D. F. (2013). Auditors' reactions to inconsistencies

between financial and nonfinancial measures: The interactive effects of fraud risk

assessment and a decision prompt. Behavioral Research in Accounting, 26(1), 131-

156.

Council, F.R., 2013. Proposed International Standard on Auditing (ISA) 701: Communicating

Key Audit Matters in the Independent Auditor’s Report (2013).

Cox, R. A., Dayanandan, A., & Donker, H. (2014). Materiality disclosure and litigation risks:

A Canadian perspective. International Journal of Disclosure and Governance, 11(3),

284-298.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

References

Aasb.gov.au. (2019). Materiality. Retrieved 27 August 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB1031_12-13.pdf

Amin, K., Krishnan, J., & Yang, J. S. (2014). Going concern opinion and cost of

equity. Auditing: A Journal of Practice & Theory, 33(4), 1-39.

Badara, M. A. S., & Saidin, S. Z. (2014). Internal audit effectiveness: Data screening and

preliminary analysis. Asian Social Science, 10(10), 76-85.

Baker, C. R., Bédard, J., & Prat dit Hauret, C. (2014). The regulation of statutory auditing: an

institutional theory approach. Managerial Auditing Journal, 29(5), 371-394.

Boq.com.au. (2019). 2018 ANNUAL REPORT. Retrieved 27 August 2019, from

https://www.boq.com.au/content/dam/boq/files/shareholder-centre/financial-results/

2018/FY2018_Annual_Report.pdf

Brazel, J. F., Jones, K. L., & Prawitt, D. F. (2013). Auditors' reactions to inconsistencies

between financial and nonfinancial measures: The interactive effects of fraud risk

assessment and a decision prompt. Behavioral Research in Accounting, 26(1), 131-

156.

Council, F.R., 2013. Proposed International Standard on Auditing (ISA) 701: Communicating

Key Audit Matters in the Independent Auditor’s Report (2013).

Cox, R. A., Dayanandan, A., & Donker, H. (2014). Materiality disclosure and litigation risks:

A Canadian perspective. International Journal of Disclosure and Governance, 11(3),

284-298.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.