Assignment on Financial Management1

VerifiedAdded on 2022/04/04

|11

|1661

|14

Assignment

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Authors Note:

Financial Management

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL MANAGEMENT

1

Table of Contents

Question 1:.................................................................................................................................2

a) Long-term debt, first $550 000:.............................................................................................2

b) Long-term debt, greater than $550 000:................................................................................2

c) Preference shares, all amounts:..............................................................................................2

d) Ordinary share capital, first $1.75 million:............................................................................2

e) Ordinary share capital, greater than $1.75 million:...............................................................2

f) Breaking point:.......................................................................................................................3

g) WACC calculation:................................................................................................................3

h) Providing Graph.....................................................................................................................4

Question 2:.................................................................................................................................4

a) Calculating times interest earned ratio and providing explanations:....................................4

b) Market value of Tampa’s Equity under zero growth model:.................................................5

c) Recommending the best possible capital structure:...............................................................5

Question 3:.................................................................................................................................6

Bibliography:..............................................................................................................................9

1

Table of Contents

Question 1:.................................................................................................................................2

a) Long-term debt, first $550 000:.............................................................................................2

b) Long-term debt, greater than $550 000:................................................................................2

c) Preference shares, all amounts:..............................................................................................2

d) Ordinary share capital, first $1.75 million:............................................................................2

e) Ordinary share capital, greater than $1.75 million:...............................................................2

f) Breaking point:.......................................................................................................................3

g) WACC calculation:................................................................................................................3

h) Providing Graph.....................................................................................................................4

Question 2:.................................................................................................................................4

a) Calculating times interest earned ratio and providing explanations:....................................4

b) Market value of Tampa’s Equity under zero growth model:.................................................5

c) Recommending the best possible capital structure:...............................................................5

Question 3:.................................................................................................................................6

Bibliography:..............................................................................................................................9

FINANCIAL MANAGEMENT

2

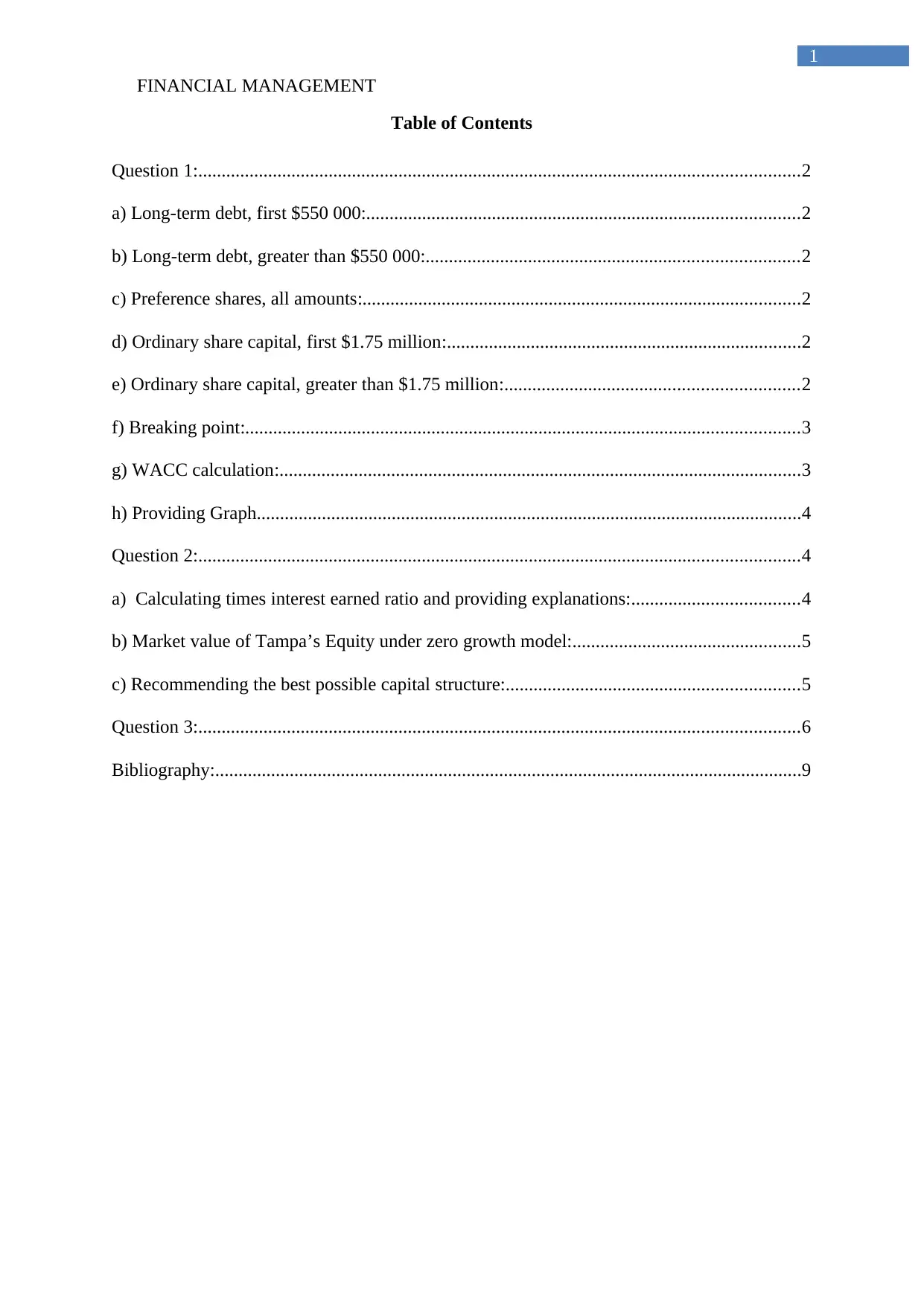

Question 1:

a) Long-term debt, first $550 000:

Particulars Value

Par 1000

Market value 960

Years 14

Coupon rate 9%

Coupon amount 90

Kd 9.48%

Long-term debt, first $550 000 5.69%

b) Long-term debt, greater than $550 000:

