Management Accounting Research Trends

VerifiedAdded on 2020/01/07

|19

|5391

|340

Literature Review

AI Summary

This assignment delves into contemporary research within the field of management accounting. It examines various themes shaping the discipline, including environmental management accounting, the influence of social and environmental considerations on organizational change, and the adoption of popular management accounting ideas like the balanced scorecard. The document also explores the role of strategic management accounting, its connection to popular culture, and methodological advancements in qualitative research within the field.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Assignment

Management Accounting

Student Name:

Student ID:

College Name:

College ID:

1

Management Accounting

Student Name:

Student ID:

College Name:

College ID:

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Introduction.................................................................................................................................3

Task 1...........................................................................................................................................3

LO1: Explanation of the management accounting system.....................................................3

P1: Essential requirements of the different types of management accounting system.............3

P2: Methods of management accounting system......................................................................6

Task 2...........................................................................................................................................8

LO2: Application of the Management accounting techniques...............................................8

P3: Preparation of the income statement by using the marginal and absorption costs.............8

Task 3.........................................................................................................................................13

LO3: Use of different planning tools in the management accounting system....................13

P4: Explanation of the advantages and disadvantages of using the different types of planning

tools used for budgetary control..............................................................................................13

LO4: The process that should be followed by organisations to use the management

accounting system to respond the financial problems.........................................................14

P5: The process that should be followed by the organisation to adapt management

accounting system to resolve the financial problems..............................................................14

Conclusion.................................................................................................................................17

Bibliography..............................................................................................................................17

2

Introduction.................................................................................................................................3

Task 1...........................................................................................................................................3

LO1: Explanation of the management accounting system.....................................................3

P1: Essential requirements of the different types of management accounting system.............3

P2: Methods of management accounting system......................................................................6

Task 2...........................................................................................................................................8

LO2: Application of the Management accounting techniques...............................................8

P3: Preparation of the income statement by using the marginal and absorption costs.............8

Task 3.........................................................................................................................................13

LO3: Use of different planning tools in the management accounting system....................13

P4: Explanation of the advantages and disadvantages of using the different types of planning

tools used for budgetary control..............................................................................................13

LO4: The process that should be followed by organisations to use the management

accounting system to respond the financial problems.........................................................14

P5: The process that should be followed by the organisation to adapt management

accounting system to resolve the financial problems..............................................................14

Conclusion.................................................................................................................................17

Bibliography..............................................................................................................................17

2

Introduction

Accountability is a vital part of the business organisations. Organisations do different

business activities to survive in the industry. Therefore, organisations have to invest a

lot of money to do the business activities in an efficient manner. Organisations also

have to adopt an accountability process to calculate the expenses made in the business

activities and keep the record of expenses that will be used by the auditor to prepare

the financial statement of the company (Fullerton et al. 2014, p. 420). Organisations

have to calculate the cost of the business activities in an efficient manner to minimize

the cost of the organisations and maximize the profit of the organisation. Organisation

basically does their business activities for achieving different objectives but wealth and

profit maximization. Organisations can easily achieve the profit maximization objectives

by using the management accounting. Organisations prepare the budget for the

business activities by using past experiences and techniques of the management

accounting. The preparation of budgets provide organisations a detail information about

the cost and income of a particular business activity in the organisation. The following

study will discuss about the application of management accounting in the organisation

to prepare such budgets for the business activities in the organisations and the role of

management accounting behind the success of the organisations.

Task 1

LO1: Explanation of the management accounting system

P1: Essential requirements of the different types of management accounting system

Management accounting system played a vital role in the financial management

department of the organisations. Management accounting is a process by which

organisations prepare the sources of the capital to invest in the business activity,

analyze the cost areas of the business activity in which organisations have to invest the

3

Accountability is a vital part of the business organisations. Organisations do different

business activities to survive in the industry. Therefore, organisations have to invest a

lot of money to do the business activities in an efficient manner. Organisations also

have to adopt an accountability process to calculate the expenses made in the business

activities and keep the record of expenses that will be used by the auditor to prepare

the financial statement of the company (Fullerton et al. 2014, p. 420). Organisations

have to calculate the cost of the business activities in an efficient manner to minimize

the cost of the organisations and maximize the profit of the organisation. Organisation

basically does their business activities for achieving different objectives but wealth and

profit maximization. Organisations can easily achieve the profit maximization objectives

by using the management accounting. Organisations prepare the budget for the

business activities by using past experiences and techniques of the management

accounting. The preparation of budgets provide organisations a detail information about

the cost and income of a particular business activity in the organisation. The following

study will discuss about the application of management accounting in the organisation

to prepare such budgets for the business activities in the organisations and the role of

management accounting behind the success of the organisations.

Task 1

LO1: Explanation of the management accounting system

P1: Essential requirements of the different types of management accounting system

Management accounting system played a vital role in the financial management

department of the organisations. Management accounting is a process by which

organisations prepare the sources of the capital to invest in the business activity,

analyze the cost areas of the business activity in which organisations have to invest the

3

resources properly and communicate different ideas that help the decision makers of

the organisation to makes some effective decisions towards the different aspects

business activities (Otley and Emmanuel, 2013, p. 225). Management accounting

system is a combination of accounting, finance and management therefore, this system

provide relevant information associated with such activities in the organisation. The

skills and techniques of the management accountant not only keep the account of the

different business activities but also provide advice to the managers of about the

implication of different financial measures in the activities, take some major decisions in

the activity, formulation of different business strategies in the organisation to monitoring

the risk and maintain a sustainable success of the organisations. Organisations have to

understand the scope of the management accounting system to understand the

requirements of this system in the organization (Cooper et al. 2017, p. 455).

A) Management accounting system provide some relevant information about the status

of national and global economy that help the organisation not only to prepare some

effective financial strategy to finance the activities but also help to prepare the

marketing and resource management strategies to run the business activities of

organisation successfully.

B) Management accounting system also help the organisation to manage the

performance of the business activities by providing some relevant information

associated with the performance of the business activities. Management accounting

measure the performance of the activities based on the financial performance therefore,

organisation can get a clear vision about the financial performance of different aspects

of the business activities in details (Ax, and Greve, 2017, p.65).

C) As management accounting provides different information about the national and

global economy therefore, the organisation can get a clear view about the risk

associated with such business activities. Management accounting also provide some

tools and techniques to manage such risk associated with the business activities.

