Indirect Tax: VAT Regulations, Calculations, and Reporting for Finance

VerifiedAdded on 2020/10/05

|13

|3782

|329

Report

AI Summary

This report provides a comprehensive overview of indirect tax, specifically focusing on Value Added Tax (VAT). It begins with an introduction to indirect tax and its significance, followed by an analysis of various sources of VAT information and how organizations should interact with the relevant gover...

INDIRECT TAX

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Identify sources of information on VAT..........................................................................1

1.2 Explain how an organisation should interact with the relevant government agency.......1

1.3 Explain VAT registration requirements...........................................................................2

1.4 Identify the information that must be included on business documentation of VAT

registered businesses..............................................................................................................3

1.5 Explain the requirements and the frequency of reporting for VAT schemes...................4

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or

legislation...............................................................................................................................4

TASK 2............................................................................................................................................5

2.1 Extract relevant data for a specific period from the accounting system...........................5

2.2 Calculate relevant inputs and outputs using VAT classifications...................................5

2.3 Calculate the VAT due to, or from, the relevant tax authority.........................................5

2.4 Complete and submit a VAT return and any associated payment within the statutory time

limits.......................................................................................................................................6

TASK 3............................................................................................................................................6

3.1 Explain the implications and penalties for an organisation resulting from failure to abide

by VAT regulations................................................................................................................6

3.2 Make adjustments and declarations for any errors or omissions identified in previous VAT

periods....................................................................................................................................7

TASK 4............................................................................................................................................9

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts....................................................................................................9

4.2 Advise relevant people of changes in VAT legislation which would have an effect on an

organisation’s recording systems...........................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Identify sources of information on VAT..........................................................................1

1.2 Explain how an organisation should interact with the relevant government agency.......1

1.3 Explain VAT registration requirements...........................................................................2

1.4 Identify the information that must be included on business documentation of VAT

registered businesses..............................................................................................................3

1.5 Explain the requirements and the frequency of reporting for VAT schemes...................4

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or

legislation...............................................................................................................................4

TASK 2............................................................................................................................................5

2.1 Extract relevant data for a specific period from the accounting system...........................5

2.2 Calculate relevant inputs and outputs using VAT classifications...................................5

2.3 Calculate the VAT due to, or from, the relevant tax authority.........................................5

2.4 Complete and submit a VAT return and any associated payment within the statutory time

limits.......................................................................................................................................6

TASK 3............................................................................................................................................6

3.1 Explain the implications and penalties for an organisation resulting from failure to abide

by VAT regulations................................................................................................................6

3.2 Make adjustments and declarations for any errors or omissions identified in previous VAT

periods....................................................................................................................................7

TASK 4............................................................................................................................................9

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts....................................................................................................9

4.2 Advise relevant people of changes in VAT legislation which would have an effect on an

organisation’s recording systems...........................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Indirect tax is the tax which is gathered on the product and services which are purchased

by the people and customers. The people can later file the tax return which is forwarded to

government including the return. This tax is collected by the individuals in supply chain and then

paid to the government for increasing the economic revenue of the country. The people are

paying tax which ultimately leads to paying more for the purchased product. This report will

identify the sources of information on VAT along with the explanation of interacting of

organisations with the government agency along with the VAT registration requirements. This

report will further calculate the relevant inputs and outputs using these VAT classifications and

VAT due to, or from, the relevant tax authority. In the end, VAT penalties are analysed and

adjustments will be made for previous errors to communicate the VAT information to the

manager.

TASK 1

1.1 Identify sources of information on VAT

Taxation is an essential process which is collected by the government of a country to

increase their revenue for the country. This revenue is used for development of country in terms

of improving the infrastructure and to implement various governmental schemes and policies.

There are different sources of information on VAT which are available for the organisations to

understand the implementation of tax which is gathered by the government of a country. This tax

is controlled and regulated by the HM revenue and customs who is majorly governed by the

value added tax act, 1994 (Abbott and Bogenschneider, 2018). This act was introduced on 5th

July 1994 for collecting the tax on products and services offered by the firms. This act was

adopted by the UK government in order to collect the tax for the development of their country.

is the law which has been adopted by legislation of UK. This act was approved by the queen of

the UK by taking advices from their various cabinet ministers and politicians.

1.2 Explain how an organisation should interact with the relevant government agency

Any firm who is operating in a country needs to follow the laws and regulations

implemented by the government while operating their business operations. It is the major work

for the companies to follow these rules and laws for paying the tax and liabilities as well as to

calculate the tax of the current year. HMRC is an institution which is developed for helping the

1

Indirect tax is the tax which is gathered on the product and services which are purchased

by the people and customers. The people can later file the tax return which is forwarded to

government including the return. This tax is collected by the individuals in supply chain and then

paid to the government for increasing the economic revenue of the country. The people are

paying tax which ultimately leads to paying more for the purchased product. This report will

identify the sources of information on VAT along with the explanation of interacting of

organisations with the government agency along with the VAT registration requirements. This

report will further calculate the relevant inputs and outputs using these VAT classifications and

VAT due to, or from, the relevant tax authority. In the end, VAT penalties are analysed and

adjustments will be made for previous errors to communicate the VAT information to the

manager.