Particulars Value

Kd 14%

Tax 40%

Long-term debt, greater than $550 000 8.10%

c) Preference shares, all amounts:

Particulars Value

Dp 80

Np 75

Annual dividend % 14%

Dividend 11.2

Preferred stock, all amounts

14.93

%

d) Ordinary share capital, first $1.75 million:

Particulars Value

Expected dividends 0.96

Current share 14

Growth 12%

Ke (Ordinary share capital, first $1.75 million) 18.86%

e) Ordinary share capital, greater than $1.75 million:

Particulars Value

Expected dividends 0.96

Netting price 10

2

Question 1:

a) Long-term debt, first $550 000:

Particulars Value

Par 1000

Market value 960

Years 14

Coupon rate 9%

Coupon amount 90

Kd 9.48%

Long-term debt, first $550 000 5.69%

b) Long-term debt, greater than $550 000:

Particulars Value

Kd 14%

Tax 40%

Long-term debt, greater than $550 000 8.10%

c) Preference shares, all amounts:

Particulars Value

Dp 80

Np 75

Annual dividend % 14%

Dividend 11.2

Preferred stock, all amounts

14.93

%

d) Ordinary share capital, first $1.75 million:

Particulars Value

Expected dividends 0.96

Current share 14

Growth 12%

Ke (Ordinary share capital, first $1.75 million) 18.86%

e) Ordinary share capital, greater than $1.75 million:

Particulars Value

Expected dividends 0.96

Netting price 10

FINANCIAL MANAGEMENT

3

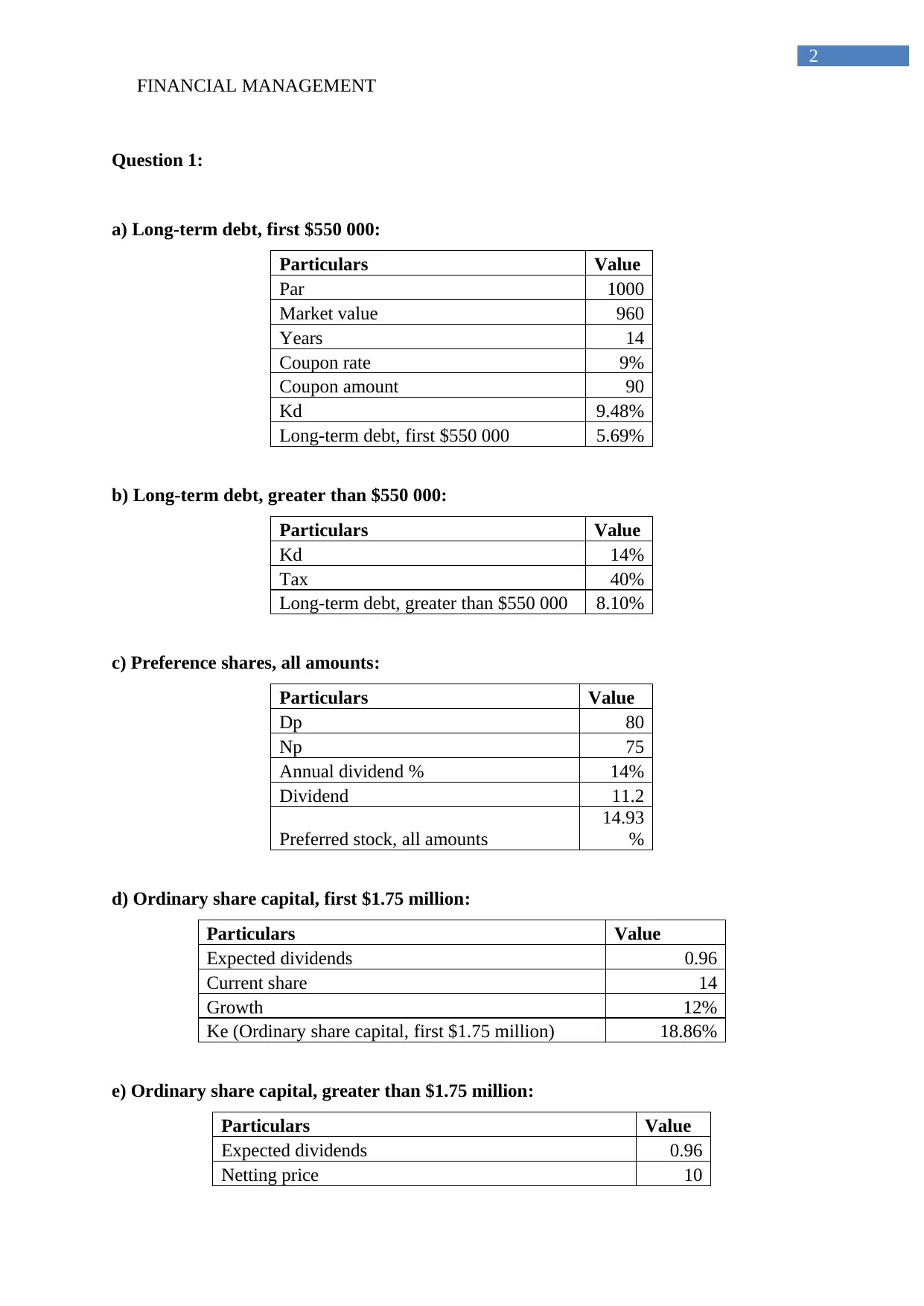

Growth 12%

Ke (Ordinary share capital, greater than $1.75

million) 21.60%

f) Breaking point:

Particulars Value

long term debt 550,000

Weight 35%

Breaking point 1,571,428.57

Particulars Value

long term debt 1,750,000

Weight 50%

Breaking point 3,500,000

g) WACC calculation:

Particulars

Targeted Capital

Structure

Cost of capital

source

Weighted

cost

From:$0 to $1,571,429

Long-term debt 30.00% 5.69% 1.71%

Preferred stock 10.00% 14.93% 1.49%

Common stock equity 60.00% 18.86% 11.31%

WACC 14.51%

From:$1,571,429 to

$3,500,000

Long-term debt 30.00% 8.10% 2.43%

Preferred stock 10.00% 14.93% 1.49%

Common stock equity 60.00% 18.86% 11.31%

WACC 15.24%

Above $3,500,000

Long-term debt 30.00% 8.10% 2.43%

Preferred stock 10.00% 14.93% 1.49%

Common stock equity 60.00% 21.60% 12.96%

WACC 16.88%

3

Growth 12%

Ke (Ordinary share capital, greater than $1.75

million) 21.60%

f) Breaking point:

Particulars Value

long term debt 550,000

Weight 35%

Breaking point 1,571,428.57

Particulars Value

long term debt 1,750,000

Weight 50%

Breaking point 3,500,000

g) WACC calculation:

Particulars

Targeted Capital

Structure

Cost of capital

source

Weighted

cost

From:$0 to $1,571,429

Long-term debt 30.00% 5.69% 1.71%

Preferred stock 10.00% 14.93% 1.49%

Common stock equity 60.00% 18.86% 11.31%

WACC 14.51%

From:$1,571,429 to

$3,500,000

Long-term debt 30.00% 8.10% 2.43%

Preferred stock 10.00% 14.93% 1.49%

Common stock equity 60.00% 18.86% 11.31%

WACC 15.24%

Above $3,500,000

Long-term debt 30.00% 8.10% 2.43%

Preferred stock 10.00% 14.93% 1.49%

Common stock equity 60.00% 21.60% 12.96%

WACC 16.88%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL MANAGEMENT

4

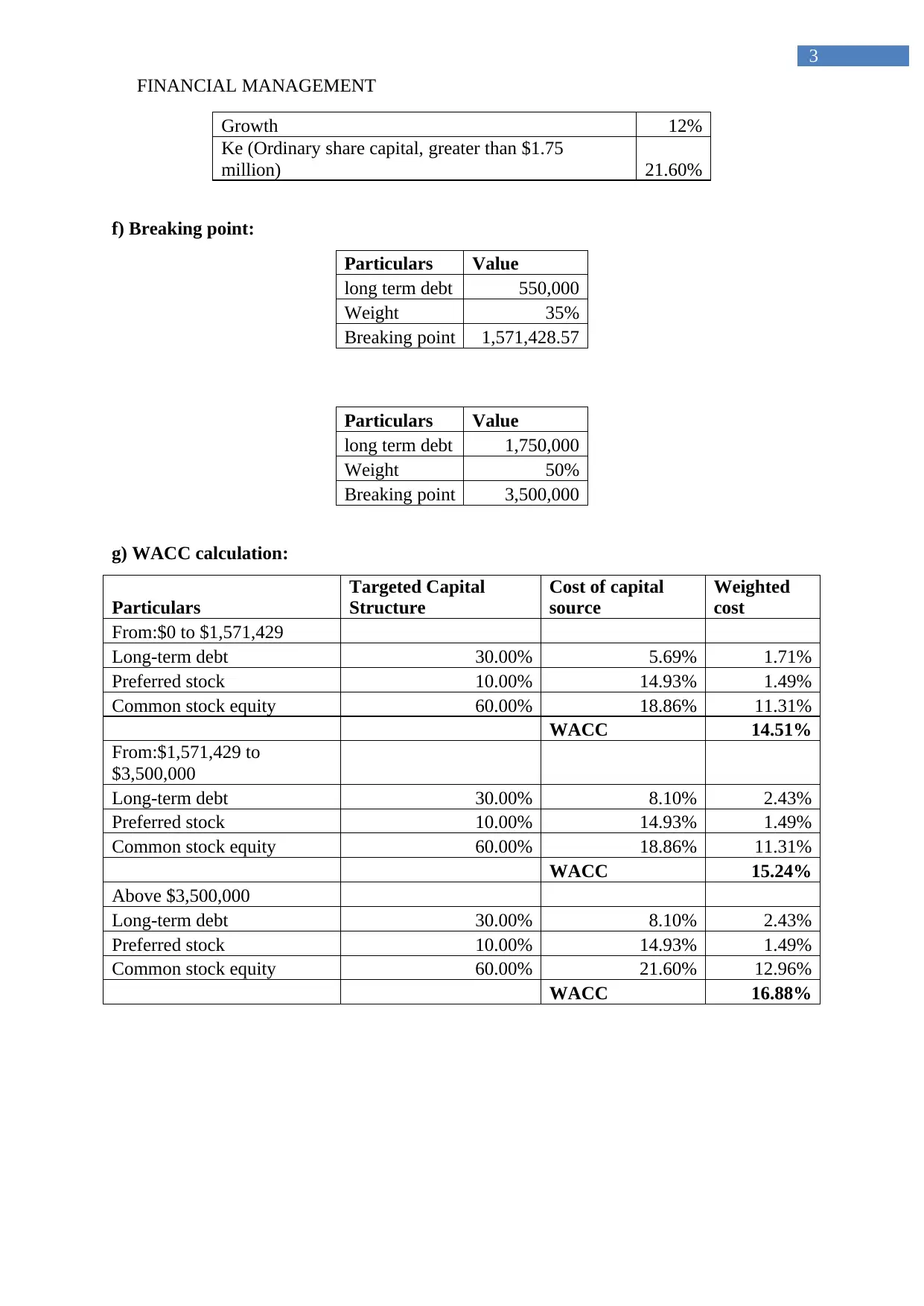

h) Providing Graph

$0 $1,000,000 $2,000,000 $3,000,000 $4,000,000 $5,000,000 $6,000,000 $7,000,000

13.00%

13.50%

14.00%

14.50%

15.00%

15.50%

16.00%

16.50%

17.00%

17.50%

WACC

$0 $1,000,000 $2,000,000 $3,000,000 $4,000,000 $5,000,000 $6,000,000 $7,000,000

13.00%

13.50%

14.00%

14.50%

15.00%

15.50%

16.00%

16.50%

17.00%

17.50%

0%

5%

10%

15%

20%

25%

30%

i) Recommendation for the investment option:

From calculation it can be detected that Project B,E,C,F,G and A can be selected for

the investment.