Cost accounting system- The system under which firm able to analyse about

costing level which incurred in various process of business. In this,

administrative, marketing, production, employee etc. related costs are recorded

4

the organisation to makes some effective decisions towards the different aspects

business activities (Otley and Emmanuel, 2013, p. 225). Management accounting

system is a combination of accounting, finance and management therefore, this system

provide relevant information associated with such activities in the organisation. The

skills and techniques of the management accountant not only keep the account of the

different business activities but also provide advice to the managers of about the

implication of different financial measures in the activities, take some major decisions in

the activity, formulation of different business strategies in the organisation to monitoring

the risk and maintain a sustainable success of the organisations. Organisations have to

understand the scope of the management accounting system to understand the

requirements of this system in the organization (Cooper et al. 2017, p. 455).

A) Management accounting system provide some relevant information about the status

of national and global economy that help the organisation not only to prepare some

effective financial strategy to finance the activities but also help to prepare the

marketing and resource management strategies to run the business activities of

organisation successfully.

B) Management accounting system also help the organisation to manage the

performance of the business activities by providing some relevant information

associated with the performance of the business activities. Management accounting

measure the performance of the activities based on the financial performance therefore,

organisation can get a clear vision about the financial performance of different aspects

of the business activities in details (Ax, and Greve, 2017, p.65).

C) As management accounting provides different information about the national and

global economy therefore, the organisation can get a clear view about the risk

associated with such business activities. Management accounting also provide some

tools and techniques to manage such risk associated with the business activities.

Cost accounting system- The system under which firm able to analyse about

costing level which incurred in various process of business. In this,

administrative, marketing, production, employee etc. related costs are recorded

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

properly in the books of account. Basic requirement of this kind of management

accounting system within business entity is to assess overall costs and expenses

of the products and services. Apart from this, to determine selling price of goods

and services are to be taken by management with the help of cost accounting.

Job costing system- Within business enterprise there are different jobs are

used to produce products and services. At this condition to assess total cost of

every job there is job costing system is taken into account. This kind of

management accounting system is generally used in the construction company

where costs of different jobs is analysed. Along with this, allocation of financial

resources to specific jobs is also done effectively by the management after using

job costing system.

Batch costing system- In the firm, different types of products as well as

services are to be manufactured in various batches. With the help of batch

costing system the company able to record costs of every batch which supports

to analyse costing of various number of batches. For instance, there is a firm

which produce toffees of three flavours like vanilla, chocolate and strawberry.

Moreover, by using batch costing system it able to know cost of all the three

kinds of toffees which helps to charge selling prices in accordance to that.

Inventory management system- Stock is one of the major component of every

company and lower the inventory level is beneficial for it. The company requires

respective kind of system to manage and reduce the stock within firm as well as

utilise it in optimum manner. When management able to optimum utilisation of

stock then can generate high revenue and profit. Along with this, valuation of

stock is also done by firm with the support of various methods like LIFO, FOFO

as well as weighted average.

Price optimisation system- In the business entity, pricing factor plays highly

significant role because by this it able to sale its products and services up to

consumers. With the help of price optimising system firm able to adopt specific

selling price which will be profitable for it. For example: management charge four

level of prices and particular level at which more number of users attract then it

will opt that specific selling price.

5

accounting system within business entity is to assess overall costs and expenses

of the products and services. Apart from this, to determine selling price of goods

and services are to be taken by management with the help of cost accounting.

Job costing system- Within business enterprise there are different jobs are

used to produce products and services. At this condition to assess total cost of

every job there is job costing system is taken into account. This kind of

management accounting system is generally used in the construction company

where costs of different jobs is analysed. Along with this, allocation of financial

resources to specific jobs is also done effectively by the management after using

job costing system.

Batch costing system- In the firm, different types of products as well as

services are to be manufactured in various batches. With the help of batch

costing system the company able to record costs of every batch which supports

to analyse costing of various number of batches. For instance, there is a firm

which produce toffees of three flavours like vanilla, chocolate and strawberry.

Moreover, by using batch costing system it able to know cost of all the three

kinds of toffees which helps to charge selling prices in accordance to that.

Inventory management system- Stock is one of the major component of every

company and lower the inventory level is beneficial for it. The company requires

respective kind of system to manage and reduce the stock within firm as well as

utilise it in optimum manner. When management able to optimum utilisation of

stock then can generate high revenue and profit. Along with this, valuation of

stock is also done by firm with the support of various methods like LIFO, FOFO

as well as weighted average.

Price optimisation system- In the business entity, pricing factor plays highly

significant role because by this it able to sale its products and services up to

consumers. With the help of price optimising system firm able to adopt specific

selling price which will be profitable for it. For example: management charge four

level of prices and particular level at which more number of users attract then it

will opt that specific selling price.

5

P2: Methods of management accounting system

The all above scope of the management accounting system help the organisation to

understand the importance of the management accounting in the organisation. The

study also provides a brief information about the requirements of the management

accounting to the organisation. The importances of the management accounting system

in the organisations are as follows:

A) Management accounting system provides clear information about the different

sources of capital that can be used by the organisation to meet the requirements of

capital for doing the business activities (Wagenhofer, 2016, p.115). Management

accounting also help the organisation by preparing different financial statements that

will be used by the organisation to attract the investors for the different capital market.

Management accounting also provide some measures to the organisation that can be

used to satisfy the investors and attract more investors to increase the capital of the

organisations. Continuous flow of capital in the organisation help to do the business

activities without any interruptions for the supply of raw materials, power and other

essential resources in the business activities

B) Management accounting also help the organisation by providing relevant information

about the different aspects of cost associated with the business activities. Based on

such information management accounting system develop some budget for the

business activities of the organization (Van der Stede, 2016 p.101). Organisation gets a

clear idea about the cost of the activity and the amount of revenue generated from the

activity. Management accountant also provide some measures to minimize the cost of

the activities and maximize the revenues generated from the business activities. The

minimization of cost and the maximization of revenues help the organisation to

maximize the profit and wealth of the company.

C) Management accounting analyzes the different aspects of cost associated with the

business activities in details and tries to get some vital information about the

performance of the activities. While the performance of the business activities are not

well at this situation management accounting try to identify the problems in the system

of the activities for which the performance of the activity suffering. Management

accounting also try to create some solutions to do the business activities in an efficient

6

The all above scope of the management accounting system help the organisation to

understand the importance of the management accounting in the organisation. The

study also provides a brief information about the requirements of the management

accounting to the organisation. The importances of the management accounting system

in the organisations are as follows:

A) Management accounting system provides clear information about the different

sources of capital that can be used by the organisation to meet the requirements of

capital for doing the business activities (Wagenhofer, 2016, p.115). Management

accounting also help the organisation by preparing different financial statements that

will be used by the organisation to attract the investors for the different capital market.