TASK 1

1.1 Identify sources of information on VAT

Taxation is an essential process which is collected by the government of a country to

increase their revenue for the country. This revenue is used for development of country in terms

of improving the infrastructure and to implement various governmental schemes and policies.

There are different sources of information on VAT which are available for the organisations to

understand the implementation of tax which is gathered by the government of a country. This tax

is controlled and regulated by the HM revenue and customs who is majorly governed by the

value added tax act, 1994 (Abbott and Bogenschneider, 2018). This act was introduced on 5th

July 1994 for collecting the tax on products and services offered by the firms. This act was

adopted by the UK government in order to collect the tax for the development of their country.

is the law which has been adopted by legislation of UK. This act was approved by the queen of

the UK by taking advices from their various cabinet ministers and politicians.

1.2 Explain how an organisation should interact with the relevant government agency

Any firm who is operating in a country needs to follow the laws and regulations

implemented by the government while operating their business operations. It is the major work

for the companies to follow these rules and laws for paying the tax and liabilities as well as to

calculate the tax of the current year. HMRC is an institution which is developed for helping the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

people in paying their taxes and to clarify the questions associated with the tax and its collection.

This institution has various departments whose responsibility is to interact with the government

agencies (Beneke, Lustig and Oliva, 2017). The institution has 25 departments which are helpful

for the companies to monitor and pay their debts and taxes. Also through the website of this

institution, firms when facing any issue in paying or calculating the tax can checks for the rules

and regulations which defines the rate of tax on a particular product or service. If such issues are

not resolved through the website, then firms can write a letter to the departments for their advice

on the issue of paying their tax. The institution has a different website for increasing the

knowledge of the tax payers regarding the rules and regulations. This website is updated on

regular basis or when necessary. The departments of the HMRC stays open from Monday to

Saturday between the timings 8 am to 8 pm whereas on Sunday, the departments stays open

from 9 to 5 in day time.

1.3 Explain VAT registration requirements

The process of VAT registration is not easy and compulsory until the firms reaches the

threshold amount which is provided by the government. The threshold limit for registering the

VAT is 85,00 Euros in terms of Turnover of the company. Companies are eligible for the VAT

registration when there turnover exceeds the threshold limit of Euros 85,000. This amount is the

minimum amount which is required by the firms to register for VAT. In order to register for

VAT, firms needs to apply to HMRC. This institution has developed a online portal in which

companies can register the VAT through online network. Also this institution has allowed agents

or accountants to register the VAT for providing the flexibility to companies in register. There

are several steps which must be followed by the firms in order to get a certificate which is issues

after the VAT registration (Boadway and Pestieau, 2011). There are also some problems when

applying through online portal of the institution. Such as when any firm apply for registration

through the online portal then the firm needs to do the registration process by using VAT1 form

and through the Post. Also similar problems can arise when a firm desires to apply for separate

VAT number for registering their business division or when the firm wants to apply for

Agriculture flat rate. Companies needs to file VAT1A when their business operations exists in

Europe and when the companies is in distance selling, then they needs to file VAT1B for selling

their products of more than 85,000 Euros. When the companies are disposing their assets for

2

This institution has various departments whose responsibility is to interact with the government

agencies (Beneke, Lustig and Oliva, 2017). The institution has 25 departments which are helpful

for the companies to monitor and pay their debts and taxes. Also through the website of this

institution, firms when facing any issue in paying or calculating the tax can checks for the rules

and regulations which defines the rate of tax on a particular product or service. If such issues are

not resolved through the website, then firms can write a letter to the departments for their advice

on the issue of paying their tax. The institution has a different website for increasing the

knowledge of the tax payers regarding the rules and regulations. This website is updated on

regular basis or when necessary. The departments of the HMRC stays open from Monday to

Saturday between the timings 8 am to 8 pm whereas on Sunday, the departments stays open

from 9 to 5 in day time.

1.3 Explain VAT registration requirements

The process of VAT registration is not easy and compulsory until the firms reaches the

threshold amount which is provided by the government. The threshold limit for registering the

VAT is 85,00 Euros in terms of Turnover of the company. Companies are eligible for the VAT

registration when there turnover exceeds the threshold limit of Euros 85,000. This amount is the

minimum amount which is required by the firms to register for VAT. In order to register for

VAT, firms needs to apply to HMRC. This institution has developed a online portal in which

companies can register the VAT through online network. Also this institution has allowed agents

or accountants to register the VAT for providing the flexibility to companies in register. There

are several steps which must be followed by the firms in order to get a certificate which is issues

after the VAT registration (Boadway and Pestieau, 2011). There are also some problems when

applying through online portal of the institution. Such as when any firm apply for registration

through the online portal then the firm needs to do the registration process by using VAT1 form

and through the Post. Also similar problems can arise when a firm desires to apply for separate

VAT number for registering their business division or when the firm wants to apply for

Agriculture flat rate. Companies needs to file VAT1A when their business operations exists in

Europe and when the companies is in distance selling, then they needs to file VAT1B for selling

their products of more than 85,000 Euros. When the companies are disposing their assets for

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

claiming the 8th or 13th directive refunds, then they can use the VAT1C form. When successfully

registered, company can submit their returns to the HMRC.

