Business Finance: Evaluating the SSHA Project for Booli Electronics

VerifiedAdded on 2021/06/18

|11

|2254

|27

Report

AI Summary

This report evaluates the acceptability of Booli Electronics' new SSHA project, a new model for their existing product. The analysis includes calculating the non-discounted payback period, profitability index, internal rate of return (IRR), and net present value (NPV) to determine the project's financial viability. Furthermore, the report performs sensitivity analyses to assess the impact of changes in selling prices and quantities on the NPV, providing a comprehensive understanding of the project's risks and potential. The conclusion recommends producing the new SSHA model based on the positive financial indicators, with a recommendation to consider potential sales losses from other projects. The sensitivity analysis reveals that the NPV is highly sensitive to changes in selling price and moderately sensitive to changes in selling quantity.

Running head: BUSINESS FINANCE

Business finance

Name of the student

Name of the university

Student ID

Author note

Business finance

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUSINESS FINANCE

Table of Contents

Introduction................................................................................................................................2

Answer 1 – Non-discounted payback period.............................................................................2

Answer 2 – profitability index...................................................................................................3

Answer 3 – internal rate of return..............................................................................................3

Answer 4 – net present value.....................................................................................................3

Answer 5 – Sensitivity analysis for price change......................................................................3

Answer 6 - Sensitivity analysis for price change.......................................................................6

Answer 7 – Conclusion..............................................................................................................8

Answer 8 – Recommendation....................................................................................................8

Reference....................................................................................................................................9

Table of Contents

Introduction................................................................................................................................2

Answer 1 – Non-discounted payback period.............................................................................2

Answer 2 – profitability index...................................................................................................3

Answer 3 – internal rate of return..............................................................................................3

Answer 4 – net present value.....................................................................................................3

Answer 5 – Sensitivity analysis for price change......................................................................3

Answer 6 - Sensitivity analysis for price change.......................................................................6

Answer 7 – Conclusion..............................................................................................................8

Answer 8 – Recommendation....................................................................................................8

Reference....................................................................................................................................9

2BUSINESS FINANCE

Introduction

Booli Electronics is the electronics manufacturer that carries on its business from

Carlton, Victoria, Australia. Owing to the technological changes the company wants to make

new model for their existing product SSHA. The focus of this report will be evaluating the

acceptability of new SSHA project through various measures. These measures will include

the calculation of net present value, Profitability index, Payback period and internal rate of

return (McAuliffe 2015). Another objective of the report is to perform the sensitivity analysis

of NPV with regard to changes in the selling prices and changes in the selling quantity.

Answer 1 – Non-discounted payback period

Payback period is used to calculate the time in which the initial investment of the

project will be recovered. The main issue with payback period is that it does not consider the

time value of money which is an important aspect to consider (Leung et al. 2014). Further, it

is concerned about the time in which the initial investment is recovered but ignores the cash

flows after that Period.

Year Cash inflow Cumulative cash flow

0 $ (47,025,000.00)

1 $ 9,158,160.00 $ 9,158,160.00

2 $ 34,307,097.60 $ 43,465,257.60

3 $ 25,842,344.45 $ 69,307,602.05

4 $ 16,194,120.97 $ 85,501,723.02

5 $ 23,547,757.33 $ 109,049,480.35

Non-discounted payback period = 2 + (47,025,000 – 43.465,257.60) / (69,307,602.05 –

43,465,257.60) = 2.14 years.

Introduction

Booli Electronics is the electronics manufacturer that carries on its business from

Carlton, Victoria, Australia. Owing to the technological changes the company wants to make

new model for their existing product SSHA. The focus of this report will be evaluating the

acceptability of new SSHA project through various measures. These measures will include

the calculation of net present value, Profitability index, Payback period and internal rate of

return (McAuliffe 2015). Another objective of the report is to perform the sensitivity analysis

of NPV with regard to changes in the selling prices and changes in the selling quantity.

Answer 1 – Non-discounted payback period

Payback period is used to calculate the time in which the initial investment of the

project will be recovered. The main issue with payback period is that it does not consider the

time value of money which is an important aspect to consider (Leung et al. 2014). Further, it

is concerned about the time in which the initial investment is recovered but ignores the cash

flows after that Period.