Management accounting also provide some measures to the organisation that can be

used to satisfy the investors and attract more investors to increase the capital of the

organisations. Continuous flow of capital in the organisation help to do the business

activities without any interruptions for the supply of raw materials, power and other

essential resources in the business activities

B) Management accounting also help the organisation by providing relevant information

about the different aspects of cost associated with the business activities. Based on

such information management accounting system develop some budget for the

business activities of the organization (Van der Stede, 2016 p.101). Organisation gets a

clear idea about the cost of the activity and the amount of revenue generated from the

activity. Management accountant also provide some measures to minimize the cost of

the activities and maximize the revenues generated from the business activities. The

minimization of cost and the maximization of revenues help the organisation to

maximize the profit and wealth of the company.

C) Management accounting analyzes the different aspects of cost associated with the

business activities in details and tries to get some vital information about the

performance of the activities. While the performance of the business activities are not

well at this situation management accounting try to identify the problems in the system

of the activities for which the performance of the activity suffering. Management

accounting also try to create some solutions to do the business activities in an efficient

6

manner. Management accountant have to communicate with the organisations for

providing all such relevant information associated with business activities and provide

some effective measures to apply the solutions in the activity to solve the problems.

D) Management accounting also analyze the different aspects associated with the

global and national environment for the organisation. The detail analysis of the

information associated with the environment provides a brief knowledge about the

changes in the economy, politically, socially and technologically (Northcott, 2014,

p.114). Such analyses help the organisation to avoid the risk associated with the

environmental factors. Management accounting is also analysis the development of

technological environment to get the information about the new cost effective

machineries and production process. Management accounting suggest the company to

install and adopt such machineries and production process in the production activity to

reduce the production cost and improve the quality of the products. The low cost of

production also provide a competitive advantages to the in the market and the company

can sale good quality products at a low price. These measures help the company to

maximize the market share in the industry (Christ and Burritt, 2013, p.165).

E) The budgets prepared by the management accounting help the organisation to

prepare some efficient strategy to manage the activities in an efficient manner.

Sometime management accounting suggests the company to announce the interim

dividend or bonus for the investors of the capital market. That increases the price of the

shares of the company in the capital market and increase the goodwill of the shares of

the company among the investors. Increment in the goodwill and price of the shares

attract more investors to buy the shares of the company that increase the capital of the

company.

The all above activities done by the management accounting system increase its

requirements in the organization (Contrafatto and Burns, 2013, p.355). In the present

global situation of the economy also increase the requirements of the management

accounting system in the organisation because it is not possible for the company to

manage the business activities in an efficient manner without management accounting

system.

7

providing all such relevant information associated with business activities and provide

some effective measures to apply the solutions in the activity to solve the problems.

D) Management accounting also analyze the different aspects associated with the

global and national environment for the organisation. The detail analysis of the

information associated with the environment provides a brief knowledge about the

changes in the economy, politically, socially and technologically (Northcott, 2014,

p.114). Such analyses help the organisation to avoid the risk associated with the

environmental factors. Management accounting is also analysis the development of

technological environment to get the information about the new cost effective

machineries and production process. Management accounting suggest the company to

install and adopt such machineries and production process in the production activity to

reduce the production cost and improve the quality of the products. The low cost of

production also provide a competitive advantages to the in the market and the company

can sale good quality products at a low price. These measures help the company to

maximize the market share in the industry (Christ and Burritt, 2013, p.165).

E) The budgets prepared by the management accounting help the organisation to

prepare some efficient strategy to manage the activities in an efficient manner.

Sometime management accounting suggests the company to announce the interim

dividend or bonus for the investors of the capital market. That increases the price of the

shares of the company in the capital market and increase the goodwill of the shares of

the company among the investors. Increment in the goodwill and price of the shares

attract more investors to buy the shares of the company that increase the capital of the

company.

The all above activities done by the management accounting system increase its

requirements in the organization (Contrafatto and Burns, 2013, p.355). In the present

global situation of the economy also increase the requirements of the management

accounting system in the organisation because it is not possible for the company to

manage the business activities in an efficient manner without management accounting

system.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 2

LO2: Application of the Management accounting techniques

P3: Preparation of the income statement by using the marginal and absorption costs

Management accounting system is using different types of techniques to manage the

performance of the activities of the organisation efficiently. The techniques of

management accounting system are as follows:

Financial planning: Maximize the profit of the company is one of the major objectives

of the management accounting system. Management accounting system prepares

some appropriate plan to manage the activities of the organisation. The financial plan

prepared by the management accounting system help the company to reduce the cost

of the activity and increase the revenue generated from the activity. In this way

Company can achieve the objective of the profit maximization because the differences

between the cost and revenue present the profit of the company.

Analysis of the financial statements: Management accounting also analyze the

different financial statements prepared by the organisations such as income statements,

profit and loss statement, Balance Sheet etc. The analysis of the income statement

helps the .management accounting to calculate the value of the shares in the capital

market (Lapsley and Rekers, 2017, p.175). Management accounting also suggest the

price of the shares to the organisations to attract more investments from the capital

market. Management accountant analyze the profit and loss statements to get some

detail information about the expenditure and revenue of the company. Management

accountant analyze the balance sheet to provide detail information about the assets

and liabilities acquired by the organisation to the investors. Therefore, the investors can

get some clear perception about the redemption ability of the organisation by sale the

assets of the organisation.

Cost accounting: Management accountant also calculate the cost associated with the

different business activities in the organisations based on the product, process,

department and branch etc of the organisation. Management accountant also compare

the cost information with the budgeted cost this comparison provide a detail information

8

LO2: Application of the Management accounting techniques

P3: Preparation of the income statement by using the marginal and absorption costs

Management accounting system is using different types of techniques to manage the

performance of the activities of the organisation efficiently. The techniques of

management accounting system are as follows:

Financial planning: Maximize the profit of the company is one of the major objectives

of the management accounting system. Management accounting system prepares

some appropriate plan to manage the activities of the organisation. The financial plan

prepared by the management accounting system help the company to reduce the cost

of the activity and increase the revenue generated from the activity. In this way

Company can achieve the objective of the profit maximization because the differences

between the cost and revenue present the profit of the company.

Analysis of the financial statements: Management accounting also analyze the

different financial statements prepared by the organisations such as income statements,

profit and loss statement, Balance Sheet etc. The analysis of the income statement

helps the .management accounting to calculate the value of the shares in the capital

market (Lapsley and Rekers, 2017, p.175). Management accounting also suggest the

price of the shares to the organisations to attract more investments from the capital

market. Management accountant analyze the profit and loss statements to get some

detail information about the expenditure and revenue of the company. Management

accountant analyze the balance sheet to provide detail information about the assets

and liabilities acquired by the organisation to the investors. Therefore, the investors can

get some clear perception about the redemption ability of the organisation by sale the

assets of the organisation.

