Study of GST and Capital Gain Tax Cases

VerifiedAdded on 2022/12/27

|9

|2854

|35

AI Summary

This assignment deals with the study of the two given cases which are related to two distinct taxes of Australia. The brief study of both the taxes is been carried out for answering both the questions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ASSIGNMENT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Introduction........................................................................................................................3

Answer 1............................................................................................................................3

GST................................................................................................................................3

Introduction to GST........................................................................................................3

Reference of Case given in question.............................................................................3

Introduction to Reverse Charge Mechanism..................................................................3

Case Solution.................................................................................................................4

Introduction of Input Tax Credit......................................................................................4

Input Tax Credit in the context of Case..........................................................................4

Conclusion of the case...................................................................................................5

Answer 2............................................................................................................................5

Introduction of the Capital Gain Tax...............................................................................5

Capital Losses................................................................................................................5

Tax Payment..................................................................................................................5

Tax on Sell of shares......................................................................................................6

Cost inclusions...............................................................................................................6

Collectibles.....................................................................................................................6

Study of the Given Case................................................................................................6

Share Sale......................................................................................................................8

Stamp collection purchase by Emma from a Private collector.......................................8

Year 2015....................................................................................................................8

Sale of Grand piano....................................................................................................8

References.........................................................................................................................8

2

Introduction........................................................................................................................3

Answer 1............................................................................................................................3

GST................................................................................................................................3

Introduction to GST........................................................................................................3

Reference of Case given in question.............................................................................3

Introduction to Reverse Charge Mechanism..................................................................3

Case Solution.................................................................................................................4

Introduction of Input Tax Credit......................................................................................4

Input Tax Credit in the context of Case..........................................................................4

Conclusion of the case...................................................................................................5

Answer 2............................................................................................................................5

Introduction of the Capital Gain Tax...............................................................................5

Capital Losses................................................................................................................5

Tax Payment..................................................................................................................5

Tax on Sell of shares......................................................................................................6

Cost inclusions...............................................................................................................6

Collectibles.....................................................................................................................6

Study of the Given Case................................................................................................6

Share Sale......................................................................................................................8

Stamp collection purchase by Emma from a Private collector.......................................8

Year 2015....................................................................................................................8

Sale of Grand piano....................................................................................................8

References.........................................................................................................................8

2

Introduction

This assignment deals with the study of the two given cases which are related to two

distinct taxes of Australia. The brief study of both the taxes is been carried out for

answering both the questions. All the cases are been solved with the context of these

laws and the study is been given below.

Answer 1

GST

Introduction to GST

The first case is been given related to the goods and service tax. This tax is also known

as value-added tax. This name is given to this tax as it adds on the value to the goods.

The value of the commodity increases at each at every level that is the value is added

at every chain of supply and reaches the final customer with the last value addition. The

tax GST is the tax which is the destination-based tax. This is a consumption tax on

which tax is to be paid by the actual consumer the theory on which this tax is based on

is that the tax pain should be borne by the consumer or the last person using it. There

are a number of persons involved in the transaction. This is the pain which was to be

borne by the consumer and the person who is the actual bearer would be giving the tax

and the rest of the people who will be paying the tax will get the credit back out of it.

All the firms who are eligible to get registered under the GST shall get registered under

the law as well as the persons and firms which voluntarily want to register can also get

registered with the tax law. All the persons who get registered should follow all the

provisions and rules and should work in accordance with that only. (Anon., n.d.)

Reference of Case given in the question

The case given in the question says that the company has taken the services of the

Lawyer and that are used for the business purpose and for the received services they

have to pay a fee to the lawyer. This transaction will attract GST and will be paid in the

way discussed below.

Introduction to Reverse Charge Mechanism

This is a scheme specified in the GST law and this scheme has a list of several services

on which the tax is to be paid by the person or entity that is paying the charges for the

services they have received. There are a number of services specified in this list and

hence these are the services where tax is to be paid by the entity which is registered

under the law. (Anon., n.d.)

3

This assignment deals with the study of the two given cases which are related to two

distinct taxes of Australia. The brief study of both the taxes is been carried out for

answering both the questions. All the cases are been solved with the context of these

laws and the study is been given below.

