Detailed Report on Income Tax Return and Financial Analysis FY 2018/19

VerifiedAdded on 2021/02/19

|14

|3894

|39

Report

AI Summary

This report analyzes an individual's income tax return for the 2018/19 financial year, calculating a total tax payable liability of $33,503 based on an assessable income of $203,928 and allowed deductions of $33,135, resulting in a taxable income of $170,793. The analysis includes detailed breakdowns of income sources such as director's salary, fringe benefits, and dividend income, along with capital gains from the disposal of BHP and MYR shares. Deductions for rental property, car expenses, and other items are also examined. The report addresses various tax implications, including Medicare levy, budget repair levy, and the treatment of franked dividends. It further explores capital gains tax, rental property deductions (including depreciation), and other deductible expenses, such as car expenses and membership fees. The report also covers the preservation of supporting documents and provides recommendations for maintaining accurate records. The analysis concludes with a summary of the individual's financial position and tax obligations.

MAJOR ASSESSMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

LETTER...........................................................................................................................................1

INCOME......................................................................................................................................2

OTHER INCOME.......................................................................................................................3

CAPITAL GAINS.......................................................................................................................4

RENTAL PROPERTY ...............................................................................................................6

DEDUCTIONS............................................................................................................................7

OTHER ISSUES..........................................................................................................................7

TAX PAYABLE, OFFSETS AND LEVIES...............................................................................8

REFERENCES..............................................................................................................................10

LETTER...........................................................................................................................................1

INCOME......................................................................................................................................2

OTHER INCOME.......................................................................................................................3

CAPITAL GAINS.......................................................................................................................4

RENTAL PROPERTY ...............................................................................................................6

DEDUCTIONS............................................................................................................................7

OTHER ISSUES..........................................................................................................................7

TAX PAYABLE, OFFSETS AND LEVIES...............................................................................8

REFERENCES..............................................................................................................................10

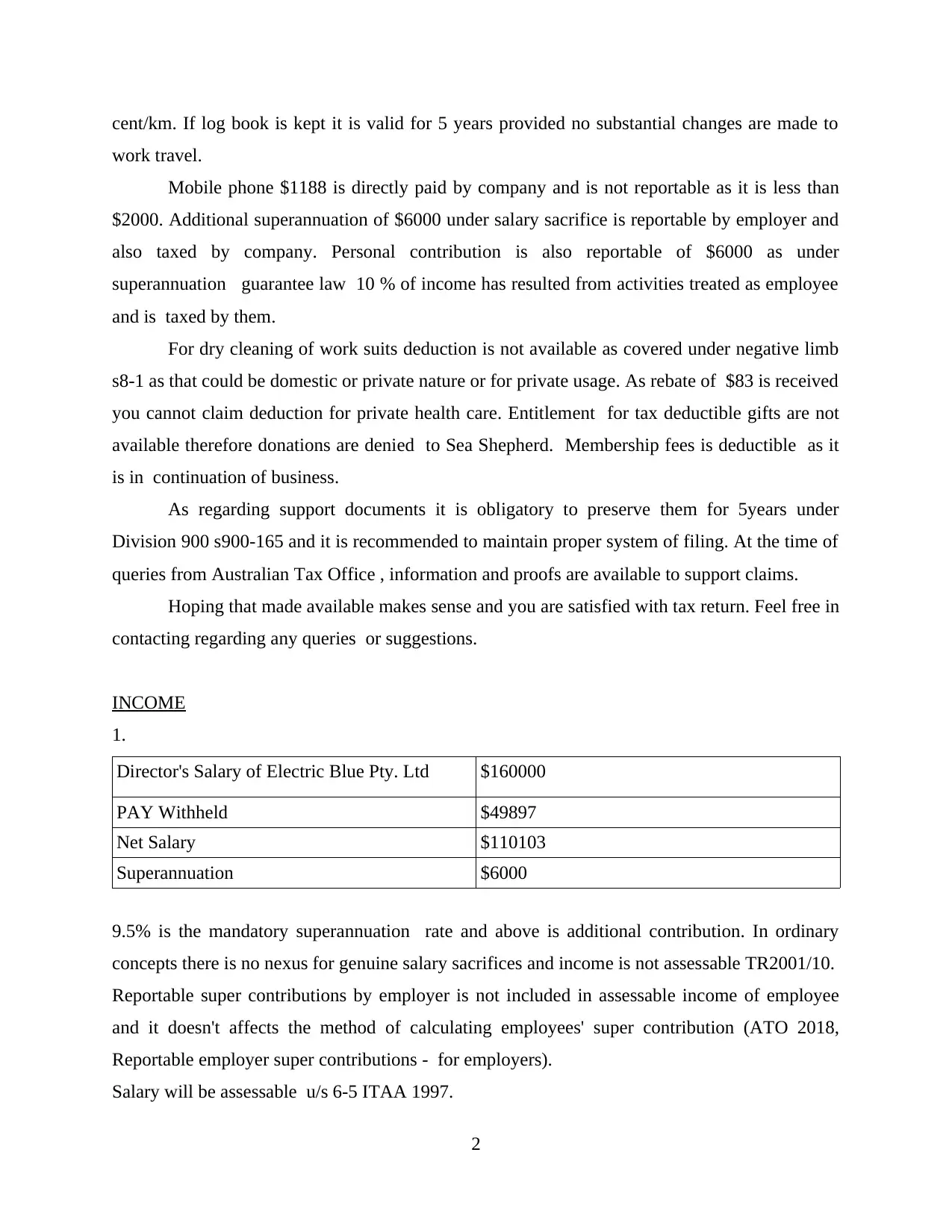

LETTER

22nd January 2018

This letter is written regarding income tax return for financial year 2018/19.

Tax payable liability net this year amounts to $ 33503 . It is assumed all information provided by

you are correct. It is calculated on total assessable income $203928 less allowed deductions of $

33135. This is giving taxable income amounting to $170793 and placing you in tax bracket of

37cents /$. Income tax payable is $50690. 2% flat rate is applicable on taxable income as

Medicare levy. Private health care was not taken for full financial year therefore liability of

paying medical surcharge for days for which you did not had health care and it amounts to 1.5%

for 274 days. 2% Budget repair levy is charged over taxable income due to large debt owing of

Australia on income over $180000.

Dividends received during year from from Electric Blue amounts to $84000 which are

fully franked. Inheritance of dividend from father of $2465 are fully franked. Amounts are

grossed by tax paid and included to assessable income and after tax calculations are allowed as

offset.

BHP is pre CGT asset and was acquired at market value at death date on July 15, 2016.

Shares were valued at $20.30 per share on this date and were sold for $ 64075on 5th Jan at

$25.63. Profit of $13210 on disposal of BHP.

MYR is post CGT asset that was acquired at cost price and shares were purchased by

father at $4.10. Shares are sold at $1.35 for 13500 on 5th January which resulted in loss $23430. I

was not able to determine the reason behind selling these shares at such loss on disposal of BHP

shares. Loss resulted from disposing MYR will offset gain of BHP & the net loss of $10220 will

be carried forward to offset future gains of next year.

Capital work deduction of $4500 is allowable for rental property. There are some

deductible expenses for producing assessable income. Interest on loan is deductible as loan is for

rental property and producing income. Since the rent rates are within normal rates prevailing and

at arm's length transaction it is not differently treated for in come tax.