Year Cash inflow Cumulative cash flow

0 $ (47,025,000.00)

1 $ 9,158,160.00 $ 9,158,160.00

2 $ 34,307,097.60 $ 43,465,257.60

3 $ 25,842,344.45 $ 69,307,602.05

4 $ 16,194,120.97 $ 85,501,723.02

5 $ 23,547,757.33 $ 109,049,480.35

Non-discounted payback period = 2 + (47,025,000 – 43.465,257.60) / (69,307,602.05 –

43,465,257.60) = 2.14 years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUSINESS FINANCE

Answer 2 – profitability index

It recognizes the cost and benefit correlation of the project. The profitability index of new

SSHA model is calculated as follows –

PI = PV of future cash flows / Initial investment

PI = $ 77,573,881.43 / 47,025,000 = 1.65

Answer 3 – internal rate of return

IRR is the point at which the cash inflows and cash outflows of the project are equal

(Leyman and Vanhoucke 2016). As per the Excel calculation the IRR of new SSHA model is

19.77%.

Answer 4 – net present value

It is the difference among the present value of cash inflows and cash outflows.

Generally, the acceptability of the project is evaluated through calculating the NPV (Gallo

2014). If the NPV is positive then the project is accepted and if the NPV is negative the

project is not accepted. The NPV of new SSHA model project is $ 30,548,881.43 (Pasqual,

Padilla and Jadotte 2013).