Cost accounting: Management accountant also calculate the cost associated with the

different business activities in the organisations based on the product, process,

department and branch etc of the organisation. Management accountant also compare

the cost information with the budgeted cost this comparison provide a detail information

8

about the performance of the activity. While the cost of the activity is higher than the

estimated cost then the management accountant tries to identify which aspects of the

activities consume more cost than the expected and try to solve the problem of the

particular aspects to control the cost (Hill et al. 2014, p.105).

Fund and cash flow analysis: Management accountant also follow the techniques of

analyzing the flow of fund and cash in the organisation. The analysis of the flow of fund

and cash in the organisation help to determine the aspects in which organisation

expense the fund and cash. Organisation can get a clear perception about the source

generation of the cash and fund in the organisation and the aspects in which

organisation expense the funds and cash.

Standard costing: Standard costing help to compare the estimated cost with the actual

cost of the business activities. The adoption of this technique by the management

accountant helps to determine the actual performance of the activity.

Marginal costing: The adoption of marginal costing by the management accountant of

the company help to determine the prices of the products determine the sales mix for

the products and help to use raw materials and other resources in the business activity

optimistically. The technique of marginal costing also help to take some relevant

decisions about the buy or make decision, expansion of the market in the other regions

or import and export decisions.

Budgetary control: Management accountant also follow the budgetary control

technique to prepare the estimated cost and revenue for the business activities of the

company. The company tries to expense the resources according to the budget and

generate revenues from the business activities according to the budget. While, business

activities cannot perform according to the budget prepared by the company than the

management accountant try to identify the issues for which activity does not perform

according to the budget and try to create some solution control the budget ( Noordin, R.,

2016, p. 365).

Revaluation Accounting: In this this technique management accountant helps the

organisation by evaluating the value of assets acquired by the company. The

continuous use of this technique provides a clear perception about the value of the

assets of the company to the investors.

9

estimated cost then the management accountant tries to identify which aspects of the

activities consume more cost than the expected and try to solve the problem of the

particular aspects to control the cost (Hill et al. 2014, p.105).

Fund and cash flow analysis: Management accountant also follow the techniques of

analyzing the flow of fund and cash in the organisation. The analysis of the flow of fund

and cash in the organisation help to determine the aspects in which organisation

expense the fund and cash. Organisation can get a clear perception about the source

generation of the cash and fund in the organisation and the aspects in which

organisation expense the funds and cash.

Standard costing: Standard costing help to compare the estimated cost with the actual

cost of the business activities. The adoption of this technique by the management

accountant helps to determine the actual performance of the activity.

Marginal costing: The adoption of marginal costing by the management accountant of

the company help to determine the prices of the products determine the sales mix for

the products and help to use raw materials and other resources in the business activity

optimistically. The technique of marginal costing also help to take some relevant

decisions about the buy or make decision, expansion of the market in the other regions

or import and export decisions.

Budgetary control: Management accountant also follow the budgetary control

technique to prepare the estimated cost and revenue for the business activities of the

company. The company tries to expense the resources according to the budget and

generate revenues from the business activities according to the budget. While, business

activities cannot perform according to the budget prepared by the company than the

management accountant try to identify the issues for which activity does not perform

according to the budget and try to create some solution control the budget ( Noordin, R.,

2016, p. 365).

Revaluation Accounting: In this this technique management accountant helps the

organisation by evaluating the value of assets acquired by the company. The

continuous use of this technique provides a clear perception about the value of the

assets of the company to the investors.

9

Decision making accounting: Use of these techniques by the management

accountant help the organisation to take some effective decisions about the different

business activities of the organisation. Company can choose a profitable business

activity from the alternative business activities (DRURY, 2013, p.210).

Management Information system: The technique of management information system

help the management accountant to store the relevant information associated with the

business activities of the organisation. Such information helps the management

accountant to prepare some budgets for doing such similar activities (Strumickas and

Valanciene, 2015, p. 263).

Apart from the above techniques management accountant use some other techniques

such as statistical techniques, management reporting, historical cost accounting and

ratio analysis to take some effective decisions about the business activities and use

some effective measures to improve the performance of such activities.