For the car Audi Q5 deduction is claimed under cents/km method. The deduction of

$3400 is available. Depreciation is not claimable by for car expenses that are calculated on

1

22nd January 2018

This letter is written regarding income tax return for financial year 2018/19.

Tax payable liability net this year amounts to $ 33503 . It is assumed all information provided by

you are correct. It is calculated on total assessable income $203928 less allowed deductions of $

33135. This is giving taxable income amounting to $170793 and placing you in tax bracket of

37cents /$. Income tax payable is $50690. 2% flat rate is applicable on taxable income as

Medicare levy. Private health care was not taken for full financial year therefore liability of

paying medical surcharge for days for which you did not had health care and it amounts to 1.5%

for 274 days. 2% Budget repair levy is charged over taxable income due to large debt owing of

Australia on income over $180000.

Dividends received during year from from Electric Blue amounts to $84000 which are

fully franked. Inheritance of dividend from father of $2465 are fully franked. Amounts are

grossed by tax paid and included to assessable income and after tax calculations are allowed as

offset.

BHP is pre CGT asset and was acquired at market value at death date on July 15, 2016.

Shares were valued at $20.30 per share on this date and were sold for $ 64075on 5th Jan at

$25.63. Profit of $13210 on disposal of BHP.

MYR is post CGT asset that was acquired at cost price and shares were purchased by

father at $4.10. Shares are sold at $1.35 for 13500 on 5th January which resulted in loss $23430. I

was not able to determine the reason behind selling these shares at such loss on disposal of BHP

shares. Loss resulted from disposing MYR will offset gain of BHP & the net loss of $10220 will

be carried forward to offset future gains of next year.

Capital work deduction of $4500 is allowable for rental property. There are some

deductible expenses for producing assessable income. Interest on loan is deductible as loan is for

rental property and producing income. Since the rent rates are within normal rates prevailing and

at arm's length transaction it is not differently treated for in come tax.

For the car Audi Q5 deduction is claimed under cents/km method. The deduction of

$3400 is available. Depreciation is not claimable by for car expenses that are calculated on

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cent/km. If log book is kept it is valid for 5 years provided no substantial changes are made to

work travel.

Mobile phone $1188 is directly paid by company and is not reportable as it is less than

$2000. Additional superannuation of $6000 under salary sacrifice is reportable by employer and

also taxed by company. Personal contribution is also reportable of $6000 as under

superannuation guarantee law 10 % of income has resulted from activities treated as employee

and is taxed by them.

For dry cleaning of work suits deduction is not available as covered under negative limb

s8-1 as that could be domestic or private nature or for private usage. As rebate of $83 is received

you cannot claim deduction for private health care. Entitlement for tax deductible gifts are not

available therefore donations are denied to Sea Shepherd. Membership fees is deductible as it

is in continuation of business.

As regarding support documents it is obligatory to preserve them for 5years under

Division 900 s900-165 and it is recommended to maintain proper system of filing. At the time of

queries from Australian Tax Office , information and proofs are available to support claims.

Hoping that made available makes sense and you are satisfied with tax return. Feel free in

contacting regarding any queries or suggestions.

INCOME

1.

Director's Salary of Electric Blue Pty. Ltd $160000

PAY Withheld $49897

Net Salary $110103

Superannuation $6000

9.5% is the mandatory superannuation rate and above is additional contribution. In ordinary

concepts there is no nexus for genuine salary sacrifices and income is not assessable TR2001/10.

Reportable super contributions by employer is not included in assessable income of employee

and it doesn't affects the method of calculating employees' super contribution (ATO 2018,

Reportable employer super contributions - for employers).

Salary will be assessable u/s 6-5 ITAA 1997.

2

work travel.

Mobile phone $1188 is directly paid by company and is not reportable as it is less than

$2000. Additional superannuation of $6000 under salary sacrifice is reportable by employer and

also taxed by company. Personal contribution is also reportable of $6000 as under

superannuation guarantee law 10 % of income has resulted from activities treated as employee

and is taxed by them.

For dry cleaning of work suits deduction is not available as covered under negative limb

s8-1 as that could be domestic or private nature or for private usage. As rebate of $83 is received

you cannot claim deduction for private health care. Entitlement for tax deductible gifts are not

available therefore donations are denied to Sea Shepherd. Membership fees is deductible as it

is in continuation of business.

As regarding support documents it is obligatory to preserve them for 5years under

Division 900 s900-165 and it is recommended to maintain proper system of filing. At the time of

queries from Australian Tax Office , information and proofs are available to support claims.

Hoping that made available makes sense and you are satisfied with tax return. Feel free in

contacting regarding any queries or suggestions.

INCOME

1.

Director's Salary of Electric Blue Pty. Ltd $160000

PAY Withheld $49897

Net Salary $110103

Superannuation $6000

9.5% is the mandatory superannuation rate and above is additional contribution. In ordinary

concepts there is no nexus for genuine salary sacrifices and income is not assessable TR2001/10.

Reportable super contributions by employer is not included in assessable income of employee

and it doesn't affects the method of calculating employees' super contribution (ATO 2018,

Reportable employer super contributions - for employers).

Salary will be assessable u/s 6-5 ITAA 1997.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