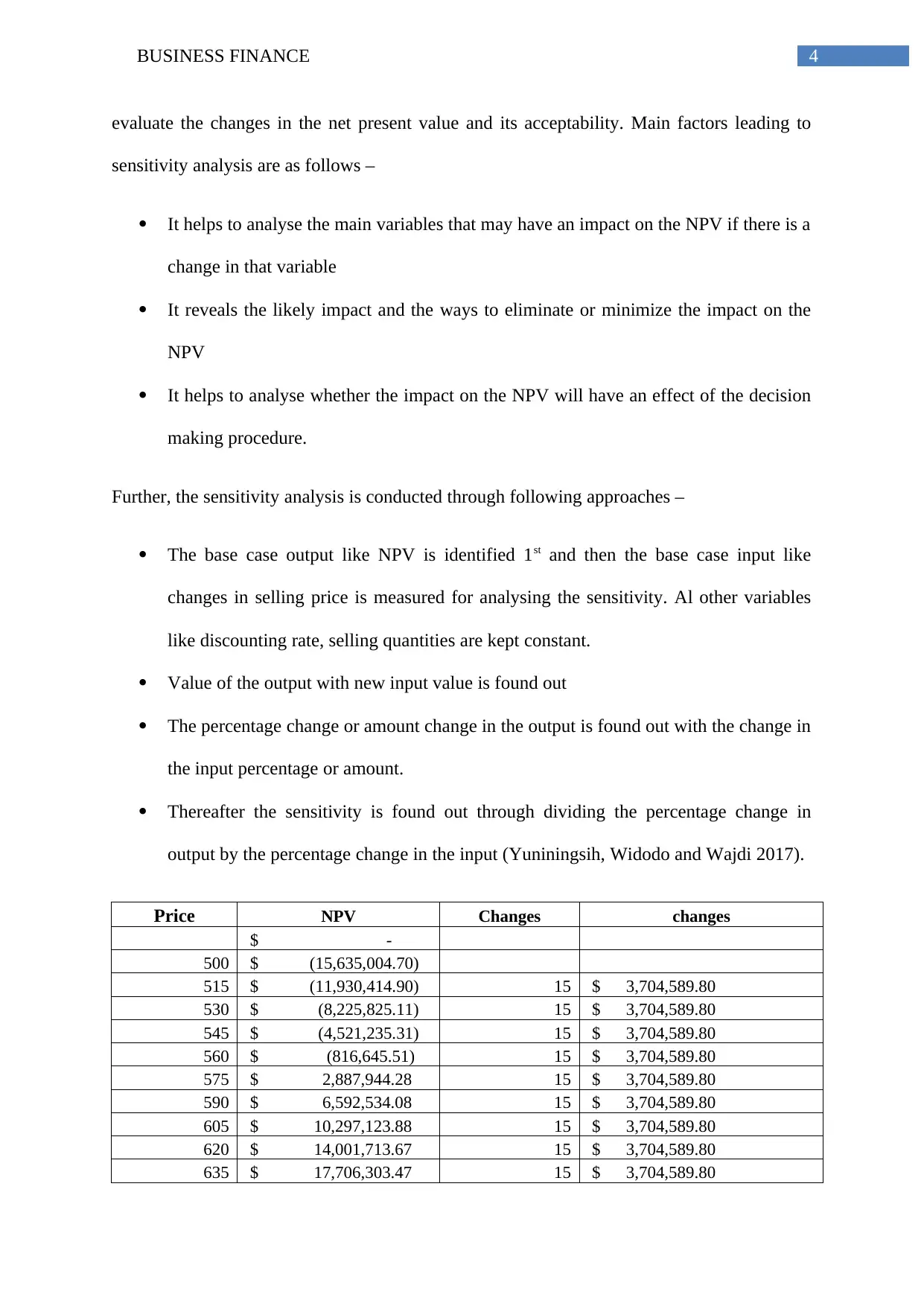

Answer 5 – Sensitivity analysis for price change

It is the technique of evaluating the impact of changes in the variables of the project

and the variables selected are those variables which can be expected most. While the

sensitivity analysis is performed generally the unfavourable situations are taken into

consideration. The variables taken into consideration are taken based on the most likely

expected factors like changes in the selling price or the selling quantity in the given case

(Brooks 2015). However, the impact of the changes of these variables shall be analysed to

Answer 2 – profitability index

It recognizes the cost and benefit correlation of the project. The profitability index of new

SSHA model is calculated as follows –

PI = PV of future cash flows / Initial investment

PI = $ 77,573,881.43 / 47,025,000 = 1.65

Answer 3 – internal rate of return

IRR is the point at which the cash inflows and cash outflows of the project are equal

(Leyman and Vanhoucke 2016). As per the Excel calculation the IRR of new SSHA model is

19.77%.

Answer 4 – net present value

It is the difference among the present value of cash inflows and cash outflows.

Generally, the acceptability of the project is evaluated through calculating the NPV (Gallo

2014). If the NPV is positive then the project is accepted and if the NPV is negative the

project is not accepted. The NPV of new SSHA model project is $ 30,548,881.43 (Pasqual,

Padilla and Jadotte 2013).

Answer 5 – Sensitivity analysis for price change

It is the technique of evaluating the impact of changes in the variables of the project

and the variables selected are those variables which can be expected most. While the

sensitivity analysis is performed generally the unfavourable situations are taken into

consideration. The variables taken into consideration are taken based on the most likely

expected factors like changes in the selling price or the selling quantity in the given case

(Brooks 2015). However, the impact of the changes of these variables shall be analysed to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUSINESS FINANCE

evaluate the changes in the net present value and its acceptability. Main factors leading to

sensitivity analysis are as follows –

It helps to analyse the main variables that may have an impact on the NPV if there is a

change in that variable

It reveals the likely impact and the ways to eliminate or minimize the impact on the

NPV

It helps to analyse whether the impact on the NPV will have an effect of the decision

making procedure.

Further, the sensitivity analysis is conducted through following approaches –

The base case output like NPV is identified 1st and then the base case input like

changes in selling price is measured for analysing the sensitivity. Al other variables

like discounting rate, selling quantities are kept constant.

Value of the output with new input value is found out

The percentage change or amount change in the output is found out with the change in

the input percentage or amount.

Thereafter the sensitivity is found out through dividing the percentage change in

output by the percentage change in the input (Yuniningsih, Widodo and Wajdi 2017).

Price NPV Changes changes

$ -

500 $ (15,635,004.70)

515 $ (11,930,414.90) 15 $ 3,704,589.80

530 $ (8,225,825.11) 15 $ 3,704,589.80

545 $ (4,521,235.31) 15 $ 3,704,589.80

560 $ (816,645.51) 15 $ 3,704,589.80

575 $ 2,887,944.28 15 $ 3,704,589.80

590 $ 6,592,534.08 15 $ 3,704,589.80

605 $ 10,297,123.88 15 $ 3,704,589.80

620 $ 14,001,713.67 15 $ 3,704,589.80

635 $ 17,706,303.47 15 $ 3,704,589.80

evaluate the changes in the net present value and its acceptability. Main factors leading to

sensitivity analysis are as follows –

It helps to analyse the main variables that may have an impact on the NPV if there is a

change in that variable

It reveals the likely impact and the ways to eliminate or minimize the impact on the

NPV

It helps to analyse whether the impact on the NPV will have an effect of the decision

making procedure.