1.4 Identify the information that must be included on business documentation of VAT registered

businesses

When registering the VAT, companies needs to provide several documents and also they

needs to change their manner of trading. When a company is registered to VAT then they needs

to provide the payment invoice to each and very customers whom they sell their products.

Companies needs to follow the regulation 16 after successfully registering with the VAT in

which some elements must be followed for providing the invoice to consumers as discussed

below:

An unique identity number

Time and date of selling the products should be mentioned.

Name, address and registration number of seller must be mentioned.

On the top of invoice name, address and registration number of supplier must be entered.

The invoice must have several types of supply as given below:

▪ Sale

▪ Purchase

▪ Loan

▪ Way of exchange

▪ Customers product

▪ Sale on commission

identification number of products and services must be provided on Invoice.

For every item, rate of tax must be provided.

MRP and VAT amount in separate column

Cash discount should be separately mentioned

The firm also needs to maintain their accounts book which assist the firm in filing the

VAT return. When any misstatement is identified in return which is filed by the firm then the

firm needs to handle such books to the authorities. The company needs to maintain the record of

all the invoices.

3

registered, company can submit their returns to the HMRC.

1.4 Identify the information that must be included on business documentation of VAT registered

businesses

When registering the VAT, companies needs to provide several documents and also they

needs to change their manner of trading. When a company is registered to VAT then they needs

to provide the payment invoice to each and very customers whom they sell their products.

Companies needs to follow the regulation 16 after successfully registering with the VAT in

which some elements must be followed for providing the invoice to consumers as discussed

below:

An unique identity number

Time and date of selling the products should be mentioned.

Name, address and registration number of seller must be mentioned.

On the top of invoice name, address and registration number of supplier must be entered.

The invoice must have several types of supply as given below:

▪ Sale

▪ Purchase

▪ Loan

▪ Way of exchange

▪ Customers product

▪ Sale on commission

identification number of products and services must be provided on Invoice.

For every item, rate of tax must be provided.

MRP and VAT amount in separate column

Cash discount should be separately mentioned

The firm also needs to maintain their accounts book which assist the firm in filing the

VAT return. When any misstatement is identified in return which is filed by the firm then the

firm needs to handle such books to the authorities. The company needs to maintain the record of

all the invoices.

3

1.5 Explain the requirements and the frequency of reporting for VAT schemes

There are various types of reporting styles and schemes which must be followed by the

registered firms for performing their functions in an effective manner. Some of such schemes are

discussed below:

Annual Accounting Scheme: In this scheme, firms need to pay their return once in a year

but they needs to pay their monthly or quarterly payment for their VAT bills (Bucheli and et. al.,

2013). This scheme provides the flexibility to the concerned business through which the firms

can pay in instalments for a period of year. The firm needs to have a annual turnover of

1.35million Euros for registering under the Annual accounting scheme.

Cash Accounting scheme: In this scheme, firm needs to pay VAT based on the amount

received from their total sales. Under this scheme, business firms needs to pay the invoice to

their customers even when the VAT is not paid by the customers. This scheme is mostly adopted

by the small and medium business firms (Dowell, 2013). In this scheme, the return which is filed

by the firm is based on the amount collected from the sales not on the basis of invoice received

by the firm.

Flat rate scheme: In this scheme, the small firms can use the alternative for accounting

the VAT instead of using the normal method of accounting. In this, firms can calculate the

amount of VAT by using the flat rate which is decided by the government based on the total

turnover of the business (Flues and Thomas, 2015). Firms having more than turnover of 150,000

Euros can use this method for their accounting process. Flat rate turnover and flat rate percentage

must be used by the firms for selecting this method. firm can use the online return filling tools

for paying their VAT.

Standard method: In this method, the VAT is paid on the basis of issued invoices by the

firm. The paid VAT then recorded and reported to the HMRC. In such system, firm needs to pay

the return minimum 4 times per year which also includes payments on quarterly basis. Also the

due VAT is paid on quarterly basis.

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation

Maintaining the updated knowledge regarding the changes in legislation is very essential

for the firms in calculating the overall amount of VAT which must be paid to the government

that has to be paid to government. This is necessary because changes were made in the rate of tax

by the government on a yearly basis and companies needs to determine such changes and needs

4

There are various types of reporting styles and schemes which must be followed by the

registered firms for performing their functions in an effective manner. Some of such schemes are

discussed below:

Annual Accounting Scheme: In this scheme, firms need to pay their return once in a year

but they needs to pay their monthly or quarterly payment for their VAT bills (Bucheli and et. al.,

2013). This scheme provides the flexibility to the concerned business through which the firms

can pay in instalments for a period of year. The firm needs to have a annual turnover of

1.35million Euros for registering under the Annual accounting scheme.