Answer 1

GST

Introduction to GST

The first case is been given related to the goods and service tax. This tax is also known

as value-added tax. This name is given to this tax as it adds on the value to the goods.

The value of the commodity increases at each at every level that is the value is added

at every chain of supply and reaches the final customer with the last value addition. The

tax GST is the tax which is the destination-based tax. This is a consumption tax on

which tax is to be paid by the actual consumer the theory on which this tax is based on

is that the tax pain should be borne by the consumer or the last person using it. There

are a number of persons involved in the transaction. This is the pain which was to be

borne by the consumer and the person who is the actual bearer would be giving the tax

and the rest of the people who will be paying the tax will get the credit back out of it.

All the firms who are eligible to get registered under the GST shall get registered under

the law as well as the persons and firms which voluntarily want to register can also get

registered with the tax law. All the persons who get registered should follow all the

provisions and rules and should work in accordance with that only. (Anon., n.d.)

Reference of Case given in the question

The case given in the question says that the company has taken the services of the

Lawyer and that are used for the business purpose and for the received services they

have to pay a fee to the lawyer. This transaction will attract GST and will be paid in the

way discussed below.

Introduction to Reverse Charge Mechanism

This is a scheme specified in the GST law and this scheme has a list of several services

on which the tax is to be paid by the person or entity that is paying the charges for the

services they have received. There are a number of services specified in this list and

hence these are the services where tax is to be paid by the entity which is registered

under the law. (Anon., n.d.)

3

The services of the lawyer received for the purpose of business are also included in this

list. In this case, the services are received from the lawyer for the purpose of business

and hence the Sky City Company is registered under the GST law so in this case, the

company is liable to pay tax as this is a service which is under the list of Reverse

Charge.

Further detailed analysis is carried below.

Case Solution

In this case, the services of the lawyer are taken by the Sky City Company are listed

under the reverse charge mechanism and hence the company became liable to pay the

tax.

This list is made by the Australian Tax Office because there is a number of lawyers who

provide services to many entities and they are not registered under the law so this

becomes difficult for the government to collect taxes from each one of them separately.

This is made for the convincing of the Australian government so that they can easily

collect the taxes. For this purpose the Government gives the burden of tax to the

entities which are registered under the law and they can easily collect the taxes from

them.(Anon., n.d.)

The fees of $300,000 are paid to the lawyer by the sky city company and hence the

company will pay the taxes to the government on the behalf of the lawyer and for this

the company can ask the lawyer for the reduced payments as the taxes are to be paid

on the amount of the services they have rendered to the entity.

Introduction of Input Tax Credit

Input tax credit refers to the tax credit which is given by the government to the person

who has paid GST in the whole supply chain and hence is not the actual consumer of

the goods. This credit is given to the person who has paid the tax to the government

and has not consumed the goods or the services.

These are the credit amounts that the government pays back so as to avoid the

situation of multiple taxations over one good or services. The government pays back the

tax paid in the form of credit so that the tax can be ultimately charged form the final

consumers of goods and service

Input Tax Credit in the context of Case

The company sky city pays the tax on the behalf of the lawyer and these services are

received by the company for the construction of the apartments that the company will go

to sell in the near future to the consumers. The consumer will be the final consumer of

the services received and hence they would be ultimate tax bearers of the services.

4

list. In this case, the services are received from the lawyer for the purpose of business

and hence the Sky City Company is registered under the GST law so in this case, the

company is liable to pay tax as this is a service which is under the list of Reverse

Charge.

Further detailed analysis is carried below.

Case Solution

In this case, the services of the lawyer are taken by the Sky City Company are listed

under the reverse charge mechanism and hence the company became liable to pay the

tax.

This list is made by the Australian Tax Office because there is a number of lawyers who

provide services to many entities and they are not registered under the law so this

becomes difficult for the government to collect taxes from each one of them separately.

This is made for the convincing of the Australian government so that they can easily

collect the taxes. For this purpose the Government gives the burden of tax to the

entities which are registered under the law and they can easily collect the taxes from

them.(Anon., n.d.)