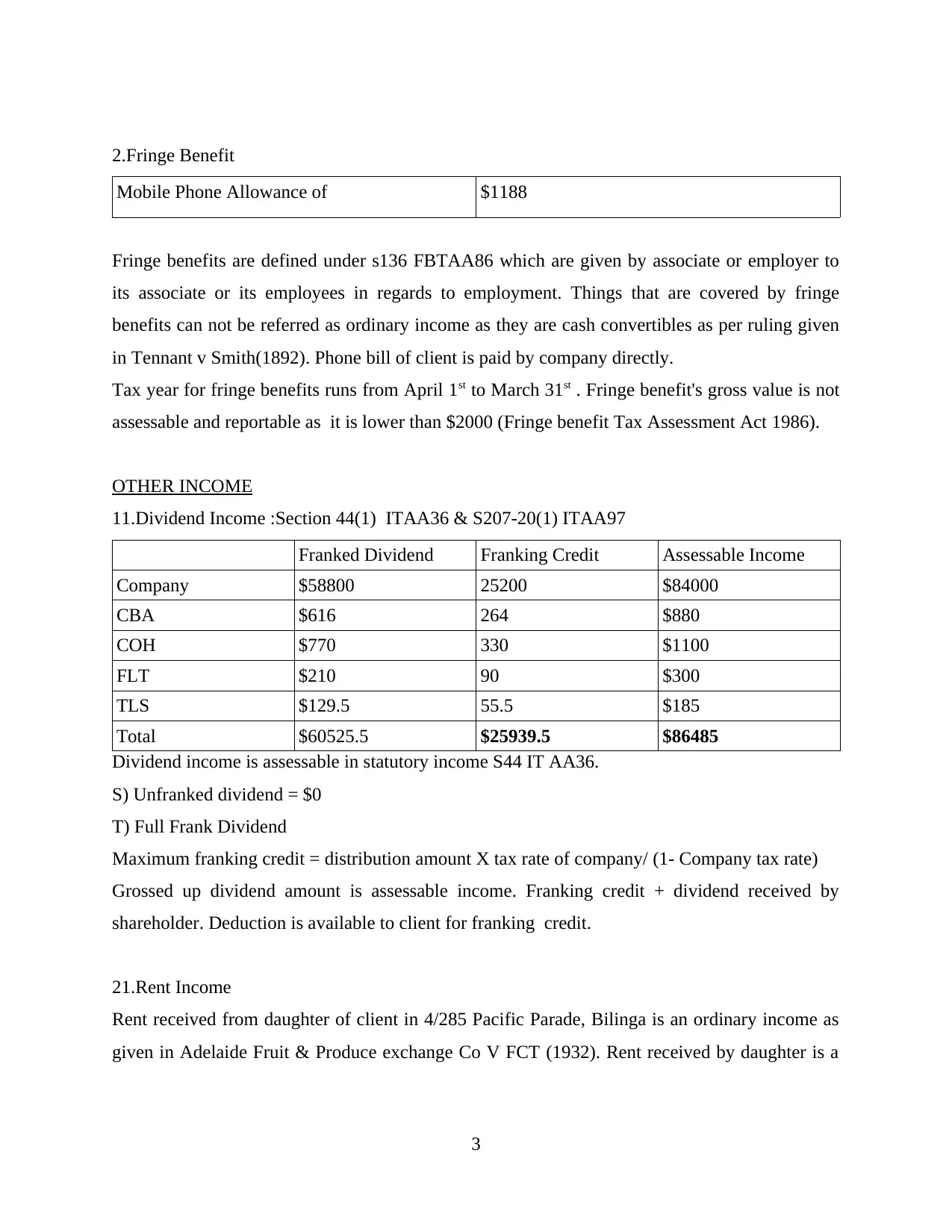

2.Fringe Benefit

Mobile Phone Allowance of $1188

Fringe benefits are defined under s136 FBTAA86 which are given by associate or employer to

its associate or its employees in regards to employment. Things that are covered by fringe

benefits can not be referred as ordinary income as they are cash convertibles as per ruling given

in Tennant v Smith(1892). Phone bill of client is paid by company directly.

Tax year for fringe benefits runs from April 1st to March 31st . Fringe benefit's gross value is not

assessable and reportable as it is lower than $2000 (Fringe benefit Tax Assessment Act 1986).

OTHER INCOME

11.Dividend Income :Section 44(1) ITAA36 & S207-20(1) ITAA97

Franked Dividend Franking Credit Assessable Income

Company $58800 25200 $84000

CBA $616 264 $880

COH $770 330 $1100

FLT $210 90 $300

TLS $129.5 55.5 $185

Total $60525.5 $25939.5 $86485

Dividend income is assessable in statutory income S44 IT AA36.

S) Unfranked dividend = $0

T) Full Frank Dividend

Maximum franking credit = distribution amount X tax rate of company/ (1- Company tax rate)

Grossed up dividend amount is assessable income. Franking credit + dividend received by

shareholder. Deduction is available to client for franking credit.

21.Rent Income

Rent received from daughter of client in 4/285 Pacific Parade, Bilinga is an ordinary income as

given in Adelaide Fruit & Produce exchange Co V FCT (1932). Rent received by daughter is a

3

Mobile Phone Allowance of $1188

Fringe benefits are defined under s136 FBTAA86 which are given by associate or employer to

its associate or its employees in regards to employment. Things that are covered by fringe

benefits can not be referred as ordinary income as they are cash convertibles as per ruling given

in Tennant v Smith(1892). Phone bill of client is paid by company directly.

Tax year for fringe benefits runs from April 1st to March 31st . Fringe benefit's gross value is not

assessable and reportable as it is lower than $2000 (Fringe benefit Tax Assessment Act 1986).

OTHER INCOME

11.Dividend Income :Section 44(1) ITAA36 & S207-20(1) ITAA97

Franked Dividend Franking Credit Assessable Income

Company $58800 25200 $84000

CBA $616 264 $880

COH $770 330 $1100

FLT $210 90 $300

TLS $129.5 55.5 $185

Total $60525.5 $25939.5 $86485

Dividend income is assessable in statutory income S44 IT AA36.

S) Unfranked dividend = $0

T) Full Frank Dividend

Maximum franking credit = distribution amount X tax rate of company/ (1- Company tax rate)

Grossed up dividend amount is assessable income. Franking credit + dividend received by

shareholder. Deduction is available to client for franking credit.

21.Rent Income

Rent received from daughter of client in 4/285 Pacific Parade, Bilinga is an ordinary income as

given in Adelaide Fruit & Produce exchange Co V FCT (1932). Rent received by daughter is a

3

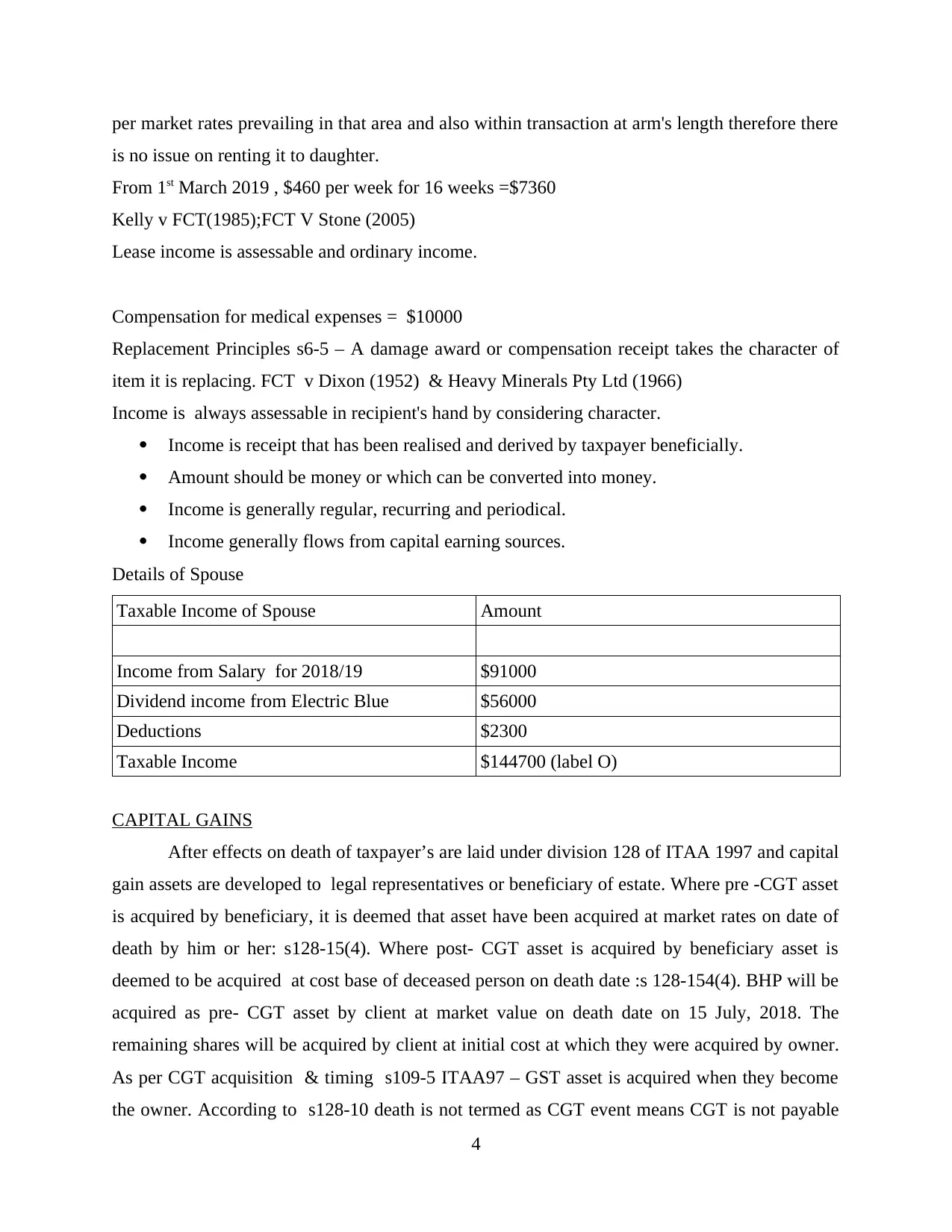

per market rates prevailing in that area and also within transaction at arm's length therefore there

is no issue on renting it to daughter.