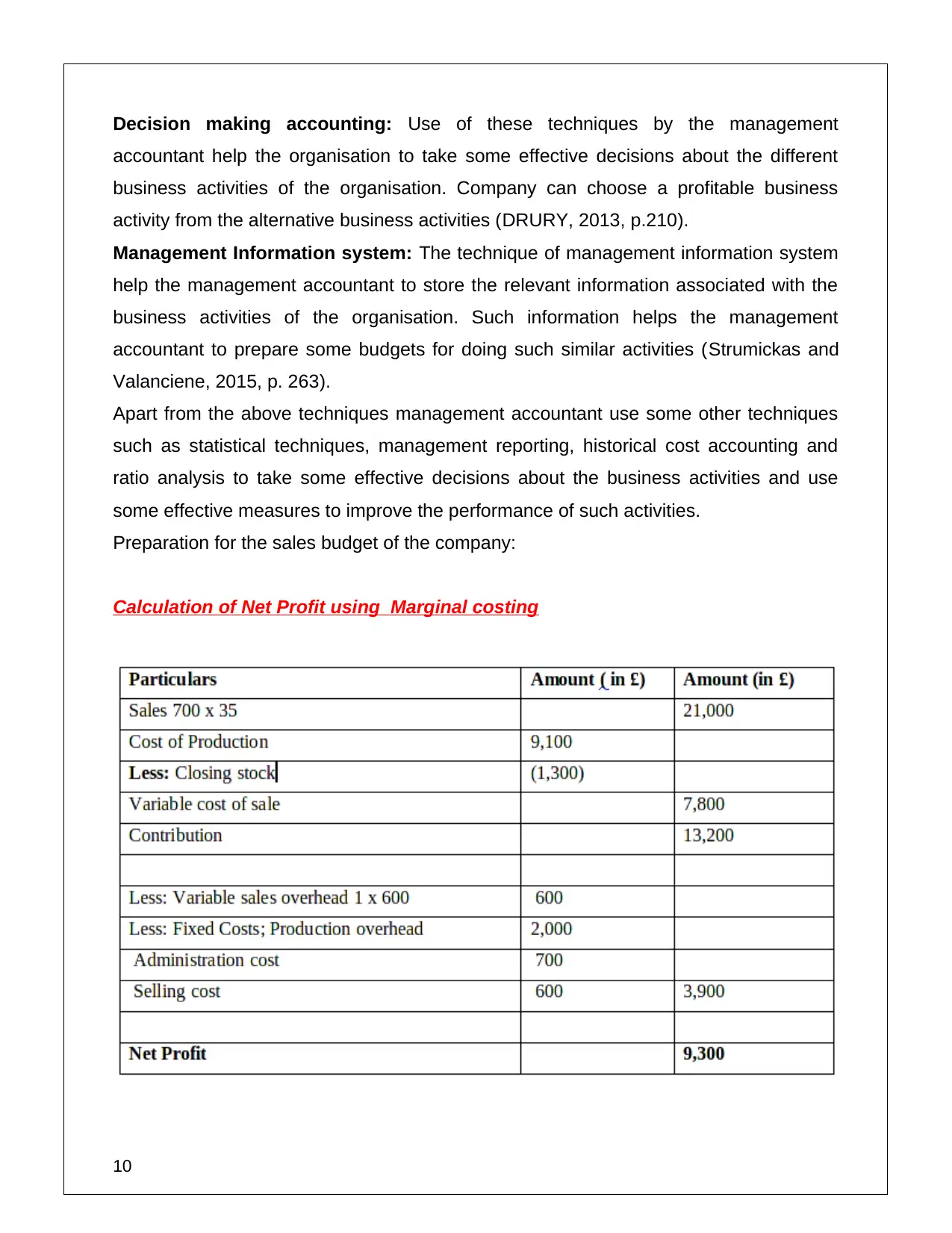

Preparation for the sales budget of the company:

Calculation of Net Profit using Marginal costing

10

accountant help the organisation to take some effective decisions about the different

business activities of the organisation. Company can choose a profitable business

activity from the alternative business activities (DRURY, 2013, p.210).

Management Information system: The technique of management information system

help the management accountant to store the relevant information associated with the

business activities of the organisation. Such information helps the management

accountant to prepare some budgets for doing such similar activities (Strumickas and

Valanciene, 2015, p. 263).

Apart from the above techniques management accountant use some other techniques

such as statistical techniques, management reporting, historical cost accounting and

ratio analysis to take some effective decisions about the business activities and use

some effective measures to improve the performance of such activities.

Preparation for the sales budget of the company:

Calculation of Net Profit using Marginal costing

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

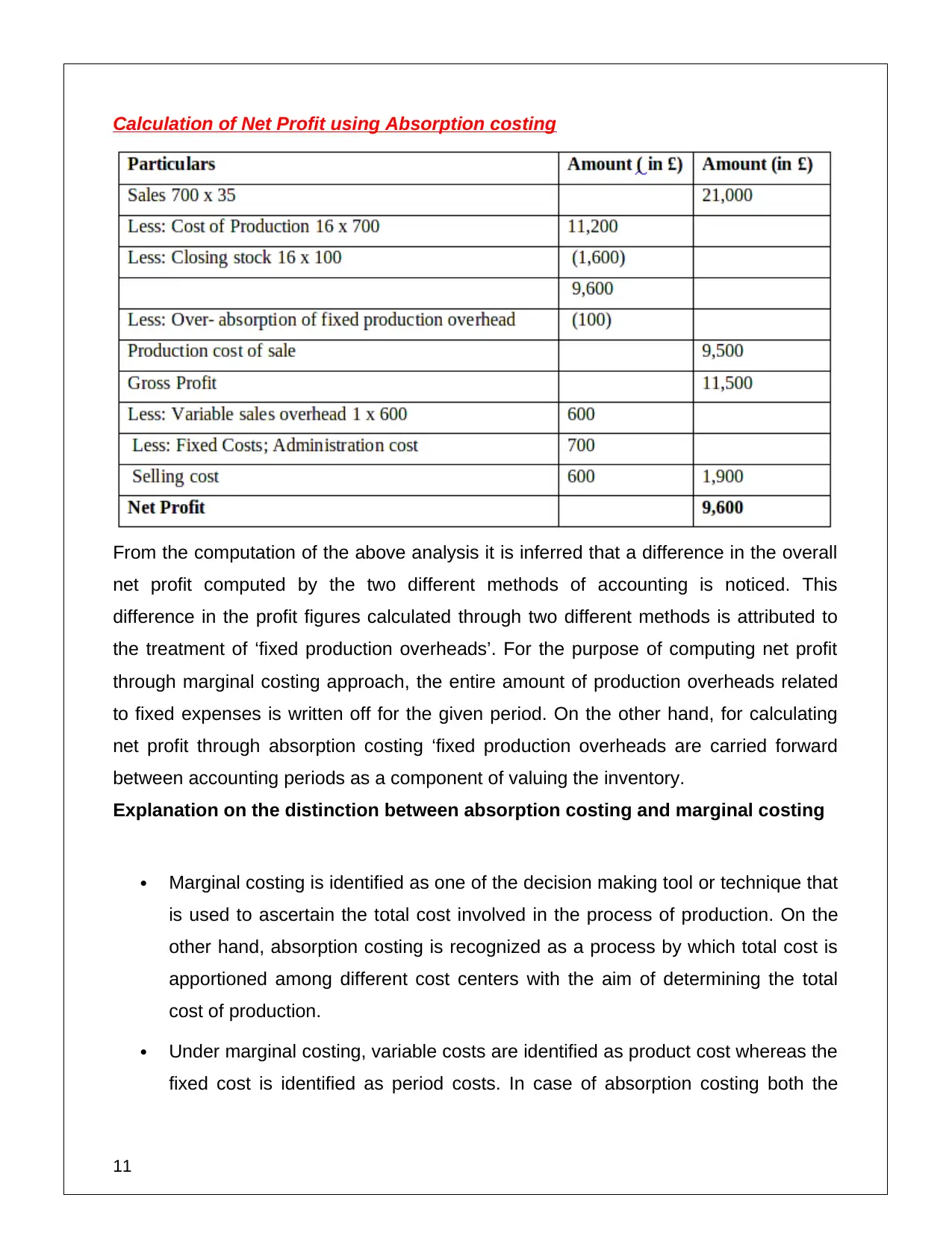

Calculation of Net Profit using Absorption costing

From the computation of the above analysis it is inferred that a difference in the overall

net profit computed by the two different methods of accounting is noticed. This

difference in the profit figures calculated through two different methods is attributed to

the treatment of ‘fixed production overheads’. For the purpose of computing net profit

through marginal costing approach, the entire amount of production overheads related

to fixed expenses is written off for the given period. On the other hand, for calculating

net profit through absorption costing ‘fixed production overheads are carried forward

between accounting periods as a component of valuing the inventory.