The fees of $300,000 are paid to the lawyer by the sky city company and hence the

company will pay the taxes to the government on the behalf of the lawyer and for this

the company can ask the lawyer for the reduced payments as the taxes are to be paid

on the amount of the services they have rendered to the entity.

Introduction of Input Tax Credit

Input tax credit refers to the tax credit which is given by the government to the person

who has paid GST in the whole supply chain and hence is not the actual consumer of

the goods. This credit is given to the person who has paid the tax to the government

and has not consumed the goods or the services.

These are the credit amounts that the government pays back so as to avoid the

situation of multiple taxations over one good or services. The government pays back the

tax paid in the form of credit so that the tax can be ultimately charged form the final

consumers of goods and service

Input Tax Credit in the context of Case

The company sky city pays the tax on the behalf of the lawyer and these services are

received by the company for the construction of the apartments that the company will go

to sell in the near future to the consumers. The consumer will be the final consumer of

the services received and hence they would be ultimate tax bearers of the services.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

With context to the study of the Input Tax Credit, we could conclude that the company

will be eligible to get the input tax credit and hence will not the ultimate bearers of the

GST. The company is eligible to claim the credit of the taxes they have paid and will

receive the credit for these taxes they have paid. (Anon., n.d.)

Conclusion of the case

In the above case, the company is liable for the payment of tax under the scheme of

reverse charge and hence would be eligible to claim the input tax credit too. This credit

would be granted to the company as it is not the actual consumer of the services.

This is a complete conclusion and this is how we can come to know when and why the

GST has to pay.

Answer 2

Introduction of the Capital Gain Tax

Capital gain is the amount that an assessee has earned from the sale of an asset. The

gain amount can be calculated as the difference between the sale amount of the asset

and the cost of acquisition of the assets. If the amount calculated from the above

equation is negative than the amount is called as capital loss.

Capital tax is the tax which is paid on the amount of capital gain. The gain on the capital

is considered as the income of the assessee and is shown in his income statement and

hence is considered as the income while calculating the assessable income of the

assessee. This tax forms a part of the income tax and hence the calculation of this is

taken under the income tax similar to that of others. (Anon., n.d.)

The capital gain taxes are applicable only on those assets which have been acquired

after the date 20 September 1985.

There are a number of assets which does not fall under the head of capital gain taxes or

can be said that they are exempt from the capital gain taxes these are personal assets

which are used for personal uses.

Capital Losses

The losses that have occurred from the disposing of of the assets will be settled off only

from the income from the head of the capital gain only that it these losses cannot be

settled off from the income from any other source.

Tax Payment

The person who is an Australian resident is always liable to pay to the taxes on capital

gain whether they sell their asset in Australia or anywhere out of Australia. The

5

will be eligible to get the input tax credit and hence will not the ultimate bearers of the

GST. The company is eligible to claim the credit of the taxes they have paid and will

receive the credit for these taxes they have paid. (Anon., n.d.)

Conclusion of the case

In the above case, the company is liable for the payment of tax under the scheme of

reverse charge and hence would be eligible to claim the input tax credit too. This credit

would be granted to the company as it is not the actual consumer of the services.

This is a complete conclusion and this is how we can come to know when and why the

GST has to pay.

Answer 2

Introduction of the Capital Gain Tax

Capital gain is the amount that an assessee has earned from the sale of an asset. The

gain amount can be calculated as the difference between the sale amount of the asset

and the cost of acquisition of the assets. If the amount calculated from the above

equation is negative than the amount is called as capital loss.

Capital tax is the tax which is paid on the amount of capital gain. The gain on the capital

is considered as the income of the assessee and is shown in his income statement and

hence is considered as the income while calculating the assessable income of the

assessee. This tax forms a part of the income tax and hence the calculation of this is

taken under the income tax similar to that of others. (Anon., n.d.)

The capital gain taxes are applicable only on those assets which have been acquired

after the date 20 September 1985.

There are a number of assets which does not fall under the head of capital gain taxes or

can be said that they are exempt from the capital gain taxes these are personal assets

which are used for personal uses.

Capital Losses

The losses that have occurred from the disposing of of the assets will be settled off only

from the income from the head of the capital gain only that it these losses cannot be

settled off from the income from any other source.