From 1st March 2019 , $460 per week for 16 weeks =$7360

Kelly v FCT(1985);FCT V Stone (2005)

Lease income is assessable and ordinary income.

Compensation for medical expenses = $10000

Replacement Principles s6-5 – A damage award or compensation receipt takes the character of

item it is replacing. FCT v Dixon (1952) & Heavy Minerals Pty Ltd (1966)

Income is always assessable in recipient's hand by considering character.

Income is receipt that has been realised and derived by taxpayer beneficially.

Amount should be money or which can be converted into money.

Income is generally regular, recurring and periodical.

Income generally flows from capital earning sources.

Details of Spouse

Taxable Income of Spouse Amount

Income from Salary for 2018/19 $91000

Dividend income from Electric Blue $56000

Deductions $2300

Taxable Income $144700 (label O)

CAPITAL GAINS

After effects on death of taxpayer’s are laid under division 128 of ITAA 1997 and capital

gain assets are developed to legal representatives or beneficiary of estate. Where pre -CGT asset

is acquired by beneficiary, it is deemed that asset have been acquired at market rates on date of

death by him or her: s128-15(4). Where post- CGT asset is acquired by beneficiary asset is

deemed to be acquired at cost base of deceased person on death date :s 128-154(4). BHP will be

acquired as pre- CGT asset by client at market value on death date on 15 July, 2018. The

remaining shares will be acquired by client at initial cost at which they were acquired by owner.

As per CGT acquisition & timing s109-5 ITAA97 – GST asset is acquired when they become

the owner. According to s128-10 death is not termed as CGT event means CGT is not payable

4

is no issue on renting it to daughter.

From 1st March 2019 , $460 per week for 16 weeks =$7360

Kelly v FCT(1985);FCT V Stone (2005)

Lease income is assessable and ordinary income.

Compensation for medical expenses = $10000

Replacement Principles s6-5 – A damage award or compensation receipt takes the character of

item it is replacing. FCT v Dixon (1952) & Heavy Minerals Pty Ltd (1966)

Income is always assessable in recipient's hand by considering character.

Income is receipt that has been realised and derived by taxpayer beneficially.

Amount should be money or which can be converted into money.

Income is generally regular, recurring and periodical.

Income generally flows from capital earning sources.

Details of Spouse

Taxable Income of Spouse Amount

Income from Salary for 2018/19 $91000

Dividend income from Electric Blue $56000

Deductions $2300

Taxable Income $144700 (label O)

CAPITAL GAINS

After effects on death of taxpayer’s are laid under division 128 of ITAA 1997 and capital

gain assets are developed to legal representatives or beneficiary of estate. Where pre -CGT asset

is acquired by beneficiary, it is deemed that asset have been acquired at market rates on date of

death by him or her: s128-15(4). Where post- CGT asset is acquired by beneficiary asset is

deemed to be acquired at cost base of deceased person on death date :s 128-154(4). BHP will be

acquired as pre- CGT asset by client at market value on death date on 15 July, 2018. The

remaining shares will be acquired by client at initial cost at which they were acquired by owner.

As per CGT acquisition & timing s109-5 ITAA97 – GST asset is acquired when they become

the owner. According to s128-10 death is not termed as CGT event means CGT is not payable

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

till the sale of shares. Clients are not required to worry about share values or or their effects on

taxable or assessable income till they are sold.

Inheritance of shares from the deceased father

Share Date of

purchase by

father

Number of

shares

Price paid per

share

Market value

on death date,

15 July 2018

Total value

inherited

BHP 04/01/85 2500 $ 5 $ 20.30 $ 50750

CBA 12/09/91 2000 $ 5.4 $ 75.94 $ 10800

COH 04/12/95 1000 $ 2.9 $ 124.77 $ 2900

FLT 01/12/95 1000 $ 0.95 $ 32.29 $ 950

MYR 07/11/09 9000 $ 4.10 $ 1.21 $ 36900

TLS 03/11/09 2000 $ 3.3 $ 5.75 $ 6600

TOTAL 17500 $ 108900

Capital proceeds 116-20 ITAA97 Usually amount of money or/and market value of property

received or receivable in respect of CGT by taxpayer.

Share Disposal s104-5 A1 ITAA 97

Number Selling

price

Brokerage

fees

Net

Disposal

CGT

Profit / loss

on disposal

5th Jan,2017

Disposal of

BHP

2500 $25.63 $64075 $ 115 $63960 $ 13210

5th Jan,2017

Disposal of

MYR

10000 $1.35 $13500 $ 50 $13450 $ -23450

Brokerage fees are added as incidental cost s110-25(3) ITAA97.

BHP shares were not held by client for more than 12 months therefore discount method will not

apply and full profits will be taxed on disposing BHP shares of $ 13210.

Profit of BHP shares will be off setted by client with loss from MYR shares. Offset is not

available for other taxable items but only against capital gains as per s102-15(1) ITAA97. Gain

5

taxable or assessable income till they are sold.

Inheritance of shares from the deceased father

Share Date of

purchase by

father

Number of

shares

Price paid per

share

Market value

on death date,

15 July 2018

Total value

inherited

BHP 04/01/85 2500 $ 5 $ 20.30 $ 50750

CBA 12/09/91 2000 $ 5.4 $ 75.94 $ 10800

COH 04/12/95 1000 $ 2.9 $ 124.77 $ 2900

FLT 01/12/95 1000 $ 0.95 $ 32.29 $ 950

MYR 07/11/09 9000 $ 4.10 $ 1.21 $ 36900

TLS 03/11/09 2000 $ 3.3 $ 5.75 $ 6600

TOTAL 17500 $ 108900

Capital proceeds 116-20 ITAA97 Usually amount of money or/and market value of property

received or receivable in respect of CGT by taxpayer.

Share Disposal s104-5 A1 ITAA 97

Number Selling

price

Brokerage

fees

Net

Disposal

CGT

Profit / loss

on disposal

5th Jan,2017

Disposal of

BHP

2500 $25.63 $64075 $ 115 $63960 $ 13210

5th Jan,2017

Disposal of

MYR

10000 $1.35 $13500 $ 50 $13450 $ -23450

Brokerage fees are added as incidental cost s110-25(3) ITAA97.

BHP shares were not held by client for more than 12 months therefore discount method will not

apply and full profits will be taxed on disposing BHP shares of $ 13210.

Profit of BHP shares will be off setted by client with loss from MYR shares. Offset is not

available for other taxable items but only against capital gains as per s102-15(1) ITAA97. Gain

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

on disposal of BHP shares is reduced s104-10(5) ITAA97. The client is having net Capital gain

loss of $ 10220.