Explanation on the distinction between absorption costing and marginal costing

Marginal costing is identified as one of the decision making tool or technique that

is used to ascertain the total cost involved in the process of production. On the

other hand, absorption costing is recognized as a process by which total cost is

apportioned among different cost centers with the aim of determining the total

cost of production.

Under marginal costing, variable costs are identified as product cost whereas the

fixed cost is identified as period costs. In case of absorption costing both the

11

From the computation of the above analysis it is inferred that a difference in the overall

net profit computed by the two different methods of accounting is noticed. This

difference in the profit figures calculated through two different methods is attributed to

the treatment of ‘fixed production overheads’. For the purpose of computing net profit

through marginal costing approach, the entire amount of production overheads related

to fixed expenses is written off for the given period. On the other hand, for calculating

net profit through absorption costing ‘fixed production overheads are carried forward

between accounting periods as a component of valuing the inventory.

Explanation on the distinction between absorption costing and marginal costing

Marginal costing is identified as one of the decision making tool or technique that

is used to ascertain the total cost involved in the process of production. On the

other hand, absorption costing is recognized as a process by which total cost is

apportioned among different cost centers with the aim of determining the total

cost of production.

Under marginal costing, variable costs are identified as product cost whereas the

fixed cost is identified as period costs. In case of absorption costing both the

11

costs namely, fixed and variable costs are identified as product cost (DRURY,

2013, p.210)..

In marginal costing, the overheads are classified into fixed overheads and

variable overheads. In the case of absorption costing, overheads are classified in

the form of production overhead, administration overhead, selling and distribution

overhead.

In context to marginal costing, it is observed that any kind of variation in the

opening stock and closing stock does not create any impact on per unit cost of

the output. Whereas in the case of absorption costing, it is observed that

variation in the opening stock or closing stock results in affecting per unit cost of

the output.

In marginal costing contribution per unit is derived whereas in the case of

absorption costing net profit per unit is derived (Lapsley and Rekers, 2017,

p.328).

Calculation of marginal cost is considered to be part of modern management

accounting techniques whereas the computation of absorption costing is

considered to be a part of traditional management accounting techniques.

12

2013, p.210)..

In marginal costing, the overheads are classified into fixed overheads and

variable overheads. In the case of absorption costing, overheads are classified in

the form of production overhead, administration overhead, selling and distribution

overhead.

In context to marginal costing, it is observed that any kind of variation in the

opening stock and closing stock does not create any impact on per unit cost of

the output. Whereas in the case of absorption costing, it is observed that

variation in the opening stock or closing stock results in affecting per unit cost of

the output.

In marginal costing contribution per unit is derived whereas in the case of

absorption costing net profit per unit is derived (Lapsley and Rekers, 2017,

p.328).

Calculation of marginal cost is considered to be part of modern management

accounting techniques whereas the computation of absorption costing is

considered to be a part of traditional management accounting techniques.

12

Task 3

LO3: Use of different planning tools in the management accounting

system

P4: Explanation of the advantages and disadvantages of using the different types of

planning tools used for budgetary control

Budgetary control is an important tool in the management accounting system.

Management accountant can estimate the cost of the activities by preparing such

budgets. The other advantages of the budgetary control are as follows:

A) The major advantage of the budgetary control is it helps the organisation to establish

a relationship of the business activities with other departments of the organisation.

B) Budget helps the organisation to implement the strategic plan in the business activity

to manage the use of resources and revenues in the activities according to the

strategies (Strumickas and Valanciene, 2015, p. 279).

C) Budget provides some important information about the past experiences of the

business activities. Company try to avoid the past mistakes in the present business

activity and implement the effective measures learn from the past to increase the

effectiveness of the activity.

D) Budget also help the organisation to communicate with the employees to provide

information about the use of resources in the activity. Budget also provides some

guidelines to the employees for using the machineries and raw material efficiently in the

production activity.

E) Budget also improves the resources allocation ability of the organisation by providing

important information about the requirements of the resources in the activity (Hill et al.

2014, p.111).

F) Budget also provides a scope to the organisation for correcting the mistakes in the

activity by providing the reallocation tool.

13

LO3: Use of different planning tools in the management accounting

system

P4: Explanation of the advantages and disadvantages of using the different types of

planning tools used for budgetary control

Budgetary control is an important tool in the management accounting system.

Management accountant can estimate the cost of the activities by preparing such

budgets. The other advantages of the budgetary control are as follows:

A) The major advantage of the budgetary control is it helps the organisation to establish

a relationship of the business activities with other departments of the organisation.

B) Budget helps the organisation to implement the strategic plan in the business activity

to manage the use of resources and revenues in the activities according to the

strategies (Strumickas and Valanciene, 2015, p. 279).

C) Budget provides some important information about the past experiences of the

business activities. Company try to avoid the past mistakes in the present business

activity and implement the effective measures learn from the past to increase the

effectiveness of the activity.

D) Budget also help the organisation to communicate with the employees to provide

information about the use of resources in the activity. Budget also provides some

guidelines to the employees for using the machineries and raw material efficiently in the

production activity.

E) Budget also improves the resources allocation ability of the organisation by providing

important information about the requirements of the resources in the activity (Hill et al.

2014, p.111).

F) Budget also provides a scope to the organisation for correcting the mistakes in the

activity by providing the reallocation tool.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Apart from all the advantages company also face some issues while using the budget in

the business activity. The issues create some disadvantages for the use of the budget

in the organisation. The disadvantages of the budgets are as follows:

A) The problem raise while the company apply the budget practically and mechanically

in the business activities.

B) The budget discourages the employees to work in the business activities because

the lack of participation of the employees while preparing the budget. Budget can

provide some unconditional pressure on the employees.

C) While budgets prepare with the high expectation of the company and the budget

have no relation with the reality for this reason the quality of the products of the

company can be fall.

D) Budget can create some competition for resources among the different activities of

the organisation.

E) Budget reduce the scope of creativity and innovation in the activity and the

employees are not motivated to apply their creativity to complete the activity.

The overall impact of budget on the organisation is positive. Therefore, the organisation

can use the budget to complete the activities with cost efficiencies (Contrafatto and

Burns, 2013, p.359).

