Analysis of Management Accounting Principles, Budgets, and Strategies

VerifiedAdded on 2019/09/16

|9

|2274

|361

Homework Assignment

AI Summary

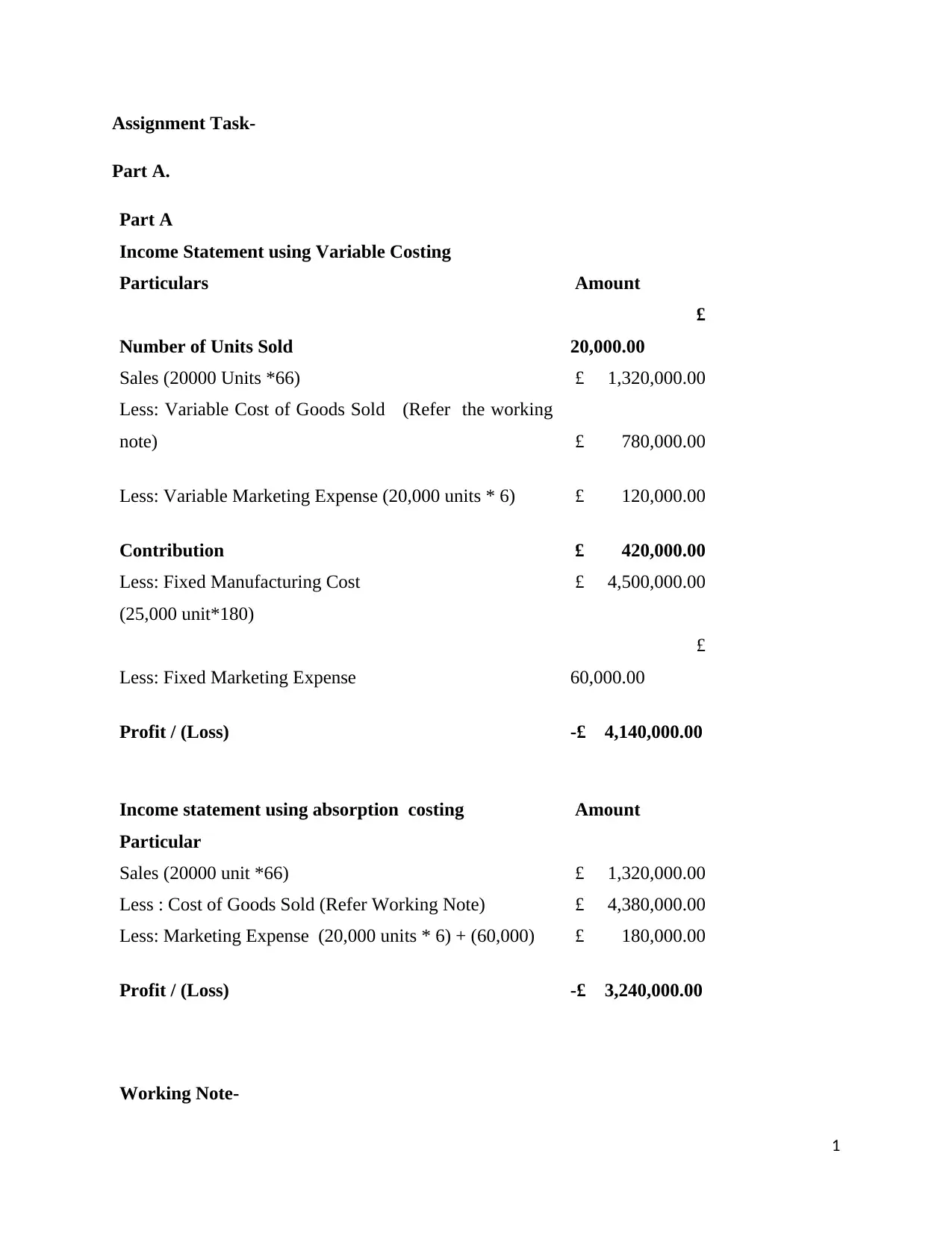

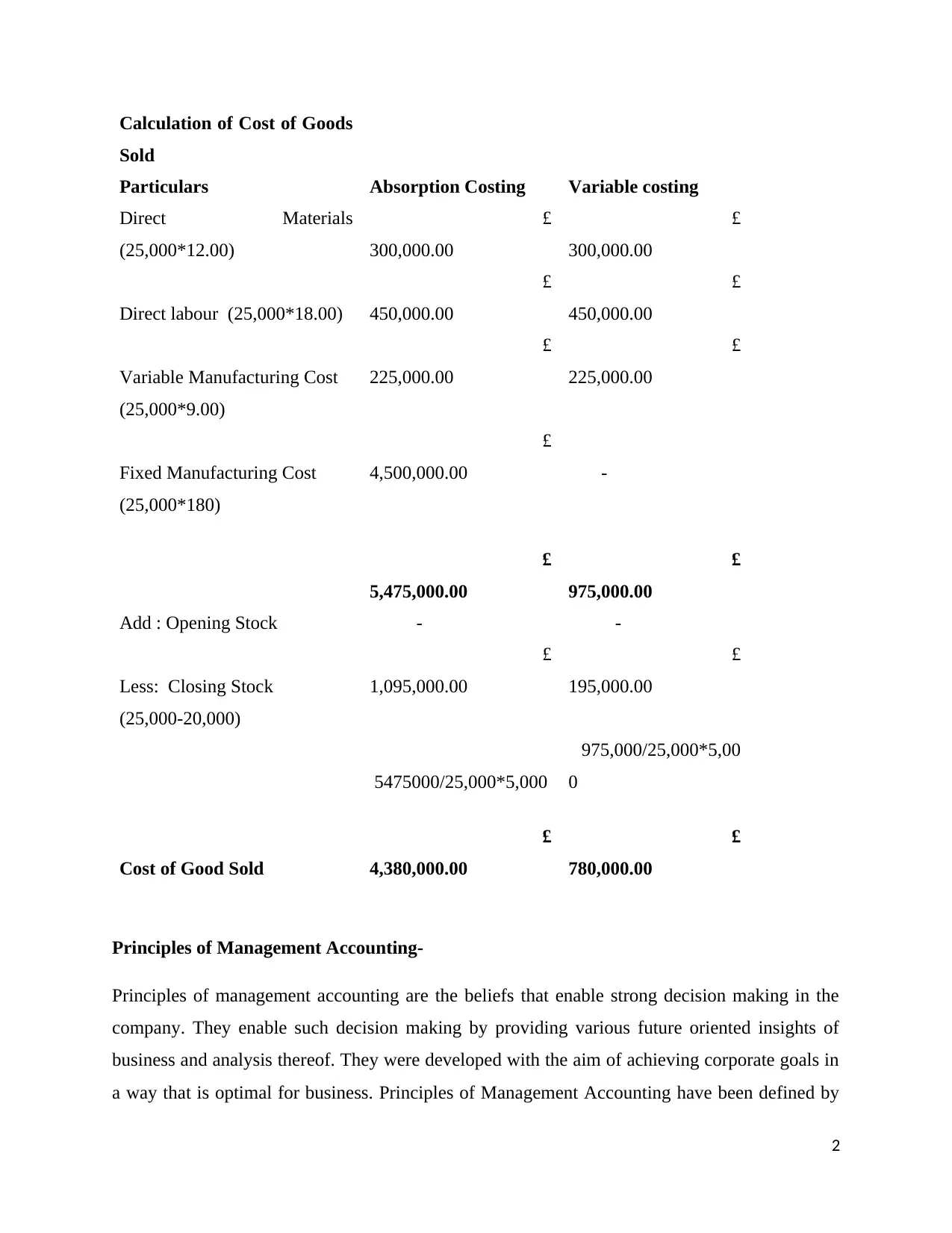

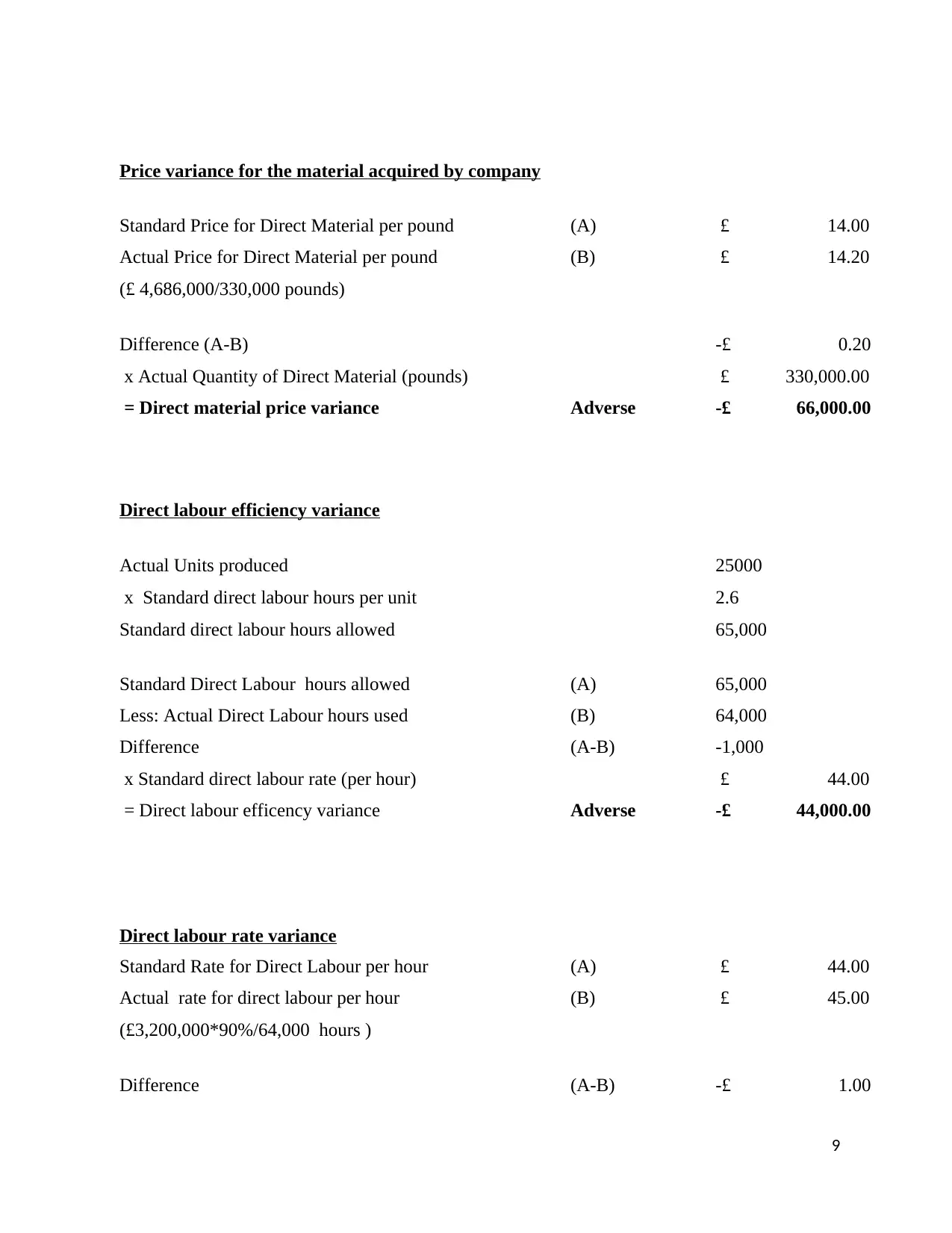

This assignment presents a comprehensive analysis of management accounting principles and practices. Part A focuses on income statements, comparing variable and absorption costing methods, along with detailed working notes for cost of goods sold calculations. It also discusses the principles, role, and integration of management accounting within an organization, including its impact on decision-making and transaction memory systems. Part B delves into operating budgets, pricing strategies, and standard costing, including the preparation of an operating budget, and an analysis of cash flow budgets, unit pricing based on cost methods, and variance analysis for direct materials and labor. The assignment provides practical examples and calculations to illustrate key concepts in management accounting, offering valuable insights into financial planning, cost control, and performance evaluation. The assignment covers the concepts of management accounting, including variable and absorption costing, budgeting, pricing strategies, and standard costing, along with variance analysis. The analysis includes income statements, cash flow budgets, and calculations for unit pricing, providing a comprehensive overview of financial management techniques.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.