Corporate and Financial Accounting Task 2022

VerifiedAdded on 2022/09/17

|11

|3503

|15

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate and financial accounting

Name of the student

Name of the university

Student ID

Author note

Corporate and financial accounting

Name of the student

Name of the university

Student ID

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CORPORATE AND FINANCIAL ACCOUNTING

Abstract

Aim of the task is to analyse the financial statements of 2 ASX listed entities Rio Tinto and

BHP Billiton for the past 3 years covering 2016 to 2018. The report will concentrate on

different items reported under the owner’s equity section and liability section of both the

entities and will report the movements for those amount along with the reasons behind the

same. Further, in next section the report will focus on small proprietary entity, large

proprietary entity and reporting entity ad the reporting requirements of these entities.

Abstract

Aim of the task is to analyse the financial statements of 2 ASX listed entities Rio Tinto and

BHP Billiton for the past 3 years covering 2016 to 2018. The report will concentrate on

different items reported under the owner’s equity section and liability section of both the

entities and will report the movements for those amount along with the reasons behind the

same. Further, in next section the report will focus on small proprietary entity, large

proprietary entity and reporting entity ad the reporting requirements of these entities.

2CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction............................................................................................................................3

Part A.....................................................................................................................................3

(i) Owner’s equity............................................................................................................3

(ii) Movement of each item under owner’s equity..........................................................4

(iii) Liability......................................................................................................................5

(iv) Movement of each item under owner’s equity..........................................................6

(v) Advantages and disadvantages of source of funds.................................................7

Part B.....................................................................................................................................8

Conclusion.............................................................................................................................9

Reference.............................................................................................................................10

Table of Contents

Introduction............................................................................................................................3

Part A.....................................................................................................................................3

(i) Owner’s equity............................................................................................................3

(ii) Movement of each item under owner’s equity..........................................................4

(iii) Liability......................................................................................................................5

(iv) Movement of each item under owner’s equity..........................................................6

(v) Advantages and disadvantages of source of funds.................................................7

Part B.....................................................................................................................................8

Conclusion.............................................................................................................................9

Reference.............................................................................................................................10

3CORPORATE AND FINANCIAL ACCOUNTING

Introduction

Being the pioneer in metal and mining sector, Rio Tinto is engaged in producing

essential material required for human progress. Major products of the organisation include

copper, aluminium, gold, diamond, uranium, iron ore and industrial materials including

titanium oxides, borates and salt. Minerals and metals produced by them plays major role

in hosting day to day items as well as innovative technologies. That assists in working in

modern life (Riotinto.com 2019). On the other hand, BHP Billiton that is the outcome of a

merger among Billiton and Broken Hill Proprietary (BHP). It is engaged in production of

copper, steel, silver, oil, gas and aluminium. It has interests in transportation and

engineering (BHP 2019.).

Part A

Balance sheet of the entity represents the shareholder’s equity, assets and liabilities

at a particular point of time and offers the basis to compute the return rate and analysis of

capital structure.

(i) Owner’s equity

Rio Tinto – looking into the balance sheet of Rio Tinto for the past 3 years covering the

years 2016 to 2018 it can be identified that the owner’s equity section of the balance sheet

includes the following items –

Share capital – share capital is the fund raised by the entity in exchange of

issuance of ownership interests in entity though shares. Generally there 2 types of

share capital including preferred stock and common stock. However share capital

of Rio Tinto only includes ordinary shares. An ordinary share that is also known as

common shares are with lower priority for the assets of the entity and receive only

dividends with the managements of the entity’s discretion (Williams and Dobelman

2017).

Share premium account – it represents the difference among the issue or

subscription price and share’s par value. This account is statutory reserve account

and is not distributable.

Other reserves – other reserves of Rio Tinto includes different reserves like capital

redemption reserves, cash flow hedge reserve, revaluation reserve on account of

available for sale and foreign currency translation reserve (Robinson et al. 2015).

Retained earnings – it is the profit generated by the firm which is not distributable to

the stockholders and is reported after making payment for dividends. If the entity

has large amount of retained earning balance it suggests that the entity is

financially healthy (Wahlen, Baginski and Bradshaw 2014)

BHP Billiton – looking into the balance sheet of BHP Billiton for the past 3 years covering

the years 2016 to 2018 it can be identified that the owner’s equity section of the balance

sheet includes the following items –

Share capital – share capital of BHP Billiton includes fully paid ordinary shares,

shares with special voting and preference shares. Shares with special voting are

issued by BHP Billiton and BHP Billiton Plc. jointly to facilitate the joint voting by the

shareholders. Preference shares are with the right of repayments for the value paid

up on nominal value and unpaid dividends, if any on prior basis against holder of

other share class in the instance of winding up or return of the capital (Hotchkiss,

Strömberg and Smith 2014)

Introduction

Being the pioneer in metal and mining sector, Rio Tinto is engaged in producing

essential material required for human progress. Major products of the organisation include

copper, aluminium, gold, diamond, uranium, iron ore and industrial materials including

titanium oxides, borates and salt. Minerals and metals produced by them plays major role

in hosting day to day items as well as innovative technologies. That assists in working in

modern life (Riotinto.com 2019). On the other hand, BHP Billiton that is the outcome of a

merger among Billiton and Broken Hill Proprietary (BHP). It is engaged in production of

copper, steel, silver, oil, gas and aluminium. It has interests in transportation and

engineering (BHP 2019.).

Part A

Balance sheet of the entity represents the shareholder’s equity, assets and liabilities

at a particular point of time and offers the basis to compute the return rate and analysis of

capital structure.

(i) Owner’s equity

Rio Tinto – looking into the balance sheet of Rio Tinto for the past 3 years covering the

years 2016 to 2018 it can be identified that the owner’s equity section of the balance sheet

includes the following items –

Share capital – share capital is the fund raised by the entity in exchange of

issuance of ownership interests in entity though shares. Generally there 2 types of

share capital including preferred stock and common stock. However share capital

of Rio Tinto only includes ordinary shares. An ordinary share that is also known as

common shares are with lower priority for the assets of the entity and receive only

dividends with the managements of the entity’s discretion (Williams and Dobelman

2017).