Cash Accounting scheme: In this scheme, firm needs to pay VAT based on the amount

received from their total sales. Under this scheme, business firms needs to pay the invoice to

their customers even when the VAT is not paid by the customers. This scheme is mostly adopted

by the small and medium business firms (Dowell, 2013). In this scheme, the return which is filed

by the firm is based on the amount collected from the sales not on the basis of invoice received

by the firm.

Flat rate scheme: In this scheme, the small firms can use the alternative for accounting

the VAT instead of using the normal method of accounting. In this, firms can calculate the

amount of VAT by using the flat rate which is decided by the government based on the total

turnover of the business (Flues and Thomas, 2015). Firms having more than turnover of 150,000

Euros can use this method for their accounting process. Flat rate turnover and flat rate percentage

must be used by the firms for selecting this method. firm can use the online return filling tools

for paying their VAT.

Standard method: In this method, the VAT is paid on the basis of issued invoices by the

firm. The paid VAT then recorded and reported to the HMRC. In such system, firm needs to pay

the return minimum 4 times per year which also includes payments on quarterly basis. Also the

due VAT is paid on quarterly basis.

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation

Maintaining the updated knowledge regarding the changes in legislation is very essential

for the firms in calculating the overall amount of VAT which must be paid to the government

that has to be paid to government. This is necessary because changes were made in the rate of tax

by the government on a yearly basis and companies needs to determine such changes and needs

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to follow them properly in an effective manner (Herger, Kotsogiannis and McCorriston, 2016). If

such changes are not followed by the firms then it can leads to huge penalties on the firm by the

government. From the 1 January onwards, new laws and rules are implemented by the

government of UK for avoiding the disclosure regarding the disclosure and avoidance schemes

which covers the direct and indirect tax including the value added tax. Also new schemes are

implemented for applying online.

TASK 2

2.1 Extract relevant data for a specific period from the accounting system

Zoe wants to complete her VAT return for the quarter ending on 31 march 2018. Some of

the information regarding this is discussed below:

The total of sales invoice is £128000 which is issued for the standard rated sales.

The amount of Standard rated expenses is £24800.

On the date of 15 February 2013, Gwen buy machinery equipments of £24150 which are

inclusive of VAT.

2.2 Calculate relevant inputs and outputs using VAT classifications

Output VAT

Sales (128000*20%)

£ 25600

Input VAT

Expenses (24800*20%) (£4960)

Machinery (24150*20/120) (£4960)

VAT payable £16615

2.3 Calculate the VAT due to, or from, the relevant tax authority

When the money of tax which must be paid to the business entity is more than the

amount which must be paid, then it is called as the amount due to tax department. To calculate

such amount, input and output tax calculations are done.

Standard supplies- Amount of VAT is calculated on applicable rate of 20%. Zoe has

pending amount of £16615 which must be paid to the VAT department which is authorised by

HMRC.

5

such changes are not followed by the firms then it can leads to huge penalties on the firm by the

government. From the 1 January onwards, new laws and rules are implemented by the

government of UK for avoiding the disclosure regarding the disclosure and avoidance schemes

which covers the direct and indirect tax including the value added tax. Also new schemes are

implemented for applying online.

TASK 2

2.1 Extract relevant data for a specific period from the accounting system

Zoe wants to complete her VAT return for the quarter ending on 31 march 2018. Some of

the information regarding this is discussed below:

The total of sales invoice is £128000 which is issued for the standard rated sales.

The amount of Standard rated expenses is £24800.

On the date of 15 February 2013, Gwen buy machinery equipments of £24150 which are

inclusive of VAT.

2.2 Calculate relevant inputs and outputs using VAT classifications

Output VAT

Sales (128000*20%)

£ 25600

Input VAT

Expenses (24800*20%) (£4960)

Machinery (24150*20/120) (£4960)

VAT payable £16615

2.3 Calculate the VAT due to, or from, the relevant tax authority

When the money of tax which must be paid to the business entity is more than the

amount which must be paid, then it is called as the amount due to tax department. To calculate

such amount, input and output tax calculations are done.

Standard supplies- Amount of VAT is calculated on applicable rate of 20%. Zoe has

pending amount of £16615 which must be paid to the VAT department which is authorised by

HMRC.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Zero-rated supplies: Zero-rated supplies are the products on which the tax charged is

zero. This amount is helpful in taking credit for the business as the input tax (Reynolds and

Smolensky, 2013). Input tax that must be receivable by the Zoe is of £2500.

Exempted supplies: For supplying the products and services which are not yet registered

are exempted as registration is not required. So, output VAT is not payable along with the non-

receivable input tax.

2.4 Complete and submit a VAT return and any associated payment within the statutory time

limits

A VAT return is the return which sum the sales and purchase of firm. This return consist

of total sales and output tax which has to be paid by the company. This return can be filed from

the online portal provided by the HMRC. Company needs to fill the suitable boxes in which their

entries fall.