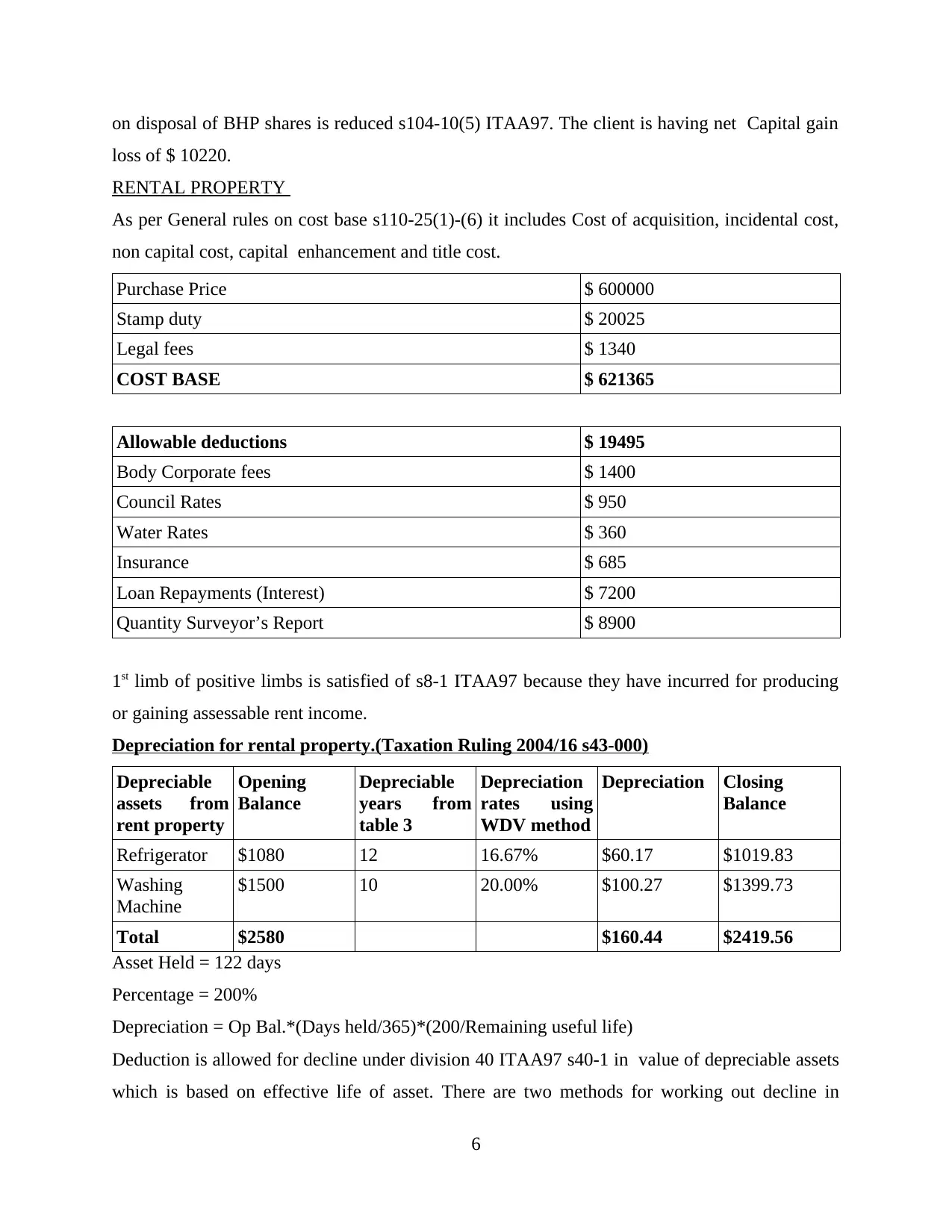

RENTAL PROPERTY

As per General rules on cost base s110-25(1)-(6) it includes Cost of acquisition, incidental cost,

non capital cost, capital enhancement and title cost.

Purchase Price $ 600000

Stamp duty $ 20025

Legal fees $ 1340

COST BASE $ 621365

Allowable deductions $ 19495

Body Corporate fees $ 1400

Council Rates $ 950

Water Rates $ 360

Insurance $ 685

Loan Repayments (Interest) $ 7200

Quantity Surveyor’s Report $ 8900

1st limb of positive limbs is satisfied of s8-1 ITAA97 because they have incurred for producing

or gaining assessable rent income.

Depreciation for rental property.(Taxation Ruling 2004/16 s43-000)

Depreciable

assets from

rent property

Opening

Balance

Depreciable

years from

table 3

Depreciation

rates using

WDV method

Depreciation Closing

Balance

Refrigerator $1080 12 16.67% $60.17 $1019.83

Washing

Machine

$1500 10 20.00% $100.27 $1399.73

Total $2580 $160.44 $2419.56

Asset Held = 122 days

Percentage = 200%

Depreciation = Op Bal.*(Days held/365)*(200/Remaining useful life)

Deduction is allowed for decline under division 40 ITAA97 s40-1 in value of depreciable assets

which is based on effective life of asset. There are two methods for working out decline in

6

loss of $ 10220.

RENTAL PROPERTY

As per General rules on cost base s110-25(1)-(6) it includes Cost of acquisition, incidental cost,

non capital cost, capital enhancement and title cost.

Purchase Price $ 600000

Stamp duty $ 20025

Legal fees $ 1340

COST BASE $ 621365

Allowable deductions $ 19495

Body Corporate fees $ 1400

Council Rates $ 950

Water Rates $ 360

Insurance $ 685

Loan Repayments (Interest) $ 7200

Quantity Surveyor’s Report $ 8900

1st limb of positive limbs is satisfied of s8-1 ITAA97 because they have incurred for producing

or gaining assessable rent income.

Depreciation for rental property.(Taxation Ruling 2004/16 s43-000)

Depreciable

assets from

rent property

Opening

Balance

Depreciable

years from

table 3

Depreciation

rates using

WDV method

Depreciation Closing

Balance

Refrigerator $1080 12 16.67% $60.17 $1019.83

Washing

Machine

$1500 10 20.00% $100.27 $1399.73

Total $2580 $160.44 $2419.56

Asset Held = 122 days

Percentage = 200%

Depreciation = Op Bal.*(Days held/365)*(200/Remaining useful life)

Deduction is allowed for decline under division 40 ITAA97 s40-1 in value of depreciable assets

which is based on effective life of asset. There are two methods for working out decline in

