Fast Feet Couriers Ltd: Cash Flow Statement and Financial Analysis

VerifiedAdded on 2020/05/03

|8

|1589

|41

Practical Assignment

AI Summary

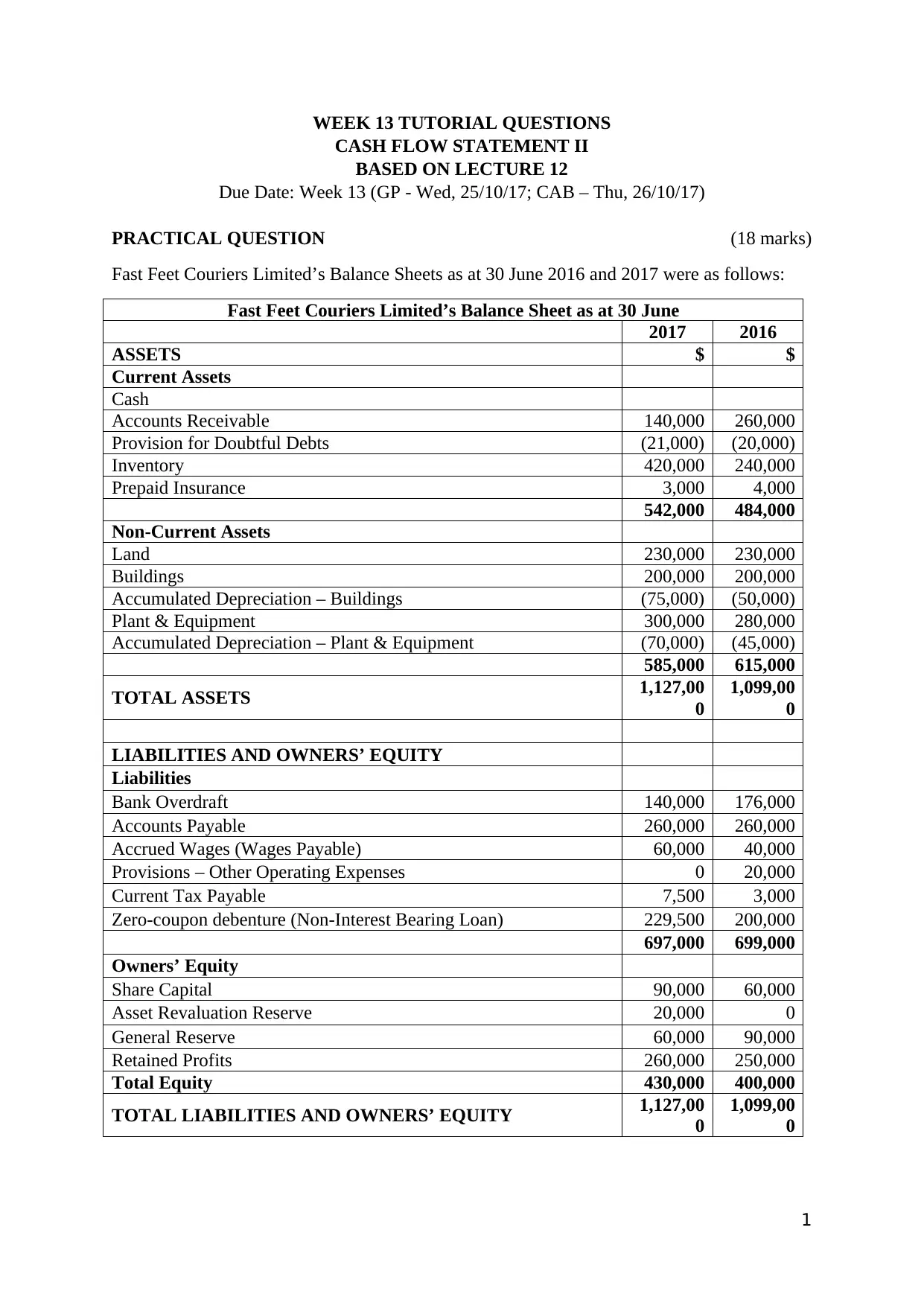

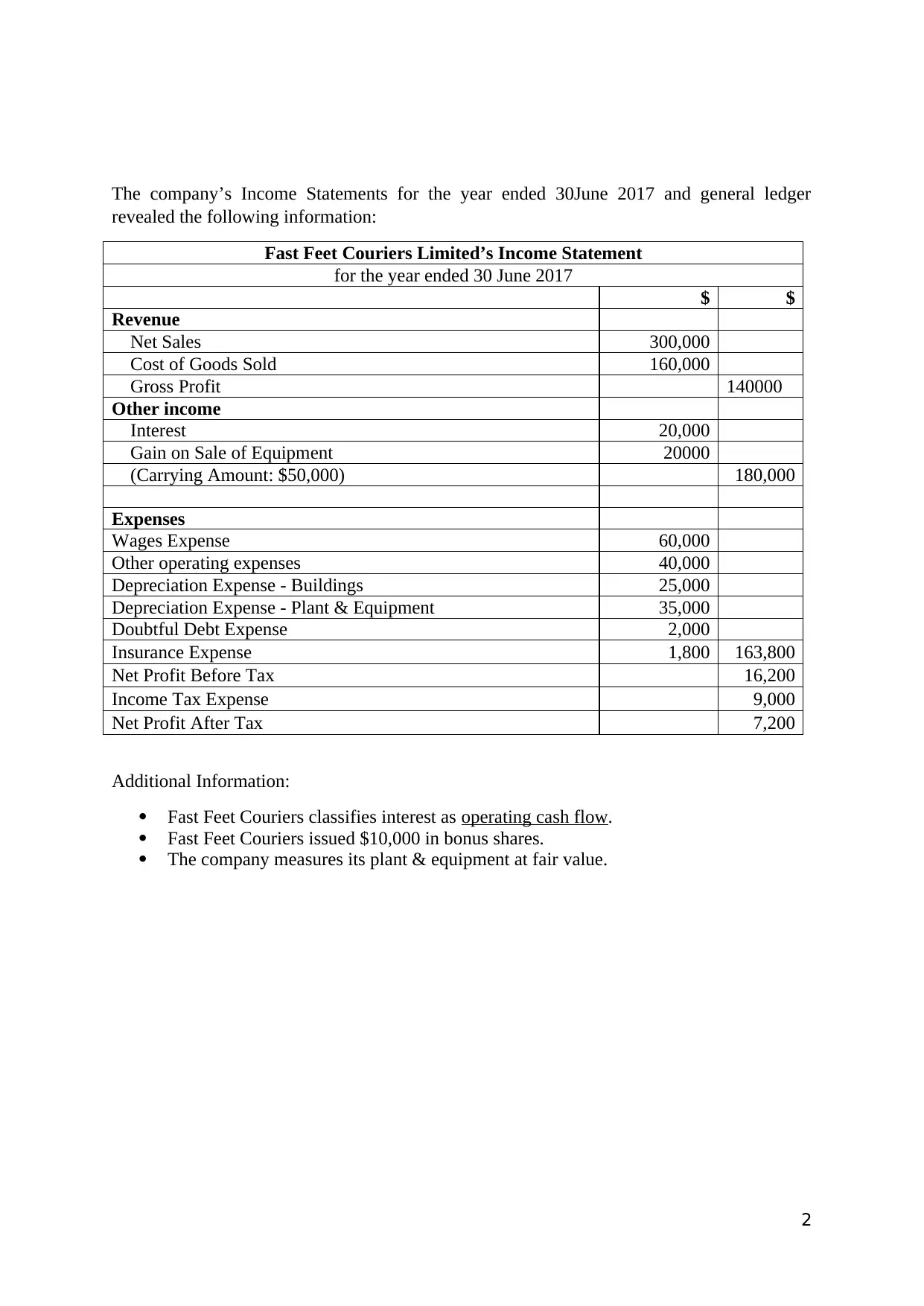