Share premium account – it represents the difference among the issue or

subscription price and share’s par value. This account is statutory reserve account

and is not distributable.

Other reserves – other reserves of Rio Tinto includes different reserves like capital

redemption reserves, cash flow hedge reserve, revaluation reserve on account of

available for sale and foreign currency translation reserve (Robinson et al. 2015).

Retained earnings – it is the profit generated by the firm which is not distributable to

the stockholders and is reported after making payment for dividends. If the entity

has large amount of retained earning balance it suggests that the entity is

financially healthy (Wahlen, Baginski and Bradshaw 2014)

BHP Billiton – looking into the balance sheet of BHP Billiton for the past 3 years covering

the years 2016 to 2018 it can be identified that the owner’s equity section of the balance

sheet includes the following items –

Share capital – share capital of BHP Billiton includes fully paid ordinary shares,

shares with special voting and preference shares. Shares with special voting are

issued by BHP Billiton and BHP Billiton Plc. jointly to facilitate the joint voting by the

shareholders. Preference shares are with the right of repayments for the value paid

up on nominal value and unpaid dividends, if any on prior basis against holder of

other share class in the instance of winding up or return of the capital (Hotchkiss,

Strömberg and Smith 2014)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CORPORATE AND FINANCIAL ACCOUNTING

Treasury shares – it is the part of shares that is kept by an entity as its own shares.

It generally comes from the part of float and the outstanding shares before it is

repurchased by the entity or that has not been issued to the public ever. While the

entity buys back these shares the same become (Schroeder, Clark and Cathey

2019)

Other reserves – other reserves of the entity includes share premium account,

employee share awards reserves, foreign currency translation reserves, hedging

reserves, financial asset reserves, non-controlling interest contribution reserves and

share buyback reserves

Retained earnings – it is the profits earned by the entity till closing of the year 2018

after deducting the amount of dividend and any amount distributed to the investors.

The same is adjusted if any entry is made that has an impact on the expense or

revenue account (Cao, Chychyla and Stewart 2015)

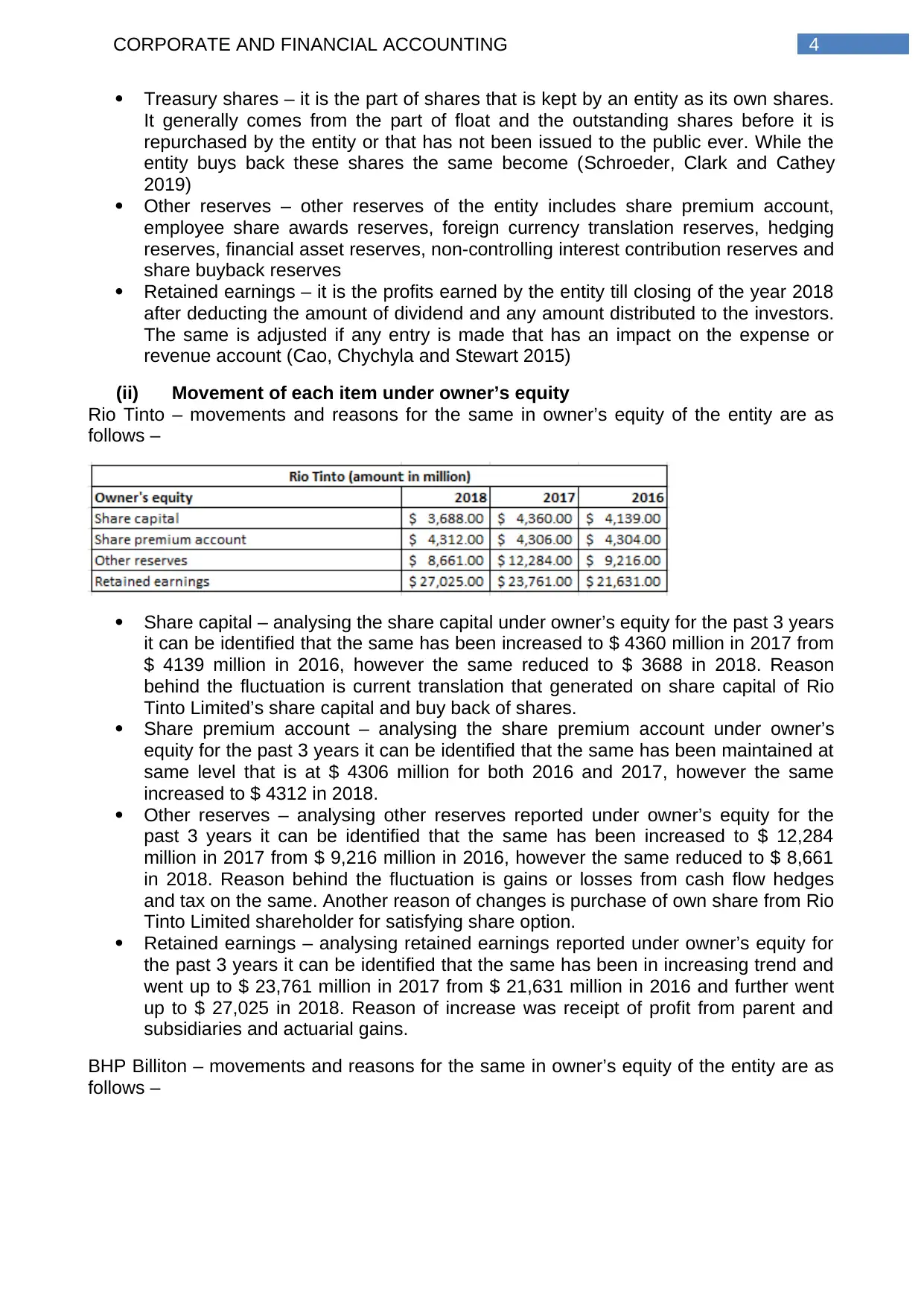

(ii) Movement of each item under owner’s equity

Rio Tinto – movements and reasons for the same in owner’s equity of the entity are as

follows –

Share capital – analysing the share capital under owner’s equity for the past 3 years

it can be identified that the same has been increased to $ 4360 million in 2017 from

$ 4139 million in 2016, however the same reduced to $ 3688 in 2018. Reason

behind the fluctuation is current translation that generated on share capital of Rio

Tinto Limited’s share capital and buy back of shares.