Further, the sensitivity analysis is conducted through following approaches –

The base case output like NPV is identified 1st and then the base case input like

changes in selling price is measured for analysing the sensitivity. Al other variables

like discounting rate, selling quantities are kept constant.

Value of the output with new input value is found out

The percentage change or amount change in the output is found out with the change in

the input percentage or amount.

Thereafter the sensitivity is found out through dividing the percentage change in

output by the percentage change in the input (Yuniningsih, Widodo and Wajdi 2017).

Price NPV Changes changes

$ -

500 $ (15,635,004.70)

515 $ (11,930,414.90) 15 $ 3,704,589.80

530 $ (8,225,825.11) 15 $ 3,704,589.80

545 $ (4,521,235.31) 15 $ 3,704,589.80

560 $ (816,645.51) 15 $ 3,704,589.80

575 $ 2,887,944.28 15 $ 3,704,589.80

590 $ 6,592,534.08 15 $ 3,704,589.80

605 $ 10,297,123.88 15 $ 3,704,589.80

620 $ 14,001,713.67 15 $ 3,704,589.80

635 $ 17,706,303.47 15 $ 3,704,589.80

5BUSINESS FINANCE

650 $ 21,410,893.27 15 $ 3,704,589.80

665 $ 25,115,483.06 15 $ 3,704,589.80

680 $ 28,820,072.86 15 $ 3,704,589.80

695 $ 32,524,662.66 15 $ 3,704,589.80

710 $ 36,229,252.46 15 $ 3,704,589.80

725 $ 39,933,842.25 15 $ 3,704,589.80

740 $ 43,638,432.05 15 $ 3,704,589.80

755 $ 47,343,021.85 15 $ 3,704,589.80

770 $ 51,047,611.64 15 $ 3,704,589.80

785 $ 54,752,201.44 15 $ 3,704,589.80

800 $ 58,456,791.24 15 $ 3,704,589.80

815 $ 62,161,381.03 15 $ 3,704,589.80

830 $ 65,865,970.83 15 $ 3,704,589.80

845 $ 69,570,560.63 15 $ 3,704,589.80

860 $ 73,275,150.43 15 $ 3,704,589.80

875 $ 76,979,740.22 15 $ 3,704,589.80

890 $ 80,684,330.02 15 $ 3,704,589.80

905 $ 84,388,919.82 15 $ 3,704,589.80

450 500 550 600 650 700 750 800 850 900 950

$(40,000,000.00)

$(20,000,000.00)

$-

$20,000,000.00

$40,000,000.00

$60,000,000.00

$80,000,000.00

$100,000,000.00

Selling price

N

P

V

Changes in price 2%

Changes in NPV 12%

Sensitivity 555.41%

From the above it can be identified that the output that is the NPV increases with the

increase in the input that is selling price. As per the above table and graph with the selling

price ranged from $ 500 to $ 905 the NPV is increased from -$15,635004.70 to $

650 $ 21,410,893.27 15 $ 3,704,589.80

665 $ 25,115,483.06 15 $ 3,704,589.80

680 $ 28,820,072.86 15 $ 3,704,589.80

695 $ 32,524,662.66 15 $ 3,704,589.80

710 $ 36,229,252.46 15 $ 3,704,589.80

725 $ 39,933,842.25 15 $ 3,704,589.80

740 $ 43,638,432.05 15 $ 3,704,589.80

755 $ 47,343,021.85 15 $ 3,704,589.80

770 $ 51,047,611.64 15 $ 3,704,589.80

785 $ 54,752,201.44 15 $ 3,704,589.80

800 $ 58,456,791.24 15 $ 3,704,589.80

815 $ 62,161,381.03 15 $ 3,704,589.80

830 $ 65,865,970.83 15 $ 3,704,589.80

845 $ 69,570,560.63 15 $ 3,704,589.80

860 $ 73,275,150.43 15 $ 3,704,589.80

875 $ 76,979,740.22 15 $ 3,704,589.80

890 $ 80,684,330.02 15 $ 3,704,589.80

905 $ 84,388,919.82 15 $ 3,704,589.80

450 500 550 600 650 700 750 800 850 900 950

$(40,000,000.00)

$(20,000,000.00)