LO4: The process that should be followed by organisations to use the

management accounting system to respond the financial

problems

P5: The process that should be followed by the organisation to adapt management

accounting system to resolve the financial problems

The adaption of management accounting system in the organisational activities helps

the organisations to manage the activities with efficiency. Management accountant not

only determine the problems of the activity but also create some solutions to solve such

problems of the activity. Management accountant use different resources, techniques

and tools to create the transparency in the performance of the activities that help the

14

the business activity. The issues create some disadvantages for the use of the budget

in the organisation. The disadvantages of the budgets are as follows:

A) The problem raise while the company apply the budget practically and mechanically

in the business activities.

B) The budget discourages the employees to work in the business activities because

the lack of participation of the employees while preparing the budget. Budget can

provide some unconditional pressure on the employees.

C) While budgets prepare with the high expectation of the company and the budget

have no relation with the reality for this reason the quality of the products of the

company can be fall.

D) Budget can create some competition for resources among the different activities of

the organisation.

E) Budget reduce the scope of creativity and innovation in the activity and the

employees are not motivated to apply their creativity to complete the activity.

The overall impact of budget on the organisation is positive. Therefore, the organisation

can use the budget to complete the activities with cost efficiencies (Contrafatto and

Burns, 2013, p.359).

LO4: The process that should be followed by organisations to use the

management accounting system to respond the financial

problems

P5: The process that should be followed by the organisation to adapt management

accounting system to resolve the financial problems

The adaption of management accounting system in the organisational activities helps

the organisations to manage the activities with efficiency. Management accountant not

only determine the problems of the activity but also create some solutions to solve such

problems of the activity. Management accountant use different resources, techniques

and tools to create the transparency in the performance of the activities that help the

14

organisation to evaluate the performance of the activities. To adapt the management

accounting system in the organisational culture the company has to take some effective

measures. Company has to provide full authorization to the management accountant to

access the financial information of the company. Therefore, Company have to provide

all financial statements to the management accountant that the management

accountant to determine the financial problem of the organisation. After analyzing the

financial statements management accountant can provide a brief knowledge about the

financial problem of the organisations and create some effective solutions to solve such

problems. Management accountant also can access the information about the

performance of the past activities of the organisation to prepare an efficient budget for

the future activities of the organisation. The analysis of the performance of the past

activities also helps the management accountant to determine source of financial

problems in the organisation. As the differences between the cost and revenues

represent the profit of the company for this reason the management accountant use

budgetary control to reduce and control the cost of production and increase the profit of

the company. Management accountant also prepare the standard costing to measure

the actual performance of the activities done by the organisation. In the standard

costing measure the performance of the activity based cost of the activities. If the

activity consumes higher cost than the estimated then there are some problems with the

performance of the activity. Management accountant try to determine the problems of

the activity and create some solution to increase the performance of the activity by

solving such problems. In this way the companies have to provide all financial

information to the management accountant to adapt a string management accounting

system to solve the financial problem of the company (Christ and Burritt, 2013, p.168).

Key performance indicators- By considering the KPIs management able to

analyse easily that company is performing in which trend like increasing or

decreasing. When it derives that performance of the entity reducing consistently

then take corrective actions in against to that. Different KPIs which used to

measure performance and provide response are like cost, quality, net profit,

earned value, variance, sales and revenue etc. When such all the criterias

15

accounting system in the organisational culture the company has to take some effective

measures. Company has to provide full authorization to the management accountant to

access the financial information of the company. Therefore, Company have to provide

all financial statements to the management accountant that the management

accountant to determine the financial problem of the organisation. After analyzing the

financial statements management accountant can provide a brief knowledge about the

financial problem of the organisations and create some effective solutions to solve such

problems. Management accountant also can access the information about the

performance of the past activities of the organisation to prepare an efficient budget for

the future activities of the organisation. The analysis of the performance of the past

activities also helps the management accountant to determine source of financial

problems in the organisation. As the differences between the cost and revenues

represent the profit of the company for this reason the management accountant use

budgetary control to reduce and control the cost of production and increase the profit of

the company. Management accountant also prepare the standard costing to measure

the actual performance of the activities done by the organisation. In the standard

costing measure the performance of the activity based cost of the activities. If the

activity consumes higher cost than the estimated then there are some problems with the

performance of the activity. Management accountant try to determine the problems of

the activity and create some solution to increase the performance of the activity by

solving such problems. In this way the companies have to provide all financial

information to the management accountant to adapt a string management accounting

system to solve the financial problem of the company (Christ and Burritt, 2013, p.168).

Key performance indicators- By considering the KPIs management able to

analyse easily that company is performing in which trend like increasing or

decreasing. When it derives that performance of the entity reducing consistently

then take corrective actions in against to that. Different KPIs which used to

measure performance and provide response are like cost, quality, net profit,

earned value, variance, sales and revenue etc. When such all the criterias

15

having negative and unfavorable change year by year then it will prepare

beneficial and appropriate strategies.

Bench marking- This kind of system of management accounting supports in

terms of making specific target as well as achieve it. There are several standards

and benchmarks available and after following them chances to reduce financial

performance can be resolve up to the better level. In opposite to that, if company

not prepares benchmarks and meet them then cannot perform better and well

within whole industry. For example, if it makes benchmark for net profit that in

next year necessary to improve by 10% then able to resolve such kind of

constraints. Moreover, for the liquidity position like current ratio industry set

standards value which is 2:1. Here if entity meet and excess by ideal ratio then

there is no chance to incur financial problems.

Financial governance- Corporate governance of the business organisation is

divided in small parts which take care of various aspects. In order to assess the

financial aspect, financial governance take care that company properly records

all the transactions in books of account or not. Furthermore, it analyses that

management meeting to the benchmarks and agreed financial objectives in

appropriate ways or not. Hence, it can be said that financial governance is one of

the highly better kind of management accounting system in order to assessing

performance and resolving financial problems from the workplace.

Budgetary targets- In the budgeting process targets are determined by the

company after preparing budget for the upcoming accounting period. On the

basis of this management able to measure business performance by comparing

actual and budgetary targets which called as variance analysis. Through this, if

firm founds that business performance is in unfavorable condition then make

effectual strategies and tactics to achieve budgeted data.

16

beneficial and appropriate strategies.

Bench marking- This kind of system of management accounting supports in

terms of making specific target as well as achieve it. There are several standards

and benchmarks available and after following them chances to reduce financial

performance can be resolve up to the better level. In opposite to that, if company

not prepares benchmarks and meet them then cannot perform better and well

within whole industry. For example, if it makes benchmark for net profit that in

next year necessary to improve by 10% then able to resolve such kind of

constraints. Moreover, for the liquidity position like current ratio industry set

standards value which is 2:1. Here if entity meet and excess by ideal ratio then

there is no chance to incur financial problems.