TASK 3

3.1 Explain the implications and penalties for an organisation resulting from failure to abide by

VAT regulations

The organisations gets a default in the favour of company when they are failed in paying

their VAT liability. There are several conditions which must be followed by the firms when

filing the return or tax online (Nye, 2018). When the conditions are met by the firm then it leads

to default. These conditions involves the not filling of return in the given deadline or because of

the due return which hasn't been paid on time. When such conditions are met and the debt of the

6

zero. This amount is helpful in taking credit for the business as the input tax (Reynolds and

Smolensky, 2013). Input tax that must be receivable by the Zoe is of £2500.

Exempted supplies: For supplying the products and services which are not yet registered

are exempted as registration is not required. So, output VAT is not payable along with the non-

receivable input tax.

2.4 Complete and submit a VAT return and any associated payment within the statutory time

limits

A VAT return is the return which sum the sales and purchase of firm. This return consist

of total sales and output tax which has to be paid by the company. This return can be filed from

the online portal provided by the HMRC. Company needs to fill the suitable boxes in which their

entries fall.

TASK 3

3.1 Explain the implications and penalties for an organisation resulting from failure to abide by

VAT regulations

The organisations gets a default in the favour of company when they are failed in paying

their VAT liability. There are several conditions which must be followed by the firms when

filing the return or tax online (Nye, 2018). When the conditions are met by the firm then it leads

to default. These conditions involves the not filling of return in the given deadline or because of

the due return which hasn't been paid on time. When such conditions are met and the debt of the

6

firm is not paid, Then it automatically goes into surcharge period of 12 months. When the

company pay its VAT as late return then the surcharge period is not applicable. The amount of

surcharge is the VAT percentage which is still due for the default accounting period. This rate

increase each time when the default is made (Higgins and Pereira, 2014). While in 2nd default,

the amount is increased by 2% or as prescribed by the government. The HMRC charge the

penalties when the return is overstated or contains a careless or deliberate inaccuracy which can

extend up to 100% of tax. The HMRC sends a notice related with the paid amount and if firm

does not reply within 30 days then 30% of assessment will be taken by the HMRC. When the

firm is ready to submit a paper VAT return than 400 Euros penalty will be paid by the company.