Share premium account – analysing the share premium account under owner’s

equity for the past 3 years it can be identified that the same has been maintained at

same level that is at $ 4306 million for both 2016 and 2017, however the same

increased to $ 4312 in 2018.

Other reserves – analysing other reserves reported under owner’s equity for the

past 3 years it can be identified that the same has been increased to $ 12,284

million in 2017 from $ 9,216 million in 2016, however the same reduced to $ 8,661

in 2018. Reason behind the fluctuation is gains or losses from cash flow hedges

and tax on the same. Another reason of changes is purchase of own share from Rio

Tinto Limited shareholder for satisfying share option.

Retained earnings – analysing retained earnings reported under owner’s equity for

the past 3 years it can be identified that the same has been in increasing trend and

went up to $ 23,761 million in 2017 from $ 21,631 million in 2016 and further went

up to $ 27,025 in 2018. Reason of increase was receipt of profit from parent and

subsidiaries and actuarial gains.

BHP Billiton – movements and reasons for the same in owner’s equity of the entity are as

follows –

Treasury shares – it is the part of shares that is kept by an entity as its own shares.

It generally comes from the part of float and the outstanding shares before it is

repurchased by the entity or that has not been issued to the public ever. While the

entity buys back these shares the same become (Schroeder, Clark and Cathey

2019)

Other reserves – other reserves of the entity includes share premium account,

employee share awards reserves, foreign currency translation reserves, hedging

reserves, financial asset reserves, non-controlling interest contribution reserves and

share buyback reserves

Retained earnings – it is the profits earned by the entity till closing of the year 2018

after deducting the amount of dividend and any amount distributed to the investors.

The same is adjusted if any entry is made that has an impact on the expense or

revenue account (Cao, Chychyla and Stewart 2015)

(ii) Movement of each item under owner’s equity

Rio Tinto – movements and reasons for the same in owner’s equity of the entity are as

follows –

Share capital – analysing the share capital under owner’s equity for the past 3 years

it can be identified that the same has been increased to $ 4360 million in 2017 from

$ 4139 million in 2016, however the same reduced to $ 3688 in 2018. Reason

behind the fluctuation is current translation that generated on share capital of Rio

Tinto Limited’s share capital and buy back of shares.

Share premium account – analysing the share premium account under owner’s

equity for the past 3 years it can be identified that the same has been maintained at

same level that is at $ 4306 million for both 2016 and 2017, however the same

increased to $ 4312 in 2018.

Other reserves – analysing other reserves reported under owner’s equity for the

past 3 years it can be identified that the same has been increased to $ 12,284

million in 2017 from $ 9,216 million in 2016, however the same reduced to $ 8,661

in 2018. Reason behind the fluctuation is gains or losses from cash flow hedges

and tax on the same. Another reason of changes is purchase of own share from Rio

Tinto Limited shareholder for satisfying share option.

Retained earnings – analysing retained earnings reported under owner’s equity for

the past 3 years it can be identified that the same has been in increasing trend and

went up to $ 23,761 million in 2017 from $ 21,631 million in 2016 and further went

up to $ 27,025 in 2018. Reason of increase was receipt of profit from parent and

subsidiaries and actuarial gains.

BHP Billiton – movements and reasons for the same in owner’s equity of the entity are as

