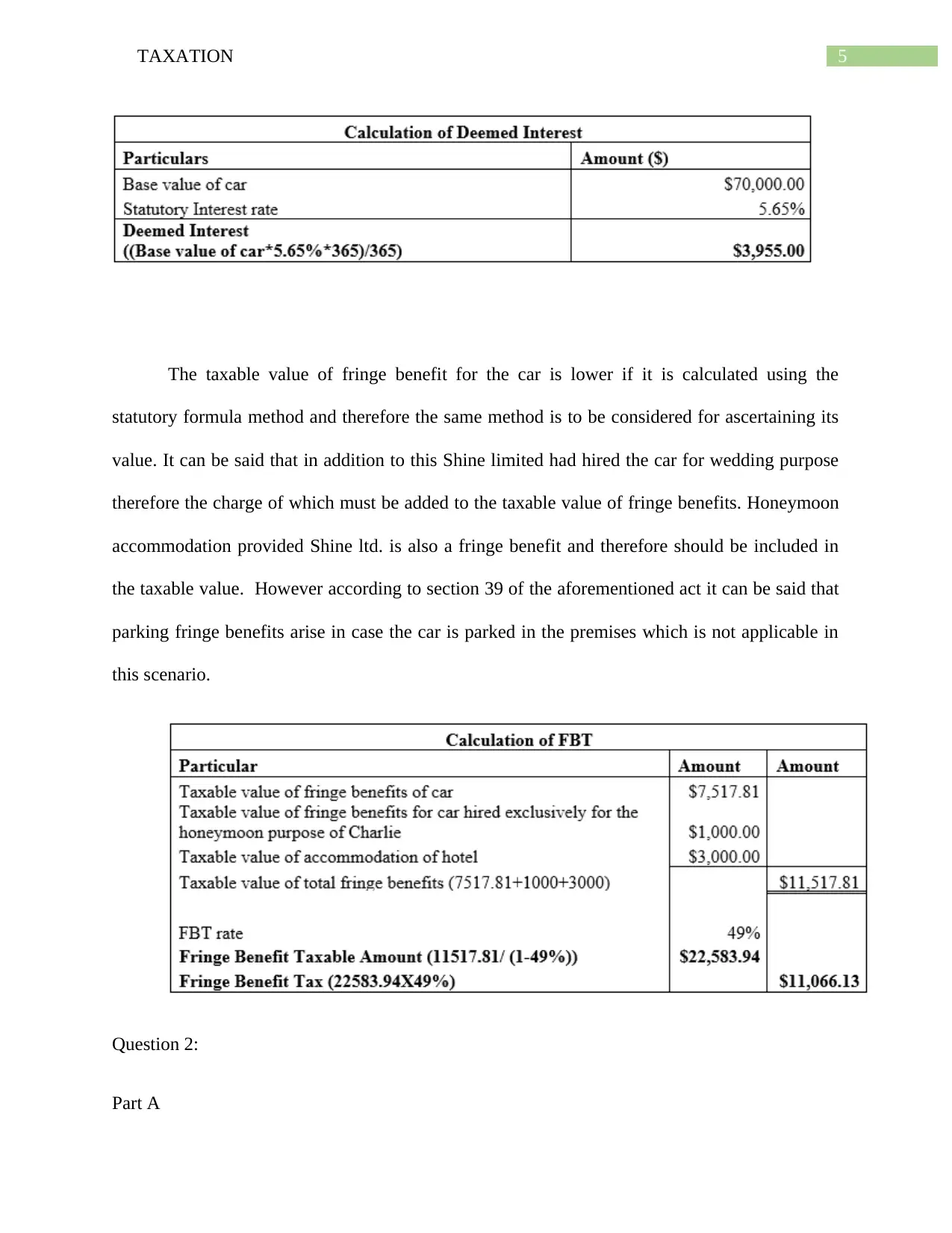

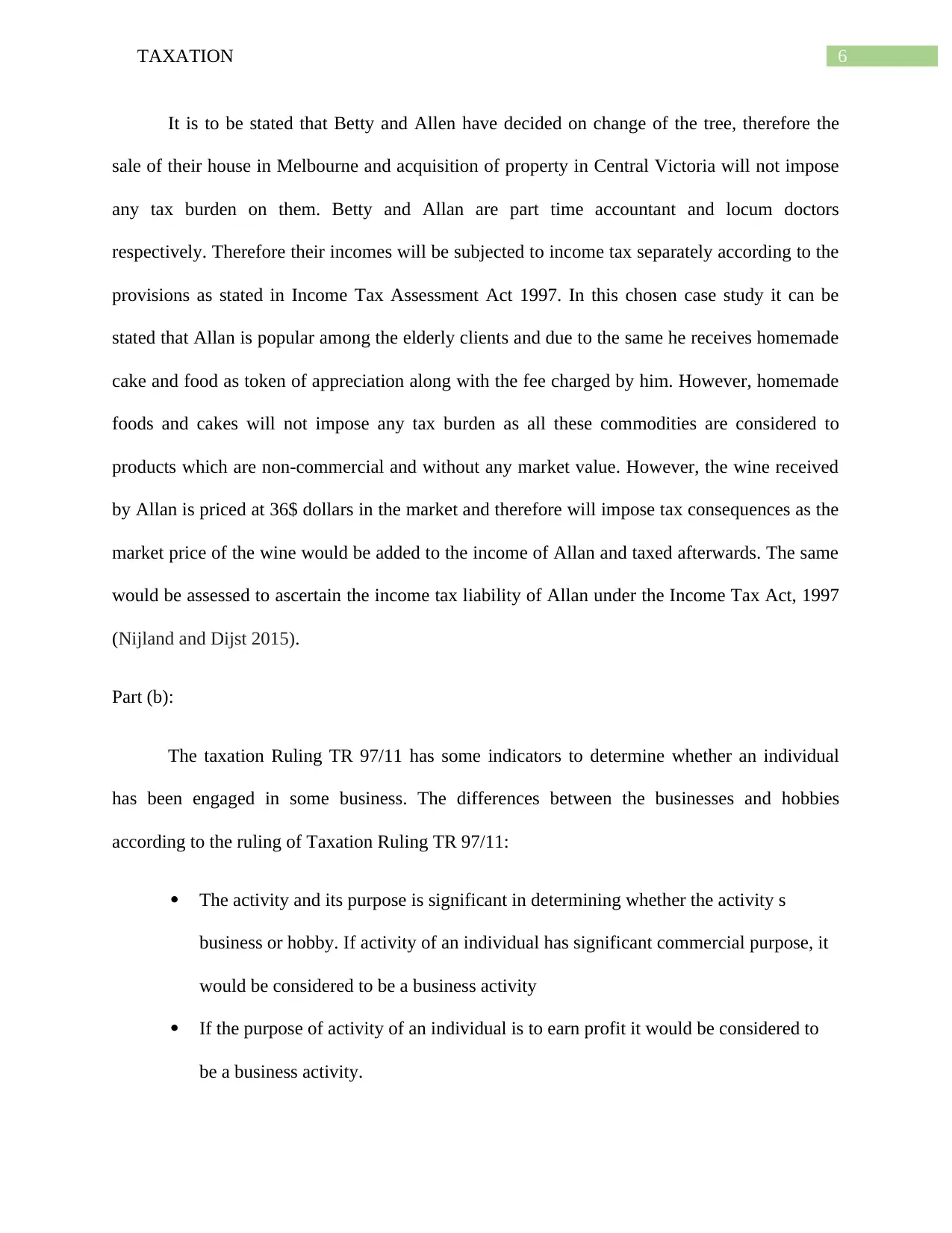

Understanding FBT and Income Tax on Barter in Australia

VerifiedAdded on 2020/05/28

|10

|1595

|150

AI Summary

The assignment provides an in-depth analysis of Fringe Benefits Tax (FBT) and Income Tax as they relate to barter transactions within the Australian context. It begins by exploring FBT implications on in-house employee benefits and barter exchanges, examining how such arrangements are treated under tax legislation like the Income Tax Assessment Act 1997. The document also investigates the conversion of personal hobbies into business activities, highlighting the income tax considerations when profits emerge from these endeavors. Furthermore, it elucidates how barter transactions are subjected to both GST and ITAA regulations in Australia, equating them with traditional cash or credit transactions for tax purposes. Through a detailed exploration of legal precedents and taxation rulings, such as TR 97/11, the assignment distinguishes between business activities and hobbies, offering clarity on their tax implications. The analysis is supported by references to authoritative texts and case law, enriching the reader's understanding of Australian taxation laws concerning fringe benefits and barter exchanges.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.