6

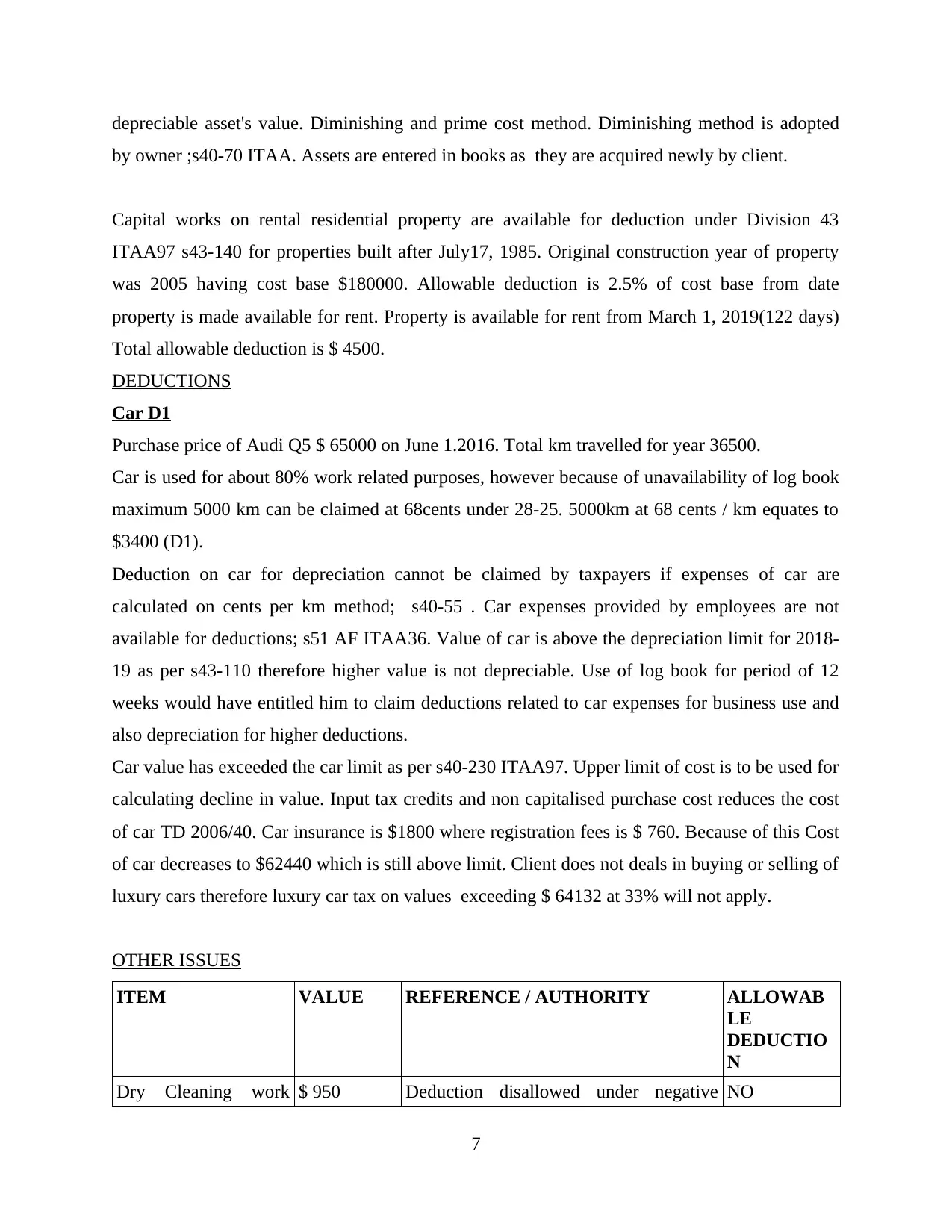

depreciable asset's value. Diminishing and prime cost method. Diminishing method is adopted

by owner ;s40-70 ITAA. Assets are entered in books as they are acquired newly by client.

Capital works on rental residential property are available for deduction under Division 43

ITAA97 s43-140 for properties built after July17, 1985. Original construction year of property

was 2005 having cost base $180000. Allowable deduction is 2.5% of cost base from date

property is made available for rent. Property is available for rent from March 1, 2019(122 days)

Total allowable deduction is $ 4500.

DEDUCTIONS

Car D1

Purchase price of Audi Q5 $ 65000 on June 1.2016. Total km travelled for year 36500.

Car is used for about 80% work related purposes, however because of unavailability of log book

maximum 5000 km can be claimed at 68cents under 28-25. 5000km at 68 cents / km equates to

$3400 (D1).

Deduction on car for depreciation cannot be claimed by taxpayers if expenses of car are

calculated on cents per km method; s40-55 . Car expenses provided by employees are not

available for deductions; s51 AF ITAA36. Value of car is above the depreciation limit for 2018-

19 as per s43-110 therefore higher value is not depreciable. Use of log book for period of 12

weeks would have entitled him to claim deductions related to car expenses for business use and

also depreciation for higher deductions.

Car value has exceeded the car limit as per s40-230 ITAA97. Upper limit of cost is to be used for

calculating decline in value. Input tax credits and non capitalised purchase cost reduces the cost

of car TD 2006/40. Car insurance is $1800 where registration fees is $ 760. Because of this Cost

of car decreases to $62440 which is still above limit. Client does not deals in buying or selling of

luxury cars therefore luxury car tax on values exceeding $ 64132 at 33% will not apply.

OTHER ISSUES

ITEM VALUE REFERENCE / AUTHORITY ALLOWAB

LE

DEDUCTIO

N

Dry Cleaning work $ 950 Deduction disallowed under negative NO

7

by owner ;s40-70 ITAA. Assets are entered in books as they are acquired newly by client.

Capital works on rental residential property are available for deduction under Division 43

ITAA97 s43-140 for properties built after July17, 1985. Original construction year of property

was 2005 having cost base $180000. Allowable deduction is 2.5% of cost base from date

property is made available for rent. Property is available for rent from March 1, 2019(122 days)

Total allowable deduction is $ 4500.

DEDUCTIONS

Car D1

Purchase price of Audi Q5 $ 65000 on June 1.2016. Total km travelled for year 36500.

Car is used for about 80% work related purposes, however because of unavailability of log book

maximum 5000 km can be claimed at 68cents under 28-25. 5000km at 68 cents / km equates to

$3400 (D1).

Deduction on car for depreciation cannot be claimed by taxpayers if expenses of car are

calculated on cents per km method; s40-55 . Car expenses provided by employees are not

available for deductions; s51 AF ITAA36. Value of car is above the depreciation limit for 2018-

19 as per s43-110 therefore higher value is not depreciable. Use of log book for period of 12

weeks would have entitled him to claim deductions related to car expenses for business use and

also depreciation for higher deductions.

Car value has exceeded the car limit as per s40-230 ITAA97. Upper limit of cost is to be used for

calculating decline in value. Input tax credits and non capitalised purchase cost reduces the cost

of car TD 2006/40. Car insurance is $1800 where registration fees is $ 760. Because of this Cost

of car decreases to $62440 which is still above limit. Client does not deals in buying or selling of

luxury cars therefore luxury car tax on values exceeding $ 64132 at 33% will not apply.