Tax Payment

The person who is an Australian resident is always liable to pay to the taxes on capital

gain whether they sell their asset in Australia or anywhere out of Australia. The

5

government of Australia mandates it for the resident people to pay the taxes on ever to

sell off their capital asset anywhere in the world.

Tax on Sell of shares

Shares are the small units of the companies that are traded in the market. The shares

also attract the capital gain taxes if they are held with the person for the period of more

than 12 months. This tax is not applicable to the person who is solely involved in buying

and selling of shares that is the person who does the business of buying and selling of

shares.

Cost inclusions

There are a number of costs that are included in the cost of acquisition of the asset. It is

not just only the cost of purchase but the other costs which are attributable to the

purchase of the asset or the installation of the asset. The cost of an asset includes-

brokerage charges, commission directly charged for the asset, stamp duties paid, the

purchase price, transportation charges and the costs incurred for the asset to make the

asset ready to use by the organization.(Anon., n.d.)

From the date 21 August 1991, the costs that are incurred for the repairs and the

maintenance of the land and also the charges of the premium are included in the cost of

the assets.

While calculating the gain or loss from the capital asset the cost of acquisition is taken

which consider all these costs in it.

Collectibles

These are the goods which are for the personal enjoyment of any person. This is an

endless list and includes several things in it such as- paintings, artworks, the

photographs and many more.

These goods are also chargeable for the capital tax but only at the time if they have

exceeded the value of the $500. This is the initial condition that is needed to be fulfilled

so as to make this liable for the tax.(Anon., n.d.)

There are few points that should be kept in mind so that it could easily be said

that they are considered as capital gains or losses or are not considered:

Price of the collectible is less than or equal to $500

Purchase is less than $500 as in terms of market price

Before 16 December 1995,the acquired interest in any collectible $500 or less

Any losses occurred from the sale of these collectibles than they could be settled from

the income of the same head only.

6

sell off their capital asset anywhere in the world.

Tax on Sell of shares

Shares are the small units of the companies that are traded in the market. The shares

also attract the capital gain taxes if they are held with the person for the period of more

than 12 months. This tax is not applicable to the person who is solely involved in buying

and selling of shares that is the person who does the business of buying and selling of

shares.

Cost inclusions

There are a number of costs that are included in the cost of acquisition of the asset. It is

not just only the cost of purchase but the other costs which are attributable to the

purchase of the asset or the installation of the asset. The cost of an asset includes-

brokerage charges, commission directly charged for the asset, stamp duties paid, the

purchase price, transportation charges and the costs incurred for the asset to make the

asset ready to use by the organization.(Anon., n.d.)

From the date 21 August 1991, the costs that are incurred for the repairs and the

maintenance of the land and also the charges of the premium are included in the cost of

the assets.

While calculating the gain or loss from the capital asset the cost of acquisition is taken

which consider all these costs in it.

Collectibles

These are the goods which are for the personal enjoyment of any person. This is an

endless list and includes several things in it such as- paintings, artworks, the

photographs and many more.

These goods are also chargeable for the capital tax but only at the time if they have

exceeded the value of the $500. This is the initial condition that is needed to be fulfilled

so as to make this liable for the tax.(Anon., n.d.)

There are few points that should be kept in mind so that it could easily be said

that they are considered as capital gains or losses or are not considered:

Price of the collectible is less than or equal to $500

Purchase is less than $500 as in terms of market price

Before 16 December 1995,the acquired interest in any collectible $500 or less

Any losses occurred from the sale of these collectibles than they could be settled from

the income of the same head only.