follows –

5CORPORATE AND FINANCIAL ACCOUNTING

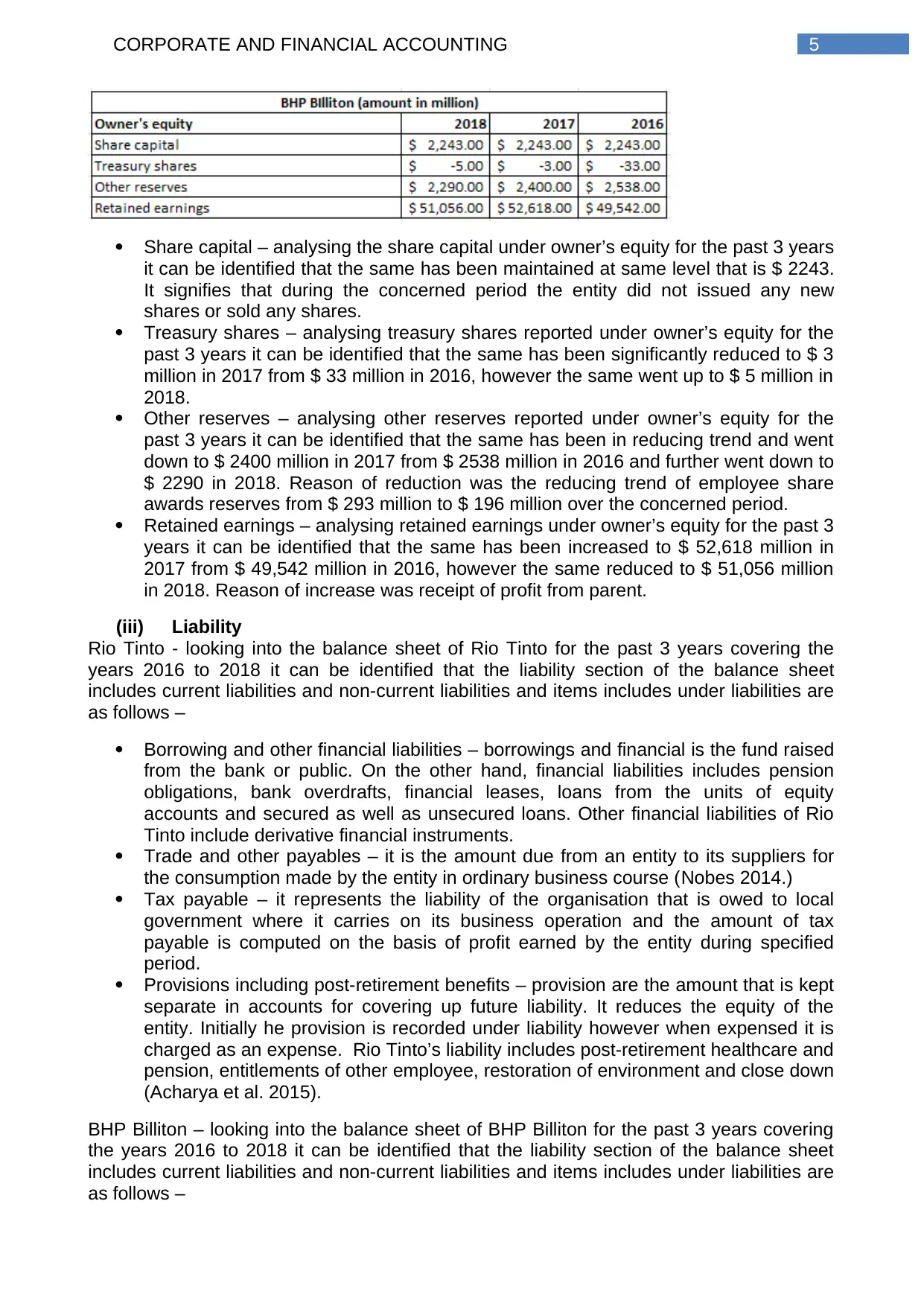

Share capital – analysing the share capital under owner’s equity for the past 3 years

it can be identified that the same has been maintained at same level that is $ 2243.

It signifies that during the concerned period the entity did not issued any new

shares or sold any shares.

Treasury shares – analysing treasury shares reported under owner’s equity for the

past 3 years it can be identified that the same has been significantly reduced to $ 3

million in 2017 from $ 33 million in 2016, however the same went up to $ 5 million in

2018.

Other reserves – analysing other reserves reported under owner’s equity for the

past 3 years it can be identified that the same has been in reducing trend and went

down to $ 2400 million in 2017 from $ 2538 million in 2016 and further went down to

$ 2290 in 2018. Reason of reduction was the reducing trend of employee share

awards reserves from $ 293 million to $ 196 million over the concerned period.

Retained earnings – analysing retained earnings under owner’s equity for the past 3

years it can be identified that the same has been increased to $ 52,618 million in

2017 from $ 49,542 million in 2016, however the same reduced to $ 51,056 million

in 2018. Reason of increase was receipt of profit from parent.

(iii) Liability

Rio Tinto - looking into the balance sheet of Rio Tinto for the past 3 years covering the

years 2016 to 2018 it can be identified that the liability section of the balance sheet

includes current liabilities and non-current liabilities and items includes under liabilities are

as follows –

Borrowing and other financial liabilities – borrowings and financial is the fund raised

from the bank or public. On the other hand, financial liabilities includes pension

obligations, bank overdrafts, financial leases, loans from the units of equity

accounts and secured as well as unsecured loans. Other financial liabilities of Rio

Tinto include derivative financial instruments.

Trade and other payables – it is the amount due from an entity to its suppliers for

the consumption made by the entity in ordinary business course (Nobes 2014.)

Tax payable – it represents the liability of the organisation that is owed to local

government where it carries on its business operation and the amount of tax

payable is computed on the basis of profit earned by the entity during specified

period.

Provisions including post-retirement benefits – provision are the amount that is kept

separate in accounts for covering up future liability. It reduces the equity of the

entity. Initially he provision is recorded under liability however when expensed it is

charged as an expense. Rio Tinto’s liability includes post-retirement healthcare and

pension, entitlements of other employee, restoration of environment and close down

(Acharya et al. 2015).

BHP Billiton – looking into the balance sheet of BHP Billiton for the past 3 years covering

the years 2016 to 2018 it can be identified that the liability section of the balance sheet

includes current liabilities and non-current liabilities and items includes under liabilities are

as follows –

Share capital – analysing the share capital under owner’s equity for the past 3 years

it can be identified that the same has been maintained at same level that is $ 2243.

It signifies that during the concerned period the entity did not issued any new

shares or sold any shares.

Treasury shares – analysing treasury shares reported under owner’s equity for the

past 3 years it can be identified that the same has been significantly reduced to $ 3

million in 2017 from $ 33 million in 2016, however the same went up to $ 5 million in

2018.

Other reserves – analysing other reserves reported under owner’s equity for the

past 3 years it can be identified that the same has been in reducing trend and went

down to $ 2400 million in 2017 from $ 2538 million in 2016 and further went down to

$ 2290 in 2018. Reason of reduction was the reducing trend of employee share

awards reserves from $ 293 million to $ 196 million over the concerned period.

Retained earnings – analysing retained earnings under owner’s equity for the past 3

years it can be identified that the same has been increased to $ 52,618 million in

2017 from $ 49,542 million in 2016, however the same reduced to $ 51,056 million

in 2018. Reason of increase was receipt of profit from parent.

(iii) Liability

Rio Tinto - looking into the balance sheet of Rio Tinto for the past 3 years covering the

years 2016 to 2018 it can be identified that the liability section of the balance sheet

includes current liabilities and non-current liabilities and items includes under liabilities are

as follows –

Borrowing and other financial liabilities – borrowings and financial is the fund raised

from the bank or public. On the other hand, financial liabilities includes pension

obligations, bank overdrafts, financial leases, loans from the units of equity

accounts and secured as well as unsecured loans. Other financial liabilities of Rio

Tinto include derivative financial instruments.

Trade and other payables – it is the amount due from an entity to its suppliers for

the consumption made by the entity in ordinary business course (Nobes 2014.)

Tax payable – it represents the liability of the organisation that is owed to local

government where it carries on its business operation and the amount of tax

payable is computed on the basis of profit earned by the entity during specified

period.