Question 2:

a) Calculating times interest earned ratio and providing explanations:

Capital Structure

Particulars Current-15% A-40% B-60%

Debt $1,000,000 $4,000,000 $6,000,000

4

h) Providing Graph

$0 $1,000,000 $2,000,000 $3,000,000 $4,000,000 $5,000,000 $6,000,000 $7,000,000

13.00%

13.50%

14.00%

14.50%

15.00%

15.50%

16.00%

16.50%

17.00%

17.50%

WACC

$0 $1,000,000 $2,000,000 $3,000,000 $4,000,000 $5,000,000 $6,000,000 $7,000,000

13.00%

13.50%

14.00%

14.50%

15.00%

15.50%

16.00%

16.50%

17.00%

17.50%

0%

5%

10%

15%

20%

25%

30%

i) Recommendation for the investment option:

From calculation it can be detected that Project B,E,C,F,G and A can be selected for

the investment.

Question 2:

a) Calculating times interest earned ratio and providing explanations:

Capital Structure

Particulars Current-15% A-40% B-60%

Debt $1,000,000 $4,000,000 $6,000,000

FINANCIAL MANAGEMENT

5

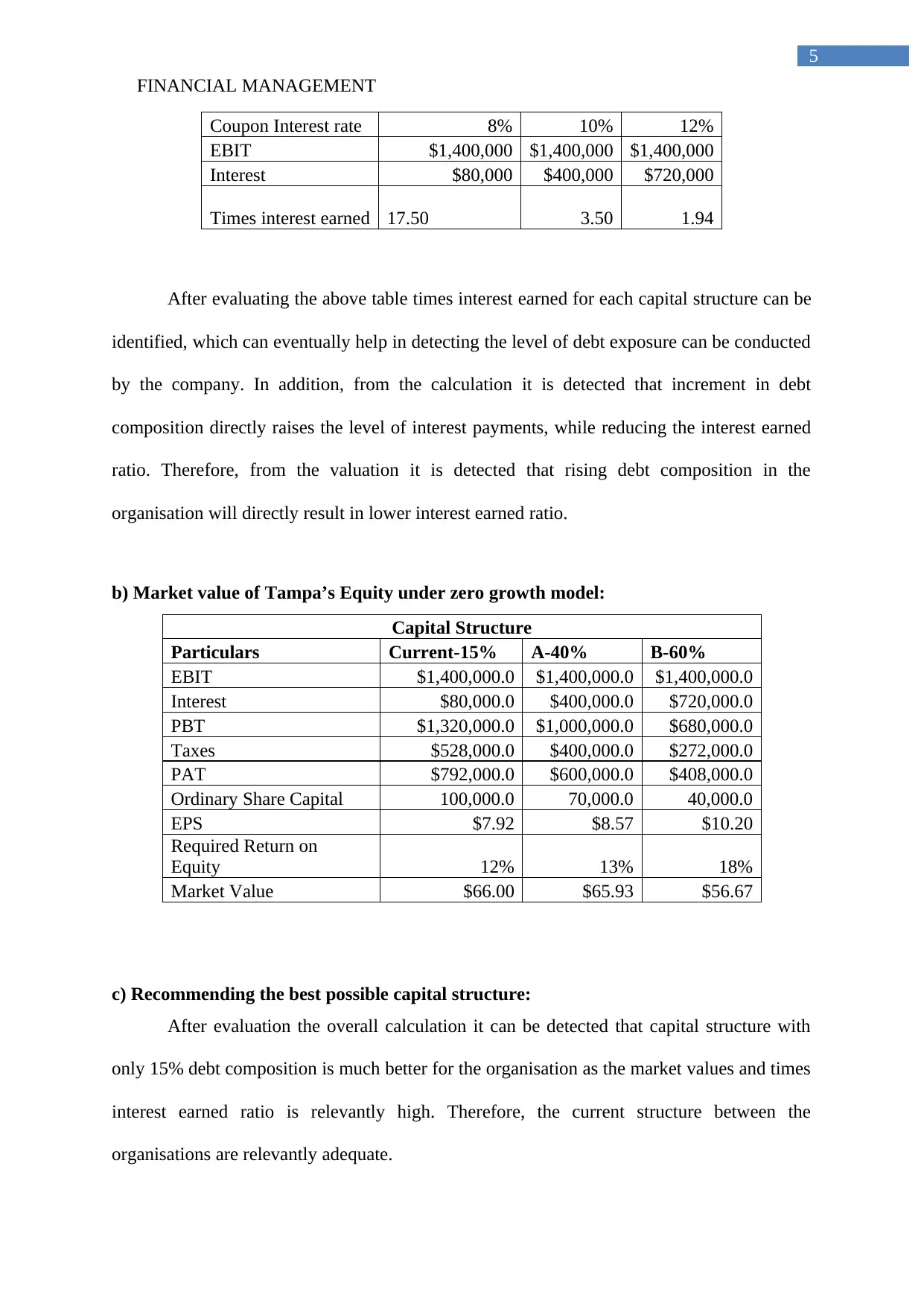

Coupon Interest rate 8% 10% 12%

EBIT $1,400,000 $1,400,000 $1,400,000

Interest $80,000 $400,000 $720,000

Times interest earned 17.50 3.50 1.94

After evaluating the above table times interest earned for each capital structure can be

identified, which can eventually help in detecting the level of debt exposure can be conducted

by the company. In addition, from the calculation it is detected that increment in debt

composition directly raises the level of interest payments, while reducing the interest earned

ratio. Therefore, from the valuation it is detected that rising debt composition in the

organisation will directly result in lower interest earned ratio.

b) Market value of Tampa’s Equity under zero growth model:

Capital Structure

Particulars Current-15% A-40% B-60%

EBIT $1,400,000.0 $1,400,000.0 $1,400,000.0

Interest $80,000.0 $400,000.0 $720,000.0

PBT $1,320,000.0 $1,000,000.0 $680,000.0

Taxes $528,000.0 $400,000.0 $272,000.0

PAT $792,000.0 $600,000.0 $408,000.0

Ordinary Share Capital 100,000.0 70,000.0 40,000.0

EPS $7.92 $8.57 $10.20

Required Return on

Equity 12% 13% 18%

Market Value $66.00 $65.93 $56.67

c) Recommending the best possible capital structure:

After evaluation the overall calculation it can be detected that capital structure with

only 15% debt composition is much better for the organisation as the market values and times

interest earned ratio is relevantly high. Therefore, the current structure between the

organisations are relevantly adequate.