OTHER ISSUES

ITEM VALUE REFERENCE / AUTHORITY ALLOWAB

LE

DEDUCTIO

N

Dry Cleaning work $ 950 Deduction disallowed under negative NO

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

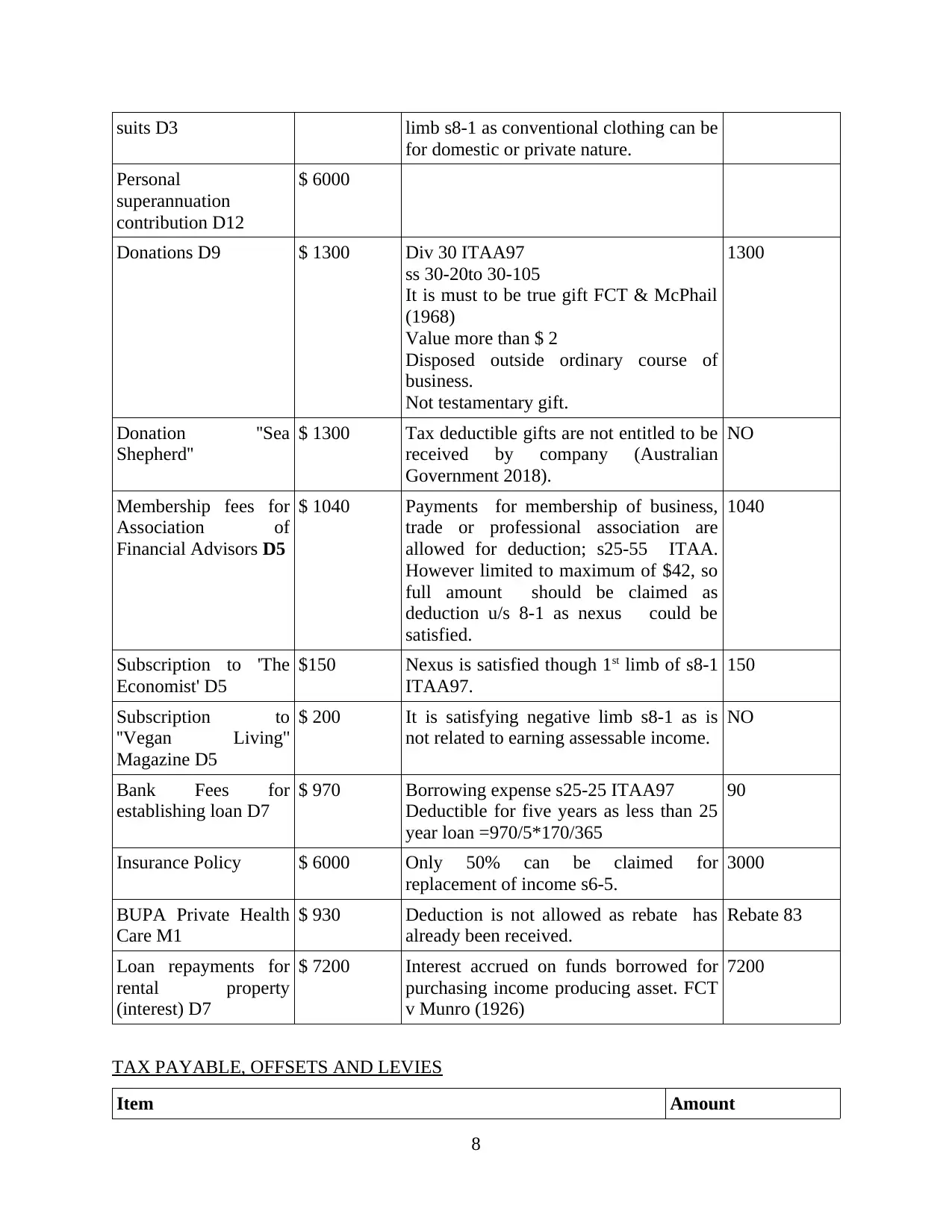

suits D3 limb s8-1 as conventional clothing can be

for domestic or private nature.

Personal

superannuation

contribution D12

$ 6000

Donations D9 $ 1300 Div 30 ITAA97

ss 30-20to 30-105

It is must to be true gift FCT & McPhail

(1968)

Value more than $ 2

Disposed outside ordinary course of

business.

Not testamentary gift.

1300

Donation ''Sea

Shepherd''

$ 1300 Tax deductible gifts are not entitled to be

received by company (Australian

Government 2018).

NO

Membership fees for

Association of

Financial Advisors D5

$ 1040 Payments for membership of business,

trade or professional association are

allowed for deduction; s25-55 ITAA.

However limited to maximum of $42, so

full amount should be claimed as

deduction u/s 8-1 as nexus could be

satisfied.

1040

Subscription to 'The

Economist' D5

$150 Nexus is satisfied though 1st limb of s8-1

ITAA97.

150

Subscription to

''Vegan Living''

Magazine D5

$ 200 It is satisfying negative limb s8-1 as is

not related to earning assessable income.

NO

Bank Fees for

establishing loan D7

$ 970 Borrowing expense s25-25 ITAA97

Deductible for five years as less than 25

year loan =970/5*170/365

90

Insurance Policy $ 6000 Only 50% can be claimed for

replacement of income s6-5.

3000

BUPA Private Health

Care M1

$ 930 Deduction is not allowed as rebate has

already been received.

Rebate 83

Loan repayments for

rental property

(interest) D7

$ 7200 Interest accrued on funds borrowed for

purchasing income producing asset. FCT

v Munro (1926)

7200

TAX PAYABLE, OFFSETS AND LEVIES

Item Amount

8

for domestic or private nature.

Personal

superannuation

contribution D12

$ 6000

Donations D9 $ 1300 Div 30 ITAA97

ss 30-20to 30-105

It is must to be true gift FCT & McPhail

(1968)

Value more than $ 2

Disposed outside ordinary course of

business.

Not testamentary gift.

1300

Donation ''Sea

Shepherd''

$ 1300 Tax deductible gifts are not entitled to be

received by company (Australian

Government 2018).

NO

Membership fees for

Association of

Financial Advisors D5

$ 1040 Payments for membership of business,

trade or professional association are

allowed for deduction; s25-55 ITAA.

However limited to maximum of $42, so

full amount should be claimed as

deduction u/s 8-1 as nexus could be

satisfied.

1040

Subscription to 'The

Economist' D5

$150 Nexus is satisfied though 1st limb of s8-1

ITAA97.

150

Subscription to

''Vegan Living''

Magazine D5

$ 200 It is satisfying negative limb s8-1 as is

not related to earning assessable income.

NO

Bank Fees for

establishing loan D7

$ 970 Borrowing expense s25-25 ITAA97

Deductible for five years as less than 25

year loan =970/5*170/365

90

Insurance Policy $ 6000 Only 50% can be claimed for

replacement of income s6-5.

3000

BUPA Private Health

Care M1

$ 930 Deduction is not allowed as rebate has

already been received.

Rebate 83

Loan repayments for

rental property

(interest) D7

$ 7200 Interest accrued on funds borrowed for

purchasing income producing asset. FCT

v Munro (1926)

