Ask a question from expert

Principals of Management Accounting

9 Pages2274 Words361 Views

Added on 2019-09-16

Principals of Management Accounting

Added on 2019-09-16

BookmarkShareRelated Documents

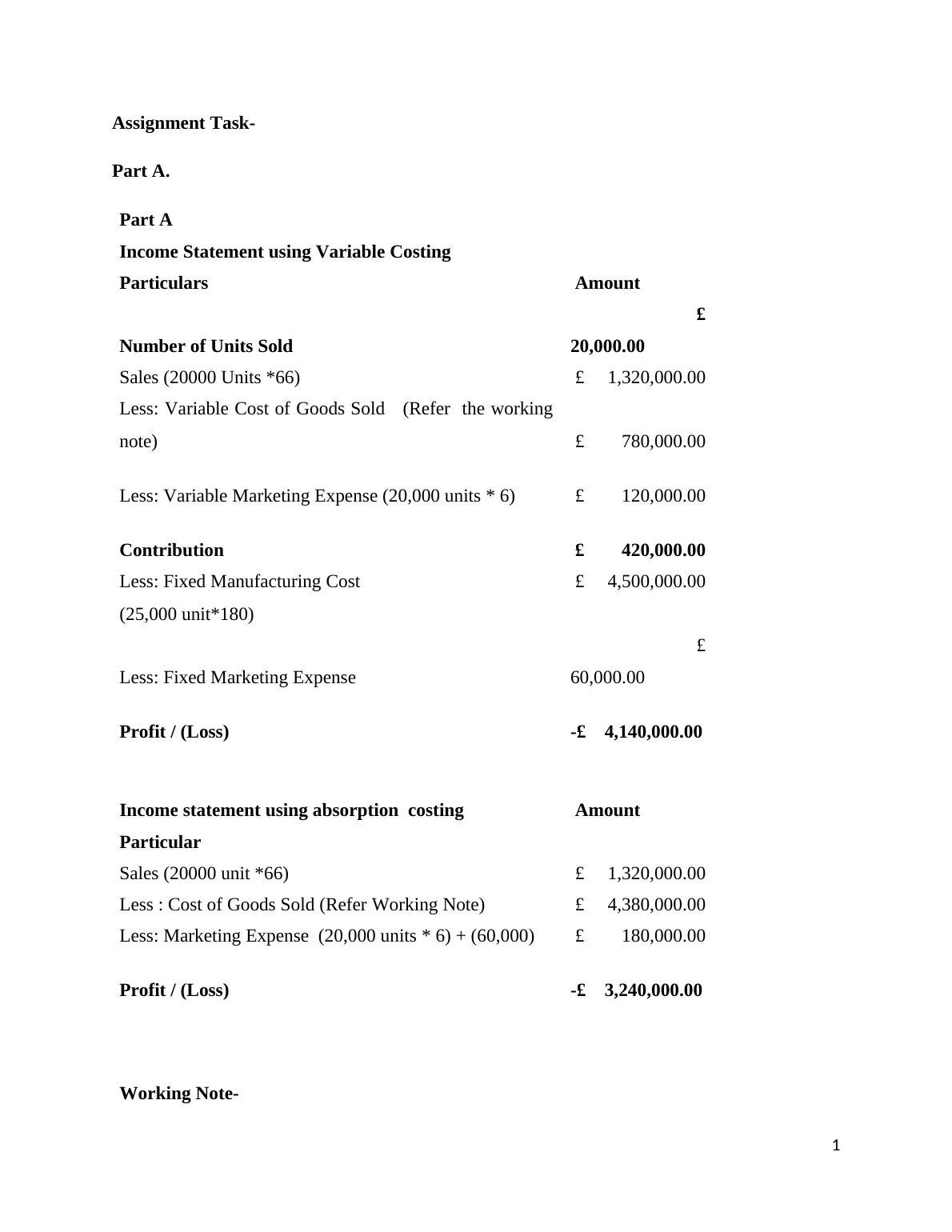

Assignment Task-Part A.Part AIncome Statement using Variable Costing Particulars Amount Number of Units Sold£20,000.00 Sales (20000 Units *66) £ 1,320,000.00Less: Variable Cost of Goods Sold (Refer the workingnote) £ 780,000.00Less: Variable Marketing Expense (20,000 units * 6) £ 120,000.00Contribution £ 420,000.00Less: Fixed Manufacturing Cost £ 4,500,000.00(25,000 unit*180)Less: Fixed Marketing Expense£60,000.00 Profit / (Loss)-£ 4,140,000.00Income statement using absorption costing Amount ParticularSales (20000 unit *66) £ 1,320,000.00Less : Cost of Goods Sold (Refer Working Note) £ 4,380,000.00Less: Marketing Expense (20,000 units * 6) + (60,000) £ 180,000.00Profit / (Loss)-£ 3,240,000.00Working Note-Calculation of Cost of GoodsSold ParticularsAbsorption Costing Variable costing DirectMaterials(25,000*12.00)£300,000.00 £300,000.00 Direct labour (25,000*18.00)££1