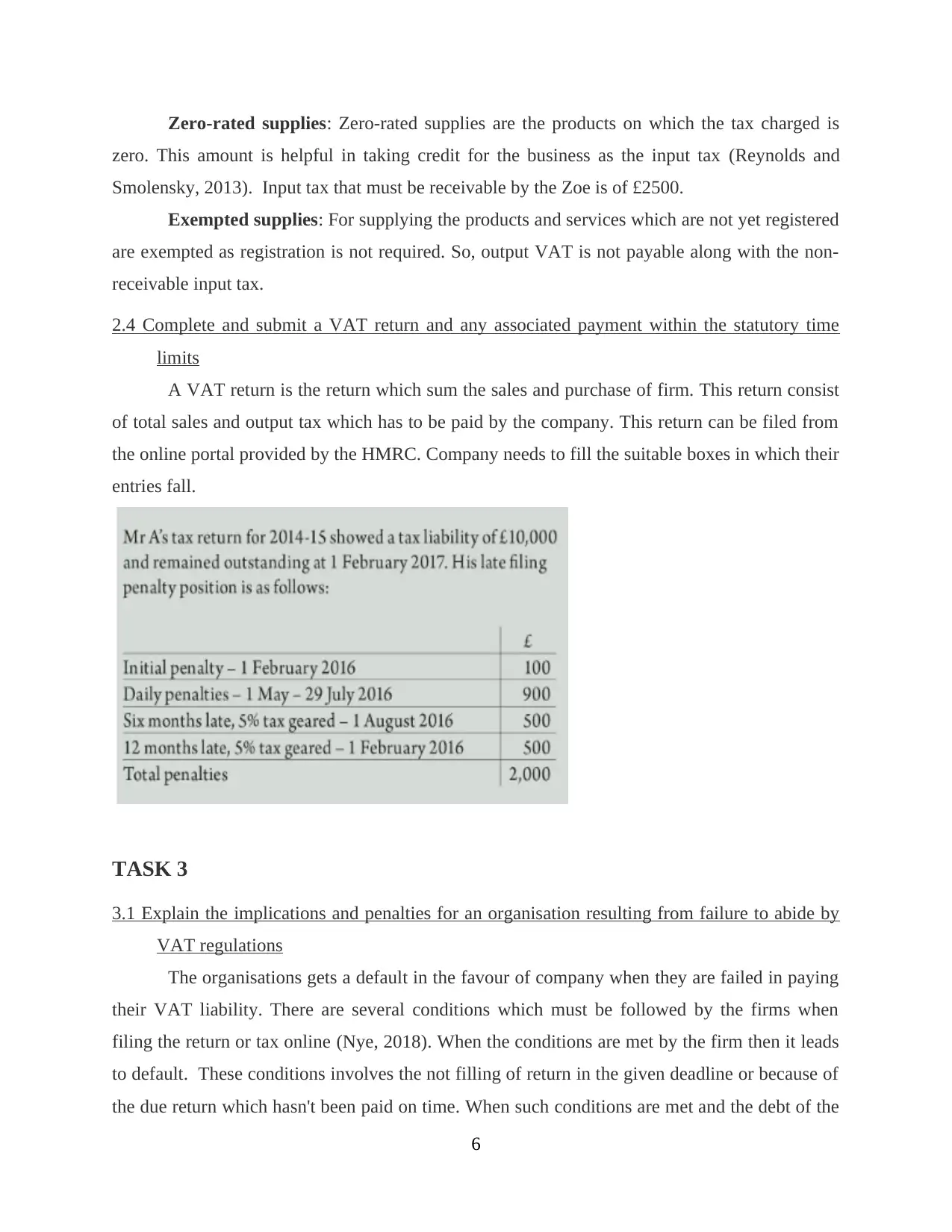

3.2 Make adjustments and declarations for any errors or omissions identified in previous VAT

periods

Company needs to file VAT 652 online to the HMRC department in order to make

adjustments in the errors of the firm (Mason and Stephenson Jr, 2017). This form is filled when

the firm has made some mistake in filling the return or when less return is paid. In the end, firm

needs to made a declaration in which all data is provided which suit best according to the

knowledge of the firm.

7

company pay its VAT as late return then the surcharge period is not applicable. The amount of

surcharge is the VAT percentage which is still due for the default accounting period. This rate

increase each time when the default is made (Higgins and Pereira, 2014). While in 2nd default,

the amount is increased by 2% or as prescribed by the government. The HMRC charge the

penalties when the return is overstated or contains a careless or deliberate inaccuracy which can

extend up to 100% of tax. The HMRC sends a notice related with the paid amount and if firm

does not reply within 30 days then 30% of assessment will be taken by the HMRC. When the

firm is ready to submit a paper VAT return than 400 Euros penalty will be paid by the company.

3.2 Make adjustments and declarations for any errors or omissions identified in previous VAT

periods

Company needs to file VAT 652 online to the HMRC department in order to make

adjustments in the errors of the firm (Mason and Stephenson Jr, 2017). This form is filled when

the firm has made some mistake in filling the return or when less return is paid. In the end, firm

needs to made a declaration in which all data is provided which suit best according to the