7200

TAX PAYABLE, OFFSETS AND LEVIES

Item Amount

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

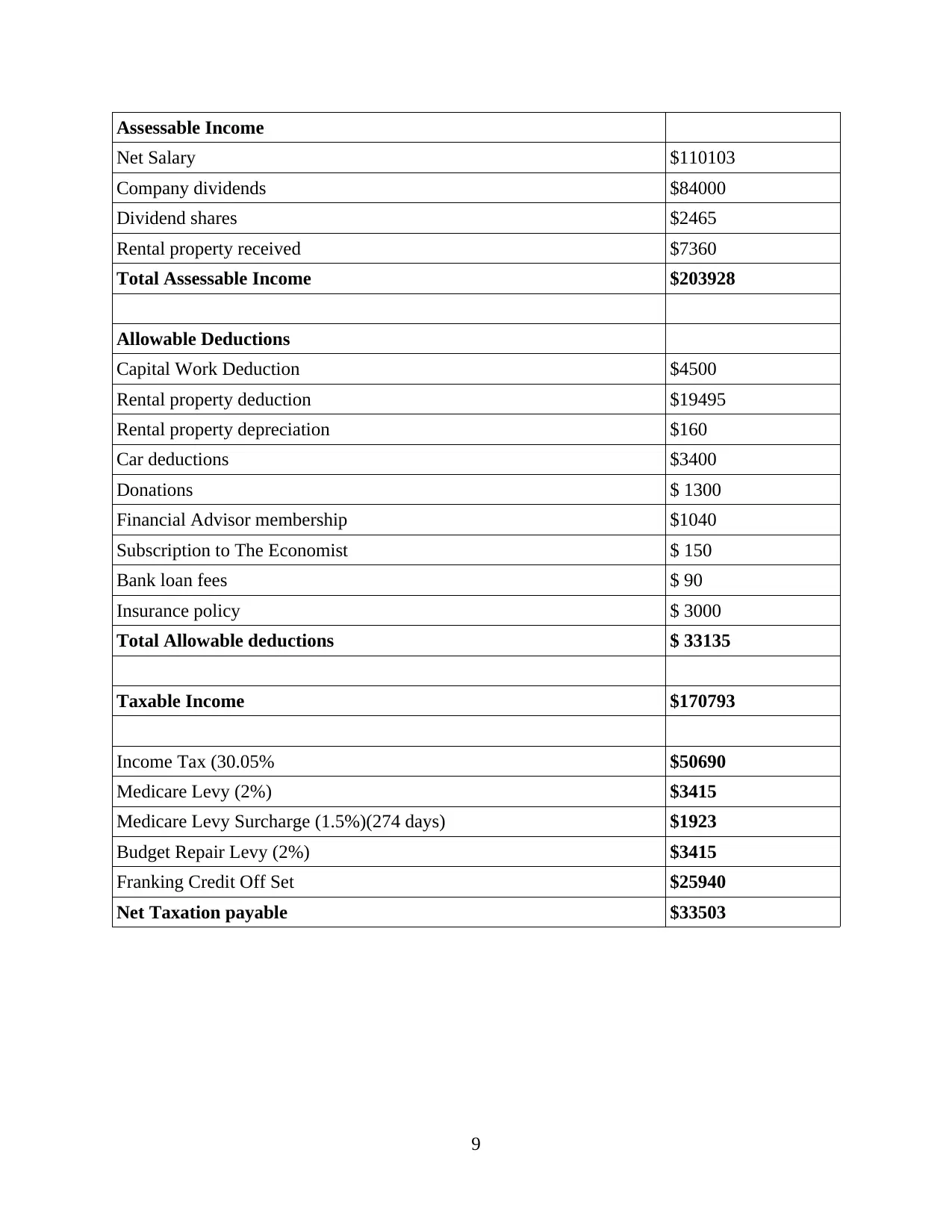

Assessable Income

Net Salary $110103

Company dividends $84000

Dividend shares $2465

Rental property received $7360

Total Assessable Income $203928

Allowable Deductions

Capital Work Deduction $4500

Rental property deduction $19495

Rental property depreciation $160

Car deductions $3400

Donations $ 1300

Financial Advisor membership $1040

Subscription to The Economist $ 150

Bank loan fees $ 90

Insurance policy $ 3000

Total Allowable deductions $ 33135

Taxable Income $170793

Income Tax (30.05% $50690

Medicare Levy (2%) $3415

Medicare Levy Surcharge (1.5%)(274 days) $1923

Budget Repair Levy (2%) $3415

Franking Credit Off Set $25940

Net Taxation payable $33503

9

Net Salary $110103

Company dividends $84000

Dividend shares $2465

Rental property received $7360

Total Assessable Income $203928

Allowable Deductions

Capital Work Deduction $4500

Rental property deduction $19495

Rental property depreciation $160

Car deductions $3400

Donations $ 1300

Financial Advisor membership $1040

Subscription to The Economist $ 150

Bank loan fees $ 90

Insurance policy $ 3000

Total Allowable deductions $ 33135

Taxable Income $170793

Income Tax (30.05% $50690

Medicare Levy (2%) $3415

Medicare Levy Surcharge (1.5%)(274 days) $1923

Budget Repair Levy (2%) $3415

Franking Credit Off Set $25940

Net Taxation payable $33503

9

REFERENCES

Books and Journals

Anaf, J., Baum, F. and Fisher, M., 2018. A citizens’ jury on regulation of McDonald's products

and operations in Australia in response to a corporate health impact assessment. Australian

and New Zealand journal of public health. 42(2). pp.133-139.

Appel, H., 2018. How Neoliberal Reforms Lose Their Partisan Identity: Flat Tax Diffusion in

Eastern Europe and Post-Soviet Eurasia. Europe-Asia Studies. 70(7). pp.1121-1142.

Buchanan, R. and Consett, E., 2016. Section 974-80 ITAA97: The current state of play. Tax

Specialist. 19(5). p.217.

Buchmueller, T. C. and et.al., 2016. Effect of the Affordable Care Act on racial and ethnic

disparities in health insurance coverage. American journal of public health. 106(8).

pp.1416-1421.

Campbell, S., 2018. Personal liability of a trustee to tax on trust income: Part 1. Taxation in

Australia. 53(5). p.263.

Campbell, S., 2018. Personal liability of a trustee to tax on trust income: Part 2. Taxation in

Australia. 53(6). p.322.

De Bruyne, J., 2018. A Conceptual and Comparative Analysis of the Obligations of Third-Party

Certifiers. Ohio NUL Rev. 44. p.203.

Hodgson, H. and Pearce, P., 2015. TravelSmart of Travel Tax Breaks: Is the Fringe Benefits

Tax a Barrier to Active Commuting in Australia. EJTR. 13. p.819.

Lee, J., 2018. The Effectiveness of Part IVA of the Income Tax Assessment Act 1936 (CTH):

Time for a Not Merely Incidental'Purpose Test. J. Austl. Tax'n. 20. p.1.

McGregor-Lowndes, M. and Williamson, A., 2018. Foundations in Australia: Dimensions for

international comparison. American Behavioral Scientist. 62(13). pp.1759-1776.

Neilson, T., 2018. Effect of share premium account on continuity of ownership test analysis.

Tax Specialist. 22(1). p.15.

10

Books and Journals

Anaf, J., Baum, F. and Fisher, M., 2018. A citizens’ jury on regulation of McDonald's products

and operations in Australia in response to a corporate health impact assessment. Australian

and New Zealand journal of public health. 42(2). pp.133-139.

Appel, H., 2018. How Neoliberal Reforms Lose Their Partisan Identity: Flat Tax Diffusion in

Eastern Europe and Post-Soviet Eurasia. Europe-Asia Studies. 70(7). pp.1121-1142.

Buchanan, R. and Consett, E., 2016. Section 974-80 ITAA97: The current state of play. Tax

Specialist. 19(5). p.217.

Buchmueller, T. C. and et.al., 2016. Effect of the Affordable Care Act on racial and ethnic

disparities in health insurance coverage. American journal of public health. 106(8).

pp.1416-1421.

Campbell, S., 2018. Personal liability of a trustee to tax on trust income: Part 1. Taxation in

Australia. 53(5). p.263.

Campbell, S., 2018. Personal liability of a trustee to tax on trust income: Part 2. Taxation in

Australia. 53(6). p.322.

De Bruyne, J., 2018. A Conceptual and Comparative Analysis of the Obligations of Third-Party

Certifiers. Ohio NUL Rev. 44. p.203.

Hodgson, H. and Pearce, P., 2015. TravelSmart of Travel Tax Breaks: Is the Fringe Benefits

Tax a Barrier to Active Commuting in Australia. EJTR. 13. p.819.

Lee, J., 2018. The Effectiveness of Part IVA of the Income Tax Assessment Act 1936 (CTH):

Time for a Not Merely Incidental'Purpose Test. J. Austl. Tax'n. 20. p.1.

McGregor-Lowndes, M. and Williamson, A., 2018. Foundations in Australia: Dimensions for

international comparison. American Behavioral Scientist. 62(13). pp.1759-1776.

Neilson, T., 2018. Effect of share premium account on continuity of ownership test analysis.

Tax Specialist. 22(1). p.15.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.