$-

$20,000,000.00

$40,000,000.00

$60,000,000.00

$80,000,000.00

$100,000,000.00

Selling price

N

P

V

Changes in price 2%

Changes in NPV 12%

Sensitivity 555.41%

From the above it can be identified that the output that is the NPV increases with the

increase in the input that is selling price. As per the above table and graph with the selling

price ranged from $ 500 to $ 905 the NPV is increased from -$15,635004.70 to $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUSINESS FINANCE

84,388,919.82. Thus, there is a change of $ 37,04,589.80 in the NPV with every $ 15 increase

in the selling price. In other words, for every 2% changes in the selling price there is 12%

changes in the NPV. Therefore the resultant sensitivity is 555.41%. Therefore, there is

positive correlation between the input and output. To be more specific, with the increase in

input that is selling price there is an increase of output that is NPV. Thus, the NPV is highly

sensitive with regard to changes in the selling price (Arrow et al. 2013).

Answer 6 - Sensitivity analysis for price change

In case of changes in the selling quantity and measuring the sensitivity of NPV,

selling quantity will be input and NPV will be the output. The changes in the NPV will be

measured with regard to the changes in the selling quantity being the other things like selling

price and discounting rate at same level (Baucells and Borgonovo 2013). However, the

limitations involved in the sensitivity analysis is that it may produce ambiguous result as it

depends on the user’s decision regarding what is pessimistic and what is optimistic. Further,

underlying variable is considered as independent. However, in reality it may not be the

condition. In this section the variable is taken as the selling quantity and its sensitivity will be

analysed with regard to the NPV.

Sales volume Amount Changes Changes

$ -

25000 $ 22,354,148.82

45000 $ 24,800,337.66 20000 2,446,188.84

65000 $ 27,246,526.50 20000 2,446,188.84

85000 $ 29,692,715.34 20000 2,446,188.84

105000 $ 32,138,904.18 20000 2,446,188.84

125000 $ 34,585,093.02 20000 2,446,188.84

145000 $ 37,031,281.86 20000 2,446,188.84

165000 $ 39,477,470.70 20000 2,446,188.84

185000 $ 41,923,659.54 20000 2,446,188.84

205000 $ 44,369,848.38 20000 2,446,188.84

225000 $ 46,816,037.22 20000 2,446,188.84

245000 $ 49,262,226.06 20000 2,446,188.84

84,388,919.82. Thus, there is a change of $ 37,04,589.80 in the NPV with every $ 15 increase

in the selling price. In other words, for every 2% changes in the selling price there is 12%

changes in the NPV. Therefore the resultant sensitivity is 555.41%. Therefore, there is

positive correlation between the input and output. To be more specific, with the increase in

input that is selling price there is an increase of output that is NPV. Thus, the NPV is highly

sensitive with regard to changes in the selling price (Arrow et al. 2013).

Answer 6 - Sensitivity analysis for price change

In case of changes in the selling quantity and measuring the sensitivity of NPV,

selling quantity will be input and NPV will be the output. The changes in the NPV will be

measured with regard to the changes in the selling quantity being the other things like selling

price and discounting rate at same level (Baucells and Borgonovo 2013). However, the

limitations involved in the sensitivity analysis is that it may produce ambiguous result as it

depends on the user’s decision regarding what is pessimistic and what is optimistic. Further,

underlying variable is considered as independent. However, in reality it may not be the

condition. In this section the variable is taken as the selling quantity and its sensitivity will be

analysed with regard to the NPV.

Sales volume Amount Changes Changes

$ -

25000 $ 22,354,148.82

45000 $ 24,800,337.66 20000 2,446,188.84

65000 $ 27,246,526.50 20000 2,446,188.84

85000 $ 29,692,715.34 20000 2,446,188.84

105000 $ 32,138,904.18 20000 2,446,188.84

125000 $ 34,585,093.02 20000 2,446,188.84

145000 $ 37,031,281.86 20000 2,446,188.84

165000 $ 39,477,470.70 20000 2,446,188.84

185000 $ 41,923,659.54 20000 2,446,188.84

205000 $ 44,369,848.38 20000 2,446,188.84

225000 $ 46,816,037.22 20000 2,446,188.84

245000 $ 49,262,226.06 20000 2,446,188.84

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS FINANCE

265000 $ 51,708,414.90 20000 2,446,188.84

285000 $ 54,154,603.74 20000 2,446,188.84

0 50000 100000 150000 200000 250000 300000

$-

$10,000,000.00

$20,000,000.00

$30,000,000.00

$40,000,000.00

$50,000,000.00

$60,000,000.00

Sales volume

N

P

V

Changes in quantity 22%

Changes in NPV 8%

Sensitivity 36.83%

From the above it can be identified that the output that is the NPV increases with the

increase in the input that is selling quantity. As per the above table and graph with the selling

quantity ranged from 25000 to 285,000 the NPV is increased from $ 22,354,148.82 to $