Provisions including post-retirement benefits – provision are the amount that is kept

separate in accounts for covering up future liability. It reduces the equity of the

entity. Initially he provision is recorded under liability however when expensed it is

charged as an expense. Rio Tinto’s liability includes post-retirement healthcare and

pension, entitlements of other employee, restoration of environment and close down

(Acharya et al. 2015).

BHP Billiton – looking into the balance sheet of BHP Billiton for the past 3 years covering

the years 2016 to 2018 it can be identified that the liability section of the balance sheet

includes current liabilities and non-current liabilities and items includes under liabilities are

as follows –

6CORPORATE AND FINANCIAL ACCOUNTING

Trade and other payables – as mentioned above for Rio Tinto

Interest bearing liabilities – BHP Billiton’s interest bearing liabilities include

debentures and notes, bank loans, short-term borrowings, bank overdraft and

finance leases.

Other financial liabilities – as mentioned above for Rio Tinto (Coleman, Cotei and

Farhat 2016)

Current tax and deferred tax – deferred tax I the tax liability that is due for current

period or assessed by has not been paid yet. Deferral generates from timing

difference between while tax is accrued and the same is paid.

Provisions – as mentioned above for Rio Tinto

Deferred income – deferred revenue or the unearned revenue is the advance

payments received by the entity for the service to be provided or goods to be

delivered in future period (Coleman, Cotei and Farhat 2016).

(iv) Movement of each item under owner’s equity

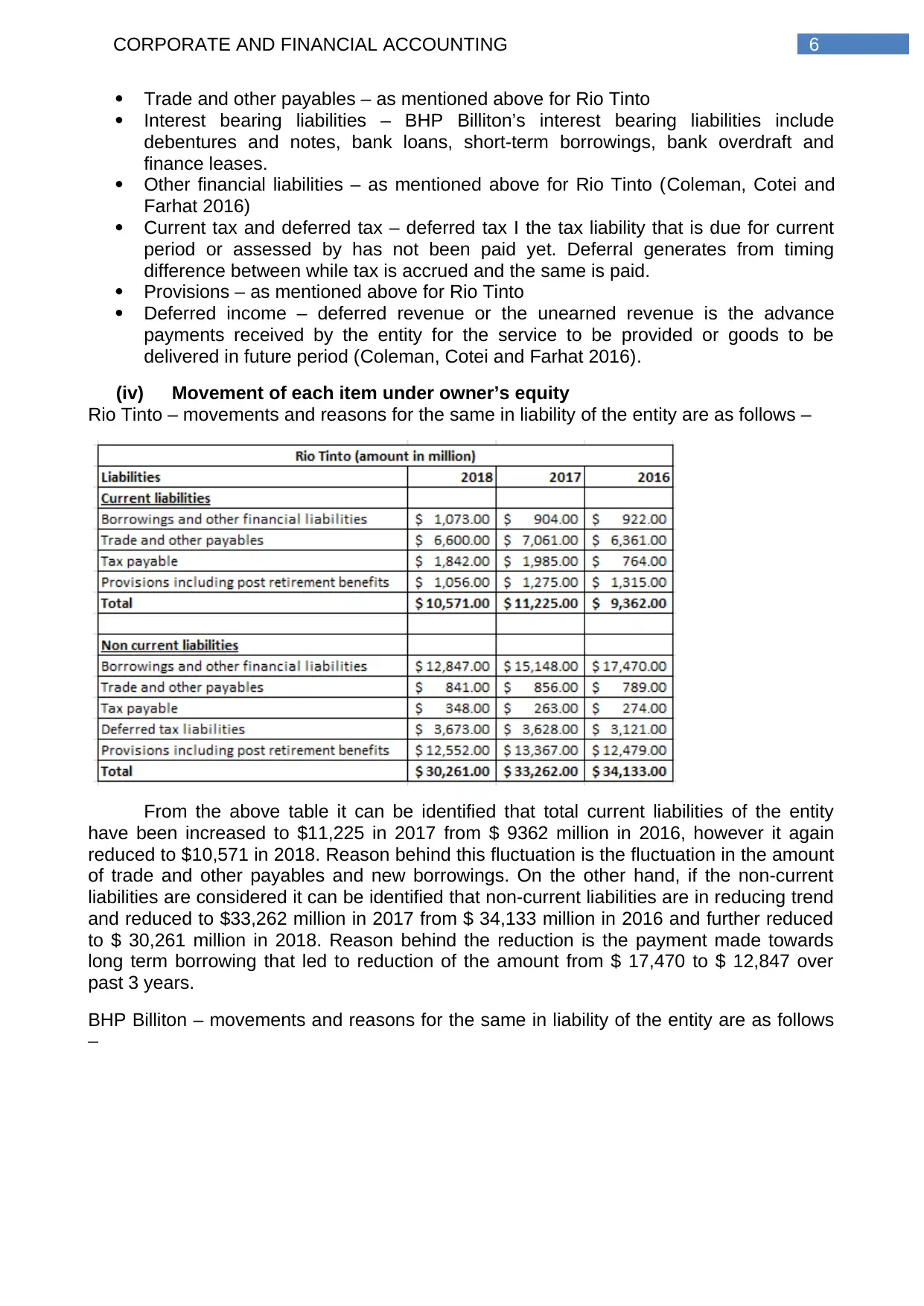

Rio Tinto – movements and reasons for the same in liability of the entity are as follows –

From the above table it can be identified that total current liabilities of the entity

have been increased to $11,225 in 2017 from $ 9362 million in 2016, however it again

reduced to $10,571 in 2018. Reason behind this fluctuation is the fluctuation in the amount

of trade and other payables and new borrowings. On the other hand, if the non-current

liabilities are considered it can be identified that non-current liabilities are in reducing trend

and reduced to $33,262 million in 2017 from $ 34,133 million in 2016 and further reduced

to $ 30,261 million in 2018. Reason behind the reduction is the payment made towards

long term borrowing that led to reduction of the amount from $ 17,470 to $ 12,847 over

past 3 years.