6

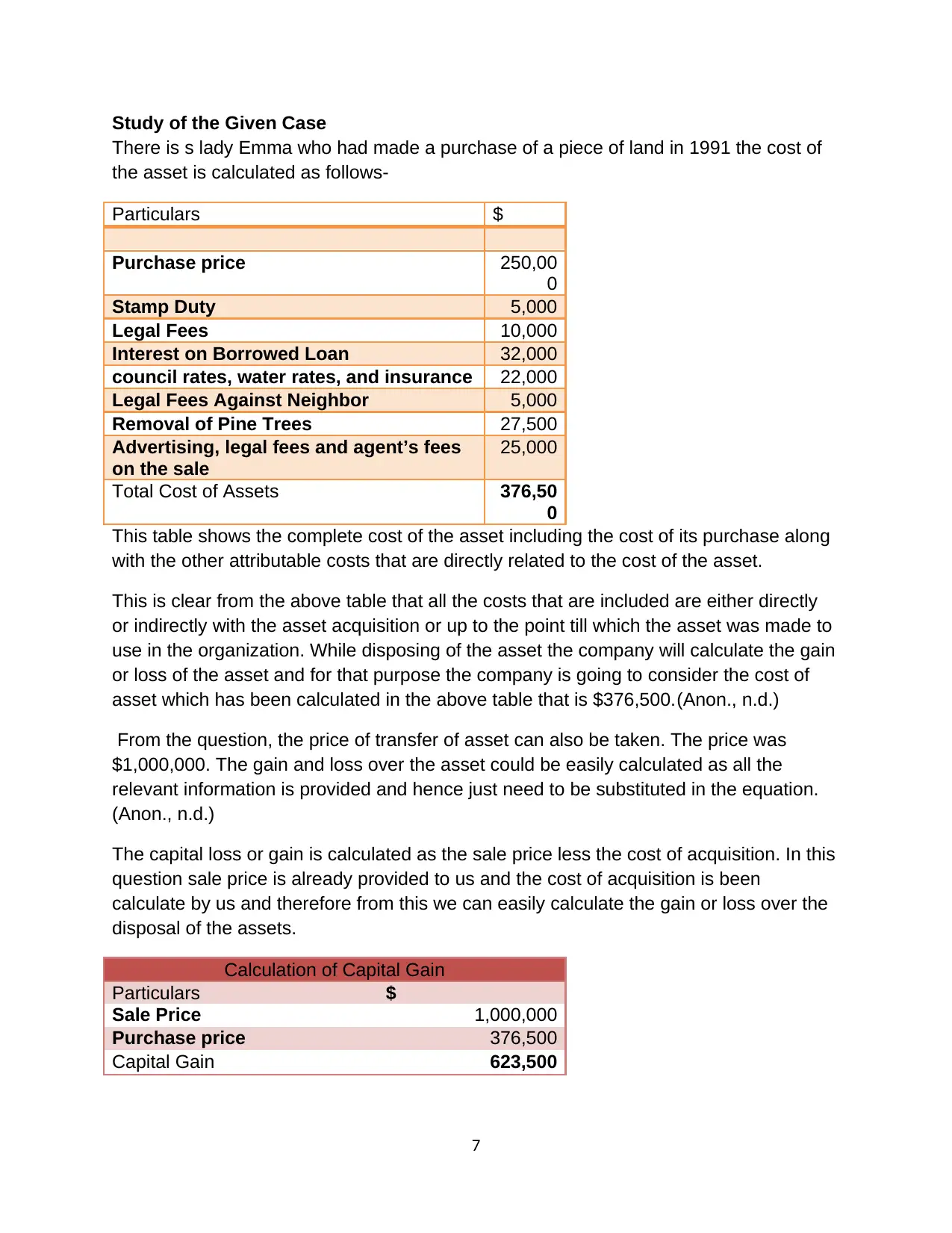

Study of the Given Case

There is s lady Emma who had made a purchase of a piece of land in 1991 the cost of

the asset is calculated as follows-

Particulars $

Purchase price 250,00

0

Stamp Duty 5,000

Legal Fees 10,000

Interest on Borrowed Loan 32,000

council rates, water rates, and insurance 22,000

Legal Fees Against Neighbor 5,000

Removal of Pine Trees 27,500

Advertising, legal fees and agent’s fees

on the sale

25,000

Total Cost of Assets 376,50

0

This table shows the complete cost of the asset including the cost of its purchase along

with the other attributable costs that are directly related to the cost of the asset.

This is clear from the above table that all the costs that are included are either directly

or indirectly with the asset acquisition or up to the point till which the asset was made to

use in the organization. While disposing of the asset the company will calculate the gain

or loss of the asset and for that purpose the company is going to consider the cost of

asset which has been calculated in the above table that is $376,500.(Anon., n.d.)