54,154,603.74. Thus, there is a change of $ 24,46,188.84 in the NPV with every 20000

increase in the selling quantity. In other words, for every 22% changes in the selling quantity

there is 8% change in the NPV. Therefore the resultant sensitivity is 36.83%. Therefore, there

is positive correlation between the input and output (Iooss and Lemaître 2015). To be more

specific, with the increase in input that is selling quantity there is an increase of output that is

NPV. However, the NPV is moderately sensitive with regard to changes in the selling price

(Butler et al. 2015). Therefore, if the decision is made with regard to the sensitivity of selling

265000 $ 51,708,414.90 20000 2,446,188.84

285000 $ 54,154,603.74 20000 2,446,188.84

0 50000 100000 150000 200000 250000 300000

$-

$10,000,000.00

$20,000,000.00

$30,000,000.00

$40,000,000.00

$50,000,000.00

$60,000,000.00

Sales volume

N

P

V

Changes in quantity 22%

Changes in NPV 8%

Sensitivity 36.83%

From the above it can be identified that the output that is the NPV increases with the

increase in the input that is selling quantity. As per the above table and graph with the selling

quantity ranged from 25000 to 285,000 the NPV is increased from $ 22,354,148.82 to $

54,154,603.74. Thus, there is a change of $ 24,46,188.84 in the NPV with every 20000

increase in the selling quantity. In other words, for every 22% changes in the selling quantity

there is 8% change in the NPV. Therefore the resultant sensitivity is 36.83%. Therefore, there

is positive correlation between the input and output (Iooss and Lemaître 2015). To be more

specific, with the increase in input that is selling quantity there is an increase of output that is

NPV. However, the NPV is moderately sensitive with regard to changes in the selling price

(Butler et al. 2015). Therefore, if the decision is made with regard to the sensitivity of selling

8BUSINESS FINANCE

quantity with the NPV, the decision maker shall keep in mind that there is positive correlation

among the 2 factors that is for earning more NPV the selling quantity is to be increased.

However, the sensitivity analysis gives the appropriate insight with regard to the

issues associated with reference model that is to take decision regarding the project.

Moreover, the decision maker gets the idea regarding how the output (NPV in the given case)

is sensitive to changes in the input (selling quantity in the given case) and he can analyse the

optimum solution based on the sensitivity (Levy 2015).

Answer 7 – Conclusion

From the above discussions it can be concluded that Booli Enterprise shall produce

New SSHA model. The decision is taken based on the factors that the NPV of the project is

positive that is $ 30,548,881.41. Further, the payback period of the project is 2.14 that is less

than 5 years. Moreover, the IRR of the project is 19.77% that is more than the required rate of

return that is 12%. Therefore, new SSHA model shall be produced.

Answer 8 – Recommendation

If owing to taking up the new SSHA project the company loses sales on other project

then the loss shall be included in the cost of initial investment. if including the loss leads to

negative NPV then new SSHA project shall not be taken up. However, if even after including

the SSHA project the NPV remains positive then the new SSHA shall be produced.

quantity with the NPV, the decision maker shall keep in mind that there is positive correlation

among the 2 factors that is for earning more NPV the selling quantity is to be increased.

However, the sensitivity analysis gives the appropriate insight with regard to the

issues associated with reference model that is to take decision regarding the project.

Moreover, the decision maker gets the idea regarding how the output (NPV in the given case)

is sensitive to changes in the input (selling quantity in the given case) and he can analyse the

optimum solution based on the sensitivity (Levy 2015).

Answer 7 – Conclusion

From the above discussions it can be concluded that Booli Enterprise shall produce

New SSHA model. The decision is taken based on the factors that the NPV of the project is

positive that is $ 30,548,881.41. Further, the payback period of the project is 2.14 that is less

than 5 years. Moreover, the IRR of the project is 19.77% that is more than the required rate of

return that is 12%. Therefore, new SSHA model shall be produced.