knowledge of the firm.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

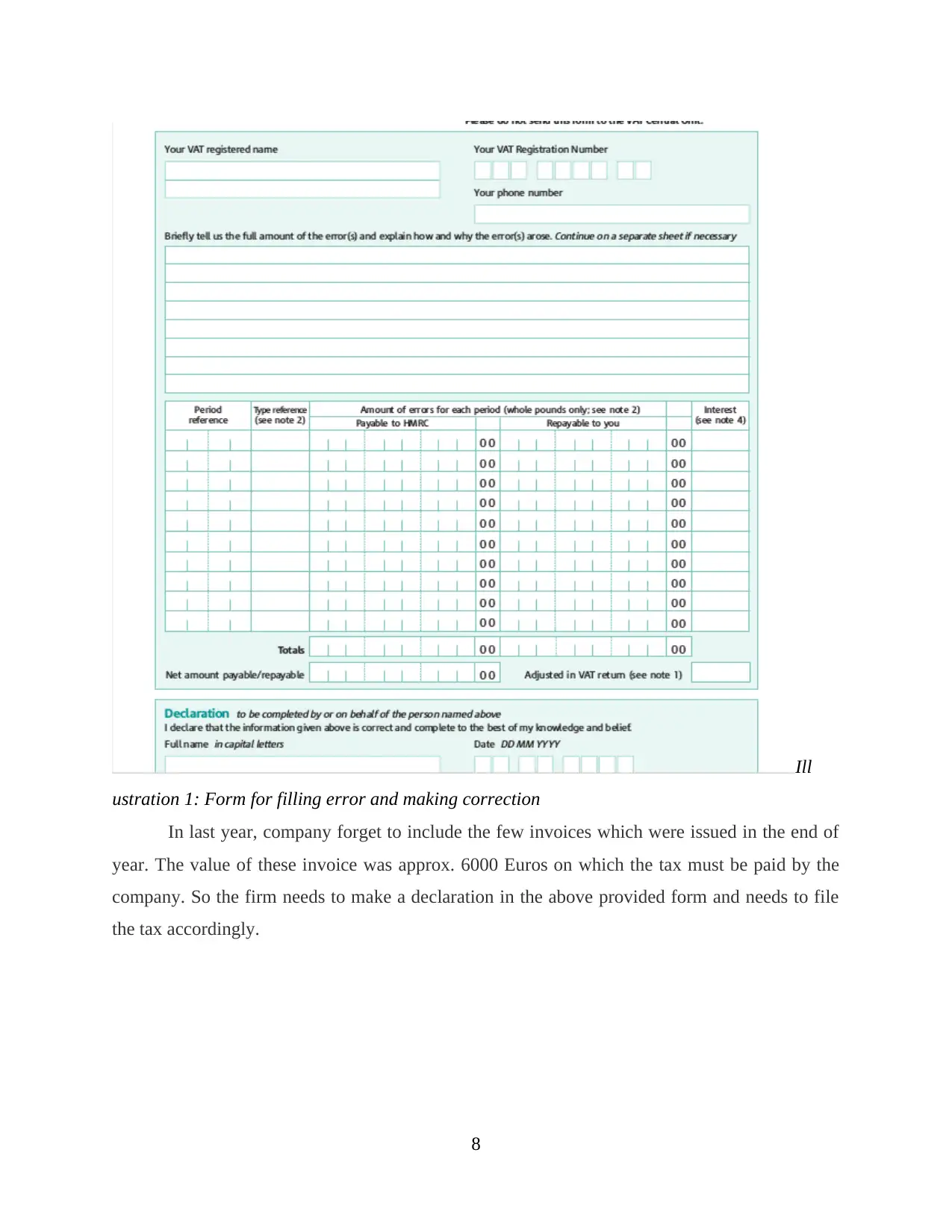

Ill

ustration 1: Form for filling error and making correction

In last year, company forget to include the few invoices which were issued in the end of

year. The value of these invoice was approx. 6000 Euros on which the tax must be paid by the

company. So the firm needs to make a declaration in the above provided form and needs to file

the tax accordingly.

8

ustration 1: Form for filling error and making correction

In last year, company forget to include the few invoices which were issued in the end of

year. The value of these invoice was approx. 6000 Euros on which the tax must be paid by the

company. So the firm needs to make a declaration in the above provided form and needs to file

the tax accordingly.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts

VAT is the main source of revenue for the government which is helpful in raising the

money indirectly. When a firm gets register under the VAT act then the firm needs to pay the

VAT money which is gathered from the customers by the firm. It can positively impact the

financial performance of the firm as the cost for producing the goods will b reduced and the cost

of raw materials also get lowered for compensating the value of added percentage (Kaplanoglou,

2015). The money was gathered from the suppliers and sellers which must be paid in the end of

month or year. This money is helpful in maintaining the cash flow without any charging any

interest. The VAT is also helpful in development of the economy as well as of the company for

improving the infrastructure and market.

4.2 Advise relevant people of changes in VAT legislation which would have an effect on an

organisation’s recording systems

VAT is known as the major issues for the small and medium size firms in UK. The firms

needs to follow the regulations and guidelines when registered under the VAT act regardless of

their size, sales and profit. The VAT act changes every year so the M&S needs to build their own

team for determining such changes in the VAT act. Through this, the team can calculate and

submit the VAT return on timely manner (Llerena and et. al., 2015). The management needs to

determine the various VAT rate on different product sold by the firm. It is very essential for the

firm to determine the impact of change in the VAT act in regular intervals. Therefore, the

workers of the firms needs to check for such changes and comply with them for reducing the

impact on recording styles of themselves.

CONCLUSION

It can be concluded from the above report that the VAT is the necessary elements which

must be paid by the firms to the government. This VAT is collected by the government which is

used for development of the country. The firms needs to take care of documents and turnover

while registering under the VAT act. The firm also needs to provide the invoice to their

customers which will ultimately be used for filing the return. There are various types of reporting

styles and schemes such as Annual Accounting Scheme, Cash Accounting scheme and Flat rate

9

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts

VAT is the main source of revenue for the government which is helpful in raising the

money indirectly. When a firm gets register under the VAT act then the firm needs to pay the

VAT money which is gathered from the customers by the firm. It can positively impact the

financial performance of the firm as the cost for producing the goods will b reduced and the cost

of raw materials also get lowered for compensating the value of added percentage (Kaplanoglou,

2015). The money was gathered from the suppliers and sellers which must be paid in the end of

month or year. This money is helpful in maintaining the cash flow without any charging any

interest. The VAT is also helpful in development of the economy as well as of the company for

improving the infrastructure and market.

4.2 Advise relevant people of changes in VAT legislation which would have an effect on an

organisation’s recording systems

VAT is known as the major issues for the small and medium size firms in UK. The firms

needs to follow the regulations and guidelines when registered under the VAT act regardless of

their size, sales and profit. The VAT act changes every year so the M&S needs to build their own

team for determining such changes in the VAT act. Through this, the team can calculate and

submit the VAT return on timely manner (Llerena and et. al., 2015). The management needs to

determine the various VAT rate on different product sold by the firm. It is very essential for the

firm to determine the impact of change in the VAT act in regular intervals. Therefore, the

workers of the firms needs to check for such changes and comply with them for reducing the

impact on recording styles of themselves.