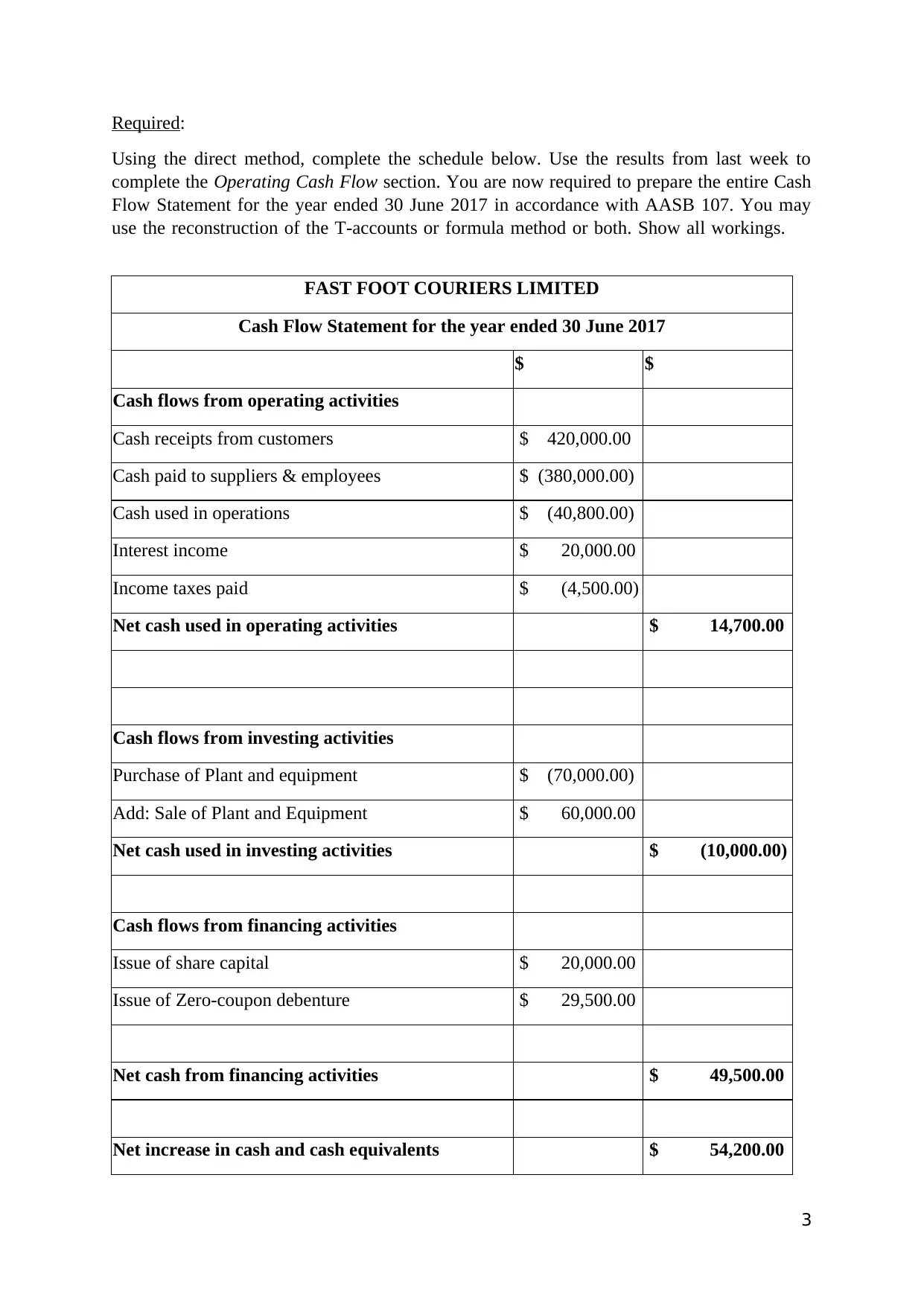

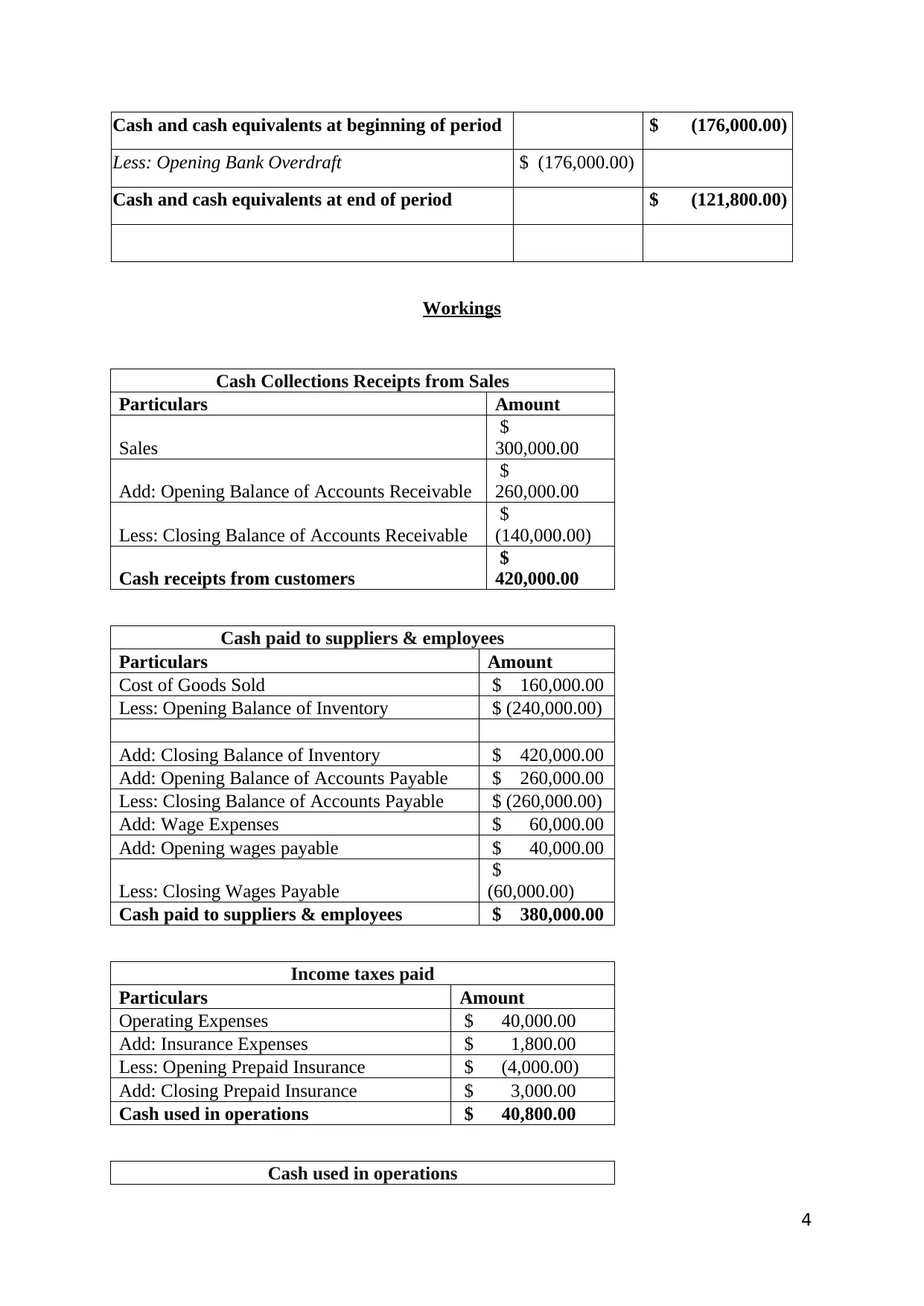

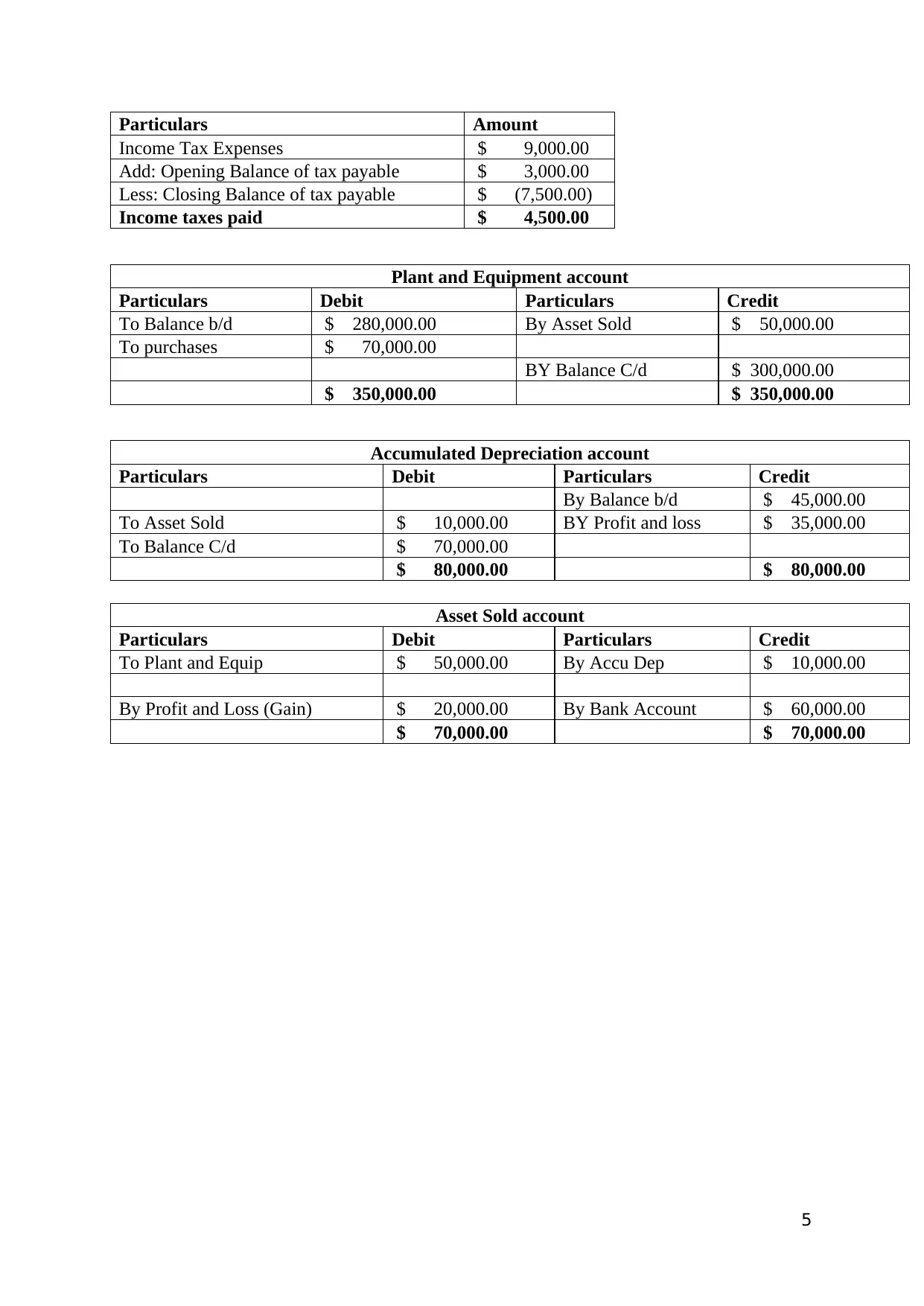

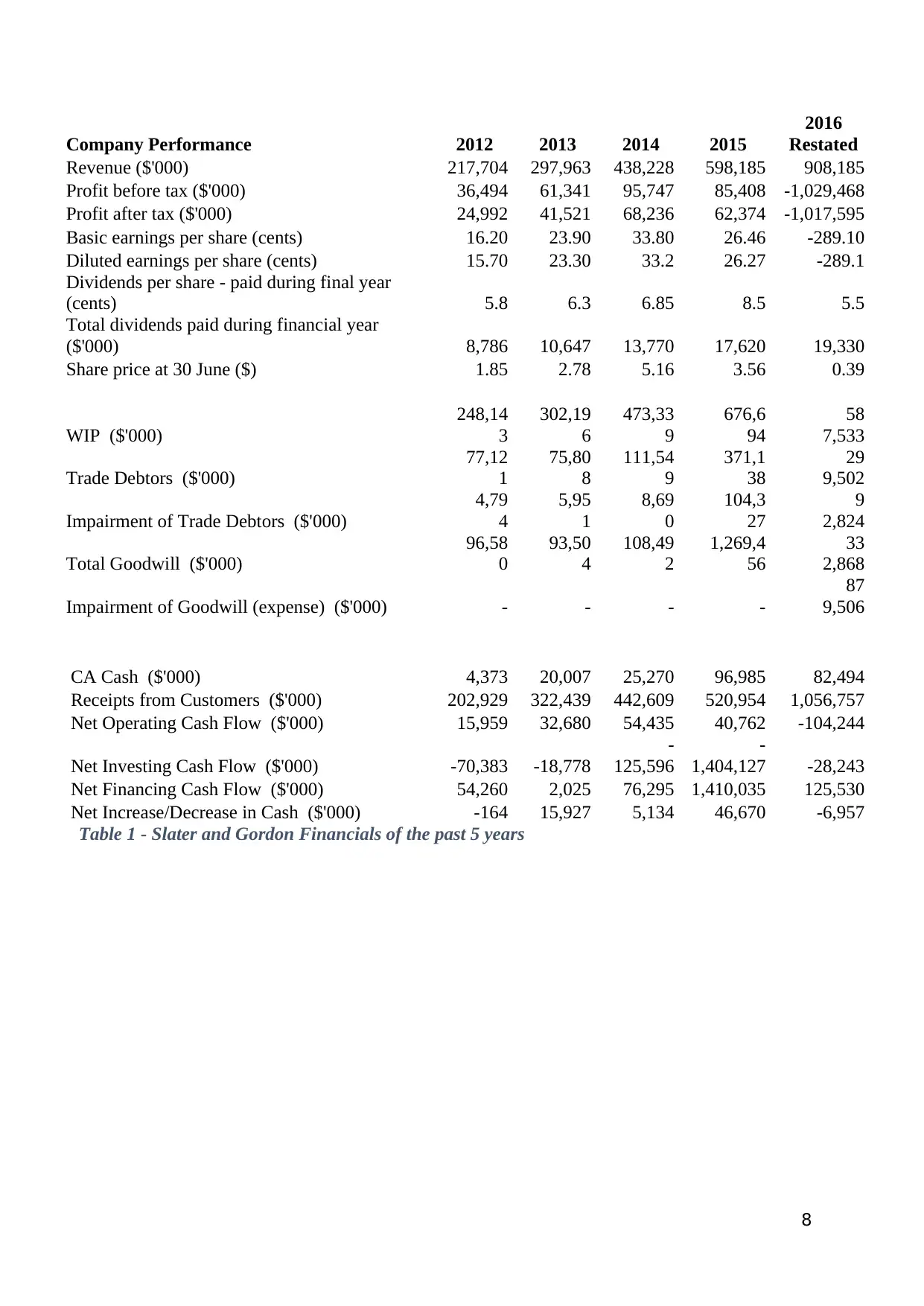

This assignment focuses on preparing a cash flow statement for Fast Feet Couriers Limited for the year ended 30 June 2017, utilizing the direct method as per AASB 107. It involves analyzing balance sheets, income statements, and additional financial information to calculate cash flows from operating, investing, and financing activities. The assignment requires students to complete the cash flow statement, including detailed workings for cash receipts from customers, cash paid to suppliers and employees, and income taxes paid. Furthermore, it includes a critical thinking section requiring an analysis of the accounting issues surrounding Slater and Gordon, evaluating the company's financial trends based on provided data and addressing the reasons for the company's decline and associated accounting irregularities and misleading investors.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.