Answer 8 – Recommendation

If owing to taking up the new SSHA project the company loses sales on other project

then the loss shall be included in the cost of initial investment. if including the loss leads to

negative NPV then new SSHA project shall not be taken up. However, if even after including

the SSHA project the NPV remains positive then the new SSHA shall be produced.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUSINESS FINANCE

Reference

Arrow, K., Cropper, M., Gollier, C., Groom, B., Heal, G., Newell, R., Nordhaus, W.,

Pindyck, R., Pizer, W., Portney, P. and Sterner, T., 2013. Determining benefits and costs for

future generations. Science, 341(6144), pp.349-350.

Baucells, M. and Borgonovo, E., 2013. Invariant probabilistic sensitivity

analysis. Management Science, 59(11), pp.2536-2549.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Butler, M.P., Reed, P.M., Fisher-Vanden, K., Keller, K. and Wagener, T., 2014. Identifying

parametric controls and dependencies in integrated assessment models using global

sensitivity analysis. Environmental modelling & software, 59, pp.10-29.

Gallo, A., 2014. A refresher on net present value. Harvard Business Review, 19.

Iooss, B. and Lemaître, P., 2015. A review on global sensitivity analysis methods.

In Uncertainty management in simulation-optimization of complex systems (pp. 101-122).

Springer, Boston, MA.

Leung, B., Springborn, M.R., Turner, J.A. and Brockerhoff, E.G., 2014. Pathway‐level risk

analysis: the net present value of an invasive species policy in the US. Frontiers in Ecology

and the Environment, 12(5), pp.273-279.

Levy, H., 2015. Stochastic dominance: Investment decision making under uncertainty.

Springer.

Reference

Arrow, K., Cropper, M., Gollier, C., Groom, B., Heal, G., Newell, R., Nordhaus, W.,

Pindyck, R., Pizer, W., Portney, P. and Sterner, T., 2013. Determining benefits and costs for

future generations. Science, 341(6144), pp.349-350.

Baucells, M. and Borgonovo, E., 2013. Invariant probabilistic sensitivity

analysis. Management Science, 59(11), pp.2536-2549.

Brooks, R., 2015. Financial management: core concepts. Pearson.

Butler, M.P., Reed, P.M., Fisher-Vanden, K., Keller, K. and Wagener, T., 2014. Identifying

parametric controls and dependencies in integrated assessment models using global

sensitivity analysis. Environmental modelling & software, 59, pp.10-29.

Gallo, A., 2014. A refresher on net present value. Harvard Business Review, 19.

Iooss, B. and Lemaître, P., 2015. A review on global sensitivity analysis methods.

In Uncertainty management in simulation-optimization of complex systems (pp. 101-122).

Springer, Boston, MA.

Leung, B., Springborn, M.R., Turner, J.A. and Brockerhoff, E.G., 2014. Pathway‐level risk

analysis: the net present value of an invasive species policy in the US. Frontiers in Ecology

and the Environment, 12(5), pp.273-279.

Levy, H., 2015. Stochastic dominance: Investment decision making under uncertainty.

Springer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUSINESS FINANCE

Leyman, P. and Vanhoucke, M., 2016. Payment models and net present value optimization

for resource-constrained project scheduling. Computers & Industrial Engineering, 91,

pp.139-153.

McAuliffe, R.E., 2015. Net Present Value. Wiley Encyclopedia of Management, pp.1-1.

Pasqual, J., Padilla, E. and Jadotte, E., 2013. Equivalence of different profitability criteria

with the net present value. International Journal of Production Economics, 142(1), pp.205-

210.

Yuniningsih, Y., Widodo, S. and Wajdi, M.B.N., 2017. An analysis of Decision Making in

the Stock Investment. Economic: Journal of Economic and Islamic Law, 8(2), pp.122-128.

Leyman, P. and Vanhoucke, M., 2016. Payment models and net present value optimization

for resource-constrained project scheduling. Computers & Industrial Engineering, 91,

pp.139-153.

McAuliffe, R.E., 2015. Net Present Value. Wiley Encyclopedia of Management, pp.1-1.

Pasqual, J., Padilla, E. and Jadotte, E., 2013. Equivalence of different profitability criteria

with the net present value. International Journal of Production Economics, 142(1), pp.205-

210.

Yuniningsih, Y., Widodo, S. and Wajdi, M.B.N., 2017. An analysis of Decision Making in

the Stock Investment. Economic: Journal of Economic and Islamic Law, 8(2), pp.122-128.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.