CONCLUSION

It can be concluded from the above report that the VAT is the necessary elements which

must be paid by the firms to the government. This VAT is collected by the government which is

used for development of the country. The firms needs to take care of documents and turnover

while registering under the VAT act. The firm also needs to provide the invoice to their

customers which will ultimately be used for filing the return. There are various types of reporting

styles and schemes such as Annual Accounting Scheme, Cash Accounting scheme and Flat rate

9

scheme which must be followed by the registered firms for performing their functions in an

effective manner. The firms also needs to take care of the implications and penalties which can

be imposed on them when the rules and regulations are not followed accordingly.

10

effective manner. The firms also needs to take care of the implications and penalties which can

be imposed on them when the rules and regulations are not followed accordingly.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Abbott, R. and Bogenschneider, B., 2018. Should Robots Pay Taxes: Tax Policy in the Age of

Automation. Harv. L. & Pol'y Rev.. 12 . p.145.

Beneke, M., Lustig, N. and Oliva, J.A., 2017. The Impact of Taxes and Social Spending on

Inequality and Poverty in El Salvador.

Boadway, R. and Pestieau, P., 2011. Indirect taxes for redistribution: Should necessity goods be

favored?.

Bucheli and et. al., 2013. Social spending, taxes and income redistribution in Uruguay. The

World Bank.

Dowell, S., 2013. History of Taxation and Taxes in England Volumes 1-4. Routledge.

Flues, F. and Thomas, A., 2015. The distributional effects of energy taxes.

Herger, N., Kotsogiannis, C. and McCorriston, S., 2016. Multiple taxes and alternative forms of

FDI: evidence from cross-border acquisitions. International Tax and Public Finance.

23(1). pp.82-113.

Higgins, S. and Pereira, C., 2014. The effects of Brazil’s taxation and social spending on the

distribution of household income. Public Finance Review. 42(3). pp.346-367.

Kaplanoglou, G., 2015. Who pays indirect taxes in Greece? From EU entry to the fiscal crisis.

Public Finance Review. 43(4). pp.529-556.

Llerena and et. al., 2015. Social Spending, Taxes and Income Redistribution in Ecuador (No.

28). Tulane University, Department of Economics.

Mason, A.T. and Stephenson Jr, D.G., 2017. American constitutional law: introductory essays

and selected cases. Routledge.

Nye, J.V., 2018. War, Wine, and Taxes: The Political Economy of Anglo-French Trade, 1689-

1900 (Vol. 20). Princeton University Press.

Reynolds, M. and Smolensky, E., 2013. Public expenditures, taxes, and the distribution of

income: The United States, 1950, 1961, 1970. Academic Press.

Online

Errors in VAT records. 2015. [Online]. Available

through:<https://www.gov.uk/government/publications/vat-notice-70045-how-to-

correct-vat-errors-and-make-adjustments-or-claims/vat-notice-70045-how-to-correct-

vat-errors-and-make-adjustments-or-claims>

11

Books and Journals

Abbott, R. and Bogenschneider, B., 2018. Should Robots Pay Taxes: Tax Policy in the Age of

Automation. Harv. L. & Pol'y Rev.. 12 . p.145.

Beneke, M., Lustig, N. and Oliva, J.A., 2017. The Impact of Taxes and Social Spending on

Inequality and Poverty in El Salvador.

Boadway, R. and Pestieau, P., 2011. Indirect taxes for redistribution: Should necessity goods be

favored?.

Bucheli and et. al., 2013. Social spending, taxes and income redistribution in Uruguay. The

World Bank.

Dowell, S., 2013. History of Taxation and Taxes in England Volumes 1-4. Routledge.

Flues, F. and Thomas, A., 2015. The distributional effects of energy taxes.

Herger, N., Kotsogiannis, C. and McCorriston, S., 2016. Multiple taxes and alternative forms of

FDI: evidence from cross-border acquisitions. International Tax and Public Finance.

23(1). pp.82-113.

Higgins, S. and Pereira, C., 2014. The effects of Brazil’s taxation and social spending on the

distribution of household income. Public Finance Review. 42(3). pp.346-367.

Kaplanoglou, G., 2015. Who pays indirect taxes in Greece? From EU entry to the fiscal crisis.

Public Finance Review. 43(4). pp.529-556.

Llerena and et. al., 2015. Social Spending, Taxes and Income Redistribution in Ecuador (No.

28). Tulane University, Department of Economics.

Mason, A.T. and Stephenson Jr, D.G., 2017. American constitutional law: introductory essays

and selected cases. Routledge.

Nye, J.V., 2018. War, Wine, and Taxes: The Political Economy of Anglo-French Trade, 1689-

1900 (Vol. 20). Princeton University Press.

Reynolds, M. and Smolensky, E., 2013. Public expenditures, taxes, and the distribution of

income: The United States, 1950, 1961, 1970. Academic Press.

Online

Errors in VAT records. 2015. [Online]. Available

through:<https://www.gov.uk/government/publications/vat-notice-70045-how-to-

correct-vat-errors-and-make-adjustments-or-claims/vat-notice-70045-how-to-correct-

vat-errors-and-make-adjustments-or-claims>

11

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.