From the question, the price of transfer of asset can also be taken. The price was

$1,000,000. The gain and loss over the asset could be easily calculated as all the

relevant information is provided and hence just need to be substituted in the equation.

(Anon., n.d.)

The capital loss or gain is calculated as the sale price less the cost of acquisition. In this

question sale price is already provided to us and the cost of acquisition is been

calculate by us and therefore from this we can easily calculate the gain or loss over the

disposal of the assets.

Calculation of Capital Gain

Particulars $

Sale Price 1,000,000

Purchase price 376,500

Capital Gain 623,500

7

There is s lady Emma who had made a purchase of a piece of land in 1991 the cost of

the asset is calculated as follows-

Particulars $

Purchase price 250,00

0

Stamp Duty 5,000

Legal Fees 10,000

Interest on Borrowed Loan 32,000

council rates, water rates, and insurance 22,000

Legal Fees Against Neighbor 5,000

Removal of Pine Trees 27,500

Advertising, legal fees and agent’s fees

on the sale

25,000

Total Cost of Assets 376,50

0

This table shows the complete cost of the asset including the cost of its purchase along

with the other attributable costs that are directly related to the cost of the asset.

This is clear from the above table that all the costs that are included are either directly

or indirectly with the asset acquisition or up to the point till which the asset was made to

use in the organization. While disposing of the asset the company will calculate the gain

or loss of the asset and for that purpose the company is going to consider the cost of

asset which has been calculated in the above table that is $376,500.(Anon., n.d.)

From the question, the price of transfer of asset can also be taken. The price was

$1,000,000. The gain and loss over the asset could be easily calculated as all the

relevant information is provided and hence just need to be substituted in the equation.

(Anon., n.d.)

The capital loss or gain is calculated as the sale price less the cost of acquisition. In this

question sale price is already provided to us and the cost of acquisition is been

calculate by us and therefore from this we can easily calculate the gain or loss over the

disposal of the assets.

Calculation of Capital Gain

Particulars $

Sale Price 1,000,000

Purchase price 376,500

Capital Gain 623,500

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From all the values and calculation, we can conclude that there was a profit over the

sale of the asset and hence this also means that the capital gain tax would be attracted

and hence Emma becomes liable to pay tax to the Australian government over this

transaction.

We cannot take the method of indexation in this question so the tax would be calculated

using the method of discounting. Using this method the calculations areas-

=$623,500*50%

=$311750

This gives the amount $311,750 and this is the actual amount on which tax will be

calculated and Emma would b liable to pay tax on this amount and hence will be

included in the income tax of this Financial Year.

Share Sale

Emma was involved in the sale of the shares and they are not involved in the payment

of capital gain taxes. She would not pay any tax over this.(Anon., n.d.)

Stamp collection purchase by Emma from a Private collector

The year 2015

These are the purchases that are for the collectibles. This purchase was made

by Emma in year 2015.

The cost of acquisition- $60,000

Additional charges- $5000

Sale Price- $50,000

The loss of capital asset is charged as $15,000.

These losses which have occurred and they cannot be settled from any other

income heads. These losses can be set off from the amount of the gains of

collectibles. These losses are allowed to carry forward for the upcoming years

and there is no specific time for carrying these losses forward.(Anon., n.d.)

Sale of Grand piano

There was a purchase made by Emma in the year 2000 and that cost of

acquisition was $80,000 and the disposal price was $30,000.

There is a loss on the sale.

This purchase was made for the personal use and hence does not attract any of

the capital gain losses or taxes. So, therefore, no losses and gains are there in

the year.

8

sale of the asset and hence this also means that the capital gain tax would be attracted

and hence Emma becomes liable to pay tax to the Australian government over this

transaction.

We cannot take the method of indexation in this question so the tax would be calculated

using the method of discounting. Using this method the calculations areas-

=$623,500*50%

=$311750

This gives the amount $311,750 and this is the actual amount on which tax will be

calculated and Emma would b liable to pay tax on this amount and hence will be

included in the income tax of this Financial Year.