BHP Billiton – movements and reasons for the same in liability of the entity are as follows

–

Trade and other payables – as mentioned above for Rio Tinto

Interest bearing liabilities – BHP Billiton’s interest bearing liabilities include

debentures and notes, bank loans, short-term borrowings, bank overdraft and

finance leases.

Other financial liabilities – as mentioned above for Rio Tinto (Coleman, Cotei and

Farhat 2016)

Current tax and deferred tax – deferred tax I the tax liability that is due for current

period or assessed by has not been paid yet. Deferral generates from timing

difference between while tax is accrued and the same is paid.

Provisions – as mentioned above for Rio Tinto

Deferred income – deferred revenue or the unearned revenue is the advance

payments received by the entity for the service to be provided or goods to be

delivered in future period (Coleman, Cotei and Farhat 2016).

(iv) Movement of each item under owner’s equity

Rio Tinto – movements and reasons for the same in liability of the entity are as follows –

From the above table it can be identified that total current liabilities of the entity

have been increased to $11,225 in 2017 from $ 9362 million in 2016, however it again

reduced to $10,571 in 2018. Reason behind this fluctuation is the fluctuation in the amount

of trade and other payables and new borrowings. On the other hand, if the non-current

liabilities are considered it can be identified that non-current liabilities are in reducing trend

and reduced to $33,262 million in 2017 from $ 34,133 million in 2016 and further reduced

to $ 30,261 million in 2018. Reason behind the reduction is the payment made towards

long term borrowing that led to reduction of the amount from $ 17,470 to $ 12,847 over

past 3 years.

BHP Billiton – movements and reasons for the same in liability of the entity are as follows

–

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE AND FINANCIAL ACCOUNTING

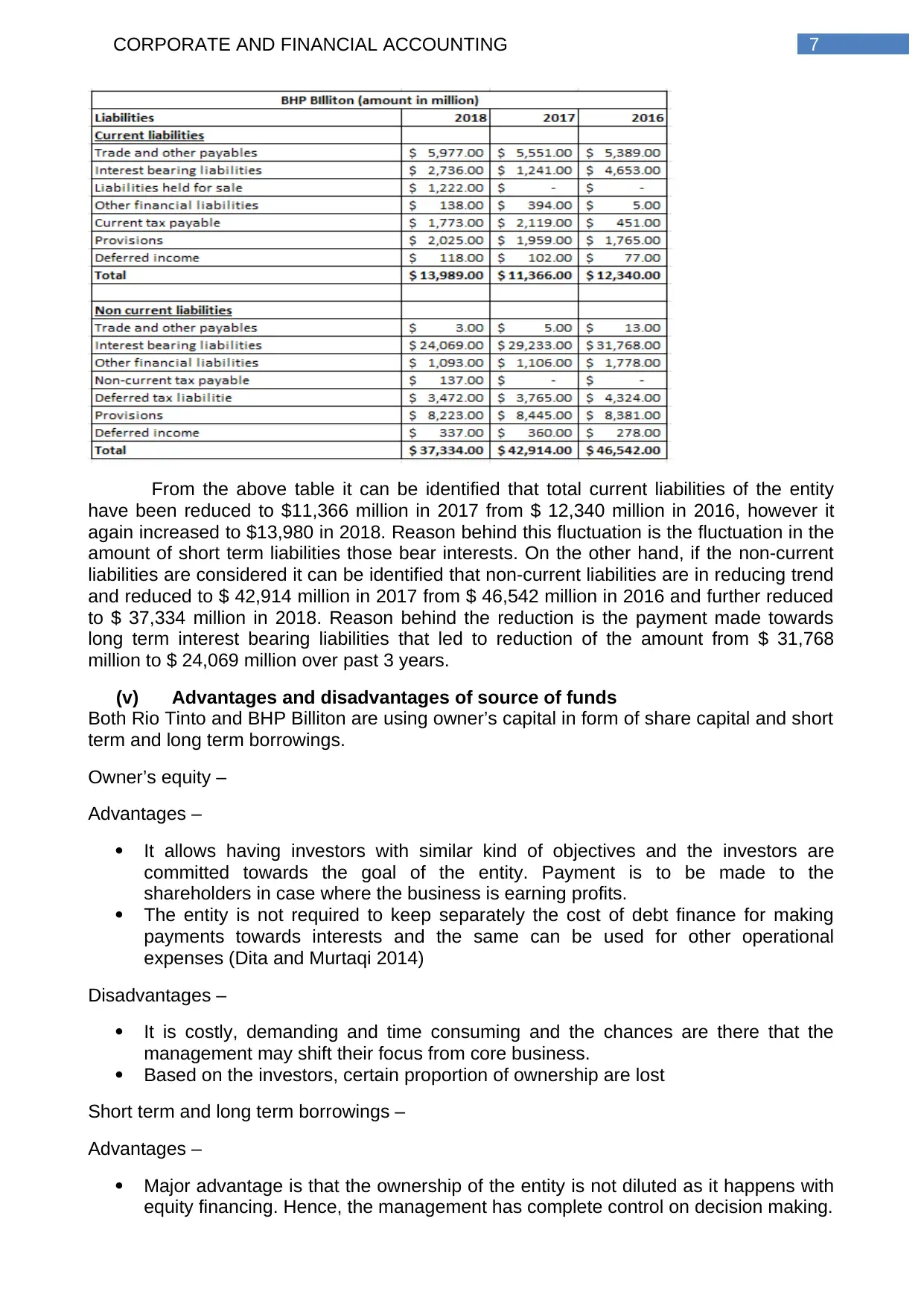

From the above table it can be identified that total current liabilities of the entity

have been reduced to $11,366 million in 2017 from $ 12,340 million in 2016, however it

again increased to $13,980 in 2018. Reason behind this fluctuation is the fluctuation in the

amount of short term liabilities those bear interests. On the other hand, if the non-current

liabilities are considered it can be identified that non-current liabilities are in reducing trend

and reduced to $ 42,914 million in 2017 from $ 46,542 million in 2016 and further reduced

to $ 37,334 million in 2018. Reason behind the reduction is the payment made towards

long term interest bearing liabilities that led to reduction of the amount from $ 31,768

million to $ 24,069 million over past 3 years.

