Accounting Homework: Impairment Analysis and Journal Entries

VerifiedAdded on 2020/02/23

|8

|1343

|238

Homework Assignment

AI Summary

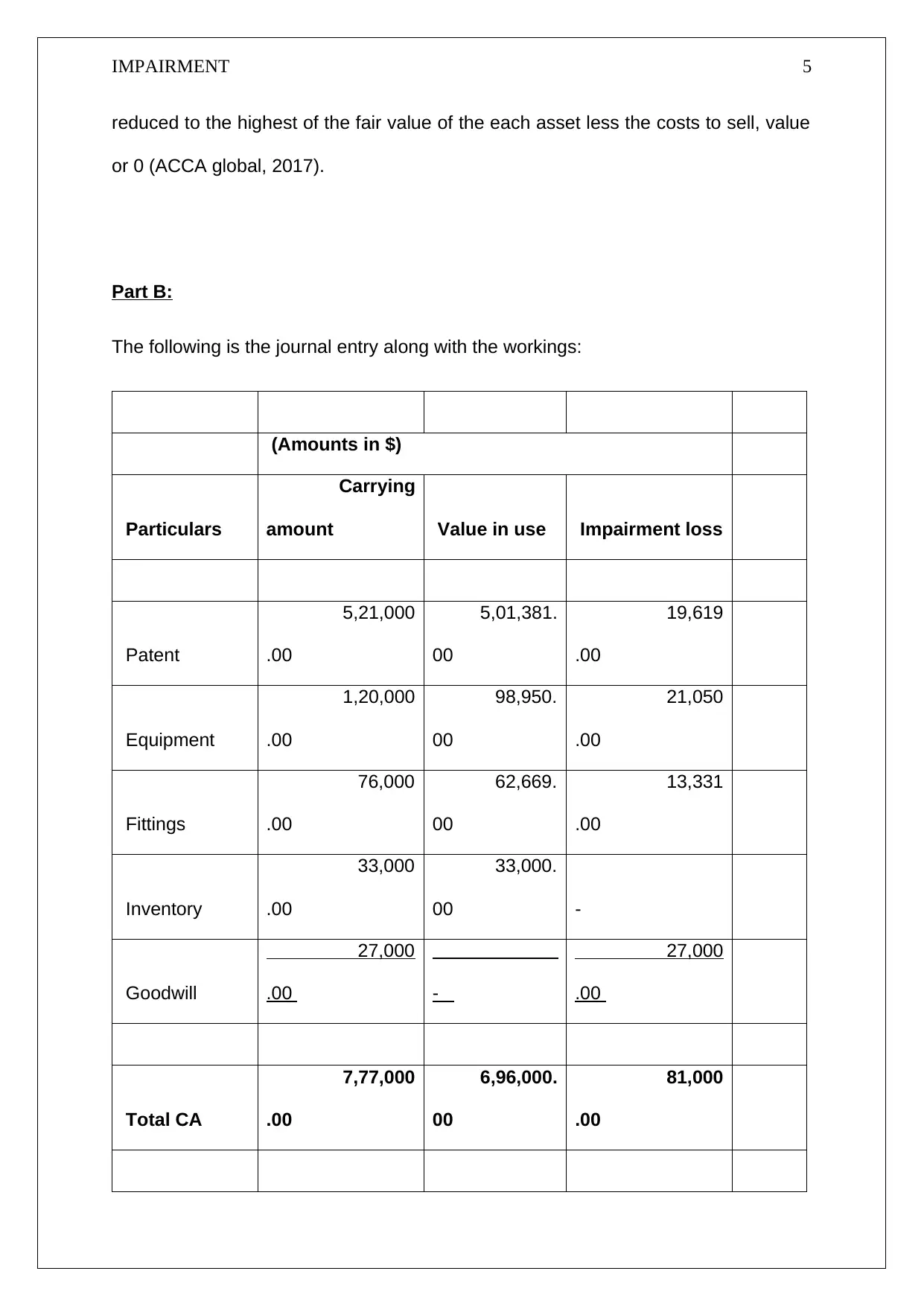

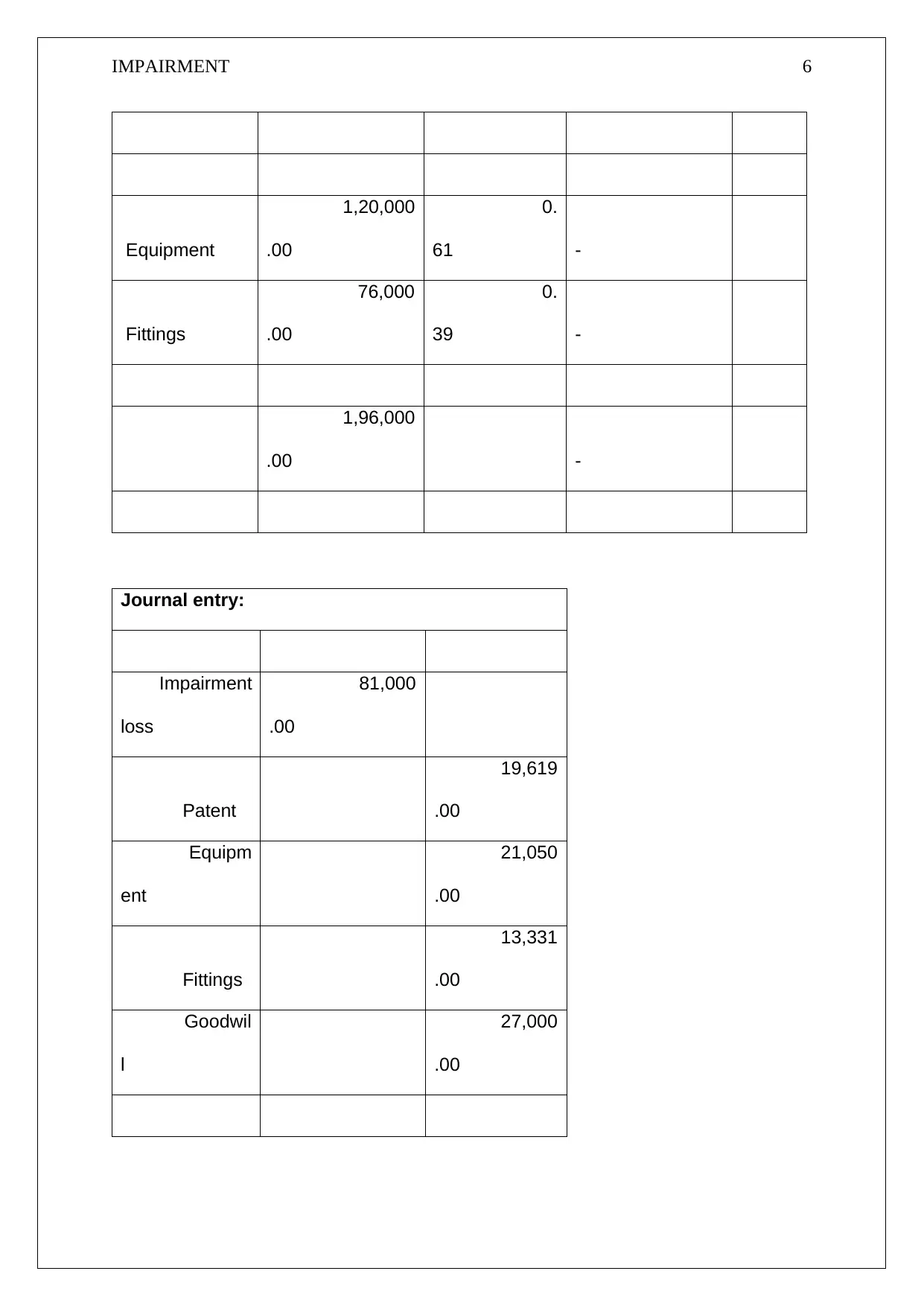

This homework assignment delves into the core principles of impairment analysis within financial accounting, focusing on the concept that assets should not be reported above their recoverable amount. The solution outlines the process of comparing carrying values with recoverable amounts, which is the higher of fair value less costs to sell and value in use, to identify impairment losses. It addresses the testing of various assets, including goodwill and intangible assets, and explains the concept of cash-generating units. The assignment provides a detailed journal entry to account for an impairment loss, including specific calculations for patents, equipment, fittings, inventory, and goodwill. The document references relevant accounting standards, such as IAS 36, and includes a breakdown of the impairment loss allocation across different asset types. This solution offers a comprehensive understanding of the practical application of impairment accounting principles.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.