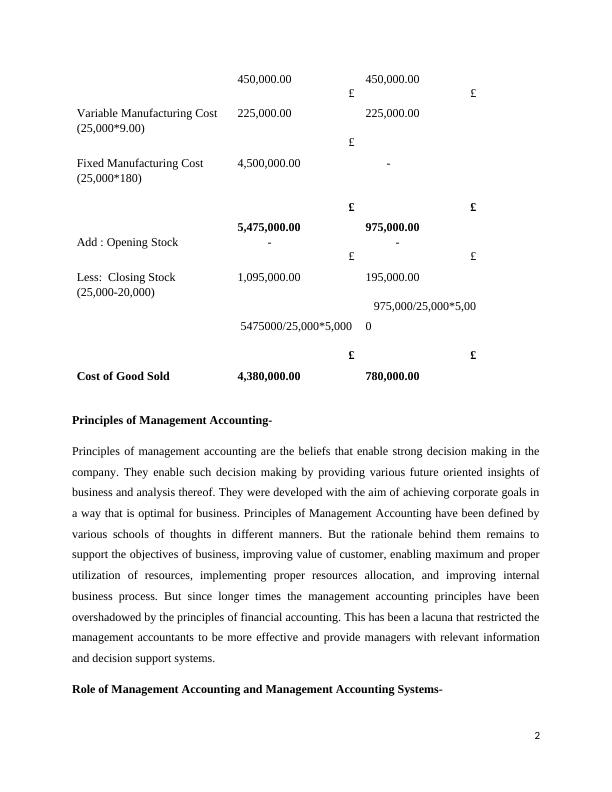

450,000.00 450,000.00 Variable Manufacturing Cost £225,000.00 £225,000.00 (25,000*9.00)Fixed Manufacturing Cost£4,500,000.00 - (25,000*180)£5,475,000.00 £975,000.00 Add : Opening Stock - - Less: Closing Stock £1,095,000.00 £195,000.00 (25,000-20,000) 5475000/25,000*5,000 975,000/25,000*5,000 Cost of Good Sold£4,380,000.00 £780,000.00 Principles of Management Accounting-Principles of management accounting are the beliefs that enable strong decision making in thecompany. They enable such decision making by providing various future oriented insights ofbusiness and analysis thereof. They were developed with the aim of achieving corporate goals ina way that is optimal for business. Principles of Management Accounting have been defined byvarious schools of thoughts in different manners. But the rationale behind them remains tosupport the objectives of business, improving value of customer, enabling maximum and properutilization of resources, implementing proper resources allocation, and improving internalbusiness process. But since longer times the management accounting principles have beenovershadowed by the principles of financial accounting. This has been a lacuna that restricted themanagement accountants to be more effective and provide managers with relevant informationand decision support systems.Role of Management Accounting and Management Accounting Systems-2

Just like there are various schools of its principles, the role of management accounting has alsobeen defined by various thinkers and school of thoughts. But whichever way one might look at it,all these different thinking seems to collaborate at the point that management accounting has gotan important role to play within organization. During past, several ‘best methods’ ofmanagement accounting were developed in the early twentieth century as ‘tools’ of themanufacturer. Further, it was seen as a key factor which helped in coordinating the activities of afirm over a large geographical area. Various schools also thought management accounting as aprocess to create a “governable person”. Thus the management accountant and the managementaccounting has a powerful position to influence an organization with its thoughts and discipline.But unlike the financial information which becomes available widely in a public domain over aperiod of time, management accounting information is developed, shared and analyzed in aresponsible manner and fashion. The management at the top level and at the middle level of an organization has to study andanalyze the strategic issues that can affect the performance of the business in order to survive ina competitive environment. The information that the management accounting systems provideare related to the both internal as well external environment prevailing around the business. Thiswould help the business managers to relate the firm's strengths and weaknesses to the variousspecific opportunities and threats.It is un-debatable that the Management Accounting Systemswould certainly has the capacity to impact and influence the development of TransactionMemory System. This can be explained with the help of an example, Management AccountingSystem may facilitate encoding, storing, and retrieving information for Transaction MemorySystem’s development.Techniques and methods used in Management Accounting by presenting calculation for anincome statement using variable costing-Financial Accounting requirements are basically period based reporting mechanisms, that is tosay that it does not differentiate between Fixed costs of production and variable costs ofproduction. Whereas it is of extreme importance for the management of a company to determineand know the break-up of costs in fixed and variable. Variable costs are those costs which aredirectly related to the level of production. That is they increase when the level of activityincreases and vice versa. Whereas the fixed costs are such costs which are fixed for all levels of3

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting Assignment - Tesco plclg...

|9

|2426

|447

Management Accounting - Deskliblg...

|5

|946

|160

Marginal and Absorption Costinglg...

|10

|1066

|38

Unit 5 Management Accounting - Management Accounting Principleslg...

|15

|772

|28

Management Accounting: Absorption Costing vs Marginal Costinglg...

|8

|1801

|49

Costing Method Assignment (Solved)lg...

|10

|2370

|49