5

Coupon Interest rate 8% 10% 12%

EBIT $1,400,000 $1,400,000 $1,400,000

Interest $80,000 $400,000 $720,000

Times interest earned 17.50 3.50 1.94

After evaluating the above table times interest earned for each capital structure can be

identified, which can eventually help in detecting the level of debt exposure can be conducted

by the company. In addition, from the calculation it is detected that increment in debt

composition directly raises the level of interest payments, while reducing the interest earned

ratio. Therefore, from the valuation it is detected that rising debt composition in the

organisation will directly result in lower interest earned ratio.

b) Market value of Tampa’s Equity under zero growth model:

Capital Structure

Particulars Current-15% A-40% B-60%

EBIT $1,400,000.0 $1,400,000.0 $1,400,000.0

Interest $80,000.0 $400,000.0 $720,000.0

PBT $1,320,000.0 $1,000,000.0 $680,000.0

Taxes $528,000.0 $400,000.0 $272,000.0

PAT $792,000.0 $600,000.0 $408,000.0

Ordinary Share Capital 100,000.0 70,000.0 40,000.0

EPS $7.92 $8.57 $10.20

Required Return on

Equity 12% 13% 18%

Market Value $66.00 $65.93 $56.67

c) Recommending the best possible capital structure:

After evaluation the overall calculation it can be detected that capital structure with

only 15% debt composition is much better for the organisation as the market values and times

interest earned ratio is relevantly high. Therefore, the current structure between the

organisations are relevantly adequate.

FINANCIAL MANAGEMENT

6

Question 3:

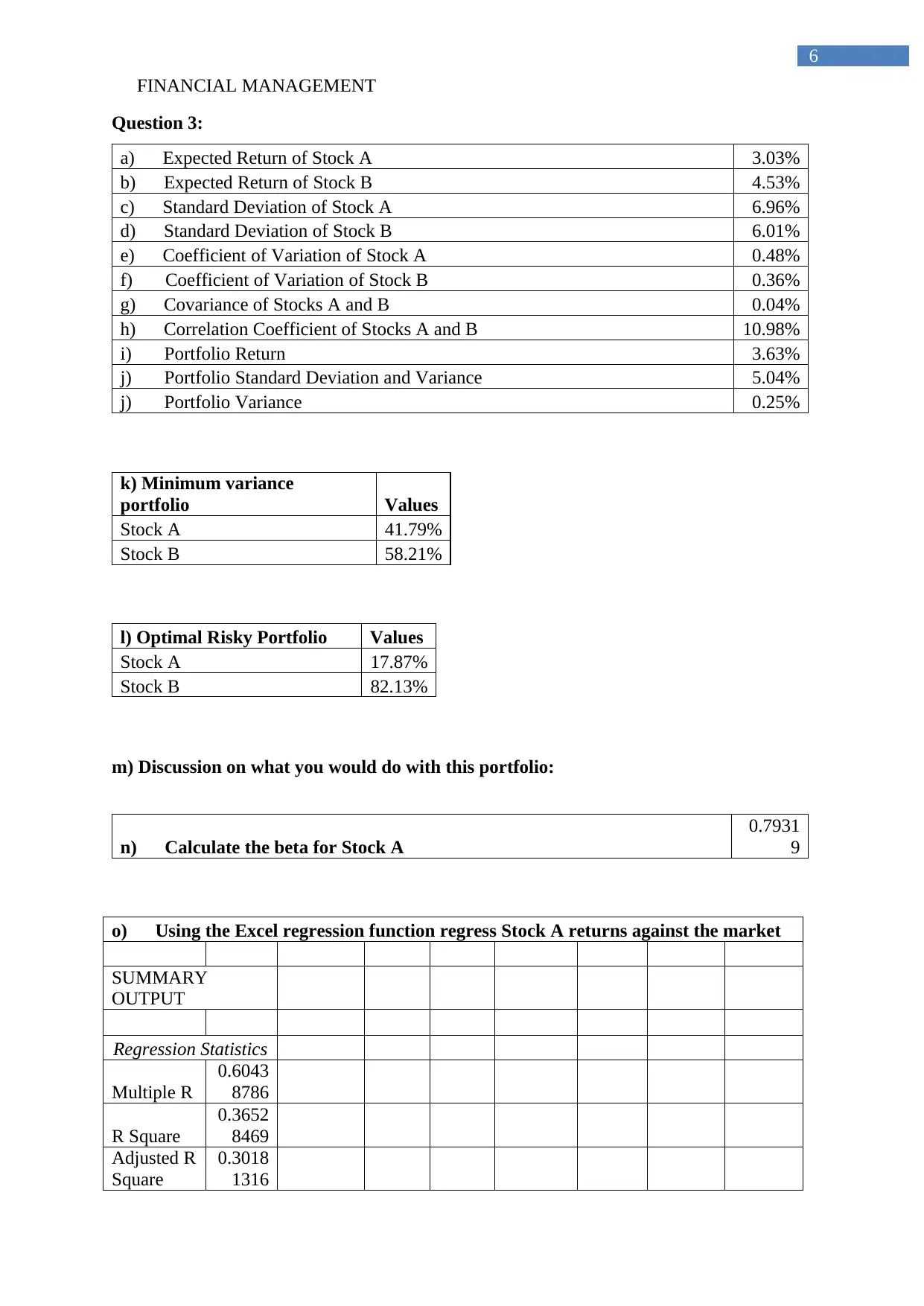

a) Expected Return of Stock A 3.03%

b) Expected Return of Stock B 4.53%

c) Standard Deviation of Stock A 6.96%

d) Standard Deviation of Stock B 6.01%

e) Coefficient of Variation of Stock A 0.48%

f) Coefficient of Variation of Stock B 0.36%

g) Covariance of Stocks A and B 0.04%

h) Correlation Coefficient of Stocks A and B 10.98%

i) Portfolio Return 3.63%

j) Portfolio Standard Deviation and Variance 5.04%

j) Portfolio Variance 0.25%

k) Minimum variance

portfolio Values

Stock A 41.79%

Stock B 58.21%

l) Optimal Risky Portfolio Values

Stock A 17.87%

Stock B 82.13%

m) Discussion on what you would do with this portfolio:

n) Calculate the beta for Stock A

0.7931

9

o) Using the Excel regression function regress Stock A returns against the market