(v) Advantages and disadvantages of source of funds

Both Rio Tinto and BHP Billiton are using owner’s capital in form of share capital and short

term and long term borrowings.

Owner’s equity –

Advantages –

It allows having investors with similar kind of objectives and the investors are

committed towards the goal of the entity. Payment is to be made to the

shareholders in case where the business is earning profits.

The entity is not required to keep separately the cost of debt finance for making

payments towards interests and the same can be used for other operational

expenses (Dita and Murtaqi 2014)

Disadvantages –

It is costly, demanding and time consuming and the chances are there that the

management may shift their focus from core business.

Based on the investors, certain proportion of ownership are lost

Short term and long term borrowings –

Advantages –

Major advantage is that the ownership of the entity is not diluted as it happens with

equity financing. Hence, the management has complete control on decision making.

From the above table it can be identified that total current liabilities of the entity

have been reduced to $11,366 million in 2017 from $ 12,340 million in 2016, however it

again increased to $13,980 in 2018. Reason behind this fluctuation is the fluctuation in the

amount of short term liabilities those bear interests. On the other hand, if the non-current

liabilities are considered it can be identified that non-current liabilities are in reducing trend

and reduced to $ 42,914 million in 2017 from $ 46,542 million in 2016 and further reduced

to $ 37,334 million in 2018. Reason behind the reduction is the payment made towards

long term interest bearing liabilities that led to reduction of the amount from $ 31,768

million to $ 24,069 million over past 3 years.

(v) Advantages and disadvantages of source of funds

Both Rio Tinto and BHP Billiton are using owner’s capital in form of share capital and short

term and long term borrowings.

Owner’s equity –

Advantages –

It allows having investors with similar kind of objectives and the investors are

committed towards the goal of the entity. Payment is to be made to the

shareholders in case where the business is earning profits.

The entity is not required to keep separately the cost of debt finance for making

payments towards interests and the same can be used for other operational

expenses (Dita and Murtaqi 2014)

Disadvantages –

It is costly, demanding and time consuming and the chances are there that the

management may shift their focus from core business.

Based on the investors, certain proportion of ownership are lost

Short term and long term borrowings –

Advantages –

Major advantage is that the ownership of the entity is not diluted as it happens with

equity financing. Hence, the management has complete control on decision making.

8CORPORATE AND FINANCIAL ACCOUNTING

Payments towards interest associated with debt financing are deductible under tax.

The business has the flexibility of raising through short term or long term as per its

requirements (Dita and Murtaqi 2014)

Disadvantages –

Business has to keep separately the amount to be paid as interest and principle

amount repayments.

It has adverse impact on the credit rating of the entity which in turn has to pay

higher interest if it issues debentures (Dita and Murtaqi 2014)

Part B

Small proprietary company – from the financial year starting from 1st July 2019 large

proprietary entity needs to satisfy at least 2 among below mentioned criteria –

Consolidated revenue of it is less than $ 25 million for the year under concern

Value of gross assets of it is less than $ 25 million

The entity has less than 100 employees (Asic.gov.au 2019).

Reporting requirements – it must prepare financial report prepared in compliance with Pt

2M.3 of Corporation Act 2001, must be audited if requested by ASIC under sec 294 (1) of

Corporation act, sent to the members within 4 months after the close of financial year if

requested by ASIC under sec 294 (1) of Corporation act lodged the same with ASIC if if

requested by ASIC under sec 294 (1) of Corporation act (Asic.gov.au 2019).

Large proprietary company – from the financial year starting from 1st July 2019 large

proprietary entity needs to satisfy at least 2 among below mentioned criteria –

Consolidated revenue of it and any other entity controlled by it is $ 50 million or

more

Value of gross consolidated assets of it and any other entity controlled by it is $ 25

million or more

The entity and any other entity controlled by it have 100 or more than 100

employees (Asic.gov.au 2019).

Reporting requirements – it must prepare the annual financial reports as per the

requirements of Chapter 2M of Corporation Act 200. Financial report of the entity shall be

audited unless the conditions as per ASIC Corporations (Audit Relief) Instrument 2016/784

are met, shall be lodged with the ASIC within 4 months of closing the financial year and

shall sent the same to the members within 4 months of closing the financial year

(Asic.gov.au 2019).

Reporting entity – it is the entity where it can be reasonably expected that the users are

dependent on GPFR (general purpose financial report) for gaining understanding of

financial position and the entity’s performance and taking decisions on the basis of

financial information (Asic.gov.au 2019).

Reporting requirements – it shall prepare GPFR in accordance with the statements of

accounting concepts as well as accounting standards (Asic.gov.au 2019).

Conclusion

It is concluded based on above discussion that for both Rio Tinto and BHP Billiton,

owner’s equity basically includes share capital, retied earnings and other reserves and

Payments towards interest associated with debt financing are deductible under tax.

The business has the flexibility of raising through short term or long term as per its

requirements (Dita and Murtaqi 2014)

Disadvantages –

Business has to keep separately the amount to be paid as interest and principle

amount repayments.

It has adverse impact on the credit rating of the entity which in turn has to pay

higher interest if it issues debentures (Dita and Murtaqi 2014)

Part B

Small proprietary company – from the financial year starting from 1st July 2019 large

proprietary entity needs to satisfy at least 2 among below mentioned criteria –

Consolidated revenue of it is less than $ 25 million for the year under concern

Value of gross assets of it is less than $ 25 million

The entity has less than 100 employees (Asic.gov.au 2019).

Reporting requirements – it must prepare financial report prepared in compliance with Pt

2M.3 of Corporation Act 2001, must be audited if requested by ASIC under sec 294 (1) of

Corporation act, sent to the members within 4 months after the close of financial year if

requested by ASIC under sec 294 (1) of Corporation act lodged the same with ASIC if if

requested by ASIC under sec 294 (1) of Corporation act (Asic.gov.au 2019).