Share Sale

Emma was involved in the sale of the shares and they are not involved in the payment

of capital gain taxes. She would not pay any tax over this.(Anon., n.d.)

Stamp collection purchase by Emma from a Private collector

The year 2015

These are the purchases that are for the collectibles. This purchase was made

by Emma in year 2015.

The cost of acquisition- $60,000

Additional charges- $5000

Sale Price- $50,000

The loss of capital asset is charged as $15,000.

These losses which have occurred and they cannot be settled from any other

income heads. These losses can be set off from the amount of the gains of

collectibles. These losses are allowed to carry forward for the upcoming years

and there is no specific time for carrying these losses forward.(Anon., n.d.)

Sale of Grand piano

There was a purchase made by Emma in the year 2000 and that cost of

acquisition was $80,000 and the disposal price was $30,000.

There is a loss on the sale.

This purchase was made for the personal use and hence does not attract any of

the capital gain losses or taxes. So, therefore, no losses and gains are there in

the year.

8

References

Anon., n.d. Calculating the cost base for real estate. [Online]

Available at: https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-

real-estate/Calculating-the-cost-base-for-real-estate/

Anon., n.d. Capital gains tax. [Online]

Available at: https://www.ato.gov.au/General/Capital-gains-tax/

Anon., n.d. CGT assets and exemptions. [Online]

Available at: https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-

exemptions/#collectables

Anon., n.d. Cost base. [Online]

Available at: https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-

gain-or-loss/Cost-base/

Anon., n.d. Elements of the cost base and reduced cost base. [Online]

Available at: https://www.ato.gov.au/general/capital-gains-tax/working-out-your-capital-

gain-or-loss/cost-base/elements-of-the-cost-base-and-reduced-cost-base/

Anon., n.d. GST. [Online]

Available at: https://www.ato.gov.au/Business/GST/

Anon., n.d. Modifications and interaction with other rules. [Online]

Available at: https://www.ato.gov.au/general/capital-gains-tax/working-out-your-capital-

gain-or-loss/cost-base/modifications-and-interaction-with-other-rules/

Anon., n.d. Shares, units, and similar investments. [Online]

Available at: https://www.ato.gov.au/general/capital-gains-tax/shares,-units-and-similar-

investments/

Anon., n.d. When to charge GST (and when not to). [Online]

Available at: https://www.ato.gov.au/Business/GST/When-to-charge-GST-%28and-

when-not-to%29/

Anon., n.d. Working out your capital gain or loss. [Online]

Available at: https://www.ato.gov.au/general/capital-gains-tax/working-out-your-capital-

gain-or-loss/

9

Anon., n.d. Calculating the cost base for real estate. [Online]

Available at: https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-

real-estate/Calculating-the-cost-base-for-real-estate/

Anon., n.d. Capital gains tax. [Online]

Available at: https://www.ato.gov.au/General/Capital-gains-tax/

Anon., n.d. CGT assets and exemptions. [Online]

Available at: https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-

exemptions/#collectables

Anon., n.d. Cost base. [Online]

Available at: https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-

gain-or-loss/Cost-base/

Anon., n.d. Elements of the cost base and reduced cost base. [Online]

Available at: https://www.ato.gov.au/general/capital-gains-tax/working-out-your-capital-

gain-or-loss/cost-base/elements-of-the-cost-base-and-reduced-cost-base/

Anon., n.d. GST. [Online]

Available at: https://www.ato.gov.au/Business/GST/

Anon., n.d. Modifications and interaction with other rules. [Online]

Available at: https://www.ato.gov.au/general/capital-gains-tax/working-out-your-capital-

gain-or-loss/cost-base/modifications-and-interaction-with-other-rules/

Anon., n.d. Shares, units, and similar investments. [Online]

Available at: https://www.ato.gov.au/general/capital-gains-tax/shares,-units-and-similar-

investments/

Anon., n.d. When to charge GST (and when not to). [Online]

Available at: https://www.ato.gov.au/Business/GST/When-to-charge-GST-%28and-

when-not-to%29/

Anon., n.d. Working out your capital gain or loss. [Online]

Available at: https://www.ato.gov.au/general/capital-gains-tax/working-out-your-capital-

gain-or-loss/

9

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.