SUMMARY

OUTPUT

Regression Statistics

Multiple R

0.6043

8786

R Square

0.3652

8469

Adjusted R

Square

0.3018

1316

6

Question 3:

a) Expected Return of Stock A 3.03%

b) Expected Return of Stock B 4.53%

c) Standard Deviation of Stock A 6.96%

d) Standard Deviation of Stock B 6.01%

e) Coefficient of Variation of Stock A 0.48%

f) Coefficient of Variation of Stock B 0.36%

g) Covariance of Stocks A and B 0.04%

h) Correlation Coefficient of Stocks A and B 10.98%

i) Portfolio Return 3.63%

j) Portfolio Standard Deviation and Variance 5.04%

j) Portfolio Variance 0.25%

k) Minimum variance

portfolio Values

Stock A 41.79%

Stock B 58.21%

l) Optimal Risky Portfolio Values

Stock A 17.87%

Stock B 82.13%

m) Discussion on what you would do with this portfolio:

n) Calculate the beta for Stock A

0.7931

9

o) Using the Excel regression function regress Stock A returns against the market

SUMMARY

OUTPUT

Regression Statistics

Multiple R

0.6043

8786

R Square

0.3652

8469

Adjusted R

Square

0.3018

1316

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL MANAGEMENT

7

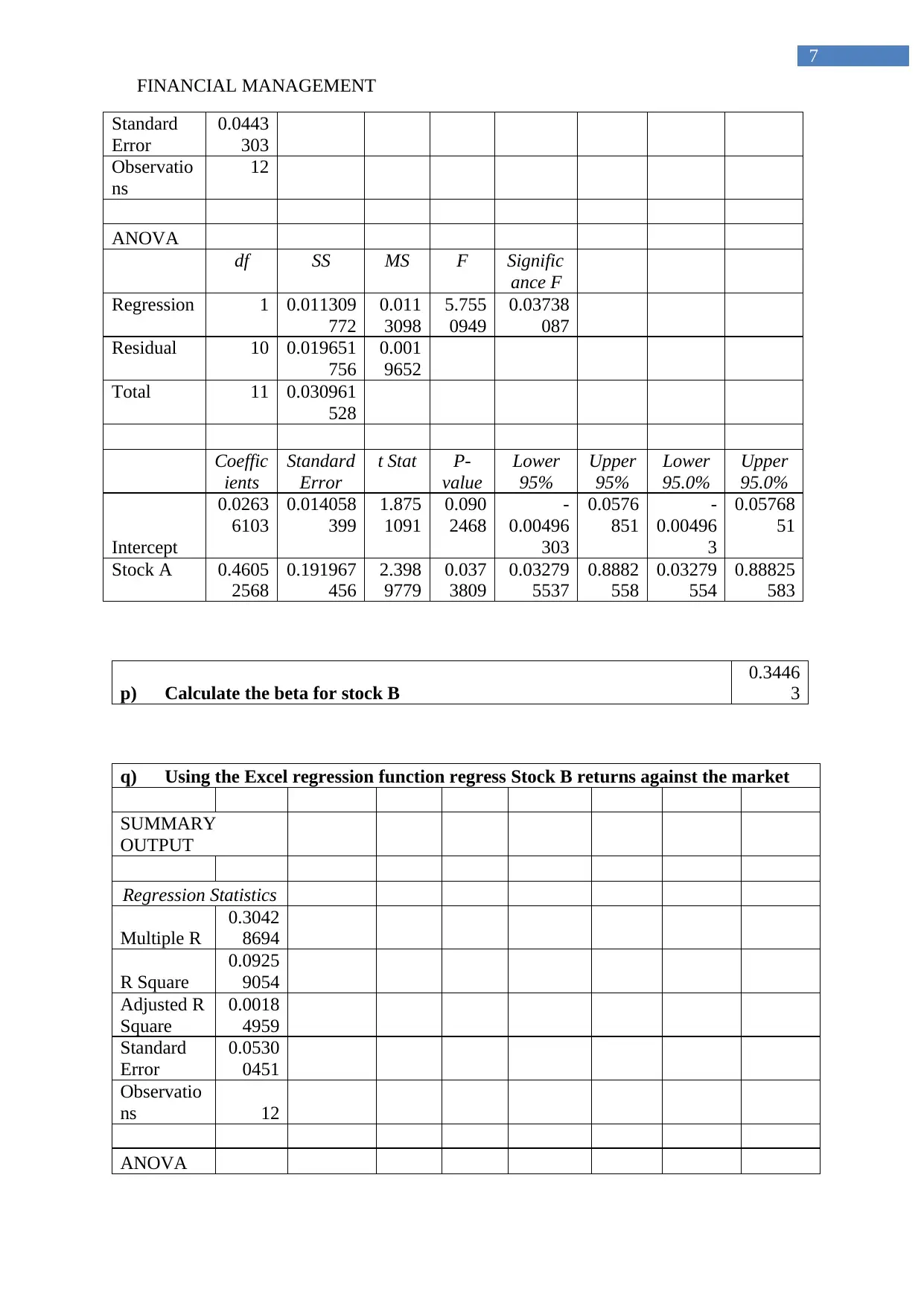

Standard

Error

0.0443

303

Observatio

ns

12

ANOVA

df SS MS F Signific

ance F

Regression 1 0.011309

772

0.011

3098

5.755

0949

0.03738

087

Residual 10 0.019651

756

0.001

9652

Total 11 0.030961

528

Coeffic

ients

Standard

Error

t Stat P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

0.0263

6103

0.014058

399

1.875

1091

0.090

2468

-

0.00496

303

0.0576

851

-

0.00496

3

0.05768

51

Stock A 0.4605

2568

0.191967

456

2.398

9779

0.037

3809

0.03279

5537

0.8882

558

0.03279

554

0.88825

583

p) Calculate the beta for stock B

0.3446

3

q) Using the Excel regression function regress Stock B returns against the market