Large proprietary company – from the financial year starting from 1st July 2019 large

proprietary entity needs to satisfy at least 2 among below mentioned criteria –

Consolidated revenue of it and any other entity controlled by it is $ 50 million or

more

Value of gross consolidated assets of it and any other entity controlled by it is $ 25

million or more

The entity and any other entity controlled by it have 100 or more than 100

employees (Asic.gov.au 2019).

Reporting requirements – it must prepare the annual financial reports as per the

requirements of Chapter 2M of Corporation Act 200. Financial report of the entity shall be

audited unless the conditions as per ASIC Corporations (Audit Relief) Instrument 2016/784

are met, shall be lodged with the ASIC within 4 months of closing the financial year and

shall sent the same to the members within 4 months of closing the financial year

(Asic.gov.au 2019).

Reporting entity – it is the entity where it can be reasonably expected that the users are

dependent on GPFR (general purpose financial report) for gaining understanding of

financial position and the entity’s performance and taking decisions on the basis of

financial information (Asic.gov.au 2019).

Reporting requirements – it shall prepare GPFR in accordance with the statements of

accounting concepts as well as accounting standards (Asic.gov.au 2019).

Conclusion

It is concluded based on above discussion that for both Rio Tinto and BHP Billiton,

owner’s equity basically includes share capital, retied earnings and other reserves and

9CORPORATE AND FINANCIAL ACCOUNTING

liabilities include short term and long-term borrowings, trade payables, tax payable and

provisions. Further, both the entities are using owner’s capital in form of share capital and

short term and long term borrowings.

liabilities include short term and long-term borrowings, trade payables, tax payable and

provisions. Further, both the entities are using owner’s capital in form of share capital and

short term and long term borrowings.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CORPORATE AND FINANCIAL ACCOUNTING

Reference

Acharya, V., Cecchetti, S.G., De Gregorio, J., Kalemli-Özcan, Ş., Lane, P.R. and Panizza,

U., 2015. Corporate debt in emerging economies: A threat to financial stability?.

Asic.gov.au. 2019. Are you a large or small proprietary company | ASIC - Australian

Securities and Investments Commission . [online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-

financial-reports/are-you-a-large-or-small-proprietary-company/ [Accessed 16 Sep. 2019].

Asic.gov.au. 2019. Lodgement of financial reports | ASIC - Australian Securities and

Investments Commission . [online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-

financial-reports/lodgement-of-financial-reports/ [Accessed 16 Sep. 2019].

BHP. 2019. BHP | A leading global resources company. [online] Available at:

https://www.bhp.com/ [Accessed 16 Sep. 2019].

Bloom, N., Sadun, R. and Van Reenen, J., 2015. Do private equity owned firms have

better management practices?. American Economic Review, 105(5), pp.442-46.

Cao, M., Chychyla, R. and Stewart, T., 2015. Big Data analytics in financial statement

audits. Accounting Horizons, 29(2), pp.423-429.

Coleman, S., Cotei, C. and Farhat, J., 2016. The debt-equity financing decisions of US

startup firms. Journal of Economics and Finance, 40(1), pp.105-126.

Dita, A.H. and Murtaqi, I., 2014. The Effect of Net Profit Margin, Price to Book Value and

Debt to Equity Ratio to Stock Return in the Indonesian Consumer Goods Industry. Journal

of Business and Management, 3(3), pp.305-315.

Hotchkiss, E.S., Strömberg, P. and Smith, D.C., 2014, March. Private equity and the

resolution of financial distress. In AFA 2012 Chicago Meetings Paper.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Riotinto.com. 2019. Global home. [online] Available at: https://www.riotinto.com/ [Accessed

16 Sep. 2019].

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Wahlen, J.M., Baginski, S.P. and Bradshaw, M., 2014. Financial reporting, financial

statement analysis and valuation. Nelson Education.

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World Scientific

Book Chapters, pp.109-169.

Reference

Acharya, V., Cecchetti, S.G., De Gregorio, J., Kalemli-Özcan, Ş., Lane, P.R. and Panizza,

U., 2015. Corporate debt in emerging economies: A threat to financial stability?.

Asic.gov.au. 2019. Are you a large or small proprietary company | ASIC - Australian

Securities and Investments Commission . [online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-

financial-reports/are-you-a-large-or-small-proprietary-company/ [Accessed 16 Sep. 2019].

Asic.gov.au. 2019. Lodgement of financial reports | ASIC - Australian Securities and

Investments Commission . [online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-

financial-reports/lodgement-of-financial-reports/ [Accessed 16 Sep. 2019].

BHP. 2019. BHP | A leading global resources company. [online] Available at:

https://www.bhp.com/ [Accessed 16 Sep. 2019].

Bloom, N., Sadun, R. and Van Reenen, J., 2015. Do private equity owned firms have

better management practices?. American Economic Review, 105(5), pp.442-46.

Cao, M., Chychyla, R. and Stewart, T., 2015. Big Data analytics in financial statement

audits. Accounting Horizons, 29(2), pp.423-429.

Coleman, S., Cotei, C. and Farhat, J., 2016. The debt-equity financing decisions of US

startup firms. Journal of Economics and Finance, 40(1), pp.105-126.

Dita, A.H. and Murtaqi, I., 2014. The Effect of Net Profit Margin, Price to Book Value and

Debt to Equity Ratio to Stock Return in the Indonesian Consumer Goods Industry. Journal

of Business and Management, 3(3), pp.305-315.

Hotchkiss, E.S., Strömberg, P. and Smith, D.C., 2014, March. Private equity and the

resolution of financial distress. In AFA 2012 Chicago Meetings Paper.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Riotinto.com. 2019. Global home. [online] Available at: https://www.riotinto.com/ [Accessed

16 Sep. 2019].

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Wahlen, J.M., Baginski, S.P. and Bradshaw, M., 2014. Financial reporting, financial

statement analysis and valuation. Nelson Education.

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World Scientific

Book Chapters, pp.109-169.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.