Financial governance- Corporate governance of the business organisation is

divided in small parts which take care of various aspects. In order to assess the

financial aspect, financial governance take care that company properly records

all the transactions in books of account or not. Furthermore, it analyses that

management meeting to the benchmarks and agreed financial objectives in

appropriate ways or not. Hence, it can be said that financial governance is one of

the highly better kind of management accounting system in order to assessing

performance and resolving financial problems from the workplace.

Budgetary targets- In the budgeting process targets are determined by the

company after preparing budget for the upcoming accounting period. On the

basis of this management able to measure business performance by comparing

actual and budgetary targets which called as variance analysis. Through this, if

firm founds that business performance is in unfavorable condition then make

effectual strategies and tactics to achieve budgeted data.

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Conclusion

Business organisations can adapt the management accounting system to improve the

financial status in the industry. The above study tries to provide a brief knowledge to the

organisations about the advantages and disadvantages of the management accounting

system in the organisation. The implementation of the management accounting system

in the business activities of the organisation also mentioned in the above study. The

modern business organisations also recognize the essentiality of the management

accounting system to improve the cost efficiency of the business activities.

Bibliography

Ax, C. and Greve, J., 2017. Adoption of management accounting

innovations: Organizational culture compatibility and perceived

outcomes. Management Accounting Research, 34, pp.59-74.

Butterworth, S., Subramaniam, N. and Phang, M.M., 2015. Carbon Risk

Management: A Comparative Case Study of Two Companies within the

Australian Energy Sector. Journal of Applied Management Accounting

Research, 13(1), p.9.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution

of management accounting and its integration into management

control. Accounting, Organizations and Society, 47, pp.1-13.

Christ, K.L. and Burritt, R.L., 2013. Environmental management accounting:

the significance of contingent variables for adoption. Journal of Cleaner

Production, 41, pp.163-173.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting,

organisational change and management accounting: A processual

view. Management Accounting Research, 24(4), pp.349-365.

Cooper, D.J., Ezzamel, M. and Qu, S.Q., 2017. Popularizing a

management accounting idea: The case of the balanced

17

Business organisations can adapt the management accounting system to improve the

financial status in the industry. The above study tries to provide a brief knowledge to the

organisations about the advantages and disadvantages of the management accounting

system in the organisation. The implementation of the management accounting system

in the business activities of the organisation also mentioned in the above study. The

modern business organisations also recognize the essentiality of the management

accounting system to improve the cost efficiency of the business activities.

Bibliography

Ax, C. and Greve, J., 2017. Adoption of management accounting

innovations: Organizational culture compatibility and perceived

outcomes. Management Accounting Research, 34, pp.59-74.

Butterworth, S., Subramaniam, N. and Phang, M.M., 2015. Carbon Risk

Management: A Comparative Case Study of Two Companies within the

Australian Energy Sector. Journal of Applied Management Accounting

Research, 13(1), p.9.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution

of management accounting and its integration into management

control. Accounting, Organizations and Society, 47, pp.1-13.

Christ, K.L. and Burritt, R.L., 2013. Environmental management accounting:

the significance of contingent variables for adoption. Journal of Cleaner

Production, 41, pp.163-173.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting,

organisational change and management accounting: A processual

view. Management Accounting Research, 24(4), pp.349-365.

Cooper, D.J., Ezzamel, M. and Qu, S.Q., 2017. Popularizing a

management accounting idea: The case of the balanced

17

scorecard. Contemporary Accounting Research.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean

manufacturing and firm performance: The incremental contribution of lean

management accounting practices. Journal of Operations

Management, 32(7), pp.414-428.

Hasan, M.S. and Omar, N., 2016. How do we assess the quality of

corporate financial reporting?: A methodological issue. Aestimatio, (13),

p.2.

Hill, C.W., Jones, G.R. and Schilling, M.A., 2014. Strategic management:

theory: an integrated approach. Cengage Learning.

Lapsley, I. and Rekers, J.V., 2017. The relevance of strategic management

accounting to popular culture: The world of West End

Musicals. Management Accounting Research.

Noordin, R., 2016. Strategic management accounting information elements:

Malaysian evidence. Asia-Pacific Management Accounting Journal, 4(1).

Northcott, D., 2014. Ten years of Qualitative Research in Accounting &

Management: celebrations and reflections. Qualitative Research in

Accounting & Management, 11(1).

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for

management control. Springer.

Otley, D., 2016. The contingency theory of management accounting and

control: 1980–2014. Management accounting research, 31, pp.45-62.

Strumickas, M. and Valanciene, L., 2015. Research of management

accounting changes in Lithuanian business organizations. Engineering

Economics, 63(4).

Van der Stede, W.A., 2016. Management accounting in context: Industry,

regulation and informatics. Management Accounting Research, 31, pp.100-

102.

Wagenhofer, A., 2016. Exploiting regulatory changes for research in

management accounting. Management Accounting Research, 31, pp.112-

18

DRURY, C.M., 2013. Management and cost accounting. Springer.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean

manufacturing and firm performance: The incremental contribution of lean

management accounting practices. Journal of Operations

Management, 32(7), pp.414-428.

Hasan, M.S. and Omar, N., 2016. How do we assess the quality of

corporate financial reporting?: A methodological issue. Aestimatio, (13),

p.2.

Hill, C.W., Jones, G.R. and Schilling, M.A., 2014. Strategic management:

theory: an integrated approach. Cengage Learning.

Lapsley, I. and Rekers, J.V., 2017. The relevance of strategic management

accounting to popular culture: The world of West End

Musicals. Management Accounting Research.

Noordin, R., 2016. Strategic management accounting information elements:

Malaysian evidence. Asia-Pacific Management Accounting Journal, 4(1).

Northcott, D., 2014. Ten years of Qualitative Research in Accounting &

Management: celebrations and reflections. Qualitative Research in

Accounting & Management, 11(1).

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for

management control. Springer.

Otley, D., 2016. The contingency theory of management accounting and

control: 1980–2014. Management accounting research, 31, pp.45-62.

Strumickas, M. and Valanciene, L., 2015. Research of management

accounting changes in Lithuanian business organizations. Engineering

Economics, 63(4).

Van der Stede, W.A., 2016. Management accounting in context: Industry,

regulation and informatics. Management Accounting Research, 31, pp.100-

102.

Wagenhofer, A., 2016. Exploiting regulatory changes for research in

management accounting. Management Accounting Research, 31, pp.112-

18

117.

19

19

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.