SUMMARY

OUTPUT

Regression Statistics

Multiple R

0.3042

8694

R Square

0.0925

9054

Adjusted R

Square

0.0018

4959

Standard

Error

0.0530

0451

Observatio

ns 12

ANOVA

7

Standard

Error

0.0443

303

Observatio

ns

12

ANOVA

df SS MS F Signific

ance F

Regression 1 0.011309

772

0.011

3098

5.755

0949

0.03738

087

Residual 10 0.019651

756

0.001

9652

Total 11 0.030961

528

Coeffic

ients

Standard

Error

t Stat P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

0.0263

6103

0.014058

399

1.875

1091

0.090

2468

-

0.00496

303

0.0576

851

-

0.00496

3

0.05768

51

Stock A 0.4605

2568

0.191967

456

2.398

9779

0.037

3809

0.03279

5537

0.8882

558

0.03279

554

0.88825

583

p) Calculate the beta for stock B

0.3446

3

q) Using the Excel regression function regress Stock B returns against the market

SUMMARY

OUTPUT

Regression Statistics

Multiple R

0.3042

8694

R Square

0.0925

9054

Adjusted R

Square

0.0018

4959

Standard

Error

0.0530

0451

Observatio

ns 12

ANOVA

FINANCIAL MANAGEMENT

8

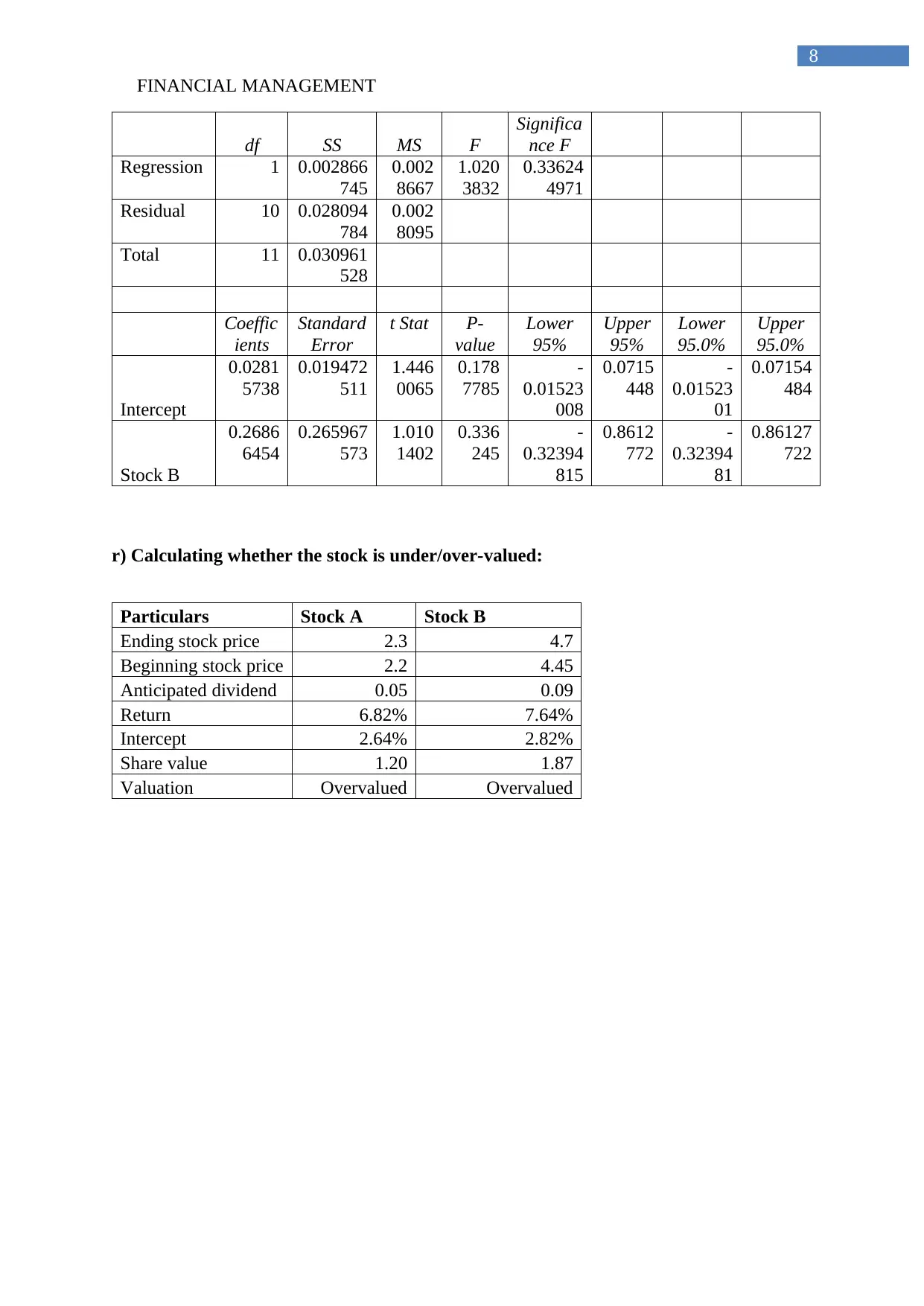

df SS MS F

Significa

nce F

Regression 1 0.002866

745

0.002

8667

1.020

3832

0.33624

4971

Residual 10 0.028094

784

0.002

8095

Total 11 0.030961

528

Coeffic

ients

Standard

Error

t Stat P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

0.0281

5738

0.019472

511

1.446

0065

0.178

7785

-

0.01523

008

0.0715

448

-

0.01523

01

0.07154

484

Stock B

0.2686

6454

0.265967

573

1.010

1402

0.336

245

-

0.32394

815

0.8612

772

-

0.32394

81

0.86127

722

r) Calculating whether the stock is under/over-valued:

Particulars Stock A Stock B

Ending stock price 2.3 4.7

Beginning stock price 2.2 4.45

Anticipated dividend 0.05 0.09

Return 6.82% 7.64%

Intercept 2.64% 2.82%

Share value 1.20 1.87

Valuation Overvalued Overvalued

8

df SS MS F

Significa

nce F

Regression 1 0.002866

745

0.002

8667

1.020

3832

0.33624

4971

Residual 10 0.028094

784

0.002

8095

Total 11 0.030961

528

Coeffic

ients

Standard

Error

t Stat P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept

0.0281

5738

0.019472

511

1.446

0065

0.178

7785

-

0.01523

008

0.0715

448

-

0.01523

01

0.07154

484

Stock B

0.2686

6454

0.265967

573

1.010

1402

0.336

245

-

0.32394

815

0.8612

772

-

0.32394

81

0.86127

722

r) Calculating whether the stock is under/over-valued:

Particulars Stock A Stock B

Ending stock price 2.3 4.7

Beginning stock price 2.2 4.45

Anticipated dividend 0.05 0.09

Return 6.82% 7.64%

Intercept 2.64% 2.82%

Share value 1.20 1.87

Valuation Overvalued Overvalued

FINANCIAL MANAGEMENT

9

Bibliography:

Baker, M., & Wurgler, J. (2015). Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. American Economic

Review, 105(5), 315-20.

Balios, D., Daskalakis, N., Eriotis, N., & Vasiliou, D. (2016). SMEs capital structure

determinants during severe economic crisis: The case of Greece. Cogent Economics &

Finance, 4(1), 1145535.

Berger, P. G., Chen, H. J., & Li, F. (2018). Firm specific information and the cost of equity

capital. Feng, Firm Specific Information and the Cost of Equity Capital (April 2,

2018).

Core, J. E., Hail, L., & Verdi, R. S. (2015). Mandatory disclosure quality, inside ownership,

and cost of capital. European Accounting Review, 24(1), 1-29.

Daskalakis, N., Balios, D., & Dalla, V. (2017). The behaviour of SMEs' capital structure

determinants in different macroeconomic states. Journal of Corporate Finance, 46,

248-260.

Frank, M. Z., & Shen, T. (2016). Investment and the weighted average cost of

capital. Journal of Financial Economics, 119(2), 300-315.

Graham, J. R., Leary, M. T., & Roberts, M. R. (2015). A century of capital structure: The

leveraging of corporate America. Journal of Financial Economics, 118(3), 658-683.

Hadi, A. R. A., & Suryanto, T. (2017). Capital Structure Determinants: Evidence From

Palestine and Egypt Stock Exchanges. IKONOMIKA, 1(2), 118-130.

9

Bibliography:

Baker, M., & Wurgler, J. (2015). Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. American Economic

Review, 105(5), 315-20.

Balios, D., Daskalakis, N., Eriotis, N., & Vasiliou, D. (2016). SMEs capital structure

determinants during severe economic crisis: The case of Greece. Cogent Economics &

Finance, 4(1), 1145535.

Berger, P. G., Chen, H. J., & Li, F. (2018). Firm specific information and the cost of equity

capital. Feng, Firm Specific Information and the Cost of Equity Capital (April 2,

2018).

Core, J. E., Hail, L., & Verdi, R. S. (2015). Mandatory disclosure quality, inside ownership,

and cost of capital. European Accounting Review, 24(1), 1-29.

Daskalakis, N., Balios, D., & Dalla, V. (2017). The behaviour of SMEs' capital structure

determinants in different macroeconomic states. Journal of Corporate Finance, 46,

248-260.

Frank, M. Z., & Shen, T. (2016). Investment and the weighted average cost of

capital. Journal of Financial Economics, 119(2), 300-315.

Graham, J. R., Leary, M. T., & Roberts, M. R. (2015). A century of capital structure: The

leveraging of corporate America. Journal of Financial Economics, 118(3), 658-683.

Hadi, A. R. A., & Suryanto, T. (2017). Capital Structure Determinants: Evidence From

Palestine and Egypt Stock Exchanges. IKONOMIKA, 1(2), 118-130.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL MANAGEMENT

10

Kanatani, M., & Yaghoubi, R. (2017). Determinants of Corporate Capital Structure in New

Zealand. AMR, 1.

Maillet, B., Tokpavi, S., & Vaucher, B. (2015). Global minimum variance portfolio

optimisation under some model risk: A robust regression-based approach. European

Journal of Operational Research, 244(1), 289-299.

Onaolapo, A. A., Kajola, S. O., & Nwidobie, M. B. (2015). Determinants of capital structure:

A study of Nigerian quoted companies. Methodology, 7, 23.

Yang, L., Couillet, R., & McKay, M. R. (2015). A robust statistics approach to minimum

variance portfolio optimization. IEEE Transactions on Signal Processing, 63(24),

6684-6697.

10

Kanatani, M., & Yaghoubi, R. (2017). Determinants of Corporate Capital Structure in New

Zealand. AMR, 1.

Maillet, B., Tokpavi, S., & Vaucher, B. (2015). Global minimum variance portfolio

optimisation under some model risk: A robust regression-based approach. European

Journal of Operational Research, 244(1), 289-299.

Onaolapo, A. A., Kajola, S. O., & Nwidobie, M. B. (2015). Determinants of capital structure:

A study of Nigerian quoted companies. Methodology, 7, 23.

Yang, L., Couillet, R., & McKay, M. R. (2015). A robust statistics approach to minimum

variance portfolio optimization. IEEE Transactions on Signal Processing, 63(24),

6684-6697.

1 out of 11

Related Documents

![[SOLVED] JB HiFi Ltd Investment Analysis](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fwh%2F8a736aa746774d07b1a1dbe34576782e.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.